Content

Aniline Market Size, Share, Growth and Forecast 2026-2035

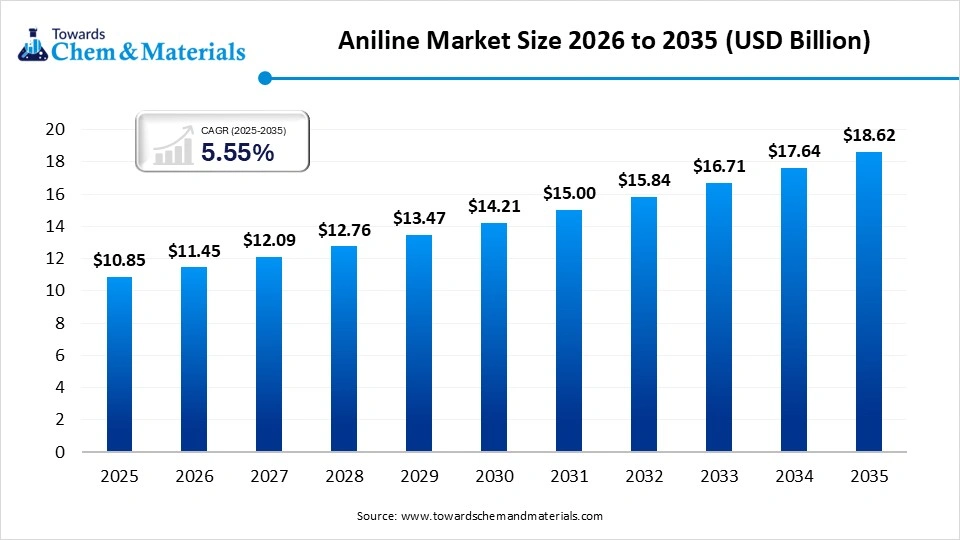

The global aniline market size was estimated at USD 10.85 billion in 2025 and is expected to increase from USD 11.45 billion in 2026 to USD 18.62 billion by 2035, growing at a CAGR of 4.95% from 2026 to 2035. North America dominated the aniline with the largest revenue share of 53.00% in 2025. The growth of the market is driven by rising automotive production, infrastructure expansion, and a shift towards bio-based aniline. The aniline market is significant as a critical driver of the chemical industry, driven by high demand for methylene diphenyl diisocyanate (MDI), used in polyurethane foams for construction, insulation, and automotive lightweighting, alongside extensive applications in rubber processing and dyes. Aniline is crucial for manufacturing rubber additives, which are in high demand for tire production, driving growth in countries like India. Investments are increasingly directed toward green chemistry practices and bio-based aniline variants.

")

Market Highlights

- The North America dominated aniline market with the largest revenue share of 53.00% in 2025. The rebound in the automotive industry has increased demand for rubber

- By region, Europe is expected to have the fastest growth in the market in the forecast period between 2026 and 2035. The market is focusing on sustainable production to meet european regulatory standards.

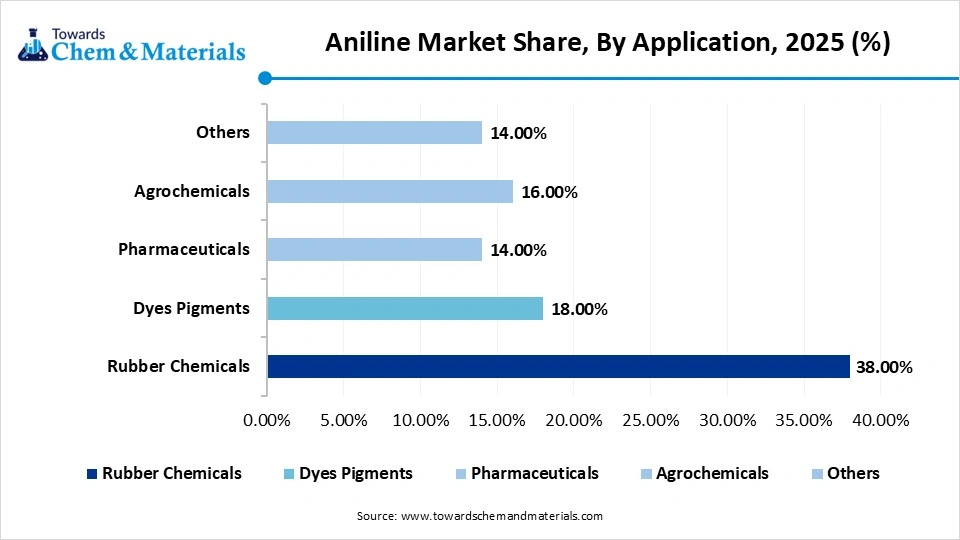

- By application, the rubber chemicals segment dominated the market and accounted for the largest revenue share of 38.00% in 2025. The market was also supported by the expansion of related downstream industries.

- By application, the dyes pigments segment is projected to grow at the fastest CAGR between 2026 and 2035, and is seeing faster growth due to demand for high-performance colorants.

- By type, the aniline segment led the market with the largest revenue share in 2025. driven by rapid urbanization and massive infrastructure investment.

- By type, the toluidine segment is projected to grow at the fastest CAGR between 2026 and 2035. There is a significant shift towards sustainable production methods and the adoption of bioaniline.

- By end use, the automotive segment dominated the market and accounted for the largest revenue share in 2025. Aniline is crucial in producing antioxidants and vulcanization accelerators.

- By end use, the pharmaceutical segment is projected to grow at the fastest CAGR between 2026 and 2035, due to the rising demand for active ingredient synthesis.

Key Technological Shifts In The Aniline Market:

The market is undergoing significant technological shifts driven by the demand for sustainable production, improved efficiency in methylene diphenyl diisocyanate (MDI) manufacturing, and the need for greener alternatives. Key shifts include the transition towards bio-based aniline, advanced catalytic hydrogenation processes, and the integration of digital technologies to optimize production. The industry is moving toward more efficient, lower-emission aniline production technologies.

Trade Analysis of the Aniline Market: Import & Export Statistics

- According to Global Export Data, the world exported 5,447 Aniline shipments between July 2024 and June 2025 (TTM) through 528 verified exporters and 822 buyers.

- The United Arab Emirates, India, and the United States lead as the top Aniline importers, while India with 16,073 shipments, China with 4,561 shipments, and Belgium with 1,151, rank as the largest global Aniline exporters.

Top-performing Global Aniline Exporters by volume:

- AARTI INDUSTRIES LIMITED 71 UDYOG KSHETRA 2ND FLR: 12,087 shipments (78%)

- KEMPAR ENERGY PTE LTD: 1,687 shipments (11%)

- INDUSTRIAL SOLVENTS CHEMICALS PVT LTD: 385 shipments (2%)

Recent Market Growth Trends:

- Shift to Bio-based Aniline: To improve sustainability, manufacturers are shifting towards producing eco-friendly "bio-aniline" from waste sugar biomass.

- Pharmaceutical & Agro Demand: Rising demand for aniline in the production of pharmaceuticals and rubber processing chemicals (for tires) is strengthening market growth.

- Bio-aniline Development: Due to environmental regulations on toxic chemicals, there is a rising trend in producing aniline from biomass to create eco-friendly alternatives, with bio-derived variants expected to capture significant demand.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 11.45 Billion |

| Revenue Forecast in 2035 | USD 18.62 Billion |

| Growth Rate | CAGR 5.55% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segment Covered | By Application, By Type, By End-Use, By Regions |

| Key companies profiled | Sumitomo Chemical Co., Ltd., Mitsui Chemicals, Inc., Tosoh Corporation, PetroChina Company Limited, China Petroleum & Chemical Corporation (Sinopec), BASF Corporation, BONDALTI, Borsodchem Mchz, Covestro AG, Dow, GNFC, Huntsman International LLC, Jilin Connell Chemical Industry Co., Ltd., Mitsubishi Chemical, Sabic, SP Chemicals Holdings Ltd., Sumika Bayer Urethane Co., Ltd., The Dow Chemical Company, Wanhua Chemical Group Co. Ltd. |

Aniline Market Supply Chain Analysis

Chemical Production and Processing

- Aniline is produced through catalytic hydrogenation of nitrobenzene, followed by purification and processing for use in dyes, rubber chemicals, pharmaceuticals, and polyurethane intermediates.

- Key players BASF, Covestro, Huntsman Corporation, Wanhua Chemical

Quality Testing and Certification

- Aniline must comply with chemical purity standards, hazardous material regulations, and environmental safety guidelines before industrial application.

- Key players: European Chemicals Agency, U.S. Environmental Protection Agency, International Organization for Standardization, Occupational Safety and Health Administration.

Distribution to Industrial Users

- Aniline is supplied to polyurethane manufacturers, rubber processing industries, dye and pigment producers, pharmaceutical companies, and agrochemical manufacturers.

- Key players: BASF, Covestro, Wanhua Chemical.

Aniline Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| US | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Toxic Substances Control Act (TSCA); Clean Air Act; OSHA Hazard Communication Standard | Chemical safety, occupational exposure, emissions control | Aniline is classified as a hazardous chemical, requiring strict workplace exposure limits and environmental compliance in industrial applications such as dyes and rubber processing. |

| Europe | European Chemicals Agency (ECHA); European Commission | REACH Regulation; CLP Regulation; Industrial Emissions Directive (IED) | Chemical registration, hazard classification, and environmental emissions | The EU enforces strict labeling, handling, and environmental controls for aniline due to its toxicity and potential health risks. |

| China | Ministry of Ecology and Environment (MEE); Ministry of Emergency Management (MEM) | Environmental Protection Law; Work Safety Law | Industrial chemical safety, pollution control | China regulates aniline production and use with strict environmental and workplace safety standards, particularly in dye and chemical manufacturing. |

| India | Ministry of Environment, Forest and Climate Change (MoEFCC); Central Pollution Control Board (CPCB) | Environment Protection Act; Manufacture, Storage, and Import of Hazardous Chemicals Rules | Hazardous chemical management, industrial emissions | Aniline is regulated as a toxic substance, requiring adherence to safety, storage, and emission norms in chemical industries. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of Health, Labour and Welfare (MHLW) | Chemical Substances Control Law (CSCL); Industrial Safety and Health Act | Chemical risk management, occupational safety | Chemical risk management, occupational safety Japan imposes strict controls on aniline handling and worker exposure due to its toxicological properties. |

| Brazil | Brazilian Institute of Environment and Renewable Natural Resources (IBAMA); National Health Surveillance Agency (ANVISA) | National Environmental Policy Act; Chemical Safety Regulations | Environmental protection, worker safety | Brazil regulates aniline under chemical safety frameworks, focusing on safe industrial usage and environmental impact mitigation. |

Segmental Insights

Application Insights

How did the Rubber Chemicals Segment Dominate the Aniline Market in 2025?

The rubber chemicals segment dominated the market share 38.00% in 2025, by supplying essential rubber processing chemicals for the booming global tire and automotive industries. This demand was largely fueled by increasing vehicle production, particularly for lightweighting components and high-performance rubber products, complementing the dominant polyurethane/MDI applications. Rubber chemicals, such as anti-degradants, improved the durability and performance of rubber products.

")

The dyes pigments segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by expanding applications in textiles, plastics, and paints, which fuel the growth of the market. Development of specialty colorants and sustainable pigments supports market expansion. Increased demand for reactive dyes on synthetic materials like polyester and nylon drives aniline usage. Rising demand for durable organic pigments in automotive coatings and plastics boosts the consumption of aniline derivatives.

Aniline Market Share, By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Rubber Chemicals | 38.00% |

| Dyes Pigments | 18.00% |

| Pharmaceuticals | 14.00% |

| Agrochemicals | 16.00% |

| Others | 14.00% |

- Rubber Chemicals (38.00%) Why it dominates: "Accounts for 38.00% of the market, driven by strong demand from the tire and automotive industries, where aniline is widely used in the production of rubber processing chemicals."

- Dyes Pigments (18.00%) Why it is gaining momentum: "Holds 18.00% share, supported by increasing demand in textiles, printing, and coatings industries for vibrant and durable color solutions."

- Agrochemicals (16.00%) Why it is gaining momentum: "Represents 16.00% of the market, driven by growing agricultural activities and demand for crop protection chemicals."

- Pharmaceuticals (14.00%) Why it is gaining momentum: "Accounts for 14.00% share, supported by expanding use in drug intermediates and increasing healthcare demand."

- Others (14.00%) Why it is gaining momentum: "Captures 14.00% of the market, driven by diverse applications across specialty chemicals and industrial processes."

Type Insights

Which Type Dominated the Aniline Market in 2025?

The aniline segment dominated the market in 2025, driven by surging demand for Methylene Diphenyl Diisocyanate (MDI) in polyurethane foams for construction, insulation, and automotive industries, driving growth. High-volume use in automotive lightweight components and construction materials propelled the market. A robust recovery and growth in the automotive industry heightened demand for aniline-based rubber processing chemicals and rubber additives.

The toluidine segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by demand for methylene diphenyl diisocyanate (MDI) and rubber processing chemicals. The market is expanding through diverse derivatives such as dyes, pigments, and agricultural chemicals. Growth is fueled by increasing use of polyurethane foams in construction and automotive lightweighting, alongside rising demand for rubber chemicals in tire manufacturing.

End Use Insights

How did the Automotive Segment Dominate the Aniline Market in 2025?

The automotive segment dominated the market in 2025. primarily through high demand for Methylene Diphenyl Diisocyanate (MDI)-based polyurethane foams used in vehicle interiors, seating, and insulation. Aniline is a key precursor to MDI, which offers lightweighting capabilities, durability, and comfort, while aniline-based rubber chemicals enhance tire performance. Rapidly expanding automobile production, particularly in emerging markets like India and China, has accelerated the consumption of aniline-based products.

The pharmaceutical segment is projected to have the fastest CAGR in the market between 2026 and 2035, driven by its critical role as an intermediate in pharmaceuticals, agrochemicals, and MDI (polyurethane) production. a focus on sustainable production, capacity expansion, and increasing demand from the pharmaceutical sector, which is projected to grow significantly in the market.

Regional Insights

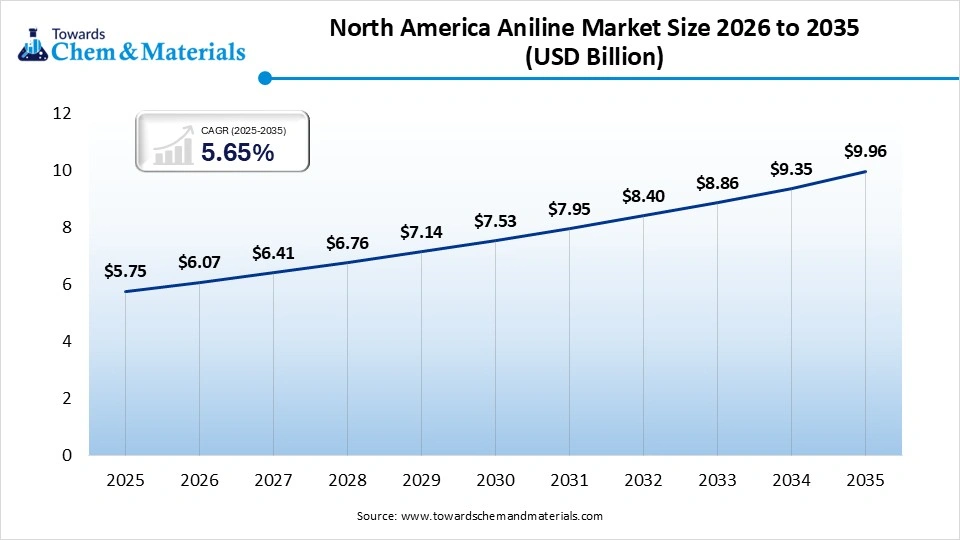

The North America aniline market size was valued at USD 5.75 billion in 2025 and is expected to be worth around USD 9.96 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.65% over the forecast period from 2026 to 2035. North America dominates the market share 53.00%, through high-value specialty derivative production, robust demand for Methylene Diphenyl Diisocyanate (MDI) in construction/automotive sectors, and strategic investments in sustainable, bio-based aniline technologies. Major upgrades by players like BASF increased capacity to meet demand for polyurethane foams. Stringent Environmental Protection Agency (EPA) regulations and a market shift toward sustainable products have encouraged North American companies, such as BASF and Covestro, to lead in bio-based aniline research and development.

")

U.S. Aniline Market Growth Factor

The U.S. aniline market is primarily driven by robust demand for Methylene Diphenyl Diisocyanate (MDI), a key component in producing polyurethane foams for automotive insulation and construction industries. Rising demand for lightweight vehicles and infrastructure development, alongside reliance on aniline-based rubber processing chemicals, fuels market expansion. The US represents a mature and strategic hub in North America for aniline production, balancing domestic consumption and export needs.

Europe Aniline Market Growth Factor

Europe aniline market segment accounted for the major revenue share of xx% in 2025 .Europe is expected to have the fastest growth in the market in the forecast period between 2026 and 2035, driven by high demand for methylene diphenyl diisocyanate (MDI) in polyurethane foam production, catering to the automotive, construction, and insulation sectors. The other key growth drivers include the rising adoption of lightweight materials in automotives, increased investment in energy-efficient building insulation, and expanding pharmaceutical and rubber processing industries, which support the growth in the market.

")

Germany Aniline Market Growth Factor

The German aniline market is projected to grow steadily, driven by strong demand from the automotive, construction, and chemical sectors, rising demand for methylene diphenyl diisocyanate (MDI) used in polyurethanes, increasing production of rubber-based automotive components, and investments in bio-based aniline. There is a growing shift toward eco-friendly, bio-aniline, allowing manufacturers to reduce their environmental impact and align with sustainable development goals.

Asia Pacific Aniline Market Growth Factor

Asia Pacific aniline market segment accounted for the major revenue share of xx% in 2025 .The Asia Pacific aniline market is primarily driven by surging demand for Methylene Diphenyl Diisocyanate (MDI) in polyurethane foams, rapid urbanization, and automotive production growth. As the largest consumer, the region's market is bolstered by increased construction activity and rubber processing, particularly in China and India. Rapid urbanization and infrastructure projects across China, India, and Southeast Asia drive demand for polyurethane-based insulation and coatings.

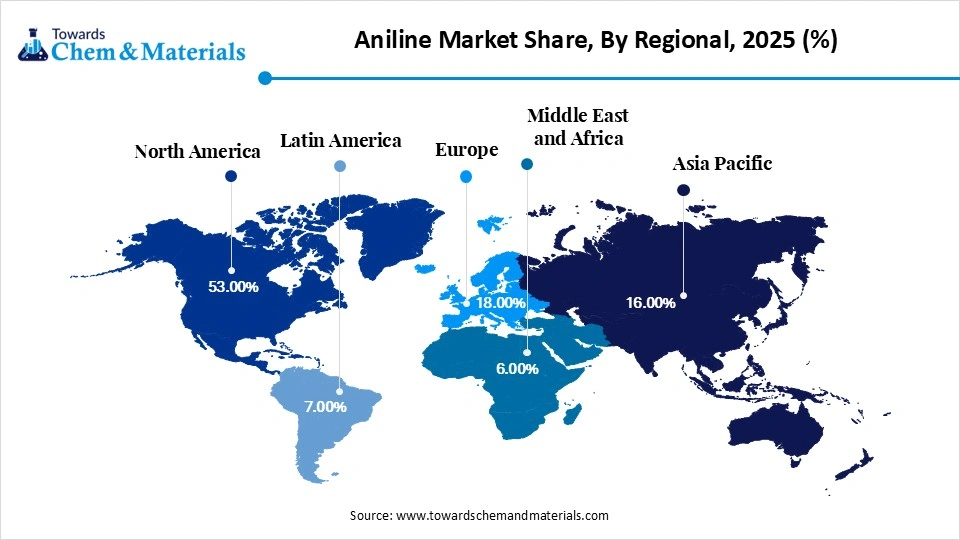

Aniline Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 53.00% |

| Europe | 18.00% |

| Asia Pacific | 16.00% |

| Latin America | 7.00% |

| Middle East & Africa | 6.00% |

- North America (53.00%) Why it dominates: "Accounts for 53.00% of the market, driven by strong presence of chemical manufacturing facilities, high demand from automotive and rubber industries, and advanced industrial infrastructure."

- Europe (18.00%) Why it is gaining momentum: "Holds 18.00% share, supported by established chemical industry and increasing focus on specialty and sustainable chemical production."

- Asia Pacific (16.00%) Why it is gaining momentum: "Represents 16.00% of the market, driven by expanding industrial base, growing automotive sector, and rising chemical production capacity."

- Latin America (7.00%) Why it is gaining momentum: "Accounts for 7.00% share, supported by developing industrial activities and increasing demand from agriculture and manufacturing sectors."

- Middle East & Africa (6.00%) Why it is gaining momentum: "Captures 6.00% of the market, driven by gradual industrial development and investments in chemical and manufacturing industries."

India Aniline Market Growth Factor

The Indian aniline market drivers include robust demand from the pharmaceutical, rubber processing, and dye industries, alongside rising methylene diphenyl diisocyanate (MDI) demand for polyurethane foams in construction and automotive sectors. The pharmaceutical industry is a leading consumer of aniline, particularly for producing compounds like paracetamol, contributing significantly to market growth. As India's textile sector expands, the demand for aniline-based dyes and pigments for color enhancement is growing.

Recent Developments

- In July 2025, the Government of India officially withdrew the Quality Control Orders (QCOs) for Aniline, Acetic Acid, and Methanol, removing mandatory Bureau of Indian Standards (BIS) certification for these industrial chemicals. This regulatory shift simplifies compliance for manufacturers and importers, reducing costs associated with mandatory ISI certification. (Source: www.indianchemicalnews.com)

- In May 2025, Jaguar Land Rover is preparing to launch a new, India-exclusive Range Rover Himalayan Edition, featuring design elements inspired by Himalayan landscapes and a strictly limited production run. As a follow-up to the Ranthambore Edition, this new model will be locally assembled at JLR's Pune facility, following high demand for bespoke, themed vehicles.(Source: ackodrive.com)

Top players in the Aniline Market & Their Offerings:

- Sumitomo Chemical Co., Ltd.: Sumitomo Chemical supplies aniline for use in rubber processing chemicals, dyes, and agrochemicals. The company has strong production capabilities in Asia and focuses on specialty chemical applications.

- Mitsui Chemicals, Inc.: Mitsui Chemicals produces aniline for downstream applications, including polyurethane production, coatings, and specialty intermediates. The company emphasizes innovation and advanced material solutions.

- Tosoh Corporation: Tosoh manufactures aniline for use in isocyanates, dyes, and rubber processing chemicals. Its integrated chemical operations support a consistent supply to industrial markets.

- PetroChina Company Limited: PetroChina produces aniline as part of its petrochemical operations, supplying domestic and international markets. The company benefits from strong feedstock integration and large-scale refining capacity.

- China Petroleum & Chemical Corporation (Sinopec): Sinopec is a major producer of aniline in Asia, leveraging its extensive petrochemical infrastructure.

- BASF Corporation

- BONDALTI

- Borsodchem Mchz

- Covestro AG

- Dow

- GNFC

- Huntsman International LLC

- Jilin Connell Chemical Industry Co., Ltd.

- Mitsubishi Chemical

- Sabic

- SP Chemicals Holdings Ltd.

- Sumika Bayer Urethane Co., Ltd.

- The Dow Chemical Company

- Wanhua Chemical Group Co. Ltd.

Segments Covered:

By Application

- Rubber Chemicals

- Dyes Pigments

- Pharmaceuticals

- Agrochemicals

- Others

By Type

- Aniline

- Nitroaniline

- Chloroaniline

- Toluidine

- Others

By End-Use

- Automotive

- Textile

- Pharmaceutical

- Agriculture

- Others

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)