Content

What is the Current Microplastics Market Size and share?

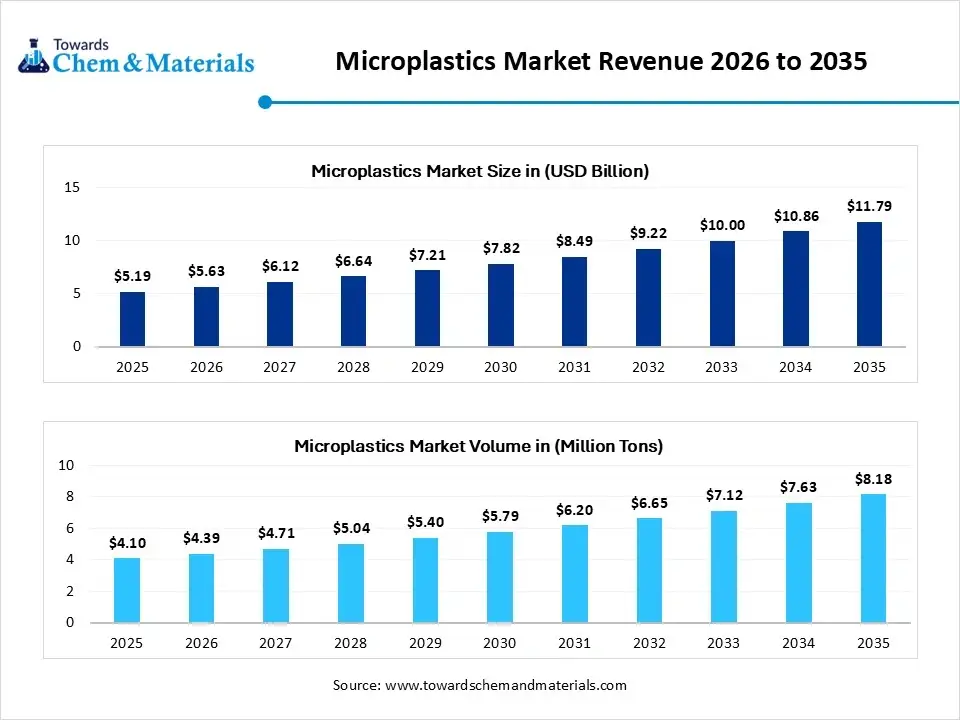

The global microplastics market was valued at USD 5.19 billion in 2025, is estimated to reach USD 5.63 billion in 2026, and is projected to reach USD 11.79 billion by 2035, growing at a CAGR of 8.55% from 2026 to 2035. In terms of volume, the microplastics market is projected to grow from 4.1 million tons in 2025 to 8.18 million tons by 2035, growing at a CAGR of 7.15% from 2026 to 2035. Also, surged industrial demand for sustainable materials and recycling, coupled with the rising adoption of biodegradable alternatives, can fuel market growth further. Microplastics are defined as synthetic solid polymer particles, either in irregular or regular shapes, measuring less than 5 millimeters in length, which are insoluble in water. The market focuses on identifying these materials across soil, aquatic, and atmospheric samples using techniques such as Raman spectroscopy and Fourier-transform infrared (FTIR).

Microplastics originate from diverse sources, primarily through the degradation of larger plastic debris into progressively smaller fragments. Furthermore, manufactured polyethylene fragments known as microbeads are intentionally introduced into various personal care products, including cleansers and toothpastes, to serve as exfoliating agents. This sector encompasses downstream waste management and water processing solutions, featuring advanced filtration systems, automated screening technologies, and specialized coagulants. These methods are employed by municipal treatment plants and industrial facilities to remove microscopic plastic particles from wastewater prior to environmental discharge.

Key Takeaways

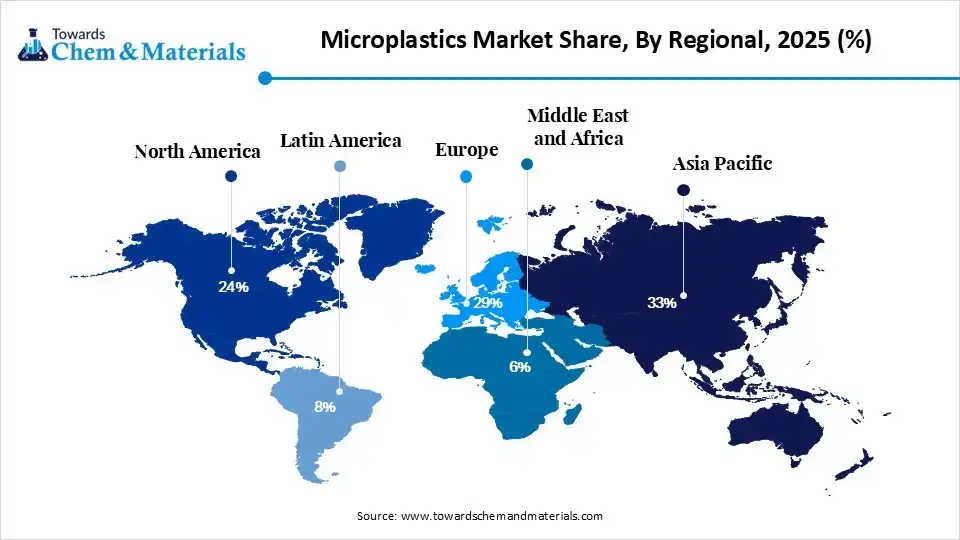

- By region, Asia Pacific dominated the market with the largest share of 33% in 2025 and is expected to grow at the fastest CAGR of 10.20% over the forecast period. The dominance and growth of the region can be attributed to rapid urbanization and industrialization in emerging economies.

- By region, Europe held a market share of 29% in 2025. The growth of the region can be credited to stringent plastic regulations emphasizing microplastic mitigation initiatives.

- By source, the secondary microplastics segment dominated the market with the largest share of 62% in 2025 and is expected to grow at the fastest CAGR of 9.60% over the forecast period. The dominance and growth of the segment can be attributed to the increasing generation of secondary particles.

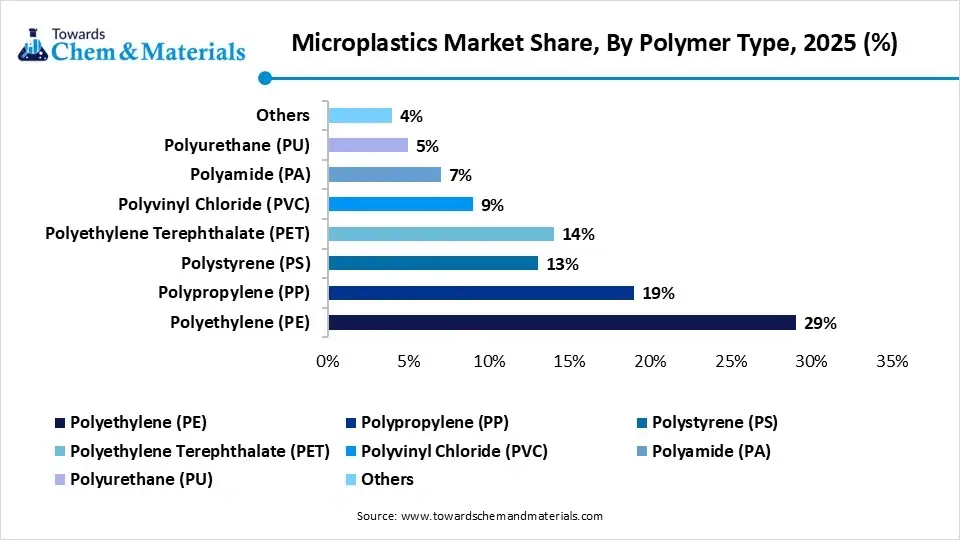

- By polymer type, the polyethylene (PE) segment dominated the market with the largest share of 29% in 2025. The dominance of the segment can be linked to extensive packaging consumption across various industries.

- By polymer type, the polyethylene terephthalate (PET) segment is expected to grow at the fastest CAGR of 8.8% over the forecast period. The growth of the segment can be driven by increasing PET microplastic formation.

- By shape, the fragments segment dominated the market with the largest share of 34% in 2025. The dominance of the segment is owing to the surge in consumer and packaging waste.

- By shape, the fibers segment is expected to grow at the fastest CAGR of 9.4% during the projected period. The growth of the segment is due to the increase in the manufacturing of apparel.

- By size, the 100 µm–500 µm segment dominated the market with the largest share of 33% in 2025. The dominance of the segment can be attributed to the rise in environmental monitoring programs.

- By size, the less than 100 µm segment is expected to grow at the fastest CAGR of 9.5% over the forecast period. The growth of the segment can be credited to growing health concerns.

- By end-use industry, the packaging segment dominated the market with the largest share of 28% in 2025. The dominance of the segment can be linked to increasing e-commerce activity.

- By end-use industry, the textile segment is expected to grow at the fastest CAGR of 9.3% during the study period. The growth of the segment can be driven by the increase in synthetic clothing production.

- By environmental medium, the marine water segment dominated the market with the largest share of 37% in 2025. The dominance of the segment is owing to increasing packaging and fishing activities.

- By environmental medium, the airborne microplastics segment is expected to grow at the fastest CAGR of 10.1% during the projected period. The growth of the segment is due to the growing detection of indoor and outdoor particles.

- By detection & analysis technology, the spectroscopy segment dominated the market with the largest share of 34% in 2025. the dominance of the segment can be attributed to the growing adoption of spectroscopy by research institutions across the globe.

- By detection & analysis technology, the AI-based detection systems segment is expected to grow at the fastest CAGR of 11.2% during the projected period. the growth of the segment can be credited to increasing investments in advanced filtration infrastructure.

- By remediation method, the filtration systems segment dominated the market with the largest share of 36% in 2025. the dominance of the segment can be linked to the increasing deployment of advanced filtration technologies.

- By remediation method, the biological remediation segment is expected to grow at the fastest CAGR of 10.3% during the forecast period. the growth of the segment can be driven by research institutions increasingly developing enzyme-assisted degradation systems.

At a Glance

- Market Estimated Size (2025): USD 5.19 Billion | CAGR (2026–2035): 8.55%

- Market Projected Size (2035): USD 11.79 Billion

- Asia Pacific: largest Market Revenue Share of 49% in 2025.

- Market Estimated Volume (2025): 4.10 Million Tons | Volume CAGR (2026–2035): 7.15%

- Market Projected Volume (2035): 8.18 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,485 per Ton

- Average Selling Price (2025): USD 2,765 per Ton

- Pricing CAGR (2025–2035): 3.19%

Microplastics Market Trends

- Increasing collaboration between different stakeholders, such as non-profit organizations, governments, and corporations, is the latest trend in the market, shaping positive market growth. These partnerships are helpful in the development of more convenient recycling technologies by formulating policies that promote sustainability.

- Many organizations are minimizing their environmental footprint, enhancing their brand image, and fulfilling the eco-conscious expectations of consumers by emphasizing the reuse, repair, and recycling of materials. Business models that prioritize the circular use of resources, such as microplastic recycling, are increasingly gaining momentum.

- Laboratories are transitioning toward automated high-resolution platforms, which is another major trend in the market, shaping positive market growth. Moreover, increasing emphasis on microplastic recycling aims to divert secondary microplastics from landfills.

How Cutting-Edge Technologies Are Revolutionizing the Microplastics Market?

Advanced technologies such as magnetic extraction, AI-driven robotics, and innovative filtration are transforming the market by allowing large-scale, efficient removal and detection. Furthermore, to prevent microplastic formation, researchers are increasingly developing new biodegradable materials and coatings for packaging that improve breakdown properties in natural environments.

Supply Chain Analysis of the Microplastics Market

Feedstock Procurement

It refers to the sourcing, collection, and processing of essential raw materials required to manufacture either conventional microplastics or to create biodegradable/alternative microplastic materials.

- Major Players: Cospheric LLC, Thermo Fisher Scientific

Chemical Synthesis and Processing

It refers to the industrial creation, deliberate design, structural manipulation, and chemical tracking of plastic particles measuring less than 5 millimeters in size.

- Major Players: Bruker Corporation, Shimadzu Corporation

Packaging and Labeling

It includes two distinct, highly technical intersecting industrial domains focused on tracking, identifying, and mitigating microplastic (MP) contamination.

- Major Players: Nestlé, Procter & Gamble, TotalEnergies, Corbion

Regulatory Compliance and Safety Monitoring

It involves the technologies, services, and analytical tools created to detect, quantify, and report microplastic contamination (particles <5mm) to meet government regulations.

- Major Players: PerkinElmer Inc., Horiba Ltd.

Microplastics Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union | Starting 31 May 2026, manufacturers using microplastics under temporary exemptions (e.g., industrial formulations or encapsulated actives) must submit granular, annual emission estimates directly to the European Chemicals Agency (ECHA). |

| United States | Over five progressive states including California, New York, Connecticut, and Illinois have individual policies. State legislatures are passing study bills and extending bans to target secondary microplastics by phasing out packaging and textiles that degrade into microparticles. |

| India | While India lacks a specific, comprehensive regulatory policy targeted explicitly at atmospheric or loose microplastics, it acts indirectly by updating its Plastic Waste Management Rules, mandating strict Extended Producer Responsibility (EPR) compliance and banning single-use plastics under 120 microns. |

Market Dynamics

Drivers

Lower Manufacturing Cost

Recycled microplastic products offer a great revenue stream for industries and help minimize overall manufacturing costs. It also reduces environmental damage as the amount of plastic entering oceans and landfills is significantly decreased through recycling microplastics. In addition, continuous research into recycling technologies is transforming plastic waste into valuable resources, creating significant growth opportunities in construction (building materials) and electronics. Innovations further enable wider adoption of recycled materials.

Restraints

Lack of Standardization

Industry research lacks universally recognized grades and standardized methodology, causing highly inconsistent data collection across laboratories, which is the major factor hindering the growth of the market. Moreover, insufficient feedstock availability and inadequate infrastructure pose significant obstacles to demand. Additionally, the increased costs of these processes relative to conventional recycling methods hamper the economic competitiveness of industry stakeholders.

Opportunities

Growth in Emerging Markets

Developing economies and their increasing populations increase the consumption of plastic products and hence raise plastic waste, which shows a substantial opportunity for the growth of the market in these regions, the increasing product demand from various sectors such as textiles, automotive & transportation, packaging, and consumer goods creates lucrative opportunities for microplastic recycling ventures. Also, to address environmental sustainability, manufacturers in the clean beauty sector are actively seeking organic, abrasive, and exfoliating alternatives to replace synthetic plastic microbeads in facial scrubs and oral care products.

Segmental Insights

Source Insights

The Secondary Microplastics Segment Dominated the Microplastics Market with 62% of Market Share in 2025

The secondary microplastics segment dominated the market with the largest share of 62% in 2025 and is expected to grow at the fastest CAGR of 9.60% over the forecast period. The dominance and growth of the segment can be attributed to the increasing generation of secondary particles across the globe and rapid urbanization in emerging economies. Also, packaging fragmentation boosts environmental accumulation.

Microplastics Market Share, By Source, 2025 (%)

| By Source | Revenue Share, 2025 (%) |

| Primary Microplastics | 38% |

| Secondary Microplastics | 62% |

The primary microplastics segment held the market share of 38% in 2025. The growth of the segment can be credited to the increasing tracking of intentionally produced microplastics and the manufacturing and textile industry generating persistent synthetic particles.

Polymer Type Insights

The Polyethylene (PE) Segment Dominated the Market with 29% of Market Share in 2025

The polyethylene (PE) segment dominated the market with the largest share of 29% in 2025. The dominance of the segment can be linked to the extensive packaging consumption across various industries and the ongoing fragmentation of flexible plastic waste. Recycling inefficiencies sustain environmental accumulation rates.

The polyethylene terephthalate (PET) segment held the market share of 14% in 2025 and is expected to grow at the fastest CAGR of 8.8% over the forecast period. The growth of the segment can be driven by increasing PET microplastic formation due to textile microfiber shedding and the expanding fashion industry across the globe. Beverage packaging waste fuels large-scale environmental dispersion.

Shape Insights

The Fragments Segment Dominated the Market with 34% of Market Share in 2025

The fragments segment dominated the market with the largest share of 34% in 2025. The dominance of the segment is owing to the surge in consumer and packaging waste, coupled with the rapid degradation of large plastic products. In addition, environmental weathering boosts formation in oceans and soils.

Microplastics Market Share, By Shape, 2025 (%)

| By Shape | Revenue Share, 2025 (%) |

| Fragments | 34% |

| Fibers | 27% |

| Beads | 11% |

| Films | 12% |

| Foams | 9% |

| Granules | 7% |

The fibers segment held the market share of 27% in 2025 and is expected to grow at the fastest CAGR of 9.4% during the projected period. The growth of the segment is due to an increase in the manufacturing of apparel and an increase in synthetic textile washing, which releases significant microfiber volume in the air.

Size Insights

The 100 µm–500 µm Segment Dominated the Market with 33% of Market Share in 2025

The 100 µm–500 µm segment dominated the market with the largest share of 33% in 2025. The dominance of the segment can be attributed to the rise in environmental monitoring programs focusing on mid-sized particles and the growing failure rate of water systems to capture these particles completely.

Microplastics Market Share, By Size, 2025 (%)

| By Size | Revenue Share, 2025 (%) |

| Less than 100 µm | 21% |

| 100 µm–500 µm | 33% |

| 500 µm–1 mm | 26% |

| 1 mm–5 mm | 20% |

The less than 100 µm segment held the market share of 21% in 2025 and is expected to grow at the fastest CAGR of 9.5% over the forecast period. The growth of the segment can be credited to the growing health concerns surrounding inhalation and ingestion, along with the growing use of advanced analytical tools.

End-Use Industry Insights

The Packaging Segment Dominated the Market with 28% of Market Share in 2025

The packaging segment dominated the market with the largest share of 28% in 2025. The dominance of the segment can be linked to the increasing e-commerce activity in flexible packaging and increasing environmental leakage rates. Single-use plastic packaging remains the largest source of microplastic generation.

Microplastics Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Packaging | 28% |

| Textile | 22% |

| Automotive | 14% |

| Construction | 11% |

| Personal Care & Cosmetics | 8% |

| Marine & Fisheries | 7% |

| Electronics | 6% |

| Healthcare | 4% |

The textile segment held the market share of 22% in 2025 and is expected to grow at the fastest CAGR of 9.3% during the study period. The growth of the segment can be driven by an increase in synthetic clothing production and rapid fast fashion consumption across the globe. Textile wastewater management remains insufficient in many regions.

Environmental Medium Insights

The Marine Water Segment Dominated the Microplastics Market with 37% of Market Share in 2025

The marine water segment dominated the market with the largest share of 37% in 2025. The dominance of the segment is owing to the increasing packaging and fishing activities, facilitating ocean pollution, and ongoing global marine programs expanding contamination assessments. River discharge transports large microplastic volumes into marine ecosystems.

Microplastics Market Share, By Environmental Medium, 2025 (%)

| By Environmental Medium | Revenue Share, 2025 (%) |

| Marine Water | 37% |

| Freshwater | 22% |

| Soil & Sediment | 18% |

| Airborne Microplastics | 11% |

| Wastewater Systems | 12% |

The airborne microplastics segment held the market share of 11% in 2025 and is expected to grow at the fastest CAGR of 10.1% during the projected period. The growth of the segment is due to the growing detection of indoor and outdoor particle detection, coupled with the surge in health concerns. Textile fibers further increase atmospheric contamination levels.

Detection & Analysis Technology Insights

The Spectroscopy Segment Dominated the Market with 34% of Market Share in 2025

The spectroscopy segment dominated the market with the largest share of 34% in 2025. The dominance of the segment can be attributed to the growing adoption of spectroscopy by research institutions across the globe, and FTIR and Raman technologies improving precise polymer identification capabilities.

Microplastics Market Share, By Detection & Analysis Technology, 2025 (%)

| By Detection & Analysis Technology | Revenue Share, 2025 (%) |

| Marine Water | 37% |

| Freshwater | 22% |

| Soil & Sediment | 18% |

| Airborne Microplastics | 11% |

| Wastewater Systems | 12% |

The AI-based detection systems segment held the market share of 14% in 2025 and is expected to grow at the fastest CAGR of 11.2% during the projected period. The growth of the segment can be credited to the increasing investments in advanced filtration infrastructure and the surge in wastewater plants. Treatment inefficiencies allow persistent particles to enter pathways.

Remediation Method Insights

The Filtration Systems Segment Dominated the Market with 36% of Market Share in 2025

The filtration systems segment dominated the market with the largest share of 36% in 2025. The dominance of the segment can be linked to the increasing deployment of advanced filtration technologies and regulatory standards, boosting filtration infrastructure growth.

Microplastics Market Share, By Remediation Method, 2025 (%)

| By Remediation Method | Revenue Share, 2025 (%) |

| Filtration Systems | 36% |

| Chemical Treatment | 18% |

| Biological Remediation | 16% |

| Electrocoagulation | 14% |

| Adsorption Technology | 16% |

The biological remediation segment held the market share of 16% in 2025 and is expected to grow at the fastest CAGR of 10.3% during the forecast period. The growth of the segment can be driven by research institutions increasingly developing enzyme-assisted degradation systems, along with a surge in investment for suitable remediation solutions.

Regional Insights

How did Asia Pacific Dominate the Microplastics Market in 2025?

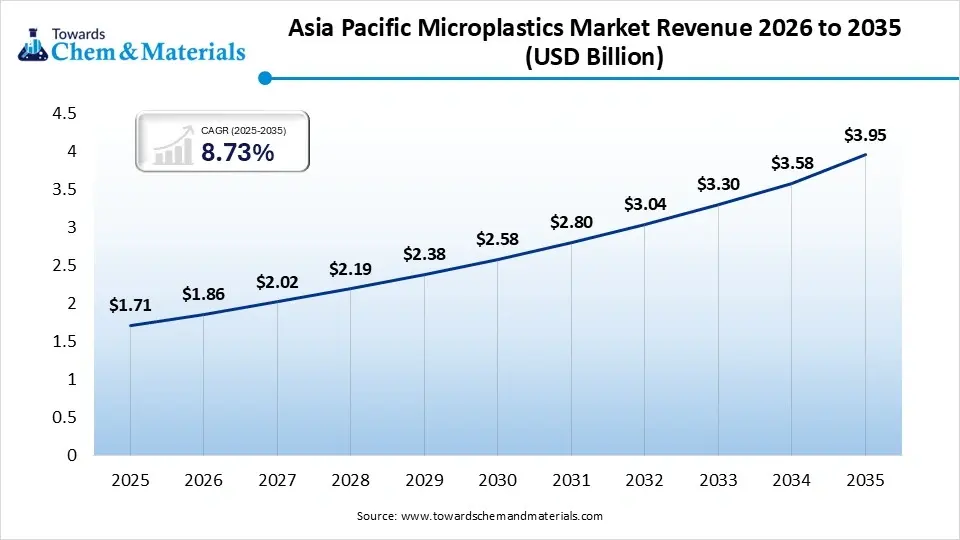

The Asia Pacific microplastics market size was estimated at USD 1.71 billion in 2025 and is projected to reach USD 3.95 billion by 2035, growing at a CAGR of 8.73% from 2026 to 2035. The dominance and growth of the region can be attributed to the rapid urbanization and industrialization in emerging economies, along with the expanding textile and packaging sectors. In addition, increasing public awareness regarding the health and environmental impacts of microplastics is fuelling research and funding for detection technology.

")

China Microplastics Market Trends

In the Asia Pacific, China dominated the market owing to the ongoing urbanisation and industrial growth, especially in eastern coastal regions, along with the surge in awareness regarding environmental and health impacts. Also, high consumption of packaged goods and e-commerce growth are contributing to the increase in plastic in urban areas.

Europe held the market share of 29% in 2025. The growth of the region can be credited to the stringent plastic regulations emphasizing microplastic mitigation initiatives and ongoing innovation in remediation technologies. Furthermore, increasing consumer awareness regarding plastic pollution in food and health is prompting market players to adopt sustainable practices.

Germany Microplastics Market Trends

The growth of the market in the country is due to the country's robust g R&D infrastructure, encouraging the development of innovative microscopic and spectroscopic techniques for detecting microplastics. Moreover, industrial facilities and water treatment plants are rapidly adopting cutting-edge filtration systems to remove microplastics.

Recent Development

- In March 2026, Finnish startup Elea & Lili emerged from stealth mode, securing €2.5 million ($2.9 million) in funding to launch a sustainable cellulose alternative to fossil-based polymers. The company's proprietary technology replaces non-biodegradable superabsorbent polymers (SAPs), which are traditionally utilized in the diaper industry for fluid retention.

Microplastics Market Companies

- Lamberti S.p.A.: Lamberti S.p.A. is a significant player in the global microplastics market, specifically focusing on the development and production of specialized polymer microbeads (also known as microspheres) used as functional additives across various industries.

- Cospheric LLC: Cospheric LLC is a California-based manufacturer and global supplier specializing in high-precision, spherical microparticles, including microspheres, nanospheres, and beads.

Companies in the Microplastics Market

- Applied Microspheres GmbH

- EPRUI Biotech Co., Ltd.

- Nanjing Chemical Material Corp.

- Bangs Laboratories, Inc.

- Polysciences, Inc.

Microplastics Market Segments Covered in the Report

By Source

- Primary Microplastics

- Microbeads

- Industrial Pellets

- Synthetic Fibers

- Paint & Coating Particles

- Secondary Microplastics

- Packaging Waste Degradation

- Tire Wear Particles

- Textile Fragmentation

- Fishing Gear Degradation

- Construction Material Degradation

By Polymer Type

- Polyethylene (PE)

- LDPE

- HDPE

- Polypropylene (PP)

- Polystyrene (PS)

- Expanded PS

- General Purpose PS

- Polyethylene Terephthalate (PET)

- Polyvinyl Chloride (PVC)

- Polyamide (PA)

- Polyurethane (PU)

- Others

By Shape

- Fragments

- Fibers

- Beads

- Films

- Foams

- Granules

By Size

- Less than 100 µm

- 100 µm–500 µm

- 500 µm–1 mm

- 1 mm–5 mm

By End-Use Industry

- Packaging

- Textile

- Automotive

- Construction

- Personal Care & Cosmetics

- Marine & Fisheries

- Electronics

- Healthcare

By Environmental Medium

- Marine Water

- Freshwater

- Soil & Sediment

- Airborne Microplastics

- Wastewater Systems

By Detection & Analysis Technology

- Spectroscopy

- FTIR

- Raman Spectroscopy

- Microscopy

- Optical Microscopy

- Electron Microscopy

- Thermal Analysis

- Chromatography

- AI-Based Detection Systems

By Remediation Method

- Filtration Systems

- Chemical Treatment

- Biological Remediation

- Electrocoagulation

- Adsorption Technology

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)