Content

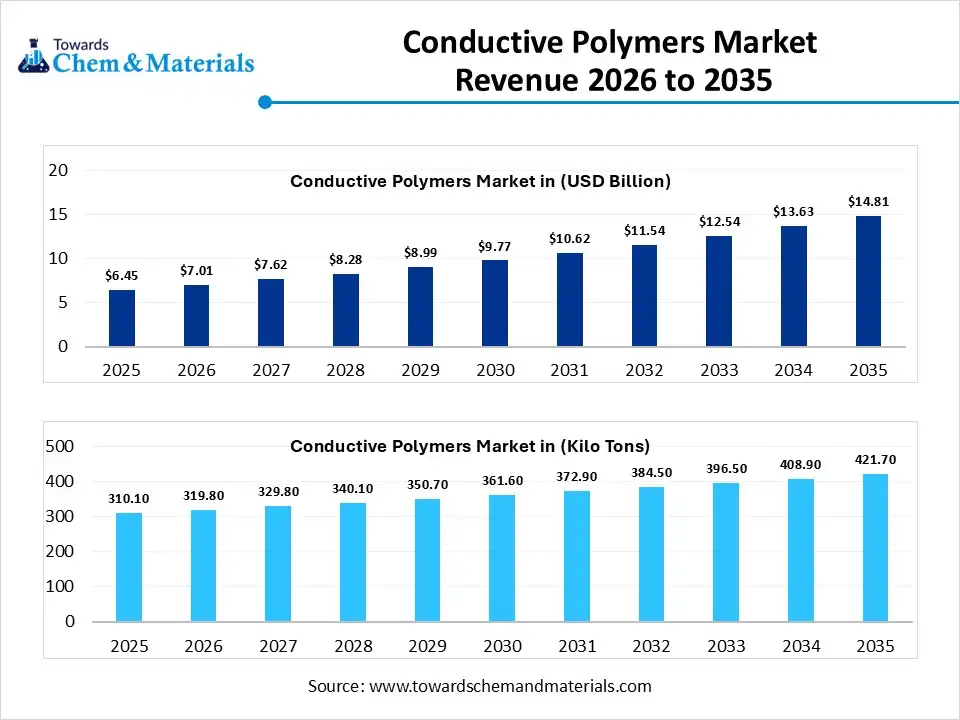

Conductive polymers market Size and Volume Forecast

- Market Estimated Size (2025): USD 8.95 Billion | CAGR (2026–2035): 10.75%

- Market Projected Size (2035): USD 24.85 Billion

- Market Volume (2025): 2.11 Million Tons | Volume CAGR (2026–2035):9.65%

- Market Projected Volume (2035): 5.30 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 6,210/Ton

- Average Selling Price: USD 8,160/Ton

- Pricing CAGR (2025–2035): 4.33%

The global conductive polymers market was valued at USD 8.95 billion in 2025, is estimated to reach USD 9.91 billion in 2026, and is projected to reach USD 24.85 billion by 2035, growing at a CAGR of 10.75% from 2026 to 2035. In terms of volume, the conductive polymers market is projected to grow from 2.11 million tons in 2025 to 5.3 million tons by 2035. growing at a CAGR of 9.65% from 2026 to 2035. The market encompasses the manufacturing and sale of specialized organic materials that involve the processing ease of plastics with the electrical conductivity of metals. It includes s intrinsically conducting polymers (ICPs) such as PEDOT and polyaniline used in batteries, electronics, sensors, and shielding, generally called electroactive polymers.

Key Takeaways

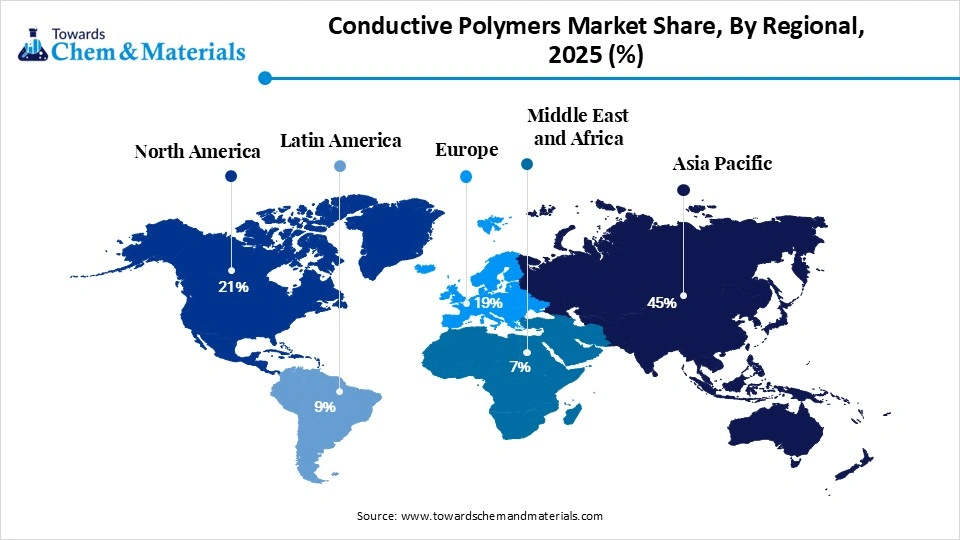

- By region, Asia Pacific dominated the market with the largest share of 45% in 2025.

- By region, Middle East & Africa held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 11.90 % over the forecast period.

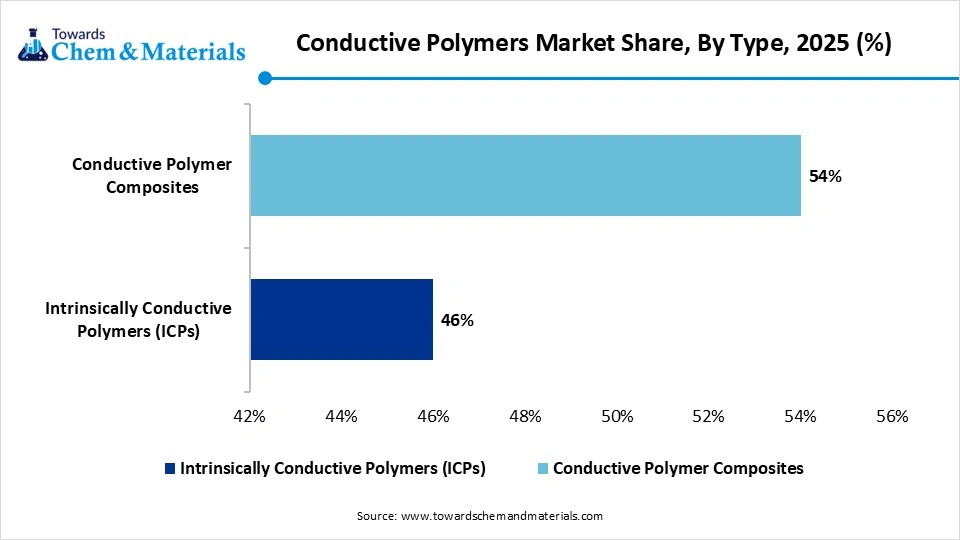

- By type, the intrinsically conductive polymers (ICPs) segment dominated the market with the largest share of 46% in 2025.

- By type, the conductive polymer composites are expected to grow at the fastest CAGR of 10.10% over the forecast period.

- By conductivity mechanism, the electronic conductive polymers segment dominated the market with the largest share of 63% in 2025.

- By conductivity mechanism, the ionic conductive polymers segment is expected to grow at the fastest CAGR of 11.40% over the forecast period.

- By application, the antistatic packaging segment dominated the market with the largest share of 18% in 2025.

- By application, the batteries segment is expected to grow at the fastest CAGR of 12.30% over the projected period.

- By end-use industry, the electrical & electronics segment dominated the market with the largest share of 34% in 2025.

- By end-use industry, the healthcare segment is expected to grow at the fastest CAGR of 12.10% during the projected period.

- By form, the films segment dominated the market with the largest share of 29% in 2025.

- By form, the inks segment is expected to grow at the fastest CAGR of 12.40% during the study period.

Conductive Polymers Market Trends

- Growing utilisation of lightweight materials is the latest trend in the market, shaping positive market growth. A surge in awareness towards enhancements in fuel economy is anticipated to support the usage of ABS and PPS in wiring systems. These materials are generally utilized in the form of conducting materials.

- The demand for conductive polymers is expected to increase owing to their extensive deployment in the electronics sector, as they have low thermal conductivity and the ability to offer exceptional thermal insulation. Also, these polymers are installed in lasers used in the screens of mobile phones and televisions.

- Growing demand for advanced electronic devices is another major trend in the market, driving market growth. With the ongoing evolution of technology and the growing consumer preference for lightweight, smaller, and high-performance electronic devices, there is an increasing demand for conductive polymers that give improved flexibility and cost-effectiveness.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 9.91 Billion / 2.31 Million Tons |

| Expected Size and Volume by 2035 | USD 24.85 Billion / 5.3 Million Tons |

| Growth Rate from 2026 to 2035 | CAGR 10.75% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia-Pacific |

| Segment Covered | By Type, By Conductivity Mechanism, By Application, By End-Use Industry, By Form and By Regions |

| Key companies profiled | SABIC, PolyOne Corporation, Lehmann & Voss & Co., RTP Company, Parker Hannifin, Sumitomo Chemical, Premix Oy, Heraeus Group, The Lubrizol Corporation, Covestro |

How Cutting-Edge Technologies Are Revolutionizing the Conductive Polymers Market?

Advanced technologies are transforming the market by improving conductivity, flexibility, and processability for high-tech applications, fuelled by advancements in nanotechnology and 3D printing. Furthermore, conductive polymers are increasing efficiency in supercapacitors, organic solar cells, and lithium-ion batteries, promoting the adoption of renewable energy.

Supply Chain Analysis of the Conductive Polymers Market

Feedstock Procurement

It involves sourcing of the raw materials, monomers, and specialized conductive fillers necessary to manufacture conductive polymer composites (CPCs) and conductive polymers (ICPs).

- Major Players: Heraeus Group, Agfa-Gevaert NV

Chemical Synthesis and Processing

It refers to the industrial production techniques used to create conductive polymer chains and turn them into usable products like coatings, films, and fibers that can conduct electricity.

- Major Players: Solvay SA,3M Company

Packaging and Labelling

It refers to the use of functional polymers that offer crucial protective and electrical properties to packaging materials. Conductive polymers such as Polypyrrole (PPy) and PEDOT: PSS are used to create smart and protective packaging.

- Major Players: SABIC, Avient Corporation

Regulatory Compliance and Safety Monitoring

It refers to the strict adherence to chemical safety standards, environmental regulations, and industry-associated performance protocols for conducting plastics, coatings, and adhesives.

- Major Players: BASF SE, SABIC

Conductive Polymers Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union (EU) | REACH Regulation (EC) No 1907/2006: In 2023, updated mandates required the registration and evaluation of chemicals, including conductive polymers, to ensure human and environmental safety. Manufacturers must provide detailed safety assessments and risk management procedures. |

| United States | TSCA (Toxic Substances Control Act): Managed by the EPA, this regulation governs the introduction of new or existing chemicals. Conductive polymers must be listed on the TSCA Inventory for commercial use. |

| Asia-Pacific | Emerging economies like China and India have an increasing "regulatory inclination" toward promoting Foreign Direct Investment (FDI) to bolster local manufacturing and R&D for conductive materials |

Market Dynamics

Driver

Expanding Electronic Industry

The market is witnessing a surge in demand for electronic devices due to their extensive deployment in electronics as they hold much lower thermal conductivity and offer exceptional thermal insulation. These create better safety for electronic products.

Restraint

High Production Costs

The high manufacturing costs associated with conductive polymers are the major trend in the market, hindering market expansion. Despite their beneficial properties, the manufacturing processes for conductive polymers can be expensive and complex, which can limit the extensive adoption of conductive polymers.

Opportunity

Increasing Emphasis on Energy Storage Solutions

The global shift towards renewable energy and the growing need for r energy storage solutions are fuelling the adoption of f conductive polymers in capacitors and batteries. Furthermore, there is an increasing demand for high-performance and efficient energy storage devices, creating lucrative opportunities in the market in the near future.

Segmental Insights

Type Insights

The Intrinsically Conductive Polymers (ICPs) Segment Dominated the Market with 46% of Market Share in 2025

The intrinsically conductive polymers (ICPs) segment dominated the market with the largest share of 46% in 2025. The dominance of the segment can be attributed to its growing use in sensors and capacitors, along with its high flexibility and conductivity. Also, continuous innovations enhance performance further.

The conductive polymer composites segment held the market share of 54% in 2025 and is expected to grow at the fastest CAGR of 10.10% over the forecast period. The growth of the segment can be credited to the growing industrial demand and its ability to offer cost-effective solutions to support large-scale applications. Carbon-based fillers enhance conductivity effectively.

Conductivity Mechanism Insights

The Electronic Conductive Polymers Segment Dominated the Market with 63% of Market Share in 2025

The electronic conductive polymers segment dominated the market with the largest share of 63 % in 2025. The dominance of the segment can be linked to its growing demand in the electronics and semiconductor industry, coupled with the high conductivity. Miniaturization trends increase its usage further.

Conductive polymers market Share,By Conductivity Mechanism, 2025 (%)

| By Conductivity Mechanism | Revenue Share, 2025 (%) |

| Electronic Conductive Polymers | 63% |

| Ionic Conductive Polymers | 37% |

The ionic conductive polymers segment held the market share of 37% in 2025 and is expected to grow at the fastest CAGR of 11.40% over the forecast period. The growth of the segment can be driven by its growing demand in batteries and fuel cells, and innovation in energy storage demand. Solid state battery adoption propels shortly.

Application Insights

The Antistatic Packaging Segment Dominated the Market with 18% of Market Share in 2025

The antistatic packaging segment dominated the market with the largest share of 18% in 2025. The dominance of the segment is owed to the growing demand for electronics packaging and expansion in the semiconductor industry. Static protection improves overall product safety.

Conductive polymers market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Antistatic Packaging | 19% |

| Electrostatic Discharge (ESD) Protection | 15% |

| Capacitors | 12% |

| Batteries | 16% |

| Sensors | 13% |

| Actuators | 8% |

| Organic Electronics | 17% |

The batteries segment held the market share of 16% in 2025 and is expected to grow at the fastest CAGR of 12.30% over the projected period. The growth of the segment is due to a rise in R&D investments and growing demand for EV and energy storage systems. Conductive polymers improve overall battery performance.

The organic electronics segment held the market share of 18% in 2025. The growth of the segment can be attributed to the growth in OLED and OPV technologies along with growing applications of flexible electronics. Innovative display technologies support market growth shortly.

End-Use Industry Insights

The Electrical & Electronics Segment Dominated the Market with 34% of Market Share in 2025

The electrical & electronics segment dominated the market with the largest share of 34% in 2025. The dominance of the segment can be credited to the increasing demand for EV and energy storage with a growing R&D investment. Conductive polymers improve battery performance.

Conductive polymers market Share,By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Electrical & Electronics | 34% |

| Automotive | 18% |

| Healthcare | 13% |

| Aerospace & Defense | 11% |

| Energy | 14% |

| Industrial | 10% |

The healthcare segment held the market share of 13% in 2025 and is expected to grow at the fastest CAGR of 12.10% during the projected period. The growth of the segment can be linked to the increase in demand for wearable devices and surge in aging population globally. Biocompatible materials promote medical innovation.

The automotive segment held the market share of 18% in 2025. The growth of the segment can be driven by rising adoption of EV with a rapid electronic integration. Lightweight materials improve efficiency further.

Form Insights

The Films Segment Dominated the Market with 29% of Market Share in 2025

The films segment dominated the market with the largest share of 29% in 2025. The dominance of the segment is owed to growing demand for flexible electronics and display technologies. Lightweight properties improve the scope of applications shortly.

Conductive polymers market Share,By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Films | 29% |

| Fibers | 14% |

| Coatings | 21% |

| Inks | 18% |

| Bulk Materials | 18% |

The inks segment held the market share of 18% in 2025 and is expected to grow at the fastest CAGR of 12.40% during the study period. The growth of the segment can be attributed to the rapid expansion of printed electronics and cost-effective production. Moreover, flexible circuits drive demand soon.

The coatings segment held the market share of 21% in 2025. The growth of the segment is due to rising industrial demand for coatings and increasing use of corrosion resistance materials. Protective and conductive coatings are gaining traction.

Regional Insights

How did Asia Pacific Dominate the Conductive Polymers Market in 2025?

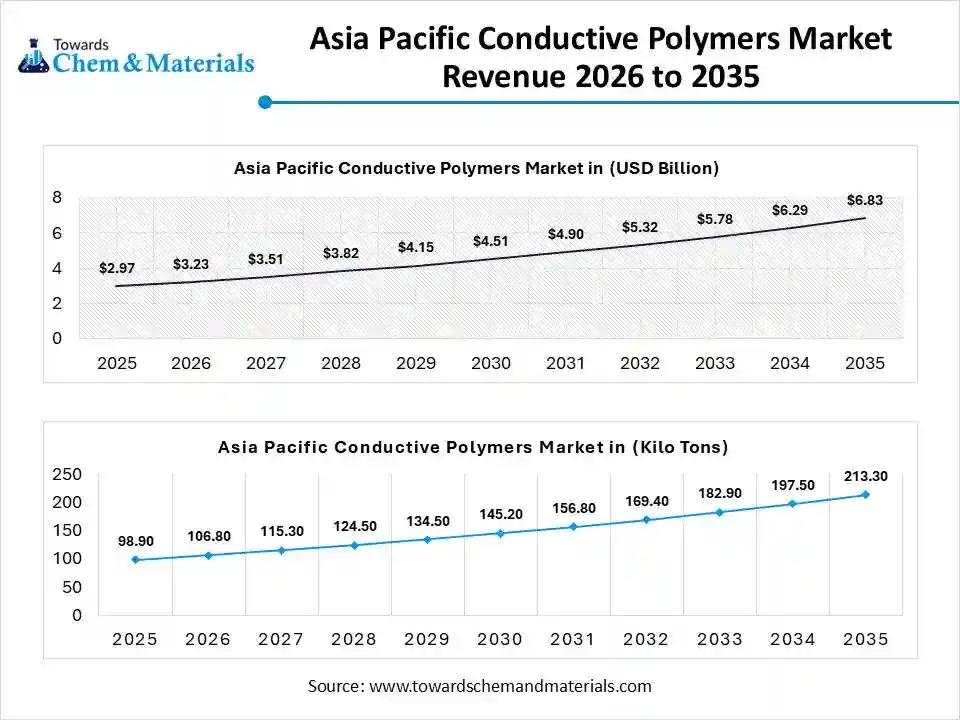

The Asia Pacific conductive polymers market size was estimated at USD 4.03 billion in 2025 and is projected to reach USD 11.31 billion by 2035, growing at a CAGR of 10.87% from 2026 to 2035 The dominance and growth of the region can be attributed to the growing demand for ESD/EMI shielding and the growing adoption of EV batteries, along with the localized manufacturing in emerging economies. In addition, favourable government policies supporting clean energy and drawing foreign direct investments (FDI) in production encourage local production and market growth.

")

China Conductive Polymers Market Trends

In the Asia Pacific, China dominated the market owing to the ongoing innovations in electric vehicles (EVs), electronics, and renewable energy. Also, rapid transition towards biodegradable conductive polymers and lightweight materials to enhance energy efficiency can fuel market expansion soon.

The Middle East & Africa region held the market share of 8% and is expected to grow at the fastest CAGR of 11.90% in 2025. The growth of the region can be credited to the growing investments in energy infrastructure and the ongoing implementation of diversification strategies. Furthermore, ongoing expansion in the industrial sectors, especially in Gulf Cooperation Council (GCC) countries, needs advanced materials for displays, sensors, and electronics components.

Saudi Arabia Conductive Polymers Market Trends

The growth of the market in the country is due to a surge in investments in renewable energy projects, electric vehicles (EVs), and innovative ESD/EMI shielding applications. Moreover, the growing need for high-strength materials in specialized construction applications and corrosion-resistant coatings, especially in desalination and water management projects, will lead to the country's growth soon.

Recent Development

- In September 2025, Filament Factory, a prominent manufacturer of 3D printing materials, partnered with South Africa's Council for Scientific and Industrial Research (CSIR) to engineer a nano-reinforced polymer composite. This collaborative innovation establishes a new standard in the field of advanced materials.

Conductive Polymers Market Companies

- 3M: 3M is a leading player in the global conductive polymers market, specializing in high-performance conductive adhesives and coatings for electronics, automotive, and telecommunications.

- Solvay: Solvay is a major player in the global conductive polymers market, recognized for its expertise in material science and high-performance polymer chemistry. The company maintains a strong competitive position by focusing on R&D to develop advanced solutions for electronics, automotive, and aerospace industries.

Companies in the Conductive Polymers Market

- SABIC

- PolyOne Corporation

- Lehmann&Voss&Co.

- RTP Company

- Parker Hannifin

- Sumitomo Chemical

- Premix OY

- Heraeus Group

- The Lubrizol Corporation

- Covestro

Conductive Polymers Market Segments Covered in the Report

By Type

- Intrinsically Conductive Polymers (ICPs)

- Polyaniline (PANI)

- Polypyrrole (PPy)

- Polyacetylene

- PEDOT (Poly(3,4-ethylenedioxythiophene))

- Conductive Polymer Composites

- Carbon-Based Fillers

- Carbon Black

- Carbon Nanotubes (CNT)

- Graphene

- Metal-Based Fillers

- Silver

- Copper

- Hybrid Fillers

- Carbon-Based Fillers

By Conductivity Mechanism

- Electronic Conductive Polymers

- Ionic Conductive Polymers

- Solid Polymer Electrolytes

- Gel Polymer Electrolytes

By Application

- Antistatic Packaging

- Electrostatic Discharge (ESD) Protection

- Capacitors

- Batteries

- Lithium-ion Batteries

- Solid-State Batteries

- Sensors

- Biosensors

- Chemical Sensors

- Actuators

- Organic Electronics

- OLEDs

- Organic Photovoltaics (OPVs)

By End-Use Industry

- Electrical & Electronics

- Consumer Electronics

- Semiconductors

- Automotive

- Electric Vehicles

- Interior Electronics

- Healthcare

- Medical Devices

- Wearable Electronics

- Aerospace & Defense

- Energy

- Energy Storage

- Renewable Energy Systems

- Industrial

By Form

- Films

- Fibers

- Coatings

- Inks

- Bulk Materials

By Regions

- North America:

- U.S.

- Canada

- Mexico

- Rest of North America

- Latin America:

- Brazil

- Argentina

- Rest of Latin America

- Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

- MEA:

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)