Content

What is the Current Polyolefin Market Size and Share?

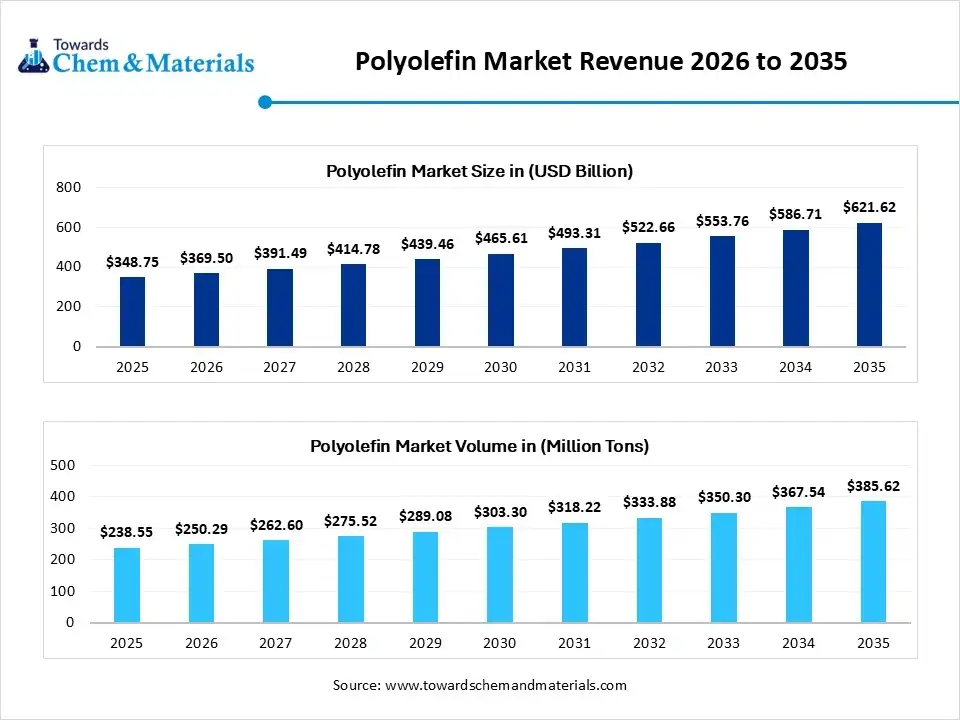

The global polyolefin market size was valued at USD 348.75 billion in 2025, is estimated to reach USD 369.50 billion in 2026, and is projected to reach USD 621.62 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035. In terms of volume, the polyolefin market is projected to grow from 238.55 million tons in 2025 to 385.62 million tons by 2035. growing at a CAGR of 4.92% from 2026 to 2035. The greater demand for the packaging industry has fueled the industry's potential in recent years.

The types of plastics that are made from simple chemicals called olefins, and primarily propylene and ethylene, are known as the polyolefins. Moreover, having unique properties such as being lightweight, durable, flexible, and affordable, polyolefins have gained major industry attention in recent years. Moreover, industries such as plastics and healthcare have been using it as an ideal material nowadays. The manufacturing regions, like North America and Asia, have been seeing heavy demand for polyolefin while investing in R&D for sustainable plastic manufacturing.

")

Also, the industry is changing because customers and governments want more environmentally friendly products. Furthermore, the new technologies are also helping manufacturers produce stronger and better-quality materials while using less energy. Another important change is the growth of bio-based and recycled polyolefins, which are made from renewable or reused materials instead of only fossil fuels. Moreover, the polyolefin industry is growing because plastic products are still needed in many sectors. At the same time, companies are trying to balance business growth with sustainability and environmental responsibility. The future of the industry will mainly depend on innovation, recycling, and smarter production methods.

Market Highlights

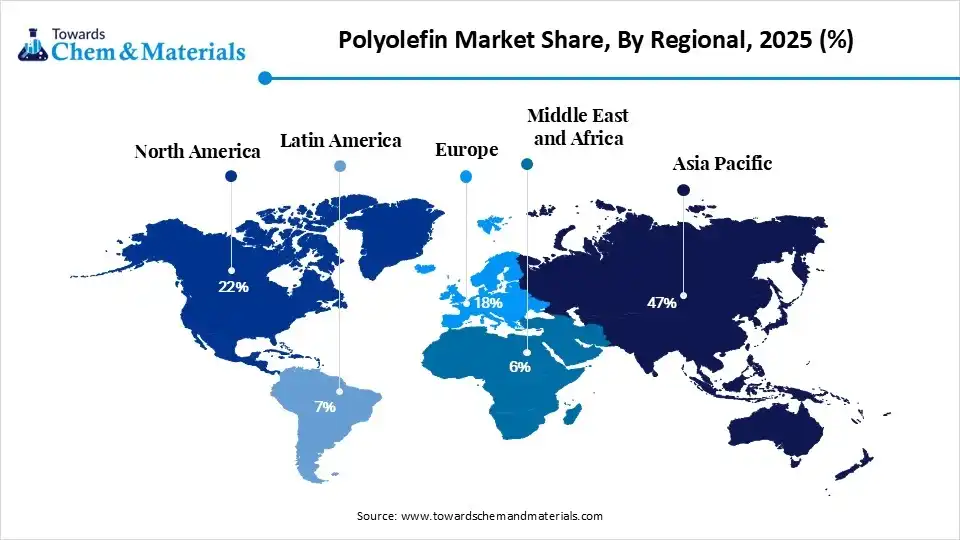

- By region, Asia Pacific dominated the market with a share of 47% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 5.43% in the forecast period, due to the region having large manufacturing industries, rapid urbanization, and a huge consumer population.

- By region, North America is notably growing with 22% market share in 2025, owing to its strong technological innovation, shale gas availability, and advanced manufacturing capabilities.

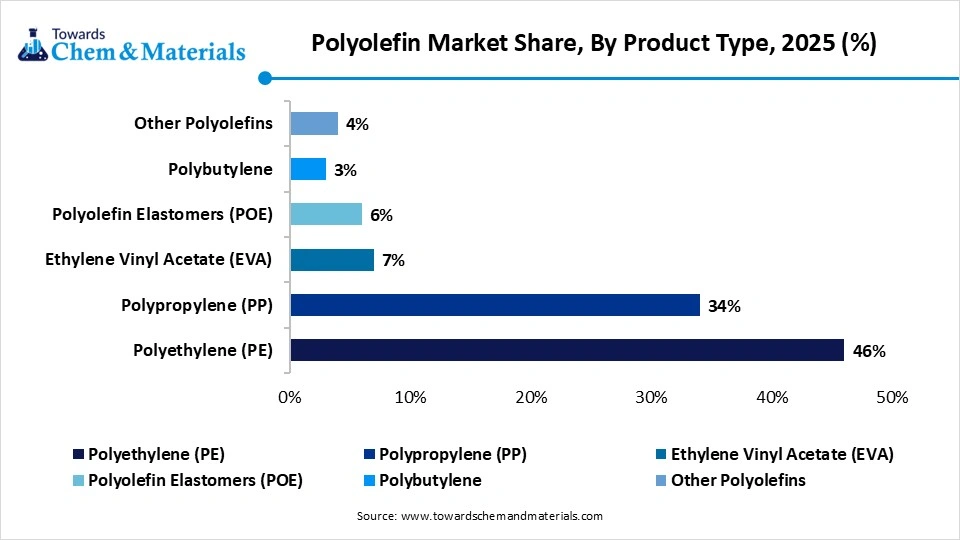

- By product type, the polyethylene (PE) waste segment dominated the market with a 46% share in 2025, as it is one of the most widely used and affordable plastics in the world.

- By product type, the polypropylene (PP) segment held the 34% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.21% in the forecast period, owing to its offering higher strength, better heat resistance, and improved durability compared to many other plastics.

- By technology, the injection molding segment dominated the market with a 29% share in 2025, as it is one of the fastest and most efficient methods for producing plastic products in large quantities.

- By technology, the film and sheet processing segment held a 16% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 5.24% in the forecast period, due to rapid growth of flexible packaging and e-commerce industries.

- By feedstock, the naphtha segment dominated the market with a 42% share in 2025, as it has been one of the most commonly available raw materials for plastic production, especially in Asia and Europe.

- By feedstock, the natural gas liquids (NGL) segment held the 38% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.36% in the forecast period, owing to their being cleaner, more cost-effective, and environmentally better compared to traditional oil-based feedstocks like naphtha.

- By form, the pellets/granule segment dominated the market with a 48% share in 2025, owing to the fact that they are the easiest and most convenient form for transportation, storage, and industrial processing.

- By form, the film segment held the 26% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.44% in the forecast period in 2025, owing to flexible plastic films becoming more important in packaging, healthcare, agriculture, and industrial applications.

- By application, the packaging segment dominated the market with a 39% share in 2025, owing to almost every industry needing safe, lightweight, and affordable packaging materials.

- By application, the automotive segment held the 14% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.31% in the forecast period, as vehicle manufacturers are focusing strongly on lightweight and fuel-efficient vehicles.

- By distribution channel, the direct sales segment dominated the market with a 46% share in 2025, owing to large industrial buyers usually preferring to purchase materials directly from manufacturers.

- By distribution channel, the online procurement platforms segment held the 9% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.94% in the forecast period, as digital purchasing is becoming faster, easier, and more transparent for businesses.

- By sustainability, the virgin polyolefins segment dominated the market with a 71% share in 2025, owing to their providing high purity, consistent quality, and strong performance for industrial applications.

- By sustainability, the recycled polyolefins segment held a 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.42% in the forecast period, as sustainability and environmental protection are becoming top priorities worldwide.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 348.75 Billion | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 621.62 Billion

- Asia Pacific: largest Market Revenue Share of 37% in 2025.

- Market Estimated Volume (2025): 238.55 Million Tons | Volume CAGR (2026–2035): 4.92%

- Market Projected Volume (2035): 385.62 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,130/Ton

- Average Selling Price (2025): USD 1,395/Ton

- Pricing CAGR (2025–2035): 3.49%

Recent Market Trends:

- The developing heavy interest in recyclable polyolefins has driven strategic transformation and sectoral scalability in recent years. Also, the major firms are trying to make products which easy to recycle and reuse in the past few years.

- The greater emergence of packaging and the e-commerce industry has allowed stakeholders to capitalize on growth opportunities in the current period. Also, the need for durable, lightweight, and low-cost packaging materials is leading to the sales of polyolefins.

- The shift towards smart materials and advanced production technologies is heavily strengthening the foundation for the future sector growth, where companies are focusing on the development of specialty polyolefins nowadays, as per the latest industry survey.

Chemical Recycling Redefining Plastic Manufacturing

The industry has observed a strong move from traditional plastic production to circular and recycling-based production systems in recent years. Also, earlier, most polyolefins were made only from crude oil and natural gas. Now, companies are focusing on chemical recycling and bio-based production methods. Chemical recycling helps convert old plastic waste back into raw material that can be reused for making new plastics.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 369.50 Billion/ 250.29 Million Tons |

| Revenue Forecast in 2035 | USD 621.62 Billion/ 385.62 Million Tons |

| Growth Rate | CAGR 5.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Technology, By Feedback, By Form, By Application, By Distribution Channel, By Sustainability, By Region |

| Key companies profiled | ExxonMobil Corporation, LyondellBasell Industries N.V., SABIC, The Dow Chemical Company, China Petrochemical Corporation, TotalEnergies SE, INEOS Group Holdings S.A., Chevron Phillips Chemical Company LLC. |

Supply Chain Analysis of the Polyolefin Market:

Distribution to Industrial Users

- Polyolefin resins reach industrial manufacturers through a streamlined supply chain optimized for volume. Large-scale plants typically receive bulk deliveries via hopper railcars or pneumatic tankers, while smaller facilities utilize super sacks.

- Once on-site, these versatile pellets are converted into high-performance textiles, protective packaging, and durable piping through specialized thermal processing.

Chemical Synthesis and Processing

- Polyolefin synthesis involves polymerizing ethylene or propylene using advanced catalysts like Ziegler-Natta or metallocene.

- Industry leaders like ExxonMobil, LyondellBasell, and Dow utilize high-pressure or gas-phase reactors to create resin.

These polymers are subsequently extruded into pellets, providing the essential raw material for diverse global manufacturing applications.

Regulatory Compliance and Safety Monitoring

- Polyolefin production stick to strict safety protocols governed by agencies like OSHA and REACH.

- These frameworks ensure chemical stability and worker protection. Quality monitoring by the FDA or EFSA is critical for food-grade applications, while ISO standards guide environmental emissions and operational safety throughout the manufacturing lifecycle.

Polyolefin Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | U.S. Food and Drug Administration (FDA). | Title 21 CFR § 177.1520 (Olefin Polymers). | Section (c): Specifies purity standards, including maximum extractable fractions in n-hexane and maximum soluble fractions in xylene. |

| Europe | European Commission (EC) |

Commission Regulation (EU) No 10/2011 (Plastics in contact with food). | Specific Migration Limits (SML): Restricts the amount of substances that can migrate into food. |

| China | State Administration for Market Regulation (SAMR) and National Health Commission (NHC) | GB 4806.6-2016 (National Food Safety Standard for Plastic Resins) and GB 4806.7-2023 (Plastic Materials and Articles). | Waste Management: National strategies, including the "14th Five-Year Plan," restrict non-degradable single-use plastics and emphasize Extended Producer Responsibility (EPR) |

Market Dynamics

Driver

Packaging and Automotive Driving the Demand

The demand for lightweight, affordable, and durable plastic materials is poised to drive the industry for long-term expansion. Also, industries like packaging, automotive, healthcare, agriculture, and construction use polyolefins because they are strong, flexible, and cost-effective. The rise of online shopping is also increasing the need for plastic packaging materials. In the automotive sector, companies are using more polyolefins to reduce vehicle weight and improve fuel efficiency. Rapid industrial growth in developing countries is another important reason for market growth.

Restraint

Strict Policies Restraining Industry Expansion

The increasing concern about plastic waste and environmental pollution is expected to create growth barriers for the industry participants in the current period. Moreover, many governments are introducing strict regulations to reduce single-use plastics and improve recycling systems. This creates pressure on manufacturers to develop eco-friendly alternatives, which can increase production costs. Also, the fluctuation in crude oil prices because traditional polyolefins are mainly made from petroleum-based raw materials.

Opportunity

Green Technologies Driving Industrial Opportunities

The growth of recyclable and bio-based plastics is expected to create lucrative opportunities for manufacturers during the forecast period. Also, the companies are investing heavily in sustainable materials because governments and consumers want environmentally friendly products. The increasing use of electric vehicles also creates new opportunities because lightweight plastic components help improve battery performance and vehicle efficiency. Furthermore, the emerging economies are also creating strong demand due to rising urbanization and industrialization.

Segmental Insights

Product Type Insights

Polyolefin Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Polyethylene (PE) | 46% |

| Polypropylene (PP) | 34% |

| Ethylene Vinyl Acetate (EVA) | 7% |

| Polyolefin Elastomers (POE) | 6% |

| Polybutylene | 3% |

| Other Polyolefins | 4% |

The Polyethylene (PE) Segment Dominated the Polyolefin Market with 46% Market Share in 2025

The polyethylene (PE) waste segment dominated the market with 46% share in 2025, as it is one of the most widely used and affordable plastics in the world. It is lightweight, moisture-resistant, flexible, and easy to process, which makes it suitable for many industries. Packaging companies use polyethylene heavily for plastic bags, bottles, films, and containers.

The polypropylene (PP) segment held the 34% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.21% in the forecast period, owing to it offers higher strength, better heat resistance, and improved durability compared to many other plastics. Industries like automotive, healthcare, electronics, and food packaging are increasing their use of polypropylene due to its lightweight and strong performance.

Technology Insights

The Injection Molding Segment Dominated the Market with 29% Market Share in 2025.

The injection molding segment dominated the market with 29% share in 2025, as it is one of the fastest and most efficient methods for producing plastic products in large quantities. This process allows manufacturers to create complex shapes with high precision and low material waste.

Polyolefin Market Share, By Technology, 2025 (%)

| By Technology | Revenue Share, 2025 (%) |

| Injection Molding | 29% |

| Blow Molding | 18% |

| Extrusion | 22% |

| Film & Sheet Processing | 16% |

| Rotational Molding | 5% |

| Thermoforming | 7% |

| Additive Manufacturing | 3% |

The film and sheet processing segment held the 16% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 5.24% in the forecast period, due to rapid growth of flexible packaging and e-commerce industries. Modern consumers prefer lightweight, convenient, and resealable packaging, which increases the demand for plastic films and sheets. Food packaging companies are also using advanced film materials to improve product freshness and safety.

Feedstock Insights

The Naphtha Segment Dominated the Polyolefin Market with 42% Market Share in 2025

The naphtha segment dominated the market with 42% share in 2025, as it has been one of the most commonly available raw materials for plastic production, especially in Asia and Europe. It is produced during crude oil refining and is heavily used in petrochemical industries to manufacture propylene and ethylene, which are main materials for polyolefins.

Polyolefin Market Share, By Feedstock, 2025 (%)

| By Feedstock | Revenue Share, 2025 (%) |

| Naphtha | 42% |

| Natural Gas Liquids (NGL) | 38% |

| Coal-Based Feedstock | 12% |

| Bio-Based Feedstock | 8% |

The natural gas liquids (NGL) segment held the 38% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.36% in the forecast period, owing to they are cleaner, more cost-effective, and environmentally better compared to traditional oil-based feedstocks like naphtha. Countries such as the United States have large shale gas reserves, which provide abundant natural gas liquids for petrochemical production.

Form Insights

The Pellets/Granule Segment Dominated the Market with 48% Market Share in 2025

The pellets/granule segment dominated the market with 48% share in 2025, owing to the they are the most convenient form for storage, transportation, and industrial processing. Manufacturers use these small plastic particles as raw material for producing a wide variety of products through moulding and extrusion processes.

Polyolefin Market Share, By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Pellets/Granules | 48% |

| Powder | 9% |

| Films | 26% |

| Sheets | 10% |

| Fibers | 7% |

The films segment held the 26% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.44% in the forecast period in 2025, owing to flexible plastic films are becoming more important in packaging, healthcare, agriculture, and industrial applications. Food companies prefer film packaging because it helps preserve freshness and extends product shelf life.

Application Insights

The Packaging Segment Dominated the Polyolefin Market with 39% Market Share in 2025

The packaging segment dominated the market with 39% share in 2025, owing to almost every industry needs safe, lightweight, and affordable packaging materials. Polyolefins are widely used in food packaging, beverage containers, plastic films, shopping bags, and protective wrapping because they are strong, moisture-resistant, and flexible.

Polyolefin Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Packaging | 39% |

| Automotive | 14% |

| Building & Construction | 13% |

| Electrical & Electronics | 9% |

| Healthcare | 7% |

| Agriculture | 6% |

| Consumer Goods | 5% |

| Textiles & Fibers | 4% |

The automotive segment held the 14% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.31% in the forecast period, as vehicle manufacturers are focusing strongly on lightweight and fuel-efficient vehicles. Polyolefins are widely used in dashboards, bumpers, interior panels, battery components, and seating systems because they are strong but lightweight. Electric vehicle production is also increasing rapidly, creating higher demand for advanced plastic materials.

Distribution Channel Insights

The Direct Sales Segment Dominated the Market with 46% Market Share in 2025

The direct sales segment dominated the market with 46% share in 2025, owing to large industrial buyers usually preferring to purchase materials directly from manufacturers. This approach helps companies receive a stable supply, better pricing, customized contracts, and technical support. Industries such as packaging, automotive, and construction require large quantities of polyolefins regularly, so direct business relationships become more efficient and cost-effective.

Polyolefin Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 46% |

| Distributors & Traders | 29% |

| Online Procurement Platforms | 9% |

| Contract Supply Agreements | 16% |

The online procurement platforms segment held the 9% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.94% in the forecast period, as digital purchasing is becoming faster, easier, and more transparent for businesses. Companies can compare prices, suppliers, product specifications, and delivery options more efficiently through an online system.

Sustainability Insights

The Virgin Polyolefins Segment Dominated the Market with 71% Market Share in 2025

The virgin polyolefins segment dominated the market with 71% share in 2025, owing to providing high purity, consistent quality, and strong performance for industrial applications. Manufacturers prefer virgin materials for food packaging, healthcare products, automotive parts, and electronics because these industries require strict safety and quality standards.

Polyolefin Market Share, By Sustainability, 2025 (%)

| By Sustainability | Revenue Share, 2025 (%) |

| Virgin Polyolefins | 71% |

| Recycled Polyolefins | 22% |

| Bio-Circular Polyolefins | 7% |

The recycled polyolefins segment held the 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.42% in the forecast period, as sustainability and environmental protection are becoming top priorities worldwide. Governments are introducing strict recycling rules, and consumers are demanding eco-friendly products. Companies are investing heavily in advanced recycling technologies to improve the quality and performance of recycled plastics.

Regional Insights

How will Asia Pacific Dominate the Polyolefin Market in 2025?

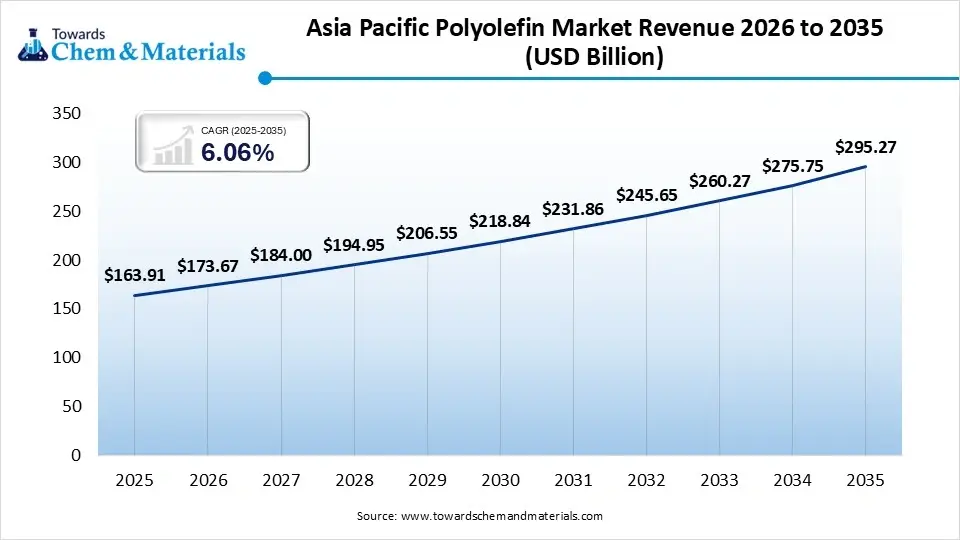

The Asia Pacific Polyolefin market size was estimated at USD 163.91 billion in 2025 and is projected to reach USD 295.27 billion by 2035, growing at a CAGR of 6.06% from 2026 to 2035. Asia Pacific dominated the market with a share of 47% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 5.43% in the forecast period, due to the region having large manufacturing industries, rapid urbanization, and a huge consumer population. Countries like China, India, Japan, and South Korea are major producers and consumers of plastic products. The packaging, automotive, electronics, and construction sectors are growing rapidly across the region, increasing polyolefin demand strongly.

")

China Expanding the Future of Polyolefins

China maintained its dominance in the market, owing to its being one of the world’s largest manufacturing and exporting countries. The country has a huge demand for packaging, electronics, automotive parts, and consumer goods, all of which require large amounts of polyolefins. China is also investing heavily in petrochemical plants and advanced recycling technologies to strengthen domestic production.

Polyolefin Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 47% |

| North America | 22% |

| Europe | 18% |

| Latin America | 7% |

| Middle East & Africa | 6% |

Polyolefin Market Evaluation in North America

North America is notably growing with 22% market share in 2025, owing to its strong technological innovation, shale gas availability, and advanced manufacturing capabilities. The region has access to large natural gas reserves, especially in the United States, which helps reduce production costs for petrochemical companies. Companies in North America are also leading in advanced recycling, sustainable plastics, and high-performance material development.

Sustainable Polyolefin Growth in the United States

The United States is expected to emerge as a prominent country for the polyolefin market in the coming years, due to its large shale gas resources and highly advanced petrochemical industry. The country produces large quantities of natural gas liquids, which provide cost-effective raw materials for polyolefin manufacturing. The United States is also investing strongly in recycling technologies, sustainable packaging, and electric vehicle production.

Recent Development

- In December 2025, Borealis and Borouge mutually introduced the latest polyolefins. Also, the newly launched polyolefins are known as Recleo™, which is specifically designed for a broad range of polyolefin applications as per the published report.

Top Vendors in the Polyolefin Market & Their Offerings:

- ExxonMobil Corporation: As a global energy giant, ExxonMobil leads the polyolefin sector through massive vertical integration. They leverage proprietary metallocene catalyst technology to produce high-performance polyethylene and polypropylene. By controlling the entire chain from feedstock to finished resin, they maintain a dominant position in delivering specialized materials for the medical and automotive industries.

- LyondellBasell Industries N.V.: Headquartered in the Netherlands, LyondellBasell is a premier licensor of polyolefin technologies and a top-tier producer of versatile resins. Their focus on circularity and advanced plastic recycling distinguishes them in the market. They specialize in high-grade polypropylene solutions, catering specifically to sustainable packaging and lightweight transportation components globally.

- SABIC: Based in Saudi Arabia, SABIC utilizes vast hydrocarbon resources to fuel its large-scale chemical manufacturing. They are renowned for innovative material science, particularly in developing durable polyolefins for the electronics and construction sectors. Through strategic partnerships, SABIC continues to expand its international footprint, emphasizing efficiency and high-volume resin production.

Other Key Players

- The Dow Chemical Company

- China Petrochemical Corporation

- TotalEnergies SE

- INEOS Group Holdings S.A.

- Chevron Phillips Chemical Company LLC

Segments Covered in the Report

By Product Type

- Polyethylene (PE)

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- Polypropylene (PP)

- Homopolymer PP

- Random Copolymer PP

- Impact Copolymer PP

- Ethylene Vinyl Acetate (EVA)

- Polyolefin Elastomers (POE)

- Polybutylene

- Other Polyolefins

By Technology

- Injection Molding

- Blow Molding

- Extrusion

- Film & Sheet Processing

- Rotational Molding

- Thermoforming

- Additive Manufacturing

By Feedback

- Naphtha

- Natural Gas Liquids (NGL)

- Ethane

- Propane

- Butane

- Coal-Based Feedstock

- Bio-Based Feedstock

By Form

- Pellets/Granules

- Powder

- Films

- Sheets

- Fibers

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Industrial Packaging

- Automotive

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Building & Construction

- Pipes & Fittings

- Insulation

- Roofing Membranes

- Electrical & Electronics

- Wire & Cable Insulation

- Consumer Electronics

- Healthcare

- Medical Packaging

- Medical Devices

- Agriculture

- Greenhouse Films

- Irrigation Systems

- Consumer Goods

- Textiles & Fibers

- Industrial Applications

By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online Procurement Platforms

- Contract Supply Agreements

By Sustainability

- Virgin Polyolefins

- Recycled Polyolefins

- Mechanically Recycled

- Chemically Recycled

- Bio-Circular Polyolefins

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (5)