Content

What is the Current Propylene Oxide Market Size and Share?

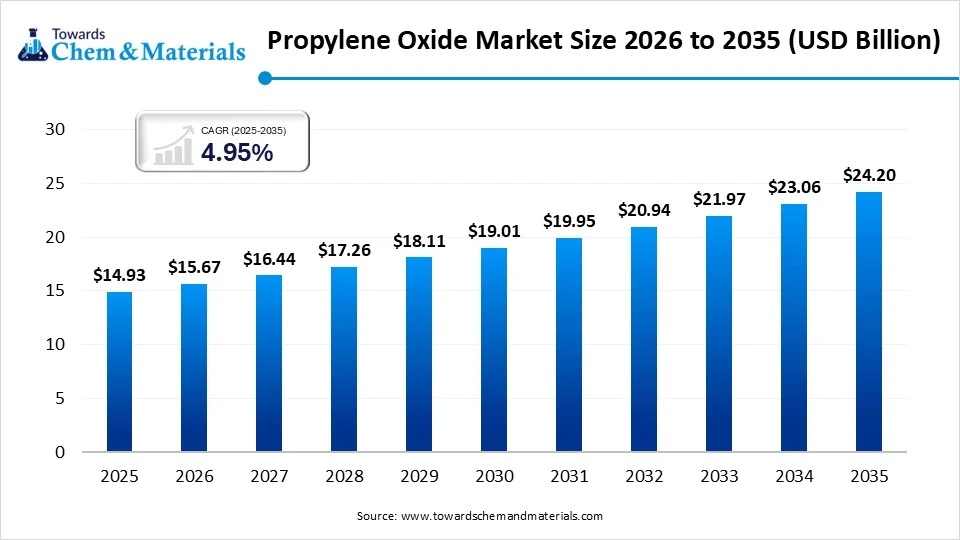

The global propylene oxide market size was estimated at USD 14.93 billion in 2025 and is expected to increase from USD 15.67 billion in 2026 to USD 24.20 billion by 2035, growing at a CAGR of 4.95% from 2026 to 2035.Asia Pacific dominated the propylene oxide market with the largest volume share of 58.00% in 2025.The emergence of sustainable chemical manufacturing has accelerated the industry growth in recent years. The industrial chemical, which emerged as the building block for the materials, and which is primarily made by propylene from petroleum processing called propylene oxide. Moreover, by easily combining with other chemicals to form new materials, the propylene oxide has gained attention from the major industries such as the automotive interior, foam mattresses, cooling fluids, and cosmetics in recent years.

Market Highlights

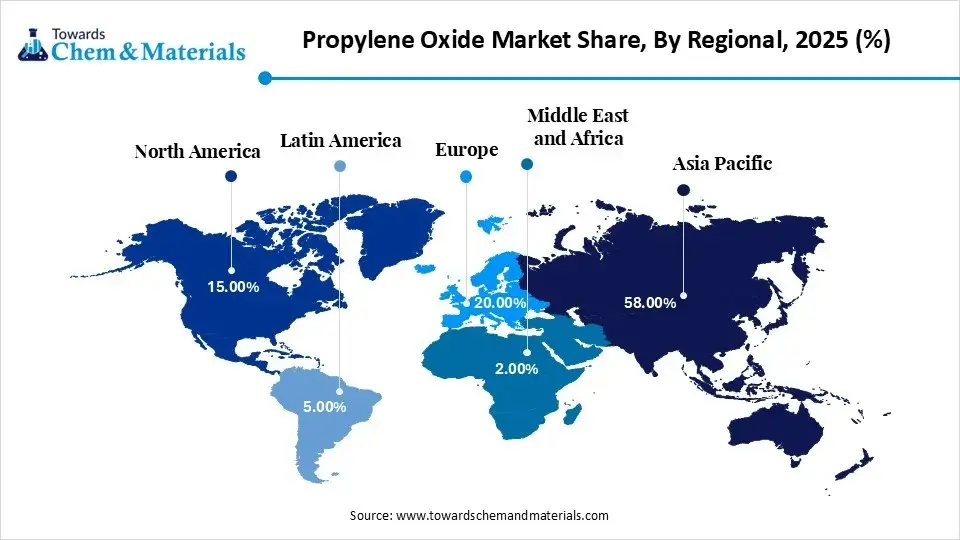

- By region, Asia Pacific dominated the propylene oxide market share 58.00% in 2025, due to it has the world's largest manufacturing base.

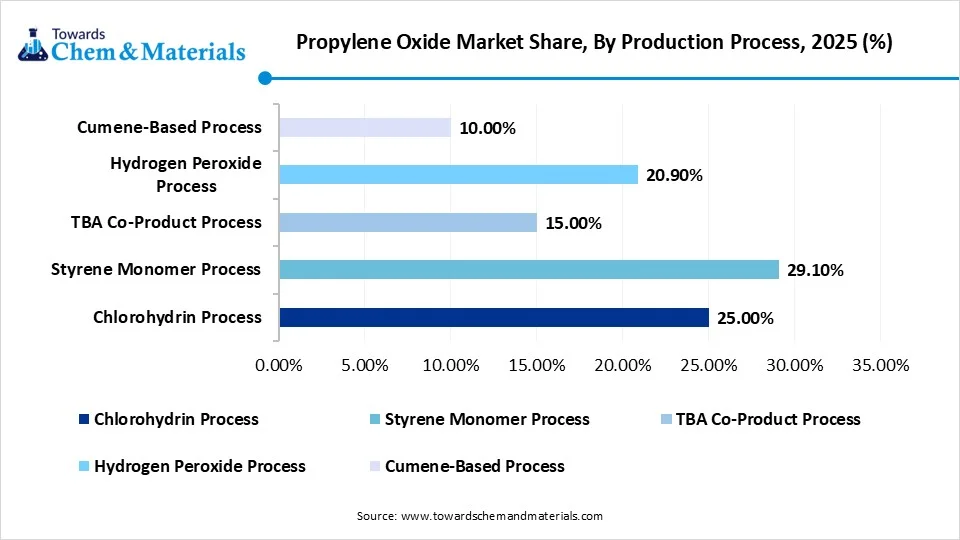

- By production process, the styrene monomer segment dominated the market revenue share 29.10% in 2025, owing to it allowed companies to produce two valuable chemicals at the same time.

- By production process, the hydrogen peroxide process segment is expected to grow during the forecast period, due to its simplicity and focus.

- By application, the polyether polyols segment led the market with the largest revenue share of 70.23% in 2025, owing to the main ingredient used to produce polyurethane foam.

- By end-use, the building and construction segment dominated the market and accounted for the largest revenue share of 34.10% in 2025, owing to modern buildings relying heavily on insulation materials.

- By end-use, the electronics segment is expected to grow during the forecast period, due to modern electronic devices requiring advanced protective materials.

Trade Analysis of the Propylene Oxide Market:

Import, Export, Consumption, and Production Statistics

- The world has observed the stable export of propylene oxide through 13 buyers and 28 exporters with 238 global shipments between July 2024 to June 2025.

- The United States has been leading the export of propylene oxide with 373 shipments, while countries such as Belgium (194 shipments) and China (40 shipments) are following in recent years.

- Also, the United States itself emerged as the leading importer of propylene oxide with 321 shipments, and Germany with 131 shipments, is following nowadays.

Market Trends

- The heavy shift towards energy-efficient materials has supported the stronger cash flows for manufacturing enterprises in recent years. As the demand grows for polyurethane foams, polypropylene oxide is likely to gain substantial industry share because it is identified as a key raw material in the polyurethane industry.

- The emergence of cleaner chemical manufacturing has driven substantial financial gains in the manufacturing sector in the current period. Also, the manufacturers of propylene oxide have actively seen investing the research and development programs for technologies that turn harmful key raw materials into environmentally friendly materials nowadays.

- The greater integration of production facilities with the large petrochemical complexes is likely to increase return on investment for manufacturers during the forecast period. The companies are planning to produce wider chemical portfolios instead of isolated chemical production in recent years.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 15.67 Billion |

| Revenue Forecast in 2035 | USD 24.20 Billion |

| Growth Rate | CAGR 4.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Production Process, By Application, By End-UseBy Region |

| Key companies profiled | BASF SE, Mitsui Chemicals, Dow Inc., Huntsman Corporation, LyondellBasell Industries Holdings, Royal Dutch Shell, Huntsman International, Asahi Glass Co., Repsol, Tokuyama Corporation, Sumitomo Chemical Co., SKC, LG Chem, Celanese Corporation, INEOS Group, SABIC, |

Modern Technologies Optimizing Propylene Oxide Output

The industry has been seen moving toward simpler and more efficient production processes. Moreover, in the past, many technologies produced large quantities of co-products that companies had to sell or manage. New technologies are designed to focus mainly on producing propylene oxide itself rather than multiple chemicals at once. This change helps companies control production volumes more easily and reduces dependence on the market demand for other chemicals.

Supply Chain Analysis of the Propylene Oxide Market:

Distribution to Industrial Users

- Propylene oxide is primarily distributed to industrial users to produce polyether polyols, which are essential for manufacturing polyurethane foams used in furniture and automotive industries.

- It also serves as a critical chemical intermediate for propylene glycol, specialty resins, and surface-active agents, typically transported via bulk tankers or pipelines.

Chemical Synthesis and Processing

- Propylene oxide is primarily synthesized via the chlorohydrin process or hydroperoxidation (the PO/TBA or PO/SM processes). These methods involve reacting propylene with chlorine or organic hydroperoxides.

- The resulting crude product undergoes rigorous distillation and purification to achieve the high industrial-grade purity required for downstream chemical manufacturing and polymerization.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance for propylene oxide involves strict adherence to OSHA and REACH standards due to its classification as a carcinogen. Safety monitoring requires continuous leak detection, specialized ventilation, and personal protective equipment.

- Facilities must maintain rigorous Risk Management Plans (RMPs) to prevent accidental release and ensure workplace exposure limits remain safe.

Propylene Oxide Market Regulatory Landscape: Global Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Clean Air Act (CAA): Section 112 | Listing as a Hazardous Air Pollutant (HAP); emission standards for manufacturing. |

| European Union | European Commission | Food Additives: Regulation (EC) No 1333/2008 | Restrictions on direct food use (unlike the US, PO-derived propylene glycol has stricter food-grade limits). |

| China | MEE | MEE Order No. 12 |

Registration and environmental management of new chemical substances. |

Segmental Insights

Production Process Insights

How did the Styrene Monomer Process Segment Dominate the Propylene Oxide Market in 2025?

The styrene monomer process segment dominated the market share 29.10% in 2025, due to it allowed companies to produce two valuable chemicals at the same time. While manufacturing propylene oxide, the process also produces styrene monomer, which is widely used to make plastics such as polystyrene and ABS. Since both chemicals have strong industrial demand, this process provided a stable business model for chemical producers.

The hydrogen peroxide process segment is expected to grow with a rapid CAGR, owing to its simplicity and focus. Unlike older processes, it mainly produces propylene oxide without generating large quantities of secondary chemicals. This makes plant operations easier to manage because companies do not need to depend on the market demand for other by-products.

Propylene Oxide Market Share, By Production Process, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Chlorohydrin Process | 25.00% |

| Styrene Monomer Process | 29.10% |

| TBA Co-Product Process | 15.00% |

| Hydrogen Peroxide Process | 20.90% |

| Cumene-Based Process | 10.00% |

- Styrene Monomer Process – Dominating with a 29.10% share, strong integration with styrene production chains and efficient co-production economics drive its leading market position.

- Chlorohydrin Process – With a 25.00% share, its long-established industrial use and relatively simple production route support steady demand, though environmental concerns limit further dominance.

- Hydrogen Peroxide Process – Holding a 20.90% share, cleaner production technology and lower environmental impact are driving increasing adoption momentum.

- TBA Co-Product Process – With a 15.00% share, value addition through co-product generation supports moderate adoption, though dependency on integrated refining complexes limits scale.

- Cumene-Based Process – With a 10.00% share, niche integration and limited commercial deployment restrict broader market penetration despite process efficiency advantages.

Application Insights

How did the Polyether Polyols Segment Dominate the Propylene Oxide Market in 2025?

The polyether polyols segment dominated the market share 70.23% in 2025, due to they are the main ingredient used to produce polyurethane foam. Also, the polyurethane foam is one of the most versatile materials used in modern manufacturing. It appears in furniture cushioning. insulation panels, automotive seats, mattresses, and refrigeration equipment. Since these products are produced in extremely large volumes worldwide, the demand for polyether polyols becomes very high.

The propylene glycols segment is expected to grow, owing to they are used in many everyday products that continue to expand globally. These include cosmetics, pharmaceutical formulations, food processing ingredients, industrial fluids, and antifreeze solutions. As consumer markets grow, especially in developing countries, the demand for personal care products, medicines, and packaged foods increases significantly.

Propylene Oxide Market Share, By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Polyether Polyols | 70.23% |

| Propylene Glycols | 18.50% |

| Glycol Ethers | 5.40% |

| Other Applications | 5.87% |

- Polyether Polyols – Dominating with a 70.23% share, extensive use in polyurethane foams for furniture, construction insulation, and automotive applications drives overwhelming demand.

- Propylene Glycols – With an 18.50% share, strong demand from pharmaceuticals, food processing, and industrial formulations supports steady consumption.

- Glycol Ethers – Holding a 5.40% share, usage as solvents in paints, coatings, and cleaning products contributes to moderate but niche demand.

- Other Applications – With a 5.87% share, diverse small-scale uses across chemical intermediates and specialty products result in limited overall market contribution.

End Use Industry Insights

How did the Building and Construction Sector Segment Dominate the Propylene Oxide Market in 2025?

The building and construction segment dominated the market share 34.10% in 2025, due to modern buildings relying heavily on insulation materials. Moreover, the polyurethane insulation made from propylene oxide derivatives helps reduce energy loss through walls, roofs, and floors. As cities expand and housing demand increases, construction activity grows significantly. Builders also prefer polyurethane insulation because it is lightweight, durable, and easy to install.

The electronics segment is expected to grow with a rapid CAGR, owing to modern electronic devices that require advanced protective materials. Also, many electronic components must be protected from heat, moisture, and chemical damage. Special polymers derived from propylene oxide are used in coatings, encapsulation materials, and insulating layers that protect sensitive circuits. As the world produces more smartphones, electric vehicles, batteries, and semiconductor devices, the need for these protective materials increases.

Propylene Oxide Market Share, By End Use Industry, 2025 (%)

| By End Use Industry | Revenue Share, 2025 (%) |

| Automotive | 27.79% |

| Building & Construction | 34.10% |

| Chemical & Pharmaceutical | 12.45% |

| Textile & Furnishing | 9.12% |

| Packaging | 4.20% |

| Electronics | 10.54% |

| Other End Use | 1.80% |

- Building & Construction – Dominating with a 34.10% share, strong demand for polyurethane foams in insulation, sealants, and structural applications drives leading consumption.

- Automotive – With a 27.79% share, extensive use of propylene oxide derivatives in lightweight materials, foams, and interior components supports high demand.

- Chemical & Pharmaceutical – Holding a 12.45% share, broad use as an intermediate in chemical synthesis and pharmaceutical formulations sustains steady industrial consumption.

- Electronics – With a 10.54% share, growing application in insulation materials and electronic component protection supports moderate market expansion.

- Textile & Furnishing – With a 9.12% share, use in foams and synthetic materials for furniture and textile applications contributes to stable demand.

- Packaging – Holding a 4.20% share, limited but steady use in specialty packaging materials restricts larger market penetration.

- Other End Use – With a 1.80% share, niche applications contribute minimal demand due to fragmented and low-volume usage.

Regional Insights

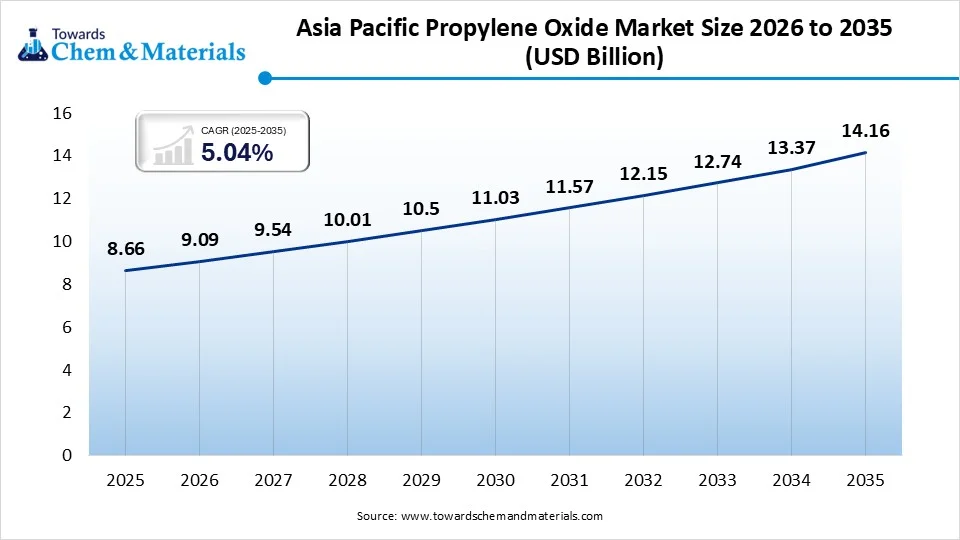

The Asia Pacific propylene oxide market size was valued at USD 8.66 billion in 2025 and is expected to be worth around USD 14.16 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.04% over the forecast period from 2026 to 2035. Asia Pacific propylene oxide market segment accounted for the major share 58.00% in 2025. Asia Pacific dominated the propylene oxide market share in 2025, due to it has the world's largest manufacturing base. Many industries that consume propylene oxide derivatives, such as construction, automotive production, electronics manufacturing, and appliance production, are heavily concentrated in this region. Countries in the region also have rapidly growing populations and expanding urban infrastructure, which increases demand for housing, transportation, and consumer products.

China’s Strong Chemical Production Dominance

China maintained its dominance in the market, owing to its combination of massive industrial demand and large-scale chemical production capacity. Also, the country manufactures huge volumes of appliances, electronics, vehicles, and construction materials, all of which use polyurethane products derived from propylene oxide. China has also invested heavily in domestic petrochemical infrastructure, allowing it to produce key raw materials locally.

Propylene Oxide Market Evaluation in the Middle East and Africa

The Middle East and Africa are expected to capture a major share 7.00% of the propylene oxide market with a rapid CAGR, owing to their strong access to raw materials used in petrochemical production. Many countries in this region produce large amounts of crude oil and natural gas, which are the starting points for many petrochemicals. Instead of exporting only raw energy resources, governments are increasingly investing in value-added industries such as plastics and chemical manufacturing.

Saudi Strategy Boosting Propylene Oxide Production

Saudi Arabia is expected to emerge as a prominent country for the propylene oxide market in the coming years, due to its long-term strategy to expand downstream petrochemical industries. The country already has strong refining capacity and access to low-cost hydrocarbon feedstocks. By developing large industrial cities and petrochemical complexes, Saudi Arabia is encouraging companies to manufacture higher-value chemical products rather than exporting only crude oil.

")

North America Propylene Oxide Market Examination

North America propylene oxide market with the largest volume share of 28.00% in 2025.North America is notably growing in the industry, owing to technological innovation and strong industrial demand. The region has advanced chemical research capabilities, which allow companies to develop improved production processes and specialty materials. Furthermore, industries such as construction, automotive manufacturing, packaging, and consumer goods continue to expand steadily.

Propylene Oxide Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 15.00% |

| Europe | 20.00% |

| Asia Pacific | 58.00% |

| Latin America | 5.00% |

| Middle East & Africa | 2.00% |

- Asia Pacific – Dominating with a 58.00% share, rapid expansion of construction, automotive manufacturing, and polyurethane demand drives strong consumption across the region.

- Europe – With a 20.00% share, well-established chemical industries and steady demand from automotive and construction sectors support consistent market presence.

- North America – Holding a 15.00% share, mature end-use industries and stable polyurethane consumption maintain steady but slower growth.

- Latin America – With a 5.00% share, developing construction and industrial sectors contribute modest demand, limiting broader market expansion.

- Middle East & Africa – Making up 2.00% of the market, limited downstream chemical capacity and slower industrial adoption restrict overall market share.

Innovation Powering the United States Chemical Industry Growth

The United States is expected to gain a significant industry share owing to its advanced petrochemical industry and strong innovation culture. Also, many chemical companies in the country focus on developing high-performance materials used in automotive, aerospace, electronics, and construction applications. The United States also has a well-developed industrial supply chain that connects raw material production, chemical manufacturing, and downstream product industries.

Recent Developments

- In April 2025, China National Chemicals is likely to start a propylene oxide project at large scale, which has the capacity of 600,000 tons of propylene oxide production annually. Also, the company has completed mechanical completion, which is ready to operate as per the company's claim.(Source: www.chemanalyst.com)

- In July 2025, Manali Petrochemical has increased capacity of the propylene glycol capacity by 50,000 annually. Moreover, the company is likely to integrate with the latest technology and hire the expertise of local talent, as per the published report.(Source: www.indianchemicalnews.com)

Top Vendors in the Propylene Oxide Market & Their Offerings:

- BASF SE: BASF SE is a leading global chemical producer that utilizes advanced HPPO (hydrogen peroxide to propylene oxide) technology. In collaboration with partners like Dow, it operates large-scale production units in Antwerp and Geismar.

- Mitsui Chemicals: Mitsui Chemicals is a major Japanese player specializing in basic chemicals and polyurethane raw materials. It produces propylene oxide primarily to support its downstream polyether polyol (PPG) business, marketed under brands like ACTCOL™.

- Dow Inc.: Dow Inc. is a top-tier producer of propylene oxide, operating key facilities in the U.S., Germany, and Brazil. It leverages integrated manufacturing to produce PO as a feedstock for polyurethanes, propylene glycol, and glycol ethers.

- Huntsman Corporation: Huntsman Corporation is a global manufacturer of differentiated chemicals, well-known for its PO/MTBE co-product technology. While it sold its North American chemical intermediates business to Indorama Ventures in 2020, it remains a key player through international joint ventures, such as the Nanjing Jinling Huntsman facility in China.

- LyondellBasell Industries Holdings

- Royal Dutch Shell

- Huntsman International

- Asahi Glass Co.,

- Repsol

- Tokuyama Corporation

- Sumitomo Chemical Co.,

- SKC

- LG Chem

- Celanese Corporation

- INEOS Group

- SABIC

Segments Covered in the Report

By Production Process

- Chlorohydrin Process

- Styrene Monomer Process

- TBA Co-Product Process

- Hydrogen Peroxide Process

- Cumene-Based Process

By Application

- Polyether Polyols

- Propylene Glycols

- Glycol Ethers

- Other Applications

By End-Use

- Automotive

- Building & Construction

- Chemical & Pharmaceutical

- Textile & Furnishing

- Packaging

- Electronics

- Other End Use

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)