Content

What is the current U.S. Polypropylene Compounds Market Size and Share?

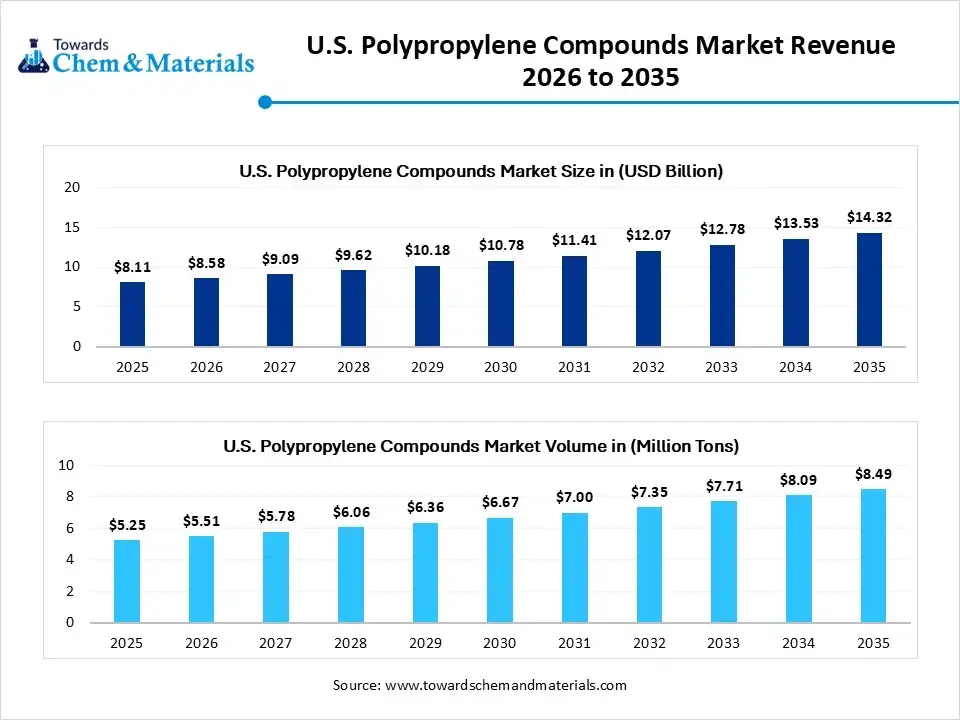

The U.S. polypropylene compounds market size was valued at USD 8.11 billion in 2025, is estimated to reach USD 8.58 billion in 2026, and is projected to reach USD 14.32 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035. In terms of volume, the U.S. polypropylene compounds market is projected to grow from 5.25 million tons in 2025 to 8.49 million tons by 2035. growing at a CAGR of 4.92% from 2026 to 2035. The U.S. polypropylene compounds market is projected to grow steadily through the forecast period, supported by increasing demand for lightweight, durable, and cost-effective materials across automotive, packaging, construction, and electronics applications. Growth is being driven by the ongoing shift toward lightweighting in vehicles, sustainability initiatives, and rising adoption of advanced polypropylene formulations that improve mechanical strength, thermal stability, and process efficiency.

The market encompasses the manufacturing, sales, and distribution of customized thermoplastic materials generated by blending base polypropylene with additives, fillers, and reinforcing agents. These compounds are highly valued for their lightweight nature, cost-efficiency, and strong mechanical performance across U.S. manufacturing industries.

Polypropylene (PP) compounds are robust, stiff, and crystalline thermoplastics that offer performance advantages across diverse sectors. They are widely used in automotive, packaging, textiles, construction, and consumer goods. At room temperature, polypropylene shows strong resistance to fats and most organic solvents, except strong oxidizing agents. Containers made from this polymer are also suitable for storing many non-oxidizing acids and bases.

Market Highlights

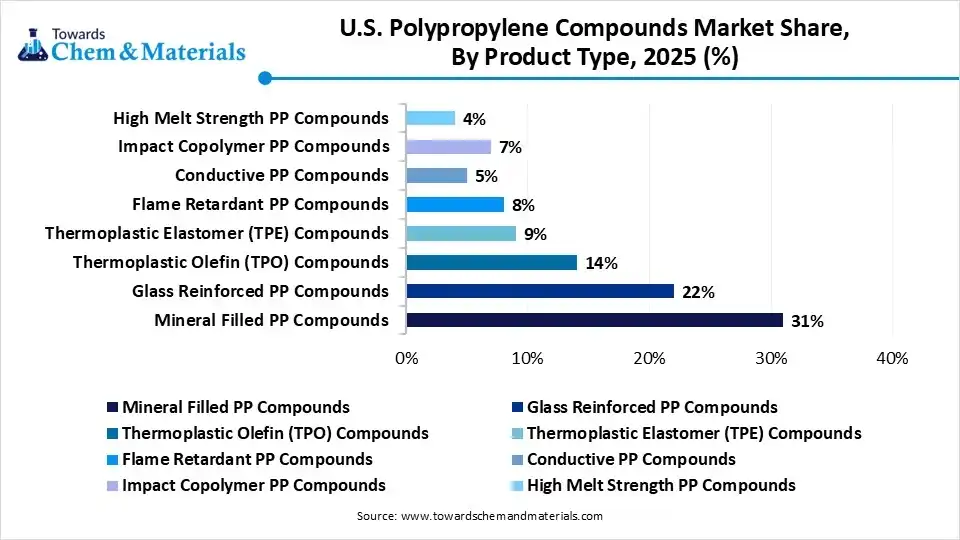

- By product type, the mineral filled PP compounds segment dominated the market with the largest share of 31% in 2025. The dominance of the segment can be attributed to the increasing demand for lightweight components.

- By product type, the flame retardant PP compounds segment is expected to grow at the fastest CAGR of 6.84% over the forecast period. The growth of the segment can be credited to the growth in EV battery systems.

- By polymer type, the homopolymer polypropylene segment dominated the market with a share of 44% in 2025. The dominance of the segment can be linked to its rigidity and cost-effectiveness.

- By polymer type, the recycled polypropylene segment is expected to grow at the fastest CAGR of 7.42% over the forecast period. The growth of the segment can be driven by manufacturers increasingly integrating PCR and PIR materials into production.

- By filler type, the talc segment dominated the market with the largest share of 29% in 2025. The dominance of the segment is owing to the surge in the manufacturing of lightweight vehicles.

- By filler type, the glass fiber segment is expected to grow at the fastest CAGR of 6.55% over the forecast period. The growth of the segment is due to automotive lightweighting strategies.

- By manufacturing process, the injection molding segment dominated the market with the largest share of 46% in 2025. The dominance of the segment can be attributed to the increasing adoption of complex molded components.

- By manufacturing process, the thermoforming segment is expected to grow at the fastest CAGR of 6.22% during the forecast period. The growth of the segment can be credited to the increasing demand for lightweight food packaging.

- By application, the automotive segment dominated the market with the largest share of 36% in 2025 and is expected to grow at the fastest CAGR of 6.44% over the forecast period. The dominance and growth of the segment can be linked to the growing adoption of polypropylene compounds.

- By end user, the automotive OEMs segment dominated the market with the largest share of 34% in 2025 and is expected to grow at the fastest CAGR of 6.52% over the forecast period. The dominance and growth of the segment can be driven by increasing demand for superior interior and exterior components.

- By property, the high impact resistance segment dominated the market with the largest share of 26% in 2025. The dominance of the segment is owing to the increasing focus on impact resistance polypropylene compounds.

- By property, the flame retardancy segment is expected to grow at the fastest CAGR of 6.62% during the projected period. The growth of the segment is due to safety regulations driving the adoption of advanced fire resistance materials.

- By distribution channel, the direct sales segment dominated the market with the largest share of 48% in 2025. The dominance of the segment can be attributed to ongoing strategic partnerships.

- By distribution channel, the online B2B platform segment is expected to grow at the fastest CAGR of 7.16% during the study period. The growth of the segment can be credited to the increasing E-commerce adoption.

Recent Market Trends

- The growing demand for polypropylene compounds across end-use sectors is a major market trend supporting growth. These materials provide a valuable combination of low weight, high strength, chemical resistance, and cost-effectiveness.

- Polypropylene compounds are increasingly replacing conventional materials such as glass, metals, and other plastics in many applications. The transition toward lightweight materials in automotive, aerospace, and consumer goods is being driven by the need to improve fuel efficiency and overall product performance.

- Ongoing innovations in automotive lightweighting are another major factor driving demand. Pressure to reduce vehicle emissions and improve EV range is accelerating the use of reinforced PP compounds in exterior, interior, and under-the-hood components.

How are Cutting-Edge Technologies Revolutionizing the U.S. Polypropylene Compounds Market?

Advanced technologies such as nanotechnology, advanced composites, and bio-based material development are reshaping the market. These innovations improve thermal resistance, mechanical strength, and environmental performance, especially for packaging and automotive applications. In addition, innovations in polymer technology are expanding the use of PP powders and advanced feedstocks in additive manufacturing and other specialized processing methods.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 8.11 Billion / 5.25 Million Tons |

| Revenue Forecast in 2035 | USD 14.32 Billion / 8.49 Million Tons |

| Growth Rate | CAGR 5.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Segment Covered | By Product Type, By Polymer Type, By Filler Type, By Manufacturing Process, By Application, By End User, By Property, By Distribution Channel |

| Key companies profiled | LyondellBasell, ExxonMobil Corporation, Avient Corporation, RTP Company, Advanced Composites, Inc., Trinseo, RheTech, Inc., SABIC, Mitsui Chemicals America, Borealis. |

Supply Chain Analysis of the U.S. Polypropylene Compounds Market

- Feedstock Procurement:It involves the sourcing and purchasing of essential materials needed to manufacture polypropylene (PP) compounds. It involves securing propylene monomer, which is then combined with additives, fillers, and reinforcements.

- Major Players: LyondellBasell, ExxonMobil

- Chemical Synthesis and Processing:It covers how raw propylene gas is transformed into base polymers and subsequently altered using advanced compounding techniques to create high-performance plastics.

- Major Players: SABIC, Braskem America

- Packaging and Labeling:It refers to the highly specialized material needs, industrial logistics, standard container practices, and regulatory guidelines used to securely distribute, store, and identify compounded polypropylene pellets.

- Major Players: Avient Corporation, ExxonMobil Chemical

- Regulatory Compliance and Safety Monitoring: It represents a section evaluating the legal, environmental, and safety frameworks governing plastic production. It analyses how stringent standards dictate the formulation, testing, and approval of polypropylene (PP) compounds.

- Major Players: Washington Penn, Avient Corporation

U.S. Polypropylene Compounds Market's Regulatory Landscape

| State | Key Regulation |

| California (SB 54) | California dictates the nation's most aggressive packaging frameworks. Under California SB 54, single-use plastic packaging utilizing PP compounds must achieve a 30% recycling rate by 2028, scaling up to 65% by 2032. |

| Oregon (SB 582) | The Oregon Recycling Modernization Act enforces producer compliance through shared financial responsibility to modernize local sorting for polymers like PP. |

| Colorado (HB 22-1355) | roducers utilizing PP packaging must join a state-designated nonprofit Producer Responsibility Organization (Circular Action Alliance), report outputs, and pay localized eco-fees. Non-compliant entities face state market bans. |

Market Dynamics

Drivers

Innovations in Material Technology

Technological innovations in materials formulation and processing techniques play a key role in the development of high-performance polypropylene compounds. These advancements can enable market players to tailor the properties of polypropylene compounds to fulfill specific industry needs and demands. In addition, ongoing research and development initiatives in polypropylene compounds have yielded advanced formulations tailored for niche markets and high-value applications. These innovations broaden the market's commercial viability and attract a diversified customer base.

Restraint

Environmental Concerns

Polypropylene, a petroleum-based plastic, can have adverse effects on the environment, which is the major factor hindering the growth of the market. As consumers are becoming more aware of the negative effects of plastic, the need for sustainable alternatives will rise significantly. Moreover, crude oil and natural gas, which serve as primary feedstocks in the manufacturing of polypropylene, exhibit significant price volatility and are highly susceptible to sudden fluctuations.

Opportunity

Growth of Construction Sector

The leading consumer of polypropylene compounds is the construction sector, which uses them in different applications like roofing materials, pipes, and insulation. The increasing demand for housing and infrastructure projects in emerging countries is creating lucrative opportunities in the market shortly. Furthermore, automakers and electronics manufacturers increasingly favor localized production facilities with shortened lead times to facilitate rapid design iterations and accelerated product refresh cycles, impacting positive market growth soon.

Segmental Insights

By Product Type Insights

The mineral-filled PP compounds segment dominated the market with the largest share of 31% in 2025. The dominance of the segment can be attributed to the increasing demand for lightweight components sustaining market penetration and cost-effective filler materials supporting high-volume production efficiency. Automotive and appliance market players are increasingly using mineral-filled compounds.

")

The flame retardant PP compounds segment held a market share of 8% in 2025 and is expected to grow at the fastest CAGR of 6.84% over the forecast period. The growth of the segment can be credited to the growth in EV battery systems strengthening demand for fire-resistance materials along with the growing adoption of flame-retardant compounds from electrical and electronics manufacturers.

By Polymer Type Insights

The homopolymer polypropylene segment dominated the market with a share of 44% in 2025. The dominance of the segment can be linked to its rigidity and cost-effectiveness across many industrial applications along with the growing demand from the packaging and consumer goods sectors. Large-scale manufacturing supports wide market penetration.

U.S. Polypropylene Compounds Market Share, By Polymer Type, 2025 (%)

| By Polymer Type | Revenue Share, 2025 (%) |

| Homopolymer Polypropylene | 44% |

| Copolymer Polypropylene | 39% |

| Recycled Polypropylene | 17% |

The recycled polypropylene segment held a market share of 17% in 2025 and is expected to grow at the fastest CAGR of 7.42% over the forecast period. The growth of the segment can be driven by manufacturers increasingly integrating PCR and PIR materials into production along with ongoing investments in circular economy initiatives.

By Filler Type Insights

The talc segment dominated the market with the largest share of 29% in 2025. The dominance of the segment is owing to the surge in manufacturing of lightweight vehicles and cost-effective reinforcement properties supporting extensive industrial applications. Talc fillers improve stiffness and thermal resistance in automotive applications.

U.S. Polypropylene Compounds Market Share, By Filler Type, 2025 (%)

| By Filler Type | Revenue Share, 2025 (%) |

| Talc | 29% |

| Calcium Carbonate | 18% |

| Glass Fiber | 24% |

| Carbon Fiber | 8% |

| Mineral Fillers | 10% |

| Natural Fiber | 5% |

| Conductive Additives | 7% |

The glass fiber segment held a market share of 24% in 2025 and is expected to grow at the fastest CAGR of 6.55% over the forecast period. The growth of the segment is due to automotive lightweighting strategies accelerating utilization coupled with its ability to improve mechanical strength and overall dimensional stability.

By Manufacturing Process Insights

The injection molding segment dominated the market with the largest share of 46% in 2025. The dominance of the segment can be attributed to the increasing adoption of complex molded components and automation technologies enhancing operational efficiency. It also possesses high productivity and durability.

U.S. Polypropylene Compounds Market Share, By Manufacturing Process, 2025 (%)

| By Manufacturing Process | Revenue Share, 2025 (%) |

| Injection Molding | 46% |

| Extrusion | 24% |

| Blow Molding | 11% |

| Thermoforming | 8% |

| Compression Molding | 6% |

| Rotational Molding | 5% |

The thermoforming segment held a market share of 8% in 2025 and is expected to grow at the fastest CAGR of 6.22% during the forecast period. The growth of the segment can be credited to the increasing demand for lightweight food packaging and automotive interior components along with market players preferring cost-efficient technologies.

By Application Insights

The automotive segment dominated the market with the largest share of 36% in 2025 and is expected to grow at the fastest CAGR of 6.44% over the forecast period. The dominance and growth of the segment can be linked to the growing adoption of polypropylene compounds by automotive market players to reduce vehicle weight along with the growth of EV manufacturing boosting advanced polymer demand.

U.S. Polypropylene Compounds Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Automotive | 36% |

| Packaging | 24% |

| Electrical & Electronics | 12% |

| Building & Construction | 10% |

| Consumer Goods | 8% |

| Medical | 5% |

| Industrial | 3% |

| Textiles | 2% |

The packaging segment held a market share of 24% in 2025. The growth of the segment can be attributed to the increasing demand for recyclable rigid packaging and ongoing e-commerce expansion across the globe. Food and consumer goods packaging industries are using polypropylene compounds for lightweight solutions.

By End User Insights

The automotive OEMs segment dominated the market with the largest share of 34% in 2025 and is expected to grow at the fastest CAGR of 6.52% over the forecast period. The dominance and growth of the segment can be driven by increasing demand for superior interior and exterior components and sustainability initiatives boosting recyclable polymer usage. Vehicle manufacturers are increasingly using lightweight polypropylene compounds to enhance fuel efficiency.

U.S. Polypropylene Compounds Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Automotive OEMs | 34% |

| Packaging Manufacturers | 25% |

| Electronics Manufacturers | 13% |

| Construction Companies | 10% |

| Consumer Goods Manufacturers | 9% |

| Healthcare Manufacturers | 5% |

| Industrial Equipment Manufacturers | 4% |

The packaging manufacturers segment held a market share of 25% in 2025. The growth of the segment can be linked to the increasing food safety needs strengthening polymer utilization and a surge in high-value packaging production. Packaging companies are increasingly adopting polypropylene solutions for flexible and rigid packaging solutions.

By Property Insights

The high impact resistance segment dominated the market with the largest share of 26% in 2025. The dominance of the segment is owing to the increasing focus on impact-resistance polypropylene compounds for structural durability and improved crash performance supporting vehicle safety applications.

U.S. Polypropylene Compounds Market Share, By Property, 2025 (%)

| By Property | Revenue Share, 2025 (%) |

| High Impact Resistance | 26% |

| Heat Resistance | 18% |

| Chemical Resistance | 17% |

| Flame Retardancy | 11% |

| Lightweight | 16% |

| Electrical Conductivity | 7% |

| UV Resistance | 5% |

The flame retardancy segment held a market share of 11% in 2025 and is expected to grow at the fastest CAGR of 6.62% during the projected period. The growth of the segment is due to safety regulations driving the adoption of advanced fire-resistance materials and non-halogenated solutions gaining strong commercial traction over the upcoming period.

By Distribution Channel Insights

The direct sales segment dominated the market with the largest share of 48% in 2025. The dominance of the segment can be attributed to ongoing strategic partnerships strengthening market positioning and bulk purchasing improving overall pricing efficiency and supply chain stability.

U.S. Polypropylene Compounds Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 48% |

| Distributors & Wholesalers | 31% |

| Online B2B Platforms | 8% |

| Third-Party Compounders | 13% |

The online B2B platforms segment held a market share of 8% in 2025 and is expected to grow at the fastest CAGR of 7.16% during the study period. The growth of the segment can be credited to the increasing e-commerce adoption, improving overall transaction efficiency along with the rapid integration of online supply chains boosting market expansion.

Recent Development

- In January 2026, Saudi Basic Industries Corp. (SABIC) entered into agreements to divest two of its overseas businesses in Europe and the Americas for a combined total of $950 million. This strategic initiative aligns with the corporation's ongoing efforts to optimize its asset portfolio and reallocate capital toward higher-yield segments. (Source: www.arabnews.com)

U.S. Polypropylene Compounds Market Companies

- LyondellBasell: LyondellBasell (LYB) is the dominant market leader in the U.S. polypropylene (PP) compounds market, controlling a significant portion of both domestic supply and the global market.

- ExxonMobil Corporation: ExxonMobil Corporation is a major supplier in the U.S. polypropylene (PP) compounds market, focusing on high-performance resins. Their portfolio is driven by the automotive, packaging, and appliance industries, catering to lightweighting and sustainability trends.

Other Companies in the Market

- Avient Corporation

- RTP Company

- Advanced Composites, Inc.

- Trinseo

- RheTech, Inc.

- SABIC

- Mitsui Chemicals America

- Borealis

Segments Covered in the Report

By Product Type

- Mineral Filled PP Compounds

- Talc Filled

- Calcium Carbonate Filled

- Glass Bead Filled

- Glass Reinforced PP Compounds

- Short Glass Fiber Reinforced

- Long Glass Fiber Reinforced

- Thermoplastic Olefin (TPO) Compounds

- Thermoplastic Elastomer (TPE) Compounds

- Flame Retardant PP Compounds

- Halogenated

- Non-Halogenated

- Conductive PP Compounds

- Impact Copolymer PP Compounds

- High Melt Strength PP Compounds

By Polymer Type

- Homopolymer Polypropylene

- Copolymer Polypropylene

- Random Copolymer

- Block Copolymer

- Recycled Polypropylene

- Post-Consumer Recycled PP

- Post-Industrial Recycled PP

By Filler Type

- Talc

- Calcium Carbonate

- Glass Fiber

- Carbon Fiber

- Mineral Fillers

- Natural Fiber

- Conductive Additives

By Manufacturing Process

- Injection Molding

- Extrusion

- Blow Molding

- Thermoforming

- Compression Molding

- Rotational Molding

By Application

- Automotive

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Battery Components

- Packaging

- Rigid Packaging

- Flexible Packaging

- Electrical & Electronics

- Appliance Components

- Cable Insulation

- Consumer Electronics

- Building & Construction

- Pipes & Fittings

- Insulation Components

- Panels & Sheets

- Consumer Goods

- Furniture

- Household Appliances

- Storage Products

- Medical

- Industrial

- Textiles

By End User

- Automotive OEMs

- Packaging Manufacturers

- Electronics Manufacturers

- Construction Companies

- Consumer Goods Manufacturers

- Healthcare Manufacturers

- Industrial Equipment Manufacturers

By Property

- High Impact Resistance

- Heat Resistance

- Chemical Resistance

- Flame Retardancy

- Lightweight

- Electrical Conductivity

- UV Resistance

By Distribution Channel

- Direct Sales

- Distributors & Wholesalers

- Online B2B Platforms

- Third-Party Compounders

FAQ's

Select User License to Buy

Figures (2)