Content

What is the current Europe Polymer Market Size and Share?

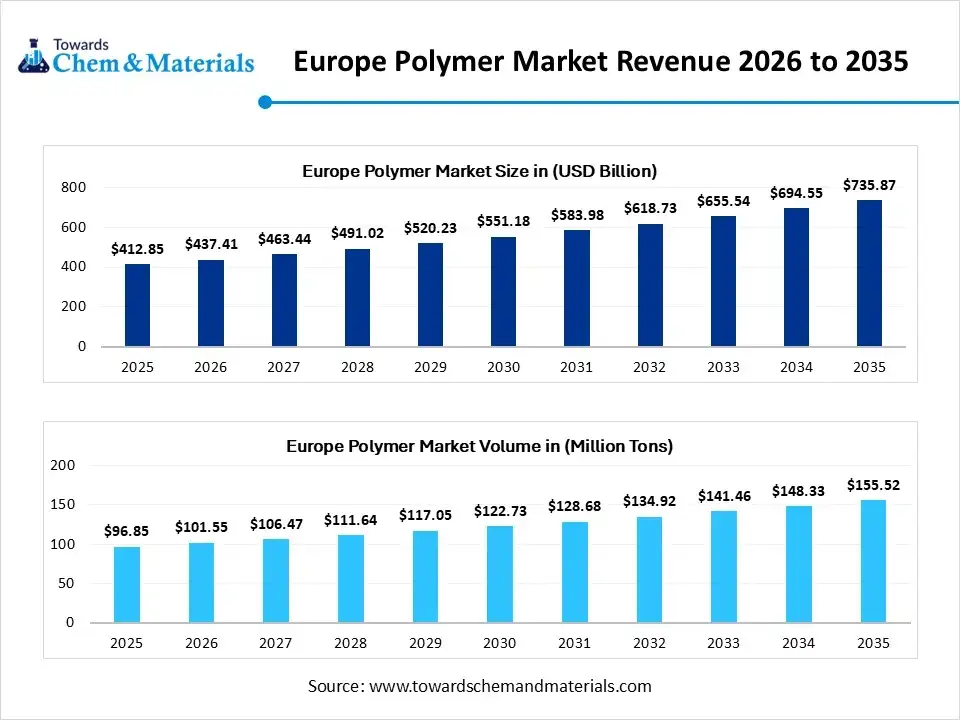

The Europe polymer market size was valued at USD 412.85 billion in 2025, is estimated to reach USD 437.41 billion in 2026, and is projected to reach USD 735.87 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035. In terms of volume, the Europe polymer market is projected to grow from 96.85 million tons in 2025 to 155.52 million tons by 2035. growing at a CAGR of 4.85% from 2026 to 2035. The increasing use of lightweight materials from various end-user industries is the key factor driving market growth. Also, the ongoing advancements in polymer chemistry and processing technologies, coupled with the growing demand for sustainable polymers, can fuel market growth further.

Key Takeaways

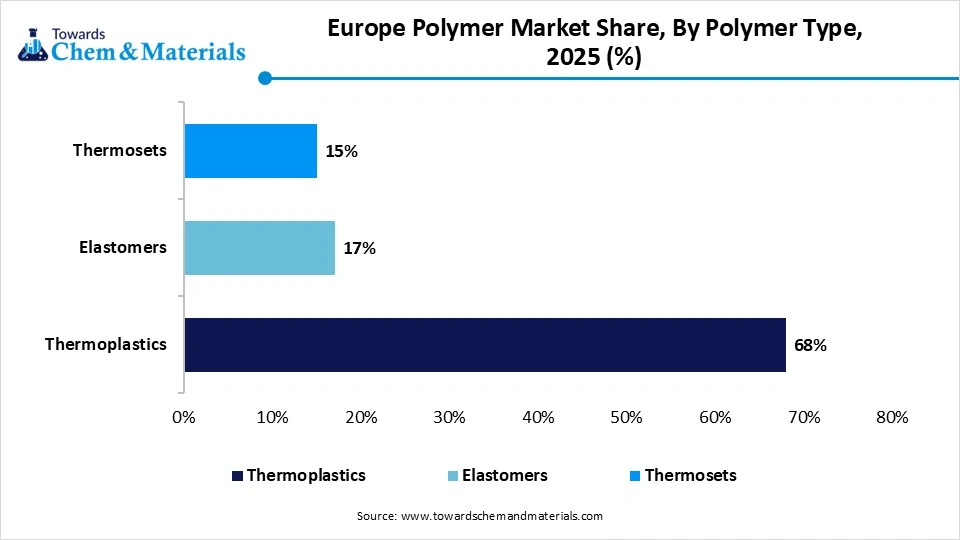

- By polymer type, the Thermoplastics segment dominated the market with a 68% share in 2025.

- By polymer type, the Elastomers segment is expected to grow at the fastest CAGR over the forecast period.

- By manufacturing, the addition polymerization segment held a 34% market share in 2025.

- By manufacturing, the emulsion polymerization segment is expected to grow at the fastest CAGR over the forecast period.

- By application, the packaging segment held a 33% market share in 2025.

- By application, the healthcare segment is expected to grow at the fastest CAGR over the projected period.

- By recycling method, the mechanical recycling segment dominated the market by holding a 62% share in 2025.

- By recycling method, the chemical recycling segment is expected to grow at the fastest CAGR over the study period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 412.85 Billion | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 735.87 Billion

- Market Estimated Volume (2025): 96.85 Million Tons | Volume CAGR (2026–2035): 4.85%

- Market Projected Volume (2035): 155.52 Million Tons

- Pricing Data (2025):

- Average Manufacturing Price (2025): USD 3,290/Ton

- Average Selling Price (2025): USD 4,125/Ton

- Pricing CAGR (2026–2035): 2.45%

What is Polymer?

A growing emphasis on achieving a circular economy target by 2030 is one of the major factors fuelling market growth. The market encompasses the manufacturing, sale, and application of polymers across various industries such as automotive, packaging, and electronics. The market includes a range of polymer types, from commodities to high-grade specialty polymers. Polymers offer properties such as flexibility, clarity, and durability for different medical products.

Europe Polymer Market Outlook:

- Industry Growth Overview: Between 2025 and 2034, the market is anticipated to witness substantial growth due to rapid innovations in blending, recycling, and smart material applications, which are enabling the new uses for eco-friendly polymers. Urbanization and infrastructure development are boosting the demand for polymer-based insulation, pipes, and window frames with other building materials.

- Sustainability Trends: The ongoing inclination towards recycled and bio-based polymers is a key sustainability trend in the market, fuelled by regulatory pressure from frameworks such as REACH and the EU Green Deal and the push for a circular economy. Also, the packaging sector is a significant driver, with a focus on compostable, biodegradable, and highly recyclable polymer solutions.

- Global Expansion: Major players in the market, such as BASF SE, are heavily investing in bio-based polymers and expanding their production portfolio. Also, Dow Inc. is working on innovating the circular economy through enhanced recycling and increased use of recycled materials by expanding manufacturing capacity in Europe.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 437.41 Billion |

| Expected Size by 2035 | USD 735.87 Billion |

| Growth Rate from 2025 to 2035 | CAGR 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Polymer Type, By Manufacturing Process, By Application, By Recycling Method, |

| Key Companies Profiled | Solvay SA, Lanxess AG, LyondellBasell Industries N.V., Versalis S.p.A., SABIC, Dow Inc., Arkema S.A., Wacker Chemie AG, Celanese Corporation, Evonik Industries AG, Asahi Kasei Corporation, Clariant AG, 3M Company, Lubrizol Corporation, DIC Corporation, Sumitomo Chemical Co., Ltd., JSR Corporation |

Key Technological Shifts in the Europe Polymer Market:

Key technological shifts in the market include the extensive adoption of digitalization, with AI and IoT, along with a significant emphasis on sustainability through recyclable, biodegradable, and bio-based polymers to fulfill circular economy goals. Integration of nanotechnology and novel recycling technologies is also a major driver for enhanced material properties.

Companies such as DOW, BASF, and Mondelēz International are heavily investing in R&D and new production lines to adapt to regulatory pressures and increasing consumer demand for eco-friendly products. Companies are shifting from linear models to circular economy practices, focusing on waste reuse and recycling.

Trade Analysis of Europe Polymer Market: Import & Export Statistics

- Based on 2023 data, Europe is a net exporter of PVC, with exports exceeding 1 million tons against imports of approximately 700,000 tons.

- The United Kingdom exported 445 shipments of polymers between June 2024 and May 2025 (TTM), a 23% increase year-over-year.

- Turkey was the top exporter to Europe in 2023. European buyers are reportedly avoiding Chinese PET due to an anti-dumping investigation.

Value Chain Analysis of Europe Polymer Market

- Feedstock Procurement : It involves the acquisition of the raw materials required for polymer production, such as petrochemicals and recycled feedstock.

- Chemical Synthesis and Processing : It refers to the industrial processes that create polymer materials from chemical components and then convert them for various applications.

- Packaging and Labelling : Packaging and labelling of the polymers in the region are heavily influenced by the new Packaging Waste Regulation (PPWR), which focuses on environmental sustainability.

- Regulatory Compliance and Safety Monitoring : It refers to the adherence to established regulations, law, guidelines, standards, and specifications related to the manufacturing, use, and disposal of polymers within the EU.

Europe Polymer Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union | REACH Regulation (EC) No 1907/2006 deals with the Registration, Evaluation, Authorization, and Restriction of Chemicals. It is a cornerstone of EU chemicals regulation |

| Germany | A major player in the European market, Germany has a strong focus on innovation and sets international standards for manufacturing processes. |

| United Kingdom | Holds significant market share, with a focus on the automotive and construction industries, and has its own national recycling initiatives. |

Market Opportunity

The Growing Use of Smart Polymers

The growing use of smart polymers is the latest trend, creating lucrative opportunities in the market. These polymers are generally in demand from the health sector. Furthermore, they are used in artificial body parts and biosensors, etc. The biocompatible nature of smart polymers is going to boost their demand and overall growth in the upcoming years.

Market Challenge

Recycling Infrastructure Limitations

The lack of adequate recycling infrastructure and waste management exacerbates plastic waste concerns, which is a major factor hindering market growth. Moreover, the market is highly competitive, which leads to pricing issues in mature segments such as construction and packaging. Hence, small and mid-sized market players may find it challenging to keep pace with regulatory and technological changes.

Segmental Insights

Polymer Type Insight

Which Polymer Type Segment Dominated the Europe Polymer Market in 2025?

The Thermoplastics segment dominated the market with a 68% share in 2025. It is a sub-segment of the thermoplastic segment. The dominance of the segment can be attributed to the growing product demand from the automotive industry for fuel-efficient and lightweight vehicle parts. Additionally, PE's low density makes it crucial for minimizing vehicle weight by enhancing overall fuel efficiency and safety.

")

The polyamide (PA) segment is expected to grow at the fastest CAGR over the forecast period. It is another subsegment of the thermoplastic segment. The growth of the segment can be credited to its superior thermal and chemical resistance, strength-to-weight ratio, and electrical insulating properties. Also, polyamide is extensively used in food packaging for applications such as sausage casings and meat packaging.

Europe Polymer Market Share, By Polymer Type , 2025 (%)

| By Polymer Type | Revenue Share, 2025 (%) |

| Thermoplastics | 68% |

| Elastomers | 17% |

| Thermosets | 15% |

- Thermoplastics: Thermoplastics dominate the European polymer market due to their versatility, ease of processing, and wide range of applications in industries such as automotive, packaging, and electronics. Thermoplastics hold 68% of the market share.

- Elastomers: Elastomers, known for their flexibility and stretchability, are increasingly used in automotive, healthcare, and consumer goods sectors. Their demand is growing due to their unique properties, making them essential in products like tires and seals. Elastomers account for 17% of the market share.

- Thermosets: Thermosets are used in applications that require high heat resistance and structural integrity, such as in electronics and aerospace. Despite their lower share, thermosets are crucial for high-performance applications. This segment contributes 15% to the market share.

Manufacturing Process

How Much Share Did the Addition Polymerization Segment Held in 2025?

The addition polymerization segment held a 34% market share in 2025. The dominance of the segment can be linked to the growing demand for polypropylene (PP) and polyethylene (PE) in automotive, packaging, and consumer goods. In addition, market players are introducing new technologies and formulations to enhance the performance and sustainability of these polymers, driving segment growth further.

The emulsion polymerization segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be driven by growing demand for high-performance and sustainable paints and coatings in the automotive and construction sectors, coupled with innovations in bio-based materials. Moreover, the EU's emphasis on sustainability and circular economy models propels the recyclable emulsion polymers.

Europe Polymer Market Share, By Manufacturing Process , 2025 (%)

| By Manufacturing Process | Revenue Share, 2025 (%) |

| Addition Polymerization | 34% |

| Condensation Polymerization | 23% |

| Emulsion Polymerization | 16% |

| Suspension Polymerization | 11% |

| Melt Polymerization | 16% |

- Addition Polymerization: Addition polymerization is widely used due to its efficiency in producing high-quality polymers such as polyethylene and polypropylene, which have applications in packaging, textiles, and automotive industries. Addition polymerization holds 34% of the market share.

- Condensation Polymerization: This process is commonly used for producing durable and heat-resistant polymers, such as polyesters and polyamides, which are crucial in applications like fibers, films, and engineering plastics. Condensation polymerization accounts for 23% of the market share.

- Emulsion Polymerization: Emulsion polymerization is essential in producing water-based coatings and adhesives, as it allows for a more sustainable production process with fewer volatile emissions. This segment holds 16% of the market share.

- Suspension Polymerization: Suspension polymerization is used primarily in the production of high molecular weight polymers for applications in paints, coatings, and automotive parts. Suspension polymerization contributes 11% to the market share.

- Melt Polymerization: Melt polymerization is widely used for its cost-effectiveness and simplicity in producing polymers like PET and nylon, which are used in textiles, packaging, and engineering plastics. This segment holds 16% of the market share.

Application Insight

Which Application Segment Dominated the Europe Polymer Market in 2025?

The packaging segment held a 33% market share in 2025. The dominance of the segment is owed to the consumer lifestyle changes, such as a preference for convenience foods and the growing e-commerce sector. The rising demand for natural, paraben-free, and cruelty-free cosmetic products is driving towards greater use of sustainable and recyclable packaging for these goods.

The healthcare segment is expected to grow at the fastest CAGR over the projected period. The growth of the segment is due to growing demand for medical devices along with the rise in chronic diseases, which fuels the demand for high-performance polymers. Additionally, the growing adoption of minimally invasive surgeries, which minimize recovery times and pain, increases the need for durable and biocompatible polymeric components

Europe Polymer Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Packaging | 33% |

| Automotive | 19% |

| Construction | 21% |

| Electrical & Electronics | 11% |

| Healthcare | 6% |

| Textiles | 7% |

| Renewable Energy | 3% |

- Packaging: The packaging industry dominates the polymer market due to the widespread use of polymers like polyethylene and polypropylene in producing flexible and rigid packaging materials. Packaging holds 33% of the market share.

- Automotive: Polymers are increasingly used in the automotive sector for lightweight components, fuel efficiency, and improved safety features. The automotive industry is adopting polymers for both interior and exterior applications, making it a key segment with 19% of the market share.

- Construction: The demand for durable, insulating, and lightweight materials in construction has led to the increased use of polymers in pipes, windows, flooring, and insulation. The construction segment represents 21% of the market share.

- Electrical & Electronics: Polymers are crucial in the electrical and electronics sector for insulating wires, producing housings, and various electronic components, owing to their electrical insulating properties. This sector contributes 11% to the market share.

- Healthcare: Polymers are essential in healthcare for applications like medical devices, drug delivery systems, and disposable items. With innovations in biocompatibility, the healthcare sector holds 6% of the market share.

- Textiles: Polymers, especially synthetic fibers like polyester and nylon, are widely used in the textile industry for clothing, upholstery, and industrial fabrics. The textiles sector captures 7% of the market share.

- Renewable Energy: Polymers are increasingly used in renewable energy applications, such as solar panel production and wind turbine blades, due to their lightweight and durable properties. This segment accounts for 3% of the market share.

Recycling Method Insight

Why Did The Mechanical Recycling Segment Dominated The Europe Polymer Market 2025?

The mechanical recycling segment dominated the market by holding a 62% share in 2025. The dominance of the segment can be attributed to the growing demand for sustainable products and ongoing investments in recycling infrastructure. Furthermore, advancements in mechanical recycling practices are driving the manufacturing of high-quality recycled plastics that meet international standards.

The chemical recycling segment is expected to grow at the fastest CAGR over the study period. The growth of the segment can be credited to the integration of recycled plastics into sectors such as automotive, packaging, and textiles. The cost-effectiveness of recyclable materials can offer incentives for companies to adopt circular practices, leading to further market expansion.

Europe Polymer Market Share, By Recycling Method , 2025 (%)

| By Recycling Method | Revenue Share, 2025 (%) |

| Mechanical Recycling | 62% |

| Chemical Recycling | 27% |

| Biological Recycling | 11% |

- Mechanical Recycling: Mechanical recycling is the most widely used method due to its simplicity and cost-effectiveness in recycling post-consumer and post-industrial plastic waste back into usable products like containers, textiles, and packaging. Mechanical recycling holds 62% of the market share.

- Chemical Recycling: Chemical recycling is gaining traction as it allows for the breakdown of polymers into their monomers, enabling the recycling of more complex plastics that are not suitable for mechanical recycling. This segment accounts for 27% of the market share.

- Biological Recycling: Biological recycling is a relatively newer method that focuses on using biological processes to break down polymers, particularly biodegradable plastics. While promising, it currently holds a smaller share of the market, contributing 11%.

Country Insights

The Western Europe held a 50% market share in 2025. The dominance of the region can be attributed to the ongoing advancements in bioplastic and innovative recycling technologies, coupled with the consumer demand for eco-friendly products. In addition, the increasing demand for energy-efficient and durable plastic components is driving regional growth soon.

The Eastern Europe is expected to grow at the fastest CAGR during the forecast period. The growth of the segment can be credited to the favorable government initiatives, rapid industrialization, and rapid infrastructure development in this European region. Furthermore, collaboration among public and private sectors with access to EU funding facilitates a dynamic advancement in the ecosystem in Eastern Europe.

Country-level Investments & Funding Trends for the Europe Polymer Market:

- Germany: Leads in R&D, advanced manufacturing, and the commercialization of Polymer Polyol technologies.

- France: France is a leader in R&D and sustainability, with strong government backing for innovative and eco-friendly solutions.

- United Kingdom (UK): Rapid adoption of next-generation Polymer Polyol technologies is supported by favourable government policies.

Top Vendors in Europe Polymer Market & Their Offerings:

- BASF SE: BASF SE is a global leader in the chemical industry, with a significant presence in the polymer market through its Performance Materials segment, offering a broad range of engineering plastics.

- INEOS Group: INEOS is a major global player in the polymer market, with major European and North American polymer businesses, and a focus on producing olefins and polyolefins for diverse industries.

- Covestro AG: Covestro AG is a leading global company in the high-tech polymer materials market, developing innovative solutions for sectors like automotive, construction, and electronics.

Other Players

- Solvay SA

- Lanxess AG

- LyondellBasell Industries N.V.

- Versalis S.p.A.

- SABIC

- Dow Inc.

- Arkema S.A.

- Wacker Chemie AG

- Celanese Corporation

- Evonik Industries AG

- Asahi Kasei Corporation

- Clariant AG

- 3M Company

- Lubrizol Corporation

- DIC Corporation

- Sumitomo Chemical Co., Ltd.

- JSR Corporation

Recent Development

- In March 2025, Agilyx ASA introduced Plastyx in partnership with Carlos Monreal for feedstock management. Plastyx aims to be the region's major feedstock supplier to the developed plastic recycling market.(Source: www.indianchemicalnews.com)

Segment Covered

By Polymer Type

- Thermoplastics

- Polyethylene (PE)

- HDPE

- LDPE

- LLDPE

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Rigid PVC

- Flexible PVC

- Polystyrene (PS)

- GPPS

- HIPS

- Polyamides (PA)

- PA6

- PA66

- Polycarbonate (PC)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyethylene Terephthalate (PET)

- Polyoxymethylene (POM)

- Polymethyl Methacrylate (PMMA)

- Polyethylene (PE)

- Elastomers

- Styrene-Butadiene Rubber (SBR)

- Nitrile Rubber (NBR)

- Ethylene Propylene Diene Monomer (EPDM)

- Thermoplastic Elastomers (TPE)

- Styrenic Block Copolymers (SBC)

- Thermoplastic Polyolefins (TPO)

- Thermosets

- Epoxy Resins

- Phenolic Resins

- Unsaturated Polyester Resins (UPR)

- Melamine Formaldehyde

- Urea Formaldehyde

- Polyurethane (Thermoset)

By Manufacturing Process

- Addition Polymerization

- Condensation Polymerization

- Emulsion Polymerization

- Suspension Polymerization

- Melt Polymerization

By Application

- Packaging

- Rigid (Bottles, Containers)

- Flexible (Films, Pouches)

- Automotive

- Interior Components (Dashboard, Seats)

- Exterior Components (Bumpers, Panels)

- Construction

- Pipes & Fittings

- Insulation Materials

- Window Profiles

- Electrical & Electronics

- Insulation Materials

- Cable Sheathing

- Healthcare

- Medical Devices

- Diagnostic Equipment

- Textiles

- Fibers & Yarns

- Nonwoven Fabrics

- Renewable Energy

- Wind Turbine Blades

- Solar Panel Components

By Recycling Method

- Mechanical Recycling

- Shredding

- Pelletizing

- Chemical Recycling

- Depolymerization

- Biological Recycling

- Composting

- Enzymatic Degradation

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (2)