Content

What is the Current Magnesium Oxide Market Size and Share?

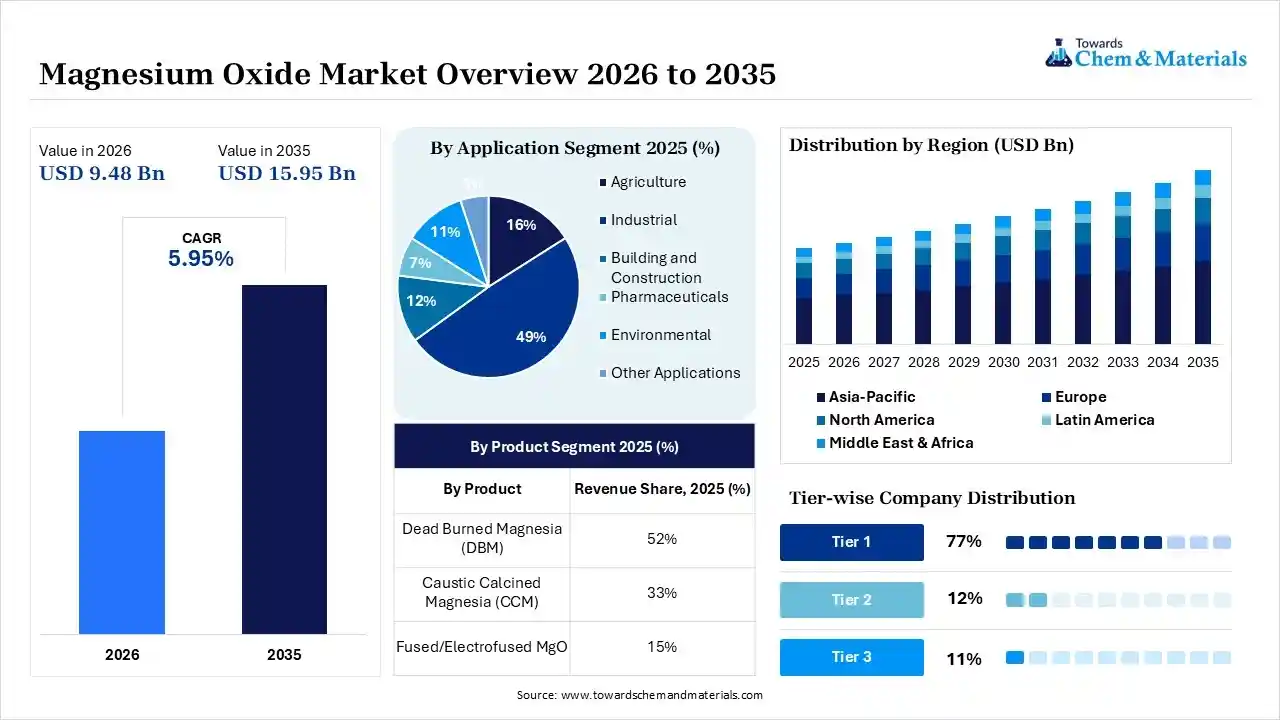

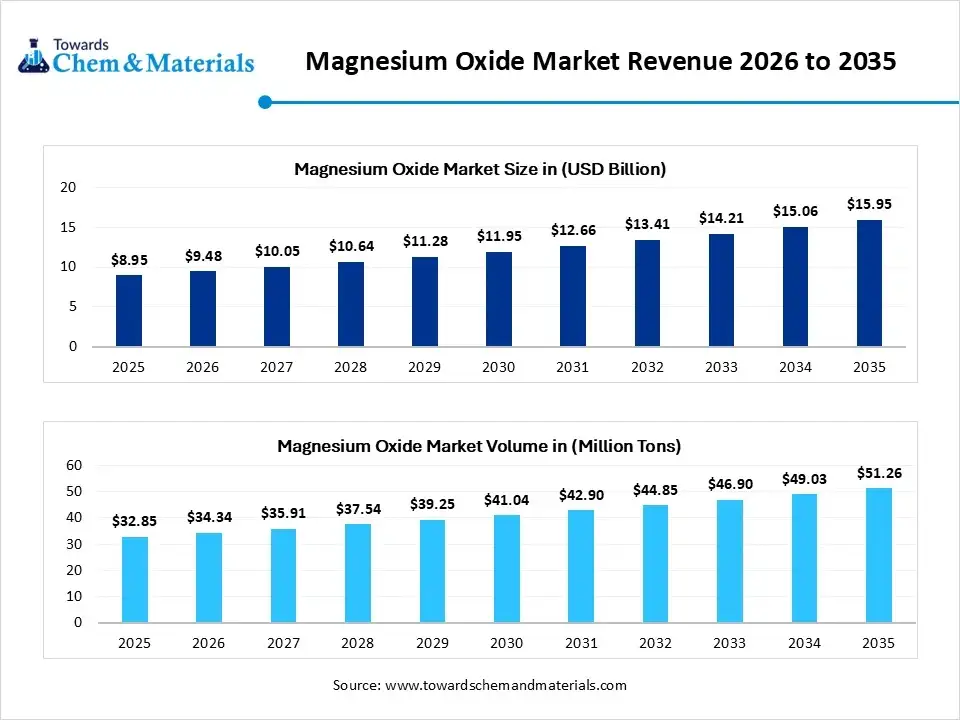

The global magnesium oxide market size was valued at USD 8.95 billion in 2025, is estimated to reach USD 9.48 billion in 2026, and is projected to reach USD 15.95 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the magnesium oxide market with the largest revenue share of 49% in 2025 and is expected to grow at the fastest CAGR of 6.05% during the forecast period. In terms of volume, the magnesium oxide market is projected to grow from 32.85 million tons in 2025 to 51.26 million tons by 2035. growing at a CAGR of 4.55% from 2026 to 2035. The growth of the market is driven by the expanding steel and cement industries, along with the rising adoption of fire-resistant construction materials, aligning with strict environmental regulations, which fuel growth. The key players like Israel Chemicals Ltd., Nedmag, and Martin Marietta Magnesia Specialities play a significant role in the market by growing investment and application, according to the report.

Market Highlights

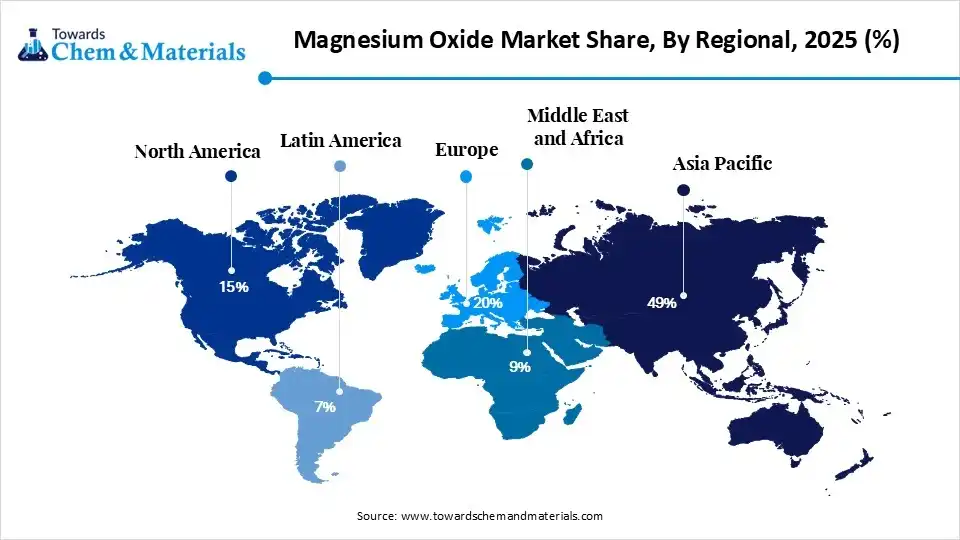

- By region, Asia Pacific dominated the market with a share of 49% in 2025. Mature industrial base supports demand.

- By region, North America held 15% market share in 2025 and is expected to experience the fastest growth with a CAGR of 6.80% in the forecast period. The large steel sector consumes significant MgO volumes.

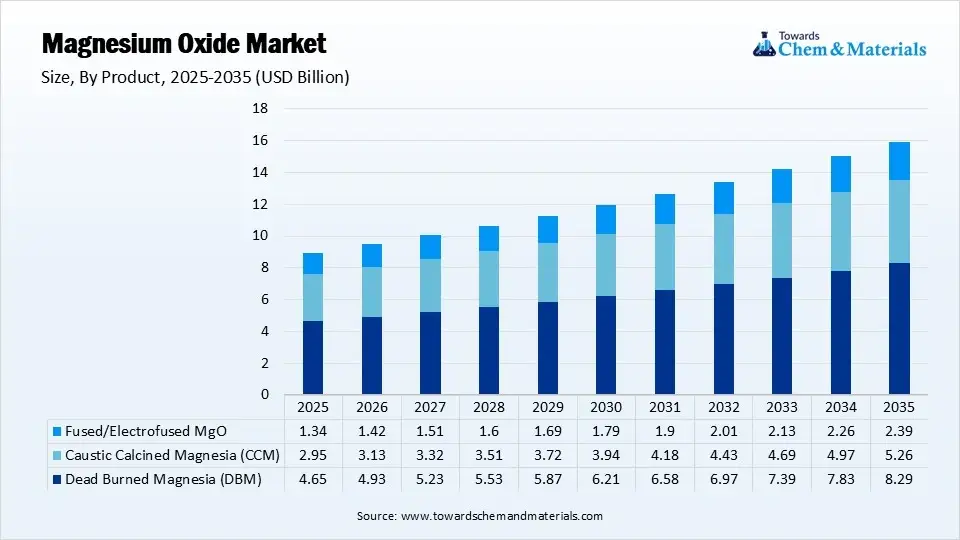

- By product, the dead burned magnesia (DBM) segment dominated the market with 52% share in 2025. Strong refractory demand from the steel and cement industries.

- By product, the caustic calcined magnesia (CCM) segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.40% in the forecast period. Agricultural nutrient management boosts demand.

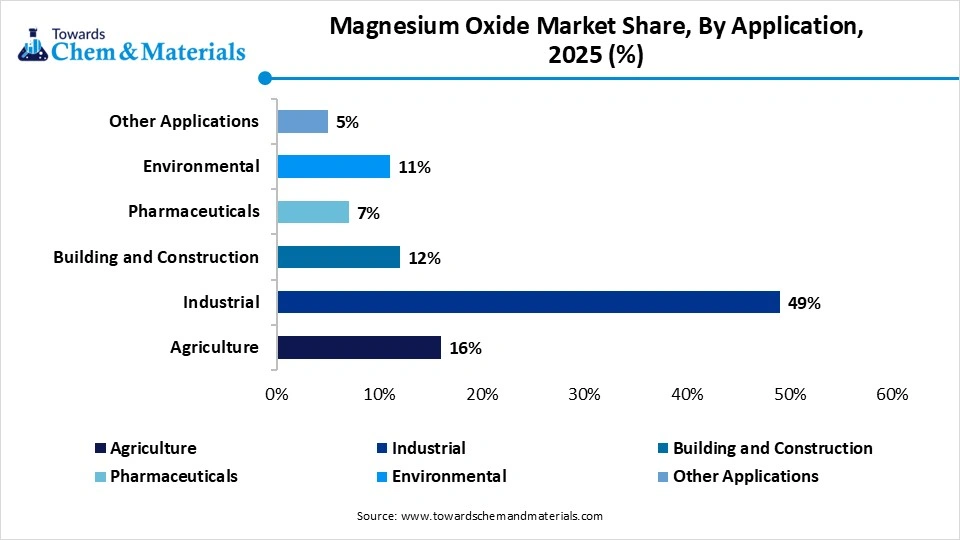

- By application, the industrial segment dominated the market with 49% share in 2025. Steel, refractory, and metallurgical sectors consume large volumes.

- By application, the environmental segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.10% in the forecast period. Wastewater treatment investments accelerate globally.

Quick Stats at a Glance

- Market in Size 2025: USD 8.95 Billion | CAGR (2026–2035): 5.95%

- Market Estimated Size in 2026: USD 9.48 Billion

- Market Projected Size by 2035: USD 15.95 Billion

- Asia Pacific: largest Regional Market Revenue Share of 49% in 2025|USD 4.39 Billion

- North America: Fastest-growing Regional Market Revenue Share of 15% in 2025|USD 1.34 Billion

- By country: The China held the largest Market share of 52% in 2025

- Market Volume in 2025: 32.85 Million Tons| Volume CAGR (2026–2035): 4.55%

- Market Estimated Volume in 2026: 34.34 Million Tons

- Market Projected Volume by 2035: 51.26 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 245/Ton

- Average Selling Price: USD 395/Ton

- Pricing CAGR (2026–2035): 3.19%

What Is the Significance of the Magnesium Oxide Market?

The magnesium oxide market is crucial due to its role as an essential raw material across heavy industries, agriculture, and healthcare. Its high thermal stability, chemical resistance, and fireproof qualities make it vital for infrastructure, sustainability, and health. Dead-burned magnesia, valued for its high melting point, is key in producing bricks and linings for steel furnaces, cement kilns, and glass manufacturing.

The construction industry increasingly uses MgO for fire-resistant materials like cement boards and panels that resist fire, moisture, and mold. Additionally, MgO is widely employed in flue gas desulfurization to remove sulfur dioxide emissions and in industrial wastewater treatment as a neutralizer. It is also used as a mineral supplement in animal feed to prevent magnesium deficiency and to enrich soil in agriculture. Pharmaceutical-grade MgO is a common component in antacids, laxatives, and dietary supplements.

For instances,

- Paul Lohmann announced the launch of LomaChelateX Magnesium Bisglycinate, which provides fewer gastrointestinal side effects and high bioavailability, targeting gut health.(Source: nutritioninsight.com)

Global Investment Flow for Magnesium Oxide Market 2026

Investments are surging globally in the magnesium oxide market as companies and governments prioritize supply-chain resilience, sustainable construction, and high-performance electronics.

- For instance, US Green Magnesium has been selected by the U.S. Department of Energy (DOE) to participate in the High-Performance Computing for Energy Innovation (HPC4EI) program. The project partners the company with Lawrence Livermore National Laboratory to advance eco-friendly magnesium extraction, aiming to reduce reliance on foreign supply chains.(Source: usgreenmagnesium.com)

The expansion of the production facilities and development of large-scale speciality chemical plants led to global expansion of the market requiring high-end investments from the collaboration and government initiatives.

- For instance, on April 2025, the Brunswick County Board of Commissioners officially approved the sale of 22 acres of county-owned land to the company US MgO. US MgO will construct a 75,000-square-foot manufacturing plant inside the Leland Innovation Park. The project represents a $5 million capital investment and will create at least 35 new local jobs.(Source: brunswickcountync.gov)

Growth Trends

- Sustainable Construction: MgO boards and panels are highly sought after as eco-friendly alternatives to conventional building materials due to their fire resistance, durability, and moisture control.

- Agriculture & Animal Nutrition: The usage of magnesium oxide as a soil amendment and livestock feed supplement is seeing rapid uptake, improving crop yields and preventing metabolic issues in grazing animals.

- Environmental & Water Treatment: Stricter industrial emissions and wastewater regulations are driving MgO consumption in flue gas desulfurization (FGD) and wastewater neutralization processes.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 9.48 Billion / 34.34 Million Tons |

| Revenue Forecast in 2035 | USD 15.95 Billion / 51.26 Million Tons |

| Growth Rate | CAGR 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Product, By Application, By region |

| Key Companies Profiled | Martin Marietta Magnesia Specialties, Grecian Magnesite S.A., RHI Magnesita, Tateho Chemical Industries Co., Ltd., Konoshima Chemical Co., Ltd., Magnezit Group, Israel Chemicals Ltd. (ICL), Ube Corporation, Nedmag B.V., Haicheng Guangling Refractory Manufacturing Co., Ltd., Baymag Inc., Imerys, Industrias Peñoles, LKAB Minerals, Kyowa Chemical Industry Co., Ltd., KÜMAS Manyezit Sanayi A.Ş., American Elements, Huber Engineered Materials, US Magnesium LLC, Elementis, Lehmann&Voss&Co KG, Omya International AG, Haicheng Jiusheng Refractory Manufacturing Co., Ltd, Dashiqiao Huamei Group Co., Ltd., TIMAB Magnesium, Nanoshel LLC, Hebei Meishen Technology Co., Ltd., Inframat Advanced Materials, LLC, SkySpring Nanomaterials, Inc., Refratechnik Holding GmbH |

Magnesium Oxide Market: Transition from Traditional to Advanced Facility

The global magnesium oxide market is undergoing a major shift as it transitions from traditional bulk refractories toward high-purity, specialty-grade materials. This transformation is driven by the integration of IoT-enabled, AI-driven processing and sustainable manufacturing methods tailored for electronics, pharmaceuticals, and next-generation battery industries. Machine learning algorithms and automated systems enable real-time monitoring of extraction and purification processes. This allows for the extreme chemical purity and precise particle sizing required for advanced high-tech applications.

Magnesium Oxide Market Dynamics

| Drivers | Restrains | Opportunities |

| Stricter Environmental Regulations:Industrial facilities utilize MgO to neutralize acid gases, absorb CO₂, and treat wastewater to comply with strict global emission and pollution control standards. | Stringent Environmental Regulations:Tightening emission controls and mining regulations are increasing compliance costs. These stringent policies limit raw material extraction and require heavy capital investments into waste heat recovery and carbon-efficient methods. | Advanced Refractories:With robust infrastructure and industrialization scaling in emerging markets like India and Brazil, there is a sustained need for refractory-grade MgO to line high-temperature industrial furnaces and steelmaking ladles. |

| Sustainable Construction Materials:MgO is a key component in eco-friendly "green" building products. It is increasingly used in the manufacturing of fireproof boards, panels, and specialized cements due to its structural strength, non-combustibility, and lower carbon footprint during production. | High Energy Consumption and Costs: The production of specialty grades, such as fused magnesium oxide and dead-burned magnesium oxide, requires extreme temperatures. High energy requirements for calcination and purification heavily inflate operational expenses | High-Purity Medical and Electronic Grades:High-purity MgO is in increasing demand for specialized applications, including lithium-ion battery components, pharmaceutical antacids, and high-quality dietary supplements. |

| Pharmaceutical and Electronics Growth:High-purity grades of MgO are seeing increased adoption in healthcare as antacids and nutritional supplements, and in the electronics sector due to the material's excellent electrical insulation properties. | Competition from Substitutes:In crucial end-use sectors like building materials and wastewater treatment, magnesium oxide faces strong competition from cheaper, readily available alternative materials like calcium oxide, specialized cements, and polymers. | Low-Carbon Manufacturing: Developing low-carbon calcination and energy-efficient processing techniques presents significant potential for cost reduction and compliance with ESG (Environmental, Social, and Governance) targets. |

Supply Chain Analysis of Magnesium Oxide Market:

- Magnesium Oxide Production & Processing:Magnesium oxide is produced through calcination of magnesite ore, magnesium hydroxide, or seawater-derived magnesium compounds, followed by purification and grading for industrial, agricultural, environmental, and refractory applications.

- Calcination temperatures dictate the final product's reactivity, ranging from highly reactive light-burned magnesia to unreactive dead-burned magnesia used in industrial refractories.

- Key players: Martin Marietta, Grecian Magnesite, Premier Magnesia, RHI Magnesita

- Quality Testing and Certification:Magnesium oxide must comply with standards for purity, particle size, chemical composition, reactivity, and safety requirements depending on its end-use application.

- Magnesium oxide (MgO) quality testing and certification evaluate its purity, physical properties, and trace impurities. Testing is governed by pharmacopeial (USP/BP/EP) and industrial standards. Compliance is typically verified through accredited third-party laboratories, resulting in comprehensive Certificates of Analysis (CoA).

- Key Authorities & Standards: International Organization for Standardization, ASTM International, U.S. Food and Drug Administration, European Chemicals Agency

- Distribution to Industrial Users:Magnesium oxide is supplied to refractory manufacturers, agriculture industries, environmental treatment facilities, construction material producers, pharmaceutical companies, and chemical processing sectors.

- Dead-burned and fused magnesia are shipped in bulk to metallurgy and cement plants, while specialty and caustic-calcined grades are distributed in smaller packaging to pharmaceutical, agricultural, and construction sectors through specialized chemical distributors.

- Key players: Martin Marietta, Grecian Magnesite, RHI Magnesita.

Magnesium Oxide Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Toxic Substances Control Act (TSCA); OSHA Hazard Communication Standards | Industrial minerals, workplace safety | The U.S. regulates magnesium oxide use in refractories, environmental applications, agriculture, and pharmaceuticals. |

| European Union | European Chemicals Agency (ECHA); European Commission | REACH Regulation; CLP Regulation | Chemical safety, sustainable industrial materials | Europe emphasizes safe handling and environmentally compliant use of magnesium oxide across industrial sectors. |

| China | Ministry of Ecology and Environment (MEE); Ministry of Industry and Information Technology (MIIT) | Environmental Protection Law; Industrial Mineral Standards | Refractories, steel production, environmental protection | China is the largest producer and consumer of magnesium oxide, supported by its steel and refractory industries. |

| India | Ministry of Mines; Central Pollution Control Board (CPCB) | Mines and Minerals Act; Environmental Protection Act | Industrial minerals, refractory materials | India is expanding magnesium oxide consumption in steelmaking, agriculture, and wastewater treatment applications. |

| Japan | Ministry of Economy, Trade and Industry (METI) | Chemical Substances Control Law (CSCL) | High-purity magnesium oxide, specialty applications | Japan focuses on advanced magnesium oxide grades for electronics, pharmaceuticals, and specialty ceramics. |

| Brazil | National Mining Agency (ANM); Ministry of Environment | Mining Regulations; Environmental Licensing Standards | Mineral processing, industrial applications | Brazil supports magnesium oxide production for refractories, agriculture, and environmental treatment applications. |

Segmental Insights

Product Insights

The dead burned magnesia (DBM) segment dominated the market with 52% share in 2025, driven primarily by its indispensable role as a refractory material in the global iron, steel, and cement industries. Also primarily driven by soaring demand from the steel and cement industries and a global shift toward Electric Arc Furnace (EAF) steelmaking. DBM is a critical component for the refractory linings in cement rotary kilns. Sustained growth in global construction and urbanization requires a continued high output of these materials.

")

The caustic calcined magnesia (CCM) segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.40% in the forecast period, due to its unique chemical reactivity and high-water solubility. Industries are increasingly utilizing CCM for wastewater treatment and flue gas desulfurization to strip sulfur dioxide from plant emissions. CCM is preferred over other alkaline materials because it provides controlled alkalinity, reduces corrosion risks, & minimizes sludge.

Magnesium Oxide Market Share, By Product, 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Dead Burned Magnesia (DBM) | 52% |

| Caustic Calcined Magnesia (CCM) | 33% |

| Fused/Electrofused MgO | 15% |

Application Insights

The industrial segment dominated the market with 49% share in 2025, driven by surging demand for advanced refractory materials, stringent environmental regulations, and a massive push for sustainable construction. MgO plays a critical role in industrial sustainability, experiencing heightened demand in flue gas desulfurization cleaning industrial exhaust and wastewater neutralization.

") The environmental segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.10% in the forecast period, driven by stringent global emissions regulations and a pivot toward sustainable, eco-friendly industrial practices. Governments worldwide are increasingly mandating cleaner industrial operations, fueling rapid adoption of MgO in pollution control and water treatment. Demand for sustainable building materials has boosted the popularity of MgO-based boards and cement panels.

The environmental segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.10% in the forecast period, driven by stringent global emissions regulations and a pivot toward sustainable, eco-friendly industrial practices. Governments worldwide are increasingly mandating cleaner industrial operations, fueling rapid adoption of MgO in pollution control and water treatment. Demand for sustainable building materials has boosted the popularity of MgO-based boards and cement panels.

Magnesium Oxide Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Agriculture | 16% |

| Industrial | 49% |

| Building and Construction | 12% |

| Pharmaceuticals | 7% |

| Environmental | 11% |

| Other Applications | 5% |

Regional Analysis

How did Asia Pacific dominate the Magnesium Oxide Market in 2025?

The Asia Pacific magnesium oxide market size was estimated at USD 4.39 billion in 2025 and is projected to reach USD 7.90 billion by 2035, growing at a CAGR of 6.05% from 2026 to 2035.Asia Pacific dominated the market with a share of 49% in 2025. This dominance is driven by massive infrastructure investments, booming steel production, and expanding chemical and agricultural sectors in countries like China and India. Expansive construction projects and government initiatives such as "Make in India" significantly boosted demand for standard-grade magnesia and fire-resistant MgO boards across the region. Rising healthcare awareness and expanding livestock industries in India and China spiked the need for feed-grade MgO in animal nutrition and soil conditioning.

India

- India's robust manufacturing sector relies heavily on high-purity MgO for refractory linings, while surging consumer health awareness boosts demand in domestic wellness products.

- There is an upward trajectory in the utilization of pharmaceutical-grade magnesium oxide for antacids, dietary supplements, and functional foods.

China

- China’s magnesium oxide market is experiencing steady growth, primarily driven by the steel and refractory industries, rigorous environmental protection policies, and expanding construction and electronics sectors.

- The Chinese government has implemented strict ecological and sustainable development policies.

Europe Magnesium Oxide Market Growth Factor

The Europe magnesium oxide market size was estimated at USD 1.97 billion in 2025 and is projected to reach USD 3.59 billion by 2035, growing at a CAGR of 6.18% from 2026 to 2035.Europe held the market share of 20% in 2025, primarily driven by stringent environmental regulations requiring flue gas desulfurization, expanding pharmaceutical and chemical processing sectors, and high demand for refractory materials in automotive manufacturing and steelmaking. Strict emissions regulations in the EU demand more efficient scrubbing technologies. Magnesium oxide is highly preferred for removing sulfur dioxide from industrial exhaust because it yields less toxic waste compared to limestone scrubbers.

Germany

- As Germany’s automotive sector shifts toward electric vehicles (EVs), demand is surging for lightweight, durable magnesium components and silicon steel used in electrical powertrains and grids.

- EU circular-economy regulations encourage the use of mineral-based fire retardants like Magnesium Oxide nanopowder over traditional halogenated alternatives, providing strong regulatory tailwinds.

Italy

- Italy possesses strong manufacturing roots in steel, glass, and ceramics. The high thermal stability of MgO makes it indispensable for kiln and furnace linings, directly correlating market growth with local industrial output.

- The ongoing push for energy-efficient and fireproof building materials has led to increased MgO adoption in Italian construction and cement applications.

North America Magnesium Oxide Market Growth Factor

The North America magnesium oxide market size was estimated at USD 1.34 billion in 2025 and is projected to reach USD 2.47 billion by 2035, growing at a CAGR of 6.31% from 2026 to 2035.North America held the market share of 15% in 2025 and is expected to experience significant growth while growing with a CAGR of 6.80% in the forecast period, primarily driven by expanding agriculture and livestock sectors, a surge in fire-resistant green building construction, and continuous demand for refractory linings in steel manufacturing. The region's iron and steel industries continuously demand dead-burned and fused magnesia to line high-temperature furnaces.

U.S.

- U.S. producers are leveraging government initiatives to onshore supply chains while supplying vital, high-temperature components to the booming domestic steel and automotive sectors.

- U.S. defense and critical raw materials policies are encouraging domestic mining and production to reduce reliance on foreign supply streams like those from China, heavily incentivizing on-shoring efforts.

Canada

- MgO acts as a vital soil conditioner and is a staple mineral supplement in livestock feed. Canada's vast agricultural sector continuously drives demand for high-quality, synthetic, and natural feed-grade magnesium oxide.

- The Canadian construction industry is shifting toward magnesium oxide boards (MgO boards) as fireproof, moisture-resistant, and eco-friendly alternatives to traditional wallboards and cement.

Latin America Magnesium Oxide Market Growth Factor

The Latin America magnesium oxide market size was estimated at USD 0.63 billion in 2025 and is projected to reach USD 1.20 billion by 2035, growing at a CAGR of 6.66% from 2026 to 2035.Latin America held the market share of 7% in 2025, which is primarily driven by expanding agricultural activities, iron and steel production, and the chemical and pharmaceutical sectors. Rising awareness of sustainable industrial practices is boosting MgO use in wastewater treatment and flue gas desulfurization across the continent. The region's major agrarian economies heavily rely on MgO for soil treatment and as an essential nutrient in livestock feed.

")

Brazil

- Brazil’s massive chemical and pharmaceutical industries continuously drive consumption for cosmetics, dietary supplements, and specialized chemical production.

- Brazil is a major global steel producer. Magnesium oxide is crucial for making heat-resistant refractory linings for blast furnaces, which directly ties demand to domestic steel output.

Argentina

Magnesium oxide market growth in Argentina is primarily driven by the expansion of the domestic steel industry, increasing agricultural demand for fertilizers and livestock supplements, and a growing consumer health sector.

Because Argentina is an industrial hub reliant on imported specialty minerals, local consumption is heavily shaped by macroeconomic trends and import-export dynamics.

Middle East and Africa Magnesium Oxide Market Growth Factor

The Middle East and Africa magnesium oxide market size was estimated at USD 0.81 billion in 2025 and is projected to reach USD 1.52 billion by 2035, growing at a CAGR of 6.50% from 2026 to 2035.The Middle East and Africa held the market share of 9% in 2025, driven by massive infrastructure investments, expanding oil and gas projects, and growth in the metal processing sectors. Increasing construction and cement production continue to boost regional demand.

Massive government projects such as Saudi Arabia's Vision 2030 developments and various UAE real estate initiatives heavily utilize MgO boards and cement. Magnesium oxide is favored for its fire resistance, moisture control, and durability in harsh desert climates

Magnesium Oxide Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 15% |

| Europe | 20% |

| Asia-Pacific | 49% |

| Latin America | 7% |

| Middle East & Africa | 9% |

Saudi Arabia

- Saudi Arabia market growth is driven by mega-projects like the NEOM developments and Vision 2030. MgO is in high demand for manufacturing fireproof building materials, specialty cements, ceramics, and insulation boards due to its high thermal stability.

- As a major oil and gas hub, Saudi Arabia utilizes high-grade caustic calcined magnesia in refining processes, catalysts, and specialized lubricant additives.

UAE

- MgO is increasingly utilized in Middle Eastern desalination plants and wastewater treatment to balance pH levels and neutralize acidic compounds.

- Growing demand for specialty nano-MgO in livestock feed supplements and localized sustainable agricultural initiatives is providing a fresh boost to the regional market.

Competitive Analysis

- European nations continue to roll out state-funded procurement opportunities. For instance, recent public sector tenders in Slovenia explicitly target verified chemical contractors for state-backed magnesium oxide resource acquisition.

- The partnership between Canada Nickel Company and NetCarb aims to establish a zero-carbon industrial cluster in Northeastern Ontario by combining regional biomass with NetCarb's proprietary carbon mineralization technology. (Source: prnewswire.com)

- The European Union and the United States have launched a strategic partnership, formalized by a Memorandum of Understanding and an Action Plan, to secure critical mineral supply chains. Signed by EU Commissioner Maroš Šefčovič and US Secretary of State Marco Rubio, the agreement focuses on bilateral cooperation across the entire raw materials value chain to counter global supply concentrations.(Source: ec.europa.eu)

Competitive advantage is increasingly driven by access to high-quality magnesite reserves, vertically integrated operations, technological expertise, and the ability to supply customized magnesium oxide grades for diverse end-use industries.

Top players in the Magnesium Oxide Market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Magnesium Oxide Offerings | Key Offering/Strength |

| Martin Marietta Magnesia Specialties | Major producer of industrial minerals and magnesium products | Raleigh | North America, Europe, Asia Pacific | Dead-burned magnesium oxide, caustic calcined magnesia, and refractory-grade products | Strong raw material resources and diversified industrial mineral portfolio |

| Grecian Magnesite S.A. | Leading vertically integrated magnesia producer | Athens | Europe, North America, Asia Pacific, Middle East | Caustic calcined magnesia, dead-burned magnesia, agricultural and environmental grades | Integrated mining-to-processing operations with high-purity magnesia production |

| RHI Magnesita | Leading refractory and magnesia solutions provider | Vienna | Europe, Asia Pacific, North America, Latin America, Middle East | Fused magnesia, dead-burned magnesia, refractory-grade magnesium oxide | Extensive global refractory network and advanced magnesia processing expertise |

| Tateho Chemical Industries Co., Ltd. | Specialty magnesium oxide manufacturer | Ako | Asia Pacific, North America, Europe | High-purity magnesium oxide for electronics, pharmaceuticals, and industrial applications | Expertise in ultra-high-purity magnesium oxide and specialty applications |

| Konoshima Chemical Co., Ltd. | Specialty inorganic chemicals producer | Osaka | Asia Pacific, Europe, North America | High-purity magnesium oxide, fused magnesia, and functional inorganic materials | Strong presence in advanced ceramics, electronics, and specialty industrial markets |

Other Top Players Are

- Magnezit Group

- Israel Chemicals Ltd. (ICL)

- Ube Corporation

- Nedmag B.V.

- Haicheng Guangling Refractory Manufacturing Co., Ltd.

- Baymag Inc.

- Imerys

- Industrias Peñoles

- LKAB Minerals

- Kyowa Chemical Industry Co., Ltd.

- KÜMAS Manyezit Sanayi A.Ş.

- American Elements

- Huber Engineered Materials

- US Magnesium LLC

- Elementis

- Lehmann&Voss&Co KG

- Omya International AG

- Haicheng Jiusheng Refractory Manufacturing Co., Ltd

- Dashiqiao Huamei Group Co., Ltd.

- TIMAB Magnesium

- Nanoshel LLC

- Hebei Meishen Technology Co., Ltd.

- Inframat Advanced Materials, LLC

- SkySpring Nanomaterials, Inc.

- Refratechnik Holding GmbH

Recent Development

- In March 2026, Decode Age, India’s leading longevity ecosystem, announced the launch of its significantly upgraded Mag7(TM), a next-generation magnesium supplement that is formulated for a specific physiological function.(Source: thewire.in)

Segments Covered

By Product

- Dead Burned Magnesia (DBM)

- Refractory Grade DBM

- Steelmaking Grade DBM

- Cement Kiln Grade DBM

- Caustic Calcined Magnesia (CCM)

- Agricultural Grade CCM

- Industrial Grade CCM

- Feed Grade CCM

- Environmental Grade CCM

- Fused/Electrofused MgO

- Standard Fused MgO

- High-Purity Fused MgO

- Electrical Grade Fused MgO

By Application

- Agriculture

- Fertilizers

- Animal Feed Supplements

- Soil Conditioning

- Industrial

- Refractories

- Steel Manufacturing

- Non-Ferrous Metallurgy

- Chemicals Processing

- Building and Construction

- Magnesium-Based Cement

- Fireproof Boards

- Insulation Materials

- Pharmaceuticals

- Antacids

- Laxatives

- Pharmaceutical Intermediates

- Environmental

- Water Treatment

- Flue Gas Desulfurization

- Wastewater Neutralization

- Other Applications

- Rubber Processing

- Electronics

- Ceramics

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Tags

Select User License to Buy

Figures (7)