Content

What is the Current Polymers Market Size and Share?

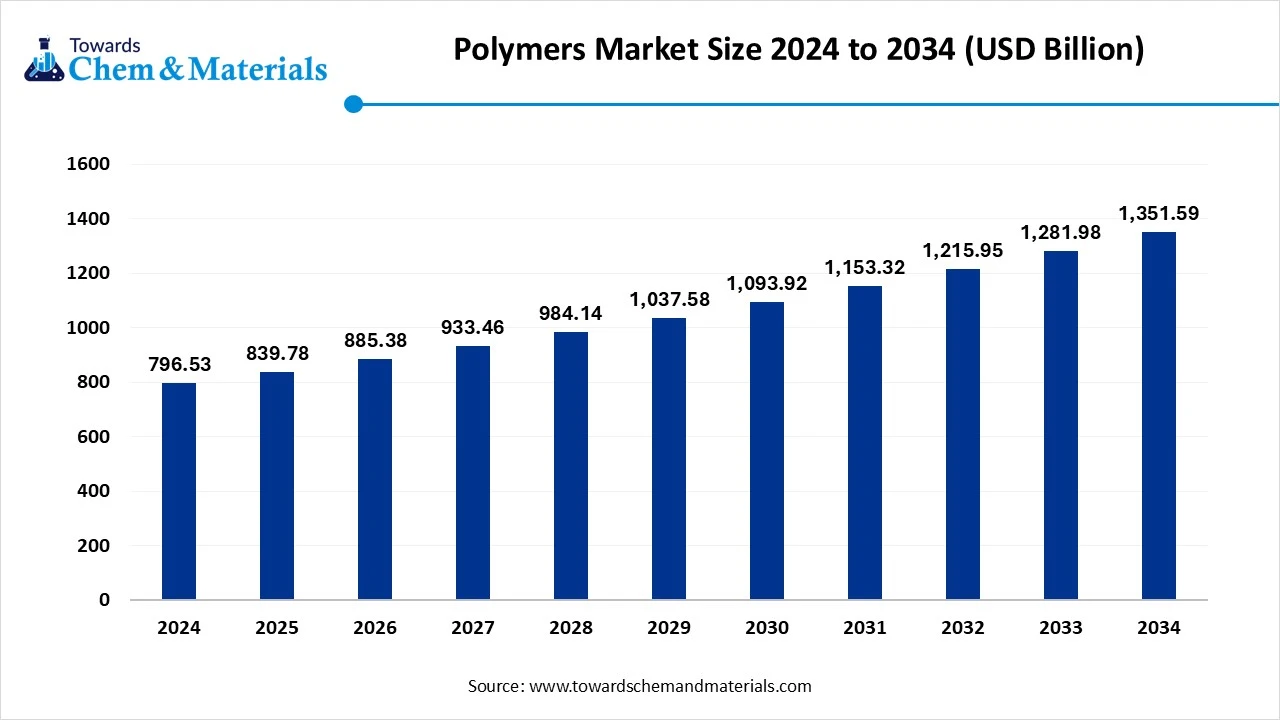

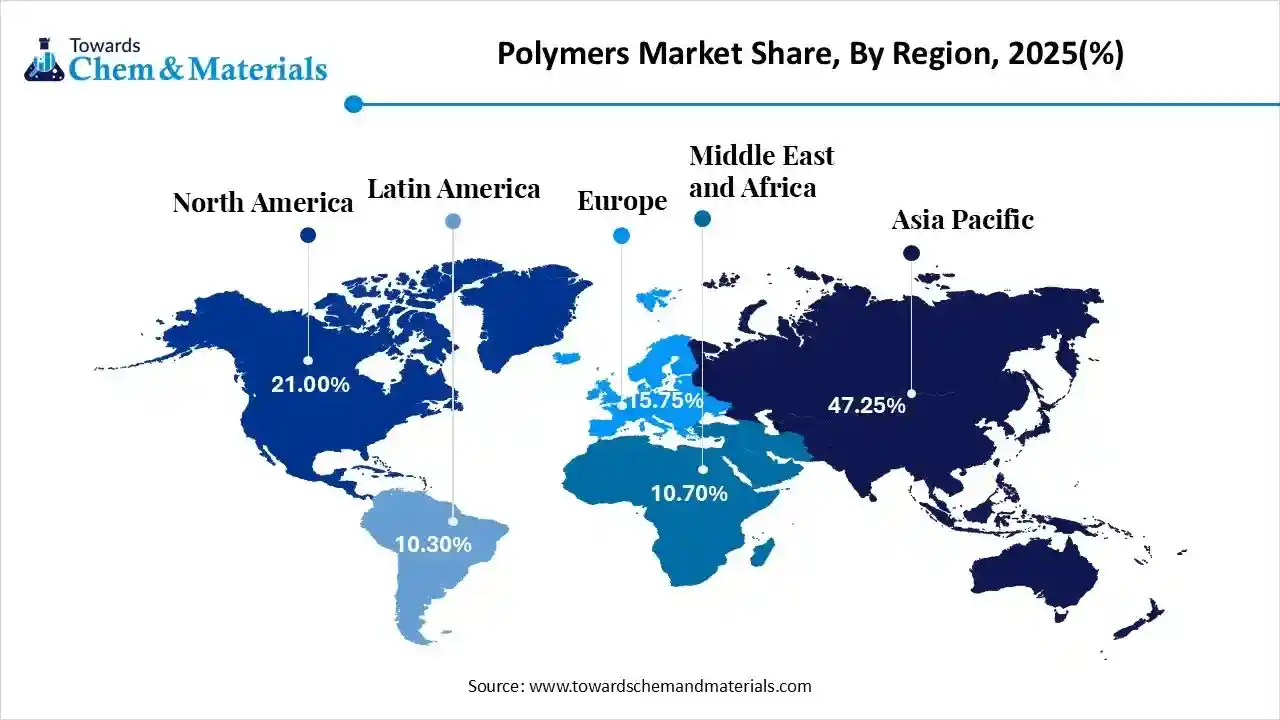

The global polymers market size was estimated at USD 839.78 billion in 2025 and is expected to increase from USD 885.38 billion in 2026 to USD 1,424.98 billion by 2035, growing at a CAGR of 5.43% from 2026 to 2035. Asia Pacific dominated the polymers market with the largest revenue share of 47.25% in 2025. The enlarged expansion of the packaging industry has accelerated industry potential in recent years.

")

Key Takeaways

- The Asia-Pacific dominated the polymers market with the largest revenue share of 47.25% in 2025.

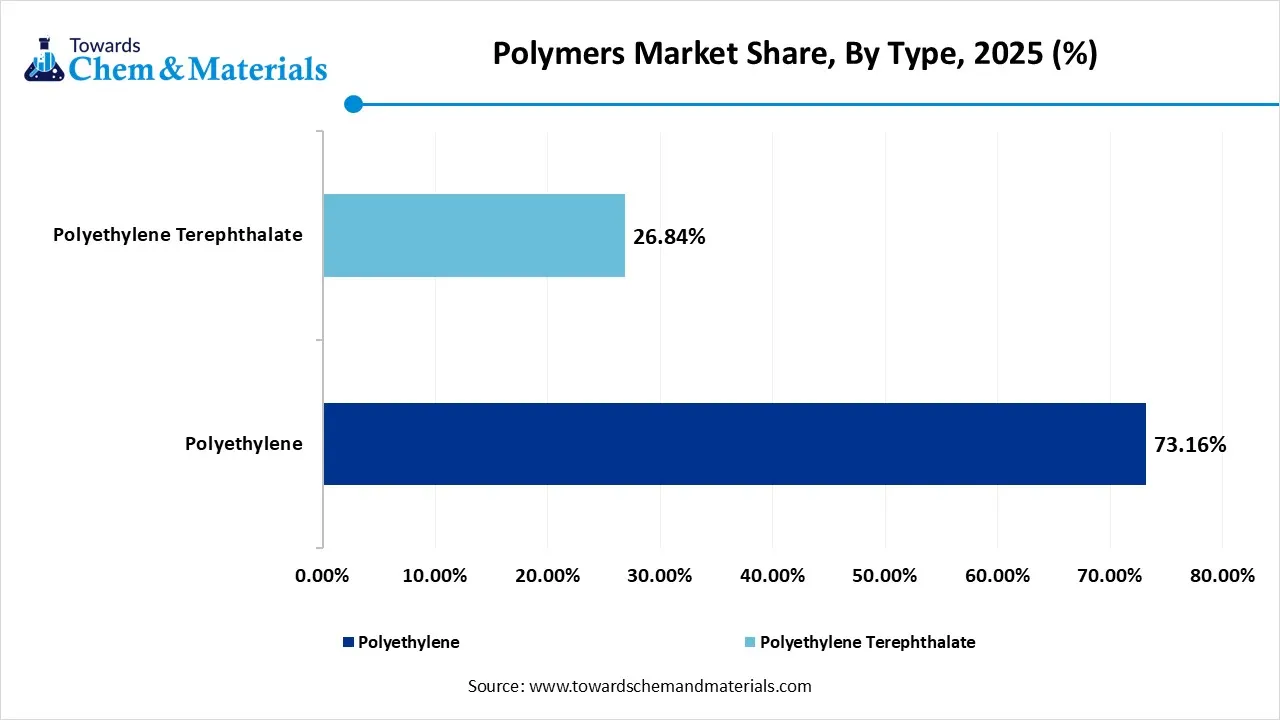

- By type, the polyethylene segment dominated the market and accounted for the largest revenue share of 26.84% in 2025.

- By origin, the synthetic polymers application segment led the market with the largest revenue share of 92.10% in 2025.

- By processing technology, the injection moulding segment dominated the market and accounted for the largest revenue share of 37.00% in 2025.

- By end-use industry, the FMCG segment led the market with the largest revenue share of 36.66% in 2025.

Market Overview

Polymers In Focus: Key Trends Driving Market Expansion

The polymers market refers to the global industry encompassing the production, distribution, and consumption of synthetic and natural macromolecules composed of repeating structural units (monomers). These materials are engineered to exhibit a wide range of physical, mechanical, and chemical properties, making them essential in applications across packaging, automotive, construction, electronics, healthcare, textiles, and other sectors.

What Factor is Driving the Polymers market?

The enlarged expansion of the packaging industry is spearheading industry growth in recent years, as polymers are considered as the ideal material used in packaging materials. Furthermore, the growth of the market is closely attached with sectors such as food delivery, e-commerce, and consumer goods, as per the recent industry survey. Also, the transportation industry is actively contributing to the industry potential as transportation materials like flexible plastic containers and films are made using polymers in recent years.

The increasing need for bio-based and biodegradable polymers has driven industry growth in recent years. Moreover, global governments have also supported these initiatives in recent years.

The integration of advanced technology in polymer production is contributing to the growth of the industry, as several manufacturers are investing in R&D for cost-effectiveness and other benefits.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 885.38 Billion |

| Expected Size by 2035 | USD 1,424.98 Billion |

| Growth Rate from 2025 to 2035 | CAGR 5.43% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Origin, By Processing Technology, By End-Use Industry, By Region |

| Key Companies Profiled | Dow Inc., Evonik Industries AG, Eastman Chemical Company, Covestro AG, Mitsui Chemicals Inc., Exxon Mobil Corporation, Royal DSM, BASF SE, Clariant International Limited, Huntsman Corporation |

Market Opportunity

Bio-Based Polymers to Lead the Charge for Sustainable Manufacturing in the Coming Years

The development of bio-based and natural polymers is expected to create lucrative opportunities for the polymers market. Global governments are seen as the heavy support for sustainable manufacturing by giving attractive benefits like tax reduction and subsidies for manufacturers in recent years.

Moreover, the manufacturer can invest in R&D for an affordable biobased polymer production method, which is likely to provide immense industry attention during the projected period, as per the future industry expectations.

Market Challenge

Eco–Friendly Production Costs May Delay Market Entry for New Players

The implementation of sustainable manufacturing initiatives is expected to hinder industry growth in the coming years, as several regions are actively implementing single-use plastic bans, which are creating growth barriers for traditional polymers in the current period. Also, the initial higher investment in eco-friendly polymer production is expected to create cost-related issues for the new market entrants and mid-sized businesses in the coming years.

Segmental Insights

Type Insights

How Did The Polyethylene Segment Dominate The Polymers Market In 2025?

The polyethylene segment held the largest share of the market in 2025 accounting for 73.16% of total revenue, due to its various applications in sectors such as films, packaging, containers, and household products. Moreover, having unique properties such as flexibility, lightweight, and durability, polyethylene has gained immense industry attention in recent years. Furthermore, the different grades availability, like polyethylene, is available in HDPE and LDPE form, which provided a wider consumer base to the segment in the past few years.

")

The polyethylene terephthalate segment is expected to grow at a notable rate during the predicted timeframe, akin to the sudden shift towards sustainability and recyclability in the packaging industry. Moreover, the increased use of beverage bottles, textiles, and food packaging has contributed to the industry growth of PET as it is considered the ideal option to produce these materials. Furthermore, the government's push towards sustainability is likely to create greater opportunities for the PET manufacturers in the upcoming years.

Polymers Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Polyethylene | 73.16% |

| Polyethylene Terephthalate | 26.84% |

Origin Type Insights

Why does the Synthetic Polymers Segment Dominate the Polymers market by the Origin Type?

The synthetic polymers segment held the largest share of the market in 2025, due to its unique characteristics, such as large-scale accessibility and cost-effectiveness. Also, the shift towards heavy manufacturing processes, the sectors such as the automotive, textiles, and packaging are actively demanding synthetic polymers in recent years, while providing a sophisticated consumer base to the manufacturers.

The natural polymers segment is expected to grow at a notable rate due to the sudden shift towards sustainable manufacturing initiatives. Moreover, several manufacturers are seen under the heavy replacement of the traditional polymers with the natural ones in recent years. Furthermore, the food packaging consumers are heavily adopting these types of polymers owing to their properties such as eco-friendliness, safety, and non-toxicity in the past few years, as per the recent industry survey.

Polymers Market Share, By Origin, 2025 (%)

| By Origin | Revenue Share, 2025 (%) |

| Synthetic Polymers | 92.10% |

| Natural Polymers | 7.90% |

Processing Technology Insights

Why Does The Injection Molding Segment Dominate The Polymers Market In 2025?

The injection molding segment dominated the market with the largest share in 2025 because it is the most common and cost-effective technique to produce complex polymer parts. It allows manufacturers to make high volumes of products with precise dimensions and consistent quality. Industries such as automotive, consumer goods, electronics, and packaging widely rely on injection moulding for efficient mass production.

The blow molding segment is expected to grow at a significant rate because of the growing demand for bottles, containers, and hollow plastic products. With rapid expansion in packaging for beverages, personal care, and household products, blow moulding is becoming more important. It allows cost-efficient mass production of lightweight yet durable products.

Polymers Market Share, By Processing Technology, 2025 (%)

| By Processing Technology | Revenue Share, 2025 (%) |

| Injection Moulding | 63.00% |

| Blow Molding | 73.00% |

| Extrusion | 5.00% |

| Compression Molding | 2.50% |

| Rotational Molding | 3.00% |

| Others (Thermoforming, Calendering, etc.) | 2.50% |

End Use Industry Insights

Why Does The FMCG Segment Dominate The Polymers Market In 2025?

The FMCG segment held the largest share of the market in 2025 due to the massive demand for packaging materials in food, beverages, cosmetics, and household goods. Polymers like polyethylene and polypropylene are widely used to produce flexible and rigid packaging that is durable, lightweight, and cost-efficient. The fast-moving consumer goods industry requires high-quality packaging to preserve product freshness and improve shelf life, which polymers provide effectively.

The medical device manufacturers’ segment is expected to grow at a notable rate during the predicted timeframe, due to growing demand for high-performance polymers in healthcare. Polymers are being increasingly used in surgical instruments, implants, drug delivery systems, and diagnostic equipment because they are lightweight, flexible, biocompatible, and safe. With aging populations and rising healthcare expenditure worldwide, the demand for medical devices is increasing sharply.

Polymers Market Share, By End-use, 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| FMCG | 63.34% |

| Automotive OEMs | 36.66% |

| Construction Firms | 5.00% |

| Electronics Manufacturers | 4.00% |

| Medical Device Manufacturers | 3.00% |

| Textile Manufacturers | 2.50% |

| Agricultural Input Producers | 2.50% |

| Industrial Equipment Manufacturers | 2.50% |

Regional Insights

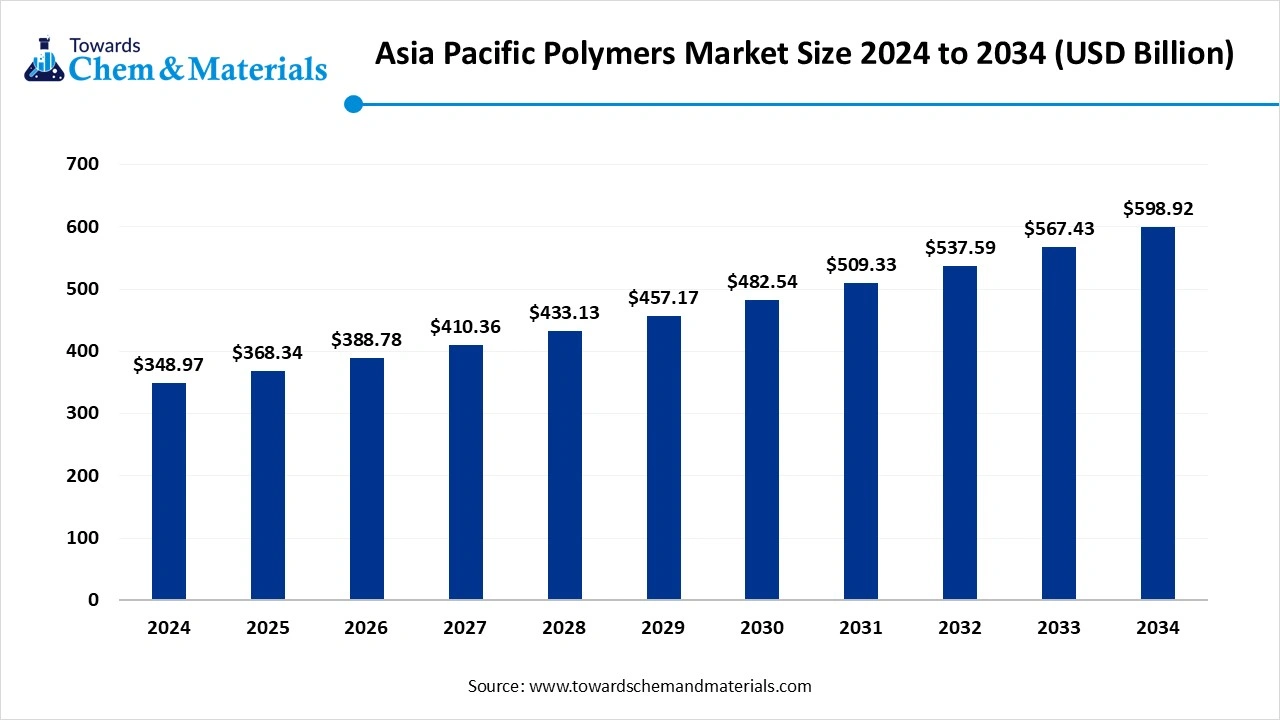

Asia Pacific polymers market size was valued at USD 396.80 billion in 2025 and is expected to be worth around USD 673.30 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.45% over the forecast period from 2026 to 2035. Asia Pacific dominated the polymers market in 2025, akin to an enlarged manufacturing structure and heavy consumer needs. Moreover, the sectors such as the packaging, construction, and automotive are actively contributing to the industry potential in recent years as they are seen under the heavy usage of the polymer in their manufacturing. Also, the regional countries are observed putting heavy investment into the polymer-based companies to fulfill the ongoing polymer requirement in their respective regions.

")

Why is China the World’s Leading Force in Polymer Manufacturing?

China maintained its dominance in the market, owing to its enlarged production and consumption of polymers in the current period. Moreover, the country is considered one of the greatest plastic producers globally, which is primarily leading industry growth while getting global attention in the past few years. Furthermore, the greater government push for domestic manufacturing is likely to contribute to the future industry growth, as per the country’s latest market observation.

")

Europe Polymers Market Trends

Europe is expected to capture a major share of the market, owing to the advanced polymer technology usage in recent years. As the regional countries such as Germany, France, and the United Kingdom are actively involved in the innovation of modern polymer technologies, which is expected to provide a sophisticated consumer base in the upcoming years, as per the future industry expectations.

How will North America surge in the Polymers Market?

North America is expected to experience notable growth in the near future. This increase is primarily driven by rapid urbanization and the investment in, as well as maintenance of, infrastructure, which necessitates durable materials such as polyvinyl chloride and high-density polyethylene for applications like pipes, insulation, and coatings. Additionally, there is a rising demand for high-performance materials in key sectors. The growing adoption of lightweight materials to enhance fuel efficiency in conventional vehicles and to extend the battery range of electric vehicles is further fueling the demand for advanced polymers.

The U.S. Polymers Market Trends:

The U.S. plays a pivotal role in this region due to its vast shale gas reserves, which provide low-cost ethylene and propylene feedstocks for polymers like polyethylene and polypropylene. The U.S. is a leader in the development of advanced, smart, and specialty polymers, particularly within the aerospace, defense, and medical sectors. Major companies such as Dow, ExxonMobil, and LyondellBasell are making significant investments in advanced recycling technologies.

Emergence of Latin America in the Polymers Market:

Latin America is emerging region in the global market, driven by rapid industrialization, increasing demand for sustainable materials, and the expansion of key end-use industries. There has been a surge in the demand for eco-friendly and biodegradable polymers, especially those derived from agricultural resources such as sugarcane and soy. Brazil and Argentina are utilizing their agricultural sectors to produce plant-based biopolymers, with the region's biopolymer market expected to grow at a rapid rate, facilitating the production of natural polymers from plants.

Brazil Polymers Market Trends:

Brazil stands out as a key player in Latin America due to its strong packaging and construction sectors and its commitment to advanced recycling and bio-based stabilizers. Companies like Braskem are investing in new recycling technologies, and Brazil is recognized as a global leader in producing green polyethylene derived from sugarcane ethanol, with major investments aimed at expanding this capacity.

Polymers Market Share, By Region, 2025(%)

| By Region | Revenue Share, 2025 (%) |

| North America | 21.00% |

| Europe | 15.75% |

| Asia Pacific | 47.25% |

| Latin America | 10.30% |

| Middle East & Africa | 10.70% |

How will the Middle East and Africa contribute to the Polymers Market?

The Middle East and Africa region is also a significant contributor to the global market. This is due to its strategic role as a low-cost manufacturing hub, extensive infrastructure development, and efforts towards economic diversification. Countries such as Saudi Arabia and the UAE are shifting away from solely relying on raw oil exports and are heavily investing in downstream petrochemical industries to create value-added polymer products, particularly in the automotive and packaging sectors. The growth of the food, beverage, and e-commerce sectors rapidly increasing the demand for flexible packaging solutions.

The UAE Polymers Market Trends

The UAE is recognized as a mature market within this region, primarily due to its focus on packaging, construction, and the growing demand for specialized polymers in areas like 3D printing and medical devices. The UAE leverages its position as a major petrochemical producer to supply raw materials. The KEZAD Polymers Park in Abu Dhabi hosts a specialized ecosystem for downstream activities, concentrating on converting raw polymers into finished products such as pipes, packaging, and automotive components.

Value Chain Analysis

Waste Management and Recycling : The waste management of polymers lies in to different methods like mechanical recycling, chemical recycling, and energy recovery

- Key Players: Waste Management Inc., Republic Services, and Clean Harbors

Chemical Synthesis and Processing : The chemical synthesis of the polymers is distributed to polymerization, living polymerization, ring-opening polymerization, and grafting.

- Key Players: BASF, DOW Inc., SABIC, and Research Institutes

Regulatory Compliance and Safety Monitoring : Polymerization processes require sophisticated regulatory compliance and safety monitoring to ensure worker safety and product quality and require regulations from institutions such as the REACH(EU), TSCA(US), GHS, and Others.

Recent Developments

- In February 2025, Tetra Pak introduced recycled polymer packaging. Moreover, the newly launched packaging material is certified by ISCC PLUS, as per the report published by the company recently.(Source: www.packaging-gateway.com)

- In January 2025, SCHOTT Pharma launched its line of syringe systems. The newly launched syringe system is called the next-gen polymer syringe system, as per the company's claim.(Source: www.contractpharma.com)

Market Top Companies

- Dow Inc.

- Evonik Industries AG

- Eastman Chemical Company

- Covestro AG

- Mitsui Chemicals Inc.

- Exxon Mobil Corporation

- Royal DSM

- BASF SE

- Clariant International Limited

- Huntsman Corporation

Segment Covered

By Type

- Thermoplastics

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyethylene Terephthalate (PET)

- Polycarbonate (PC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyamide (PA)

- Polymethyl Methacrylate (PMMA)

- Others (EVA, POM, etc.)

- Thermosetting Polymers

- Epoxy Resins

- Phenolic Resins

- Polyurethane (PU)

- Unsaturated Polyester Resins (UPR)

- Melamine Formaldehyde (MF)

- Urea Formaldehyde (UF)

- Elastomers

- Natural Rubber (NR)

- Synthetic Rubber (SBR, NBR, EPDM, etc.)

- Thermoplastic Elastomers (TPE)

By Origin

- Synthetic Polymers

- Natural Polymers (Cellulose, Starch, Proteins, etc.)

By Processing Technology

- Injection Molding

- Extrusion

- Blow Molding

- Compression Molding

- Rotational Molding

- Others (Thermoforming, Calendering, etc.)

By End-Use Industry

- FMCG

- Automotive OEMs

- Construction Firms

- Electronics Manufacturers

- Medical Device Manufacturers

- Textile Manufacturers

- Agricultural Input Producers

- Industrial Equipment Manufacturers

By Region

- North America

- U.S.

- Mexico

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Asia Pacific

- China

- India

- Japan

- South Korea

- Central & South America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

FAQ's

Select User License to Buy

Figures (5)