Content

U.S. Specialty Polymers Market Size, Share and Trends 2026 to 2035

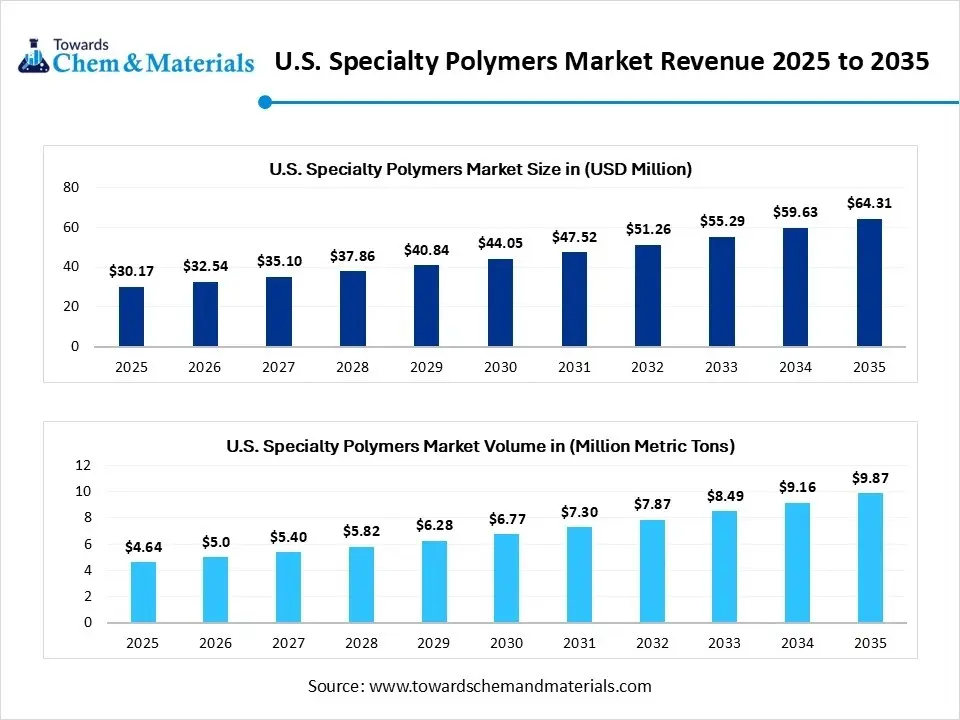

The U.S. specialty polymers market size was estimated at USD 30.17 billion in 2025 and is expected to be worth around USD 64.31 billion by 2035, growing at a CAGR of 7.86% from 2026 to 2035. In terms of volume, the U.S. specialty polymers market is projected to grow from 30.17 million metric tons in 2025 to 64.31 million metric tons by 2035. growing at a CAGR of 7.86% from 2026 to 2035. The market is a vital segment of the industrial commodities sector, experiencing ongoing growth driven by various infrastructure and manufacturing demands. As it continues to expand, the market is expected to evolve significantly, reflecting broader economic and technological trends.

Key Takeaways

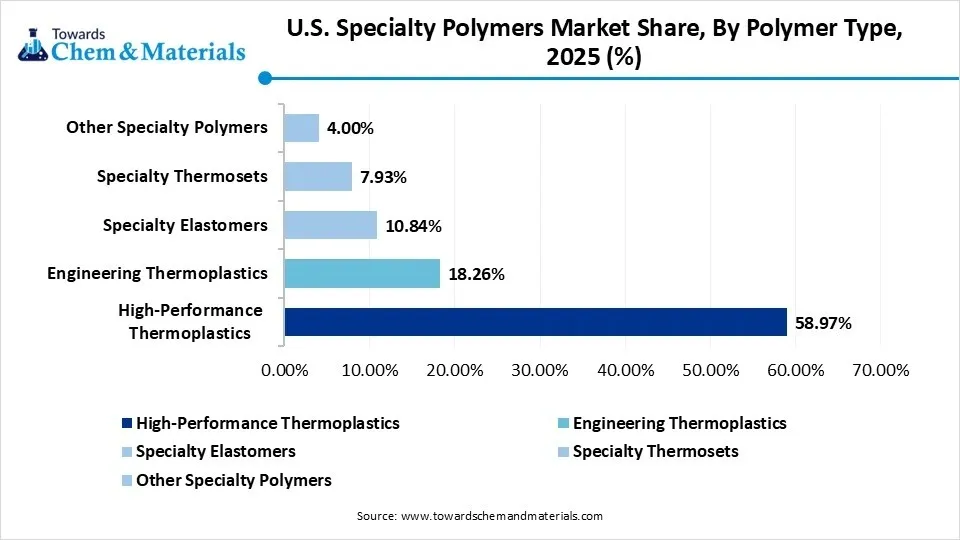

- By polymer type, the high-performance thermoplastics segment held the largest share of the market at 58.97% in 2025.

- By polymer type, the specialty elastomers segment is expected to grow at the fastest rate during the forecast period.

- By end-use industry, the automotive & transportation segment held the largest market share of 28.87% in 2025.

- By end-use industry, the medical & healthcare segment is expected to grow at the fastest rate during the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 30.17 Billion | CAGR (2026–2035): 7.86%

- Market Projected Size (2035): USD 64.31 Billion

- Market Volume (2025): 4.64 Million Metric Tons | Volume CAGR (2026–2035): 7.84%

- Market Projected Volume (2035): 9.87 Million Metric Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 4,800 per MT

- Average Selling Price: USD 6,500 per MT

Market Overview

Specialty polymers are engineered polymers with unique properties that make them suitable for specific applications, including high performance, chemical resistance, thermal stability, and electrical insulation. They are primarily used in industries like automotive, electronics, medical, aerospace, coatings, and construction.

The U.S. specialty polymers market is characterized by engineered polymers that possess unique properties tailored for specific applications. These polymers are renowned for their high performance, chemical resistance, thermal stability, and electrical insulation capabilities. Their versatility makes them essential in various industries, including automotive, electronics, medical, aerospace, coatings, and construction. As technology advances, the demand for specialty polymers is expected to rise, driven by innovations and the need for enhanced materials in manufacturing. Additionally, the growing focus on sustainability and efficiency in production processes may further propel market growth. Overall, the market is poised for significant evolution as it adapts to changing industry needs and consumer preferences.

Market Outlook

- Industry Growth Overview: Industry growth is being driven by the convergence of electrification, renewable-energy deployment, and industrial upgrading that increases copper intensity per unit of output. Fabricators and component manufacturers are expanding capacity to meet demand for motors, transformers, and high-voltage cabling.

- Meanwhile, recyclers are investing in higher-yield sorting and hydrometallurgical refining to capture urban scrap as a low-carbon feedstock. Capital-intensive mine projects remain long-lead while secondary supply can scale more rapidly, producing a layered growth profile. Strategic partnerships and offtake agreements between miners, utilities, and OEMs are smoothing the supply–demand equation. Collectively, these forces underpin m

- Sustainability Trends: Sustainability considerations stratergies, with firms pursuing low-emission smelting, renewable energy integration, and expanded recycling to reduce lifecycle carbon footprints. Circular economy models urban mining of cables, electronics, and vehicle scrap are gaining commercial traction as both environmental and supply-security measures. Water stewardship, tailings management, and community engagement have become broad level priorities for new projects.

- Major Investors: Investment originates from strategic mining houses, infrastructure funds seeking stable long-duration returns, and energy companies keen to secure materials for electrification projects. Private equity and venture capital are active in recycling, process innovation, and alloy startups that promise decarbonisation leverage. Public funding and green finance mechanisms also underwrite projects with clear emissions-reduction credentials. Collectively, capital flows favour vertically integrated models that combine production scale with environmental stewardship.

- Startup Economy: A dynamic cohort of startups focuses on urban mining, advanced separation technologies, hydrometallurgical refining, and alloy innovation for lighter, higher-performance components. Many of these ventures partner with incumbent smelters and OEMs to pilot scalable solutions. The ecosystem blends nimble innovation with capital intensity, and successful scale-ups tend to merge or partner with larger industrial players. Startups thus function as catalytic agents, accelerating decarbonization and circularity in the copper value chain.

Key Technological Shifts in the U.S. Specialty Polymers Market

The U.S. specialty polymers market is undergoing transformative technological changes driven by innovation in material science, sustainability, and advanced manufacturing. One major shift is the development of high-performance polymers with tailored properties such as heat resistance, biocompatibility, and chemical inertness for sectors like aerospace, healthcare, and electronics. Additive manufacturing 3D printing is becoming a major application and production technology, allowing polymers to be engineered at a molecular level for specific functions.

The move toward bio-based and recyclable polymers is reshaping the industry as companies reduce dependency on fossil fuels and focus on circular production systems. Advanced polymer blending and nanocomposite technologies are enabling improved mechanical strength, flexibility, and barrier performance. Additionally, AI-driven material modeling and simulation tools are accelerating polymer design and testing, helping companies shorten development cycles and innovate faster.

Trade Analysis Of the U.S. Specialty Polymers Market

- U.S. lead the world in natural polymers by $369M export in 2024.

- The largest destinations for natural polymers from U.S includes Netherlands ($6.16M), Belgium($3.68M), Japan($3.93M), Canada ($2.77M) and Mexico ($1.63M) in 2025.

- Major Importers include China ($112M), Sweden ($87.6M), Austria ($77M), Norway ($42.8M), and France ($25.9M).(Source: oec.world)

U.S. Specialty Polymers Market: Value Chain Analysis

- Raw Material Sourcing: Raw material sourcing for specialty polymers in the U.S. depends on both petrochemical and renewable feedstocks. Traditional inputs include ethylene, propylene, and styrene derived from natural gas and crude oil. However, there is a growing transition toward bio-based monomers sourced from corn, sugarcane, and lignin to produce environmentally friendly polymers such as PLA (polylactic acid) and PHA (polyhydroxyalkanoates).

- Technology Used: The technology backbone includes advanced polymerization techniques such as ring-opening polymerization, step-growth polymerization, and metallocene catalysis that offer precise control over molecular weight and structure. Reactive extrusion and plasma surface modification are also widely used to improve performance characteristics like adhesion, flexibility, and conductivity. Furthermore, automation and digital monitoring systems are being integrated into polymer plants to enhance quality, reduce waste, and ensure consistency. Collectively, these advancements are positioning the U.S. specialty polymers sector as a hub for high-performance, sustainable, and innovation-driven materials.

Market Key Trends

- Electrification of transport and grids driving sustained copper demand.

- Rapid expansion of copper recycling and urban-mining economics.

- Strategic offtake and vertical integration to secure low-carbon supply.

- Investment in low-emission smelting and renewable-powered processing.

- Geographical diversification and re-shoring of fabrication capacity.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 32.54 Billion / 5.01 Million Metric Tons |

| Expected Size by 2035 | USD 64.31 Billion/ 9.87 Million Metric Tons |

| Growth Rate from 2025 to 2035 | CAGR 7.86% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Polymer Type, By End-Use Industry |

| Key Companies Profiled | Croda International Plc , Specialty Polymers Inc. , PolyOne Corporation (Avient) , Dow Inc. , Clariant AG , Celanese Corporation, Daikin Industries, Ltd. , Huntsman Corporation , DSM Engineering Materials , Momentive Performance Materials Inc. , Lanxess AG , Eastman Chemical Company , SABIC Innovative Plastics , LG Chem , Toray Industries, Inc. |

Market Dynamics

Market Opportunity

Circular Supply Value from Scrap

The clearest opportunity lies in scaling recycling infrastructures urban mining, automated sorting, and hydrometallurgical refining to unlock secondary copper as a reliable, low-carbon feedstock. Expanding collection networks for end-of-life cables, electronics, and vehicles can insulate the market from upstream shocks. Investments that pair recycling with certification and offtake contracts will capture the growing premium for low-carbon copper.

Innovations that lower processing costs and improve recovery from complex scrap will broaden applicability across industries. Financial models that blend public incentives with private capital can accelerate facility deployment. Circular supply thus offers environmental and strategic value propositions in equal measure.

Market Challenges

Permitting and Project Realities

A major challenge in the market is the protracted permitting, environmental scrutiny, and capital intensity associated with bringing new mining and smelting capacity online. Regulatory delays and smelting capacity online. Regulatory delays and community consent processes extend lead times and increase project risk premiums.

Commodity price cyclicality can deter investment during downturns, limiting supply responsiveness to demand shocks. Logistics and concentrate supply constraints further complicate the feedstock flows to domestic smelters. These structural frictions inhibit rapid scaling of primary supply despite robust demand signals. Thus, supply-side inertia remains a persistent market constraint.

Segmental Insights

Polymer Type Insight

Why Are High-Performance Thermoplastics Segment Dominating The U.S. Specialty Polymers Market?

The high-performance thermoplastic segment is dominating the U.S. specialty polymers market by holding a share of 58.97% in 2025, driven by their dominance is underpinned by exceptional mechanical strength, chemical resistance, and thermal stability that make them indispensable across critical industries. From aerospace components to advanced automotive parts, these polymers enable lighter designs without compromising durability. Their versatility also extends to electronics, were miniaturization and heat management demand superior materials. The growing emphasis on sustainability is further propelling their use, as many variants are recyclable and exhibit longer lifespans compared to traditional plastics. This breadth of utility consolidates their status as the cornerstone of polymer innovations.

Demand for high-performance thermoplastics continues to rise as industries pursue weight reduction, fuel efficiency, and energy savings. In automotive, their adoption reduces vehicle mass, directly contributing to lower emissions and improved performance. The aerospace sector relies on them for structural applications where strength-to-weight ratios are critical. Electrical and electronic manufacturers exploit their high dielectric strength and resistance to degradation. Moreover, the healthcare sector is discovering their use in surgical tools and implants, thanks to biocompatibility and sterilization tolerance. These wide-ranging applications ensure a steady trajectory of growth for this segment.

What sets this sub-segment apart is the technological push towards newer grades and composites that enhance existing properties. Companies are investing in custom formulations that combine thermoplastics with fillers, fibers, or nanoparticles to create superior blends. As industries shift towards automation, robotics, and electrification, demand for such advanced materials will multiply. Their adaptability ensures not just relevance but centrality in next-generation applications. Global manufacturing strategies are already being recalibrated to secure steady supplies. In essence, high-performance thermoplastics are not merely a material class but an enabling technology for modern industrial progress.

")

The specialty elastomers segment anticipated the fastest growth in the U.S. specialty polymers market during the forecast period, driven by their unique elasticity, resilience, and ability to withstand harsh environments. These materials offer performance that conventional elastomers cannot, combining flexibility with high strength and chemical resistance. Their uptake in sealing systems, vibration dampening, and dynamic components is accelerating across industries. In automotive engineering, specialty elastomers ensure reliability under extreme thermal and mechanical stress. The construction sector leverages its durability in waterproofing membranes and flexible adhesives. Their ability to bridge strength with pliability has positioned them at the forefront of material innovation.

The healthcare and medical device industries are particularly drawn to specialty elastomers for their biocompatibility and customizable formulations. Applications include drug-delivery systems, prosthetics, and medical tubing that require both flexibility and non-reactivity. These elastomers also align with stricter regulatory standards, offering safer and longer-lasting solutions. Beyond healthcare, their use in consumer electronics is growing, where shock absorption and long service life are crucial. With increasing investment in renewable energy, specialty elastomers are finding roles in wind turbine components and flexible solar modules. Such cross-sectoral adoption explains the momentum behind this segment’s rapid growth.

Technological innovation is enhancing the performance profile of specialty elastomers, enabling tailored products for niche requirements. Blends with nanomaterials and bio-based inputs are being explored to augment sustainability and reduce reliance on petrochemicals. Startups are entering this space with novel formulations targeting high-margin applications. Manufacturers are also investing in automation to scale elastomer production efficiently. As industries worldwide demand reliability and resilience, specialty elastomers provide a material solution that keeps pace with evolving performance benchmarks. The trajectory is clear: this sub-segment is not only expanding but also redefining polymer performance paradigms.

U.S. Specialty Polymers Market Share, By Polymer Type, 2025(%)

| By Polymer Type | Revenue Share, 2025 (%) |

| High-Performance Thermoplastics | 58.97% |

| Engineering Thermoplastics | 18.26% |

| Specialty Elastomers | 10.84% |

| Specialty Thermosets | 7.93% |

| Other Specialty Polymers | 4.00% |

- High-Performance Thermoplastics dominate the market with a share of 58.97% driven by their superior properties and high-end industrial applications

- Engineering Thermoplastics hold 18.26% share supported by widespread use in automotive and electronics sectors

- Specialty Elastomers account for 10.84% share due to demand for flexibility and durability in advanced applications

- Specialty Thermosets capture 7.93% share reflecting usage in high-temperature and structural applications

Other Specialty Polymers contribute 4.00% share catering to niche and specialized requirements

End-User Industry Insight

Why Automotive & Transportation Segment Dominating The U.S. Specialty Polymers Market?

The automotive and transportation segment is dominating the U.S. specialty Polymers market by holding a share of 28% in 2024, driven by its lightweighting initiatives, fuel efficiency goals, and the electrification of vehicles all converge to drive this demand. Polymers replace metal in numerous structural and functional components, including bumpers, dashboards, under-the-hood systems, and electrical insulation. High-performance thermoplastics and specialty elastomers both find extensive use in this industry. As electric vehicles proliferate, the need for thermally stable, flame-retardant polymers has become even more pronounced. Thus, automotive remains both a foundation and a growth catalyst for the polymer economy.

Safety and regulatory compliance further amplify polymer adoption in this sector. Advanced polymers enhance crash resistance, provide thermal management for batteries, and enable lighter yet safer vehicle designs. Elastomers support noise reduction, sealing integrity, and vibration dampening, all crucial to ride quality. In aerospace transportation, polymers reduce weight in fuselage and cabin parts while ensuring safety under extreme conditions. Maritime and railway sectors similarly incorporate these materials for performance and longevity. Collectively, the entire transportation ecosystem is woven with polymer-based advancements.

Looking ahead, the sector’s reliance on polymers is set to deepen with the rise of autonomous and connected vehicles. These vehicles require sensors, cables, and housings with high durability and electromagnetic shielding—roles perfectly suited for advanced polymers. The shift toward hydrogen and hybrid propulsion systems also necessitates materials capable of handling new stresses and environments. Manufacturers are increasingly co-developing polymer solutions with OEMs to achieve bespoke performance. With stricter emissions norms, this symbiosis between automotive and polymer suppliers will intensify. Automotive and transportation, therefore, remains not only the largest but also one of the most strategically significant end-use markets.

Medical and healthcare segment expects the fastest growth in the U.S. specialty polymers market during the forecast period, underpinned by the sector’s unrelenting demand for performance, safety, and biocompatibility. Advanced polymers are critical in prosthetics, implants, surgical instruments, and diagnostic devices. Elastomers are employed in catheters and tubing, while thermoplastics are used in sterile packaging and surgical-grade tools. The shift toward minimally invasive procedures and personalized medicine intensifies the reliance on materials with specialized performance characteristics. Polymers that withstand sterilization cycles while maintaining integrity are especially valued. This expansion highlights healthcare’s central role in shaping polymer innovation.

The pandemic underscored the importance of resilient healthcare supply chains and accelerated adoption of advanced materials. Disposable medical devices, protective equipment, and flexible diagnostic kits all benefited from polymer innovation. Specialty elastomers gained prominence in wearable health monitors, enhancing comfort and durability. High-performance thermoplastics were deployed in ventilator components and filtration devices. With ageing populations worldwide, demand for such applications is poised to rise exponentially. Healthcare thus constitutes not just a growth segment but a societal imperative

Future growth will be catalyzed by breakthroughs in bio-based and bioresorbable polymers designed specifically for medical applications. Research collaborations between material scientists, universities, and device manufacturers are already expanding the frontiers of possibility. Innovations such as drug-eluting stents, 3D-printed implants, and smart polymers that respond to physiological cues exemplify the sector’s trajectory. Startups are entering the ecosystem with customized formulations for precision medicine. The confluence of regulation, innovation, and patient-centric care ensures that healthcare will remain the fastest-growing and most dynamic consumer of advanced polymers. This segment represents the intersection of technology, humanity, and material science at its finest.

U.S. Specialty Polymers Market Share, By End-Use Industry, 2025(%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Automotive & Transportation | 28.87% |

| Electrical & Electronics | 18.64% |

| Medical & Healthcare | 14.12% |

| Aerospace & Defense | 11.38% |

| Building & Construction | 9.26% |

| Coatings, Adhesives & Sealants | 10.73% |

| Consumer Goods | 7.00% |

- Automotive & Transportation dominate the market with a share of 28.87% driven by increasing demand for lightweight and high-performance materials

- Electrical & Electronics hold 18.64% share supported by rising use in advanced electronic components and insulation applications

- Medical & Healthcare account for 14.12% share due to growing demand for high-quality and biocompatible materials

- Aerospace & Defense capture 11.38% share reflecting usage in high-strength and temperature-resistant applications

- Coatings, Adhesives & Sealants contribute 10.73% share driven by industrial and construction applications

- Building & Construction hold 9.26% share supported by infrastructure development and material durability needs

- Consumer Goods account for 7.00% share reflecting steady demand across various end-use products

Country Insights

How West is Dominating the U.S. Specialty Polymers Market?

West dominates the regional narrative for U.S. specialty polymers market holding a share of 42% in 2024, due to its proximity to major porphyry copper deposits, established mining districts, and concentrated smelting and fabrication infrastructure. The region benefits from integrated supply chains that connect mines to ports and domestic processing facilities, enabling relatively shorter logistics and enhanced responsiveness. Historical investment in mining services and metallurgy clusters provides skilled labor and specialized contractors that accelerate project delivery. Furthermore, West America’s established regulatory and community engagement frameworks though exacting, provide clearer pathways for project maturation. As a consequence, the region hosts the bulk of primary production capacity and remains pivotal to national supply security.

West America’s dominance also stems from its strategic position as a gateway for imported concentrates from neighbouring international sources, allowing processors to blend feedstocks for optimal metallurgical performance. Renewable energy projects in the region facilitate decarbonised processing pilots, aligning extraction with sustainability goals. Mining services, equipment OEMs, and smelters co-located in this geography create productive synergies that lower total cost of delivery. The region thus functions as both the industrial heartland and the innovation testbed for lower-carbon copper value chains.

Arizona, with its deep porphyry systems and mining heritage, anchors domestic copper output and investment, while Nevada contributes diversified mineral services and refining capacity together forming the industrial axis of U.S. copper production.

Why Northeast is Fastest Growing?

Northeast America is the fastest-growing regional market driven by rapid urban infrastructure upgrades, grid modernization projects in dense population centres, and accelerated adoption of electrified public transport systems. Demand in this region is skewed toward high-value fabrication transformers, distribution cables, and building retrofits allowing local fabricators to capture premium margins. The Northeast’s dense logistics networks and proximity to major consumption centres make it attractive for recycling hubs that can rapidly collect and process end-of-life copper. Public and private investments in resilient urban infrastructure further catalyze near-term procurement. Consequently, this region is registering the most dynamic incremental demand growth nationally.

New York’s infrastructure renewal programmes and expansive transit systems drive cable and transformer demand, while Massachusetts’ concentration of advanced manufacturing and research institutions fosters high-value fabrication and recycling innovation together making the Northeast an engine of near-term copper intensity.

Recent Developments

- In September 2025, Evonik Industries, a specialty chemical company, has launched a production line at its biomanufacturing facility in Slovakia that will produce several metric tons of silk protein annually.(Source: cen.acs.org)

- In February 2025, Ashland proudly announced its compliance with forthcoming USP-NF monographs for Lactide and Glycolide polymers at the Oakwood Laboratories joint webinar, unveiling three verified versions that underscore its leadership in advanced polymer innovation.(Source: www.alchempro.com)

Top Companies

- 3M Company (is a multinational conglomerate with a diverse portfolio of products, heavily driven by its expertise in materials science.)

- Arkema S.A. (is a global specialty materials company focused on providing innovative and sustainable materials.)

- BASF SE ( provides one of the world's largest chemical companies, BASF has a vast and integrated production network.)

- Evonik Industries AG (Evonik is a global leader in specialty chemicals, known for its customer-centric innovation.)

- Solvay S.A. (Historically a diversified chemical company, Solvay underwent a significant transformation, splitting its operations into two independent publicly listed companies.)

Other Top Companies

- Croda International Plc

- Specialty Polymers Inc.

- PolyOne Corporation (Avient)

- Dow Inc.

- Clariant AG

- Celanese Corporation

- Daikin Industries, Ltd.

- Huntsman Corporation

- DSM Engineering Materials

- Momentive Performance Materials Inc.

- Lanxess AG

- Eastman Chemical Company

- SABIC Innovative Plastics

- LG Chem

- Toray Industries, Inc.

Segments Covered in the Report

By Polymer Type

- High-Performance Thermoplastics

- Polyetheretherketone (PEEK)

- Polyetherimide (PEI)

- Polyphenylene Oxide (PPO)

- Polyphenylene Sulfide (PPS)

- Liquid Crystal Polymers (LCPs)

- Polyetherketoneketone (PEKK)

- Engineering Thermoplastics

- Polycarbonate (PC)

- Polyamide (Nylon)

- Polyesters (PET, PBT)

- Polyvinylidene Fluoride (PVDF)

- Specialty Elastomers

- Fluoroelastomers

- Silicone Elastomers

- Thermoplastic Elastomers (TPEs)

- Nitrile Rubber (NBR)

- EPDM (Ethylene Propylene Diene Monomer)

- Butyl Rubber

- Specialty Thermosets

- Epoxy Resins

- Vinyl Ester Resins

- Phenolic Resins

- Polyurethane Resins

- Polyester Resins

- Other Specialty Polymers

- Conductive Polymers

- Biodegradable Polymers

- High-Temperature Polymers

By End-Use Industry

- Automotive & Transportation

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Electrical & Electronics Systems

- Electrical & Electronics

- Semiconductors

- Insulation Materials

- Connectors & Switches

- Displays & Lighting

- Medical & Healthcare

- Medical Devices

- Drug Delivery Systems

- Diagnostic Equipment

- Packaging Materials

- Aerospace & Defense

- Aircraft Components

- Spacecraft Components

- Military Equipment

- Building & Construction

- Pipes & Fittings

- Roofing Materials

- Flooring

- Insulation

- Coatings, Adhesives & Sealants

- Architectural Coatings

- Industrial Coatings

- Automotive Coatings

- Adhesives

- Sealants

- Consumer Goods

- Packaging

- Household Appliances

- Sports Equipment

- Toys

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (2)