Content

What is the Current Organosilicon Polymers Market Size and Volume?

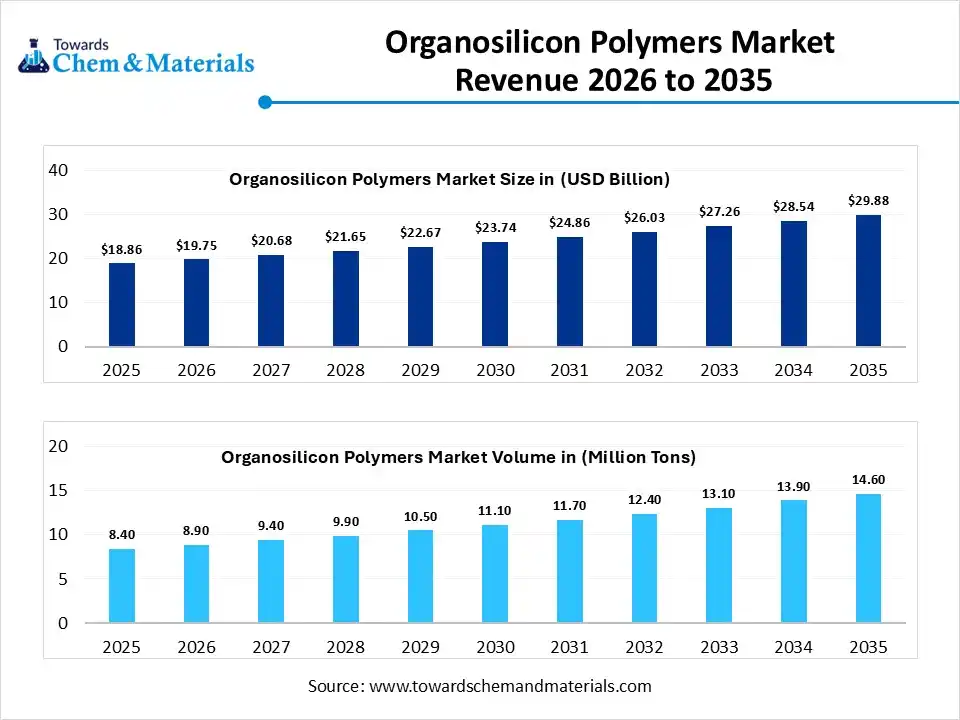

The global organosilicon polymers market size was estimated at USD 18.86 billion in 2025 and is expected to increase from USD 19.75 billion in 2026 to USD 29.88 billion by 2035, growing at a CAGR of 4.71% from 2026 to 2035. In terms of volume, the market is projected to grow from 8.40 million tons in 2025 to 14.60 million tons by 2035. growing at a CAGR of 7.10% from 2026 to 2035. Asia Pacific dominated the Organosilicon Polymers market with the largest volume share of 47.19% in 2025. The shift towards heat-resistant and stronger materials has fueled the industry's potential in recent years.

Market Highlights

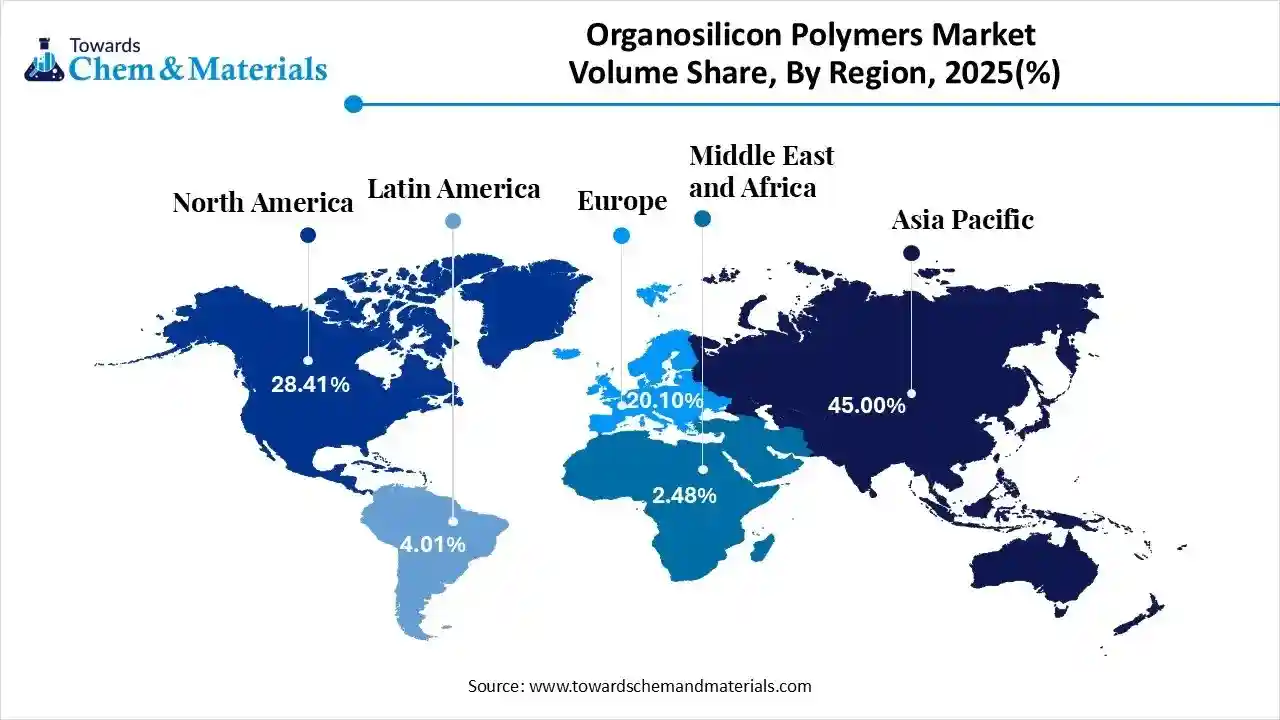

- The Asia Pacific dominated the global organosilicon polymers market with the largest volume share of 47.19% in 2025.

- The organosilicon polymers market in North America is expected to grow at a substantial CAGR of 7.49% from 2026 to 2035.

- The Europe organosilicon polymers market segment accounted for the major volume share of 20.10% in 2025.

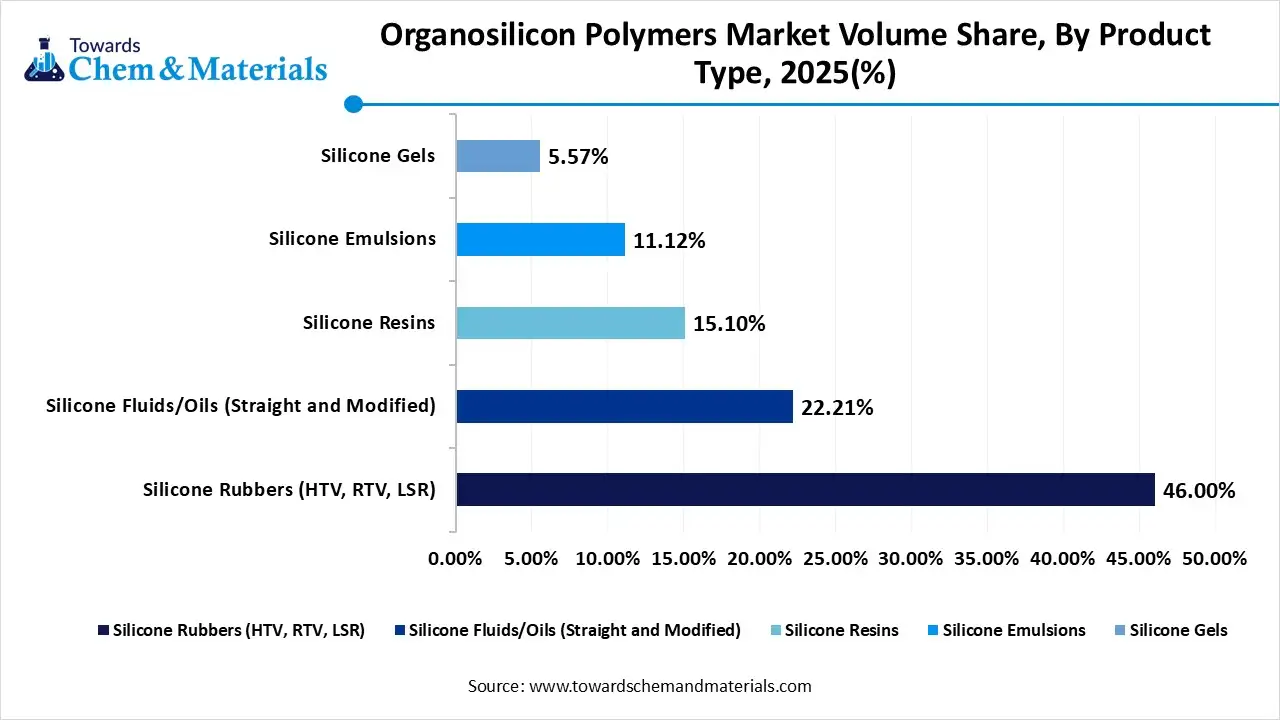

- By product type, the silicon rubbers segment dominated the market and accounted for the largest volume share of 46% in 2025.

- By product type, the silicone fluids/Oils (straight and modified) segment is expected to grow at the fastest CAGR of 8.04% from 2026 to 2035 in terms of volume.

- By end use, the building and construction segment led the market with the largest revenue volume share of 28% in 2025.

Beyond Plastics: The Organosilicon Advantage

The organosilicon polymers refer to the specific polymers that contain both organic groups and silicon in their basic chemical structure. Also, by handling the sunlight, high heat, moisture, and chemicals, the organosilicon has more preferred material than normal plastic nowadays. Also, factors like flexibility and easier processing have led the organosilicon to gain global attention in recent years, as per the latest survey.

Market Trends:

- The increased need for the high durability materials has actively supported capital growth and economic activity in the sector in recent years. Moreover, by keeping properties the same after years of usage, the organosilicon polymers have created their own industry presence in recent years, as per the latest survey.

- The organosilicon polymers have emerged as an ideal material in the medical and personal care product sector in the past few years. Moreover, the factors like gentle on skin, stability, and safe for long-term contact with the human body, the organosilicon polymers have been used in medical implants, tubing, and cosmetic formulations.

- The move and growing demand of the application-specific and customized organosilicon polymers is expected to lead to robust revenue growth across the sector in the upcoming years. Also, the manufacturers are preferring this type of customized polymer owing to their advantages, such as better performance, longer product life, and easy processing in the current period.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 19.75 Billion / 8.90 Million Tons |

| Revenue Forecast in 2035 | USD 29.88 Billion / 14.60 Million Tons |

| Growth Rate | CAGR 4.71% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Units Considered | Value (Billion / Million), Volume (Million Tons) |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By End-Use Industry, By Region |

| Key companies profiled | Dow Inc. (formerly Dow Corning), Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc, Elkem ASA (Bluestar), BASF SE, Evonik Industries AG, Hoshine Silicon Industry Co., Ltd., KCC Corporation, Stockwell Elastomerics, Inc., Saint-Gobain Performance Plastics, Specialty Silicone Products, Inc., CSL Silicones Inc., Kaneka Corporation, Zhejiang Xinan Chemical Industrial Group (Wynca), Jiangsu Yangnong Chemical Group, Mitsubishi Chemical Group, Silchem, Inc., Innospec Inc., NuSil Technology LLC (Avantor) |

From Standard Materials to Precision Polymers

The industry has seen under the transition from standardized material production to application-driven polymer engineering. Manufacturers now focus on tailoring molecular structures to meet precise performance requirements. Furthermore, this approach improves reliability, durability, and functional efficiency across industries in the coming years.

Trade Analysis of the Organosilicon Polymers Market:

Import, Export, Consumption, and Production Statistics

- China has exported organosilicon with 209 shipments from May 2024 to April 2025, as per the published report.

- The United States has seen under the greater silicon export in 2024, valued at around $1.39 billion, where other countries like Mexico have $208 million, and Canada has $139 million in silicon exports.

Value Chain Analysis of the Organosilicon Polymers Market:

- Distribution to Industrial Users: The distribution of organosilicon polymers (primarily polysiloxanes) is characterized by a mature ecosystem of global chemical giants supplying high-demand sectors like automotive, construction, and electronics.

- Key Players: Dow Inc. and Shin-Etsu Chemical

- Chemical Synthesis and Processing: The market for the chemical synthesis and processing of organosilicon polymers is shaped by a transition toward high-purity applications in electronics and sustainable, low-carbon manufacturing.

- Key Players: Wacker Chemie AG and Momentive Performance Materials

- Regulatory Compliance and Safety Monitoring: The organosilicon polymer market faces stringent regulatory oversight in 2026, primarily driven by environmental concerns over specific cyclic siloxanes (D4, D5, and D6).

- Safety Standards- EU REACH Regulation and US TSCA

Organosilicon Polymers Market Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Toxic Substances Control Act (TSCA) | Assessing the environmental fate and potential bioaccumulation of certain cyclic silicones (e.g., D4, D5) |

| European Union | European Chemicals Agency (ECHA) | REACH Regulation (EC 1907/2006) | phasing out persistent and bioaccumulative substances |

| China | Ministry of Ecology and Environment (MEE) | Environmental Protection Law | Enforcing stricter environmental standards to reduce industrial pollution |

Segmental Insights

Product Type Insights

How did the Silicon Rubbers Segment Dominate the Organosilicon Polymers Market in 2025?

The silicone rubbers (HTV, RTV, LSR) segment volume was valued at 1.6 million tons in 2025 and is projected to reach 3.2 million tons by 2035, expanding at a CAGR of 7.77% during the forecast period from 2025 to 2035. The silicon rubbers segment dominated the market with approximately 46.0% share in 2025, due to its major offerings such as flexibility, resistance, and durability. Moreover, by performing better under cold, heat, and moisture, the silicon rubber has gained a major industry share globally. Also, having the advantages like easy molding and sealing, the silicon rubbers are seen as high margin opportunity for manufacturers in the coming years.

")

The Silicone Fluids/Oils (Straight and Modified) segment volume was valued at 0.8 million tons in 2025 and is expected to surpass around 1.6 million tons by 2035, and it is anticipated to expand to 8.04% of CAGR during 2026 to 2035, owing to the increasing need for the heat resistant, rigid, and longer shelf-life materials. Also, the manufacturers prefer this material for coatings, fire-resistant material, and electrical insulation, which is expected to create lucrative opportunities during the forecast period.

Organosilicon Polymers (Polysiloxane) Market Volume and Share, By Product Type, 2025-2035

| By Product Type | Market Volume Share (%), 2025 | Market Volume ( Million Tons)2025 | Market Volume (Million Tons)2035 | CAGR(%) 2026-2035 | Market Volume Share (%), 2035 |

| Silicone Rubbers (HTV, RTV, LSR) | 46.00% | 1.6 | 3.2 | 7.77% | 45.43% |

| Silicone Fluids/Oils (Straight and Modified) | 22.21% | 0.8 | 1.6 | 8.04% | 22.44% |

| Silicone Resins | 15.10% | 0.5 | 1.1 | 8.97% | 16.48% |

| Silicone Emulsions | 11.12% | 0.4 | 0.7 | 6.80% | 10.12% |

| Silicone Gels | 5.57% | 0.2 | 0.4 | 7.83% | 5.53% |

End Use Insights

How did the Building and Construction Segment Dominate the Organosilicon Polymers Market in 2025?

The building and construction segment dominated the market with approximately 28% share in 2025, akin to organosilicon polymers improve structural reliability. They help seal joints, protect surfaces, and improve thermal performance. Builders value materials that perform consistently across different climates. Organosilicon polymers reduce repair frequency and improve building safety.

The healthcare and medical devices segment is expected to grow due to organosilicon polymers that meet strict medical standards. Also, these materials offer flexibility, durability, and chemical stability. They are suitable for repeated use and sensitive applications. As medical devices become more advanced and personalized, demand for high-performance polymers increases.

Regional Insights

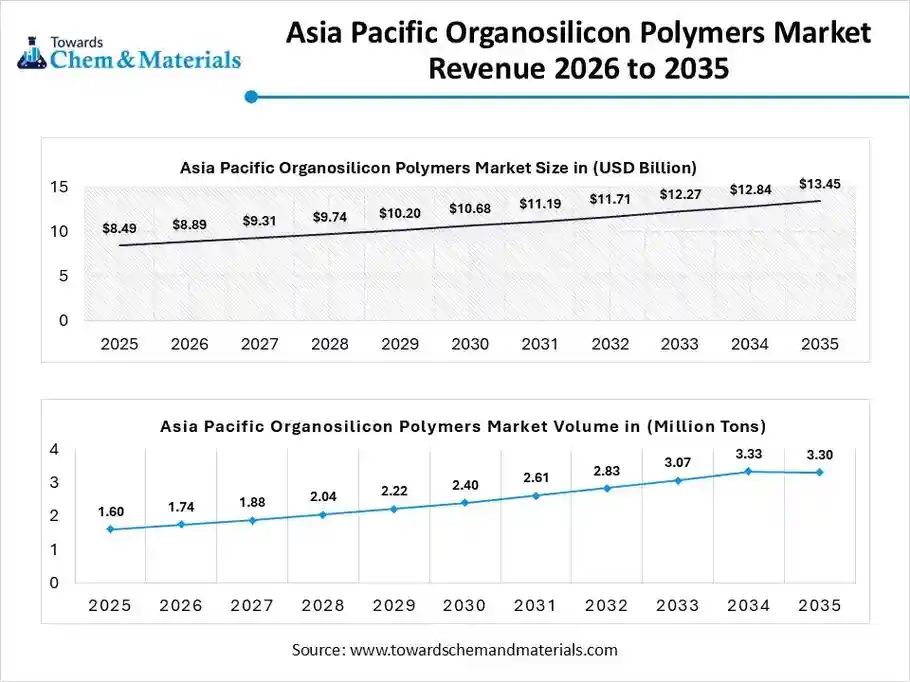

The Asia Pacific organosilicon polymers market size was valued at USD 8.49 billion in 2025 and is expected to be worth around USD 13.45 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 4.73% over the forecast period from 2026 to 2035.

The Asia Pacific organosilicon polymers market volume was estimated at 1.6 million tons in 2025 and is projected to reach 3.3 million tons by 2035, growing at a CAGR of 8.47% from 2026 to 2035. Asia Pacific dominated the organosilicon polymers market with approximately 45% share in 2025, due to the ongoing industrial expansion and heavy manufacturing bases. Moreover, the sectors like electronics, construction, and consumer goods have seen under the heavy demand for the organosilicon polymers in the region nowadays. Also, factors like skilled labor and higher production volume have been driving the regional growth in recent years.

Stronger Supply Chains Power China’s Leadership

China maintained its dominance in the market, owing to the presence of the heavy raw material supply and advanced processing facilities. Also, the stronger domestic demand for the organosilicon polymers with rapid testing and scaling facilities has driven investor confidence in the industry's future in the country. Moreover, the manufacturers in China have seen in focusing the improvement of performance with affordability.

North America Organosilicon Polymers Market Examination

The North America organosilicon polymers market volume was estimated at 1.0 million tons in 2025 and is projected to reach 1.9 million tons by 2035, growing at a CAGR of 7.49% from 2026 to 2035. North America is expected to capture a major share of the organosilicon polymers market with a rapid CAGR, owing to the greater shift towards precision materials. Moreover, the region has seeking materials that perform consistently under extreme pressure, where the organosilicon polymer is expected to emerge as an ideal material in the coming years, as per the future industry expectations.

Advanced Chemistry Drives United States Organosilicon Growth

The United States is expected to emerge as a prominent country for the organosilicon polymers market in the coming years, akin to a heavy focus on innovation and advanced chemistry. Also, the country has seen in replacing organosilicon polymers with normal plastic to tackle environmental and heat resistance challenges and fulfill the requirement of electrical insulation.

Global Organosilicon Polymers (Polysiloxane) Market Volume and Share, By Region, 2025-2035

| By Region | Market Volume Share (%), 2025 | Market Volume ( Million Tons)2025 | Market Volume (Million Tons)2035 | CAGR(%) 2026-2035 | Market Volume Share (%), 2035 |

| North America | 28.41% | 1.0 | 1.9 | 7.49% | 27.41% |

| Europe | 20.10% | 0.7 | 1.3 | 7.33% | 19.14% |

| Asia Pacific | 45.00% | 1.6 | 3.3 | 8.47% | 47.12% |

| Latin America | 4.01% | 0.1 | 0.3 | 8.27% | 4.13% |

| Middle East & Africa | 2.48% | 0.1 | 0.2 | 6.49% | 2.20% |

Europe Organosilicon Polymers Market Evaluation

The Europe organosilicon polymers market volume was estimated at 0.7 million tons in 2025 and is projected to reach 1.3 million tons by 2035, growing at a CAGR of 7.33% from 2026 to 2035. Europe is a notably growing region, owing to increased demand for reliable materials that meet strict performance and safety requirements in the region. European manufacturers emphasize lifecycle performance, meaning materials must perform consistently over many years. Organosilicon polymers meet these expectations in applications such as sealants, coatings, and electrical insulation.

Germany Builds Growth on Tested Materials

Germany is expected to gain a major industry share, as the country has adopted measures to enhance efficiency and product durability. Manufacturers value materials that perform consistently under demanding conditions. These polymers support long-term reliability in industrial and construction applications. Moreover, the German companies integrate materials only after thorough testing, which slows rapid adoption but strengthens long-term growth.

")

Organosilicon Polymers Market Study in the Middle East and Africa

The Middle East and Africa organosilicon polymers market volume was estimated at 0.1 million tons in 2025 and is projected to reach 0.2 million tons by 2035, growing at a CAGR of 6.49% from 2026 to 2035. The Middle East and Africa are expected to capture a notable share of the industry, due to large infrastructure and industrial development projects. Materials used in this region must withstand extreme heat, sunlight, and environmental stress as organosilicon polymers perform well under these conditions, making them suitable for construction and energy-related applications.

Saudi Arabia Advances with Durable Materials

Saudi Arabia is expected to emerge as a prominent country, akin to industrial modernization and large-scale infrastructure development. Also, the country focuses on materials that support durability, efficiency, and reduced maintenance. As Saudi Arabia builds advanced industrial capacity, demand for reliable materials continues to increase.

Latin America Organosilicon Polymers Market Evaluation

The Latin America organosilicon polymers market volume was estimated at 0.1 million tons in 2025 and is projected to reach 0.3 million tons by 2035, growing at a CAGR of 8.27% from 2026 to 2035. Latin America is a notably growing region due to the regional industries seeking affordable ways to improve material performance. Organosilicon polymers enhance durability and weather resistance without requiring major production changes. This makes them attractive for construction and manufacturing applications in the region for the future period.

Performance Polymers Power Brazil’s Industries

Brazil is expected to gain a major industry share, akin to the strong need from the construction and industrial sectors. These polymers improve product life and reduce maintenance needs. Moreover, the industries in the country value materials that enhance performance while controlling costs.

Top Vendors in the Organosilicon Polymers Market & Their Offerings:

- Dow Inc. (formerly Dow Corning): A global materials science company that provides a broad range of technology-based products, including high-performance silicones and specialty materials for consumer care, infrastructure, and packaging applications.

- Wacker Chemie AG: A global chemical company with a strong focus on silicones, polymers, and biosolutions, specializing in a wide range of silicone products used in construction, coatings, and electronics.

- Shin-Etsu Chemical Co., Ltd.: A world leader in silicone production, offering a vast array of high-performance silicone fluids, resins, and rubbers for diverse applications including automotive, electronics, and cosmetics.

- Momentive Performance Materials Inc: A global high-performance silicones and advanced materials company that provides innovative solutions for industries requiring specialized materials for applications in automotive, electronics, and construction.

- Elkem ASA (Bluestar)

- BASF SE

- Evonik Industries AG

- Hoshine Silicon Industry Co., Ltd.

- KCC Corporation

- Stockwell Elastomerics, Inc.

- Saint-Gobain Performance Plastics

- Specialty Silicone Products, Inc.

- CSL Silicones Inc.

- Kaneka Corporation

- Zhejiang Xinan Chemical Industrial Group (Wynca)

- Jiangsu Yangnong Chemical Group

- Mitsubishi Chemical Group

- Silchem, Inc.

- Innospec Inc.

- NuSil Technology LLC (Avantor)

Segments Covered in the Report

By Product Type

- Silicone Rubbers

- Silicone Fluids/Oils

- Silicone Resins

- Silicone Emulsions

- Silicone Gels

By End-Use Industry

- Building & Construction

- Automotive & Transportation (including EVs)

- Electrical & Electronics

- Healthcare & Medical Devices

- Personal Care & Cosmetics

- Industrial & Manufacturing

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)