Content

Polyethylene Market Size, Share and Trends Report 2035

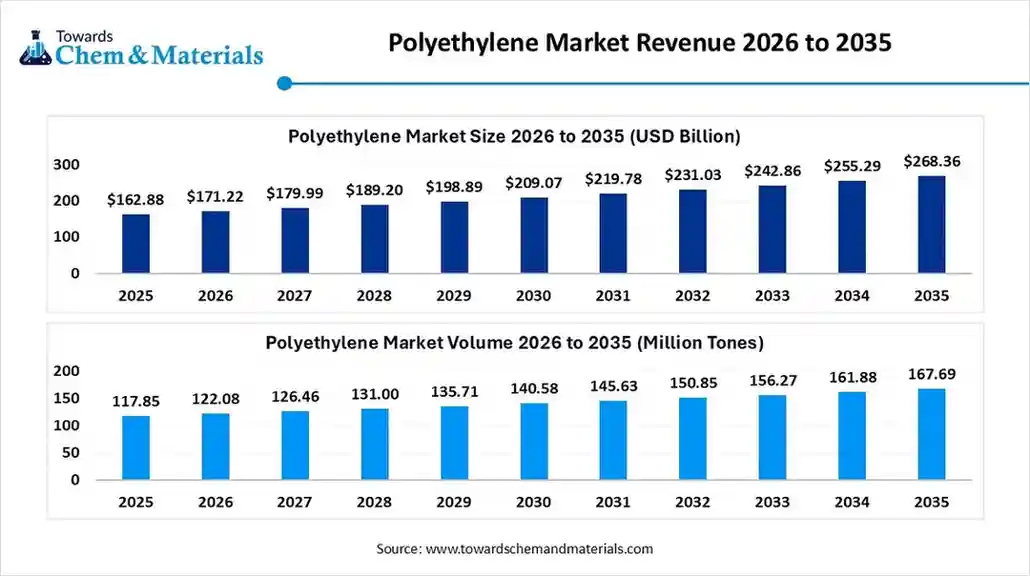

According to Towards Chemicals and Materials Analytics and Consulting, the global polyethylene market was valued at USD 168.75 billion in 2025, is estimated to reach USD 177.1 billion in 2026, and is projected to reach USD 273.57 billion by 2035, growing at a CAGR of 4.95% from 2026 to 2035. In terms of volume, the polyethylene market is projected to grow from 128.45 million tons in 2025 to 196.63 million tons by 2035. growing at a CAGR of 4.35% from 2026 to 2035.

Key Takeaways

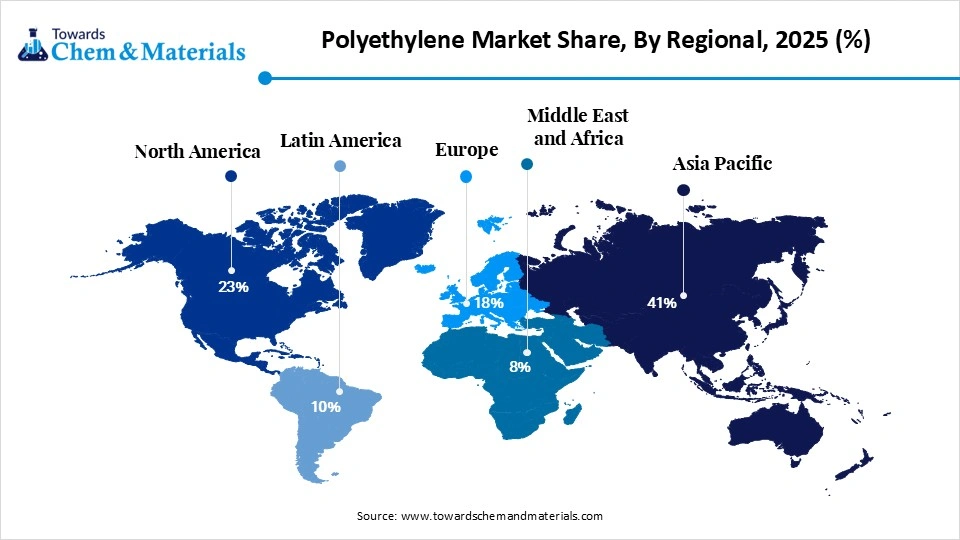

- By region, Asia Pacific dominated the polyethylene market with 41% share in 2025 and is expected to grow at the fastest CAGR of 5.6% over the forecast period.

- By region, North America held 23% market share in 2025.

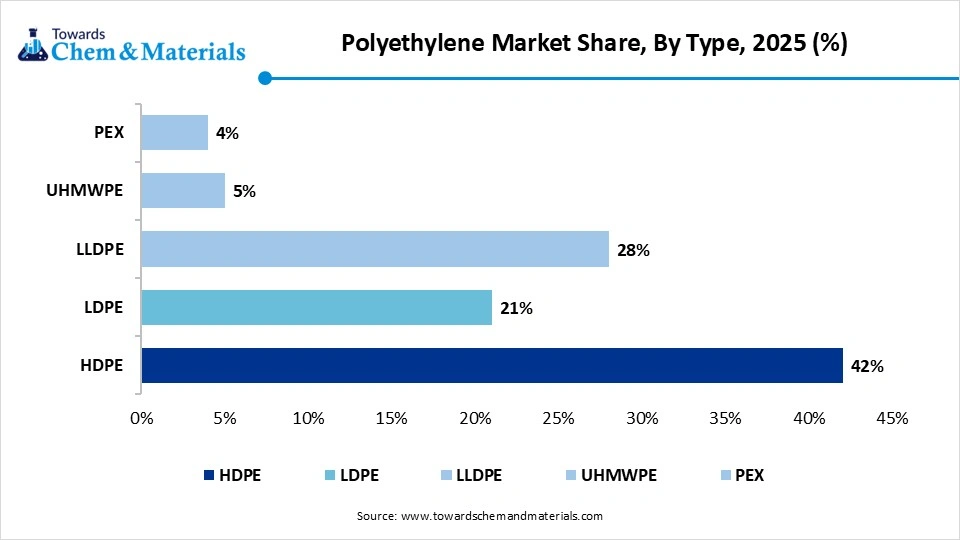

- By type, the HDPE segment dominated the market with the largest share of 42% in 2025

- By type, the LLDPE segment held 28% market share in 2025 and is expected to grow at the fastest CAGR of 5.6% over the forecast period.

- By processing technology, the extrusion segment dominated the market with a 34% share in 2025 and is expected to grow at the fastest CAGR of 5.2% over the forecast period.

- By application, packaging segment dominated the market with a 45% share in 2025 and is expected to grow at the fastest CAGR of 5.3% over the forecast period.

- By density, the high density segment dominated the market with the largest share of 48% in 2025

- By density, the low density segment held 35% market share in 2025 and is expected to grow at the fastest CAGR of 5.2% over the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2026): USD 177.10 Billion | CAGR (2026–2035): 4.95%

- Market Projected Size (2035): USD 273.57 Billion

- Market Volume (2025): 128.45 Million Tons (MT) | Volume CAGR (2026–2035): 4.35%

- Market Projected Volume (2035): 196.63 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 1,055/ton

- Average Selling Price: USD 1,285/ton

- Pricing CAGR (2025–2035): 2.8%

How is Polyethylene Market Evolving Globally?

The polyethylene market is witnessing steady growth driven by the rising demand in consumer goods construction automotive and packaging industries. The use of polyethylene for flexible packaging and infrastructure applications is growing due to increasing emphasis on recyclable and bio-based polyethylene solutions to satisfy legal and environmental requirements sustainability trends are also changing the market. Further bolstering market expansion are improvements in production efficiency and product performance brought about by major petrochemical company's capacity expansion.

Market Trends

- Sustainability-driven material innovation: The polyethylene market is increasingly shifting toward recyclable, bio-based, and circular solutions due to rising environmental concerns and stringent regulations.

- Rising demand for flexible packaging: The demand for polyethylene is growing significantly in flexible packaging applications, driven by the expansion of e-commerce and food delivery services.

- Regulatory impact on production strategies: Stringent government policies on plastic usage and waste management are compelling manufacturers to adopt sustainable and compliant production practices.

- Advancement in recycling technologies: The adoption of advanced chemical and mechanical recycling technologies is enabling efficient reuse of polyethylene and supporting circular economy initiatives.

- Strong demand from emerging economies: Rapid urbanization and industrial growth in developing regions are driving increased consumption of polyethylene across construction and consumer goods sectors.

- Capacity expansion by key players: Major industry players are expanding their production capacities to meet rising global demand and strengthen supply chain efficiency.

- Technological innovation in polymer development: Continuous advancements in polymer technology enhance polyethylene properties such as strength, flexibility, and durability for diverse applications.

- Growing adoption of lightweight materials: Industries such as automotive and packaging are increasingly adopting polyethylene to reduce product weight, improve efficiency, and lower overall costs.

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 177.1 Billion |

| Expected size by 2035 | USD 273.57 Billion |

| Growth Rate from 2025 to 2035 | CAGR 4.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 -2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Processing Technology, By Application, By Density, By region |

| Key Companies Profiled | SABIC, Dow Inc., ExxonMobil Chemical, LyondellBasell Industries, INEOS Group, Chevron Phillips Chemical, Sinopec, Braskem S.A., Formosa Plastics Corporation, Reliance Industries Limited, Borealis AG, Lotte Chemical, Mitsui Chemicals, Sumitomo Chemical, LG Chem, Arkema, Celanese Corporation |

Technological Advancements and AI

The integration of AI and automation in manufacturing processes can optimize supply chains and enhance product efficiency through smart manufacturing. The predictive analytics increase operational efficiency by lowering global production costs. The AI-powered system focuses on quality control and the development of advanced material design needed in automotive, healthcare, and telecommunication. Additionally, AI fosters innovation and development of new polymerization techniques and advanced catalysts to create polyethylene with improved strength for films in medical devices.

Supply Chain Analysis

Feedstock Procurement:

Polyethylene production depends on stable ethylene supply from oil and gas, with companies increasingly exploring bio based alternatives to reduce cost volatility.

- Key Players: ExxonMobil, Royal Dutch Shell, Saudi Aramco, Dow

Waste Management and Recycling:

The market is shifting toward recycling and circular economy practices, supported by advanced technologies and improved waste management systems.

- Key Players: Veolia, SUEZ, BAFS, LyondellBasell

Regulatory Compliance and Safety Monitoring:

Strict environmental and safety regulations are driving the adoption of advanced monitoring systems and cleaner production processes.

- Key Players: Chevron Phillips Chemical, INEOS, SABIC

Market Dynamics

Driver

Rising Demand for Sustainability and Eco-Friendly Solutions

The increasing focus on reducing environmental impact and strict regulations is driving the adoption of circular economy principles, pushing towards bio-based polyethylene and low-toxicity chemicals. Forcing manufacturers to invest in R&D to ensure sustainable products with safety and environmental standards

Restraint

Availability of alternatives, including Polypropylene and Polyethylene Terephthalate Products, to limit Polyethylene adoption Polyethylene shows chemical resistance, flexibility, moldability, and low cost, boosting demand. But the PP and PET offer superior clarity, rigidity, and heat resistance, align with the circular economy strategy, its focus on the reduction of carbon footprint. Therefore, these alternatives represent a key restraining factor for the global polyethylene market.

Market Opportunity

Are there Significant Opportunities related to Environmental Concerns and Sustainability?

The growing environmental concern and emphasis on sustainable practices are major opportunities that include bio-based polyethylene and advanced recycling. The rising focus on sustainable alternative driving market towards polyethylene derived from renewable resources. The growing investment and innovation in chemical and mechanical recycling technologies can convert plastic waste into high-quality raw feedstock for the application sector.

Segmental Insights

Type Insights

HDPE Segment Dominated the Polyethylene Market with 42% of Market Share in 2025

HDPE segment dominated the market with the largest share of 42% in 2025 motivated by its great strength resistance to chemicals and widespread applications in pipes industrial containers and rigid packaging. Its long service life and durability make it a popular choice for water management and infrastructure systems. Further bolstering its demand worldwide and growing investments in the utility and construction industries. Its adoption is also being strengthened by its increasing use in industrial dumps and chemical storage. Its long-term demand outlook is further improved by its recyclable nature and alignment with circular economy initiatives.

The LLDPE segment held a 28% market share in 2025 and is expected to grow at the fastest CAGR of 5.6% over the forecast period backed by its increased demand in film and stretch packaging applications and its exceptional flexibility. It is perfect for industrial wrapping and agricultural films due to its capacity to improve elongation and puncture resistance. Its quick growth is also a result of the retail and logistics industries' rising demand. Its expansion is also fueled by a growing desire for thin gauge to use less material. Catalyst technology advancements are also enhancing its performance attributes.

LDPE segment held the 21% market share in 2025, driven by its extensive use in agricultural films coatings and lightweight packaging because of how simple it is to process because of its softness and transparency it is frequently used in squeeze bottles lids and liners. Its steady growth is further supported by the growing need for affordable packaging options in developing nations. Its robust presence in the food packaging and healthcare industries demand even more; its industrial usage is also growing due to its compatibility with extrusion coating applications.

Processing Technology Insights

Extrusion Segment Dominated the Polyethylene Market with 34% of Market Share in 2025

The extrusion segment dominated the market with a 34% share in 2025 and is expected to grow at the fastest CAGR of 5.2% over the forecast period due to its effectiveness in large scale production of films sheets and pipes. It is very favored for continuous production processes because it lowers operating expenses and material waste. Its market position is further strengthened by rising demand for construction pipes and plastic films. Its ability to adapt to various polyethylene grades increases its manufacturing versatility. Energy efficiency and output quality are also being improved by technological developments in extrusion machinery.

Injection molding segment held the 26% market share in 2025 backed by its robust demand for producing long lasting parts for consumer goods automotive and industrial uses. It is appropriate for a variety of end use industries because it allows for the mass production of intricate shapes with high precision. Growth in the segment is also being driven by growing adoption in the production of electronics and electric vehicles its capacity to create robust yet lightweight parts help achieve sustainability objectives. Productivity and consistency are further increased by increasing automation in molding processes.

Application Insights

Packaging Segment Dominated the Polyethylene Market with 45% of Market Share in 2025

The packaging segment dominated the market with a 45% share in 2025 and is expected to grow at the fastest CAGR of 5.3% over the forecast period driven by the growing need for flexible packaging in the e-commerce food and beverage industries because of its moisture resistance and lightweight design it is perfect for prolonging the shelf life of products. Furthermore, the creation of reusable and recyclable packaging solutions is being encouraged by sustainability trend's. Demand is further accelerated by the rise of online retail and consumer convenience trends. Additionally, advances in multilayer packaging and barrier films are improving its functionality.

Construction segment held the 18% market share in 2025 backed by the growing use of polyethylene in infrastructure development pipes and insulation because of its resistance to corrosion it is frequently utilized in drainage and water distribution systems demand is being further fueled by expanding urban infrastructure projects particularly in emerging economies. Its use in geomembranes and cable insulation is also gradually growing. Its adoption is being aided by a growing emphasis on long lasting and low maintenance materials.

Density Insights

High Density Segment Dominated the Polyethylene Market with 48% of Market Share in 2025

High density segment dominated the market with the largest share of 48% in 2025 motivated by its strength and resilience for heavy duty and industrial uses because of its high tensile strength it is frequently used in pipes heavy packaging and containers its dominance if further reinforced by rising demand from the construction and industrial sectors. Its superior resistance to moisture and chemicals make it more suitable for challenging conditions. Its growth is also being aided by the increasing use of fuel tanks and industrial storage solutions.

Low density segment held the 35% market share in 2025 and is expected to grow at the fastest CAGR of 5.2% over the forecast period encourage by its adaptability and growing use in packaging and movies because of its exceptional clarity and softness it is frequently utilized in plastic bags wraps and coatings. Its use is being accelerated by growing consumer demand for lightweight and convenient packaging. Growth is also aided by its growing use in medical packaging applications. Furthermore its sustainability profile is being enhanced by developments in biodegradable blends.

Medium density segment held the 17% market share in 2025 motivated by its well balance qualities that make it ideal for specific uses. It is appropriate for packaging and piping solutions because it provides greater stress resistance than LDPE while retaining flexibility. Its increasing use in specialized industrial applications is bolstering the markets consistent expansion. The demand for gas pipes and fittings is being driven by their increasing adoption. It is appealing for mid range applications because of its cost performance balance.

Regional Insights

Asia Pacific Dominated the Polyethylene Market with 41% of Market Share in 2025

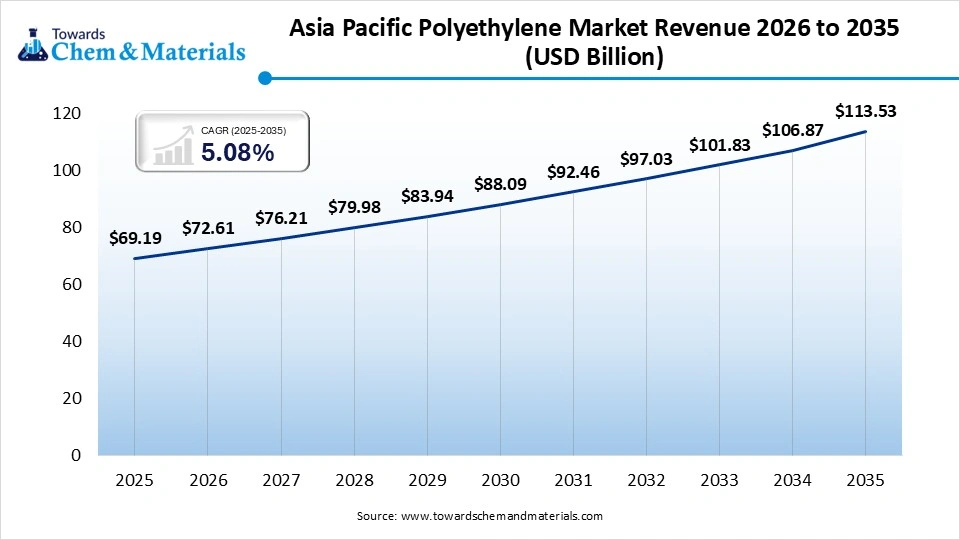

The Asia Pacific polyethylene market size was estimated at USD 69.19 billion in 2025 and is projected to reach USD 113.53 billion by 2035, growing at a CAGR of 5.08% from 2026 to 2035 Strong manufacturing bases growing populations and rising packaged goods consumption all benefit the area. Market growth is being further accelerated by government initiatives that support industrial expansion of petrochemical capacities. Sustained growth is also aided by an increase in export activity and foreign investments.

")

India Polyethylene Market Trends

India is emerging a key growth market for polyethylene fueled by the fast development of infrastructure urbanization and the growing need for flexible packaging in the retail food and e-commerce industries. Domestic production capabilities are being strengthened by government initiatives like Make in India and growing investments in petrochemical capacity. Adoption of environmentally friendly polyethylene solutions ia also being aided by increased awareness of recycling and sustainable packaging. Long term demand is also being supported by growing middle class consumption and market penetration in rural areas the use of polyethylene in various applications is also increasing due to the growth of the organized retail and FMCG industries.

North America Polyethylene Market Trends

North America held the 23% market share in 2025, backed by robust American demand and sophisticated manufacturing capabilities. A steady supply of raw materials is guaranteed by the existence of large petrochemical corporations and the availability of shale gas. Future market trends in the area are also being shaped by the growing emphasis on sustainable plastics and recycling. Competitiveness is being further boosted by innovations in polymer production and technological developments. Adoption of environmentally friendly polyethylene solutions is also being encouraged by robust regulatory frameworks.

U.S. Polyethylene Market Trends

U.S. is growing backed by plentiful shale gas resources that guarantee economical ethylene production strong demand from the automotive healthcare and packaging industries keeps the market stable. To achieve environmental and regulatory objectives, the nation is also seeing a rise in investments in sustainable polymer solutions and cutting-edge recycling technologies. Market competitiveness is further strengthened by the existence of significant petrochemical companies and ongoing technological developments. Global supply chain integration and export-oriented production are also essential for market growth.

Competitive Landscape Analysis:

Tier 1 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

|---|---|---|---|---|---|

| 1 | ExxonMobil Chemical Company | Spring, Texas | United States | One of the world's largest polyethylene producers with proprietary metallocene technologies and global manufacturing assets | HDPE, LDPE, LLDPE, Exceed™, Enable™, Exact™ performance polyethylene |

| 2 | Saudi Basic Industries Corporation (SABIC) | Riyadh | Saudi Arabia | Global leader in polyolefins with world-scale PE production plants across the Middle East, Europe, Asia, and the Americas | HDPE, LLDPE, LDPE, bimodal PE, specialty polyethylene, circular polymers |

| 3 | Dow Inc. | Midland, Michigan | United States | Industry leader in polyethylene innovation with advanced catalyst technologies and premium packaging resins | HDPE, LLDPE, LDPE, ELITE™, AFFINITY™, INNATE™, AGILITY™ polyethylene |

| 4 | LyondellBasell Industries N.V. | Houston, Texas | United States | One of the largest global PE manufacturers with proprietary Hostalen and Lupotech technologies | HDPE, LDPE, LLDPE, Hostalen®, Lupolen®, Petrothene®, CirculenRecover™ |

| 5 | China Petroleum & Chemical Corporation (Sinopec) | Beijing | China | One of the world's largest integrated petrochemical companies with extensive polyethylene production capacity serving domestic and export markets | HDPE, LLDPE, LDPE, PE compounds, specialty polyolefins |

Tier 2 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

|---|---|---|---|---|---|

| 1 | Borealis AG | Vienna | Austria | Global leader in advanced polyolefins with strong positions in infrastructure, packaging, and energy applications | Borstar® HDPE, LLDPE, pipe-grade PE, packaging polyethylene |

| 2 | Chevron Phillips Chemical Company LLC | The Woodlands, Texas | United States | Major North American PE producer utilizing proprietary MarTech™ polymerization technology | Marlex® HDPE, LLDPE, metallocene PE, specialty polyethylene |

| 3 | INEOS Group Limited | London, England | United Kingdom | One of the world's largest private petrochemical companies with extensive polyethylene manufacturing capacity | HDPE, LLDPE, LDPE, specialty PE, recycled polyethylene |

| 4 | Reliance Industries Limited | Mumbai, Maharashtra | India | Operates one of the world's largest integrated refining and petrochemical complexes with significant PE output | HDPE, LLDPE, LDPE, metallocene PE, specialty polyolefins |

| 5 | Braskem S.A. | São Paulo | Brazil | Largest polyethylene producer in Latin America and global pioneer in renewable bio-based polyethylene | HDPE, LLDPE, LDPE, I'm green™ bio-based polyethylene |

Tier 3 Companies

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Products / Material Portfolio |

|---|---|---|---|---|---|

| 1 | Formosa Plastics Corporation | Kaohsiung | Taiwan | Integrated petrochemical producer with large PE manufacturing capacity across Asia and North America | HDPE, LDPE, LLDPE, ethylene copolymers |

| 2 | Borouge PLC | Abu Dhabi | United Arab Emirates | Rapidly expanding global supplier specializing in high-performance polyethylene solutions | Borstar® HDPE, LLDPE, bimodal PE, infrastructure and packaging grades |

| 3 | PTT Global Chemical Public Company Limited | Bangkok | Thailand | Leading Southeast Asian petrochemical company with diversified polyethylene production | HDPE, LLDPE, metallocene PE, specialty polyethylene |

| 4 | Lotte Chemical Corporation | Seoul | South Korea | Major Asian petrochemical producer supplying commodity and specialty polyethylene globally | HDPE, LDPE, LLDPE, EVA, specialty polyolefins |

| 5 | MOL Group | Budapest | Hungary | Integrated Central European petrochemical producer expanding its polyethylene business through modern polymer production assets | HDPE, LLDPE, polyethylene compounds, polyolefin solutions |

Recent Developments

- In April 2026, ONGC Petro additions Limited (OPaL) announced a new MOU-linked incentive scheme for Polypropylene (PP) and Polyethylene (PE) in India. This scheme is specifically designed for the domestic markets for the month of April 2026. The announcement aims to provide targeted incentives to buyers and partners under existing memorandums of understanding.

- In January 2026, Saudi Basic Industries Corporation (SABIC) announced the sale of its European petrochemicals and ETP businesses in Europe and the America for $950 million. The move, targeting a portfolio shift toward higher-margin operations, involves divestments to firms like AEQUITA and Mutares. This restructuring aims to enhance the company's return on capital amidst an industry slowdown.

Top Companies In The Polyethylene Markets

- SABIC

- Dow Inc.

- ExxonMobil Chemical

- LyondellBasell Industries

- INEOS Group

- Chevron Phillips Chemical

- Sinopec

- Braskem S.A.

- Formosa Plastics Corporation

- Reliance Industries Limited

- Borealis AG

- Lotte Chemical

- Mitsui Chemicals

- Sumitomo Chemical

- LG Chem

- Arkema

- Celanese Corporation

Polyethylene Market Segments Covered in the Report

By Type

- High-Density Polyethylene (HDPE)

- Blow Molding Grade

- Injection Molding Grade

- Pipe Grade

- Low-Density Polyethylene (LDPE)

- Film Grade

- Coating Grade

- Linear Low-Density Polyethylene (LLDPE)

- C4 LLDPE

- C6 LLDPE

- C8 LLDP

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- Cross-linked Polyethylene (PEX)

By Processing Technology

- Injection Molding

- Blow Molding

- Extrusion

- Film Extrusion

- Sheet Extrusion

- Pipe Extrusion

- Rotational Molding

- Others

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Construction

- Pipes & Fittings

- Insulation

- Automotive

- Agriculture

- Consumer Goods

- Electrical & Electronics

By Density

- High Density

- Medium Density

- Low Density

By Region

- North America:

- U.S.

- Canada

- Mexico

- Rest of North America

- Latin America:

- Brazil

- Argentina

- Rest of Latin America

- Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

- GCC Countries

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)