Content

Polypropylene Fiber Market Trends, Growth and Market Size Analysis

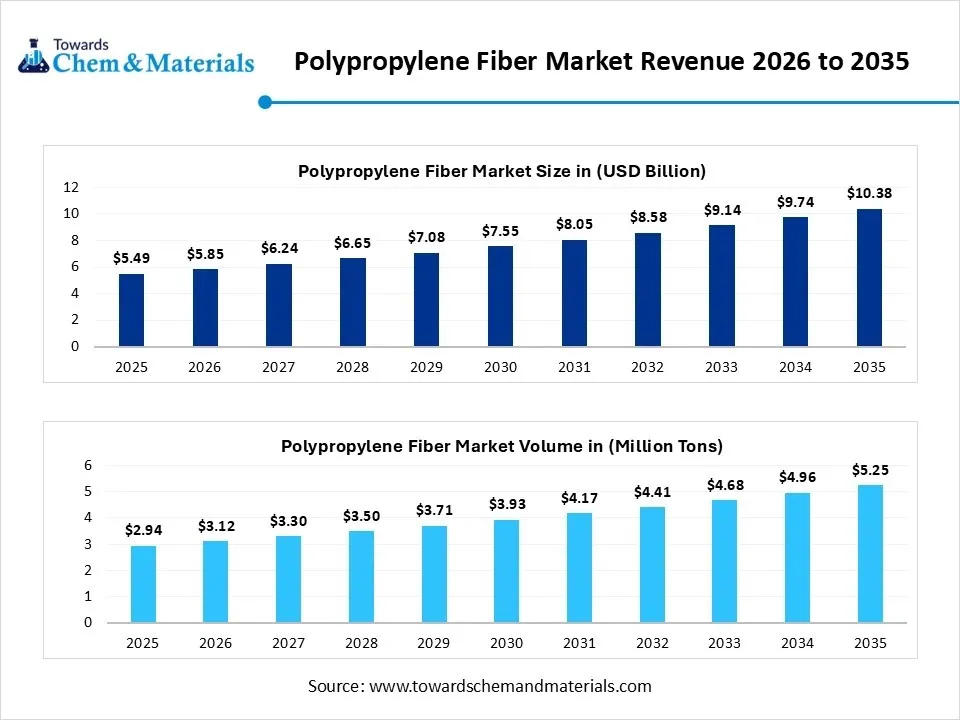

The global Polypropylene Fiber market size was estimated at USD 5.49 billion in 2025 and is expected to be worth around USD 10.38 billion by 2035, growing at a CAGR of 6.58% from 2026 to 2035. In terms of volume, the Polypropylene Fiber market is projected to grow from 2.94 million tons in 2025 to 5.25 million tons by 2035. growing at a CAGR of 5.98% from 2026 to 2035. The growth of the market is primarily driven by high demand for lightweight, cost-effective materials in automotive, construction, and hygiene sectors.

Market Highlights

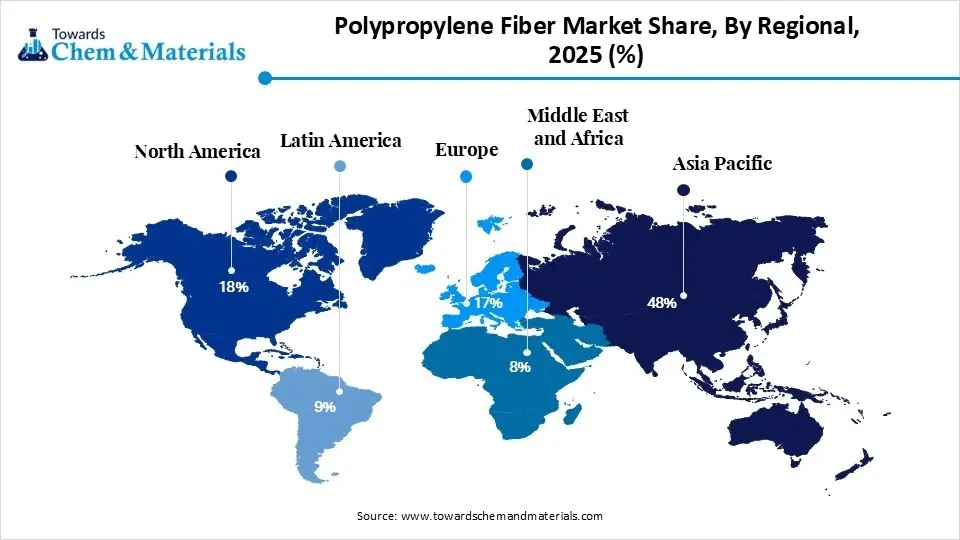

- By region, Asia Pacific dominated the market with a share of 48% in 2025 and is expected to sustain its position while growing with a CAGR of 7.2% in the forecast period.

- By region, North America held the market share of 18% in 2025.

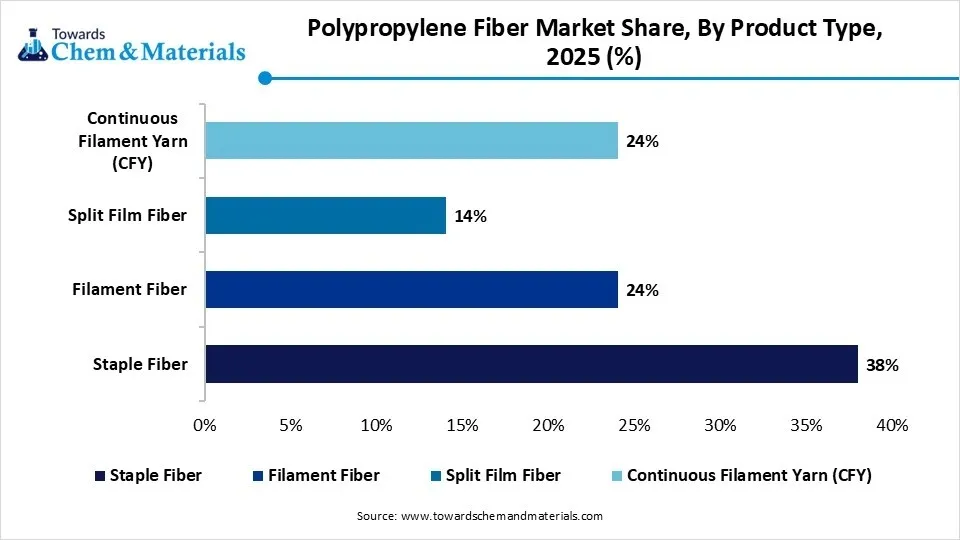

- By product type, the staple fiber segment dominated the market with 38% share in 2025.

- By product type, the continuous filament yarn (CFY) segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.1% in the forecast period.

- By process, the melt spinning segment dominated the market with 68% share in 2025.

- By process, the solution spinning segment held 18% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.9% in the forecast period.

- By application, the geotextiles segment dominated the market with 26% share in 2025.

- By application, the concrete reinforcement segment held 10% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.2% in the forecast period.

- By end-use industry, the construction segment dominated the market with 32% share in 2025.

- By end-use industry, the healthcare and hygiene segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.9% in the forecast period.

- By form, the yarn segment dominated the market with 44% share in 2025.

- By form, the nonwoven segment held 30% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.9% in the forecast period.

Market Size and Volume Forecast

- Market Size (2025): USD 5.49 Billion

- CAGR (2025–2035): 6.58%

- Market Projected Size (2035): USD 10.38 Billion

- Market Volume (2025): 2.94 Million Tons

- Volume CAGR (2025–2035): 5.98%

- Market Projected Volume (2035): 5.25 Million Tons

- Pricing Data (2025):

- Average Manufacturing Price: USD 1,420/ton

- Average Selling Price: USD 1,880/ton

- Pricing CAGR (2025–2035): 3.3%

Market Overview

What Is the Significance of The Polypropylene Fiber Market?

The polypropylene fiber market is highly significant for driving sustainable, lightweight, and cost-effective solutions in construction, automotive, hygiene, and textile sectors due to its high durability, low density, and chemical resistance. With a high demand for non-woven fabrics, PP fibers are essential for producing disposable hygiene products (diapers) and medical masks, boasting high fluid repellency and barrier efficiency.

Recent Growth Trends:

- Infrastructure & Construction Growth: Polypropylene fibers are increasingly replacing steel in construction for concrete reinforcement, offering corrosion resistance and enhanced durability in major projects.

- Sustainability Focus: Manufacturers are shifting toward bio-based polypropylene and developing sustainable, 100% recyclable fibers to meet stricter environmental regulations and circular economy targets.

- Automotive Lightweighting: The automotive industry is driving demand by using PP fibers for interior components and increasing the use of continuous fiber-reinforced PP for lighter-weight structural parts.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 5.85 Billion / 3.12 Million Tons |

| Revenue Size and Volume Forecast in 2035 | USD 10.38 Billion / 5.25 Million Tons |

| Growth Rate | CAGR 6.58% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Process, By Application, By End-Use Industry, By Form, By Regions |

| Key companies profiled | Indorama Ventures Public Company Limited, Beaulieu International Group / Fibres International NV, Radici Partecipazioni S.p.A., International Fibres Group (IFG), Sika AG, BASF SE, Mitsubishi Chemical Group, DuPont de Nemours, Inc., Sinopec (China Petrochemical Corporation), Braskem S.A., Lotte Chemical Corporation, Freudenberg Group, ABC Polymer Industries LLC, Fiberpartner Aps, Belgian Fibers Group NV, Chemosvit Fibrochem, s.r.o., Zenith Fibres Ltd., The Euclid Chemical Company, Kolon Fiber Inc., Thrace Group, Tri Ocean Textile Co. Ltd., W. Barnet GmbH & Co. KG, INEOS Group Holdings S.A., Borealis AG, Formosa Plastics Corporation, ani TotalEnergies. |

Key Technological Shifts In The Polypropylene Fiber Market:

The market is experiencing a significant transformation driven by sustainability initiatives, advanced manufacturing, and high-performance applications in construction and mobility. Key technological shifts focus on enhancing performance, increasing recycled content, and adapting to stricter environmental regulations. Manufacturers are shifting toward renewable feedstocks, such as agricultural waste, to produce bio-based polypropylene fibers. This includes the introduction of carbon-neutral PP fibers, such as those launched by Indorama Ventures in early 2026.

Supply Chain Analysis of Polypropylene Fiber Market:

Polymer Production & Fiber Processing

- Polypropylene fibers are produced through polymerization of propylene followed by melt spinning, drawing, and texturizing to create fibers for textiles, nonwovens, and industrial applications.

- Key players: Indorama Ventures, LyondellBasell, Reliance Industries, SABIC.

Quality Testing and Certification

- Polypropylene fibers must meet standards for tensile strength, durability, chemical resistance, and safety compliance across textile and industrial applications.

- Key players: International Organization for Standardization, ASTM International, OEKO-TEX, European Chemicals Agency.

Distribution to Industrial Users

- Polypropylene fibers are supplied to textile manufacturers, nonwoven fabric producers, construction companies, automotive industries, and hygiene product manufacturers.

- Key players: Indorama Ventures, Reliance Industries, SABIC.

Polypropylene Fiber Market Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA); Consumer Product Safety Commission (CPSC) | Toxic Substances Control Act (TSCA); OSHA Hazard Communication Standard; Flammable Fabrics Act | Chemical safety, textile standards, worker protection | Polypropylene fibers used in textiles, geotextiles, and hygiene products must comply with safety, flammability, and workplace exposure standards. |

| European Union | European Chemicals Agency (ECHA); European Commission | REACH Regulation; CLP Regulation; Textile Labeling Regulation | Chemical registration, product safety, sustainability | The EU enforces strict chemical usage and sustainability regulations, especially for fibers used in textiles and medical applications. |

| China | Ministry of Industry and Information Technology (MIIT); State Administration for Market Regulation (SAMR) | Textile Industry Standards; Product Quality Law | Product quality, industrial compliance | China regulates polypropylene fiber production through strict quality standards and industrial safety regulations. |

| India | Ministry of Textiles; Bureau of Indian Standards (BIS) | BIS Textile Standards; Technical Textile Guidelines | Quality compliance, technical textiles | India promotes polypropylene fiber usage in technical textiles such as geotextiles, hygiene, and infrastructure applications. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of Health, Labour and Welfare (MHLW) | Japanese Industrial Standards (JIS); Chemical Substances Control Law (CSCL) | Product safety, chemical management | Japan regulates polypropylene fibers for high-performance applications including automotive and healthcare textiles. |

| South Korea | Ministry of Environment (MoE); Ministry of Trade, Industry and Energy (MOTIE) | K-REACH; Chemicals Control Act | Chemical registration, environmental safety | South Korea enforces strict chemical and environmental regulations for polymer fibers and related materials. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Polypropylene Fiber Market?

The market is experiencing steady growth, driven primarily by high demand for lightweight materials in construction, automotive, and hygiene sectors. Key drivers include the adoption of PP fibers in concrete reinforcement, growing nonwoven applications in healthcare, and the push for sustainable, 100% recyclable materials. Increased adoption in automotive interiors, such as carpets and upholstery, along with the use of PP composites for making lighter vehicle components, boosts market growth.

Restrains

What are the Key Growth Restraints of the Polypropylene Fiber Market?

Key growth restraints for the polypropylene fiber market include high volatility in raw material (petroleum/propylene) prices, intense competition from alternatives like polyester, and increasing environmental regulations against non-biodegradable synthetic waste. Technical limitations, such as low melting points and poor dyeability, further restrict its usage in certain high-performance or aesthetic applications.

Opportunities

What are the Key Growth Opportunities of the Polypropylene Fiber Market?

The market is experiencing significant growth, driven by rising demand for lightweight materials in automotive, construction, and hygiene sectors. Key growth opportunities include the expansion of sustainable, bio-based fibers, enhanced concrete reinforcement, and specialized nonwovens for medical applications. Development of bio-based polypropylene derived from renewable feedstocks offers opportunities to meet strict environmental regulations and sustainability targets.

Segmental Insights

Product Type Insights

The Staple Fiber Segment Dominated The Market With 38% Market Share In 2025

The staple fiber segment dominated the market with 38% share in 2025. Its growth is propelled by high demand for non-woven fabrics in hygiene (diapers, masks) and construction (geotextiles, concrete reinforcement) applications, driven by its lightweight, hydrophobic properties, and cost-effectiveness. These fibers are highly popular in infrastructure projects for creating durable geotextiles for soil stabilization and erosion control.

The continuous filament yarn (CFY) segment held 24% market share in 2025 and is expected to experience the fastest growth, with a CAGR of 7.1% over the forecast period, due to its high tenacity, low-cost superiority in industrial textiles, carpeting, and geotextiles. Used extensively in civil engineering for soil stabilization and infrastructure projects, demand is driven by the need for durable, lightweight materials

")

The filament fiber segment held 24% market share in 2025, driving growth through high-efficiency production, superior for textiles/automotive applications, and cost advantages. Its growth is sustained by rapid adoption in carpets, upholstery, and hygiene, often replacing staple fibers due to reduced labor and processing costs. The shift toward lightweight, sustainable materials in vehicles is driving demand for filament in carpets, mats, and liners.

Process Insights

The Melt Spinning Segment Dominated The Market With 68% Market Share In 2025

The melt spinning segment dominated the market with 68% share in 2025, driven by high demand for cost-effective, high-throughput production of nonwovens (diapers, hygiene) and technical textiles. It is favored for its simplicity and efficiency, particularly in spunbond and melt-blown technologies, which are seeing rapid expansion for medical, filtration, and automotive applications. Melt-blown technology, a specific, high-growth subset of melt spinning, is expanding due to its ability to produce ultra-fine, efficient filtering fibers.

The solution spinning segment held 18% market share in 2025 and is expected to experience the fastest growth, with a CAGR of 6.9% over the forecast period, driven primarily by the need for high-strength, high-modulus, and ultra-high molecular weight polypropylene (UHMWPP) fibers for industrial, medical, and defense applications. While standard polypropylene fiber is produced via cost-effective melt spinning, solution-based technologies are gaining traction where superior tenacity is required.

The dry spinning segment held 14% market share in 2025, driven by its unique ability to produce highly specialized, fine-denier fibers and sophisticated, multi-grooved structures that enhance performance in high-growth, technical end-use sectors like hygiene, medical, and specialized filtration. While melt spinning is standard for commodity PP, dry spinning (often specialized within solution or hybrid processes) is becoming critical for superior, high-value applications.

Application Insights

The Geotextiles Segment Dominated The Polypropylene Fiber Market With 26% Market Share In 2025

The geotextiles segment dominated the market with 26% share in 2025 due to high demand in infrastructure, transportation, and environmental projects, driven by its superior strength, low cost, and durability. Key drivers include increased urbanization in the Asia-Pacific and rising demand for erosion control and soil stabilization, with PP leading as the preferred material for non-woven geotextiles. The segment is also experiencing growth from North American and European projects that focus on transportation and sustainable development.

The hygiene products segment held 18% market share in 2025, driven by high demand for disposable baby diapers, adult incontinence products, and feminine care items. driven by high demand for disposable baby diapers, adult incontinence products, and feminine care items. Increased spending on hygiene, particularly in emerging Asia Pacific markets, has increased the adoption of premium, disposable sanitary products.

The concrete reinforcement segment held 10% market share in 2025 and is expected to experience the fastest growth, with a CAGR of 7.2% over the forecast period, driven by rising demand for durable, crack-resistant construction materials. Growing global investments in infrastructure development, including roads and bridges, fuel demand for advanced materials.

End-Use Industry Insights

The Construction Segment Dominated The Market With 32% Market Share In 2025

The construction segment dominated the market with 32% share in 2025, driven by its widespread adoption as a durable, cost-effective, and sustainable alternative to traditional concrete reinforcements. Key drivers include rising infrastructure investment in emerging economies, the need for enhanced structural durability, and the growing focus on green building technologies. Expanding urbanization and increased government spending on infrastructure are creating high demand for durable building materials.

The textile industry segment held 22% market share in 2025, due to high demand for lightweight, moisture-wicking, and durable materials in performance sportswear, activewear, and home textiles. Its cost-effectiveness, 100% recyclability, and superior chemical/stain resistance are accelerating adoption. The fibers are heavily used in rugs, carpets, and upholstery fabrics due to their inherent stain resistance, durability, and low color fading, providing a cost-effective alternative to traditional fibers.

The healthcare & hygiene segment held 14% market share in 2025 and is expected to experience the fastest growth, with a CAGR of 6.9% over the forecast period. This expansion is primarily fueled by the surging demand for disposable hygiene products and increased adoption of single-use medical materials like masks, gowns, and sterilization wraps. The industry is moving towards premium products that use bicomponent (PE-PP) blends for improved softness in adult care, alongside advancements in sustainable and recyclable PP fibers to meet environmental standards.

Form Insights

The Yarn Segment Dominated The Market With 44% Market Share In 2025

The yarn segment dominated the market with 44% share in 2025. Its growth is driven by its dominant role in industrial applications, such as woven geotextiles, carpet backing, and high-strength packaging materials. The demand for yarn is surging in civil engineering projects, particularly in Asia-Pacific and the Middle East, for soil stabilization and reinforcement. Macro-synthetic polypropylene fibers are replacing steel in concrete reinforcement, reducing costs and providing corrosion resistance.

The nonwoven segment held 30% market share in 2025 and is expected to experience the fastest growth, with a CAGR of 6.9% over the forecast period. This growth is fueled by high demand for cost-effective, lightweight, and durable materials in hygiene products, medical applications, and construction. PP nonwoven fabrics are widely used in disposable diapers, adult incontinence products, and feminine care products due to their softness and fluid-repellent properties. The medical sector further accelerates demand for surgical masks, gowns, and drapes.

The woven segment held 26% market share in 2025, largely driven by its dominance in infrastructure projects, particularly woven geotextiles and industrial packaging. Woven PP geotextiles are favored for their superior tensile strength, durability, and cost-effectiveness in soil stabilization, making them preferred in large civil engineering projects. Woven PP is heavily utilized in concrete reinforcement and large flooring or tunnel projects to reduce plastic-shrinkage cracking.

Regional Insights

How did Asia Pacific Dominate the Polypropylene Fiber Market in 2025?

Asia Pacific dominated the market with a 48% share in 2025 and is expected to sustain its position, growing at a CAGR of 7.2% over the forecast period, due to massive manufacturing capacity in China and India, rapid urbanization, and high demand from construction, hygiene, and automotive industries. Major projects, including ExxonMobil's expanded production capacity in Singapore, strengthened the region’s ability to meet local and export demands.

India Polypropylene Fiber Market Growth Factor

The Indian market is experiencing strong growth, largely driven by the expanding technical textiles sector, rapid infrastructure development, and rising demand in the automotive and hygiene industries. The National Technical Textiles Mission is expected to boost the market. The market is expected to remain a key player in the Asia Pacific region, fueled by urbanization, increased disposable income, and government initiatives promoting manufacturing.

")

North America Polypropylene Fiber Market Growth Factor

North America held the market share of 18% in 2025, driven by strong demand in the automotive, construction, and healthcare sectors. Increased use of polypropylene fiber in concrete reinforcement and soil stabilization boosts durability in construction projects. Growing investment in eco-friendly, bio-based, and recyclable polypropylene alternatives is shaping future trends. Advances in producing high-melting-point fibers, which offer superior strength and heat resistance, are expanding application areas.

U.S. Polypropylene Fiber Market Growth Factor

The U.S. polypropylene fiber market is experiencing steady growth, driven primarily by high demand in the automotive, construction, and healthcare industries. Demand for high-performance polypropylene fiber is driven by the need for lightweight materials in vehicles to improve fuel efficiency and in electric vehicles (EVs). The development of bio-based, recyclable, and specialty-grade fibers aligns with environmental regulations, boosting adoption.

Recent Developments

- In February 2026, Polyplastics Co., Ltd. introduced new PLASTRON® RA627P long-fiber thermoplastic (LFT) grades, featuring 30% regenerated cellulose fibers in a polypropylene matrix for improved sustainability. These eco-friendly, low-density materials are designed for high-rigidity applications in automotive and audio equipment.(Source: www.chemanalyst.com)

- In July 2025, EcoTechnilin inaugurated a fourth production line at its Tychy, Poland plant, raising total annual capacity to 12,000–13,000 tonnes to meet rising demand for natural fiber, non-woven technical reinforcements. The expansion, supporting automotive and industrial applications, includes a new 250 g/m² GFPP non-woven,(Source: www.jeccomposites.com)

Top players in the Polypropylene Fiber Market & Their Offerings:

- ExxonMobil Corporation: ExxonMobil produces polypropylene resins used in fiber applications such as nonwovens, textiles, and industrial materials. The company focuses on high-performance PP grades for hygiene, automotive, and packaging sectors.

- LyondellBasell Industries N.V.: LyondellBasell is a major supplier of polypropylene and PP-based fiber materials. Its products are widely used in nonwoven fabrics, geotextiles, and construction reinforcement applications.

- SABIC: SABIC offers polypropylene resins tailored for fiber production, including applications in hygiene products, textiles, and industrial fabrics, with a focus on durability and process efficiency.

- Reliance Industries Limited: Reliance is a leading producer of polypropylene in Asia, supplying raw materials for fiber manufacturing used in packaging, textiles, and infrastructure applications.

- China Petrochemical Corporation: Sinopec is one of the largest global producers of polypropylene, supporting large-scale fiber production for textiles, construction, and industrial applications.

Other Top Players Are

- Indorama Ventures Public Company Limited

- Beaulieu International Group / Fibres International NV

- Radici Partecipazioni S.p.A.

- International Fibres Group (IFG)

- Sika AG

- BASF SE

- Mitsubishi Chemical Group

- DuPont de Nemours, Inc.

- Sinopec (China Petrochemical Corporation)

- Braskem S.A.

- Lotte Chemical Corporation

- Freudenberg Group

- ABC Polymer Industries LLC

- Fiberpartner Aps

- Belgian Fibers Group NV

- Chemosvit Fibrochem, s.r.o.

- Zenith Fibres Ltd.

- The Euclid Chemical Company

- Kolon Fiber Inc.

- Thrace Group

- Tri Ocean Textile Co. Ltd.

- W. Barnet GmbH & Co. KG

- INEOS Group Holdings S.A.

- Borealis AG

- Formosa Plastics Corporation

- TotalEnergies

Segments Covered:

By Product Type

- Staple Fiber

- Solid Staple Fiber

- Hollow Staple Fiber

- Filament Fiber

- Monofilament

- Multifilament

- Split Film Fiber

- Continuous Filament Yarn (CFY)

- Fully Drawn Yarn (FDY)

- Partially Oriented Yarn (POY)

By Process

- Melt Spinning

- Solution Spinning

- Dry Spinning

By Application

- Geotextiles

- Woven Geotextiles

- Nonwoven Geotextiles

- Hygiene Products

- Diapers

- Sanitary Products

- Carpets & Rugs

- Industrial Fabrics

- Filter Fabrics

- Protective Fabrics

- Concrete Reinforcement

- Packaging

- Woven Sacks

- Bulk Bags (FIBC)

By End-Use Industry

- Construction

- Automotive

- Textile Industry

- Packaging Industry

- Healthcare & Hygiene

By Form

- Yarn

- Nonwoven

- Woven

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (3)