Content

What is the Current Plastic Compounding Market Size and Share?

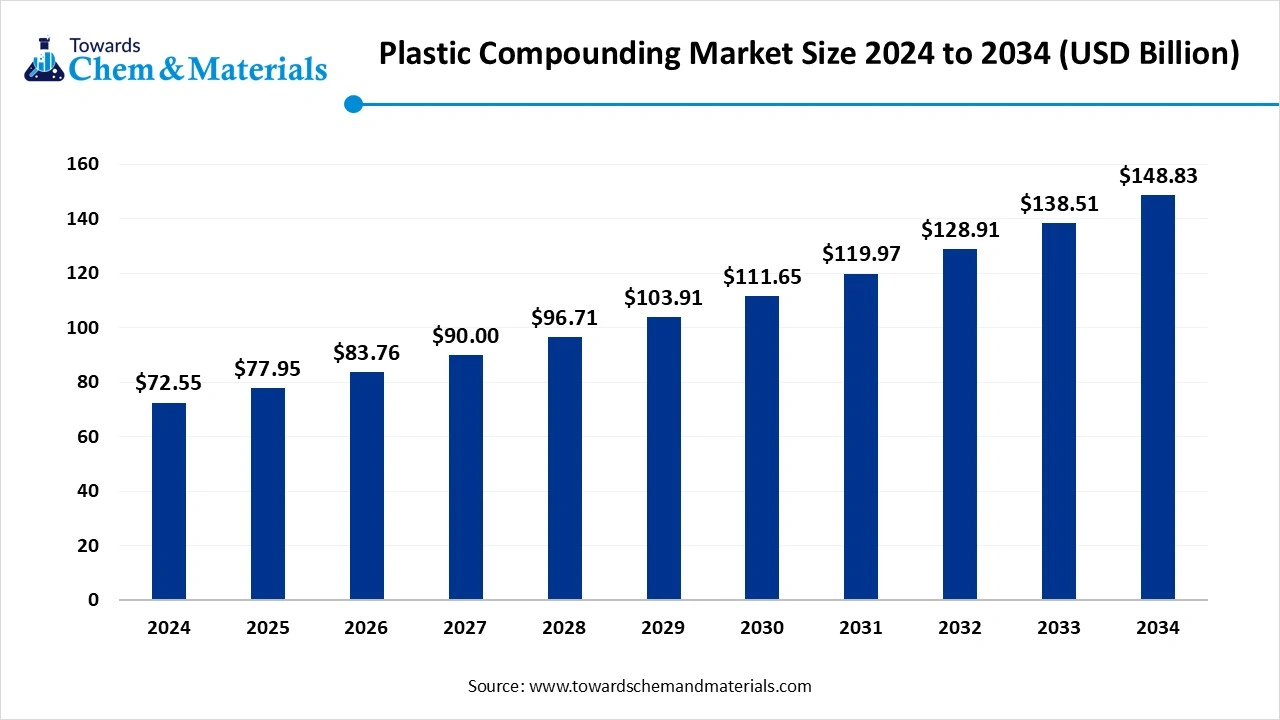

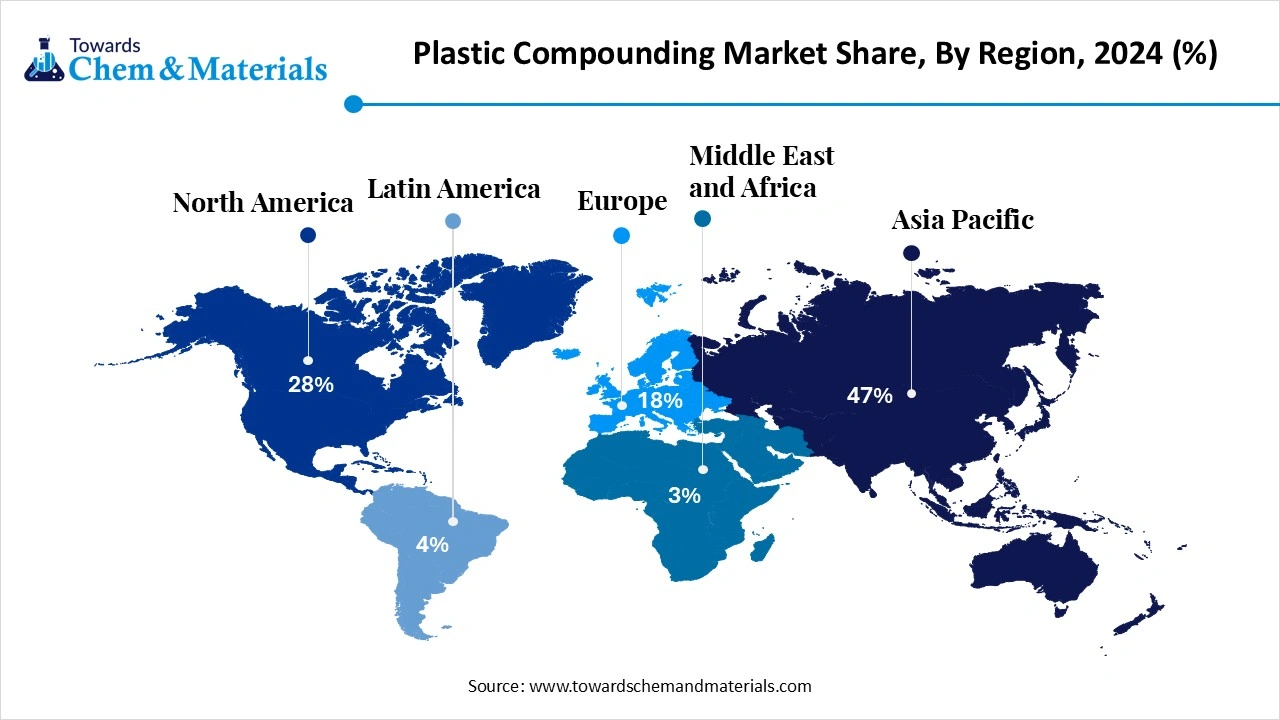

The global plastic compounding market size was estimated at USD 77.95 billion in 2025 and is expected to increase from USD 83.76 billion in 2026 to USD 159.91 billion by 2035, growing at a CAGR of 7.45% from 2026 to 2035. the Asia Pacific dominated the plastic compounding market with a market share of 47.55% in 2025. The growing urbanization and infrastructural development help the market to grow significantly in the industry.

")

Key Takeaway

- By region, Asia Pacific dominated the market 47.55% share in 2025. The growth market is due to rapid industrialization, urban development, and a robust manufacturing base.

- By region, Europe is anticipated to have significant growth in the market in the forecasted period. The growth is driven by its advanced manufacturing infrastructure and focus on sustainability

- By source, the fossil-based segment dominated the market in 2025. The demand for cost-effectiveness, wide availability, and established supply chains helps the growth.

- By source, the recycled segment is anticipated to grow significantly in the market during the forecasted period. Rising focus on sustainable alternatives to reduce environmental impact and meet regulatory requirements drives the growth.

- By product, the polypropylene segment dominated the plastic compounding market in 2025. The properties offered by the product, such as chemical resistance, low density, and high impact strength, drive the market growth.

- By product, the polyethylene segment is anticipated to grow in the forecasted period. The compound is valued for its properties like flexibility, toughness, and excellent chemical resistance, which increases the demand.

- By application, the automotive segment dominated the market in 2025. The growth is driven by the need for lightweight, durable, and cost-effective materials.

- By application, the packaging segment is anticipated to grow in the forecasted period. The growing demand for strength, flexibility, barrier protection, and lightweight characteristics of the product drives the market.

Rising Demand for Durable Materials: Plastic Compounding Market to expand

Plastic compounding is the process of combining base polymers with various additives, fillers, or reinforcements to produce tailored plastic materials with improved or specific properties. This is typically done by melting the polymer and blending it with the desired ingredients, such as stabilizers, colorants, flame retardants, or impact modifiers, using precise dosing through feeders or hoppers.

The compounding process often involves extrusion, where the molten mixture is forced through a die to form long strands. These strands are then cooled, either in a water bath or by spraying, as they travel along a conveyor. Finally, the cooled strands are chopped into uniform pellets using a granulator. These pellets are the final compound, ready to be used in manufacturing various plastic products with enhanced performance or functionality.

The plastic compounding market is driven by rising demand across key industries such as automotive, construction, electronics, and packaging. In the automotive sector, the push for lightweight, fuel-efficient vehicles has accelerated the adoption of high-performance plastic compounds. Urbanization and infrastructure development in emerging economies are also boosting the use of plastic compounds in construction. Additionally, the growing consumer electronics market requires durable and heat-resistant plastics for components.

Environmental concerns and regulations are further encouraging the development of sustainable and recyclable compounds. Technological advancements in polymer science are also enabling the creation of innovative materials with enhanced functionality and performance. These drives help the market to grow.

Market Trends

- The growing emphasis on the use of recycled products and materials, with growing concerns over environmental concerns and the use of sustainable materials, drives the growth of the market.

- The technological advancement in polymer science and the development of high-performance plastic compounds with enhanced properties drive the growth.

- Growth in automotive and electric vehicle applications, with increasing use, contributes to the overall performance of the vehicle.

- The growing demand for flexible, rigid, and sustainable packaging solutions fuels the growth of the market.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 83.76 Billion |

| Expected Size by 2035 | USD 159.91 Billion |

| Growth Rate from 2026 to 2035 | CAGR 7.45% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Source, By Product, By Application, By Region |

| Key Companies Profiled | BASF SE, SABIC, Dow, Inc., KRATON CORPORATION, LyondellBasell Industries Holdings B.V., DuPont de Nemours, Inc., RTP Company, S&E Specialty Polymers, LLC (Aurora Plastics), Asahi Kasei Corporation, Covestro AG, Washington Penn, Eurostar Engineering Plastics, KURARAY CO., LTD., Arkema, TEIJIN LIMITED, LANXESS, Solvay, SO.F.TER |

Market Dynamics

Market Drivers

The plastic compounding market is driven by rising demand from automotive, electrical and electronics, construction, and packaging industries that require customized material properties rather than commodity polymers. Regulatory fuel efficiency and emission standards enforced by agencies such as the U.S. Environmental Protection Agency and the European Commission are accelerating the substitution of metal components with lightweight compounded plastics in vehicles. In the electrical and electronics sector, safety standards related to flame retardancy, insulation performance, and durability are increasing the use of engineered compounds in connectors, housings, and cable systems. Infrastructure development programs across Asia Pacific and the Middle East are further supporting demand for compounded plastics with enhanced mechanical strength, weather resistance, and longevity.

Market Restraints

Volatility in raw material prices remains a major restraint for the plastic compounding market, as base polymers and additives are closely linked to petrochemical feedstock fluctuations. Supply disruptions caused by refinery outages, trade restrictions, or geopolitical instability can directly impact compound pricing and margins. Environmental regulations restricting certain additives, plasticizers, and flame retardants, enforced by authorities such as the European Chemicals Agency, increase compliance costs and reformulation requirements. Small and mid-sized compounders also face challenges in meeting evolving regulatory documentation and testing standards, which can limit market participation.

Market Opportunities

Opportunities are expanding through regulatory-driven demand for recycled and bio-based plastic compounds in packaging, consumer goods, and automotive interiors. Government policies such as the European Union’s Circular Economy Action Plan and Japan’s Plastic Resource Circulation Act are encouraging the use of recycled content in plastic products, increasing demand for advanced compounding technologies that improve performance consistency. High-growth applications are emerging in electric vehicles, renewable energy equipment, and data center infrastructure, where compounds with thermal stability, electrical insulation, and chemical resistance are required. Collaboration between resin producers, compounders, and OEMs is enabling the development of application-specific formulations with faster qualification timelines.

Market Challenges

Maintaining consistent quality while incorporating recycled or alternative feedstocks is a key challenge for compounders serving regulated end-use sectors. Variability in recycled material streams can affect mechanical performance, color stability, and processing behavior, requiring advanced testing and blending controls. The market also faces pressure to balance cost competitiveness with increasing requirements for sustainability reporting and lifecycle assessments. In addition, skilled labor shortages in polymer science and process engineering constrain the ability of manufacturers to scale complex formulations and adopt advanced compounding equipment efficiently.

Value Chain Analysis

- Research and Development (R&D):This focuses on developing polymer recipes, incorporating additives to meet specific end-use requirements for electric vehicles, and biocompatibility.

- Key Players: BASF SE, SABIC, Covestro AG, Arkema, DuPont de Nemours, Inc., Solvay S.A., and RTP Company.

- Raw Material Sourcing and Upstream Processing:This involves the procurement of base polymers and additives, which are petrochemical-derived or bio-based.

- Key Players: LyondellBasell Industries, the Dow Chemical Company, ExxonMobil Chemical, SABIC, andINEOS Group.

- Manufacturing:In this, raw materials are melted, blended, and extruded into homogeneous pellets to ensure proper dispersion of additives.

- Key Players: BASF, LyondellBasell, SABIC, Asahi Kasei, RTP Company, Kingfa Science & Technology, and Washington Penn.

- Conversion, Application, and Final Sale:The final, customized plastic pellets are converted by OEM manufacturers into finished products using techniques like injection molding or extrusion.

- Key Players: Volkswagen, Tesla, and Amcor.

- Post-Consumer Recycling and Circularity: With a growing number of rising environmental regulations, this stage focuses on collecting, sorting, and recycling plastic waste to be reintroduced into the compounding process.

- Key Players: Borealis AG and Sirmax Group.:

Segmental Insights

Source Insights

The fossil-based segment dominated the plastic compounding market in 2025. Fossil-based plastic compounds represent the largest segment in the market, owing to their cost-effectiveness, wide availability, and established supply chains. These compounds, derived from petroleum-based polymers like polyethylene, polypropylene, PVC, polystyrene, and ABS, offer versatility and mechanical strength, making them suitable for a broad range of applications. Industries such as automotive, construction, electronics, and packaging rely heavily on fossil-based plastics for components, casings, insulation, and containers.

Despite increasing environmental concerns, demand for fossil-based compounds remains strong due to their performance consistency and ease of processing. However, regulatory pressure and sustainability goals are gradually pushing toward alternative materials.

The recycled segment expects significant growth in the plastic compounding market during the forecast period. Recycled plastic compounds are gaining momentum as industries seek sustainable alternatives to reduce environmental impact and meet regulatory requirements. These compounds are produced from post-consumer or post-industrial plastic waste, including polyethylene, polypropylene, Polyethylene Terephthalate (PET), and polystyrene.

They are increasingly used in packaging, automotive parts, construction materials, and consumer goods. Recycled compounds offer a lower carbon footprint and help reduce landfill waste, making them attractive for companies aiming to improve their sustainability profile. Technological advancements in sorting and processing have enhanced the quality and consistency of recycled materials, which drives the growth of the market.

Product Insights

The polypropylene segment dominated the market in 2025. Polypropylene compounds are widely used in the plastic compounding market due to their excellent balance of properties, including chemical resistance, low density, and high impact strength. They are commonly utilized in automotive components, household appliances, packaging materials, and consumer products. In the automotive industry, PP compounds contribute to lightweighting and fuel efficiency, especially in interior and under-the-hood parts.

Their adaptability allows for reinforcement with fillers like glass fiber to enhance mechanical performance. The recyclability and cost-effectiveness of polypropylene further support its strong market presence. Continuous innovation in formulations is expanding its applications across more technically demanding sectors.

The polyethylene segment expects significant growth in the plastic compounding market during the forecast period. Polyethylene compounds are a key segment in the market, valued for their flexibility, toughness, and excellent chemical resistance. Available in various forms such as LDPE, HDPE, and LLDPE, these compounds are widely used in packaging films, containers, pipes, cable insulation, and household goods.

Their lightweight nature and ease of processing make them ideal for both consumer and industrial applications. In infrastructure, HDPE compounds are preferred for piping systems due to their durability and corrosion resistance. With growing interest in recyclability and sustainability, polyethylene compounds, especially recycled grades, are being further developed to align with environmental goals and circular economy efforts, which drives the plastic compounding market growth.

Application Insights

The automotive segment dominated the plastic compounding market in 2025. The automotive industry is one of the largest consumers of plastic compounds, driven by the need for lightweight, durable, and cost-effective materials. Plastic compounds are used extensively in vehicle interiors, exteriors, under-the-hood components, and electrical systems.

Materials such as polypropylene, ABS, polyamide, and reinforced composites help reduce vehicle weight, improving fuel efficiency and lowering emissions. The shift toward electric vehicles is further boosting demand for advanced plastic compounds with high thermal stability and electrical insulation. In addition, aesthetics, design flexibility, and corrosion resistance make plastics a preferred choice in automotive manufacturing. Regulatory pressure for sustainability is also encouraging the use of recycled and bio-based compounds, which drives the market.

The packaging segment expects significant growth in the market during the forecast period. The packaging industry is a major driver of the plastic compounding market, utilizing materials like polyethylene, polypropylene, PET, and polystyrene for a wide range of applications. Compounded plastics offer the strength, flexibility, barrier protection, and lightweight characteristics required for both rigid and flexible packaging formats.

These materials are commonly used in food packaging, consumer goods, pharmaceuticals, and industrial products. The sector is increasingly focused on sustainability, leading to a surge in demand for recyclable, biodegradable, and lightweight plastic compounds. Innovations in multilayer films, antimicrobial additives, and clear barrier properties are enhancing functionality, while regulatory pressures are pushing the adoption of eco-friendly solutions. This helps the market to grow.

Regional Insights

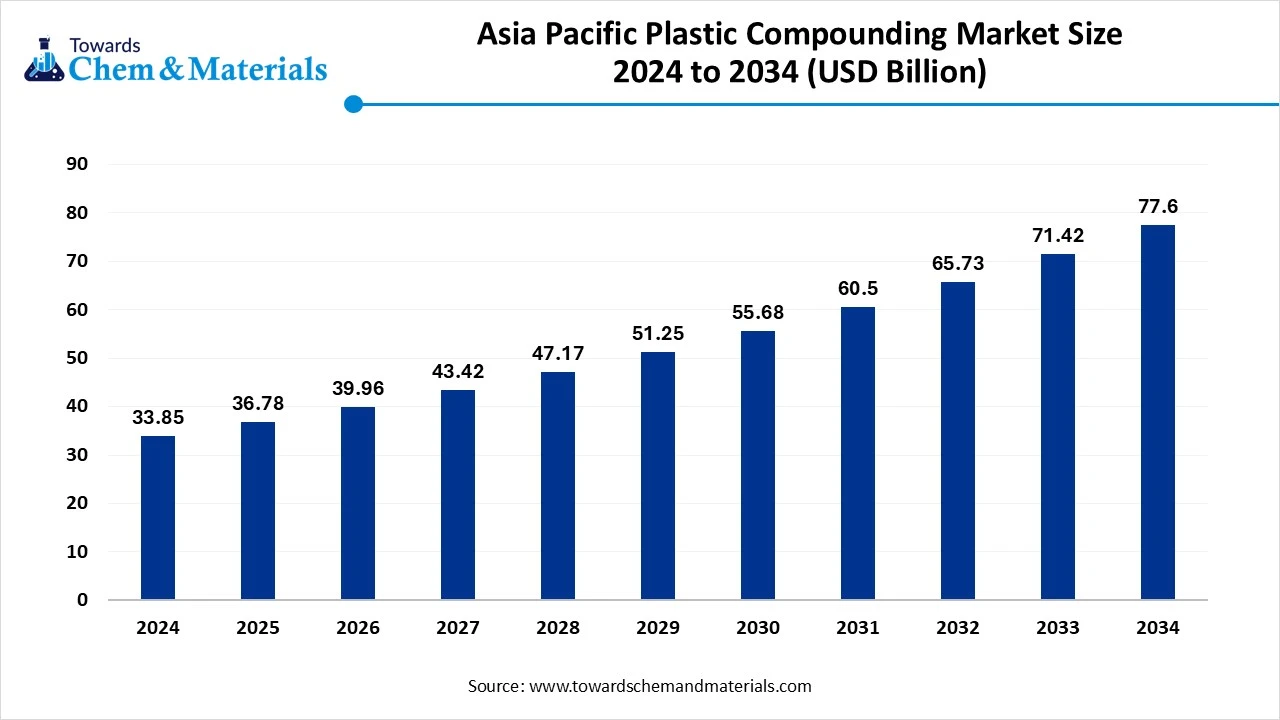

The Asia Pacific plastic compounding market size was valued at USD 36.78 billion in 2025 and is expected to be worth around USD 84.32 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 8.65% over the forecast period from 2026 to 2035.

")

The growth is seen due to rapid industrialization, urban development, and a robust manufacturing base. Countries like China, India, Japan, and South Korea are major contributors, driven by growing automotive, construction, and electronics industries.

The region benefits from low labor costs, a large consumer base, and supportive government policies promoting infrastructure and industrial growth. Additionally, rising environmental awareness is spurring demand for sustainable plastic compounds. Technological advancements and increased foreign investments are further strengthening the region’s position as a plastic compounding hub, with Asia Pacific expected to maintain the highest position in the market.

India is a leading market in plastic compounding due to the expansion of various industries.

India presents a promising landscape in the plastic compounding market due to its expanding automotive, construction, and packaging sectors. The government’s “Make in India” initiative is encouraging local manufacturing, which boosts demand for advanced plastic materials. Urbanization and infrastructure projects are creating substantial opportunities for compounded plastics in pipes, cables, and fittings.

- Furthermore, the electronics and consumer goods markets are growing rapidly, requiring high-performance compounds. Environmental regulations are also nudging the market toward bio-based and recyclable materials. India’s large skilled workforce, competitive production costs, and increasing R&D investments make it a key emerging market in the plastic compounding industry.

Europe's advanced manufacturing infrastructure and sustainability focus drive the growth of the market in the region.

Europe is anticipated to grow significantly in the plastic compounding market in the forecasted period. Europe remains a key region in the market, driven by its advanced manufacturing infrastructure and focus on sustainability. The region is known for strict environmental regulations, which are pushing industries to adopt recyclable and bio-based plastic compounds.

Major end-use sectors include automotive, construction, and electronics, all of which are evolving to meet EU climate goals. Innovation in lightweight and durable plastic materials is gaining traction, particularly for electric vehicles and green building projects. The region's strong emphasis on a circular economy is encouraging the development of advanced materials that reduce waste and enhance product life cycles, which increases the demand and helps in the growth of the market.

Germany's strong automotive and chemical sector drives the market growth.

Germany plays a central role in Europe’s plastic compounding industry because of its strong automotive, engineering, and chemical sectors. The demand for lightweight, high-performance materials is especially high in automotive manufacturing, which is increasingly shifting toward electric mobility. Germany's advanced R&D capabilities and skilled workforce make it a leader in developing innovative plastic compounds.

- Additionally, the country’s commitment to environmental standards supports the growth of sustainable plastic solutions. Industrial clusters in regions foster collaboration between manufacturers, research institutions, and policymakers, strengthening Germany’s position as a hub for high-quality and eco-friendly

How will North America be considered a Notable Region in the Plastic Compounding Market?

North America is a notable region in the global market, largely due to the push for fuel-efficient vehicles and the rapid adoption of electric vehicles, which require lightweight and durable materials to replace metal. Compounded plastics are essential for battery enclosures, interior trims, and structural parts. The United States has a mature and robust manufacturing base, particularly in the Midwest and Southeast, featuring established, high-capacity production facilities. Stringent environmental regulations and heightened consumer awareness accelerated the use of recycled and biodegradable plastic compounds.

U.S. Plastic Compounding Market Trends

The U.S. is a dominant force within the region, characterized by high-tech and innovative applications, along with considerable market consolidation. There is a strong emphasis on sustainable, bio-based, and recycled compounds to comply with EPA regulations and corporate sustainability goals. Major players in the industry, such as Dow Inc., LyondellBasell, Avient Corporation, and RTP Company, are significant contributors to this market.

Emergence of Latin America in the Plastic Compounding Market

Latin America is an emerging region in the global market. This growth is primarily driven by a surge in infrastructure development and residential and commercial construction projects in Brazil, Mexico, and Colombia, leading to increased demand for durable and lightweight building materials like PVC and polypropylene. There is also a noticeable shift toward eco-friendly solutions, as companies invest in bio-based polymers and recycled compounds to meet environmental regulations and consumer demands. The rise of e-commerce further accelerates the demand for specialized packaging materials.

Brazil Plastic Compounding Market Trends

Brazil is a key contributor within this region, focusing on expanding its industrial capacity and developing sustainable, bio-based solutions. There is a significant shift toward a circular economy, emphasizing the use of recycled feedstock and the development of bioplastics. Braskem stands out as the dominant player, recognized globally for producing green polyethylene from sugarcane to help combat plastic waste.

")

Why did the Middle East and Africa surge in the Plastic Compounding Market?

The Middle East and Africa represent another key region in the global market, driven primarily by gas-based ethane cracking, which enables low-cost, high-volume production of polypropylene and polyethylene. Countries like Saudi Arabia and the UAE are heavily investing in non-oil sectors. Major players such as SABIC are vertically integrated, ensuring a stable supply of raw materials for downstream compounding. Stricter environmental regulations, including the UAE's ban on certain plastics, are prompting a shift toward recyclable and biodegradable compounds.

UAE Plastic Compounding Market Trends

The UAE is particularly noteworthy as a mature market within the region due to rapid urban development, which drives demand for PVC pipes and insulation. The automotive sector also boosts demand for engineered plastics, with a focus on transforming both imported and local raw materials into high-performance products. Key players in this market include Borouge, APPL Industries, and Al Ghurair Investment.

Recent Developments

- In December 2025, Jyoti World Private Limited, a long-established leader in polymer engineering, announced a significant enhancement in communicating its precision machining, thick-wall molding, and materials development capabilities. The company is one of India’s rare manufacturers offering custom polymer compounding, thick-wall injection molding, and high-accuracy CNC machining within a fully integrated ecosystem, delivering consistency, performance, and engineering reliability for industrial applications.(Source : www.businesswireindia.com)

- In September 2025, Borealis announced that it is investing more than EUR 100 million to expand and upgrade its polypropylene (PP) compounding facilities in Schwechat, Austria. The new production line is scheduled to begin operations in the second half of 2026. The expansion will increase the supply of advanced PP compounds mainly used in consumer products, mobility, and infrastructure applications.(Source: www.omv.com)

Top Companies List

- BASF SE

- SABIC

- Dow, Inc.

- KRATON CORPORATION

- LyondellBasell Industries Holdings B.V.

- DuPont de Nemours, Inc.

- RTP Company

- S&E Specialty Polymers, LLC (Aurora Plastics)

- Asahi Kasei Corporation

- Covestro AG

- Washington Penn

- Eurostar Engineering Plastics

- KURARAY CO., LTD.

- Arkema

- TEIJIN LIMITED

- LANXESS

- Solvay

- SO.F.TER

Segments Covered

By Source

- Fossil-based

- Bio-based

- Recycled

By Product

- Polyethylene (PE)

- Polypropylene (PP)

- Thermoplastic Vulcanizates (TPV)

- Thermoplastic Polyolefins (TPO)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyethylene Terephthalate (PET)

- Polybutylene Terephthalate (PBT)

- Polyamide (PA)

- Polycarbonate (PC)

- Polyurethane (PU)

- Polymethyl Methacrylate (PMMA)

- Acrylonitrile Butadiene Styrene (ABS)

- Others

By Application

- Automotive

- Building & construction

- Electrical & electronics

- Packaging

- Consumer goods

- Industrial machinery

- Medical devices

- Optical media

- Aerospace & defense

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (3)