Content

What is the Current U.S. Nonwoven Fabrics Market Size and Share?

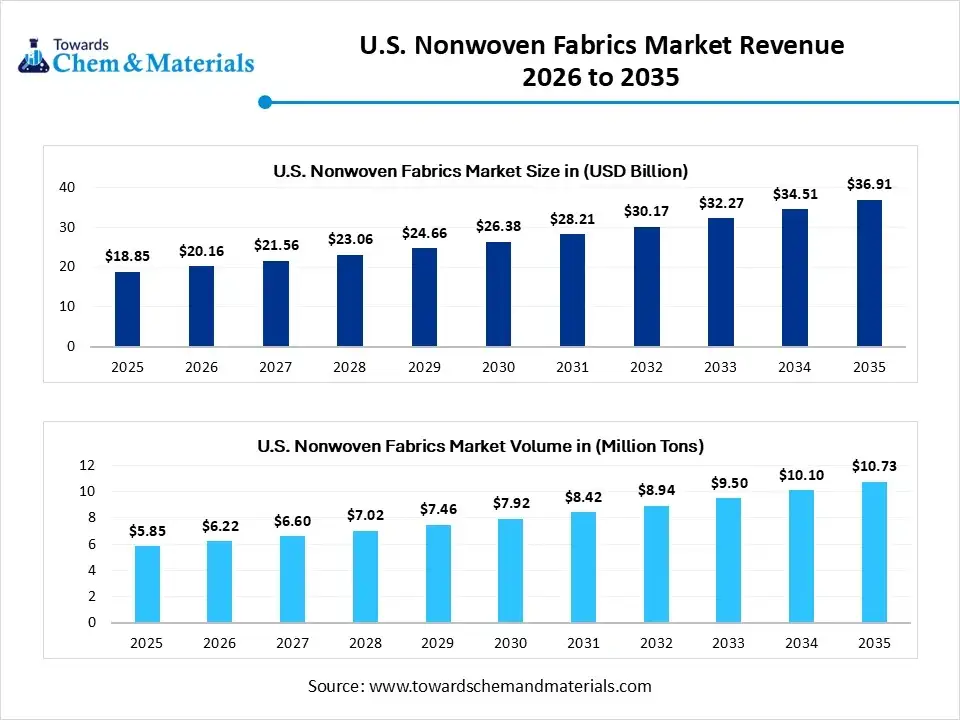

The U.S. nonwoven fabrics market size was valued at USD 18.85 billion in 2025, is estimated to reach USD 20.16 billion in 2026, and is projected to reach USD 36.91 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.95% over the forecast period from 2026 to 2035. In terms of volume, the U.S. nonwoven fabrics market is projected to grow from 5.85 million tons in 2025 to 10.73 million tons by 2035. growing at a CAGR of 6.25% from 2026 to 2035.The market growth is driven by the increasing demand for personal hygiene and personal care, as well as the growing needs of the healthcare sector, which in turn drives market expansion through increased adoption across various industries.

Key Takeaways

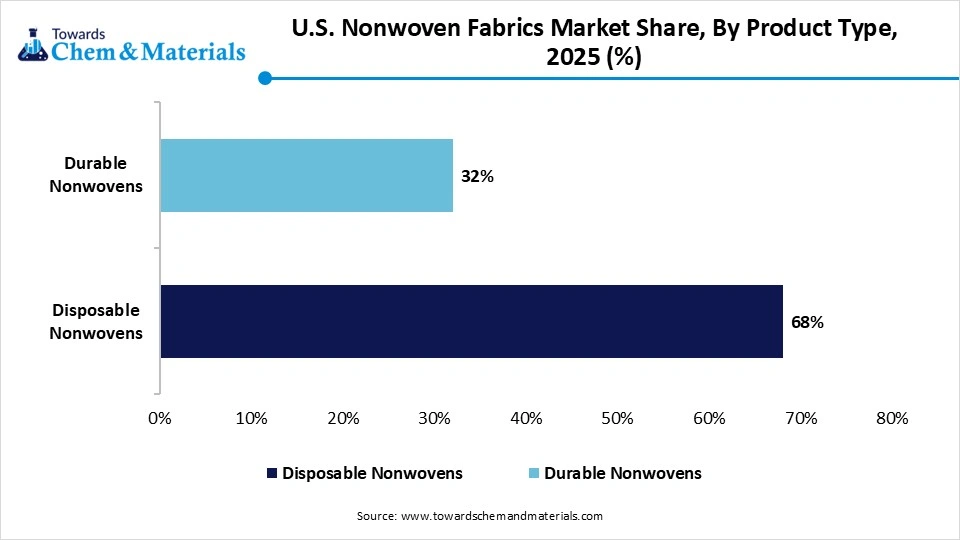

- By product type, the disposable nonwovens segment dominated the market in 2025, and the segment is expected to grow significantly in the market during the forecast period. The disposable nonwovens segment held approximately 68% share in the market in 2025. Growing demand for diapers, feminine hygiene products, surgical drapes, and face masks continues to fuel this segment.

- By product type, the durable nonwovens segment is expected to experience notable growth in the market. Sustainability efforts, including the use of recycled fibers and bio-based materials, are gaining traction, aligning with environmental goals.

- By technology, the spunbond segment dominated the market in 2025. The spunbond segment held approximately 37% share in the market in 2025. They are widely used in hygiene products, medical gowns, filtration systems, and agricultural coverings.

- By technology, the meltblown segment is expected to grow in the forecast period. Their ultrafine fiber structure provides superior filtration efficiency, making them critical in healthcare and environmental protection applications.

- By material, the polypropylene segment dominated the market in 2025. The polypropylene segment held approximately 43% share in the market in 2025. It is a preferred choice for hygiene products, medical supplies, packaging, and filtration applications.

- By material, the biocomposites segment is expected to grow in the forecast period. Their reduced environmental footprint aligns with rising consumer awareness and stricter regulatory standards.

- By end-use industry, the hygiene segment dominated the market in 2025. The hygiene segment held approximately 31% share in the market in 2025. Rising awareness of personal hygiene, coupled with an aging population, sustains this demand.

- By end-use industry, the medical segment is expected to grow in the forecast period. The demand surged with the need for surgical masks, gowns, drapes, and sterilization wraps during the pandemic and continues to remain high.

At a Glance

- Market Estimated Size (2025): USD 18.85 Billion | CAGR (2026–2035): 6.95%

- Market Projected Size (2035): USD 36.91 Billion

- Market Volume (2025): 5.85 Million Tons| Volume CAGR (2026–2035): 6.25%

- Market Projected Volume (2035): 10.73 Million Tons

- Pricing Data (2025):

- Average Manufacturing Price (2025): USD 2,750 per Ton

- Average Selling Price (2025): USD 3,495 per Ton

- Pricing CAGR (2026–2035): 4.19%

Market Overview

What Is The Significance Of The U.S. Nonwoven Fabrics Market?

The growth of the market is driven by the rising demand for disposable and durable products across multiple sectors. Nonwoven fabrics are engineered fabrics made from fibers bonded together by chemical, mechanical, heat, or solvent treatment, rather than weaving or knitting. They are used across hygiene, medical, automotive, construction, filtration, packaging, and industrial applications. These applications, due to their properties and benefits associated with the product, mark its significance in the U.S. market, contributing to its growth.

What Are The Key Growth Drivers That Support The Growth Of the U.S. Nonwoven Fabrics Market?

The growth of the US nonwoven fabrics is driven by the increasing demand from industries, especially hygiene and medical sectors, due to varied applications, with increased awareness, which has boosted the demand for nonwoven products such as baby diapers, feminine care items, adult incontinence products, and medical supplies like gowns and masks. The technological advancements, such as manufacturing innovations and smart textiles with properties like antimicrobial properties, moisture resistance, and temperature control, also help expand the applications in various industries.

Market Trends

- Growing Demand for Hygiene Products: The increasing awareness of personal hygiene and health, especially post-pandemic, drives the consumption of disposable nonwoven hygiene products such as diapers, wipes, and feminine hygiene items.

- Focus on Sustainability: There is a strong shift towards environmentally friendly nonwoven fabrics, including those made from recycled materials and biodegradable polymers, to reduce the environmental impact of synthetic fibers.

- Advancements in Technology: Innovations in manufacturing technologies like spun bond and melt-blown, along with automation and Artificial Intelligence in production, enhance efficiency, product quality, and cost-effectiveness.

- Demand for High-Performance Fabrics: Industries are seeking nonwoven materials with improved properties such as increased strength, better filtration efficiency, and enhanced moisture resistance.

- Supply Chain Adjustments: Recent tariff changes are causing manufacturers to invest more in domestic production and forge strategic partnerships to build supply chain resilience.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 20.16 Billion / 36.91 Million Tons |

| Expected Size by 2035 | USD 36.91 Billion/ 10.73 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 6.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Product Type, By Technology, By Material, By End-Use Industry |

| Key Companies Profiled | Berry Global Inc., Freudenberg Group, DuPont, Kimberly-Clark Worldwide, Inc., Ahlstrom-Munksjö, Glatfelter Corporation, Lydall Inc., Suominen Corporation, Johns Manville, PFNonwovens, Fitesa S.A., TWE Group, Sandler AG, Avgol Nonwoven Industries, Fibertex Nonwovens, Mogul Nonwoven Technologies, Toray Industries, Mitsui Chemicals, Berry Superfos, Kimberly-Clark Professional |

Market Opportunity

The Focus On Sustainability Solutions

The market is shifting towards eco-friendly solutions, creating opportunities for bio-based and recyclable nonwoven materials to meet consumer and regulatory demands for sustainability. Nonwovens are used for various applications in these sectors, including vehicle parts, noise insulation, and building materials, with growing opportunities for lightweight, high-performance fabrics.

Investments in new manufacturing technologies, such as meltblown and spunbond, and the adoption of AI and automation, improve efficiency and product quality, opening new market avenues.

Market Challenge

The High Raw Material Cost And Environmental Concerns

Key challenges in the U.S. nonwoven fabrics market include unstable raw material costs tied to crude oil prices, a need for major investments in recycling tech to address environmental concerns, and tough environmental regulations that promote alternatives to plastic-based nonwovens.

Manufacturers face higher production costs compared to traditional textiles and must innovate to boost efficiency and create sustainable, biodegradable options.

Segmental Insights

Product Type Insights

Which Product Type Segment Dominated The U.S. Nonwoven Fabrics Market In 2025?

The disposable nonwovens segment dominated the market in 2025. This is due to their widespread use in personal hygiene products, medical applications, and single-use items. They are lightweight, cost-effective, and designed for short-term use, ensuring convenience and safety. Post-pandemic awareness regarding hygiene has further accelerated adoption, while ongoing innovations in biodegradable and eco-friendly disposable nonwovens are expanding opportunities in healthcare and consumer applications.

")

The durable nonwovens segment is expected to experience notable growth in the market during the forecast period. Durable nonwoven fabrics are designed for repeated or long-term use, finding applications in automotive, upholstery, filtration, and protective clothing. In the US, industries such as construction and transportation are driving demand for durable nonwovens due to their strength, resilience, and cost-efficiency compared to traditional materials. Increasing use in industrial wipes, geotextiles, and home furnishing products is also supporting growth.

U.S. Nonwoven Fabrics Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Disposable Nonwovens | 68% |

| Durable Nonwovens | 32% |

Technology Insights

How Did The Spunbond Segment Dominate The U.S. Nonwoven Fabrics Market In 2025?

The spunbond segment dominated the market in 2025. Spunbond nonwoven fabrics hold a significant share in the U.S. market due to their durability, versatility, and affordability. The technology offers excellent tensile strength, uniformity, and lightweight properties, making it suitable for both disposable and durable applications. Continuous advancements in polymer processing and eco-friendly production methods are further enhancing the adoption of spunbond fabrics, ensuring their critical role across multiple US end-use industries.

The meltblown segment expects significant growth in the U.S. nonwoven fabrics market during the forecast period. Meltblown nonwoven fabrics are essential in applications requiring fine filtration and barrier properties. In the US, this segment gained rapid attention during the COVID-19 pandemic, particularly for N95 respirators, surgical masks, and air filtration products. Beyond medical use, meltblown fabrics are expanding into oil absorption, insulation, and battery separator markets. Investments in domestic meltblown production continue to grow, reducing supply chain vulnerabilities.

U.S. Nonwoven Fabrics Market Share, By Technology, 2025 (%)

| By Technology | Revenue Share, 2025 (%) |

| Spunbond | 37% |

| Meltblown | 18% |

| Spunlace (Hydroentanglement) | 16% |

| Airlaid | 12% |

| Wetlaid | 8% |

| Needlepunched | 9% |

Material Insights

Which Material Segment Dominated The U.S. Nonwoven Fabrics Market In 2025?

The polypropylene segment dominated the market in 2025. Polypropylene remains the most widely used material in US nonwoven fabric production due to its affordability, versatility, and excellent performance characteristics. The material offers lightweight, durable, and chemical-resistant properties, which support its extensive use in disposable products. With growing demand for sustainable practices, the market is also witnessing advancements in recyclable and modified polypropylene-based nonwovens, enhancing their relevance across consumer and industrial applications.

The biocomposites segment expects significant growth in the U.S. nonwoven fabrics market during the forecast period. Bio-composite nonwoven fabrics are emerging strongly in the market as industries shift toward sustainability and eco-friendly alternatives. Derived from natural fibers and biodegradable polymers, they are increasingly used in packaging, hygiene, automotive interiors, and medical applications. Although bio-composites currently represent a smaller share compared to polypropylene, technological advancements and increasing corporate sustainability commitments are expected to significantly boost their adoption in the coming years.

U.S. Nonwoven Fabrics Market Share, By Material, 2025 (%)

| By Material | Revenue Share, 2025 (%) |

| Polypropylene | 43% |

| Polyester | 21% |

| Polyethylene | 11% |

| Wood Pulp | 11% |

| Cotton | 6% |

| Biocomposites | 8% |

End-Use Industry Insights

How Did The Hygiene Segment Dominate The U.S. Nonwoven Fabrics Market In 2025?

The hygiene segment dominated the market in 2025. The hygiene sector is the largest consumer of nonwoven fabrics in the US, driven by strong demand for baby diapers, feminine hygiene products, adult incontinence solutions, and wipes. Post-pandemic hygiene practices and the expansion of premium, skin-friendly nonwoven products further support market growth. Innovations in absorbency, softness, and biodegradability are also reshaping the hygiene nonwovens landscape, making it a vital driver of long-term market expansion.

The medical segment expects significant growth in the U.S. nonwoven fabrics market during the forecast period. Medical applications are another critical end-use sector for nonwoven fabrics in the US. Nonwoven fabrics are valued for their barrier protection, breathability, and disposability, making them essential for infection control. The growing emphasis on healthcare safety, rising surgical procedures, and the development of antimicrobial and biodegradable medical nonwovens are boosting the sector’s significance in the market.

U.S. Nonwoven Fabrics Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Hygiene | 31% |

| Medical | 20% |

| Automotive | 12% |

| Construction | 11% |

| Filtration | 10% |

| Packaging | 6% |

| Agriculture | 4% |

| Industrial | 6% |

U.S. Nonwoven Fabrics Market Value Chain Analysis

- Chemical Synthesis and Processing: The nonwoven fabrics are synthesised and processed through web formation, bonding, and finishing.

- Key players: Magnera Corporation, Kimberly-Clark Corporation, DuPont de Nemours, Inc.

- Quality Testing and Certification: The nonwoven fabrics require OEKO-TEX® Standard 100, CPSIA (Consumer Product Safety Improvement Act), and FDA approval certification.

- Key players: ASTM International, AATCC (American Association of Textile Chemists and Colorists), and UL Solutions

- Distribution to Industrial Users: The nonwoven fabrics are distributed to the packaging, automotive, electronics, and construction industries.

- Key players: Berry Global, Ahlstrom, Suominen Corporation, and Freudenberg Group.

Recent Developments

- In April 2025, Braskem and Fitesa, the largest producer of polyolefins in America and a global market leader, announced the launch of Spunbond nonwovens, which are made from biobased high-density polyethylene with special applications.(Source: www.braskem.com.br)

- In April 2025, AGAGC Chemicals Americas, Inc. (AGCCA) introduced the launch of Non-Fluorinate Coating Technology, which helps in providing the consumer with high-performance, sustainable alternatives to fluorinated repellent technologies.(Source: www.nonwovens-industry.com)

Top Companies

- Berry Global Inc.

- Freudenberg Group

- DuPont

- Kimberly-Clark Worldwide, Inc.

- Ahlstrom-Munksjö

- Glatfelter Corporation

- Lydall Inc.

- Suominen Corporation

- Johns Manville

- PFNonwovens

- Fitesa S.A.

- TWE Group

- Sandler AG

- Avgol Nonwoven Industries

- Fibertex Nonwovens

- Mogul Nonwoven Technologies

- Toray Industries

- Mitsui Chemicals

- Berry Superfos

- Kimberly-Clark Professional

Segments Covered

By Product Type

- Disposable Nonwovens

- Hygiene Products

- Medical Products

- Wipes

- Durable Nonwovens

- Automotive Applications

- Construction Applications

- Industrial Applications

By Technology

- Spunbond

- Meltblown

- Spunlace (Hydroentanglement)

- Airlaid

- Wetlaid

- Needlepunched

By Material

- Polypropylene

- Polyester

- Polyethylene

- Wood Pulp

- Cotton

- Biocomposites

- Hemp

- Jute

By End-Use Industry

- Hygiene

- Diapers

- Feminine Hygiene

- Adult Incontinence

- Medical

- Surgical Gowns

- Face Masks

- Wound Care

- Automotive

- Acoustic & Thermal Insulation

- Upholstery

- Construction

- Roofing

- Insulation

- Geotextiles

- Filtration

- Air

- Water

- Oil

- Packaging

- Food

- Industrial

- Protective

- Agriculture

- Crop Covers

- Mulch Films

- Greenhouse Liners

- Industrial

- Cleaning Materials

- Absorbents

List of Figures

- U.S. Nonwoven Fabrics Market Size and Forecast (2025-2034) - Total Market: USD 12.14 Billion in 2025 to USD 19.01 Billion in 2034, CAGR 5.11%.

- Market Share by Product Type (2024) - Disposable Nonwovens (60%), Durable Nonwovens (40%).

- Market Share by Technology (2024) - Spunbond (45%), Meltblown (30%), Other Technologies (Spunlace, Airlaid, Needlepunched) (25%).

- Market Share by Material (2024) - Polypropylene (40%), Polyester (25%), Polyethylene (10%), Wood Pulp (5%), Cotton (10%), Biocomposites (Hemp, Jute) (10%).

- Market Share by End-Use Industry (2024) - Hygiene (50%), Medical (20%), Automotive (10%), Construction (10%), Filtration (5%), Packaging (3%), Agriculture (1%), Industrial (1%).

- Growth in Disposable Nonwoven Products Segment (2025-2034) - Disposable Nonwovens (5.8% CAGR).

- Growth in Durable Nonwoven Products Segment (2025-2034) - Durable Nonwovens (5.2% CAGR).

- Market Share by Technology: Spunbond vs. Meltblown (2025) - Spunbond (48%), Meltblown (35%), Other (17%).

- Market Share by End-Use Industry (2025-2034) - Hygiene Products (55%), Medical Products (25%), Automotive Applications (10%), Industrial Applications (10%).

- Growth of Biocomposites Segment (2025-2034) - Biocomposites (7.5% CAGR).

List of Tables

- U.S. Nonwoven Fabrics Market Size and Forecast (2025-2034) - Total Market Value and CAGR.

- Market Share by Product Type (2024) - Disposable Nonwovens (60%), Durable Nonwovens (40%).

- Market Share by Technology (2024) - Spunbond (45%), Meltblown (30%), Other Technologies (Spunlace, Airlaid, Needlepunched) (25%).

- Market Share by Material (2024) - Polypropylene (40%), Polyester (25%), Polyethylene (10%), Wood Pulp (5%), Cotton (10%), Biocomposites (Hemp, Jute) (10%).

- Market Share by End-Use Industry (2024) - Hygiene (50%), Medical (20%), Automotive (10%), Construction (10%), Filtration (5%), Packaging (3%), Agriculture (1%), Industrial (1%).

- Disposable Nonwovens Segment Growth (2025-2034) - Hygiene Products (5.8% CAGR), Medical Products (5.2% CAGR).

- Durable Nonwovens Segment Growth (2025-2034) - Automotive Applications (5.0% CAGR), Industrial Applications (5.0% CAGR), Construction Applications (5.5% CAGR).

- Technology Insights: Spunbond vs. Meltblown (2025) - Spunbond (48%), Meltblown (35%), Other (17%).

- Material Segment Growth (2025-2034) - Polypropylene (45%), Biocomposites (25%), Polyester and Other Materials (30%).

- End-Use Industry Growth Trends (2025-2034) - Hygiene (55%), Medical (25%), Automotive (15%), Other Industries (5%).

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (3)