Content

What is the PE and PP Compounding Market Size and Share ?

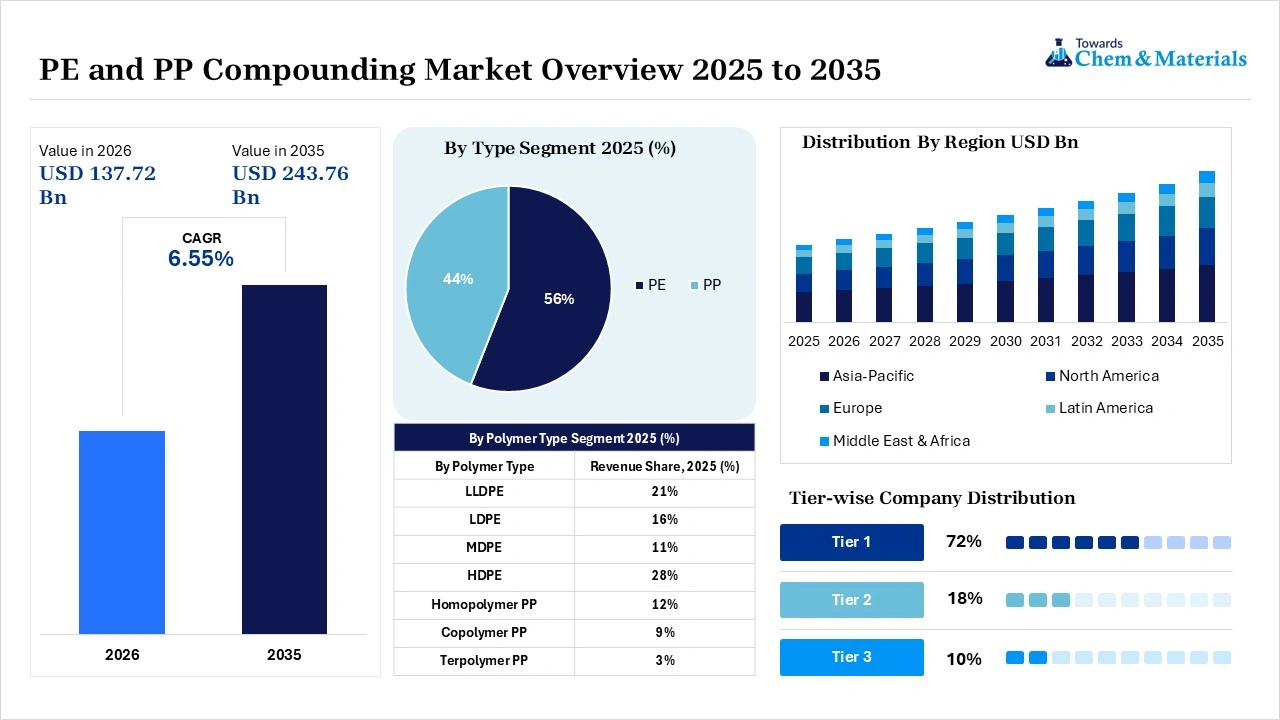

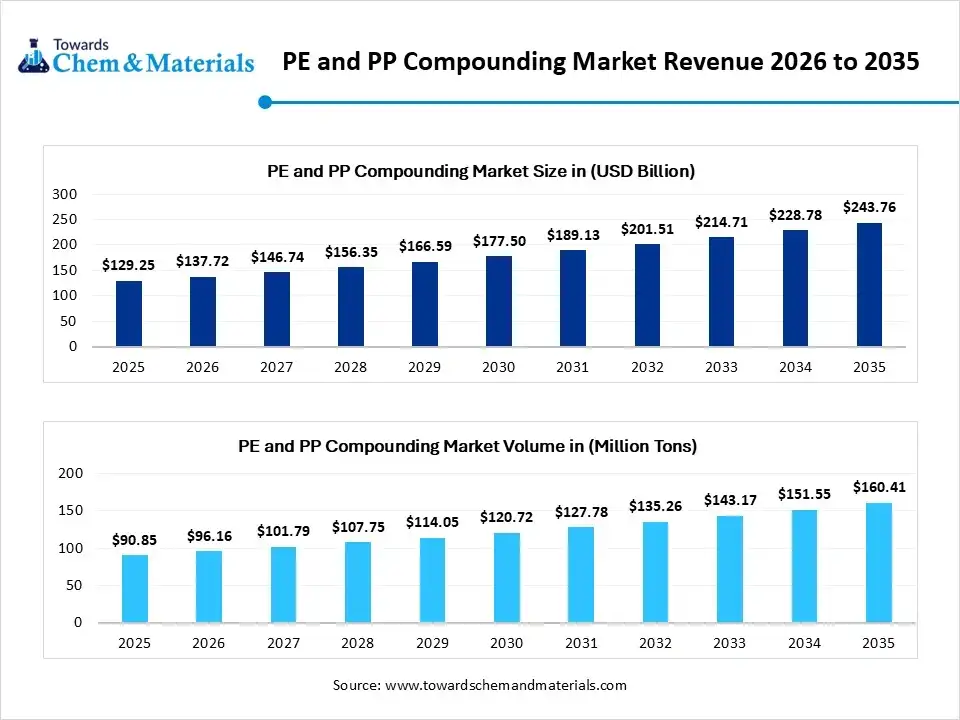

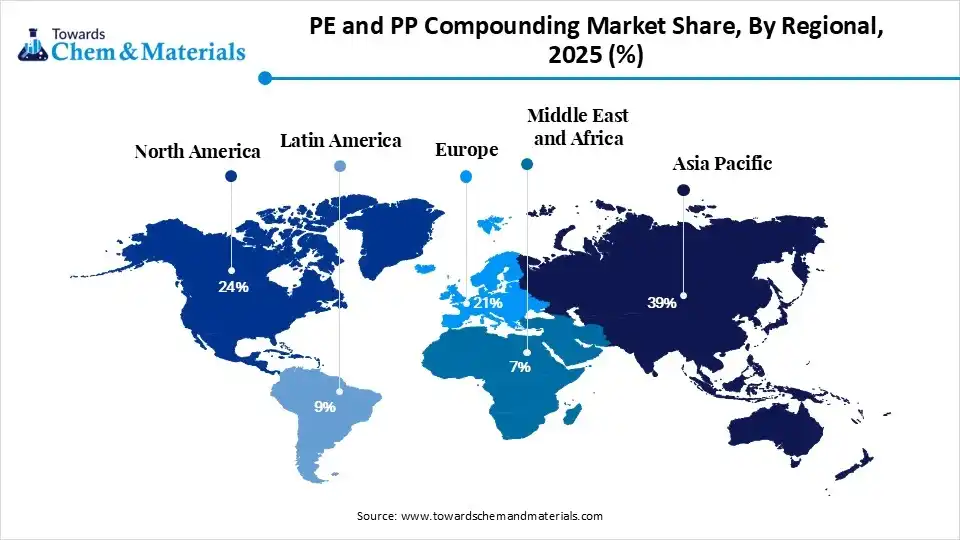

The PE and PP compounding market size was valued at USD 129.25 billion in 2025, is estimated to reach USD 137.72 billion in 2026, and is projected to reach USD 243.76 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.55% over the forecast period from 2026 to 2035.Asia Pacific dominated the PE and PP compounding market with the largest revenue share of 39% in 2025 and is expected to grow at the fastest CAGR of 6.69% during the forecast period. In terms of volume, the PE and PP compounding market is projected to grow from 90.85 million tons in 2025 to 160.41 million tons by 2035. growing at a CAGR of 5.85% from 2026 to 2035.The greater need for durable and lightweight plastic material has accelerated the market potential in recent years.

The process of combining plastic resins with specific materials like fillers, additives, and colorants to improve their chemical and physical properties is known as the PE and PP compounding. Also, the greater need for durable and flexible materials in the major industries has attracted increased capital and investment in manufacturing in recent years. Furthermore, regions like Asia Pacific, North America, and Europe have been seen in focusing on sustainable and cost-effective plastic materials, where PE and PP compounding emerged as an ideal option for the industry participants in the current period.

Market Highlights

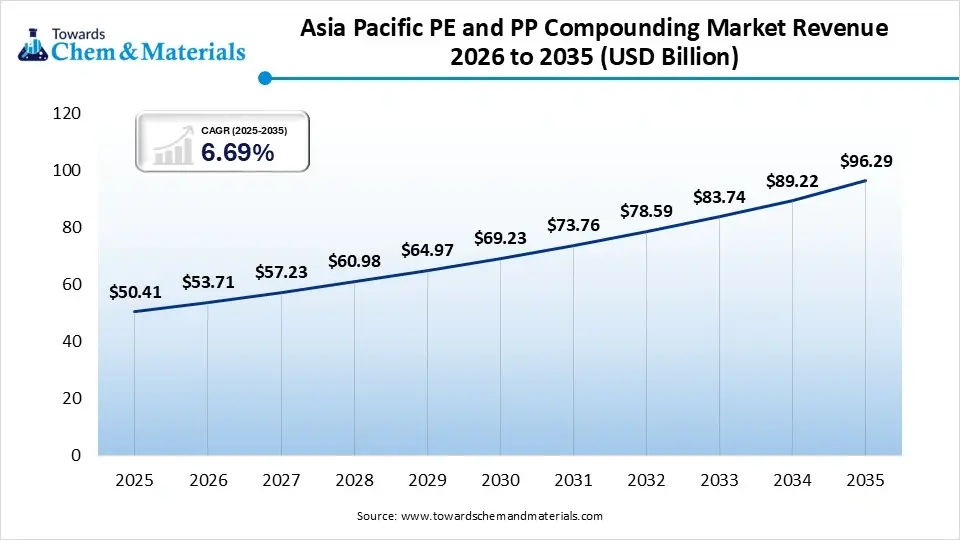

- By region, Asia Pacific dominated the market with a share of 39% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.94% in the forecast period, due to the region having strong manufacturing industries, low production costs, and high demand for plastic materials across packaging, automotive, construction, and electronics sectors.

- By region, North America is notably growing with 24% market share in 2025, owing to the region focusing strongly on advanced manufacturing technologies, sustainability, and electric vehicle production.

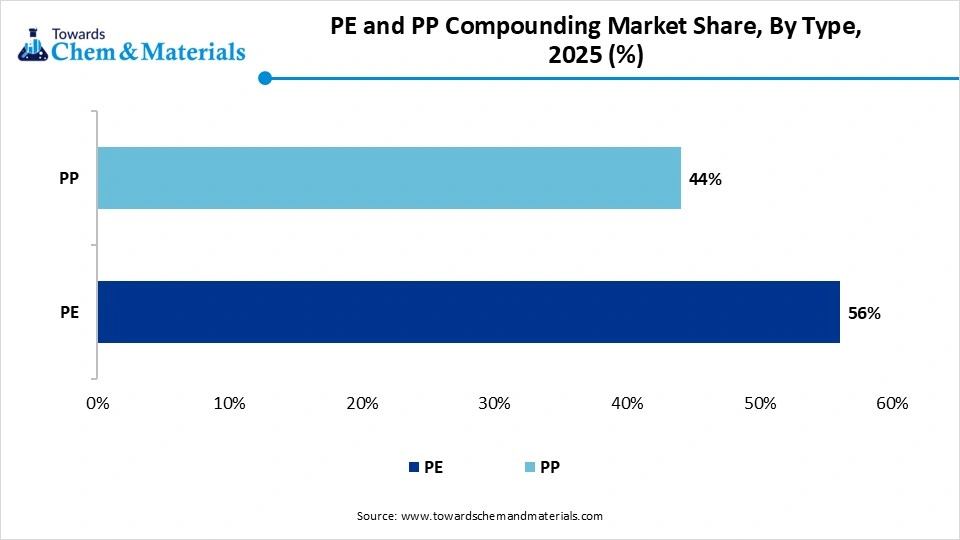

- By type, the PE segment dominated the market with 56% share in 2025, as the PE compounds are widely used across several industries due to their flexibility, durability, chemical resistance, and cost-effectiveness.

- By type, the PP segment held the 44% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.24% in the forecast period, owing to PP compounds offering excellent strength, heat resistance, lightweight performance, and design flexibility.

- By polymer type, on the basis of PE, the HDPE segment dominated the market with 28% share in 2025, as it provides superior strength, impact resistance, & chemical durability.

- By polymer type, on the basis of PP, the copolymer PP segment held the 9% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 6.41% in the forecast period, due to it provides better flexibility, toughness, and impact resistance compared to standard PP materials.

- By compound type, in the context of PE, the HDPE pipe compound segment dominated the market with 18% share in 2025, as HDPE pipes are widely used in water supply, gas distribution, sewage systems, and industrial piping applications.

- By compounding type, in the context of PP, the thermoplastic polyolefin (TPO) segment held the 6% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 7.02% in the forecast period, due to TPO materials providing lightweight performance, durability, weather resistance, and easy recyclability.

- By application, on the basis of PE, the pipe and infrastructure segment dominated the market with 22% share in 2025, as PE and PP compounds are highly suitable for water supply, sewage, gas distribution, and industrial piping systems.

- By application, on the basis of PP, the automotive segment held the 16% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 6.86% in the forecast period, due to vehicle manufacturers increasingly using lightweight plastic compounds to improve fuel efficiency and reduce emissions.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 129.25 Billion | CAGR (2026–2035): 6.55%

- Market Projected Size (2035): USD 243.76 Billion

- Asia Pacific: largest Market Revenue Share of 39% in 2025|USD 50.41 Billion

- Market Estimated Volume (2025): 90.85 Million Tons| Volume CAGR (2026–2035): 5.85%

- Market Projected Volume (2035):160.41 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025):USD 1,145/Ton

- Average Selling Price (2025): USD 1,435/Ton

- Pricing CAGR (2026–2035): 2.85%

Also, companies are investing in advanced compounding technologies to improve product quality and production efficiency. Moreover, the increasing use of recycled plastics and bio-based additives is supporting the market’s sustainability goals. The packaging sector remains one of the largest consumers of PE and PP compounds because these materials provide strong protection, flexibility, and durability.

- Furthermore, the PE and PP compounding market has become an important part of the global plastics industry due to its wide industrial applications and continuous technological advancements.

Market Trends:

- The shift towards eco-friendly and sustainable plastic compounds has supported the stronger cash flows for the manufacturing enterprises in recent years. Also, the global implementations of recycling and zero-carbon emissions rules by regional governments have led to sales in the past few years.

- The usage and heavy need for lightweight materials is elevating the earning potential for producers in the current period. Also, the manufacturers of heavy materials are trying to improve fuel efficiency and reduce emissions at the same time.

- The emergence of flexible packaging is expected to lead to better revenue growth during the forecast period, as several businesses, such as healthcare, food and beverages, and personal care industries, have been observed using compounded plastic materials akin to durability and product protection.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 137.72 Billion / 96.16 Million Tons |

| Revenue Forecast in 2035 | USD 243.76 Billion / 160.41 Million Tons |

| Growth Rate | CAGR 6.55% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Type, By Compound Type, By Application, By Region |

| Key Companies Profiled | LyondellBasell Industries, SABIC (Saudi Basic Industries Corporation), Borealis AG, Dow Inc., ExxonMobil Chemical, TotalEnergies, Chevron Phillips Chemical, Ineos Group, Braskem, Avient Corporation |

Automation Advancing Modern Plastic Compound Production

The industry is shifting toward more technological advancements where manufacturers are increasingly using automated and smart compounding systems to improve production efficiency and product consistency. These advanced systems help control temperature, mixing quality, and material flow more accurately. Moreover, automation is helping companies reduce operational costs and improve overall manufacturing performance.

Supply Chain Analysis of the PE and PP Compounding Market

- Distribution to Industrial Users :The distribution of Polyethylene (PE) and Polypropylene (PP) compounds to industrial users operates through direct enterprise contracts and regional distributors.

- Suppliers deliver customized, pelletized resins directly to automotive, packaging, construction, and electronics manufacturers. These industries rely on bulk freight shipments to feed high-volume injection moulding and extrusion systems.

- Key Players: LyondellBasell Industries, SABIC, and Borealis AG

- Chemical Synthesis and Processing :Polyethylene (PE) and Polypropylene (PP) compounds are synthesised through the catalytic polymerisation of ethylene and propylene monomers.

- Chemical processors then combine these raw base resins with specific additives, mineral fillers, and reinforcements using high-shear twin-screw extruders. The intensive thermal processing melts, mixes, and pelletises the material into custom industrial formulations.

- Key Players: Ineos Group, ExxonMobil Chemical, and Braskem

- Regulatory Compliance and Safety Monitoring :Regulatory compliance forces compounders to meet strict global safety standards like REACH, RoHS, and FDA food-contact mandates.

- Safety monitoring tracks volatile organic compounds, heavy metal contamination, and dust explosions during extrusion. Producers run meticulous trace audits and physical testing to ensure that final plastic blends remain non-toxic for consumers.

- Key Agencies: FDA, EPA, and OSHA

PE and PP Compounding Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | 21 CFR Part 177 (Polymers): Specifically, Section 177.1520 (Olefin Polymers), which explicitly dictates the legal parameters for compounding polyethylene and polypropylene destined for food contact surfaces. | Extractable Limits: Quantifying maximum hexane- and xylene-soluble fraction extractions to ensure the polymer compound does not leach chemicals into food. |

| Europe | European Commission |

EU Regulation No 10/2011 (Plastics Regulation): The foundational law governing plastic materials intended to come into contact with food, establishing a strict "Positive List" of authorized monomers and additives. | SVHC (Substances of Very High Concern): Eliminating toxic plasticizers, heavy metal pigments, and restricted additives from the masterbatch recipe. |

| China | SAMR (State Administration for Market Regulation) | GB 4806.7-2023 (National Food Safety Standard - Plastic Materials and Products for Food Contact): This updated mandatory standard fully regulates the chemical requirements for PE, PP, and starch-based plastic compounds. | Primary Aromatic Amines (PAAs): The upgraded standard enforces strict new verification limits and migration testing protocols for PAAs generated from colorants or isocyanates during extrusion. |

Market Dynamics

Driver

Cost-Effective Plastic Material Supporting Industry Leads

The growing demand for lightweight and durable plastic materials is creating profitable pathways for manufacturers in the current period. Also, in recent years, industries such as packaging, automotive, construction, and consumer goods have increasingly used PE and PP compounds because these materials provide strong performance at lower costs. Moreover, manufacturers prefer these compounds because they are easy to process, recyclable, and suitable for large-scale production.

Restraint

Unstable Crude Oil Prices Challenging Industry

Fluctuating raw material prices are expected to hamper the industry's growth during the forecast period. Also, the PE and PP compounds are mainly produced from petroleum-based raw materials, and changes in crude oil prices directly affect manufacturing costs. In the current period, unstable raw material pricing has created challenges for manufacturers in maintaining profit margins and stable product pricing.

Opportunity

Recyclable Materials May Transform Sector Potential

The heavy focus on recycled materials is anticipated to create significant opportunities for manufacturing in the coming years. Also, in recent years, industries have been focusing on reducing environmental impact by using recyclable and eco-friendly materials. Moreover, governments across several countries are supporting recycling initiatives and circular economy practices, which are encouraging manufacturers to develop advanced sustainable compounds.

Segmental Insights

Type Insights

The PE segment dominated the market with 56% share in 2025, as the PE compounds are widely used across several industries due to their flexibility, durability, chemical resistance, and cost-effectiveness. In recent years, the packaging industry has significantly increased the use of PE compounds for films, containers, pipes, and flexible packaging products. Moreover, PE materials provide excellent moisture resistance and lightweight performance, making them highly suitable for industrial and consumer applications.

")

The PP segment held the 44% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.24% in the forecast period, owing to PP compounds offering excellent strength, heat resistance, lightweight performance, and design flexibility. In the current period, automotive manufacturers are increasingly using PP compounds to reduce vehicle weight and improve fuel efficiency. Moreover, the rising demand for electric vehicles is supporting the use of advanced PP materials in automotive interiors and structural components.

PE and PP Compounding Market Share,By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| PE | 56% |

| PP | 44% |

Polymer Type Insights

On the basis of PE, the HDPE segment dominated the market with 28% share in 2025, as it provides superior strength, impact resistance, & chemical durability. In recent years, HDPE compounds have been widely used in piping systems, packaging products, industrial containers, and construction materials due to their long service life and cost-effectiveness. Moreover, HDPE materials provide strong moisture resistance and can withstand harsh environmental conditions, making them suitable for outdoor and industrial applications.

")

On the basis of PP, the copolymer PP segment held the 9% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 6.41% in the forecast period, due to it provides better flexibility, toughness, and impact resistance compared to standard PP materials. In the current period, industries such as automotive, packaging, and healthcare are increasingly using co-polymer PP compounds for advanced applications requiring higher durability and performance.

PE and PP Compounding Market Share,By Polymer Type, 2025 (%)

| By Polymer Type | Revenue Share, 2025 (%) |

| LLDPE | 21% |

| LDPE | 16% |

| MDPE | 11% |

| HDPE | 28% |

| Homopolymer PP | 12% |

| Copolymer PP | 9% |

| Terpolymer PP | 3% |

Compound Type Insights

In the context of PE, the HDPE pipe compound segment dominated the market with 18% share in 2025, as HDPE pipes are widely used in water supply, gas distribution, sewage systems, and industrial piping applications. In recent years, governments and private companies have significantly invested in infrastructure development and water management projects, increasing demand for durable piping materials.

In the context of PP, the thermoplastic polyolefin (TPO) segment held the 6% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 7.02% in the forecast period, due to TPO materials providing lightweight performance, durability, weather resistance, and easy recyclability. In the automotive industry, TPO compounds are increasingly used for bumpers, dashboards, and interior components to improve fuel efficiency and reduce vehicle weight.

PE and PP Compounding Market Share,By Compound Type, 2025 (%)

| By Compound Type | Revenue Share, 2025 (%) |

| HDPE pipe compound | 18% |

| LDPE/LLDPE modified | 10% |

| Cross-linkable PE (XLPE) | 12% |

| Carbon-black-filled PE | 8% |

| Conductive PE | 3% |

| Talc-filled | 14% |

| Glass-filled | 9% |

| Mineral-filled | 7% |

| Impact-modified | 8% |

| Thermoplastic Polyolefin (TPO) | 6% |

| Flame-Retardant (FR) PP | 3% |

| Conductive PP | 2% |

Application Insights

On the basis of PE, the pipe and infrastructure segment dominated the market with 22% share in 2025, as PE and PP compounds are highly suitable for water supply, sewage, gas distribution, and industrial piping systems. In recent years, rapid urbanization and increasing infrastructure investments have created strong demand for durable and cost-effective piping materials. Moreover, PE and PP compounds provide excellent corrosion resistance, flexibility, and long operational life compared to traditional piping materials such as metal and concrete.

On the basis of PP, the automotive segment held the 16% market share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 6.86% in the forecast period, due to vehicle manufacturers are increasingly using lightweight plastic compounds to improve fuel efficiency and reduce emissions. In the current period, PE and PP compounds are widely used in automotive interiors, bumpers, battery components, dashboards, and under-the-hood applications.

PE and PP Compounding Market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Pipe & Infrastructure | 22% |

| Wire & Cable | 13% |

| Packaging | 19% |

| Automotive | 16% |

| Construction | 12% |

| Consumer Goods & Appliances | 7% |

| Electrical & Electronics | 5% |

| Medical & Healthcare | 4% |

| Other applications | 2% |

Regional Insights

How will Asia Pacific Dominate the PE and PP Compounding Market in 2025?

The Asia Pacific PE and PP compounding market size was estimated at USD 50.41 billion in 2025 and is projected to reach USD 96.29 billion by 2035, growing at a CAGR of 6.69% from 2026 to 2035.Asia Pacific dominated the market with a share of 39% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.94% in the forecast period, due to the region having strong manufacturing industries, low production costs, and high demand for plastic materials across packaging, automotive, construction, and electronics sectors. In recent years, countries such as China, India, Japan, and South Korea have significantly increased industrial production and infrastructure activities, creating strong demand for compounded plastics.

China

China

- China is increasing the production of electric vehicles, consumer electronics, packaging materials, and construction products, which is creating high demand for compounded plastics.

- The country is focusing on recyclable and sustainable plastic materials to reduce environmental impact.

Japan

- Japan is also known for its advanced research and development activities in polymer technology, which is helping manufacturers develop innovative plastic compounds.

- Also, the growing demand for durable and heat-resistant materials in industrial applications continues to support market growth across the country.

India

- The packaging, construction, automotive, and agriculture industries are creating strong demand for PE and PP compounds across the country.

- Government initiatives supporting manufacturing and infrastructure projects are helping increase the use of plastic compounds in piping systems, packaging materials, and consumer products.

PE and PP Compounding Market Evaluation in North America

The North America PE and PP compounding market size was estimated at USD 31.02 billion in 2025 and is projected to reach USD 59.72 billion by 2035, growing at a CAGR of 6.77% from 2026 to 2035.North America is notably growing with 24% market share in 2025, owing to the region is focusing strongly on advanced manufacturing technologies, sustainability, and electric vehicle production. Furthermore, industries in the United States and Canada are increasing investments in recyclable plastic compounds and high-performance polymer materials. Moreover, the strong presence of automotive, healthcare, packaging, and consumer goods industries is supporting market growth.

United States

- The companies in the United States are adopting automation and smart manufacturing systems to improve production efficiency and product performance in the plastics industry.

- The packaging sector is also growing rapidly due to rising online shopping and food delivery services.

Canada

- The investments in water management systems and industrial modernization projects are supporting the demand for durable plastic compounds.

- Also, industries in Canada are also increasing the use of lightweight plastic materials in consumer products and industrial applications.

Europe PE and PP Compounding Industry Conditions

The Europe PE and PP compounding market size was estimated at USD 27.14 billion in 2025 and is projected to reach USD 52.41 billion by 2035, growing at a CAGR of 6.80% from 2026 to 2035.Europe held the 21% market share in 2025 owing to its strong focus on sustainability, recycling, and advanced industrial manufacturing. In recent years, strict environmental regulations have encouraged companies to develop eco-friendly and recyclable plastic compounds for industrial applications. Moreover, the region’s automotive and packaging industries are increasingly using lightweight materials to improve efficiency and reduce emissions.

Germany

- The growing demand for high-performance compounds in electronics, construction, and industrial applications.

- The automotive companies in Germany, which have a greater share globally, have increased the use of lightweight plastic compounds to improve fuel efficiency and electric vehicle performance.

Italy

- The strong food and beverage packaging industry is also increasing demand for flexible and durable plastic compounds.

- Also, the growing investments in industrial modernization and energy-efficient manufacturing systems are supporting the expansion of the PE and PP compounding market in Italy.

PE and PP Compounding Industry Survey in Latin America

The Latin America PE and PP compounding market size was estimated at USD 11.63 billion in 2025 and is projected to reach USD 23.16 billion by 2035, growing at a CAGR of 7.13% from 2026 to 2035.Latin America held the 9% market share in 2025 due to increasing industrialization, infrastructure development, and rising demand for packaging materials. Moreover, the growing middle-class population and rising urbanization are boosting demand for packaged consumer products. Manufacturers are also improving local production capabilities and adopting modern plastic processing technologies.

") Brazil

Brazil

- The country has expanded industrial and infrastructure projects, creating higher demand for durable plastic materials.

- Brazil is increasingly using PE and PP compounds in agricultural films, irrigation systems, and packaging applications.

Argentina

- The local manufacturers are adopting advanced compounding technologies to improve product quality and production efficiency in Argentina.

- The growing demand for lightweight and cost-effective materials in consumer and industrial sectors in Argentina.

Middle East & Africa’s PE and PP Compounding Sector Observation

The Middle East and Africa PE and PP compounding market size was estimated at USD 9.05 billion in 2025 and is projected to reach USD 18.28 billion by 2035, growing at a CAGR of 7.28% from 2026 to 2035.The Middle East and Africa held the 7% market share in 2025, akin to rising investments in petrochemical industries, infrastructure projects, and industrial manufacturing activities. In recent years, countries such as Saudi Arabia and the UAE have increased investments in construction, water management, and packaging industries, creating higher demand for compounded plastics. Moreover, the easy availability of petrochemical raw materials has supported the growth of local plastic production industries in the region.

PE and PP Compounding Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 24% |

| Europe | 21% |

| Asia-Pacific | 39% |

| Latin America | 9% |

| Middle East & Africa | 7% |

Saudi Arabia

- In Saudi Arabia, the country has invested heavily in infrastructure projects, industrial manufacturing, and water management systems, creating strong demand for compounded plastics.

- The country is also focusing on economic diversification and expanding downstream plastic manufacturing industries to reduce dependence on oil revenues.

UAE

- The country is investing in smart manufacturing technologies and industrial innovation to strengthen its plastics sector.

- Also, the automotive and consumer goods industries are increasing the use of lightweight plastic compounds for modern applications.

Recent Development

- In September 2025, Borealis has significantly invested in the expansion of the polypropylene compounding facilities, which are in Austria. Also, the company has invested more than EUR 100 million till and the main motive behind the investment is to increase production and supply of PP compounding, as per the company's claim.(Source: www.borealisgroup.com)

Top Vendors in the PE and PP Compounding Market & Their Offerings:

- LyondellBasell Industries: LyondellBasell is a dominant global leader in polyolefin technology and one of the largest plastics and chemical refiners. The company excels in advanced PE and PP compounding through its proprietary Catalloy and Hostacom processes. Its highly engineered materials primarily serve the automotive lightweighting, durable consumer goods, and high-performance packaging industries.

- SABIC (Saudi Basic Industries Corporation): SABIC is a petrochemical giant recognized for its extensive global manufacturing footprint in PP and PE compounding. The company focuses heavily on advanced material customization, delivering specialized compounds with high thermal resistance and mechanical strength. Its tailored resins are critical components for the automotive, mass transportation, electronics, and healthcare sectors.

- Borealis AG: Borealis is a European leader specializing in value-creating polyolefin compounding and sustainable circular plastics. Through its innovative Borstar technology, the company produces high-performance PE and PP grades designed for extreme environments. Its core commercial targets include energy power cables, infrastructure piping systems, and advanced automotive components.

Other Key Players

- Dow Inc.

- ExxonMobil Chemical

- TotalEnergies

- Chevron Phillips Chemical

- Ineos Group

- Braskem

- Avient Corporation

Segments Covered in the Report

By Type

- PE

- PP

By Polymer Type

- PE

- LLDPE

- LDPE

- MDPE

- HDPE

- PP

- Homopolymer PP

- Copolymer PP

- Terpolymer PP

By Compound Type

- PE

- HDPE pipe compound

- LDPE/LLDPE modified

- Cross-linkable PE (XLPE)

- Carbon-black-filled PE

- Conductive PE

- PP

- Talc-filled

- Glass-filled

- Mineral-filled

- Impact-modified

- Thermoplastic Polyolefin (TPO)

- Flame-Retardant (FR) PP

- Conductive PP

By Application

- PE

- Pipe & Infrastructure

- Gas distribution pipes (PE80, PE100)

- Drinking water pressure pipes

- Sewer & drainage pipes

- Cable protection ducts

- Irrigation pipes

- Wire & Cable

- Power cable insulation (XLPE)

- Medium & high voltage insulation

- Telecom cable sheathing

- Flame-retardant cable jacketing

- Semiconductive cable layers

- Packaging

- Milk & beverage bottles

- Detergent bottles

- Jerry cans & drums

- Chemical storage containers

- Food-grade bottles

- Automotive

- Fuel tanks

- Fuel lines

- Washer fluid reservoirs

- Coolant tanks

- Underbody shields

- Construction

- Geomembranes (landfill liners)

- Waterproof membranes

- Damp-proof sheets

- Protective construction films

- Other applications

- PP

- Automotive

- Bumpers

- Instrument panels

- Door trims

- Battery housings (EV)

- Air intake manifolds

- Electrical & Electronics

- Switch housings

- Circuit breaker casings

- Distribution boxes

- Cable trucking

- EV fuse housings

- Packaging

- Thin-wall food containers

- Dairy cups

- Microwave trays

- Caps & closures

- Reusable crates

- Construction

- PP-R plumbing pipes

- Hot & cold-water fittings

- Roofing membranes (TPO)

- Structural profiles

- Consumer Goods & Appliances

- Washing machine components

- Refrigerator liners

- Furniture parts

- Storage bins

- Medical & Healthcare

- Syringes

- IV components

- Lab containers

- Diagnostic trays

- Automotive

- Other applications

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (7)