Content

U.S. Gas Pipeline Infrastructure Market Size, Share, Growth and Forecast 2026-2035

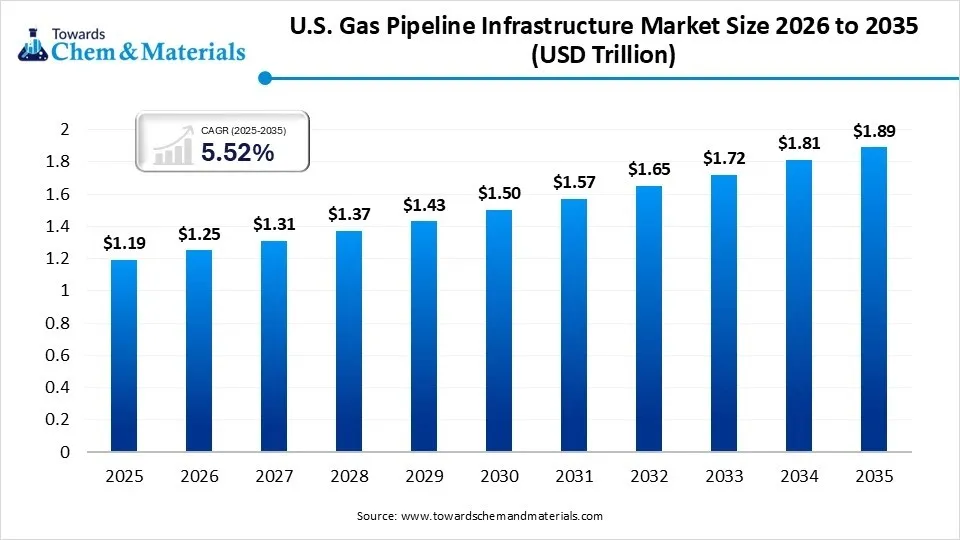

The U.S. gas pipeline infrastructure market size was valued at USD 1.19 trillion in 2025, is estimated to reach USD 1.25 trillion in 2026, and is projected to reach USD 1.89 trillion by 2035, growing at a CAGR of 5.52% from 2026 to 2035 The growing energy demand, major LNG export, and strong government support drive the market growth.

")

Key Takeaways

- By pipeline type, the transmission pipelines segment held a 45% share in the U.S. gas pipeline infrastructure market in 2024 due to the need for transportation of a high volume of natural gas.

- By pipeline type, the gathering pipelines segment is expected to grow at the fastest CAGR in the market during the forecast period due to the increasing shale gas production.

- By material, the carbon steel pipe segment held a 60% share in the market in 2024 due to the ease of installation.

- By material, the polyethylene pipe segment is expected to grow at the fastest CAGR in the market during the forecast period due to its high corrosion resistance.

- By diameter, the large-diameter segment held a 40% share in the market in 2024 due to the increasing transportation of natural gas.

- By diameter, the small-diameter segment is expected to grow at the fastest CAGR in the market during the forecast period due to the growing localized distribution of natural gas.

- By application, the industrial & process gas segment held a 30% share in the market in 2024 due to the growing industrialization.

- By application, the transport fuel segment is expected to grow at the fastest CAGR in the market during the forecast period due to the rapid growth in the transportation sector.

- By component, the pipe body segment held a 35% share in the U.S. gas pipeline infrastructure market in 2024 due to the focus on enhancing natural gas transport capacity.

- By component, the monitoring & control systems segment is expected to grow at the fastest CAGR in the market during the forecast period due to the focus on preventing leakage.

Market Size and Volume Forecast

- Market Size (2025): USD 1.19 Trillion | CAGR (2025–2035): 5.52%

- Market Projected Size (2035): USD 1.89 Trillion

- Market Volume (2025): 455.22 Thousand Miles | Volume CAGR (2025–2035): 3.95%

- Market Projected Volume (2035): 670.60 Thousand Miles

- Market Pricing (2025):

- Average Manufacturing Price: USD 1.35 Million per Mile

- Average Selling Price: USD 1.95 Million per Mile

- Pricing CAGR (2025–2035): 2.72%

Power of U.S. Gas Pipeline Infrastructure in Energy Transport & Security

The U.S. gas pipeline infrastructure is a complex & large network of pipelines to transport gas from production infrastructure to storage facilities. The components of the United States' gas pipeline infrastructure are transmission pipelines, metering stations, distribution lines, gathering lines, compressor stations, and storage facilities.

The pipelines are divided into two types: intrastate pipelines and interstate pipelines. The United States consists of the world’s largest network of natural gas pipelines and distributes natural gas throughout 48 states. Factors like the growing adoption of renewable energy sources, modernization of infrastructure, strong government support, increasing energy demand, major LNG export, and shale gas development contribute to the growth of the U.S. gas pipeline infrastructure market.

- The total number of natural gas transmission pipelines in the United States was 300,858 in 2024.(Source: www.phmsa.dot.gov)

- The total number of natural gas gathering pipelines in the United States was 110,305 in 2024.(Source: www.phmsa.dot.gov)

- The total number of natural gas transmission pipelines in the United States was 300,462 in 2023.(Source: www.phmsa.dot.gov)

Growing Power Generation Drives the Market Growth

The growth in sectors like residential electrification, data centers, and the expansion of industries in the United States increases power generation. The expansion of gas pipeline infrastructure and increasing construction activities increase demand for power generation. The focus on the adoption of clean energy sources requires power that increases demand for gas pipeline infrastructure.

The high consumption of power in various sectors increases demand for gas pipeline infrastructure. The rapid urbanization and growing commercial & residential construction activities increase demand for power. The growing expansion of industries like chemical and manufacturing requires high power, which increases demand for gas pipeline infrastructure. The growing power generation is a key driver for the growth of the U.S. gas pipeline infrastructure market.

Market Trends

- Growing Energy Demand: The growing demand for energy across various industries like construction, manufacturing, and others increases energy demand. The growing consumption of energy across the residential and commercial sectors increases demand for gas pipeline infrastructure.

- High LNG Export: The growing export of LNG on terminals like Sabine Pass & Calcasieu Pass Facilities in the Gulf Coast increases demand for gas pipeline infrastructure.

- Technological Advancements: The ongoing technological advancements, like hydraulic fracturing, integration with AI, horizontal drilling, data analytics, smart sensors, and other technologies, enhance operational efficiency and safety of gas pipeline infrastructure.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 1.25 Trillion |

| Expected Size by 2035 | USD 1.89 Trillion |

| Growth Rate from 2025 to 2035 | CAGR 5.52% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Pipeline Type, By Material, By Diameter, By Application (End-User Sector), By Component |

| Key Companies Profiled | Tenaris, Vallourec, TMK, U.S. Steel Tubular Products, Nucor Tubular Products, JM Eagle, Shawcor, McWane, Mueller Water Products, Flowserve, Emerson, Honeywell, Itron, Siemens Energy, GE Vernova, Baker Hughes, MAN Energy Solutions, Howden, Atlas Copco, Sulzer |

Market Opportunity

Infrastructure Modernization Unlocks Market Opportunity

The aging infrastructure and focus on enhancing the safety of infrastructure increase demand for the modernization of pipeline infrastructure. The rising maintenance costs and increasing wear & tear of infrastructure increase the need for infrastructure modernization. The focus on enhancing the safety of pipelines and the development of smart sensors for detecting faults increases demand for the modernization of infrastructure. It helps in performing efficient operations and reducing downtime.

The technological innovations, like Artificial Intelligence integration, advanced sensors, and data analytics, help in infrastructure modernization. The stringent regulations and strong government support for infrastructure modernization help the market growth. The infrastructure modernization creates an opportunity for the growth of the U.S. gas pipeline infrastructure market.

Market Challenge

High Capital Cost Shuts Down Expansion of the Market

With several applications of gas pipeline infrastructure in the United States, the high capital cost restricts the market growth. Factors like stringent regulatory processes, need for specialized equipment, high investment in raw materials, complex construction, high right-of-way costs, and extensive labor costs are responsible for the high capital cost. The extensive need for labor to perform various tasks, such as installation, site preparation, and welding, requires a high investment.

The need for specific land for pipelines and the high expense of engineering, regulatory filing, surveying, & project supervision increase the cost. The need for materials like steel, pipe coatings, and specialized equipment like large cranes requires a high cost. The stricter regulatory requirements and expensive construction process increase the cost. The high capital cost hampers the growth of the U.S gas pipeline infrastructure market.

Regional Insights

South U.S. Gas Pipeline Infrastructure Market Trends

The South region dominated the market in 2024. The presence of vast reserves of natural gas and high exports of LNG increases demand for gas pipeline infrastructure. The growing development of pipeline infrastructure and strong government support for clean energy sources help the market growth. The presence of an extensive network of pipelines, production areas, and storage facilities drives the overall growth of the market.

Northeast U.S. Gas Pipeline Infrastructure Market Trends

The Northeast region is experiencing the fastest growth in the market during the forecast period. The growing electricity generation and extensive natural gas demand for heating increase the adoption of gas pipeline infrastructure. The vast reserves of natural gas and lower costs help the market growth. The growing industrialization and presence of vast data centers increase demand for gas pipeline infrastructure. The shift towards cleaner energy resources and high investment in pipeline infrastructure development support the overall growth of the market.

Segmental Insights

Pipeline Type Insights

Why did the Transmission Pipelines Segment Dominate the U.S. Gas Pipeline Infrastructure Market?

The transmission pipelines segment dominated the market in 2024. The need for transporting a high volume of natural gas in urban areas & industries increases demand for transmission pipelines. The focus on energy security and the growing modernization of transmission pipelines help the market growth. The increasing shale gas production and growing power generation increase demand for transmission pipelines, driving the overall growth of the market.

The gathering pipelines segment is the fastest-growing in the market during the forecast period. The growing expansion of shale gas production and rising industrialization increase demand for gathering pipelines. The increasing demand for energy and the rising shift towards cleaner energy increase the adoption of gathering pipelines. The focus on energy independence and cost-effectiveness increases demand for gathering pipelines. The growing investment in gathering pipelines and strong government support drive the overall growth of the market.

Material Insights

How the Carbon Steel Pipe Segment Held the Largest Share in the U.S. Gas Pipeline Infrastructure Market?

The carbon steel pipe segment held the largest revenue share in the market in 2024. The ability to withstand high pressures and excellent durability increases the adoption of carbon steel pipe. The growing demand for long-distance gas transmission and focus on long service life increase the demand for carbon steel pipe. The ease of installation and growing energy sector increase the adoption of carbon steel pipe. The growing availability of carbon steel pipe in various sizes & grades and enhanced corrosion resistance drives the overall growth of the market.

The polyethylene (PE) pipe segment is experiencing the fastest growth in the market during the forecast period. The excellent corrosion resistance and focus on lowering maintenance needs increase demand for polyethylene pipe. The strong focus on lowering installation time and the need for longer pipes increases demand for PE pipe. The growing replacement of aging pipeline infrastructure and the development of renewable energy increase demand for PE pipe, supporting the overall growth of the market.

Diameter Insights

Why did the Large-Diameter Segment Dominate the U.S. Gas Pipeline Infrastructure Market?

The large-diameter (12-24 inches) segment dominated the U.S. gas pipeline infrastructure market in 2024. The need to carry a large amount of natural gas and focus on reducing compression stations increases demand for large-diameter pipes. The increasing transportation of natural gas and the rising development of inter-regional projects increase demand for large-diameter pipes. The growing consumption of energy and the development of shale gas increase demand for large-diameter pipes. The growth in LNG imports and high investment in long routes increases the adoption of large-diameter pipes, driving the overall growth of the market.

The small-diameter (<6 inches) segment is the fastest-growing in the market during the forecast period. The growing distribution of gas in the industrial, residential, and commercial sectors increases demand for small-diameter pipes. The increasing adoption of cleaner energy sources and strong government support for the development of clean energy infrastructure increase demand for small-diameter pipes. The increasing localized distribution of natural gas and aging gas pipeline infrastructure increases adoption of small-diameter pipes, supporting the overall growth of the market.

Application (End-User Sector) Insights

Which Application held the Largest Share in the U.S. Gas Pipeline Infrastructure Market?

The industrial & process gas segment held the largest revenue share in the market in 2024. The growing industries like chemicals, steel, and power generation increase demand for industrial gas. The increasing electricity generation and high demand for air conditioning increase the demand for process gas. The expansion of the petrochemical industry and the development of fertilizers increase demand for industrial gas. The rise in data centers and increasing manufacturing activities increases demand for industrial gas, driving the overall growth of the market.

The transport fuel segment is experiencing the fastest growth in the market during the forecast period. The rapid urbanization and growth in population increase the demand for transport fuel. The increasing ownership of vehicles and the lower cost of gasoline fuel increase the adoption of transport fuel. The rapid growth of e-commerce and the rise in logistics increase demand for transport fuel. The focus on enhancing the fuel efficiency of vehicles and growth in the transportation sector increases the adoption of transport fuel, supporting the overall growth of the market.

Component Insights

How Pipe Body Segment Dominated the U.S. Gas Pipeline Infrastructure Market?

The pipe body segment dominated the U.S. gas pipeline infrastructure market in 2024. The focus on high-pressure operation and enhancing the capacity of transport increases demand for the pipe body. The high transmission volume of natural gas over long distances increases demand for pipe body. The growing demand for energy across various industrial sectors and the growth in LNG terminals increase the adoption of Pipe body. The growing use of materials like alloy steel and carbon steel in the pipe body drives the overall growth of the market.

The monitoring & control systems segment is the fastest-growing in the market during the forecast period. The stringent regulations for pipelines and strict safety guidelines increase the adoption of monitoring & control systems. The ongoing technological advancements in monitoring systems like advanced leak detection, AI integration, and drone monitoring help the market growth. The strong focus on leakage prevention and expansion of pipeline networks increases demand for monitoring & control systems, supporting the overall growth of the market.

U.S. Gas Pipeline Infrastructure Market Value Chain Analysis

- Feedstock Procurement: The feedstock for gas pipeline infrastructure in the United States is high-quality plastic like polyethylene, cast iron, and carbon steel.

- Quality Testing and Certification: The quality testing involves coating inspection, materials testing, leak detection, & weld inspection, and certification includes FERC & PHMSA Safety Certification.

- Regulatory Compliance and Safety Monitoring: The regulatory compliance includes the Federal Energy Regulatory Commission and the Pipeline & Hazardous Materials Safety Administration, and safety monitoring involves environmental hazard monitoring, corrosion detection, & geometric & metal loss inspection.

Recent Developments

- In September 2025, John Crane launched a seal, 8628VL, to boost the reliability of the ethane pipeline. The seal offers zero-wear operation and improved hydrodynamic lift. The seal offers extremely low leakage and non-contacting performance. It reduces maintenance costs and offers zero failures.(Source: pgjonline.com)

- In May 2025, TC Energy Corp is set to launch the Southwest Gateway Pipeline amid increasing North American gas flows. The pipeline is 444 miles long and has a diameter of 36 inches. The pipeline starts in Tuxpan, Veracruz, and has a 416-mile offshore pipeline.(Source: naturalgasintel.com)

U.S. Gas Pipeline Infrastructure Market Top Companies

- Tenaris

- Vallourec

- TMK

- U.S. Steel Tubular Products

- Nucor Tubular Products

- JM Eagle

- Shawcor

- McWane

- Mueller Water Products

- Flowserve

- Emerson

- Honeywell

- Itron

- Siemens Energy

- GE Vernova

- Baker Hughes

- MAN Energy Solutions

- Howden

- Atlas Copco

- Sulzer

Segments Covered

By Pipeline Type

- Transmission pipelines

- Distribution pipelines

- Gathering pipelines

By Material

- Carbon steel pipe

- High-strength alloy steel pipe

- Polyethylene (PE) pipe

- Composite / fiberglass-reinforced pipe

By Diameter

- Small-diameter (< 6 inches)

- Medium-diameter (6–12 inches)

- Large-diameter (12–24 inches)

- Extra-large diameter (> 24 inches)

By Application (End-User Sector)

- Residential gas supply

- Commercial gas supply

- Industrial & process gas

- Power generation

- Transport fuel (CNG/LNG)

By Component

- Pipe body (mains & laterals)

- Compressor stations

- Pressure regulation & metering stations

- Storage facilities

- Valves & actuators

- Coatings & corrosion protection

- Monitoring & control systems (SCADA, sensors)

FAQ's

Select User License to Buy

Figures (2)