Content

Resins and Polymers Market Trends, Growth and Market Size Analysis

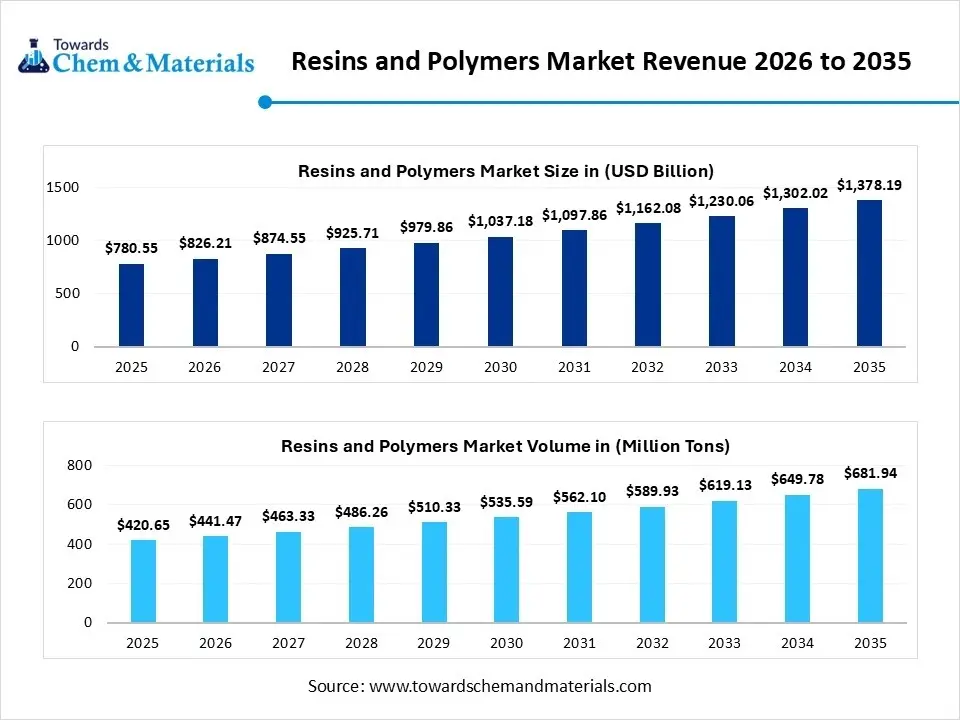

The global Resins and Polymers market size was estimated at USD 780.55 billion in 2025 and is expected to be worth around USD 1378.19 billion by 2035, growing at a CAGR of 5.85% from 2026 to 2035. In terms of volume, the Resins and Polymers market is projected to grow from 420.65 million tons in 2025 to 681.94 million tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035. The evolution of the market is propelled by the demand for application-specific solutions, renewable carbon sources, smart formulation, and high-performance specialty materials, thereby contributing to the overall growth.

Market Highlights

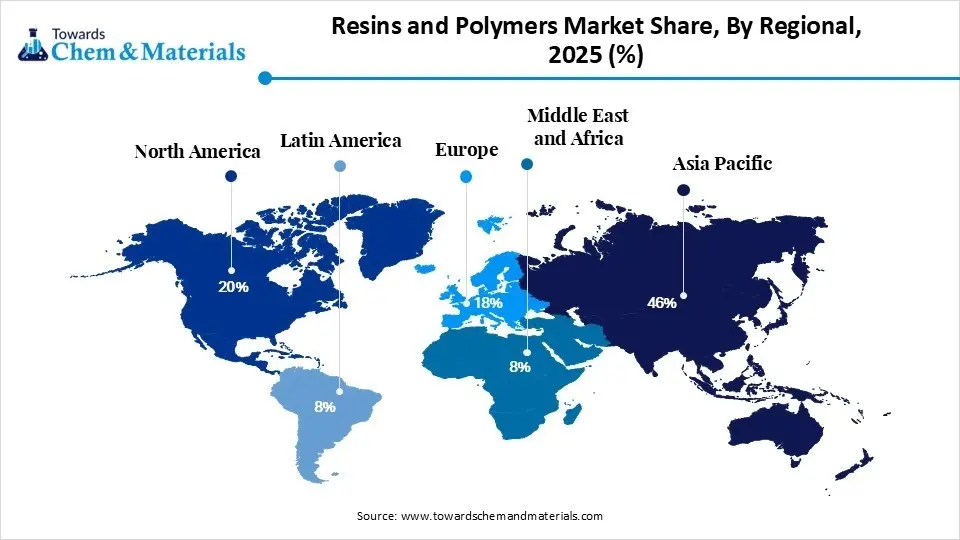

- By region, Asia Pacific dominated the resins and polymers market by holding a 46% share in 2025 and is expected to grow at the fastest with a CAGR of 6.4% during the forecast period.

- By region, North America held the 20% market share in 2025 and expects notable growth in the market with 5.10% CAGR during the forecast period.

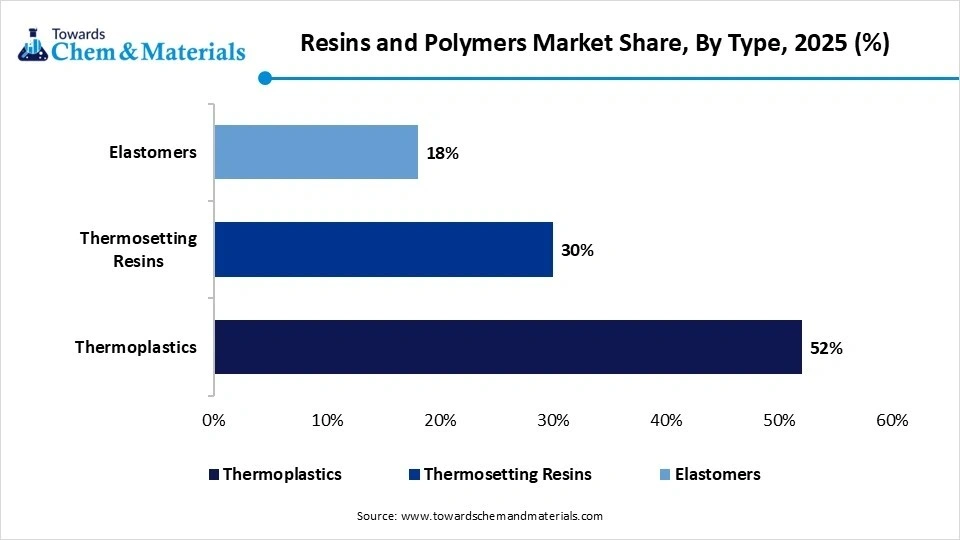

- By type, the thermoplastics segment dominated the market with the largest share of 52% in 2025

- By type, the thermosetting resins segment held 30% market share in 2025 and is expected to grow at the fastest CAGR of 5.9% over the forecast period.

- By source, the petrochemical-based segment dominated the market with the largest share of 82% in 2025

- By source, the bio-based segment held 18% market share in 2025 and is expected to grow at the fastest CAGR of 8.7% over the forecast period.

- By form, the solid segment dominated the market with the largest share of 58% in 2025

- By form, the liquid segment held 27% market share in 2025 and is expected to grow at the fastest CAGR of 6.1% over the forecast period.

- By application, the packaging segment dominated the market with the largest share of 34% in 2025

- By application, the automotive segment held 16% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period.

Market Size and Volume Forecast

- Market Size (2025): USD 780.55 Billion

- CAGR (2025–2035): 5.85%

- Market Projected Size (2035): USD 1378.19 Billion

- Market Volume (2025): 420.65 Million Tons

- Volume CAGR (2025–2035): 4.95%

- Market Projected Volume (2035): 681.94 Million Tons

- Pricing Data (2025):

- Average Manufacturing Price: USD 1,160/ton

- Average Selling Price: USD 1,490/ton

- Pricing CAGR (2025–2035): 3.25%

Market Overview

The resins and polymers market is defined as a key material for molecular science innovation and lifecycle responsibility, as the industrial shift towards de-petrolization of feedstocks and high-performance specialty grades fuels the demand for resins and polymers. The manufacturers focus on decarbonization in the supply chain and integration of bio-based feedstock to remove reliance on fossil fuels in production lines.

The resins and polymers are essential for advancing automotive, aerospace, construction, packaging, and modern telecommunications infrastructure. Additionally, the increasing demand for functional and customized coatings and smart polymers with circular chemical system driving the market expansion.

Recent Market Trends

- Urban Expansion and Industrialization: the rapidly growing population density and the expansion facilitate the development of resins and polymers for consumption infrastructure in packaged food, construction materials, and consumer goods.

- Demand in Automotive and E-Commerce: the shift towards EV and lightweight material drives demand for polymers to enhance battery range and fuel efficiency. While the surge in online shopping for flexible and rigid packaging utilizes polyethylene and polypropylene.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 826.21 Billion / 441.47 Million Tons |

| Expected Size and Volume by 2035 | USD 1378.19 Billion / 681.94 Million Tons |

| Growth Rate from 2026 to 2035 | CAGR 5.85% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia-Pacific |

| Segment Covered | By Type, By Source, By Form, By Application, By Regions |

| Key companies profiled | Eastman Chemical Company, Chevron Phillips Chemical, LyondellBasell, Avient Corporation, Braskem SA, DuPont de Nemours, Inc, Celanese Corporation, Arkema SA, Toray Industries Inc, Huntsman Corporation, Evonik Industries AG, Covestro AG, BASF SE, SABIC, Mitsubishi Chemical Group, LG Chem Ltd, Tejin Limited, Syensqo, Wacker Chemie AG, Formosa Plastics Corporation |

Key Technological Shifts and AI in the Resins and Polymers Market

The technological integration in resin and polymer manufacturing is transforming the industry from trial-and-error to predictive molecular design. The integration of AI-based autonomous laboratories and digital technology maximizes energy efficiency and yields stability.

Machine learning is accelerating the discovery of new resins and polymer formulations through specialized polymer combinations. The implementation of cognitive supply chain enhances the feedstock price volatility and real-time monitoring to achieve operational resilience and technical precision.

Supply Chain Analysis of the Resins and Polymers Market

- Feedstock and Monomer Synthesis: The stage of extraction of raw hydrocarbon and bio-feedstock through cracking and fractionation. The stage focuses on biomass conversion into high-purity chemical gases and monomers.

- Key Players: SABIC, Reliance Industries, Braskem, Shell Chemical, and ExxonMobil Chemical

- Polymerization and Resin Formation: The stage of liquid/gas monomer transforms into a polymer chain in the form of liquid, powders, and pellets through polymerization, catalysis, and compounding, where raw resin is melted and mixed with masterbatches.

- Key Players: Dow Inc., BASF SE, LyondellBasell, Arkema, Covestro, and Aditya Birla Chemicals

- Conversion and End-Use Integration: The industrial processors purchase midstream resins to finished components for automotive, construction, medical, and packaging sectors. The stage uses injection molding, extrusion, and thermoplastic processing.

- Key Players:Berry Global, Solvay, Magna International, and Huntsman

Regulatory Framework: Resins and Polymers Market

| Region | Key Regulation | Regulatory Focus |

| Global | UN Global Plastics Treaty | The global efforts for the limitation of the volume of virgin resin manufacturing and phase out of hazardous polymers. |

| European Union | PPWR and ESPR | Mandatory recycled content of resins and digital product passports to track resin additives across the value chain. |

| United States | State level- EPR Laws and TSCA | Focus on the resin manufacturer's responsibility and post-consumer resins in the new product |

| China | GB Standards for green plastic Initiative | Standard for bio-transition and pushing manufacturers towards PLA and PBAT polymers, and limits for single-use non-degradable resins. |

| India | Plastic Waste Management Rules | Producers' certification for PE films and quality testing for mechanical recycling. |

Resins and Polymers Market Dynamics

Driver

Rising Focus on Water-Based Systems

The resins and polymer market expansion is driven by the rising manufacturer focus on water-borne resins to comply with low-VOC mandates and circular economy goals. This trend is reshaping innovation and substantial investment in chemical and mechanical recycling for post-consumer resin content.

Restraints

Raw Material Instability and Infrastructure Gaps

The reliance on crude oil and natural gas enables high manufacturing costs and domestic volatility in energy prices. In emerging nations, the implementation of recycling infrastructure for polymers remains inadequate due to aging infrastructure and a regulatory framework.

Opportunity

Demand for Biodegradable Resins and Specialty Polymers

The rising environmental awareness creates massive opportunities in the market by boosting the research focus on renewable resource-driven resins and high-performance specialty polymers in electronics and aerospace, which offer superior thermal resilience and chemical resistance

Segmental Insights

Type Insights

The Thermoplastics Segment Dominated the Resins and Polymers Market with 52% of Market Share in 2025

The thermoplastics segment dominated the market with the largest share of 52% in 2025, driven by its thermal plasticity and reversible phase transition. The thermoplastics like PE, PVC, PP, PS, and engineering plastics are key catalysts for the advancement of a closed-loop economy in engineering-grade applications. The rising focus on sustainable manufacturing and post-consumer recovery in high-speed production is fueling the market growth.

Thermoplastics show the ability to melt and reform through mechanical recycling and dynamic processing.

The thermosetting resins segment held the 30% market share in 2025 and is expected to grow at the fastest CAGR of 5.9% over the forecast period. The type offers superior molecular cross-linking and thermal fatigue resistance in high-durability composites. The thermosetting resins include epoxy, phenolic, polyester, and polyurethane, which maintain higher bonding properties and creep resistance, making them key in adhesives, electronic circuitry, and protective laminates

")

The elastomers segment held the 18% market share in 2025, driven by its superior failure strain and superior viscoelastic recovery. The elastomers, such as synthetic rubber and thermoplastic elastomers, set the standard for energy dissipation and resilient interfaces in high-pressure and airtight sealings. The shift towards specialty synthetic grades is driving the adoption of elastomers.

Source Insights

The petrochemical-Based Segment Dominated the Resins and Polymers Market with 82% of Market Share in 2025

The petrochemical-based segment dominated the market with the largest share of 82% in 2025 due to its superior molecular stability and structural stability that supply crucial hydrocarbons for the cost-effective manufacturing of high-grade resin. The petrochemical-based feedstock is a key source involve extraction and cracking of crude oil and natural gas for the most demanding industrial and technical applications.

The bio-based segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 8.7% over the forecast period. The segment is a driver of renewable carbon cycles that utilize plant and organic matter as sustainable feedstock to meet reduced greenhouse gas emission standards. The bio-based source involves PLA, PHA, Bio-PE, and Bio-PET, which offer thermal resistance and functional durability. The shift towards circular sources to create high-performance polymers through established recycling streams is driving the growth.

Form Insights

The Solid Segment Dominated the Resins and Polymers Market with 58% of Market Share in 2025

The solid segment dominated the market with the largest share of 58% in 2025. It is key for efficient transportation and long-term storage stability because of its particle size distribution and bulk density. The solid form involves granules, pellets, and beads that offer handling precision in automated manufacturing practices. The solid-state polymers set a standard for high-purity industrial applications and shipping.

The liquid segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 6.1% over the forecast period, due to its higher flow dynamics in high-performance surface engineering. The liquid polymers are key to uniform thin-film protection. The rising focus on viscosity control and molecular wetting of the liquid form is essential for developing advanced laminates, structural adhesives, and encapsulants through integration of spraying and dipping processes.

The powder segment held the 15% market share in 2025, because powder form offers thermal fusion and superior flowability in dry and surface engineering. The segment is defined as a high-efficiency substrate that is utilized in durable finishes on intricate industrial hardware. The innovation focuses on micrometric reliability to achieve structural stability in selective laser sintering and the development of an advanced powder coating system, accelerating the market growth.

Application Insights

The Packaging Segment Dominated the Resins and Polymers Market with 34% of Market Share in 2025

The packaging segment dominated the market with the largest share of 34% in 2025. The resins and polymers offer product preservation and mass-market scalability in flexible and rigid packaging. The resin is essential for barrier technologies. As the packaging sector transitions towards light-weighting and the advancement of mono-material structures and recycling. By integrating smart resin additives and functionalized polymers, fueling the high-speed manufacturing and environmental reliability.

The construction segment held the 22% market share in 2025, serving as a key for infrastructure resilience where resins and polymers offer protection against structural fatigue and degradation. The construction sector focuses on superior durability binders and polymeric membranes that offer superior waterproofing and thermal insulation. The surge of integration of fiber-reinforced composites and advanced sealants for building envelopes and green construction is driving the expansion.

The automotive segment held the 16% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period, driven by rising demand for structural polymer composites, high-performance aesthetic resin, and noise-dampening elastomers in vehicle engineering. The automotive industry is a key driver for metal-to-plastic conversion that focuses on enhancing battery efficiency, passenger safety, and lowering carbon footprint in modern fleets and mobility platforms.

The electrical & electronics segment held the 12% market share in 2025. It is key for high-frequency material engineering where polymers offer dielectric precision, and resins offer low-loss tangent, crucial for high-speed data processing and telecommunications. The electrical & electronics sector focuses on thermal-gradient management and mechanical reliability, that boosting the adoption of resin and polymers in electronics infrastructure.

Regional Insights

How Did the Asia Pacific Dominated the Resins and Polymers Market in 2025?

Asia Pacific dominated the market by holding 46% share in 2025 and is expected to grow at the fastest with a CAGR of 6.4% during the forecast period, serving as a key hub for resin synthesis and a large-scale polymer conversion hub. The regional researchers focus on sustainability, and domestic players focus on scaling of chemical recycling and bio-based alternatives in industrial production. Asia Pacific is maintaining its leadership in 5G infrastructure and material self-sufficiency by maintaining export standards and domestic environmental compliance.

China Resins and Polymers Market Growth Trends

China maintains its leadership in the Asia Pacific market by setting standards for resin and polymer exporting and manufacturing. The region shifts towards specialty material self-sufficiency and its capacity expansion in ethylene and propylene. Tehe, domestic manufacturing drives the innovation in green energy and advanced electronics.

")

North America Resins and Polymers Market Growth Trends

North America held the 20% market share in 2025 and is expected to experience notable growth in the market with a 5.10% CAGR during the forecast period. It is a key region for its massive shale-gas infrastructure and feedstock-based manufacturing of resin and polymer. North America's technological innovation and its shift towards sustainability in medical-grade polymers and the aerospace sector are boosting domestic growth. The major players are investing in advanced molecular recycling to meet decarbonize supply chain.

U.S. Resins and Polymers Market Growth Trends

The United States market is experiencing continuous growth by utilizing its domestic natural gas liquids and high-specification material engineering. The regional players focus on the capacity expansion of specialty polymer performance in various applications. Additionally, U.S. reshoring initiatives and their integrated chemical recycling enable the creation of a closed-loop supply chain in resin and polymer production.

Recent Developments

- In April 2026, Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical received Japan Fair Trade Commission clearance to integrate Sumitomo's polypropylene and linear low-density polyethylene businesses into Prime Polymer. These initiatives focus on strengthening supply competitiveness in Japan for the high-performance polyolefin business.(Source: jp.mitsuichemicals.com)

- In September 2025, SABIC announced a new launch of non-fluorinated SILTEM™ resin blends with improved performance at IWCS 2025. This novel material can replace fluoropolymers in wire & cable applications utilized in the automotive, industrial, and oil & gas sectors by addressing regulatory restrictions on PFAS.(Source: www.sabic.com )

- In January 2025, Bjørn Thorsen A/S was appointed as the authorised pan-European distributor for Celanese thermoplastic elastomers. The corporation's focus on strengthening the position of Bjorn Thorsen’s product offering across Europe, including Santoprene® TPV, Hytrel® TPC, Bexloy® TPC, Laprene® TPS, and Ateva® GEVA.(Source: www.bjorn-thorsen.com)

Top Companies in the Market

- Eastman Chemical Company

- Chevron Phillips Chemical

- LyondellBasell

- Avient Corporation

- Braskem SA

- DuPont de Nemours, Inc

- Celanese Corporation

- Arkema SA

- Toray Industries Inc

- Huntsman Corporation

- Evonik Industries AG

- Covestro AG

- BASF SE

- SABIC

- Mitsubishi Chemical Group

- LG Chem Ltd

- Teijin Limited

- Syensqo

- Wacker Chemie AG

- Formosa Plastics Corporation

Segment Covered in the Report

By Type

- Thermoplastics

- Polyethylene (PE)

- HDPE

- LDPE

- LLDPE

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Engineering Plastics

- Polycarbonate (PC)

- Polyamide (PA)

- ABS

- Polyethylene (PE)

- Thermosetting Resins

- Epoxy Resins

- Phenolic Resins

- Polyester Resins

- Unsaturated Polyester Resin (UPR)

- Akyd Resins

- Polyurethane (PU)

- Elastomers

- Synthetic Rubber

- SBR

- NBR

- EPDM

- Thermoplastic Elastomers (TPE)

- Synthetic Rubber

By Source

- Petrochemical-based

- Bio-Based

- PLA

- PHA

- Bio-PE

- Bio-PET

By Form

- Solid

- Liquid

- Powder

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Construction

- Pipes & Fittings

- Insulation Materials

- Coatings & Adhesives

- Automotive

- Interior Components

- Exterior Components

- Under-the-hood Applications

- Electrical & Electronics

- Insulation Materials

- Components & Housings

- Consumer Goods

- Household Products

- Appliances

- Industrial

- Machinery Components

- Industrial Coatings

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (3)