Content

What is the Specialty Polymers Market Size and Share?

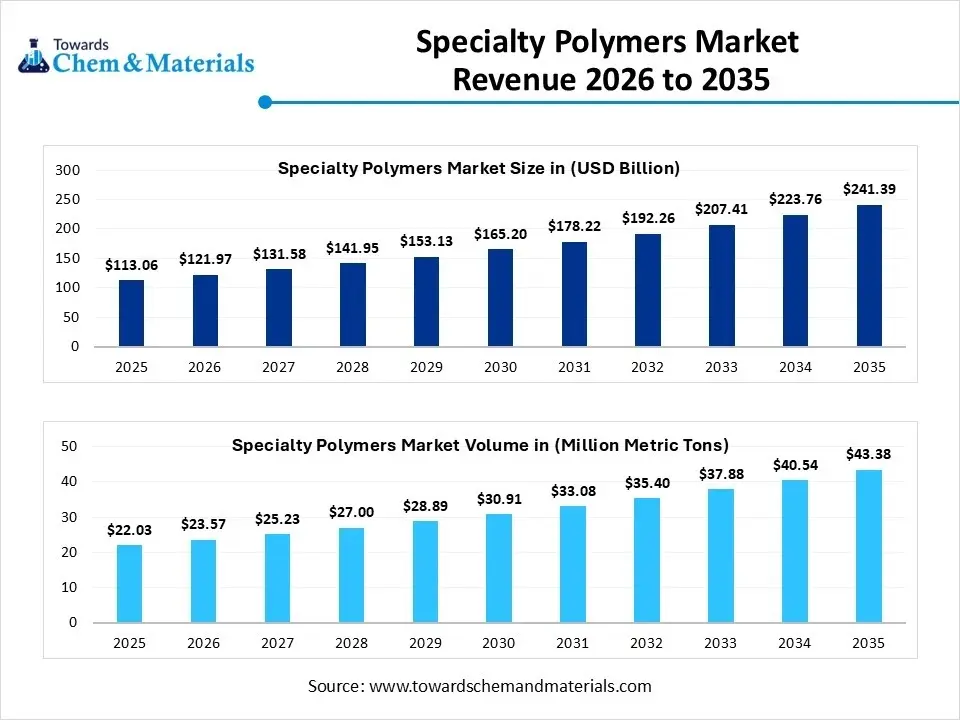

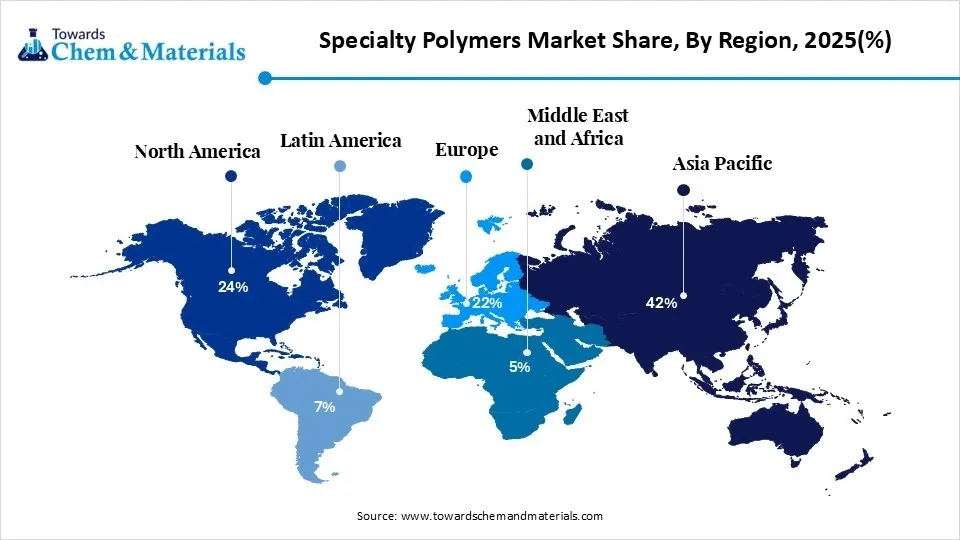

The specialty polymers market size was valued at USD 113.06 billion in 2025, is estimated to reach USD 121.97 billion in 2026, and is projected to reach USD 241.39billion by 2035, exhibiting a compound annual growth rate (CAGR) of 7.88% over the forecast period from 2026 to 2035.Asia Pacific dominated the specialty polymers market with the largest revenue share of 42% in 2025 and is expected to grow at the fastest CAGR of 8.01% during the forecast period. The properties of specialty polymers, which are tailored for their high performance, like chemical inertness, extreme heat resistance, and biocompatibility, make it a preferred choice by many consumers and sectors like electronics, aerospace, and medical devices. The key players collaborations and supply chain integration, like Arkemas collaboration for the development of biobased products for aerospace and automotive sectors, along with Gulbrandsens partnership, help boost the market, which will support growth in the coming years.

Key Takeaways

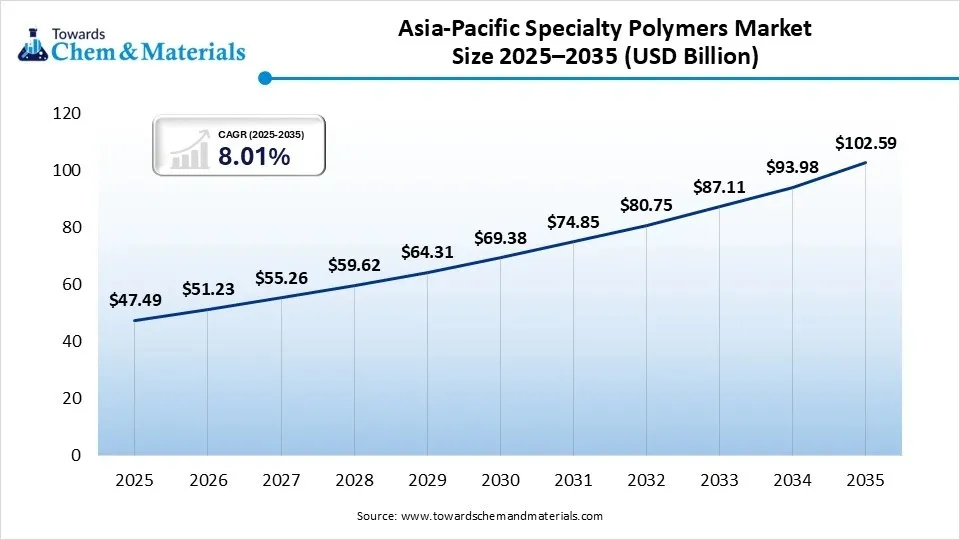

- By region, Asia Pacific dominated the specialty polymers market with a share of 42% in 2025 and is expected to grow at a CAGR of 6.80% over the forecast period.

- By region, India held 24% market share in the specialty polymers market in 2025 and is expected to experience the fastest growth with a CAGR of 8.65% in the forecast period.

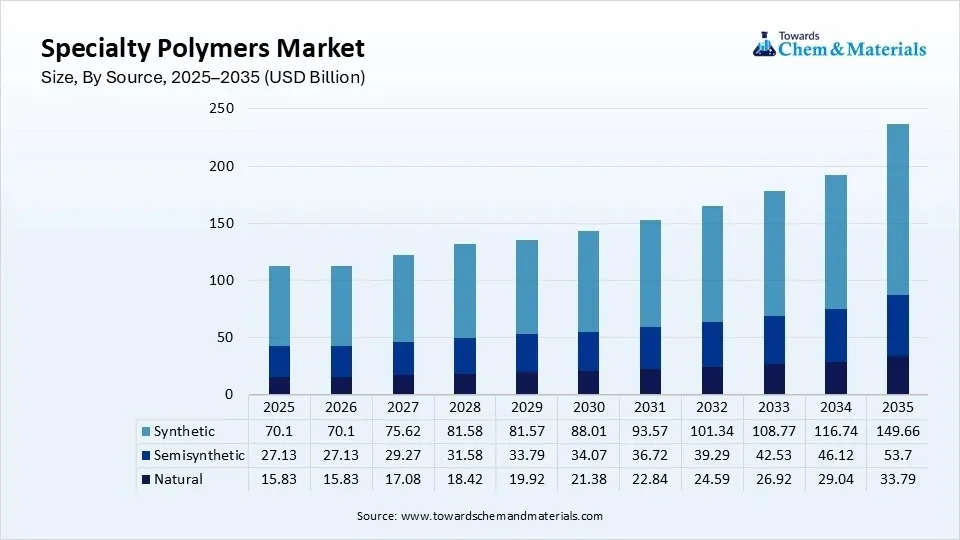

- By source, the synthetic segment dominated the market with a 62% share in 2025 and is expected to grow at a CAGR of 6.35% over the forecast period.

- By source, the natural segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.85% in the forecast period.

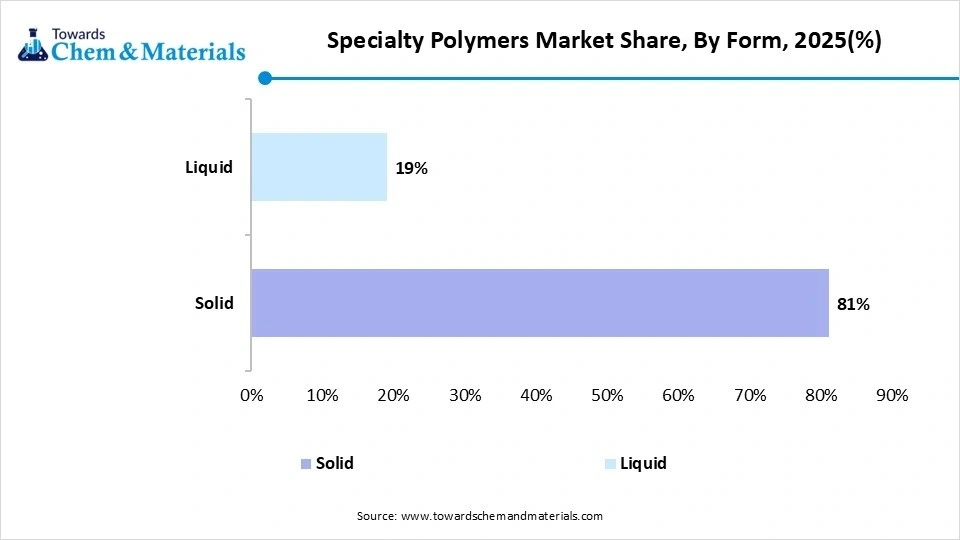

- By form, the solid segment dominated the market with an 81% share in 2025 and is expected to grow at a CAGR of 7.20% over the forecast period.

- By form, the liquid segment held 19% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.35% in the forecast period.

- By product type, the specialty thermoplastics segment dominated the market with a 36% share in 2025 and is expected to grow at a CAGR of 7.65% over the forecast period.

- By product type, the biodegradable polymers segment held 13% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.20% in the forecast period.

- By end use, the transport segment dominated the market with a 24% share in 2025 and is expected to grow at a CAGR of 7.85% over the forecast period.

- By end use, the building and construction segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.10% in the forecast period.

According to Towards Chemicals and Materials Analytics and Consulting, the global specialty polymers market volume was valued at 22.03 million metric tons in 2025 and is expected to surpass around 43.38 million metric tons by 2035, accelerating a compound annual growth rate (CAGR) of 7.01% over the forecast period from 2026 to 2035.

Specialty Polymers: Integrated Superior Properties

Specialty polymers are high-performance materials which sre driven by the growing demand from sectors like aerospace, electrical, and automotive manufacturers which are due to their high-performance ability and properties like lightweight and heat-resistant materials. The rapid expansion is driven by growing applications in electric vehicles, 5G telecommunications, and biocompatible healthcare, supporting the growth. The regional dominance is driven by demand from industries and strict environmental sustainability and regulations due to the shift towards bio-based and circular economy solutions, which fuels the growth of the market.

The specialty polymers key players are driving market growth through strategic collaborations with sectors like automotive, semiconductor manufacturers, and aerospace companies due to demand for specialized and engineered polymers. These partnerships and collaborations aim to focus on lightweight materials demand, bio-based plastics demand, and rising focus on EV thermal management, which allows suppliers to develop high-performance materials which have a specific and specialized applications, which drives the growth of the market. The key players like Solvay and BASF partner with tech manufacturers to develop specialty polymers according to the need.

- For instance, in October 2025, Syensqo introduced the industrys first certified circular content portfolio of high-performance elastomers and lubricant fluids, featuring up to 29% post-industrial recycled hydrofluoric acid. Manufactured at the Spinetta Marengo facility in Italy, these products maintain the same technical properties as virgin materials while strengthening supply chain sustainability.(Source: www.plasticstoday.com)

Global Investment Flow for Specialty Polymers Market 2026

- The growing investment by manufacturers as well as consumers is in the specialty polymers market due to growing demand for high-performance and specialized function materials due to their properties and functions by the players.

- In July 2026, Deepak Nitrite announced a massive ₹11,000 crore investment roadmap, including an ₹8,500 crore initiative to build India’s first fully integrated Polycarbonate Resin ecosystem in Dahej, Gujarat. This mega specialty materials project targets extensive import substitution for advanced engineering plastics used in electric vehicles, electronics, infrastructure, and medical devices.(Source: www.indianchemicalnews.com)

- In November 2025, Omya officially launched Omya Performance Polymer Distribution at the K 2025 trade fair in Düsseldorf, Germany. This strategic move separates Omya’s core polymer distribution business from its traditional calcium carbonate and mineral operations to create a highly focused, independent platform.(Source: www.plasticsnews.com)

The Growing Electronic Industry Surge Demand for Specialty Polymer

The growing adoption of various electronic devices like smartphones, laptops, computers, and many more increases the demand for specialty polymer. The increasing manufacturing of advanced electronic devices fuels demand for specialty polymer for the production of components like insulators, housings, connectors, and circuit boards. The growing focus on miniaturizing electronic devices increases demand for specialty polymers like PET, polyimides, and polycarbonates for maintaining performance and resisting damage. The increasing expansion of technologies like the Internet of Things and the growing availability of 5G technology fuel demand for specialty polymer for handling data processing and connectivity. The focus on the development of energy-efficient electronic devices increases the adoption of specialty polymer. The growing electronic industry is a key driver for the specialty polymer market.

Market Growth Trends:

- The demand for sustainability and bio-based formulations due to strict environmental regulations and manufacturers shift towards integration of bio-based feedstocks and advanced chemical recycling systems in production is a major growth trend.

- AI and digital material platforms like AI-assisted material design to develop personalized specialty polymers for electrical and medical applications for advanced product demand, which helps in simulate an accelerate development.

- The growing trend towards multifunctional and tailor-made additives as the industry is shifting to multifunctional solutions that have mechanical strength, chemical resistance, and thermal stability, which is a major trend in the market.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD xx Billion / xx Million Metric Tons |

| Market Size by 2035 | USD xx Billion / xx Million Metric Tons |

| Growth rate | CAGR xx% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | |

| Key Profiled Companies |

Specialty Polymer: Integration of AI in Manufacturing

Specialty polymer advancements and the shift from generic plastics to molecular-level engineering and custom-tailored materials, and demand for precision polymerization through techniques like ATRP, RAFT, and ring-opening polymerization, this helps yield advanced block copolymers and nano carriers tailored for specific applications. The shift towards AI and bio-based chemistry for critical applications drives growth. Smart and stimuli-responsive polymers and advanced medical hydrogels are the major shifts towards advancements of the product. The integration of AI in specialty polymers for creating specialized products through generative models and advanced design. The integration of AI and ML also helps in optimizing manufacturing and efficiently enhancing material performance.

Supply Chain Analysis of Specialty Polymers Market:

Specialty Polymer Production & Processing

- Specialty polymers are produced through advanced polymerization and compounding processes to develop high-performance materials with enhanced thermal stability, chemical resistance, mechanical strength, and electrical properties for demanding industrial applications.

- Victrex manufactures high-performance PEEK polymers for aerospace, automotive, medical, electronics, and energy applications. Its specialty polymers provide exceptional strength, heat resistance, chemical stability, and lightweight performance in demanding environments.

- Key Players: Solvay, BASF, Evonik Industries, Victrex.

Quality Testing & Certification

- Specialty polymers must comply with standards for thermal stability, mechanical strength, chemical resistance, flame retardancy, biocompatibility, and product safety before commercial use.

- Solvay develops specialty polymers that meet stringent international quality and regulatory standards for aerospace, healthcare, automotive, electronics, and industrial applications, ensuring reliable performance under challenging operating conditions.

- Key Authorities & Standards: International Organization for Standardization, ASTM International, Underwriters Laboratories, European Chemicals Agency.

Distribution to End-Use Industries

- Specialty polymers are supplied to aerospace manufacturers, automotive companies, electronics producers, medical device manufacturers, industrial equipment companies, and energy industries for high-performance applications.

- Evonik Industries supplies a broad portfolio of specialty polymers for medical technology, additive manufacturing, coatings, and industrial applications, helping customers improve product durability, processing efficiency, and sustainability.

- Key Suppliers: Solvay, BASF, Evonik Industries

Sustainability Analysis of Specialty Polymers

The core factor towards sustainability for specialty polymers is fossil depletion and bio-based alternatives due to the shift towards bio-based replacements to avoid volatility and reduce upstream emissions. The use in sectors such as healthcare, electronics, and aerospace. The regulations and ESG mandates, rapid shift towards bio-based feedstocks, aligning with the circular economy, and material design without altering high heat and high strength performance. The Major manufacturers are heavily investing in this transition. Companies like BASF, DuPont, Arkema, and Mitsui Chemicals are expanding manufacturing capacities specifically for high-performance, circular-economy-aligned engineering plastics.

What are Specialty Polymers?

Specialty polymers are high-performance materials that are tailored and modified according to need and industrial demand, with integration of superior properties like extreme heat resistance, mechanical strength, and chemical inertness. They are specialized or advanced, engineered for specific applications in sectors like aerospace, automotive, and electronics due to growing demand. The advanced materials include engineering thermoplastics and fluoropolymers, functional polymers that are designed with built-in functionalities, compatibilizers, and coupling agents that are used in recycling and compounding like grafted with maleic anhydride.

What are the Key Uses of Specialty Polymers?

Specialty polymers are high-performance materials with specific and exceptional properties. They are used by various sectors due to their applications.

- Electronics and Telecommunications:Their use and properties, like dielectric strength, low weight, and high thermal stability, make them a preferred choice for semiconductors and circuitry and conductivity in advanced storage and electronic sensors.

- Automotive and Aerospace:Specialty polymers ability to withstand maximum stress and extreme environments, due to their functional components providing specific properties, increases the demand for specialized polymers. The weight reduction, helping improve fuel efficiency with the replacement of traditional metals, drives growth.

- Industrial Processing and Packaging:Specialty polymers provide barriers to create multilayer and high-barrier recyclable packaging films, it also protect from harsh environments through coatings demanding high resistance to chemicals, abrasion, and UV light.

- Advanced Manufacturing and Additives:The specialty polymers act as functional and vital modifiers. The ability of polymers as compatibilizers and coupling agents allows for seamless bonding of different plastics or binding plastics to reinforcements like glass and carbon fibers.

Specialty Polymers Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Toxic Substances Control Act (TSCA); OSHA Hazard Communication Standard | High-performance polymers, chemical safety | The U.S. supports specialty polymer innovation for automotive, aerospace, electronics, healthcare, and industrial applications while ensuring environmental and workplace safety. |

| European Union | European Chemicals Agency (ECHA); European Commission | REACH Regulation; Circular Economy Action Plan | Sustainable polymers, recyclability, chemical compliance | Europe promotes environmentally compliant specialty polymers with a strong focus on circular economy and advanced material development. |

| China | Ministry of Industry and Information Technology (MIIT); Ministry of Ecology and Environment (MEE) | Environmental Protection Law; Advanced Materials Development Policies | Engineering plastics, industrial modernization | China is expanding specialty polymer production to meet growing demand from electronics, automotive, and renewable energy industries. |

| India | Ministry of Chemicals and Fertilizers; Bureau of Indian Standards (BIS) | Chemical Safety Rules; BIS Polymer Standards | Engineering polymers, domestic manufacturing | India is increasing production and consumption of specialty polymers through industrial expansion and import substitution initiatives. |

| Japan | Ministry of Economy, Trade and Industry (METI) | Chemical Substances Control Law (CSCL) | Advanced polymers, electronics, precision manufacturing | Japan focuses on high-performance specialty polymers for semiconductors, medical devices, and automotive applications. |

| Germany | Federal Environment Agency (UBA); German Chemical Industry Association (VCI) | REACH Compliance; Industrial Emissions Directive (IED) | Sustainable manufacturing, lightweight materials | Germany is a leading innovator in specialty polymers for automotive lightweighting, industrial engineering, and high-performance applications. |

Specialty Polymers Market Dynamics

Drivers

Specialty Polymers: Medical Advancements

The specialty polymer market is driven by rising demand for high-performance materials that offer superior mechanical strength, chemical resistance, thermal stability, and lightweight properties compared to commodity plastics. Growing adoption across automotive, aerospace, electronics, medical devices, and industrial applications is reinforcing market expansion. Electrification of vehicles, miniaturization of electronic components, and increased use of advanced medical materials are increasing demand for engineered polymers with precise functional characteristics. Regulatory pressure to improve energy efficiency and reduce emissions is also accelerating substitution of metals and traditional materials with specialty polymers. In addition, ongoing innovation in polymer chemistry and processing technologies is supporting development of application-specific grades.

Challenges

Specialty Polymers: High Production and Processing Costs

The key challenges in the specialty polymers market are the high production and processing costs of complex synthesis, and an energy-intensive manufacturing process due to a price-sensitive downstream market, which hinders the growth of the market. The volatility in feedstock prices, as it highly depends on petroleum feedstock, is a major hindrance to the growth of the market. Other key challenges are strict environmental and circularity regulations and competition from alternatives and substitutes.

Opportunities

Specialty Polymer: Sustainability and the Circular Economy

The specialty polymers market is driven by key growth opportunities, such as the demand for lightweight, sustainable materials use and high performance in various industries, which boosts the growth of the market. The key opportunities lie in sustainability and the circular economy to meet the growing environmental regulations and ESG goals, as producers are heavily investing in bio-based specialty polymers, a major growing factor in the market, supporting expansion.

Segmental Insights

Source Insights

The synthetic segment dominated the market with a 62% share in 2025 and is expected to grow at a CAGR of 6.35% over the forecast period. Synthetic specialty polymers are created in a laboratory and factors which have high-performance properties and are used by many key players. The primary sources are petroleum and natural gas, where monomers are extracted, which are then polymerized into advanced materials. The basic monomers or precursors are ethylene, propylene, and benzene, which are then transformed into functional compounds like vinyl, fluorinated, and carbonyls.

")

The natural segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.85% in the forecast period. Natural polymers are also known as biopolymers, which have specific or highly unique chemical and physical properties, with applications in industrial, pharmaceutical, and biomedical sectors, as they are valued for their biodegradability, sustainability, and biocompatibility. The most commonly used biopolymers are sourced from plants, microorganisms, and animals, such as chitin and chitosan, alginate, collagen and gelatine, hyaluronic acid, cellulose and starch, due to their applications and properties.

Specialty Polymers Market Share, By Source, 2025(%)

| By Source | Market Share (%) |

| Natural | 14% |

| Semisynthetic | 24% |

| Synthetic | 62% |

Form Insights

The solid segment dominated the market with an 81% share in 2025 and is expected to grow at a CAGR of 7.20% over the forecast period. Solid polymers are extensively used for the manufacturing of aerospace, biomedical devices, and advanced packaging. Market companies use solid materials such as pellets and granules, which are applicable in extrusion and smart device manufacturing. Powders are used in pharmaceutical excipients and rotational molding. Pellets are used and applicable in enteric coating, capsules, and delayed-release oral tablets.

")

The liquid segment held 19% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.35% in the forecast period. The liquid polymers are tailored for specific mechanical and chemical properties, which are widely used in coating, water treatment, sealants, adhesives, and personal care formulations. The common types of polymers are liquid HEC, polyethylene glycol derivatives, liquid silicone rubber and fluorosilicones, and UV-curable resins and anionic and cationic polyacrylamides; due to their applications and properties, they are a preferred choice.

Specialty Polymers Market Share, By Form, 2025(%)

| By Form | Market Share (%) |

| Solid | 81% |

| Liquid | 19% |

Product Type Insights

The specialty thermoplastics segment dominated the market with a 36% share in 2025 and is expected to grow at a CAGR of 7.65% over the forecast period. Specialty thermoplastics are high-performance polymers that are designed to have extraordinary mechanical, thermal, and chemical resistance even in harsh and extreme temperatures. These materials are also capable of enduring temperatures from -40°C to 300°C in sectors that demand such products, like medical devices, aerospace, and electronics. These polymers are formylated to meet regulatory standards such as UL-recognized flame retardancy.

- For instance, in July 2026, SABIC launched a new generation of high-performance thermoplastic compounds, LNP™ THERMOCOMP™ OFM76XXP and OFM76EXP, engineered for high-voltage power electronics. This specialty polymer rollout targets critical infrastructure components, including electric vehicle (EV) traction inverters, fast-charging hardware, and renewable energy storage systems.(Source: www.indianchemicalnews.com)

The biodegradable polymers segment held 13% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.20% in the forecast period. These polymers are advanced materials that are engineered with specific hydrolysable linkages kike carbonates, amides, and esters, which can degrade naturally while maintaining thermal and mechanical properties. They are used extensively in biomedical devices and in controlled drug delivery to specialized eco-friendly packaging. Commonly used biodegradable polymers are PGA, PLA, PHAs, PCL, and PEAs due to their specialised properties and applications.

- For instance, in July 2026, Lactips and SmartSolve introduced a plastic-free and water-soluble flexible packaging solution tailored for the beauty and personal care sectors. This zero-waste materials rollout addresses single-use plastics by introducing a functionalized structural compound that fully dissolves without microplastic contamination.(Source: www.packaginginsights.com)

Specialty Polymers Market Share, By Product Type, 2025(%)

| By Product Type | Market Share (%) |

| Specialty Elastomers | 21% |

| Specialty Thermoplastics | 36% |

| Specialty Thermosets | 17% |

| Biodegradable Polymers | 13% |

| Liquid Crystal Polymers | 7% |

| Others | 6% |

End Use Insights

The transport segment dominated the market with a 24% share in 2025 and is expected to grow at a CAGR of 7.85% over the forecast period. They are used in transport by replacing heavy metals with lightweight materials, which helps improve fuel efficiency and also ensures safety to withstand extreme and harsh chemicals and temperatures, along with mechanical stress, which increases the demand. The ability for safe electric insulation in modern hybrid and electric vehicles drives growth. The key applications include powertrain and under-the-hood, fluid management, structural lightweighting, interior and aesthetics, and electronics and EV battery enclosures.

The building and construction segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.10% in the forecast period. They are used in polymer-modified cement, which helps improve strength, water resistance, and flexibility in tile adhesives. They are also used due to their high durability in epoxy/polyurethane coatings, silicone sealants, and acoustic laminated glass interlayers due to their high performance and construction demand.

Regional Insights

How did Asia Pacific dominate the Specialty Polymers Market in 2025?

The Asia Pacific specialty polymers market size was estimated at USD 47.49 billion in 2025 and is projected to reach USD 102.59 billion by 2035, growing at a CAGR of 8.01% from 2026 to 2035.Asia Pacific dominated the market with a share of 42% in 2025 and is expected to grow at a CAGR of 6.80% over the forecast period. The presence of a large-scale manufacturing base in the region and growing demand from manufacturing sectors in various countries and integrated industrial clusters supporting wide consumption drives growth. The rapid expansion of the automotive sector, which demands specialty polymers to enhance fuel efficiency and durability, boosts the growth and expansion of the market in the region. The major growth factor is the presence of major chemical innovators in the region, which contributes to the production and supply chain efficiency.

")

- For instance, in May 2025, DKSH Performance Materials acquired APN Plastics to scale up its specialty polymers footprint across the Asia-Pacific region. This strategic acquisition fully integrates APNs distribution infrastructure into DKSH’s existing Specialty Chemicals business line.(Source: www.alchempro.com)

India Specialty Polymers Local Production and Supply Chain

The India specialty polymers market is experiencing rapid growth, which is driven by the presence of major giants that support domestic production, like PLUSS, which helps produce advanced functionalized polymers that help improve the processing of local polymer compounds, driving the growth of the market. The strong demand from the healthcare and electronics sectors for biobased and specialty polymers to improve performance and efficiency further boosts the growth of the market.

- For instance, in April 2026, DCM Shriram Ltd. partnered with Netherlands-based Teknor Apex B.V. to launch a joint venture named PolyTek. Branded officially as PolyTek, the venture focuses on producing and distributing advanced polymer compounds, colour concentrates, and custom specialty material solutions targeted at Indias rapidly growing industrial sector.(Source: www.alchempro.com)

China Presence of Key Players of Specialty Polymers

China specialty polymers market is experiencing robust growth driven by the growing domestic manufacturing and consumption, which increases the widespread adoption of manufacturing capacities like domestic giants Sinopec and PetroChina Company Limited, which drive chemical and petrochemical spheres, driving growth of the market. The key technological advancement in materials and high-performance plastics for battery and thermal management further boosts the growth of the market in the country.

- For instance, in November 2025, Clariant completed a major CHF 80-million investment to expand its Care Chemicals production site at Daya Bay in Huizhou, China. This strategic expansion transforms the facility into an integrated Multi-Purpose Plant and Ethylene Oxide Derivatives (EOD) hub, substantially boosting its capacity for high-value specialty materials and pharmaceutical excipients.(Source: www.clariant.com)

North America Specialty Polymers Market Shift Towards Sustainability

The North America specialty polymers market size was estimated at USD 27.13 billion in 2025 and is projected to reach USD 59.14 billion by 2035, growing at a CAGR of 8.10% from 2026 to 2035.North America held a market share of 24% in 2025 and is expected to have the fastest growth with a CAGR of 8.65% in the forecast period. The regions large investments in the industry for application in sectors like automotive, medical, and defense drive the growth. The sustainability and circular economy mandates in the region demand advanced chemical reduction methods and bio-based feedstock demand, which drives the growth. The expansion of healthcare and medical in the country demands advanced drug delivery systems and implant devices, boosting growth.

United States Specialty Polymers Market Federal Fundings

The United States specialty polymers market is experiencing growth driven by a shift towards electric vehicles, which demand specialised elastomers and lightweight composites. The market is supported by federal funding through the CHIPS and Science Act, which demand high-performance thermoplastics, boosting the growth of the market. The market is highly consolidated and competitive, with major global chemical and material science firms leading U.S. production and R&D pipelines, which helps in the expansion of the market.

- For instance, in October 2025, NNA Polymers is constructing a world-scale 200,000-metric-ton-per-year polyacrylamide plant in Big Spring, Texas. This major industrial launch aims to secure a reliable, domestic North American supply chain for critical performance polymers.(Source: www.chemanalyst.com)

Canada Growing Research in Specialty Polymers Market

The Canadian specialty polymers market is experiencing growth driven by domestic institutions and research and development in academia and industry, which are key innovators and suppliers for the specialty polymer market in Canada. The key suppliers presence in the country includes 3M Company, BASF SE, and Arkema plays major role in the growth of the market, supporting expansion. The demand for materials in key players like aerospace and defense, automotive, healthcare, and electronics fuels the growth of the market.

Europe Specialty Polymers Market Regulatory and Sustainability Focus

The Europe specialty polymers market size was estimated at USD 24.87 billion in 2025 and is projected to reach USD 54.31 billion by 2035, growing at a CAGR of 8.12% from 2026 to 2035.Europe held a market share of 22% in 2025 with a CAGR of 6.55%. Europes strict chemical regulations and government-owned regulations, which are governed by the EUs REACH compliance and alignment with circular economy mandates, drive the growth. The industrys shift towards chemical recycling and bio-based feedstock further drives the growth of the market. To maintain competitiveness, major players continue to invest in sustainable production, such as running European Performance Materials plants entirely on renewable electricity, which fuels the growth.

- For instance, in May 2026, an affiliate of Lone Star Funds has agreed to acquire the entire Engineered Materials (EM) business division of DOMO Chemicals. This major consolidation builds on Lone Stars prior purchase of RadiciGroups performance polymer units, creating a combined high-performance technical polymers platform.(Source: www.indianchemicalnews.com)

United Kingdom Specialty Polymers Top Suppliers Presence

The growth of the specialty polymers market is driven by the presence of key suppliers in the country, which provide engineering thermoplastics like PEEK and LCP, and the development of functional polymers drives the growth. The UK-based converters and industrial end users like Arkema Group, BASF SE, and Evonik Industries AG play a major role in the growth of the market. Regulatory compliance in the country, which pushes the manufacturers towards bio-based polymers and advanced chemical recycling, fuels the growth.

- For instance, in May 2026, Velogy officially launched as a standalone European polymers business following German financial group AEQUITA’s acquisition of LyondellBasell’s European olefins and polyolefins operations. Headquartered in Rotterdam, Netherlands, the newly independent producer aims to blend industrial-scale volume with heightened commercial flexibility.(Source: www.plasticstoday.com)

Italy: Strong Specialty Polymers Distribution Networks

The growth of the market in Italy is driven by the presence of major industrial hubs. Solvay Specialty Polymers, operating major production and research facilities in Bollate, plays a major role in the growth. The presence of strong distribution networks, like Solvay partners with local Italian distributors like Nevicolor S.p.A. to distribute high-performance polymers like Udel PSU and Radel PPSU across the peninsula, which supports the growth and expansion of the market in the country.

Latin America Specialty Polymers Market Regional Powerhouse

The Latin America specialty polymers market size was estimated at USD 7.91 billion in 2025 and is projected to reach USD 18.10 billion by 2035, growing at a CAGR of 8.63% from 2026 to 2035.Latin America held a market share of 6% in 2025 with a CAGR of 6.35. The growth is driven by the growing sectors and industries like automotive, healthcare, and packaging in regional powerhouses like Brazil, which supports the growth. Brazils expanding industrial and medical sectors generate the highest localized demand. Specialty thermoplastics, fluoropolymers, and high-performance elastomers are seeing increased adoption due to their superior thermal resistance, electrical insulation, and durability in the region.

Brazil Specialty Polymer Market Circular Economy

The Brazil specialty polymers market is experiencing growth driven by the abundant agricultural resources’ presence supporting circular economy initiatives and the use of bio-based feedstock. Driven by surging demand in the automotive, electrical, healthcare, and sustainable packaging sectors, the country remains a key growth hub in Latin America. Major manufacturers are expanding local production to meet high-performance material needs.

- For instance, in March 2025, RadiciGroup High Performance Polymers inaugurated a new, 17,000-square-metre production facility near São Paulo, Brazil, effectively doubling its production capacity to meet growing regional demand for engineering plastics. This new site focuses on producing advanced, sustainable materials, including Renycle® and Bionside® technopolymers, for the automotive, electrical, and industrial sectors.(Source: www.radicigroup.com)

Argentina Specialty Polymers Market Key Regulations

Argentinas specialty polymers market is a high-growth segment in Latin America, driven largely by demand in agriculture, automotive manufacturing, and eco-friendly construction. The market offers premium opportunities, with local and global players focusing on tailored formulations. Local adoption is driven by a push toward low-VOC and energy-efficient building materials, necessitating specialized resins compliant with national IRAM standards.

Middle East and Africa Specialty Polymers Market Key Players Growth

The Middle East and Africa specialty polymers market size was estimated at USD 5.65 billion in 2025 and is projected to reach USD 13.28 billion by 2035, growing at a CAGR of 8.92% from 2026 to 2035.The Middle East and Africa held a market share of 6% in 2025 with a CAGR of 6.95%. The growth is driven by regional industrial diversification, expanding automotive sectors, and infrastructure projects. Industrial equipment, smart-city infrastructure, and the rapidly growing Electric Vehicle (EV) sector require advanced materials such as flame-retardant polyamides and conductive polymers, driving the highest growth in electroactive polymers. Companies like Organik Kimya and Borouge Group play significant roles in integrating downstream processing and meeting local resin consumption.

")

Saudi Arabia Vision 2030

Saudi Arabia leads the Middle East market, fueled by its integrated petrochemical infrastructure and Vision 2030 industrial diversification goals. The UAE and South Africa are also major regional hubs for consumer goods and construction-driven polymer demand. Production and compounding are concentrated in industrial hubs like Jubail, Yanbu, Dammam, and Riyadh. The proximity to massive domestic feedstocks gives Saudi-based converters significant cost advantages.

UAE Strong Presence of Different Sectors

The UAE specialty polymers market Growth is fueled by rapid industrial diversification, infrastructure developments, and massive demand in the automotive, energy, and healthcare sectors. The growth is supported by substantial local healthcare R&D; advanced polymers are highly utilized in cardiovascular products and bioactive wound care dressings. Global and regional heavyweights drive the market, including UAE-based Borouge (Abu Dhabi), SNF Group (Dubai), as well as BASF SE, Dow Chemical, and local distributors like RAI International in Dubai.

- In March 2025, the Central Bank of the UAE (CBUAE) launched a new polymer Dh100 banknote. Released as part of the "Third Issuance of the National Currency Project," this updated note entered circulation alongside existing paper and polymer banknotes.(Source: www.khaleejtimes.com)

Recent Developments

- In February 2026, Cosmo Speciality Chemicals launched an expanded portfolio of high-performance masterbatches to strengthen its presence in value-added polymer and packaging solutions. The new portfolio is designed for advanced applications, including flexible packaging (BOPP/CPP/blown films) and industrial molding (injection, extrusion, non-wovens).(Source: www.passionateinmarketing.com)

- In April 2026, Avi Polymers, a specialty chemicals and polymer manufacturer, entered the agritech space with the launch of its AI-powered platform, KrishiBuddy. Developed by its wholly owned subsidiary, AVI Eco Spark, the smart farming assistant is engineered to deliver real-time data intelligence to Indias smallholder farmers to maximize productivity and income.(Source: www.chemanalyst.com)

- In March 2026, Mechnano launched three advanced elastomeric pellet materials: TPC-95A ESD, TPU-95A ESD, and TPU-95A EMI, designed for electrostatic discharge (ESD) and electromagnetic interference (EMI) protection. Engineered for flexible, electrically functional prototype development, the portfolio directly targets advanced manufacturing industries like aerospace, electronics, and automotive engineering.(source: 3dprintingindustry.com)

Competitive Analysis

The key collaborations and joint ventures between the companies for the development of advanced materials and for the development of new facilities drive the growth.

- In June 2025, Wacker will open a new high-speed production line for hybrid polymers at its Nünchritz facility in Germany. This new facility will produce silane-terminated polymers for high-performance adhesives and sealants used in construction and industrial applications, utilising environmentally friendly alpha-silane technology.(Source: www.european-coatings.com)

- In June 2026, SI Group and Shengxiao Group formed a joint venture called Shengnova Advanced Materials to expand Biphenol production in China to support the specialty polymers sector.(Source: www.chemanalyst.com)

- In June 2026, Lubrizol and Polyhose partnered to inaugurate a state-of-the-art medical tubing manufacturing facility in Chennai, Tamil Nadu. This high-value launch directly targets the expanding medical-grade polymer market and Indias MedTech infrastructure.(Source: agrospectrumindia.com)

- In July 2025, Clariant Catalysts signed a strategic cooperation agreement with Shanghai Boiler Works to advance the production of sustainable fuels and green chemical intermediates in China. This alliance was formed following the successful startup of a commercial biomass-to-green methanol plant in Taonan, Jilin Province.(Source: www.clariant.com)

Top players in the Specialty Polymers Market & Their Offerings:

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Specialty Polymers Offerings | Key Offering/Strength |

| BASF SE | Global specialty polymers manufacturer | Ludwigshafen, Germany | Europe, North America, Asia Pacific, South America | Engineering plastics, high-performance polymers, thermoplastic polyurethanes, and specialty polymer compounds | Broad specialty polymer portfolio supported by strong R&D and global manufacturing capabilities |

| Solvay S.A. | Advanced materials and specialty polymers producer | Brussels, Belgium | Europe, North America, Asia Pacific | High-performance polymers, fluoropolymers, specialty compounds, and composite materials | Expertise in advanced polymer technologies for aerospace, automotive, and electronics applications |

| Arkema S.A. | Specialty materials and polymers manufacturer | Colombes, France | Europe, North America, Asia Pacific | Specialty polyamides, fluoropolymers, acrylic polymers, and bio-based polymers | Strong innovation in sustainable, lightweight, and high-performance polymer solutions |

| Evonik Industries AG | Specialty chemicals and advanced polymers supplier | Essen, Germany | Europe, North America, Asia Pacific, Middle East | Polyamide specialties, high-performance polymer additives, and functional polymers | Advanced material solutions focused on durability, performance, and sustainability. |

| Celanese Corporation | Engineered materials and specialty polymers producer | Irving, Texas, USA | North America, Europe, Asia Pacific | Engineering thermoplastics, liquid crystal polymers, thermoplastic elastomers, and specialty polymer compounds | Comprehensive engineered polymer portfolio with strong expertise in industrial and automotive applications |

Other Top Players Are

- DuPont de Nemours, Inc.

- SABIC

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- Mitsubishi Chemical Group

- Victrex plc

- Sumitomo Chemical

- Toray Industries, Inc.

- 3M Company

- LANXESS AG

- Daikin Industries, Ltd.

- EMS-Chemie Holding AG

- Kuraray Co., Ltd.

- RTP Company

Segments Covered

By Source

- Natural

- Cellulose-based Polymers

- Natural Rubber Derivatives

- Starch-based Polymers

- Semisynthetic

- Cellulose Acetate

- Cellulose Nitrate

- Modified Natural Polymers

- Synthetic

- Fluoropolymers

- Polyamides

- Polyimides

- Polyether Ether Ketone (PEEK)

- Polyphenylene Sulfide (PPS)

- Others

By Form

- Solid

- Pellets

- Granules

- Powder

- Sheets

- Films

- Liquid

- Resin Solutions

- Polymer Dispersions

- Liquid Resins

By Product Type

- Specialty Elastomers

- Fluoroelastomers

- Silicone Elastomers

- Thermoplastic Elastomers

- Polyurethane Elastomers

- Specialty Thermoplastics

- Polycarbonate

- Polyamide

- PEEK

- PPS

- PSU/PES

- Specialty Thermosets

- Epoxy Resins

- Phenolic Resins

- Polyimide Resins

- Cyanate Ester Resins

- Biodegradable Polymers

- PLA

- PHA

- PBS

- Starch Blends

- Liquid Crystal Polymers

- Injection Molding Grade

- Extrusion Grade

- Others

- Conductive Polymers

- Shape Memory Polymers

- High Barrier Polymers

By End Use

- Building & Construction

- Pipes & Fittings

- Insulation

- Structural Components

- Transport

- Automotive

- Aerospace

- Marine

- Rail

- Medical & Healthcare

- Medical Devices

- Drug Delivery

- Surgical Instruments

- Textile

- Functional Fibers

- Industrial Fabrics

- Food & Beverage

- Flexible Packaging

- Rigid Packaging

- Food Processing Components

- Electrical & Electronics

- Connectors

- Semiconductor Components

- Insulation Materials

- PCB Components

- Cosmetics & Personal Care

- Packaging

- Cosmetic Ingredients

- Medical-grade Containers

- Others

- Industrial Machinery

- Energy

- Consumer Goods

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

Select User License to Buy

Figures (6)