Content

Thermoplastic Polyolefin Market Trends, Growth and Market Size Analysis

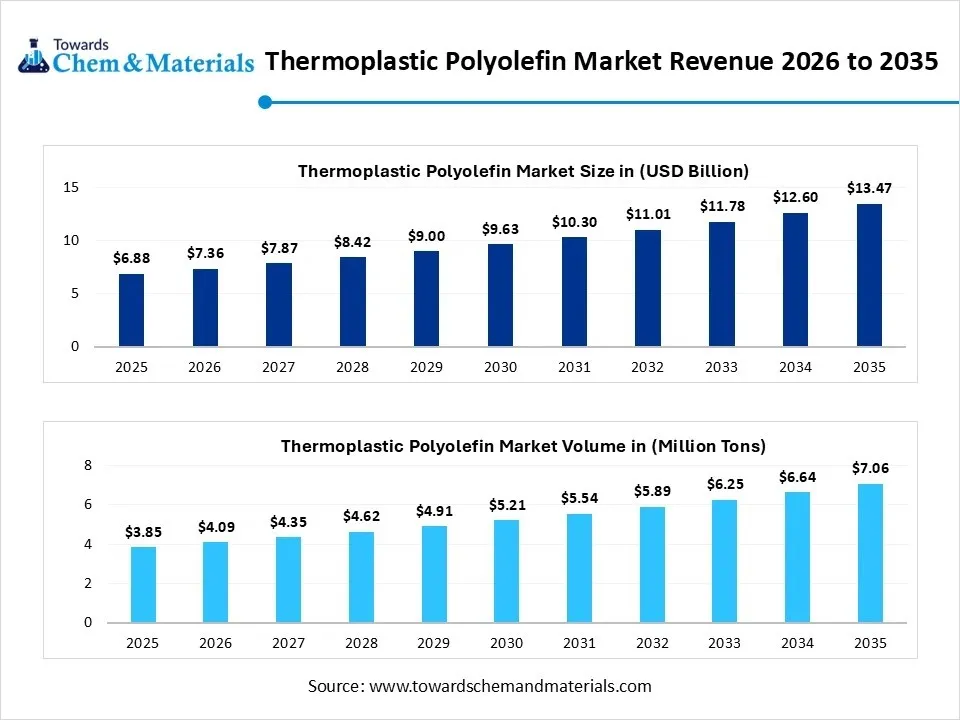

The global Thermoplastic Polyolefin market size was estimated at USD 6.88 billion in 2025 and is expected to be worth around USD 13.47 billion by 2035, growing at a CAGR of 6.95% from 2026 to 2035. In terms of volume, the Thermoplastic Polyolefin market is projected to grow from 3.85 million tons in 2025 to 7.06 million tons by 2035. growing at a CAGR of 6.95% from 2026 to 2035. Greater demand from the global automotive industry has accelerated the industry's growth in recent years.

Market Highlights

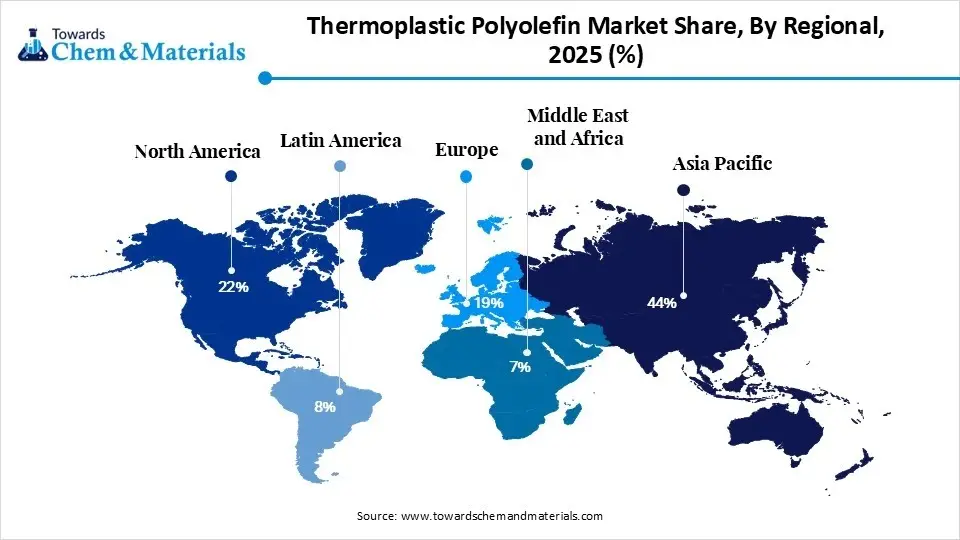

- By region, Asia Pacific dominated the market with a share of 44% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.5% in the forecast period.

- By region, North America is notably growing with 22% market share in 2025.

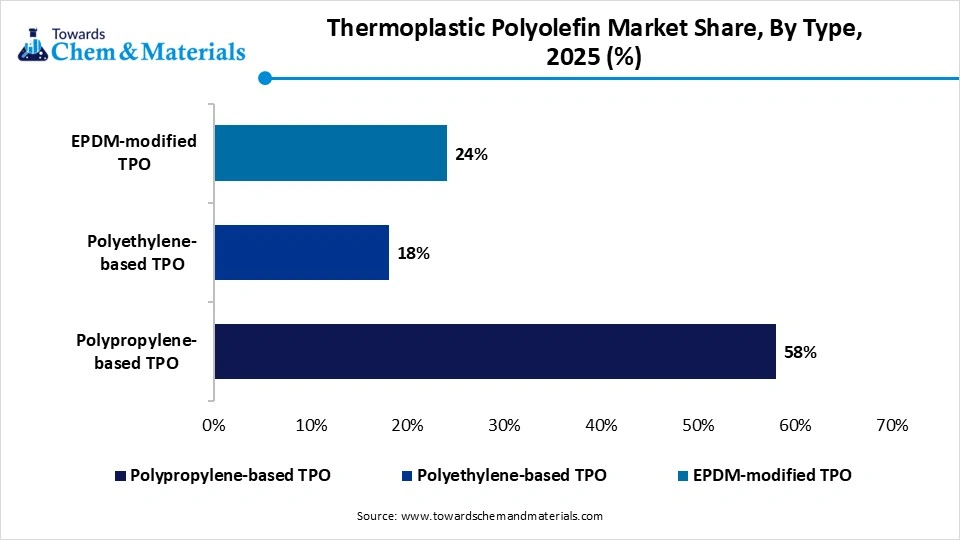

- By type, the polypropylene-based TPO segment dominated the market with 58% share in 2025.

- By type, the EPDM-modified TPO segment held the 24% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.5% in the forecast period.

- By form, the pellets segment dominated the market with 46% share in 2025.

- By form, the sheets segment held the 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.2% in the forecast period.

- By application, the automotive segment dominated the market with 52% share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.1% in the forecast period.

- By processing method, the injection molding segment dominated the market with 40% share in 2025.

- By processing method, the extrusion segment held the 32% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.9% in the forecast period in 2025.

Market Size and Volume Forecast

- Market Size (2025): USD 6.88 Billion

- CAGR (2025–2035): 6.95%

- Market Projected Size (2035): USD 13.47 Billion

- Market Volume (2025): 3.85 Million Tons

- Volume CAGR (2025–2035): 6.25%

- Market Projected Volume (2035): 13.47 Million Tons

- Pricing Data (2025):

- Average Manufacturing Price: USD 1,659/ton

- Average Selling Price: USD 2,160/ton

- Pricing CAGR (2025–2035): 3.55%

Flexible and Strong TPO Materials

The specific polymer material, which is formed by blending polypropylene with the elastomeric components like rubber, is known as the thermoplastic polyolefin. Also, by providing flexibility and rigidity to materials, the thermoplastic polyolefins have gained major attention in wider industrial works in recent years. The industries such as automotive, packaging, and construction are seen using thermoplastic polyolefins.

Recent Market Trends:

- The heavy trend towards the material design flexibility has offered substantial growth prospects for the manufacturing firms in recent years. Moreover, the consumers are demand the material which is not only durable but also support advanced product designs nowadays.

- The greater focus on efficient and faster manufacturing has enabled high-return ventures for the manufacturers in the current period. As the TPO has seen taking lower energy while manufacturing than other materials and is quickly manufactured, as per the observation.

- The shift towards the early integration in product development is likely to open profitable avenues for manufacturers in the coming years. in recent years, manufacturers are considering TPO in the initial design stage instead of using it as a replacement for other materials.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 7.36 Billion/ 4.09 Million Tons |

| Revenue Forecast in 2035 | USD 13.47 Billion/ 7.06 Million Tons |

| Growth Rate | CAGR 6.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Form, By Application, By Processing Method, By Region |

| Key companies profiled | Dow Chemical Company (Dow Inc.), Mitsui Chemicals, Inc., and Sumitomo Chemical Co., Ltd. |

Advanced Formulations Enhancing TPO Performance

The industry is heavily turning towards the development of customizable material properties. Manufacturers are now able to modify TPO characteristics such as strength, flexibility, and heat resistance based on specific application requirements. This is achieved through controlled formulation and advanced processing techniques.

Supply Chain Analysis of the Thermoplastic Polyolefin Market:

Distribution to Industrial Users

Industrial users receive thermoplastic polyolefin (TPO) primarily through bulk shipments or specialized distributors in pelletized form. Supplied in large sacks or silos, it is routed to automotive, construction, and manufacturing sectors.

Advanced logistics ensure timely delivery for injection molding and extrusion processes, meeting high-volume demands for durable, weather-resistant components

Chemical Synthesis and Processing

Thermoplastic polyolefin synthesis involves the catalytic polymerization of propylene and ethylene, often using metallocene or Ziegler-Natta catalysts. During processing, these polymers are blended with rubbery elastomers and reinforcing fillers.

Techniques like twin-screw extrusion ensure a homogenous melt, which is then pelletized for final molding into durable, high-performance industrial components.

Regulatory Compliance and Safety Monitoring

Regulatory compliance for TPO focuses on adhering to REACH and RoHS standards, ensuring materials are free from hazardous substances. Safety monitoring involves rigorous flammability testing and VOC emission analysis.

Manufacturers implement quality control protocols to meet automotive and construction safety benchmarks, guaranteeing that chemical stabilizers remain stable during high-heat industrial applications.

Thermoplastic Polyolefin Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Toxic Substances Control Act (TSCA): Section 5 requires Pre-manufacture Notification (PMN) for new chemical substances; Section 6(h) regulates persistent, bioaccumulative, and toxic (PBT) chemicals often used as additives in TPOs. | Chemical inventory management, PBT substance restrictions (e.g., flame retardants like DecaBDE), and migration limits for food-grade applications. |

| Europe | European Chemicals Agency (ECHA) |

REACH Regulation (EC) No 1907/2006: Annex XVII restricts hazardous substances; ECHA has recently proposed adding specific TPOs/additives to the Authorisation List as Substances of Very High Concern (SVHC). | Phasing out SVHCs, mandatory recycled content (via Circular Economy initiatives), and strict limit monitoring for chemical migration in packaging. |

| China | State Administration for Market Regulation (SAMR) | GB 4806.1-2016: The framework standard for all Food Contact Materials (FCM). |

Mandatory compliance with "Guobiao" (GB) national standards for market entry, rigorous safety testing for consumer goods, and standardized migration testing for specialized chemicals. |

Market Dynamics

Driver

Rising Demand Boosting Material Innovation

The increasing demand for lightweight and durable materials across industries has opened profitable pathways for manufacturers in recent years. Companies are constantly trying to reduce product weight while maintaining strength, especially in the automotive and construction sectors.

Restraint

Thermal Constraint Challenging TPO Adoption

The limited performance under very high temperatures compared to some advanced engineering plastics is expected to hinder the industry growth during the forecast period. Also, this restricts its use in certain high-heat applications.

Opportunity

Electric Vehicles Driving TPO Market Opportunity

The rise of electric vehicles creates demand for lightweight and heat-resistant materials, where TPO can play an important role, which is anticipated to create significant opportunities for manufacturers in the coming years. There is also growing potential in sustainable construction, where TPO can be used for energy-efficient roofing and insulation.

Segmental Insights

Type Insights

The Polypropylene-based TPO Segment Dominated the Thermoplastic Polyolefin Market with 58% Market Share in 2025

The polypropylene-based TPO segment dominated the market with 58% share in 2025, as it provides a strong balance of performance and cost. Polypropylene is widely available and relatively inexpensive, which helps reduce overall production costs. It also offers good stiffness, chemical resistance, and durability. When combined with rubber, it creates a material that performs well in demanding conditions.

The EPDM-modified TPO segment held the 24% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.5% in the forecast period, owing to it offers improved flexibility and weather resistance. EPDM rubber enhances the material’s ability to handle extreme temperatures and outdoor conditions. This makes it especially useful for roofing, sealing, and automotive exterior parts.

The polyethylene-based TPO segment held the 18% market share in 2025, owing to its excellent flexibility and moisture resistance. It is particularly useful in applications where softness and waterproofing are important. This makes it suitable for films, packaging, and certain construction uses. Polyethylene is also widely available, which supports its increasing use.

")

Form Insights

The Pellets Segment Dominated the Market with 46% Market Share in 2025

The pellets segment dominated the market with 46% share in 2025 because pellets are easy to handle, store, and process. They are the standard form used in most manufacturing machines such as injection molding and extrusion systems. Pellets allow consistent feeding into machines, which improves production efficiency and reduces waste.

The sheets segment held the 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.2% in the forecast period, due to increasing demand in construction and infrastructure applications. TPO sheets are widely used in roofing, wall panels, and protective coverings. They offer durability, weather resistance, and energy efficiency.

The films segment held the 18% market share in 2025, owing to rising demand in packaging and protective applications. TPO films are lightweight, flexible, and resistant to moisture, making them suitable for wrapping and covering products. Industries are increasingly looking for materials that can protect goods while reducing overall weight.

Application Insights

The Automotive Segment Dominated the Thermoplastic Polyolefin Market with 52% Market Share in 2025

The automotive segment dominated the market with 52% share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.1% in the forecast period, as strong demand for lightweight and durable materials in vehicle manufacturing. TPO is widely used in bumpers, dashboards, and interior components due to its impact resistance and flexibility. Reducing vehicle weight helps improve fuel efficiency and performance, which is a key priority for manufacturers.

The building and construction segment held the 20% market share in 2025 due to the increased demand for durable and energy-efficient materials. TPO is widely used in roofing and waterproofing applications because it can withstand harsh weather conditions. It also reflects heat, which helps reduce cooling costs in buildings.

The packaging segment held the 12% market share in 2025, owing to increasing need for lightweight and protective materials. TPO offers flexibility, strength, and resistance to moisture, making it suitable for various packaging applications. As industries focus on reducing material usage while maintaining product safety, TPO becomes a practical option.

Processing Method Insights

The Injection Molding Segment Dominated the Market with 40% Market Share in 2025

The injection molding segment dominated the market with 40% share in 2025 owing to it allows precise and efficient production of complex shapes. This method is widely used in the automotive and consumer goods industries. TPO works well with injection molding because it flows easily when heated and solidifies quickly.

The extrusion segment held the 32% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.9% in the forecast period in 2025, owing to increasing demand for continuous products such as sheets, films, and pipes. This process allows TPO to be shaped into long and uniform forms, which is useful in the construction and packaging industries. Extrusion is also efficient for large-scale production and reduces material wastage.

The blow molding segment held the 15% market share in 2025 owing to it is suitable for producing hollow products such as containers and tanks. TPO’s flexibility and strength make it ideal for this process. Industries are increasingly using blow molding to create lightweight and durable products. This method also allows efficient production with reduced material usage.

Regional Insights:

How will Asia Pacific Dominate the Thermoplastic Polyolefin Market in 2025?

Asia Pacific dominated the market with a share of 44% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.5% in the forecast period, due to its suitability for producing hollow products such as containers and tanks. TPO’s flexibility and strength make it ideal for this process. Industries are increasingly using blow molding to create lightweight and durable products. This method also allows efficient production with reduced material usage.

China’s Industrial Strength Boosts the TPO Market

China maintained its dominance in the market, owing to its large manufacturing base. It is one of the leading producers of automotive components, construction materials, and packaging products. The country has strong supply chains and access to raw materials, which support large-scale production. Rapid urbanization and infrastructure development are also increasing demand for TPO.

Thermoplastic Polyolefin Market Evaluation in North America

North America is notably growing with 22% market share in 2025, owing to industries in this region that are investing in high-performance and recyclable materials, which support TPO adoption. The presence of established automotive and construction sectors also drives demand. Additionally, technological advancements and research activities contribute to innovation in TPO applications.

")

United States Emerging as TPO Leader

United States is expected to emerge as a prominent country for the thermoplastic polyolefin market in the coming years, due to its strong automotive industry that uses TPO for lightweight and durable components. The construction sector also supports demand through roofing and insulation applications. The country is known for technological innovation, which helps in developing advanced TPO materials.

Recent Development

In March 2026, IB Roof Systems unveiled their latest thermoplastic polyolefin (TPO) membranes. Also, the newly launched membranes have been added to its commercial roofing product line, and the membranes have passed ASTM D6878 standards as per the company's claim.(Source: www.roofingcontractor.com)

Top Vendors in the Thermoplastic Polyolefin Market & Their Offerings:

- ExxonMobil: ExxonMobil is a global leader in TPO production, leveraging its proprietary metallocene catalyst technology to create high-performance resins. The company focuses on the automotive and packaging sectors, providing lightweight, durable solutions that improve fuel efficiency. Their integrated supply chain ensures consistent quality and advanced chemical properties for demanding industrial applications.

- LyondellBasell: LyondellBasell is one of the world's largest plastics and chemicals companies, renowned for its extensive polyolefin portfolio. They excel in developing customized TPO grades for automotive interiors and exteriors, prioritizing impact resistance and aesthetic finish. Their global reach and focus on circular economy initiatives drive innovation in polymer recycling.

- SABIC: SABIC is a major diversified chemical manufacturer providing specialized TPO solutions under brands like SABIC® PP compounds. They serve critical industries, including healthcare, automotive, and construction, focusing on sustainability and high-heat stability. Their research-driven approach helps clients optimize manufacturing processes while meeting stringent global regulatory and safety standards.

Other Key Players

- The Dow Chemical Company (Dow Inc.)

- Mitsui Chemicals, Inc.

- Sumitomo Chemical Co., Ltd.

- Borealis AG

Segments Covered in the Report

By Type

- Polypropylene-based TPO

- Homopolymer PP-based TPO

- Copolymer PP-based TPO

- Polyethylene-based TPO

- HDPE-based TPO

- LLDPE-based TPO

- EPDM-modified TPO

- High Rubber Content TPO

- Low Rubber Content TPO

By Form

- Pellets

- Sheets

- Films

- Powders

By Application

- Automotive

- Exterior Components

- Bumpers

- Body Panels

- Interior Components

- Dashboard

- Door Panels

- Under-the-hood Components

- Exterior Components

- Building & Construction

- Roofing Membranes

- Waterproofing Systems

- Packaging

- Flexible Packaging

- Rigid Packaging

- Electrical & Electronics

- Wire & Cable Insulation

- Appliance Components

- Industrial

- Industrial Parts

- Protective Coatings

By Processing Method

- Injection Molding

- Extrusion

- Blow Molding

- Thermoforming

Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (3)