Content

Aerospace Materials Market Size, Volume, Share, Growth, Report 2026 to 2035

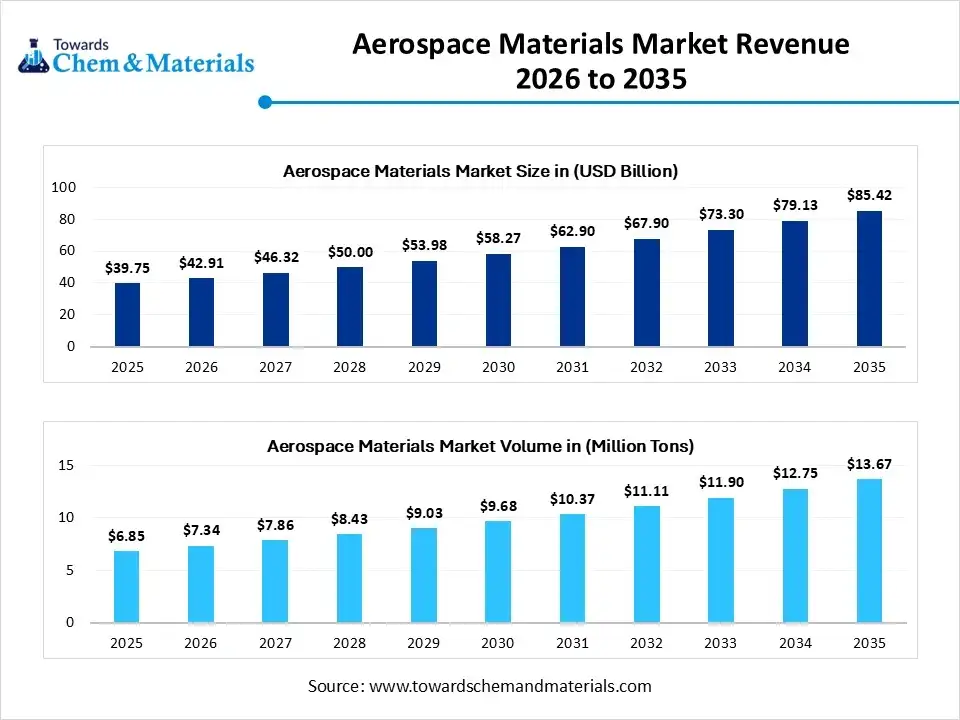

The global aerospace materials market size was estimated at USD 39.75 billion in 2025 and is expected to be worth around USD 85.42 billion by 2035, growing at a CAGR of 7.95% from 2026 to 2035. In terms of volume, the aerospace materials industry is projected to grow from 6.85 million tons in 2025 to 13.67 million tons by 2035, exhibiting a compound annual growth rate (CAGR) of 7.15% over the forecast period from 2026 to 2035. Increasing aircraft deliveries is the key factor in driving market growth. Also, a surge in defense spending, coupled with technological innovations such as 3D printing, can fuel market growth further.

Market Highlights

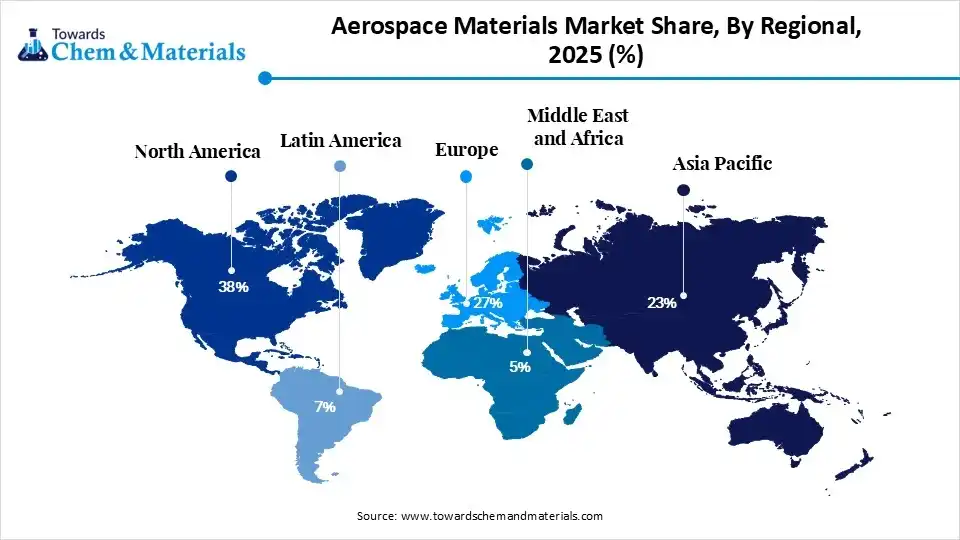

- By region, North America dominated the market with the largest share of 38% in 2025.

By region, Asia Pacific is expected to grow at the fastest CAGR of 9.1% over the forecast period. - By material type, the metals segment dominated the market with the largest share of 48% in 2025.

- By material type, the composites segment is expected to grow at the fastest CAGR of 9.2% over the forecast period.

- By aircraft type, the commercial aircraft segment dominated the market with the largest share of 46% in 2025 and is expected to grow at the fastest CAGR of 8.3% over the forecast period.

- By application, the structural components segment dominated the market with the largest share of 42% in 2025.

- By application, the engine components segment is expected to grow at the fastest CAGR of 8.4% over the forecast period.

- By manufacturing process, the forging segment dominated the market with the largest share of 28% in 2025.

- By manufacturing process, the additive manufacturing segment is expected to grow at the fastest CAGR of 10.1% during the forecast period.

- By end-use, the OEM segment dominated the market with the largest share of 63% in 2025.

- By end-use, the MRO segment is expected to grow at the fastest CAGR of 8.2% during the study period.

- By supplier type, the tier 1 suppliers segment dominated the market with the largest share of 44% in 2025.

- By supplier type, the tier 2 suppliers' segment is expected to grow at the fastest CAGR of 7.9% over the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 39.75 Billion | CAGR (2026–2035): 7.95%

- Market Projected Size (2035): USD 85.42 Billion

- Market Volume (2025): 6.85 Million Tons | Volume CAGR (2026–2035):7.15%

- Market Projected Volume (2035): 13.67 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 5,860 per ton

- Average Selling Price: USD 7,430 per ton

- Pricing CAGR (2025–2035): 3.85%

What are Aerospace Materials Market?

The market encompasses the manufacturing and supply of specialized, high-performance materials like titanium, aluminium, composites, and superalloys created for durable, lightweight structures, engines, and interiors in aircraft and spacecraft. These cutting-edge materials are created to withstand extreme operating conditions while minimizing overall aircraft weight to increase fuel efficiency.

Recent Market Trends

- Increasing demand for lightweight materials is the latest trend in the market, shaping positive market growth. Aircraft market players are rapidly adopting innovative aluminum and composite alloys to achieve weight reduction. This shift is essential for industry expansion.

- Technological innovations in materials science play a key role in the market. Advancements, including nanotechnology and additive manufacturing, are facilitating the development of high-performance materials with better properties. These developments can also enhance the reliability and performance of aerospace components.

- The growing investments in space missions by different space agencies and private market players are presenting new opportunities in the market. Harsh environmental conditions in space need materials with better temperature resistance, superior strength, and low outgassing characteristics.

Report Scope

| Report Attribute | Details |

| Market Size Value in 2026 | USD 42.91 Billion / 7.34 Million Tons |

| Revenue Forecast in 2035 | USD 85.42 Billion/ 13.67 Million Tons |

| Growth Rate | CAGR 7.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segments covered | By Type, By Aircraft Type, By Region |

| Key companies profiled | Avdel , Constellium, Solvay , DOW , Hexcel Corporation, Hindalco - Almex Aerospace Limited , Kaiser Aluminum , KOBE STEEL, LTD , Koninklijke Ten Cate bv. , Lee Aerospace , Materion Corporation , PARK AEROSPACE CORP , Renegade Materials Corporation , SGL Carbon , TATA Advanced Materials Limited , Sofitec Aero, S.L. |

How Cutting-Edge Technologies Are Revolutionizing the Aerospace Materials Market?

Advanced technologies such as innovative carbon fiber composites, additive manufacturing, and AI-driven design are transforming the market by improving fuel efficiency, increasing structural strength, and minimizing weight. Furthermore, cutting-edge composites with embedded microcapsules are rapidly being created to autonomously repair damage, substantially raising the lifespan of aircraft components.

Supply Chain Analysis of the Aerospace Materials Market

Feedstock Procurement

- It refers to the sourcing, acquisition, and logistical management of essential materials like aluminum alloys, carbon fiber, and titanium sponge necessary to manufacture aircraft components.

- Major Players: Alcoa Corporation (US), Precision Castparts Corp. (US)

Chemical Synthesis and Processing

- It includes the development, chemical reaction, and conversion of raw materials into high-performance materials used in aircraft and spacecraft.

- Major Players: Hexcel Corporation (US), Teijin Limited

Packaging and Labelling

- It refers to the specialized, highly regulated process of packing, safeguarding, and identifying crucial aircraft materials and components during storage and transit.

- Major Players: PPG Industries,3M Company

Regulatory Compliance and Safety Monitoring

- It refers to the stringent protocols, testing, and continuous oversight needed to ensure that innovative materials meet global performance, airworthiness, and safety standards.

- Major Players: Alcoa Corporation, Hexcel Corporation.

Aerospace Materials Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | A Department of Defense (DoD) mandate requiring that any specialty metals (e.g., titanium, certain steel and nickel alloys) used in military aircraft must be melted or produced within the United States or a qualifying country. |

| European Union | Annex XIV & SVHC: Lists Substances of Very High Concern. The aerospace industry must continually eliminate or find approved alternatives for restricted materials such as hexavalent chromium (used in anti-corrosion coatings) and certain epoxy resins to meet the REACH compliance deadlines. |

| India (DGCA) | Historically dependent on imported materials, the Directorate General of Civil Aviation is actively aligning with Civil Offset Policies to encourage local manufacturing and strict compliance with international testing frameworks. |

Market Dynamics

Driver

Growth of the Aerospace Industry

The rapid growth of the aerospace sector is the major factor driving market growth. As global air travel grows courageously, there is a rising demand for new aircraft with upgrades to current fleets. In addition, this growth requires a corresponding increase in the trade of aerospace materials such as metals, composites, and alloys. The rapid development of innovative aircraft models, like state-of-the-art commercial jets, further highlights the need for advanced materials.

Restraints

Complex Manufacturing Processes

The manufacturing of innovative aerospace materials, like the titanium alloys and carbon fiber composites, includes tedious processes with high capital investments, which is the key factor hindering market expansion. Moreover, these high manufacturing costs generally translate into costly products, limiting extensive adoption, especially among smaller aerospace firms and markets.

Opportunity

Increasing Demand for Fuel Efficiency

The surge in the necessity for fuel efficiency and sustainable aircraft is the key factor in creating lucrative opportunities in the market. Durable and lightweight materials like carbon fiber composites are rapidly being adopted by manufacturers and airlines to realize aircraft weight reduction while enhancing the overall fuel economy and minimizing emissions as per sustainability goals.

Segmental Insights

Material Type Insights

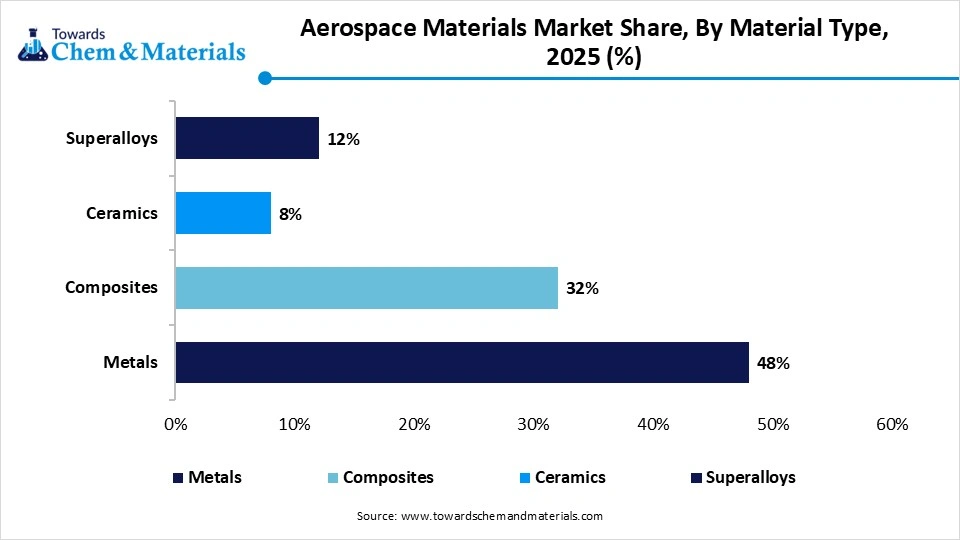

The Metals Segment Dominated the Market with 48% of Market Share in 2025

The metals segment dominated the market with the largest share of 48% in 2025. The dominance of the segment can be attributed to its high strength-to-weight ratio, extensive support for adoption, and an established manufacturing process to ensure reliability. Also, cost advantages sustain demand in aircraft structures.

The composites segment held the market share of 32% in 2025 and is expected to grow at the fastest CAGR of 9.2% over the forecast period. The growth of the segment can be credited to its increasing use in next-generation aircraft, along with its superior corrosion resistance. Lightweight materials enhance fuel efficiency further.

")

The superalloys segment held the market share of 12% in 2025. The growth of the segment can be linked to the surge in jet engine production and its superior mechanical properties compared to other materials. It is also crucial for high-temperature engine components.

Aircraft Type Insights

The Commercial Aircraft Segment Dominated the Market with 46% of Market Share in 2025

The commercial aircraft segment dominated the market with the largest share of 46% in 2025 and is expected to grow at the fastest CAGR of 8.3% over the forecast period. The dominance and growth of the segment can be driven by rising aircraft passenger traffic, fueling aircraft production, and ongoing fleet expansion. Fuel efficiency needs to propel demand for advanced materials.

The military aircraft segment held a market share of 28% in 2025. The growth of the segment is owing to the growing demand for high-performance materials from the advanced jets and ongoing modernization initiatives. Furthermore, the defense budget also supports procurement programs.

The general aviation segment held a market share of 14% in 2025. The growth of the segment is due to increasing demand from businesses and the expansion of the private aviation industry. Lightweight materials will enhance efficiency soon.

Application Insights

The Structural Components Segment Dominated the Market with 42% of Market Share in 2025

The structural components segment dominated the market with the largest share of 42% in 2025. The dominance of the segment can be attributed to its high durability, which supports long life cycles and growing demand for aircraft structural integrity. Lightweight materials reduce overall fuel consumption.

The engine components segment held the market share of 26% in 2025 and is expected to grow at the fastest CAGR of 8.4% over the forecast period. The growth of the segment can be credited to the surge in aircraft production and improvements in jet engines' efficiency. High temperature resistance fuels adoption further.

The interior components segment held a market share of 17% in 2025. The growth of the segment can be linked to the rising need for passenger comfort and rapid airline upgrades to drive material innovation. Lightweight interiors enhance fuel efficiency shortly.

Manufacturing Process Insights

The Forging Components Segment Dominated the Aerospace Materials Market with 28% of Market Share in 2025

The forging segment dominated the market with the largest share of 28% in 2025. The dominance of the segment can be driven by its reliability fueling preferences in critical parts, along with the increasing requirement for high-strength components. Aerospace standards support market expansion shortly.

The additive manufacturing segment held the market share of 22% in 2025 and is expected to grow at the fastest CAGR of 10.1% during the forecast period. The growth of the segment is owing to its lightweight and complex designs, which drive adoption, coupled with the rapid prototyping techniques. It reduces material waste to promote efficiency.

The machining segment held a market share of 26% in 2025. The growth of the segment is due to increasing demand for complex geometries and the adoption of advanced machine techniques. Also, precision manufacturing ensures component quality.

End-Use Insights

The OEM Segment Dominated the Market with 63% of Market Share in 2025

The OEM segment dominated the market with the largest share of 63% in 2025. The dominance of the segment can be attributed to the technological innovations in the production process and the surge in aircraft production. Long-term contracts ensure a steady supply.

The MRO segment held a market share of 37% in 2025 and is expected to grow at the fastest CAGR of 8.2% during the study period. The growth of the segment can be credited to the increasing air traffic and growing need for maintenance from aging aircraft fleets. Replacement parts will drive material consumption soon.

Supplier Type Insights

The Tier 1 Suppliers Segment Dominated the Market with 44% of Market Share in 2025

The tier 1 suppliers segment dominated the market with the largest share of 44% in 2025. The dominance of the segment can be linked to its advanced capabilities and growing demand for high-value components. Direct OEM partnerships ensure robust demand in the near future.

The tier 2 suppliers segment held the market share of 33% in 2025 and is expected to grow at the fastest CAGR of 7.9% over the forecast period. The growth of the segment can be driven by increasing outsourcing initiatives and the expansion of supply chains globally. Component specialization also supports segment growth.

The tier 3 suppliers segment held a market share of 23% in 2025. The growth of the segment is owing to the ongoing integration into supply chains and the growing demand for raw materials. High-volume production impacts positive market growth further.

Regional Insights

How did North America Dominate the Aerospace Materials Market in 2025?

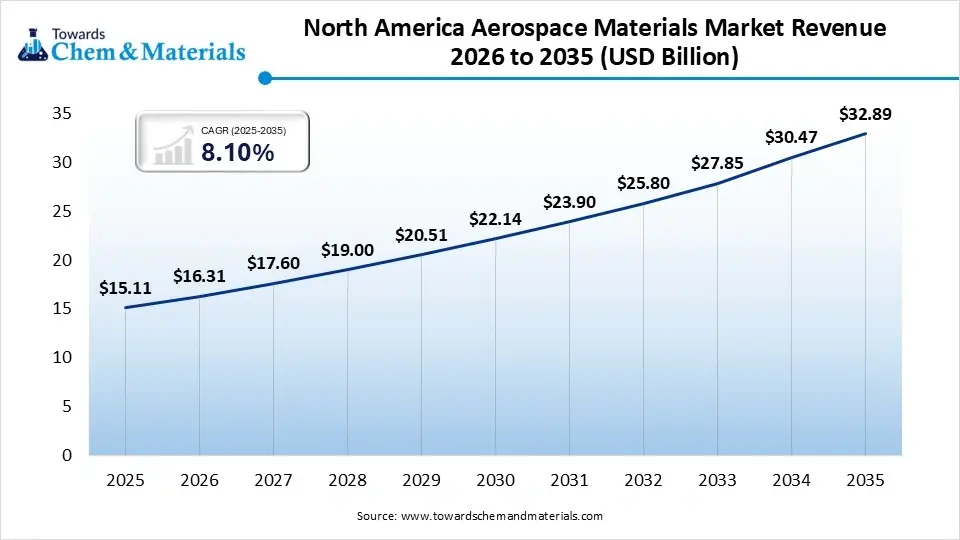

The North America aerospace materials market size was estimated at USD 15.11 billion in 2025 and is projected to reach USD 32.89 billion by 2035, growing at a CAGR of 8.10% from 2026 to 2035.North America dominated the market with the largest share of 38% in 2025. The dominance of the region can be attributed to the strong presence of an aerospace manufacturing base and a surge in defense spending to increase material usage. In addition, ongoing initiatives for sustainable aviation, such as the development of electric aircraft and the use of materials with lower environmental impact, are leading to market growth soon.

U.S. Aerospace Materials Market Trends

The growth of the market in the country is due to the increasing demand for titanium alloys, lightweight composites, and innovative aluminum materials. Also, a surge in investment in space exploration programs, along with private space ventures, needs cutting-edge thermal-resistant materials to drive market growth further.

Asia Pacific held a market share of 23% in 2025 and is expected to grow at the fastest CAGR of 9.1% over the forecast period. The growth of the region can be credited to the increasing product demand from the aviation sector and heavy government investments in aerospace manufacturing. Furthermore, increasing emphasis on green initiatives is propelling the demand for recyclable and sustainable materials, such as advanced composites and specialized aluminum alloys.

China Aerospace Materials Market Trends

In the Asia Pacific, China dominated the market owing to the surge in defense modernization and increasing demand for lightweight composite materials in the emerging part of the country. Moreover, significant investments in defense infrastructure, such as next-generation military aircraft, are fueling demand for innovative metals such as titanium

")

Recent Developments

- In March 2026, Americhem unveiled ColorFast® SFT5500, an injection-moldable, PFAS-free thermoplastic designed for aircraft interiors, addressing a limited market for high-performance, sustainable materials. The compound meets stringent FAA 55/55 OSU fire standards, low smoke, and toxicity requirements, facilitating regulatory compliance for aerospace manufacturers.(Source: www.plasticstoday.com )

Top Companies List

- Alcoa Corporation: Alcoa Corporation holds a specialized, upstream position in the global aerospace materials market, acting primarily as a critical source for high-quality raw material, while its historic downstream operations now live under separate, standalone aerospace giants.

- AMETEK Inc: AMETEK Inc. is a major global manufacturer of electronic instruments and electromechanical devices, with a significant presence in the aerospace materials and components market.

Other Companies in the Market

- AMG Advanced Metallurgical Group

- ArcelorMittal

- Arconic, Inc.

- ATI Metals. (US)

- Constellium N.V (Netherlands)

- Cytec Solvay group (Belgium)

- Doncasters Group Ltd

- DuPont de Nemours, Inc. (US)

- Global Titanium Inc

- Hexcel Corporation, (US)

- Incorporated (ATI)

- Kaiser Aluminum

- DOW

- Kobe Steel Ltd (Japan)

- Mitsubishi Chemical Holdings

- NOVELIS (US)

- Avdel

- NSSMC Group

- PPG Industries, Inc.

Segments Covered

By Material Type

- Metals

- Aluminum Alloys

- 2xxx Series

- 7xxx Series

- Titanium Alloys

- Alpha Alloys

- Beta Alloys

- Steel Alloys

- Stainless Steel

- High-strength Steel

- Aluminum Alloys

- Composites

- Carbon Fiber Reinforced Polymer (CFRP)

- Glass Fiber Reinforced Polymer (GFRP)

- Aramid Fiber Composites

- Ceramics

- Oxide Ceramics

- Non-oxide Ceramics

- Superalloys

- Nickel-based Alloys

- Cobalt-based Alloys

By Aircraft Type

- Commercial Aircraft

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional Jets

- Military Aircraft

- Fighter Jets

- Transport Aircraft

- Helicopters

- General Aviation

- Business Jets

- Light Aircraft

- Spacecraft

- Satellites

- Launch Vehicles

By Application

- Structural Components

- Fuselage

- Wings

- Tail Section

- Engine Components

- Turbine Blades

- Combustion Chambers

- Interior Components

- Seating

- Cabin Panels

- Exterior Components

- Landing Gear

- Control Surfaces

By Manufacturing Process

- Casting

- Forging

- Machining

- Additive Manufacturing (3D Printing)

By End-Use

- OEM (Original Equipment Manufacturers)

- MRO (Maintenance, Repair & Overhaul)

By Supplier Type

- Tier 1 Suppliers

- Tier 2 Suppliers

- Tier 3 Suppliers

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)