Content

Asia Pacific Plastic Compounding Market Size, Share, Growth and Forecast 2026-2035

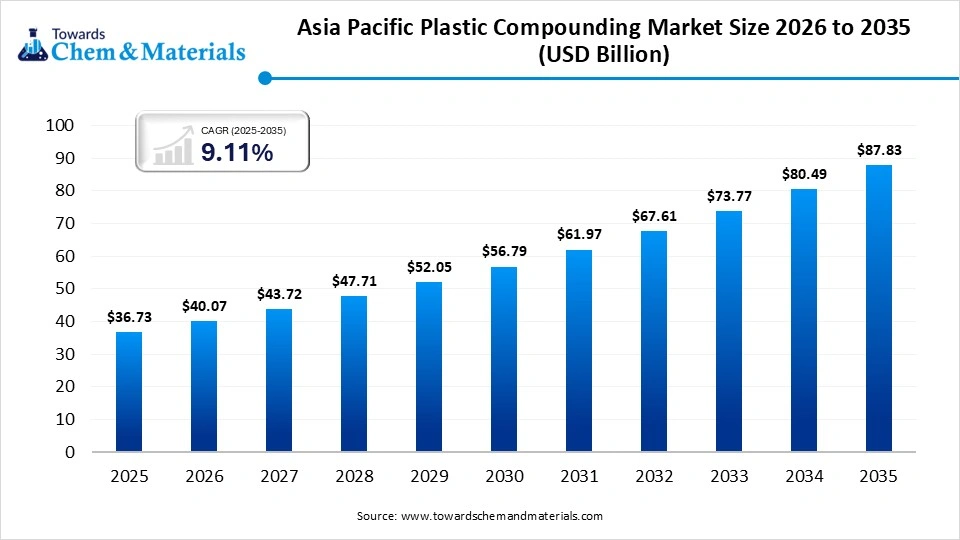

The Asia Pacific plastic compounding market size is expected to grow from USD 87.83 billion in 2025 to USD 40.07 billion in 2026 and is forecast to reach USD 87.83 billion by 2035 at a 9.11% CAGR over 2026-2035.

Key Takeaways

- China held approximately a 50% share in the Asia Pacific plastic compounding market in 2024 due to the growing automotive industry.

- India is growing at the fastest CAGR in the market during the forecast period due to the rising infrastructure development.

- By polymer, the polypropylene (PP) segment held approximately a 28% share in the market in 2024 due to the increasing production of exterior & interior automotive parts.

- By polymer, the TPE/TPU & engineering segment is expected to grow at the fastest CAGR in the market during the forecast period due to the growing adoption of consumer electronics.

- By functional formulation, the filled & reinforced segment held approximately a 38% share in the market in 2024 due to the increasing production of electric vehicles.

- By functional formulation, the flame-retardant & recycled/biobased compounds segment is expected to grow at the fastest CAGR in the market during the forecast period due to the stringent fire safety regulations.

- By end use, the automotive & transportation segment held approximately a 30% share in the market in 2024 due to the strong focus on improving fuel efficiency of vehicles.

- By end use, the electrical & electronics segment is expected to grow at the fastest CAGR in the market during the forecast period due to the increasing adoption of electronic devices.

- By processing method, the injection molding segment held approximately a 45% share in the market in 2024 due to the growing production of intricate plastic parts.

- By processing method, the film & sheet extrusion segment is expected to grow at the fastest CAGR in the market during the forecast period due to the increasing agricultural activities.

- By filler type, the talc & CaCO3 segment held approximately a 55% share in the market in 2024 due to the high heat resistance.

- By filler type, the glass fibers & nano-fillers segment is expected to grow at the fastest CAGR in the market during the forecast period due to the increasing demand for high-performance construction materials.

- By distribution, the direct to OEMs/tier-1s segment held approximately a 60% share in the Asia Pacific plastic compounding market in 2024 due to the strong focus on direct relationships.

- By distribution, the distributors/traders segment is expected to grow at the fastest CAGR in the market during the forecast period due to the availability of technical expertise.

Role of Asia Pacific Plastic Compounding in Sustainable Future

Asia Pacific plastic compounding is a process of blending polymers with additives. Plastic compounding offers properties like high strength, chemical resistance, and flexibility. The additives incorporated in plastic compounding are reinforcements, plasticizers, impact modifiers, colorants, stabilizers, and flame retardants. The plastic compounding process involves material selection, mixing, and extrusion. The benefits of plastic compounding are enhanced aesthetic qualities, lightweighting, improved processability, and cost efficiency.

The growing industrialization and infrastructure development increase demand for plastic compounding. The increasing expansion of the automotive industry and the rise in electric vehicles increase demand for plastic compounding. The increasing demand for consumer goods and growing manufacturing activities increases demand for plastic compounding. Factors like the growing automotive sector, increasing consumption of packaged foods, growth in e-commerce, and increasing construction activity contribute to the growth of the Asia Pacific plastic compounding market.

- Vietnam exported 2,970 shipments of the plastic compound.(Source: www.volza.com)

- Vietnam exported 11,182 shipments of PVC compound.(Source: www.volza.com)

- Thailand exported 5,828 shipments of polypropylene compound.(Source: www.volza.com)

Growing Construction Activities Surge Demand for Plastic Compounding

The rapid urbanization and growing construction activities in the Asia Pacific increase demand for plastic compounding. The growing investment in infrastructure projects like bridges, public buildings, and others increases the adoption of plastic compounding. The growing demand for lightweight materials in construction activities and the customization of construction increase the demand for plastic compounding.

The growing adoption of green buildings and focus on energy efficiency increases demand for plastic compounding. The increasing demand for materials like pipes, window frames, insulation, fittings, panels, flooring, and cables increases the adoption of plastic compounding. The growing commercial and residential construction activity increases demand for plastic compounding. The growing construction activity is a key driver for the growth of the Asia Pacific plastic compounding market.

Market Trends

- Growing Packaging Industry : The growing expansion of the packaging industry and increasing demand for packaging in various industries like electrical, food & beverage, electronics, and consumer goods increases demand for plastic compounding.

- Increasing Manufacturing Activity : The increasing manufacturing base in various industries like automotive, electronics, and electrical increases demand for plastic compounding for various applications.

- Growing Infrastructure Development : The increasing investment in infrastructure development, like mass housing projects, smart cities, and transportation networks, increases the demand for plastic compounding.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 40.07 Billion |

| Expected Size by 2034 | USD 87.83 Billion |

| Growth Rate from 2025 to 2034 | CAGR 9.11% |

| Base Year of Estimation | 2024 |

| Forecast Period | 2025 - 2034 |

| Segment Covered | By Polymer/Base Resin, By Functional Formulation / Additive System, By End-Use Industry, By Processing Method (Downstream Use), By Filler/Reinforcement Type, By Distribution Channel, By Region |

| Key Companies Profiled | LyondellBasell Industries N.V., Teijin Plastics, Kraton Polymers Inc., RTP Company,BASF SE, SABIC, The 3M Company, Polyplastics Asia Pacific Sdn Bhd, Melchers Malaysia, Helistrom Sdn Bhd, Sheng Foong Plastic Industries Sdn Bhd, The Inabata Group, CIPC Resin, Sin Yong Guan & Co., Eveready Manufacturing Pte Ltd., Compounding and Coloring Sdn Bhd |

Market Opportunity

Expansion of the Electronic Industry Unlocks Market Opportunity

The growing expansion of the electronic industry and the increasing adoption of electronic devices increase demand for plastic compounding. The growing adoption of electronic devices like smartphones, laptops, computers, wearable devices, and many more increases demand for plastic compounding for various electronic applications.

The ongoing miniaturization of electronic devices and the complexity of electronic devices increase demand for plastic compounding. The increasing adoption of electric vehicles increases demand for plastic compounding for the development of connectors and battery housing. The growth in smart devices and the increasing demand for electronic appliances increases the adoption of plastic compounding. The growing production of connectors, enclosures, wire insulation, and housing increases demand for plastic compounding. The growing expansion of the electronic industry creates an opportunity for the growth of the Asia Pacific plastic compounding market.

2016-2025")

Market Challenge

High Manufacturing Cost Shuts Down Expansion of Market

Despite several benefits of plastic compounding in the Asia Pacific, the high manufacturing cost restricts the market growth. Factors like the need for specialized additives, fluctuating raw material costs, stricter regulations, complex manufacturing processes, and high energy demand are responsible for high manufacturing costs.

The fluctuations in the cost of raw materials like natural gas and crude oil directly affect the market. The need for specialty additives like UV stabilizers, impact modifiers, and flame retardants increases the costs. The need for specialized equipment, like multi-screw extruders and complex manufacturing processes, increases the cost. The stricter regulations and increasing demand for maintenance of equipment increase the cost. The high manufacturing cost hampers the growth of the Asia Pacific plastic compounding market.

Regional Insights

China Asia Pacific Plastic Compounding Market Trends

China dominated the Asia Pacific plastic compounding market in 2024. The growing automotive industry and increasing adoption of electric cars increase demand for plastic compounding. The growing residential, commercial, and infrastructure development increases the adoption of plastic compounding. The strong government support for clean energy and increasing investment in R&D increases the production of plastic compounding. The well-established manufacturing infrastructure for automotive components, plastics, and electronics products increases demand for plastic compounding, driving the overall growth of the market.

- China exported 2,043 shipments of the plastic compound.(Source: www.volza.com)

- China exported 7,117 shipments of PVC compound.(Source: www.volza.com)

India Asia Pacific Plastic Compounding Market Trends

India is experiencing the fastest growth in the market during the forecast period. The growing demand for consumer goods like consumer electronics and other products increases the adoption of plastic compounding. The rapid urbanization and growing development of infrastructure increase demand for plastic compounding. The strong government support for domestic manufacturing and the expansion of the packaging sector increase demand for plastic compounding, supporting the overall growth of the market.

- India exported 6,575 shipments of the PVC compound.(Source: www.volza.com)

- Swastik Polymers is the leading supplier of the PVC compound in India.(Source: www.volza.com)

- India exported 2,496 shipments of polypropylene compound.(Source: www.volza.com)

Segmental Insights

Polymer Insights

Why did the Polypropylene Segment Dominate the Asia Pacific Plastic Compounding Market?

The polypropylene (PP) segment dominated the Asia Pacific plastic compounding market in 2024. The growing production of exterior and interior automotive parts like door panels, bumpers, dashboards, and structural parts increases the adoption of polypropylene. The growing construction activities increase demand for PP for the production of films, moisture barrier membranes, and siding. Polypropylene has high chemical resistance, excellent stiffness, and is lightweight. The growing demand for PP across various industries like consumer goods, electronics, automotive, and packaging drives the market growth.

The TPE/TPU & engineering segment is the fastest-growing in the market during the forecast period. The increasing production of consumer electronics like smartphones, laptops, and computers increases demand for TPE/TPU. The expansion of the healthcare sector and increasing production of wound care & medical tubing increase demand for TPE/TPU. The focus on lowering emissions and enhancing fuel efficiency increases demand for TPE/TPUs. The ongoing technological advancements in TPU and the focus on sustainability support the overall growth of the market.

Functional Formulation Insights

How Filled & Reinforced Segment Held the Largest Share in the Asia Pacific Plastic Compounding Market?

The filled & reinforced segment held the largest revenue share in the Asia Pacific plastic compounding market in 2024. The growing demand for glass fibers, calcium carbonate, and talc in various industries helps the market growth. The growing demand for lightweight materials in vehicles increases the adoption of filled & reinforced formulations. The growing production of electric vehicles and traditional vehicles increases demand for filled & reinforced formulation. The growing development of infrastructure and residential buildings increases demand for filled & reinforced formulations, driving the overall growth of the market.

The flame-retardant & recycled/biobased compounds segment is experiencing the fastest growth in the market during the forecast period. The stricter fire safety regulations and focus on reducing risks of fire increase demand for flame-retardant materials. The rapid industrialization and growing fire incidents increase demand for flame-retardant materials. The stricter government regulations on plastic waste and the increasing demand for eco-friendly products increase demand for recycled/biobased compounds. The growing industries like electronics, construction, and automotive increase flame-retardant & recycled/biobased compounds, supporting the overall growth of the market.

End-Use Industry Insights

Which End Use Industry Dominated the Asia Pacific Plastic Compounding Market?

The automotive & transportation segment dominated the Asia Pacific plastic compounding market in 2024. The growing production of buses, passenger cars, and trucks increases demand for plastic compounding. The increasing lightweight materials and the focus on improving fuel efficiency increase demand for plastic compounding. The growing adoption of electric vehicles and the customization of vehicle design increase demand for plastic compounding. The growing production of vehicle components like door panels, dashboards, and bumpers increases demand for plastic compounding, driving overall growth of the market.

The electrical & electronics segment is the fastest-growing in the market during the forecast period. The growing miniaturization of electronic devices and the development of complex electronic components increase demand for plastic compounding. The rise in electric vehicles increases demand for electronic components for the development of batteries and charging systems. The increasing production of electronic components like housing, wire insulation, and dashboards requires plastic compounding. The growing adoption of electronic devices like smartphones, wearables, laptops, and computers supports the overall growth of the market.

Processing Method (Downstream Use) Insights

What Made the Injection Molding Segment Held the Largest Share in the Asia Pacific Plastic Compounding Market?

The injection molding segment held the largest revenue share in the Asia Pacific plastic compounding market in 2024. The increasing production of complex plastic parts and the need for handling various plastic materials increase the demand for injection molding. The increasing production of aesthetic and structural components of vehicles requires injection molding. The growing demand for packaging industries like pharmaceutical, food & beverage, and personal care increases the adoption of injection molding. The growing demand for injection molding in industries like automotive, healthcare, packaging, and consumer goods drives the market growth.

The film & sheet extrusion segment is experiencing the fastest growth in the market during the forecast period. The growing expansion of the packaging sector and increasing consumption of packaged foods increase demand for film & sheet extrusion. The growing agricultural activities, like silage wrapping, greenhouse coverings, and mulching, increase demand for film & sheet extrusion. The growing production of protective layers, insulation, and vapor barriers increases demand for film & sheet extrusion. The growing demand for various polymer blends and advancements in film & sheet extrusion support the overall growth of the market.

Filler Type Insights

Why did Talc & CaCO3 Segment Dominate the Asia Pacific Plastic Compounding Market?

The talc & CaCO3 segment dominated the Asia Pacific plastic compounding market in 2024. The focus on improving the rigidity and stiffness of plastic materials in various applications increases demand for talc & CaCO3. The strong focus on sustainability and increasing demand for smoother surface finish increases the adoption of talc & CaCO3. They offer excellent heat resistance, reduce oxygen transmission, and offer good thermal stability. The growing demand for talc & CaCO3 in industries like construction, consumer goods, automotive, and packaging drives the overall growth of the market.

The glass fibers & nano fillers segment is the fastest-growing in the market during the forecast period. The growing demand for lightweight materials in the aerospace and automotive industries increases the adoption of glass fibers & nano fillers. The increasing demand for electric vehicles and high-performance construction materials increases the adoption of glass fibers & nano fillers. The strong focus on improving the shelf life of consumer goods increases the adoption of glass fibers & nano fillers, supporting the overall growth of the market.

Distribution Channel Insights

How Direct to OEMs or Tier-1s Segment Held the Largest Share in the Asia Pacific Plastic Compounding Market?

The direct to OEMs/tier-1s segment held the largest revenue share in the Asia Pacific plastic compounding market in 2024. The availability of customization and unique design increases demand for direct to OEMs/tier-1s. The growing consumer focus on a direct line of communication and the availability of specialized compounded plastics help the market growth. The need for streamlining supply chains and a strong focus on quality control increases buying from direct to OEMs/tier-1s, driving the overall growth of the market.

The distributors/traders segment is experiencing the fastest growth in the market during the forecast period. The strong focus on bridging the gap between end users and compounders increases demand for distributors. The need to simplify the supply chain for manufacturers and the requirement for technical knowledge increase the adoption of distributors/traders. The growing demand for tailored solutions and focus on efficient logistics increases the demand for distributors/traders, supporting the overall growth of the market.

Asia Pacific Plastic Compounding Market Value Chain Analysis

Feedstock Procurement : The feedstock procurement for Asia Pacific plastic compounding is polymers like polypropylene, polycarbonate, polyethylene, & many more additives like pigments, fillers, plasticizers, & many more.

Chemical Synthesis & Processing : The chemical synthesis & processing for Asia Pacific plastic compounding include material selection, additive selection, extrusion, pelletizing, cooling, and packaging.

- Key Players:- SABIC, LG Chem, BASF SE, and LyondellBasell

Quality Testing & Certification : The quality testing involves the Izod impact test & ASTM D882, and certifications like UL certification, REACH compliance, ISO Standards, & NSF/ANSI/CAN standards.

Recent Developments

- In April 2023, BASF launched ecovio compounding capacities in China. The ecovio is widely used in applications like food packaging, organic waste bags, agricultural mulch films, fruit & vegetable bags, & cling film, and the compound is soil-biodegradable & compostable.(Source: www.sustainableplastics.com)

- In May 2025, DOMO India expands the compounding capacity of the TECHNYL 4EARTH range in Mumbai. The company manufactures high-value engineering plastics and useful in applications like automotive components, electronic connectors, and smart devices. The range lowers production waste, energy use, and carbon emissions.(Source: www.domochemicals.com)

- In June 2024, LyondellBasell expands PP compounding production in China. The new site has four production lines with a capacity of 80000 tonnes. The PP compounding is widely used in automotive applications like instrument panels, under-the-hood components, bumpers, structural parts, body panels, and interior trims.(Source: www.lyondellbasell.com)

Asia Pacific Plastic Compounding Market Top Companies

- LyondellBasell Industries N.V.

- Teijin Plastics

- Kraton Polymers Inc.

- RTP Company

- BASF SE

- SABIC

- The 3M Company

- Polyplastics Asia Pacific Sdn Bhd

- Melchers Malaysia

- Helistrom Sdn Bhd

- Sheng Foong Plastic Industries Sdn Bhd

- The Inabata Group

- CIPC Resin

- Sin Yong Guan & Co.

- Eveready Manufacturing Pte Ltd.

- Compounding and Coloring Sdn Bhd

Segments Covered

By Polymer/Base Resin

- Polypropylene (PP)

- Polyethylene (PE: HDPE/LDPE/LLDPE)

- PVC

- ABS

- Polycarbonate (PC)

- Polyamides (PA6, PA66)

- PBT & PET

- TPE/TPU & Elastomeric Compounds

- PS & HIPS

- Engineering/Specialty (POM, PPS, PEEK), Others

By Functional Formulation / Additive System

- Filled & Reinforced (GF, talc, CaCO₃, mica)

- Flame-Retardant (incl. halogen-free)

- Impact-Modified / Toughened

- UV/Heat Stabilized & Weatherable

- Color & Masterbatches

- Conductive/EMI-Shielding & Antistatic

- Recycled/Biobased Content Compounds

By End-Use Industry

- Automotive & Transportation (ICE & EV)

- Electrical & Electronics (Consumer, 5G, Batteries)

- Packaging (Rigid & Flexible)

- Building & Construction

- Appliances/White Goods & Consumer Durables

- Healthcare & Medical Devices

- Others (Industrial, Agriculture)

By Processing Method (Downstream Use)

- Injection Molding

- Extrusion (Profiles, Sheets)

- Film & Sheet Extrusion

- Blow Molding

- Others (Rotomolding, Thermoforming)

By Filler/Reinforcement Type

- Glass Fiber

- Talc

- Calcium Carbonate

- Mica/Others

- Nano-Fillers & Specialty (CNTs, nanoclays)

By Distribution Channel

- Direct to OEMs/Tier-1s

- Through Distributors/Traders

- Contract/Custom Compounding

By Region

- China

- India

- Japan

- South Korea

- ASEAN (Indonesia, Vietnam, Thailand, Malaysia, Philippines, etc.)

- Australia & New Zealand

- Rest of APAC

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (2)