Content

What is the current PFAS Alternative Chemicals Market Size and Share?

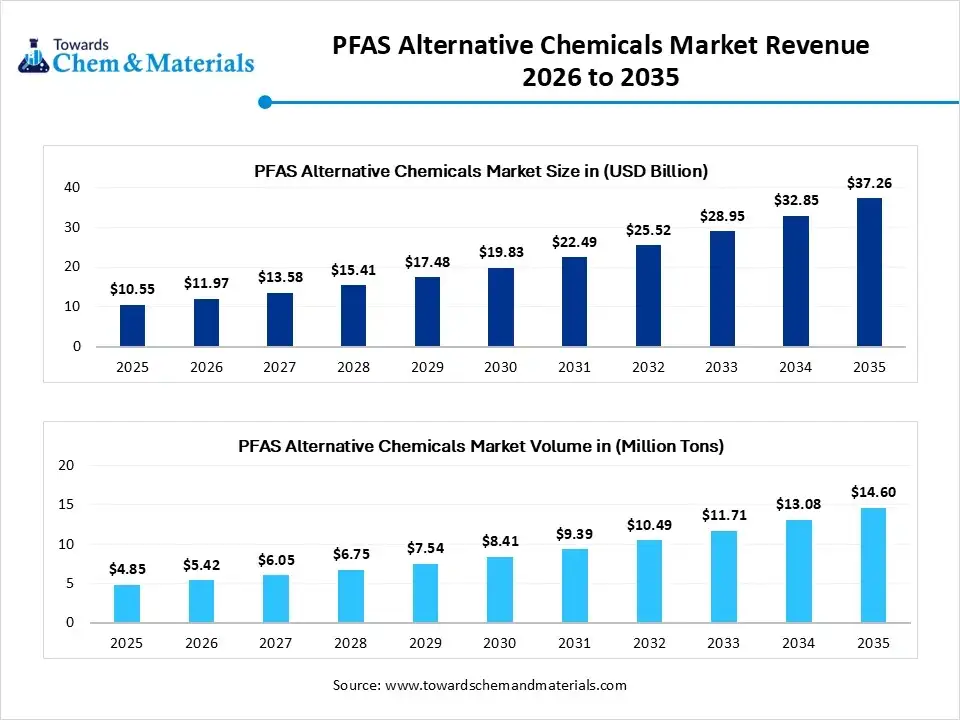

The global PFAS alternative chemicals market size was valued at USD 10.55 billion in 2025, is estimated to reach USD 11.97 billion in 2026, and is projected to reach USD 37.26 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 13.45% over the forecast period from 2026 to 2035. In terms of volume, the PFAS alternative chemicals market is projected to grow from 4.85 million tons in 2025 to 14.60 million tons by 2035. growing at a CAGR of 11.65% from 2026 to 2035. The growth of the market is driven by strict global regulations, rising health/environmental awareness, and intense demand for sustainable, fluorine-free materials in various sectors.

The market for PFAS alternative chemicals is vital as it supports the shift toward sustainable, non-toxic materials in response to global restrictions on "forever chemicals" (PFAS). It is expanding quickly to meet regulatory requirements while ensuring high performance in industries like electronics, textiles, and automotive. As governments enforce stricter regulations and bans on PFAS (per- and polyfluoroalkyl substances), this market provides essential solutions for companies to stay compliant and mitigate legal risks. It also acts as a catalyst for creating next-generation materials, such as metal-organic frameworks and hyperbranched polymers, designed for safer breakdown.

The market facilitates substituting PFAS in high-demand sectors. Key alternatives include silicone-based polymers, bio-based plastics, and natural materials, which provide similar water- and stain-resistant properties without long-term environmental impact. The main motive is to eliminate persistent pollutants associated with cancer and immune system issues.

Alternatives like bio-based plastics, silicone polymers, and natural refrigerants aim to be biodegradable and safe for health. Research is advancing rapidly on innovative solutions such as hyperbranched polymers and metal-organic frameworks to enhance the performance compared to traditional materials.

Market Highlights

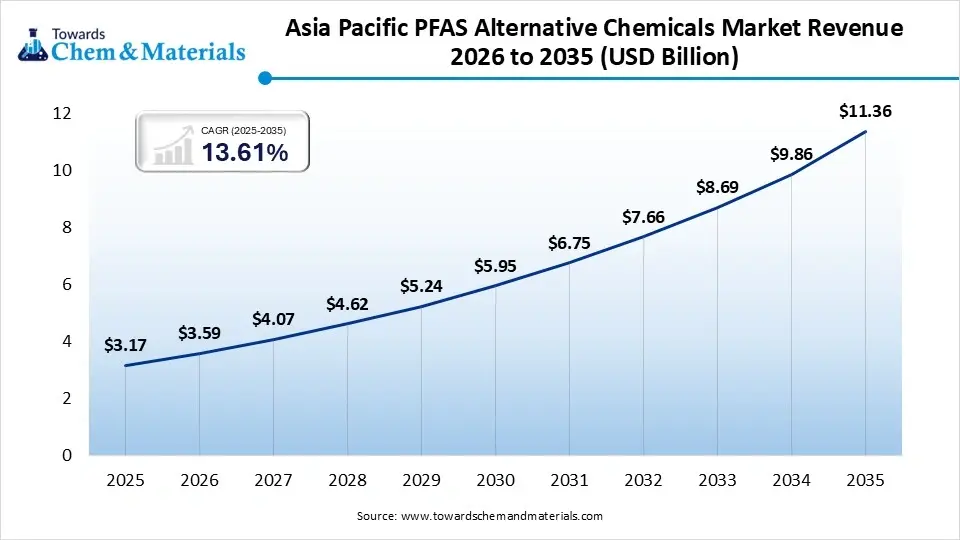

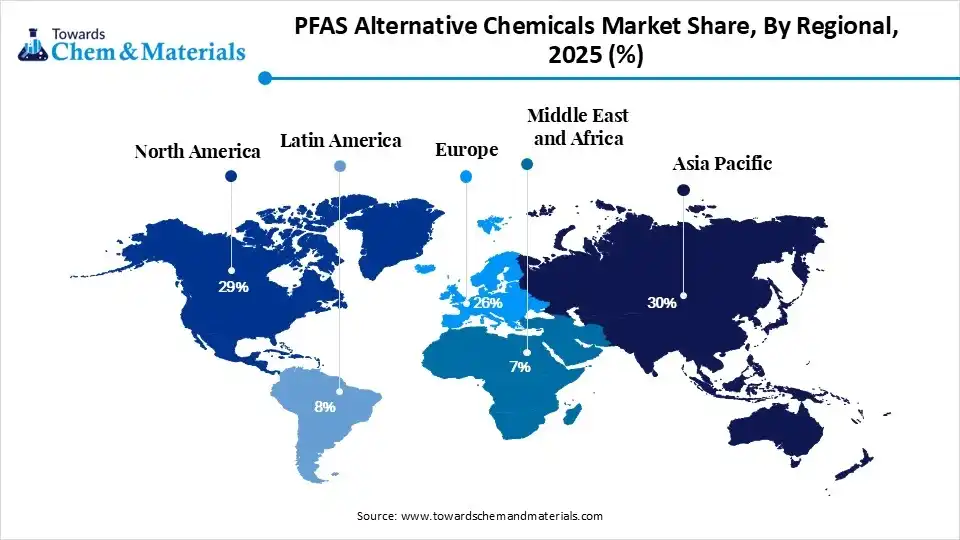

- By region, Asia Pacific dominated the market with a share of 30% in 2025 and is expected to sustain its position while growing with a CAGR of 15.1% in the forecast period. Rapid industrialization and electronics manufacturing expansion increase PFAS alternative consumption.

- By region, North America held the market share of 29% in 2025. Strict PFAS regulations in the United States and Canada accelerate the adoption of alternative chemistries.

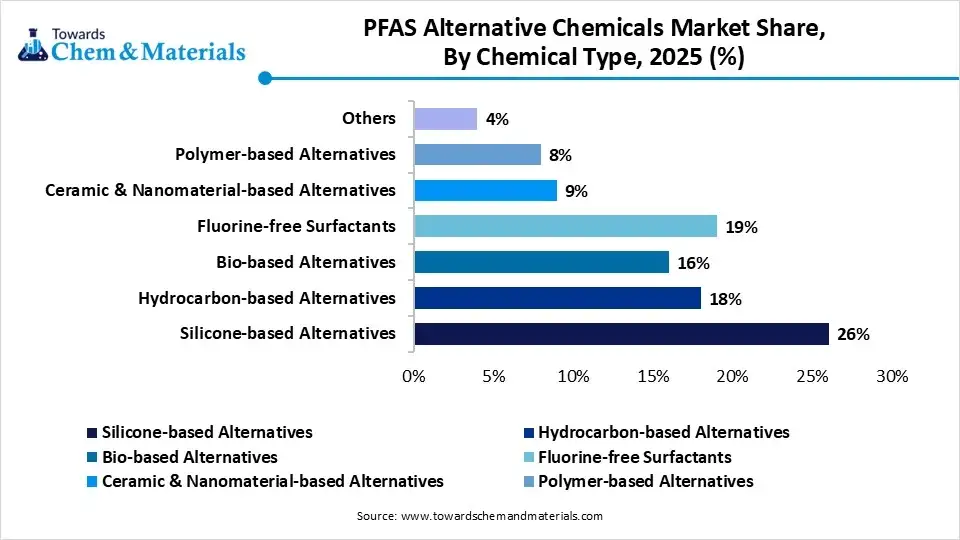

- By chemical type, the silicone-based alternatives segment dominated the market with 26% share in 2025. Textile and industrial coating manufacturers increasingly adopt silicone chemistries for durable water repellency.

- By chemical type, the bio-based alternatives segment held 16% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.8% in the forecast period. Sustainability initiatives accelerate demand for renewable and biodegradable chemical alternatives.

- By function, the water repellency segment dominated the market with 28% share in 2025. Textile, construction, and packaging sectors increasingly require non-fluorinated water-resistant solutions.

- By function, the fire suppression segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 14.8% in the forecast period. Airports, military facilities, and industrial sites phase out PFAS-containing firefighting foams.

- By application, the textile finishing segment dominated the market with 24% share in 2025. Apparel manufacturers accelerate transition toward PFAS-free durable water repellents.

- By application, the firefighting foams segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.6% in the forecast period. Government bans on PFAS-containing foams accelerate replacement programs globally.

- By form, the liquid segment dominated the market with 46% share in 2025. Liquid formulations dominate textile, coating, and firefighting foam applications due to ease of processing.

- By form, the dispersion segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 14.6% in the forecast period. Water-based dispersions gain popularity due to lower VOC emissions and environmental compliance benefits.

- By distribution channel, the direct sales segment dominated the market with 43% share in 2025. Major chemical manufacturers maintain direct supply agreements with industrial end users.

- By distribution channel, the online B2B platform segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.2% in the forecast period. Digital procurement platforms simplify specialty chemical sourcing and supplier comparison.

At a Glance

- Market Estimated Size (2025): USD 10.55 Billion | CAGR (2026–2035): 13.45%

- Market Projected Size (2035): USD 37.26 Billion

- Asia Pacific: largest Market Revenue Share of 30% in 2025.

- Market Estimated Volume (2025): 4.85 Million Tons | Volume CAGR (2026–2035): 11.65%

- Market Projected Volume (2035): 14.60 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 5,429/Ton

- Average Selling Price (2025): USD 7,186/Ton

- Pricing CAGR (2025–2035): 4.9%

Market Recent Growth Trends:

- Preferred Alternative Solutions: Industries are exploring silicone-based polymers, natural refrigerants, and bio-based plastics as effective, non-persistent replacements.

- Regulatory Pressure: Stringent, widening regulations from bodies such as the EU and US EPA are accelerating the adoption of alternatives.

- Innovation & R&D: Patent filings for PFAS-free technologies have increased significantly, with a strong focus on advanced materials like metal-organic frameworks.

Key Technological Shifts in the PFAS Alternative Chemicals Market:

The PFAS alternative chemicals market is undergoing rapid transformation, driven by strict global regulations, environmental concerns, and the need to replace "forever chemicals" with sustainable alternatives. The industry is shifting from simply replacing long-chain PFAS with short-chain fluorinated compounds toward developing entirely fluorine-free solutions and implementing advanced destruction technologies. The market, which includes both the removal of existing PFAS and the development of substitutes, is projected to grow significantly, driven by innovations in material science.

Market Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 11.97 Billion/ 5.42 Million Tons |

| Revenue Forecast in 2035 | USD 37.26 Billion/ 14.60 Million Tons |

| Growth Rate | CAGR 13.45% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Chemical Type, By Function, By Application, By Form, By Regions |

| Key companies profiled | Dow Inc, Evonik Industries AG, RUDOLF Holding SE & Co. KG, Akzo Nobel N.V., Mitsubishi Chemical Group Corporation, Archroma, Daikin Industries, Rudolf, HeiQ Materials, NICCA Chemical, CHT Group, Cerakote, James Walker Group, Victrex |

Supply Chain Analysis of PFAS Alternative Chemicals Market:

- Alternative Chemical Production & Formulation:PFAS alternative chemicals are produced through the development of fluorine-free or low-fluorine compounds designed to provide water resistance, stain protection, surfactant functionality, and thermal stability without persistent environmental impacts.

- Key players: Archroma, BASF, Dow, Chemours

- Quality Testing and Certification:TPFAS alternatives must comply with environmental safety standards, toxicity regulations, biodegradability requirements, and chemical performance certifications before commercialization.

- Key players: U.S. Environmental Protection Agency, European Chemicals Agency, International Organization for Standardization, OEKO-TEX

- Distribution to Industrial Users:PFAS alternative chemicals are supplied to textile manufacturers, packaging companies, electronics producers, firefighting foam developers, and consumer goods industries.

- Key players: Archroma, BASF, Dow.

PFAS Alternative Chemicals Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); Food and Drug Administration (FDA) | PFAS Strategic Roadmap; Toxic Substances Control Act (TSCA); Safe Drinking Water Act | PFAS phase-out, safer chemical substitutes, and environmental monitoring | The U.S. is tightening restrictions on PFAS chemicals, accelerating demand for fluorine-free and safer alternatives across industrial and consumer applications. |

| European Union | European Chemicals Agency (ECHA); European Commission | REACH Regulation; EU PFAS Restriction Proposal; POPs Regulation | PFAS elimination, sustainable chemistry, product safety | The EU is leading global PFAS restrictions, promoting broad bans on per- and polyfluoroalkyl substances and encouraging transition to safer alternatives. |

| Canada | Environment and Climate Change Canada (ECCC); Health Canada | Canadian Environmental Protection Act (CEPA) | Environmental protection, chemical substitution | Canada is increasing scrutiny on PFAS contamination and supporting the development of low-toxicity substitute chemistries. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of the Environment | Chemical Substances Control Law (CSCL) | Persistent chemical management and industrial safety | Japan regulates PFAS usage while supporting innovation in alternative coatings and surfactants. |

| China | Ministry of Ecology and Environment (MEE) | Stockholm Convention Compliance; Environmental Protection Law | Persistent pollutant control, industrial transition | China is gradually tightening PFAS-related regulations in line with global environmental agreements. |

| India | Ministry of Environment, Forest and Climate Change (MoEFCC); Central Pollution Control Board (CPCB) | Hazardous Chemicals Rules; Environmental Protection Act | Industrial emissions, chemical safety | India is at an early stage of PFAS regulation, but increasing awareness is expected to support future adoption of alternatives. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the PFAS Alternative Chemicals Market?

The PFAS alternative chemicals market is primarily driven by strict global regulations phasing out "forever chemicals," surging environmental and health awareness, and high demand for sustainable, non-toxic alternatives in manufacturing. Key drivers include the accelerated brand commitments to eliminate PFAS, particularly in textiles and consumer goods, coupled with technological advancements in fluorine-free coatings. Governments worldwide are implementing bans and restrictions on PFAS in products, forcing industries to shift toward compliant alternatives. Increasing awareness of the persistence of PFAS in the environment and human health risks is driving demand for safer, sustainable substitutes.

Restrains

What are the Key Growth Restraints of the PFAS Alternative Chemicals Market?

Key growth restraints for the PFAS alternative chemicals market include the high cost of developing and implementing new materials, inferior performance in critical applications compared to traditional PFAS, and the risk of "regrettable substitutions" where alternatives prove similarly toxic. Additionally, the lack of standardized global regulations and complex manufacturing transitions hinders widespread adoption. Developing effective, non-toxic alternatives requires significant investment in research and development, often resulting in higher prices that make them less competitive, especially in price-sensitive sectors.

Opportunities

What are the Key Growth Opportunities of the PFAS Alternative Chemicals Market?

The PFAS alternative chemicals market is experiencing rapid growth, driven by increasing regulatory bans, rising demand for sustainable products, and the need to replace "forever chemicals". Key opportunities exist in developing sustainable, non-fluorinated coatings, bio-based polymers, and specialized solutions for high-performance applications like automotive components, textiles, and semiconductor manufacturing. As governments impose bans and reporting requirements, the largest growth opportunity lies in providing alternatives that meet regulatory standards. This includes EPA-mandated monitoring and strict restrictions in regions like Europe and California.

Segmental Insights

Chemical Type Insights

The silicone-based alternatives segment dominated the market with 26% share in 2025, driven by urgent regulatory pressures and the need for sustainable, high-performance materials. The coatings industry is shifting toward silicone-based systems for their balance of high processability and moderate-to-high performance, particularly in textiles, automotive, and construction.

")

The hydrocarbon-based alternatives segment held 18% market share in 2025, driven by strong regulatory pressure and the urgent need for safe, sustainable, and fluorine-free alternatives. As manufacturers enhanced the phase-out of traditional per- and polyfluoroalkyl substances, hydrocarbon technologies like paraffin wax and specialized oil coatings are being heavily adopted to fill the gap in applications like coatings & textiles.

The bio-based alternatives segment held 16% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.8% in the forecast period, driven by stricter global regulations, increased environmental awareness, and the need for sustainable solutions. As industries move away from "forever chemicals," bio-based materials are increasingly replacing PFAS in textiles, food packaging, and coatings.

PFAS Alternative Chemicals Market Share, By Chemical Type, 2025 (%)

| By Chemical Type | Revenue Share, 2025 (%) |

| Silicone-based Alternatives | 26% |

| Hydrocarbon-based Alternatives | 18% |

| Bio-based Alternatives | 16% |

| Fluorine-free Surfactants | 19% |

| Ceramic & Nanomaterial-based Alternatives | 9% |

| Polymer-based Alternatives | 8% |

| Others | 4% |

Function Insights

The water repellency segment dominated the market with 28% share in 2025, driven by robust regulatory pressure, environmental concerns, and a growing demand for sustainable, non-toxic products in textiles & coatings. The need for Durable Water Repellents (DWR) in outdoor apparel, upholstery, and technical fabrics is pushing innovation toward PFC-free solutions.

The oil & grease resistance segment held 19% market share in 2025, driven primarily by stringent regulatory bans on fluorinated compounds in food packaging. The shift away from PFAS is accelerating in the packaging industry, where OGR coatings are essential for ensuring functionality in food-contact materials. Innovations in surface chemistry are allowing manufacturers to achieve oil resistance without using fluorinated compounds

The fire suppression segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 14.8% in the forecast period, driven by a rapid shift away from PFAS-containing Aqueous Film-Forming Foam (AFFF) toward environmentally sustainable alternatives. This market, particularly focused on fluorine-free foams (F3), is experiencing strong growth, with specialized, eco-friendly firefighting foams. The transition requires replacing existing stocks rather than just new installations, creating a massive spike in demand for fluorine-free alternatives.

PFAS Alternative Chemicals Market Share, By Function, 2025 (%)

| By Function | Revenue Share, 2025 (%) |

| Water Repellency | 28% |

| Oil & Grease Resistance | 19% |

| Surface Protection | 16% |

| Fire Suppression | 14% |

| Chemical Resistance | 9% |

| Thermal Stability | 6% |

| Anti-fouling & Non-stick Performance | 8% |

Application Insights

The textile finishing segment dominated the market with 24% share in 2025, driven by stringent regulatory bans taking effect in 2026 and increasing consumer demand for sustainable, non-toxic apparel and technical fabrics. The industry is moving away from simply eliminating PFAS and towards engineering new finishes that maintain high-level water, oil, and stain resistance.

The food packaging segment held 18% market share in 2025, driven by regulatory bans and consumer demand for safer, sustainable materials, fueling the growth of the market. This surge is fueled by innovative alternatives like bio-based coatings and molded fiber, with rapid adoption in quick-service restaurants. Rising bans on PFAS in food contact materials are accelerating the shift toward alternatives.

The firefighting foams segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.6% in the forecast period, driven by a rapid, mandated transition away from PFAS-containing Aqueous Film-Forming Foams (AFFF) toward Fluorine-Free Foams. The transition requires more than just buying new products; it involves system flushing, re-qualification, and re-stocking, which creates a high-demand, high-growth environment for manufacturers of compliant foams.

PFAS Alternative Chemicals Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Textile Finishing | 24% |

| Food Packaging | 18% |

| Firefighting Foams | 15% |

| Electronics Manufacturing | 11% |

| Industrial Processing | 10% |

| Construction Materials | 9% |

| Automotive & Transportation | 8% |

| Consumer Goods | 5% |

Form Insights

The liquid segment dominated the market with 46% share in 2025, driven by strong regulatory pressure, environmental concerns, and the demand for high-performance substitute in specialized applications. The shift away from persistent per- and polyfluoroalkyl substances (PFAS) towards safer, sustainable, and bio-derived liquid formulations is reshaping industries from textiles to industrial lubricants.

The powder segment held 21% market share in 2025, driven by the urgent need for sustainable, non-fluorinated coatings in industrial and consumer applications. As industries depart from PTFE and other PFAS additives to follow stricter regulations, the demand for high-performance, PFAS-free powder coatings is growing.

The dispersion segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 14.6% in the forecast period, driven by the urgent industrial shift toward sustainable, fluorine-free alternatives for coatings and binders. As regulatory pressures intensify with bans on PFAS in textiles and consumer goods, such as those beginning in Denmark in July 2026, and stricter standards from ECHA, companies are rapidly adopting waterborne polyurethane dispersions and other non-fluorinated, bio-derived solutions.

PFAS Alternative Chemicals Market Share, By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Liquid | 46% |

| Powder | 21% |

| Dispersion | 24% |

| Granules | 9% |

Distribution Channel Insights

The direct sales segment dominated the market with 43% share in 2025, driven by the need for close technical collaboration between chemical manufacturers and end-users, particularly in high-stakes sectors like textiles, electronics, and food packaging. This shift is fueled by a rapid, brand-driven phase-out of traditional PFAS, requiring customized, high-margin solutions.

The chemical distribution segment held 31% market share in 2025, driven by the urgent market shift toward PFAS (per- and polyfluoroalkyl substances) alternatives. This rapid expansion is fueled by strengthening regulations, particularly in the EU and US, prompting industry-wide demand for safe, non-toxic alternatives across applications like textiles, electronics, and automotive.

The online B2B platforms segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.2% in the forecast period, driven by tightening global regulations, increased demand for sustainable materials, and the need for transparent, efficient sourcing. The shift away from PFAS is accelerating due to imminent bans, forcing manufacturers to adopt alternatives such as silicon-based materials, hydrocarbon technologies, and bio-based products.

PFAS Alternative Chemicals Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Liquid | 46% |

| Powder | 21% |

| Dispersion | 24% |

| Granules | 9% |

Regional Insights

How did Asia Pacific Dominate the PFAS Alternative Chemicals Market in 2025?

Asia Pacific dominated the market with a 30% share in 2025 and is expected to sustain its position, growing at a CAGR of 15.1% over the forecast period, through a combination of rapid industrial scaling, tightening regional regulations, and intense investment in sustainable packaging and material science. This leadership was driven by China and India, focusing on scaling up biodegradable alternatives. Tightening environmental regulations modeled after international standards in countries like Japan, South Korea, and China accelerated the transition to non-fluorinated, sustainable alternatives in paper manufacturing and industrial applications.

India PFAS Alternative Chemicals Market Growth Factor

The India PFAS alternative chemicals market is primarily driven by rising environmental regulations, growing health awareness regarding "forever chemicals," and the need for sustainable, fluorine-free solutions across industries like textiles, coatings, and electronics. Growing industrialization and a shift toward cleaner manufacturing are also fueling demand for substitutes. As India enhances its environmental policies, stricter regulations are encouraging industries to shift toward PFAS-free coatings.

North America PFAS Alternative Chemicals Market Growth Factor

North America held the market share of 29% in 2025, driven by stringent regulatory bans, heightened consumer demand for non-toxic products, and industry-wide shifts toward sustainable, bio-derived, or silicone-based solutions. The market is propelled by a likely rapid transition away from "forever chemicals" across textiles, food packaging, and electronics. Expanding bans, state-level legislation in the U.S., and EPA restrictions against PFAS are forcing manufacturers to adopt safer alternatives, accelerating innovation and adoption of fluorine-free solutions.

")

U.S. PFAS Alternative Chemicals Market Growth Factor

The U.S. PFAS alternative chemicals market is experiencing rapid growth, as manufacturers move toward sustainable alternatives. Key drivers include strict environmental regulations (EPA bans), increasing consumer demand for safer products, and the need for high-performance, non-fluorinated coatings, foams, and textiles. The U.S. EPA's accelerating restrictions on PFOS and PFOA compounds are forcing industries to adopt alternatives, driving the search for compliant materials.

PFAS Alternative Chemicals Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 29% |

| Europe | 26% |

| Asia-Pacific | 30% |

| Latin America | 8% |

| Middle East & Africa | 7% |

Recent Developments

- In April 2026, the Swiss textile testing institute and official OEKO-TEX® representative, TESTEX, officially launched its advanced Non-Targeted PFAS Analysis alongside the newly established PFAS TESTED Label. This framework tackles a critical vulnerability in the textile industry. Conventional testing typically targets only a narrow list of regulated chemicals.(Source: www.fibre2fashion.com)

- In February 2026, the United Kingdom’s Department for Environment, Food and Rural Affairs (Defra) released its first dedicated national cross-government strategy to tackle "forever chemicals", titled “PFAS Plan: Building a Safer Future Together”. Led by Environment Minister Emma Hardy, the initiative establishes a unified regulatory path forward(Source: www.globalelr.com)

Top players in the PFAS Alternative Chemicals Market & Their Offerings:

- Dow Inc.: Dow provides silicone-based, acrylic, and specialty polymer alternatives to PFAS for packaging, coatings, textiles, and consumer applications. The company focuses on sustainable and non-fluorinated formulations.

- Evonik Industries AG: Evonik develops specialty additives, surfactants, and silicone alternatives used in coatings, personal care, and industrial applications to replace persistent PFAS compounds.

- RUDOLF Holding SE & Co. KG: RUDOLF develops fluorine-free finishes for textiles and technical fabrics, targeting apparel, outdoor gear, and industrial applications.

- Akzo Nobel N.V.: AkzoNobel is developing alternative coating technologies with reduced fluorochemical dependency for industrial and architectural applications.

- Mitsubishi Chemical Group Corporation: Mitsubishi Chemical develops advanced polymers and sustainable material solutions aimed at reducing PFAS usage in electronics and industrial applications.

Other Top Players Are

- Archroma

- Daikin Industries

- Rudolf

- HeiQ Materials

- NICCA Chemical

- CHT Group

- Cerakote

- James Walker Group

- Victrex

Segments Covered:

By Chemical Type

- Silicone-based Alternatives

- Silicone Surfactants

- Silicone Fluids

- Silicone Coatings

- Hydrocarbon-based Alternatives

- Alkyl-based Chemicals

- Olefin-based Chemicals

- Paraffin-based Chemicals

- Bio-based Alternatives

- Plant-derived Surfactants

- Biopolymer Coatings

- Starch-derived Additives

- Fluorine-free Surfactants

- Nonionic Surfactants

- Anionic Surfactants

- Amphoteric Surfactants

- Ceramic & Nanomaterial-based Alternatives

- Silica-based Coatings

- Graphene-based Coatings

- Nanocomposite Materials

- Polymer-based Alternatives

- Polyurethane-based

- Acrylic-based

- Epoxy-based

- Others

- Wax-based Alternatives

- Hybrid Chemistries

By Function

- Water Repellency

- Oil & Grease Resistance

- Surface Protection

- Fire Suppression

- Chemical Resistance

- Thermal Stability

- Anti-fouling & Non-stick Performance

By Application

- Textile Finishing

- Outdoor Apparel

- Industrial Fabrics

- Upholstery Fabrics

- Food Packaging

- Paper Packaging

- Molded Fiber Packaging

- Flexible Packaging

- Firefighting Foams

- Municipal Firefighting

- Aviation Firefighting

- Industrial Firefighting

- Electronics Manufacturing

- Semiconductor Processing

- Circuit Board Coatings

- Display Technologies

- Industrial Processing

- Metal Finishing

- Lubrication Systems

- Industrial Cleaning

- Construction Materials

- Architectural Coatings

- Sealants

- Waterproofing Systems

- Automotive & Transportation

- Interior Components

- Battery Systems

- Protective Coatings

- Consumer Goods

- Cookware

- Personal Care

- Household Products

By Form

- Liquid

- Powder

- Dispersion

- Granules

By Distribution Channel

- Direct Sales

- Chemical Distributors

- Online B2B Platforms

- OEM Partnerships

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)