Content

What is the current 3D Printing Plastics Market Size and Share?

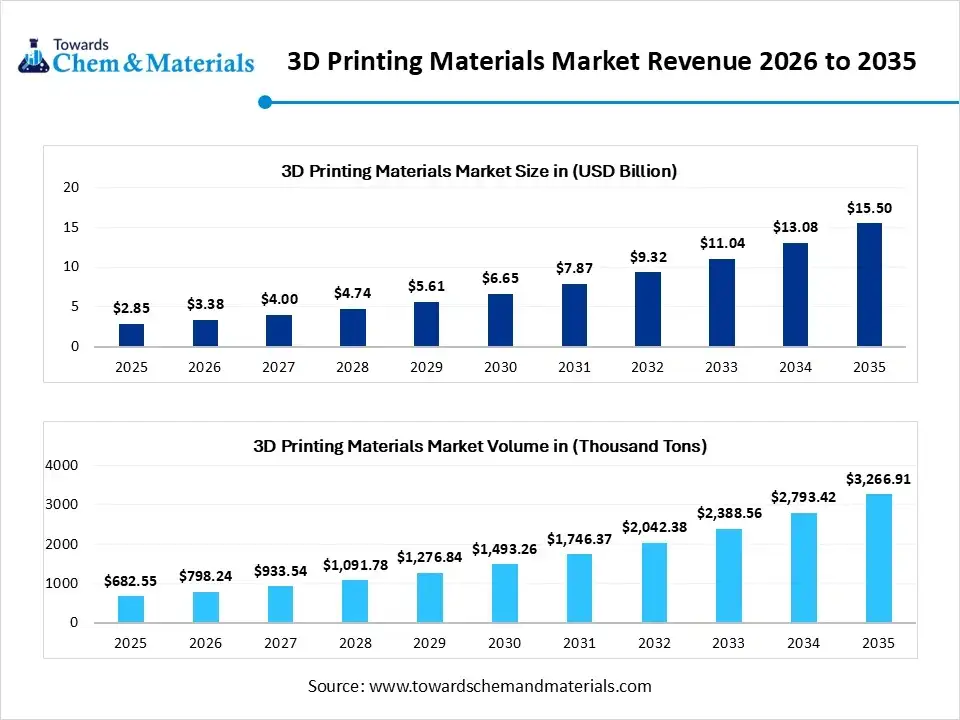

The global 3D printing plastics market size was valued at USD 2.85 billion in 2025, is estimated to reach USD 3.38 billion in 2026, and is projected to reach USD 15.50 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 18.45% over the forecast period from 2026 to 2035. In terms of volume, the 3D printing plastics market is projected to grow from 682.55 thousand tons in 2025 to 3,266.91 thousand tons by 2035. growing at a CAGR of 16.95% from 2026 to 2035.The market development is fueled by the expanding adoption of additive manufacturing across industrial and consumer goods, demand for rapid prototyping, sustainable circular formulation, and additive-driven smart factories.

Market Highlights

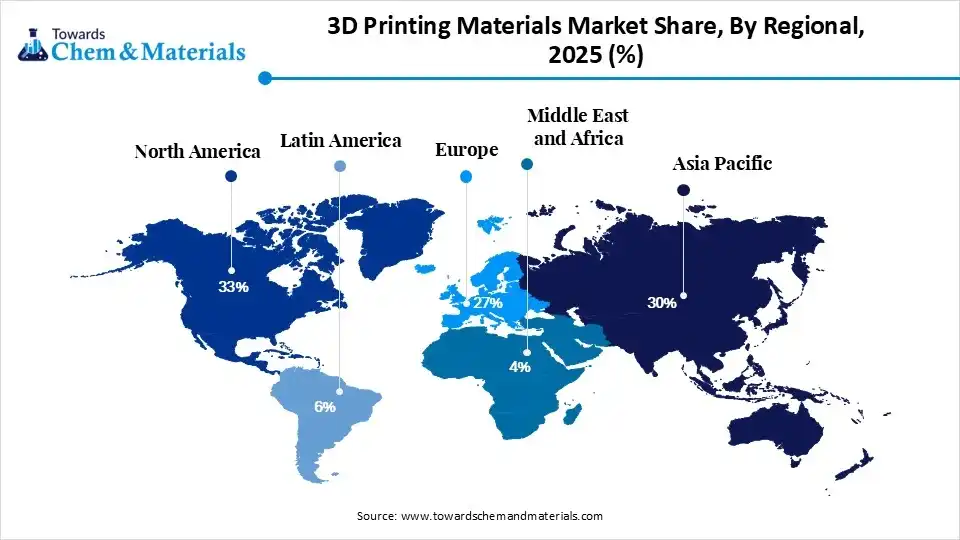

- By region, North America dominated the 3D printing plastics market by holding 33% share in 2025, driven by advanced manufacturing infrastructure and R&D investment in polymer technology.

- By region, Asia Pacific held the 30% market share in 2025 and is expected to grow at the fastest with a CAGR of 20.70% during the forecast period due to additive manufacturing capacity expansion and strong government support.

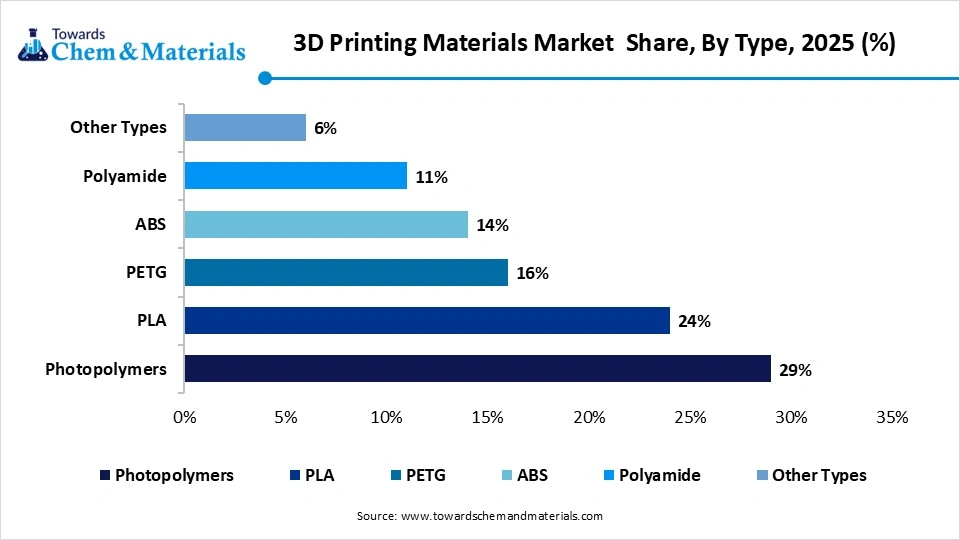

- By type, the photopolymers segment dominated the market with the largest share of 29% in 2025 due to demand for high-resolution industrial printing and SLA and DLP installation.

- By type, the PETG segment held 16% market share in 2025 and is expected to grow at the fastest CAGR of 19.6% over the forecast period, driven by its durability and chemical resistance in functional prototyping applications.

- By form, the filament segment dominated the market with the largest share of 43% in 2025, driven by demand in industrial FDM printers and cost-effectiveness.

- By form, the liquid segment held 26% market share in 2025 and is expected to grow at the fastest CAGR of 19.2% over the forecast period due to high-precision printing requirements in resin-based printers and the medical sector.

- By application, the manufacturing segment dominated the market with the largest share of 42% in 2025 and is expected to grow at the fastest CAGR of 20.10% over the forecast period, driven by industrial scalability in 3D printed components for lightweight and customization.

- By end-use industry, the automotive segment dominated the market with the largest share of 27% in 2025, driven by rapid prototyping and cost-efficient tooling for lightweight automotive components.

- By end-use industry, the healthcare segment held 21% market share in 2025 and is expected to grow at the fastest CAGR of 21.40% over the forecast period due to surgical planning models and demand for 3D printing plastics in personalized medical devices.

Market Overview

The global 3D printing plastics market is revolutionizing towards high-volume additive manufacturing. The advanced 3D printed engineered plastic offers higher mechanical strength, superior chemical resistance, and thermal stability. The demand for specialized polymers in the aerospace, healthcare, and automotive sector transforming the rapid prototyping into high-performance engineered grade. The shift towards sustainability and the circular economy targets driving the innovation of bio-based plastics and biodegradable filaments.

The industrial manufacturer implements several material forms like photopolymer resin, thermoplastic filaments, and laser-sintered powders to ensure optimized operation efficiency in high-volume production lines. The emerging trend towards recycled polymers allows manufacturers to lower their carbon footprint by providing structural integrity to the final product. The medical sector demands biocompatible plastics for customized prosthetics, dental implants, and surgical guides to meet patients' health and safety. The implementation of on-demand manufacturing enables industrial layers for supply chain resilience.

The industrial users fuel the shift towards fused deposition modeling, selective laser sintering, and stereolithography by integrating high performance material like ULTEM, PEEK, and carbon-fiber reinforced polymers, offering high efficiency, improved fuel efficacy, and higher precision. Additionally, the integration of smart 4D printing plastics and artificial intelligence is driving the 3D printing plastics as a key for next-generation digital manufacturing and smart industrial production.

Recent Market Trends

- Demand for Mass Customization: The 3D printing plastics allows manufacturers for economic viability in medical orthotics, custom dental alignments, and high-end personalized products.

- Focus on Sustainable Plastics in End-Use Industry: The 3D printing plastic components boosts the advancement of engineering-grade polymers by integrating with additive manufacturing. Industry shift toward bio-based polymers and recyclable filaments to minimize environmental impact.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 3.38 Billion/ 798.24 Thousand Tons |

| Revenue Forecast in 2035 | USD 15.50 Billion/ 3,266.91 Thousand Tons |

| Growth Rate | CAGR 18.45% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segment Covered | By Type, By Form, By Application, By End-Use Industry, By Regions |

| Key companies profiled | 3D Systems Corporation, Arkema Inc., Envisiontec Inc., Stratasys Ltd., SABIC, Evonik Industries AG, Formlabs, Solvay S.A., Huntsman Corporation, Henkel AG & Co. KGaA, Materials NV, HP INC., Eos GmbH Electro Optical Systems, PolyOne Corporation, Royal DSM N.V. |

Key Technological Shifts and AI in the 3D Printing Plastics Market

Technological integration is driving advancement in material science and closed-loop manufacturing of 3D printing plastics. Artificial Intelligence is redefining digital design by converting the value chain through AI-integrated digital threads. The generative design creates complex 3D structures to improve battery range and structural uniformity. The expansion of smart (4D) plastics drives the demand for high-performance polymers & shape memory polymers (SMPs) in modern manufacturing.

Technological advancement supports quality control, labor operations, and topology optimization. Automation in metal powder handling offers chemical purity, with direct energy deposition (DED). The integration of CNC for precision finishing. Additionally, digital warehousing and distributed manufacturing foster supply chain resilience and a lower carbon footprint by optimizing operational costs.

Supply Chain Analysis of the 3D Printing Plastics Market

- Chemical Synthesis and Resin Processing: the stage of extraction, advanced chemical synthesis, and processing techniques are used to produce high-performance 3D printing plastics, including base polymer synthesis, chemical blending, and metal powders. These processes ensure thermal stability, durability, and functionality of raw resin for additive manufacturing systems.

- Key Players: BASF, Solvay S.A., Arkema, Covestro AG, Evonik Industries AG and SABIC

- Form Conversion and Quality Testing: The raw materials convert into highly calibrated filaments, light-reactive liquid photopolymers, and SLS/HSS powder through extrusion and atomization. Strict quality-control packaging and certification standards ensure materials meet industrial requirements for reliability in additive manufacturing applications.

- Key Players: Stratasys Ltd., 3D Systems, Inc., Materialise NV, Formlabs Inc., and Polymaker

- Distribution and Industrial Fabrication: The final stage of Efficient distribution channels delivers 3D printing plastics to industrial manufacturers, prototyping labs, and research institutions. The end-user utilized 3D printers and processes like software optimization, thermal post-curing as a functional prototype for the commercial and industrial sector.

- Key Players: 3D Systems, Boeing Company, Stryker Corporation, Align Technology, Inc., BMW Group, and Proto Labs.

Regulatory Framework: 3D Printing Plastics Market

| Region | Key Regulations | Regulatory Focus |

| Global | ISO (International Organization for Standardization)/ASTM Joint Technical Committee | Standards for additive manufacturing practices for quality and plastic transformation in material extrusion. Anisotropy testing to measure structural variation. |

| European Union | EU REACH & CLP regulation, EU Medical Device regulation | Focus on the biocompatibility of resins and filaments to prevent microplastic leakage. Restrict toxic photopolymers to meet safety and health institution grants for in-house plastic printing. |

| Asia Pacific | TGA (for patient-matched plastic implants), China NMPA, India CDSCO Medical Device Rules | Focus on Material Master Files for 3D polymers, product-specific registrations, and reducing plastic waste & emissions. The localized materials standardization and approvals for domestic bio-compatible and high-performance polymer advancement |

| North America | OSHA Hazard Communication standard, FDA CDRH Guidance, and QMSR standards | Focus on sterilization validation and finished device safety. Process verification to design of experiment for printing process. With updated safety data sheets (SDS) and GHS labels with global medical compliance. |

3D Printing Plastics Market Dynamics

Driver

Advancement in Photopolymers and Pellet Extrusion

The key driver that is shaping the market is that liquid photopolymers are utilized as 3D-printed resin, like stereolithography and digital light processing, through a revolution towards dual-cure chemistry and elastomeric polyurethane integration. The next generation polymers offer excellent ultra-high surface finish & dimensional precision. The rapid commercialization of the pellet-based extrusion system allows manufacturers to print large-scale plastic components in automotive, maritime, and architectural applications by driving long-term reliability of additive manufacturing by maintaining higher deposition rates.

Restraints

High Processing Costs and Safety Regulations

The market expansion is restrained by the high specialized 3D printing plastics and operational costs for metal powder, filament, and liquid photopolymer. The stringent environmental regulations with complex certifications and workplace safety requirements for high-performance engineering plastics and operational complexity limit the market adoption.

Opportunity

Factory Tooling Optimization and Emerging Ecosystem

The key opportunity for 3D printing plastics enables the fabrication of customized manufacturing in fixtures, molding inserts, and jigs. The industrial facilities focus on lightweight tooling to optimize assembly precision and lower tool lead times through return on investment for manufacturing practices. The developing economy enhance the geographical opportunity for the 3D printing plastics industry by a well-established local distribution network & additive-driven smart factories. Additionally, the major region demands low-cost and bulk polymer alternatives in decentralized consumer and industrial product manufacturing.

Segmental Insights

Type Insights

The photopolymers segment dominated the market with the largest share of 29% in 2025. It is a liquid-based type that depends on UV-curable resins and monomers, where photopolymers offer higher micron-level accuracy and superior smooth surface finishes. The segment allow shift towards vat photopolymerization technology, like stereolithography and digital light processing. The innovation focuses on high-performance engineering-grade plastics by ensuring elastomeric resilience, biocompatibility, and superior thermal resistance essential for intricate prototyping, dental, medical, and customized infrastructure.

")

The PETG segment held the 16% market share in 2025 and is expected to grow at the fastest CAGR of 19.6% over the forecast period, driven by its ease of consumption and structural durability as a key copolymer filament. PETG is categorized as transparent and reinforced PETG, which makes them key for functional mechanical components, protective equipment, and chemical-resistance enclosure The glycol is combined into the molecular chain by offering higher interlayer adhesion, low thermal shrinkage, superior shatter resistance, and impact strength.

The PLA segment held the 24% market share in 2025, serving as renewable biopolymers derived from cornstarch, where PLA offer low thermal expansion coefficient. The precise layer deposition enables the fabrication of a high-resolution structure by maintaining superior melt viscosity. The segment characterized by high flexural modulus and susceptibility to thermal deformation makes PLA key for rapid conceptualization, anatomical visualization, and architectural models.

3D Printing Materials Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Photopolymers | 29% |

| PLA | 24% |

| PETG | 16% |

| ABS | 14% |

| Polyamide | 11% |

| Other Types | 6% |

The ABS segment held 14% market share in 2025. It is high-performance thermoplastics that offer superior structural integrity, impact resistance, and higher mechanical resilience that combine the rigidity of acrylonitrile and styrene. ABS is preferred in post-processing treatment, functional prototypes, and consumer electronics. The ABS ensures a superior heat deflection temperature that allows printed components to withstand structural deformation.

Form Insights

The filament segment dominated the market with the largest share of 43% in 2025, serving as a key form for extrusion technologies. The fused filament fabrication ecosystem maintains stable volumetric flow into domestic thermal liquefiers for accurate micro-extrusion. Filament offers superior atmospheric stability and eliminates VOC and dust exposure. The rising materials innovation focuses on anisotropic structural matrices and polymer compounding by combining carbon fibers and glass microspheres.

The powder segment held the 31% market share in 2025, driven by the utilization of selective laser sintering systems and multi-jet fusion crucial for heavy industrial manufacturing. This form optimized powder bed fusion by offering self-supporting, superior isotropic mechanical strength. The rising shift towards precise thermal consolidation and powder recyclability lowers material waste for end-use components and three-dimensional part nesting.

The liquid segment held the 26% market share in 2025 and is expected to grow at the fastest CAGR of 19.2% over the forecast period due to free-radical polymerization. The low-viscosity reactive monomer cross-links liquid into thermoset matrices. The liquids offer high sub-micron feature resolution and a smooth isotropic surface. The advancement in biocompatible liquid resins and high-temperature formulation makes liquid key for investment casting, surgical guides, and dental prosthesis.

3D Printing Materials Market Share, By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Powder | 31% |

| Liquid | 26% |

| Filament | 43% |

Application Insights

The manufacturing segment dominated the market with the largest share of 42% in 2025 and is expected to grow at the fastest CAGR of 20.10% over the forecast period. The 3D printing plastics demand is driven by high-volume consumption of the industrial sector that utilizes high-performance polymers for end-use components, and the manufacturing sector focuses on on-demand digital inventory to avoid higher operational costs and supply chain volatility. The factor engineering adopts advanced carbon-reinforced matrices for robotic end-effectors, specialized ergonomic assembly fixture ad work holding blocks, as the manufacturer of focus on optimized assembly, shortens operational cost make 3D printing a key for factory-floor structural durability.

The prototyping segment held the 38% market share in 2025 due to the utilization of versatile thermoplastics and photopolymers for design verification and fit-form-function testing. The prototyping accelerates the product development lifecycle and lowers processing time for precision evolution of mechanical tolerance and production assembly. Additionally, the segment key for geometric engineering flaws by minimizing capital expenditure risks.

The tooling segment held the 20% market share in 2025, represent ad key for designing and mass production by deploying heat-resistant thermosets and carbon-reinforced composites. The tooling eliminates complex CNF machining setups and ensures the fabrication of injection molding inserts. The printed tooling optimizes thermal dissipation for cost-effective, low-volume production runs.

3D Printing Materials Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Manufacturing | 42% |

| Prototyping | 38% |

| Tooling | 20% |

End-Use Industry Insights

The automotive segment dominated the market with the largest share of 27% in 2025, driven by high-performance engineering demand by advancing carbon-fiber composites and polyamides for lightweight and fuel efficiency. In a vehicle assembly line, automaker customized ergonomic assembly fixtures in prototyping components and end-of-line vehicle components. The rising focus on-demand spare parts logistics is driving OEM deployment of additive manufacturing.

The healthcare segment held the 21% market share in 2025 and is expected to grow at the fastest CAGR of 21.40% over the forecast period, represent as key patient-specific healthcare solution where biocompatible thermoplastics and specialized photopolymers are utilized in dental, prosthetics & implants, and surgical models. The healthcare focuses on precise anatomical visualization models and mass manufacturing of customized dental orthodontics by integrating sterilizable engineering plastics to meet patient health standards.

The aerospace & defense segment held the 23% market share in 2025 due to the adoption of high-temperature super-polymers and PEEK in aircraft components and defense equipment parts. The cabin lightweighting action plans enable the advancement of specialized interior thermoplastic for flight-certified end-use parts to meet stringent flame, smoke, and toxicity standards. The aviation sector enables demand for environmental control ducting and protection, driving the adoption of 3D printing plastics.

The consumer goods segment held 17% market share in 2025. The rising commercialization of thermoplastics and photopolymers is driving the transition towards mass customization of functional electronics and lifestyle products. The integration of flexible elastomeric resins and copolymer filaments ensures real-time testing and cost-effectiveness. The consumer preferred on-demand manufacturing, which eliminates costly injection molding tooling.

3D Printing Materials Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Aerospace & Defense | 23% |

| Automotive | 27% |

| Healthcare | 21% |

| Consumer Goods | 17% |

| Other End-use Industries | 12% |

Regional Analysis

How Did the North America Dominated the 3D Printing Plastics Market in 2025?

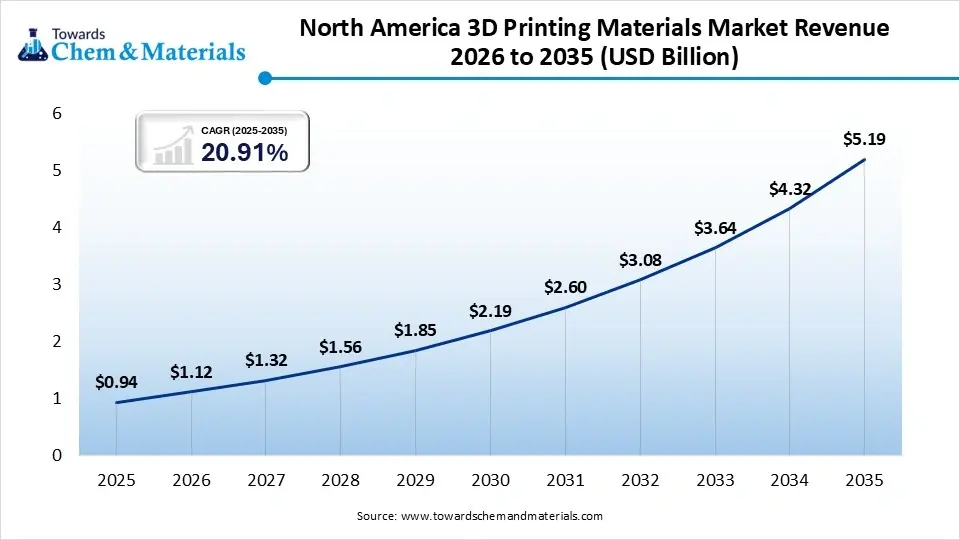

The North America 3d printing plastics market size was estimated at USD 0.94 billion in 2025 and is projected to reach USD 5.19 billion by 2035, growing at a CAGR of 20.91% from 2026 to 2035.North America dominated the market by holding 33% share in 2025, the growth is accelerated by industrial scaling and technological advancement. The regional FDA regulatory framework and sustainability mandates drive the shift towards a circular economy through the utilization of bio-based plastics and recycled filaments in industrial applications. North America players' demand for PEEK, carbon-fiber composites, and ULTEM through automated selective laser sintering and fused deposition modeling by maintaining the supply chain nearshoring.

United States

- Driven by national funding for industrial automation and venture-capital environmental for novel plastics to meet stringent FAA certifications.

- U.S. adopts carbon-fiber reinforced PEEK, biocompatible photopolymers, and ULTEM in high-value aerospace, military drone, customized orthopedic, and injection mold tooling.

Canada

- Growth is fueled by government-driven advanced manufacturing practices and emphasis on 3D printing plastics through R&D investments.

- The flame-retardant polycarbonates, bio-based PHA formulation, and PA11 &PA12 are utilized for EV lightweight components, research equipment housings, and custom dental prosthetics.

The Asia-Pacific 3d printing plastics market size was estimated at USD 0.86 billion in 2025 and is projected to reach USD 4.73 billion by 2035, growing at a CAGR of 18.59% from 2026 to 2035.Asia Pacific held the 30% market share in 2025 and is expected to grow at the fastest with a CAGR of 20.70% during the forecast period. The region is shifting towards digital manufacturing align with state-supported Industry 4.0 initiatives. The region utilized engineered-grade filaments and laser-sintered powders in the automotive supply chain, consumer electronics ad hyper-automation robotics applications. Additionally emerging trend towards biocompatible photopolymers for mass production of medical devices by maintaining a cost-competitive supply of raw materials.

China

- Driven by digital factory mandates and low-cost consumer hardware export in chemical infrastructure. China is a mass producer of PLA filaments, polyamide powders, and high-volume liquid photopolymers

- The region's large-scale demand in architectural prototyping, consumer electronics, and automotive interior components is driving the growth.

India

- The growth is driven by expanding domestic defense programs and the adoption of digitalization in engineering infrastructure.

- India's demand for PETG, standard ABS, and engineering-grade nylon blends used in localized commercial satellite components, automotive engine-bay prototypes, and customized products

The Europe 3d printing plastics market size was estimated at USD 0.77 billion in 2025 and is projected to reach USD 4.26 billion by 2035, growing at a CAGR of 20.93% from 2026 to 2035.Europe held the 27% market share in 2025, serving as a key region in advanced automotive engineering and stringent EU green mandates. Europe focuses on sustainability innovation to advanced bio-based plastics, biodegradable resins, and circular economy recycled filaments. The region is increasingly adopting selective laser sintering, ultra-high-performance PEEK, and PA12. Additionally, the domestic players advanced in aerodynamics testing by integrating 3D printing plastics to meet environmental compliance.

Germany

- Key hub for high-performance industrial engineering and stringent EU circular economy directives, integrating Industry 4.0

- Germany's demand for bio-based industrial plastics, fine-grain polyamide 12 for selective laser sintering, and flame-retardant PBT in customized manufacturing automation, automotive components, and safety-driven railway interior components.

United Kingdom

- UK demand for PEEK, ultra-lightweight carbon-fiber reinforced nylon, and engineered filaments used in wind-tunnel testing components, commercial aviation, and custom surgery guides.

- The region is leading in motorsport engineering hubs and medical printing laboratories for national health services.

")

The Latin America 3d printing plastics market size was estimated at USD 0.20 billion in 2025 and is projected to reach USD 1.16 billion by 2035, growing at a CAGR of 19.22% from 2026 to 2035.Latin America held the 6% market share in 2025 due to its high consumption of liquid biocompatible photopolymer resins and domestic manufacturing capacity. The regional manufacturing nearshoring and aerospace infrastructure demand for engineered-grade ABS, TPU, and PETG to print factory assembly jigs and robotic tooling. Latin America focuses on digital transformation and locally sources corn-derived PLA utilized for the domestic industry and agricultural sector.

Brazil

- The domestic growth is driven by domestic commercial aviation infrastructure and digital transformation in the private dental clinic and medical sectors.

- The aerospace-grade flame-retardant polymers, industrial ABS, and biocompatible resins are essential for aircraft cabin, healthcare, and consumer appliance prototypes.

Argentina

- Argentina leads in academically-driven hardware infrastructure an customize agricultural engineering for domestic farming technology.

- The agricultural-grade UV-resistant PETG, standard PLA, and flexible TPU key for advanced laboratory equipment, research models, and custom seed-drilling machinery nozzles

The Middle East & Africa 3d printing plastics market size was estimated at USD 0.11 billion in 2025 and is projected to reach USD 0.70 billion by 2035, growing at a CAGR of 20.33% from 2026 to 2035.The Middle East & Africa held the 4% market share in 2025, driven by advanced manufacturing practices and regulatory-driven industrial diversification. The domestic growth is accelerated by the oil, gas, and petrochemical sector, which enables the demand for PEEK, fluoropolymers, and PEI (ULTEM) to print chemical-inert and high-temperature components. The government funding and GC private healthcare expansion fuel the use of selective laser sintering and nylon powder.

Saudi Arabia

- Driven by their Vision 2030, economic diversification, and a rising shift towards domestic industrial supply chains.

- Saudi Arabia utilized PEI, PEEK, specialty composite, and flame-retardant structural plastics in oil & gas drilling sensors, drone replacement components, and heavy industrial pumps.

UAE

- The domestic expansion is driven by strong government mandates for 3D-printed construction elements and acts as a key hub for the advanced aerospace supply chain.

- The high-performance ULTEM, UV-resistant polycarbonates, and specialty polymers are utilized in luxurious interior architecture, specialized construction alignment tools, and drone infrastructure.

3D Printing Materials Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 33% |

| Europe | 27% |

| Asia-Pacific | 30% |

| Latin America | 6% |

| Middle East & Africa | 4% |

Recent Development

- In April 2026, Poly Precision Technology joined its global ROBOZE advanced manufacturing system to accelerate distributed manufacturing in industrial sectors. The global corporation focused on expanding advanced manufacturing capacity across the United States and a distributed production ecosystem through standardized digital workflows.(Source: www.prnewswire.com)

Top Companies in the 3D Printing Plastics Market

- 3D Systems Corporation

- Arkema Inc.

- Envisiontec Inc.

- Stratasys Ltd.

- SABIC

- Evonik Industries AG

- Formlabs

- Solvay S.A.

- Huntsman Corporation

- Henkel AG & Co. KGaA

- Materials NV

- HP INC.

- Eos GmbH Electro Optical Systems

- PolyOne Corporation

- Royal DSM N.V.

Segment Covered in the Report

By Type

- Photopolymers

- Standard Photopolymers

- Engineering Photopolymers

- Dental & Medical Photopolymers

- PLA

- Industrial Grade PLA

- Consumer Grade PLA

- PETG

- Transparent PETG

- Reinforced PETG

- ABS

- Standard ABS

- High-Impact ABS

- Polyamide

- PA11

- PA12

- Glass-Filled Polyamide

- Other Types

- PEEK

- TPU

- Composite Blends

By Form

- Powder

- Nylon Powder

- Metal-Plastic Composite Powder

- Liquid

- UV-Curable Resin

- Flexible Resin

- Filament

- Standard Filament

- Reinforced Filament

- Flexible Filament

By Application

- Manufacturing

- Production Parts

- Functional Components

- Prototyping

- Concept Modeling

- Functional Prototypes

- Tooling

- Jigs & Fixtures

- Mold Tooling

By End-Use Industry

- Aerospace & Defense

- Aircraft Components

- Defense Equipment Parts

- Automotive

- Prototyping Components

- End-Use Vehicle Parts

- Healthcare

- Dental Applications

- Prosthetics & Implants

- Surgical Models

- Consumer Goods

- Electronics Accessories

- Lifestyle Products

- Other End-Use Industries

- Education

- Construction

- Industrial Machinery

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)