Content

What is the current U.S. Renewable Diesel Market Size and Share?

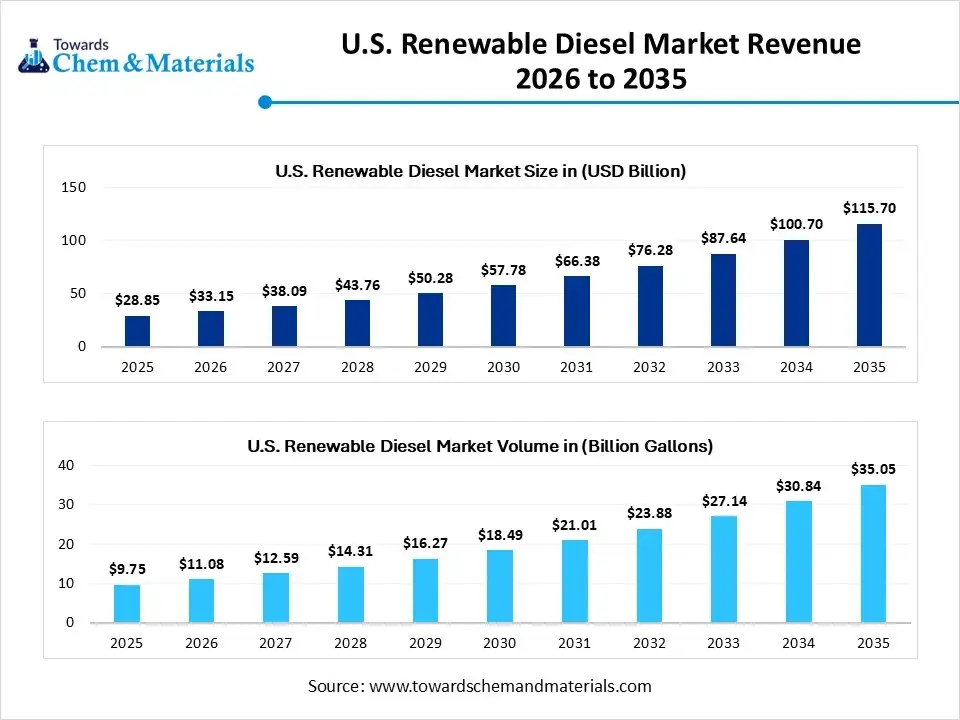

The U.S. renewable diesel market size was valued at USD 28.85 billion in 2025, is estimated to reach USD 33.15 billion in 2026, and is projected to reach USD 115.70 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 14.90% over the forecast period from 2026 to 2035. In terms of volume, the U.S. renewable diesel market is projected to grow from 9.75 billion gallons in 2025 to 35.05 billion gallons by 2035. growing at a CAGR of 13.65% from 2026 to 2035.The growth of the market is driven by the growing and rapidly changing climate and concerns associated with it, which demand sustainable and eco-friendly alternatives in alignment with government policies.

Key Takeaways

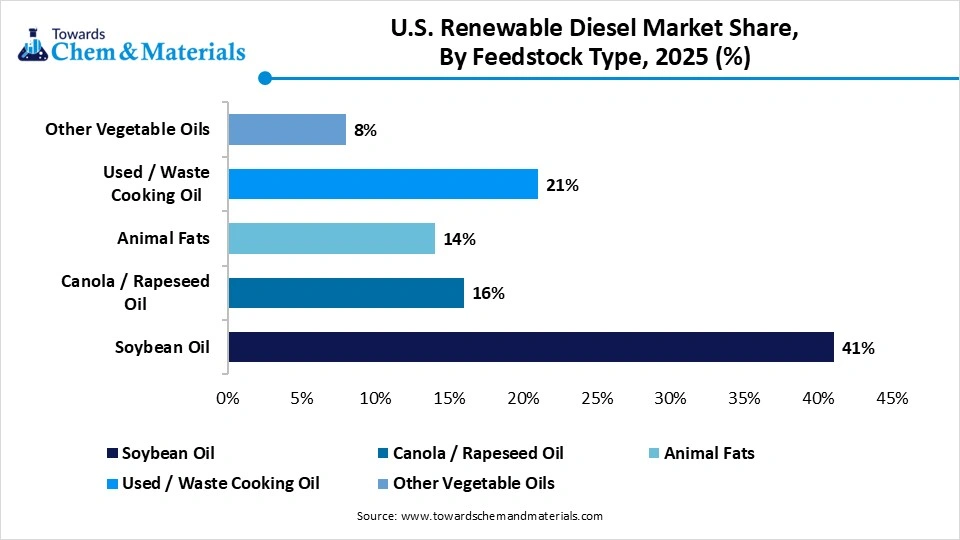

- By feedstock type, the soybean oil segment dominated the renewable diesel market with an approximate share of 41% in 2025.

- By feedstock type, the used / waste cooking oil segment expects significant growth in the renewable diesel market during the forecast period.

- By product/fuel type, the B100 (pure renewable diesel) segment dominated the renewable diesel market with an approximate share of 63% in 2025.

- By product/fuel type, the blends for the commercial fleets segment are expected to experience significant growth in the renewable diesel market during the forecast period.

- By production tech, the hydroprocessing / hefa-hvo segment dominated the renewable diesel market with an approximate share of 72% in 2025.

- By production tech, the co-processing in the refineries segment is expected to experience significant growth in the renewable diesel market during the forecast period.

- By application, the transportation (road freight & buses) segment dominated the renewable diesel market with an approximate share of 58% in 2025.

- By application, the aviation/marine segment expects significant growth in the renewable diesel market during the forecast period.

- By end user, the commercial transport fleets segment dominated the renewable diesel market with an approximate share of 39% in 2025.

- By end users, the municipal / government fleets segment expects significant growth in the renewable diesel market during the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 28.85 Billion | CAGR (2026–2035): 14.90%

- Market Projected Size (2035): USD 115.70 Billion

- Market Estimated Volume (2025): 9.75 Billion Gallons | Volume CAGR (2026–2035): 13.65%

- Market Projected Volume (2035): 35.05 Billion Gallons

- Pricing Data (2025):

- Average Manufacturing Price (2025): USD 3.51/Gallon

- Average Selling Price (2025): USD 3.85/Gallon

- Pricing CAGR (2026–2035): 2.15%

Market Overview

What Is The Significance Of The U.S. Renewable Diesel Market?

The significance of the U.S. renewable diesel market is its ability to significantly lower greenhouse gas emissions and carbon intensity in transportation amid rising environmental concerns and a growing shift towards sustainability.

This also helps in managing and enhancing the national energy security by reducing the reliance on foreign oil, which helps in increasing the economy and provides income to the farmers. The net-zero initiatives and alignment with government policies help the market to grow.

U.S. Renewable Diesel Market Outlook:

- Industry Growth Overview: Between 2025 and 2034, the U.S. renewable diesel market is expected to witness rapid growth, supported by federal and state-level incentives such as the Renewable Fuel Standard (RFS) and California’s Low Carbon Fuel Standard (LCFS). Production capacity is expanding significantly, with oil majors and biofuel companies converting existing refineries or building new plants.

- Sustainability Trends: The market is strongly aligned with decarbonization goals, with renewable diesel offering lifecycle greenhouse gas reductions of up to 80% compared to petroleum diesel. Feedstock diversification is emerging as a sustainability focus, with producers increasingly sourcing used cooking oil, animal fats, and inedible corn oil, alongside soybean and canola oils.

- Global Expansion & Investments: Leading refiners and energy companies are expanding renewable diesel production facilities across the U.S., particularly in the Gulf Coast and West Coast regions. Partnerships between agricultural producers and energy firms are strengthening domestic feedstock supply chains.

Key Technological Shifts In The U.S. Renewable Diesel Market:

Key technological shifts in the market include advancements in hydrotreating and co-processing for greater efficiency, feedstock flexibility through improved use of waste oils and fats, and innovative blending strategies (like the Chevron UltraClean Blend) to improve cold-weather performance and overcome operational constraints.

These technologies, supported by policy initiatives such as the Inflation Reduction Act and the Renewable Fuel Standard (RFS), are driving capacity expansions, reducing costs, and positioning renewable diesel as a mainstream, drop-in fuel solution.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 33.15 Billion |

| Expected Size by 2035 | USD 115.70 Billion |

| Growth Rate from 2025 to 2035 | CAGR 14.90% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Feedstock Type, By Product / Fuel Type, By Application, By End-User |

| Key Companies Profiled | Neste Corporation (U.S. operations), Diamond Green Diesel (Valero & Darling Ingredients JV), World Energy, Phillips 66 / Renewable Diesel Projects , Marathon Petroleum Corporation, REG (Renewable Energy Group) , Cargill, Inc., Bunge Limited, ADM (Archer Daniels Midland Company), Chevron / Renewable Diesel Initiatives , Tyson Foods (feedstock/animal fats supply), Gevo, Inc. (advanced biofuels / renewable diesel projects) , Renewable Energy Group / REG Life Sciences , Pacific Biodiesel Technologies , Green Plains Inc. |

Trade Analysis Of the U.S. Renewable Diesel Market: Import & Export Statistics

- In January 2025, U.S. renewable diesel exports saw a sharp increase, with the Netherlands being the primary destination.

- U.S. renewable diesel exports saw a 95% jump in January 2025, reaching 31.8 million gallons.

The main export destinations in January 2025 were the Netherlands (30.4 million gallons) and the United Kingdom (1.5 million gallons). - The Netherlands is both a major importer of biofuels and a significant exporter and re-exporter, leveraging its strategic port infrastructure. It plays a crucial role in Europe's biofuel trade, importing U.S. renewable diesel and distributing it to other European markets.

- Led by Neste, Singapore has become a major global production hub for renewable fuels and is a key exporter to markets in Europe and North America.

- Argentina is one of the world's largest exporters of biofuels, with a strong focus on biodiesel derived from soybean oil.

U.S. Renewable Diesel Market-- Value Chain Analysis

- Chemical Synthesis and Processing: The renewable diesel is synthesised and processed through hydrotreating, gasification, pyrolysis, and biological sugar upgrading.

- Key players : Diamond Green Diesel, Chevron, Marathon Petroleum, Phillips 66, Honeywell UOP, and ExxonMobil Chemical

- Quality Testing and Certification: The renewable diesel requires ASTM D975, International Sustainability and Carbon Certification, and TOP TIER Diesel Fuel certification.

- Key players: ASTM International, UL Solutions, and the Environmental Protection Agency

- Distribution to Industrial Users: The renewable diesel is distributed to the Transportation and logistics, Construction and mining, Agriculture, power generation, and Industrial and commercial operations.

- Key players: Targray, Biofuel Express, Ezfuel, Repos Energy, and World Fuel Services.

Renewable Diesel Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | U.S. EPA (Environmental Protection Agency), California Air Resources Board (CARB), U.S. Department of Energy (DOE), ASTM International | - EPA Renewable Fuel Standard (RFS2, 40 CFR Part 80) → mandates blending of renewable fuels, creates RIN credits - CARB Low Carbon Fuel Standard (LCFS) → scarbon intensity reduction targets for fuels sold in California - ASTM D975 & D975 Annex → fuel quality specifications for diesel and renewable diesel - ASTM D975 & D7467 → biodiesel/renewable diesel blends - Blender’s Tax Credit (BTC, $1/gal) – federal tax incentive for renewable diesel producers |

- GHG reduction - Fuel quality & compatibility - Compliance with blending mandates - Incentives for production & use |

California LCFS provides the strongest demand pull, while federal RFS creates a nationwide credit market (RINs). ASTM standards ensure renewable diesel is fully interchangeable with petroleum diesel. Incentives like the BTC significantly boost the economy. |

Segmental Insights

Feedstock Type Insights

Which Feedstock Type Segment Dominated The U.S. Renewable Diesel Market In 2024?

The soybean oil segment dominated the market with an approximate share of 40% in 2024. Soybean oil remains a major renewable diesel feedstock in the U.S. due to its availability and integration with existing agricultural supply chains. It offers stable yields, supports farm-based economies, and benefits from federal incentives. Producers are expanding soybean processing capacity to meet growing demand for low-carbon fuels.

") The used / waste cooking oil segment expects significant growth in the market during the forecast period. Used and waste cooking oil is gaining momentum as a sustainable feedstock for renewable diesel. Its circular economy benefits, and lower carbon intensity make it highly attractive. In the U.S., waste oil collection programs and partnerships with restaurants are increasing feedstock availability for large-scale fuel production.

The used / waste cooking oil segment expects significant growth in the market during the forecast period. Used and waste cooking oil is gaining momentum as a sustainable feedstock for renewable diesel. Its circular economy benefits, and lower carbon intensity make it highly attractive. In the U.S., waste oil collection programs and partnerships with restaurants are increasing feedstock availability for large-scale fuel production.

U.S. Renewable Diesel Market Share, By Feedstock Type , 2025 (%)

| By Feedstock Type | Revenue Share, 2025 (%) |

| Soybean Oil | 41% |

| Canola / Rapeseed Oil | 16% |

| Animal Fats | 14% |

| Used / Waste Cooking Oil | 21% |

| Other Vegetable Oils | 8% |

- Soybean Oil: Soybean oil is the most widely used feedstock for renewable diesel production due to its abundance, cost-effectiveness, and well-established supply chain. Soybean oil holds 41% of the market share.

- Canola / Rapeseed Oil: Canola oil is highly efficient for producing renewable diesel, particularly in colder climates due to its low freezing point, making it a popular choice for biodiesel production. This segment represents 16% of the market share.

- Animal Fats: Animal fats are considered a sustainable feedstock for renewable diesel, offering high energy content and the ability to reduce waste from the meat processing industry. Animal fats contribute 14% to the market share.

- Used / Waste Cooking Oil: Waste oils, such as used cooking oils, are increasingly being utilized for renewable diesel production, helping to reduce waste while contributing to sustainable fuel sources. Used / waste cooking oil holds 21% of the market share.

- Other Vegetable Oils: Other vegetable oils, such as palm oil and sunflower oil, are also used in renewable diesel production, though they are less dominant than soybean or canola oils. These oils account for 8% of the market share.

Product / Fuel Type Insights

How Did the B100 (Pure Renewable Diesel) Segment Dominated The U.S. Renewable Diesel Market In 2024?

The B100 (pure renewable diesel) segment dominated the U.S. renewable diesel market with an approximate share of 50% in 2024. B100 renewable diesel offers a fully decarbonized alternative to petroleum diesel, meeting ASTM standards for direct substitution. It is used in specialized fleets seeking maximum emissions reduction. In the U.S., demand is driven by state-level low-carbon fuel programs and municipal fleet decarbonization initiatives.

The blends for the commercial fleets segment are expected to experience significant growth in the market during the forecast period. Blended renewable diesel provides a practical transition option for commercial fleets. It improves fuel performance, reduces greenhouse gases, and integrates seamlessly into existing infrastructure. In the U.S., long-haul trucking and logistics sectors are rapidly adopting blends to meet corporate sustainability goals while balancing operational costs.

U.S. Renewable Diesel Market Share, By Product Type , 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Pure Renewable Diesel (B100) | 63% |

| Blends | 37% |

- Pure Renewable Diesel (B100): Pure renewable diesel, or B100, is preferred for its high purity and superior performance characteristics compared to blended fuels, making it a leading choice for commercial and industrial use. Pure Renewable Diesel (B100) holds 63% of the market share.

- Blends: Blended renewable diesel is a popular choice due to its compatibility with existing diesel infrastructure and engines, offering a cost-effective solution for transitioning to cleaner fuels. Blends account for 37% of the market share.

Production Tech Insights

Which Production Tech Segment Dominated The U.S. Renewable Diesel Market In 2024?

The hydroprocessing / hefa-hvo segment dominated the market with an approximate share of 65% in 2024. Hydroprocessed esters and fatty acids (HEFA-HVO) technology dominates renewable diesel production in the U.S. It ensures high-quality fuel compatible with existing engines and infrastructure. HEFA plants are expanding rapidly, supported by investment incentives and commitments from major refiners and biofuel companies to scale domestic renewable capacity.

The co-processing in the refineries segment is expected to experience significant growth in the market during the forecast period. Co-processing allows petroleum refineries to integrate renewable feedstocks with fossil streams, offering a lower-cost, transitional pathway to renewable diesel. In the U.S., refiners are increasingly adopting this approach to comply with renewable fuel standards while maximizing utilization of existing infrastructure and reducing overall carbon intensity.

U.S. Renewable Diesel Market Share, By Production Technology, 2025 (%)

| By Production Technology | Revenue Share, 2025 (%) |

| Hydroprocessing / Hydrotreated Vegetable Oils (HEFA/HVO) | 72% |

| Co-processing in Refineries | 18% |

| Emerging Catalytic & Biochemical Routes | 10% |

- Hydroprocessing / Hydrotreated Vegetable Oils (HEFA/HVO): HEFA/HVO technology is the dominant production method for renewable diesel due to its efficiency in converting vegetable oils and animal fats into high-quality renewable diesel with minimal contaminants. It holds 72% of the market share.

- Co-processing in Refineries: Co-processing involves blending renewable feedstocks with conventional refinery feedstocks, allowing existing infrastructure to be utilized while producing renewable diesel. This segment represents 18% of the market share.

- Emerging Catalytic & Biochemical Routes: New catalytic and biochemical processes offer promising alternatives to traditional methods, but they are still in the development phase. These innovative technologies account for 10% of the market share

Application Insights

How Did the Transportation Segment Dominated The U.S. Renewable Diesel Market In 2024?

The transportation (road freight & buses) segment dominated the U.S. renewable diesel market with an approximate share of 55% in 2024. Road freight and buses are the largest consumers of renewable diesel in the U.S. Its drop-in compatibility, reduced particulate matter, and lower lifecycle emissions make it attractive for heavy-duty fleets. Federal and state incentives continue to push adoption, especially in California and other low-carbon standard states.

The aviation/marine segment expects significant growth in the market during the forecast period. The aviation and marine sectors are beginning to adopt renewable diesel, often as part of early trials and blended fuels. U.S. ports and airlines are exploring renewable options to meet international emission reduction targets. Growth is expected as sustainable aviation fuel (SAF) pathways overlap with renewable diesel technologies.

U.S. Renewable Diesel Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Transportation | 58% |

| Industrial | 17% |

| Aviation | 15% |

| Power Generation / Grid Backup | 10% |

- Transportation: Renewable diesel is widely used in the transportation sector due to its compatibility with existing diesel engines and its ability to reduce greenhouse gas emissions, making it the largest application segment. Transportation holds 58% of the market share.

- Industrial: The industrial sector uses renewable diesel for heavy machinery and equipment, where sustainability is becoming a critical consideration. This segment represents 17% of the market share.

- Aviation: Renewable diesel is emerging as a more sustainable fuel alternative in the aviation industry, supporting efforts to reduce carbon emissions in air travel. The aviation segment contributes 15% to the market share.

- Power Generation / Grid Backup: Renewable diesel is increasingly being used in power generation and as a backup for grid stability, particularly in remote areas and for emergency backup systems. This application holds 10% of the market share.

End-User Insights

Which End-User Segment Dominated The U.S. Renewable Diesel Market In 2024?

The commercial transport fleets segment dominated the market with an approximate share of 50% in 2024. Commercial fleets, including logistics and delivery operators, are major adopters of renewable diesel in the U.S. The fuel’s compatibility with existing engines reduces transition costs. Companies are turning to renewable diesel to meet ESG targets, achieve carbon neutrality, and comply with evolving state regulations.

The municipal / government fleets segment expects significant growth in the market during the forecast period. Municipal and government fleets play a leading role in renewable diesel adoption, especially in California, Oregon, and Washington. Public buses, waste management trucks, and emergency vehicles increasingly run on renewable diesel to lower emissions, demonstrating government commitment to decarbonization and supporting broader market expansion.

U.S. Renewable Diesel Market Share, By End-User, 2025 (%)

| By End-User | Revenue Share, 2025 (%) |

| Commercial Transportation Fleets | 39% |

| Municipal & Government Vehicles | 18% |

| Industrial / Manufacturing Units | 19% |

| Aviation & Marine Operators | 14% |

| Refineries & Blenders | 10% |

- Commercial Transportation Fleets: Commercial fleets, including trucking and logistics, are major consumers of renewable diesel due to its compatibility with diesel engines and the industry’s push for more sustainable fuel options. This segment holds 39% of the market share.

- Municipal & Government Vehicles: Municipal and government fleets are adopting renewable diesel as part of their sustainability efforts, driven by regulatory pressures and public sector commitments to reduce carbon emissions. Municipal & government vehicles account for 18% of the market share.

- Industrial / Manufacturing Units: Industrial and manufacturing sectors use renewable diesel to power heavy machinery and reduce their carbon footprint, especially in regions with stricter environmental regulations. This segment contributes 19% to the market share.

- Aviation & Marine Operators: Renewable diesel is also being explored by aviation and marine operators as part of their transition to cleaner fuels, contributing to the sector's sustainability goals. Aviation & marine operators represent 14% of the market share.

- Refineries & Blenders: Refineries and blenders play a key role in producing and distributing renewable diesel, making them a significant end-user of the fuel in the production process. They hold 10% of the market share.

Recent Developments

- In July 2025, ExxonMobil expanded the retail availability of its Esso Renewable Diesel (R20) in Hong Kong, making the lower-emission fuel available at more service stations. The R20 blend contains a minimum of 20% renewable diesel made from waste oils and is advertised as providing a 15.4% reduction in life-cycle greenhouse gas emissions compared to conventional diesel.(Source : corporate.exxonmobil.com)

- In April 2025, Neste and DB Schenker initiated Singapore's first trial of renewable diesel for road transport, utilizing Neste MY Renewable Diesel made from waste and residue raw materials to significantly reduce greenhouse gas emissions.(Source : esgnews.com)

Top Players In The U.S. Renewable Diesel Market & Their Offerings:

- Neste Corporation (U.S. operations): a Finnish company specializing in refining waste and renewable raw materials into sustainable fuels and products. It is a global leader in producing sustainable aviation fuel (SAF) and renewable diesel.

- Diamond Green Diesel (Valero & Darling Ingredients JV): a joint venture between U.S. oil refiner Valero Energy Corporation and sustainable ingredients producer Darling Ingredients Inc. The company is a major producer of renewable diesel and sustainable aviation fuel (SAF) in North America.

- World Energy: World Energy is an advanced biofuel company and a leading producer of sustainable aviation fuel (SAF) in North America. The company primarily focuses on converting waste and inedible agricultural byproducts into clean fuels to decarbonize the transportation sector.

- Phillips 66 / Renewable Diesel Projects: Phillips 66 is actively transitioning its business to include renewable fuels, with its flagship Rodeo Renewed project in California representing a major step toward that goal. The company has focused on converting some of its existing refineries into renewable fuel facilities rather than building from scratch.

- Marathon Petroleum Corporation: Marathon Petroleum Corporation (MPC) is a major U.S. integrated downstream energy company that has been actively investing in renewable diesel to diversify its business. The company is converting some of its conventional refineries into renewable fuel facilities and has also entered key partnerships to secure feedstock.

Other Top Players Are

- Neste Corporation (U.S. operations)

- Diamond Green Diesel (Valero & Darling Ingredients JV)

- World Energy

- Phillips 66 / Renewable Diesel Projects

- Marathon Petroleum Corporation

- REG (Renewable Energy Group)

- Cargill, Inc.

- Bunge Limited

- ADM (Archer Daniels Midland Company)

- Chevron / Renewable Diesel Initiatives

- Tyson Foods (feedstock/animal fats supply)

- Gevo, Inc. (advanced biofuels / renewable diesel projects)

- Renewable Energy Group / REG Life Sciences

- Pacific Biodiesel Technologies

- Green Plains Inc.

Segments Covered

By Feedstock Type

- Soybean Oil

- Canola / Rapeseed Oil

- Animal Fats (tallow, lard)

- Used / Waste Cooking Oil

- Other Vegetable Oils (palm, sunflower, corn oil)

By Product / Fuel Type

- Pure Renewable Diesel (B100)

- Blends (B5, B20, B50)

By Production Technology

- Hydroprocessing / Hydrotreated Vegetable Oils (HEFA/HVO)

- Co-processing in Refineries

- Emerging Catalytic & Biochemical Routes

By Application

- Transportation (road freight, buses, marine diesel)

- Industrial (diesel engines, generators, machinery)

- Aviation (biojet fuel blends derived from renewable diesel streams)

- Power Generation / Grid Backup

By End-User

- Commercial Transportation Fleets (trucking, buses)

- Municipal & Government Vehicles

- Industrial / Manufacturing Units

- Aviation & Marine Operators

- Refineries & Blenders

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (2)