Content

What is the current Post-Consumer Recycled Plastics Market Size and Share?

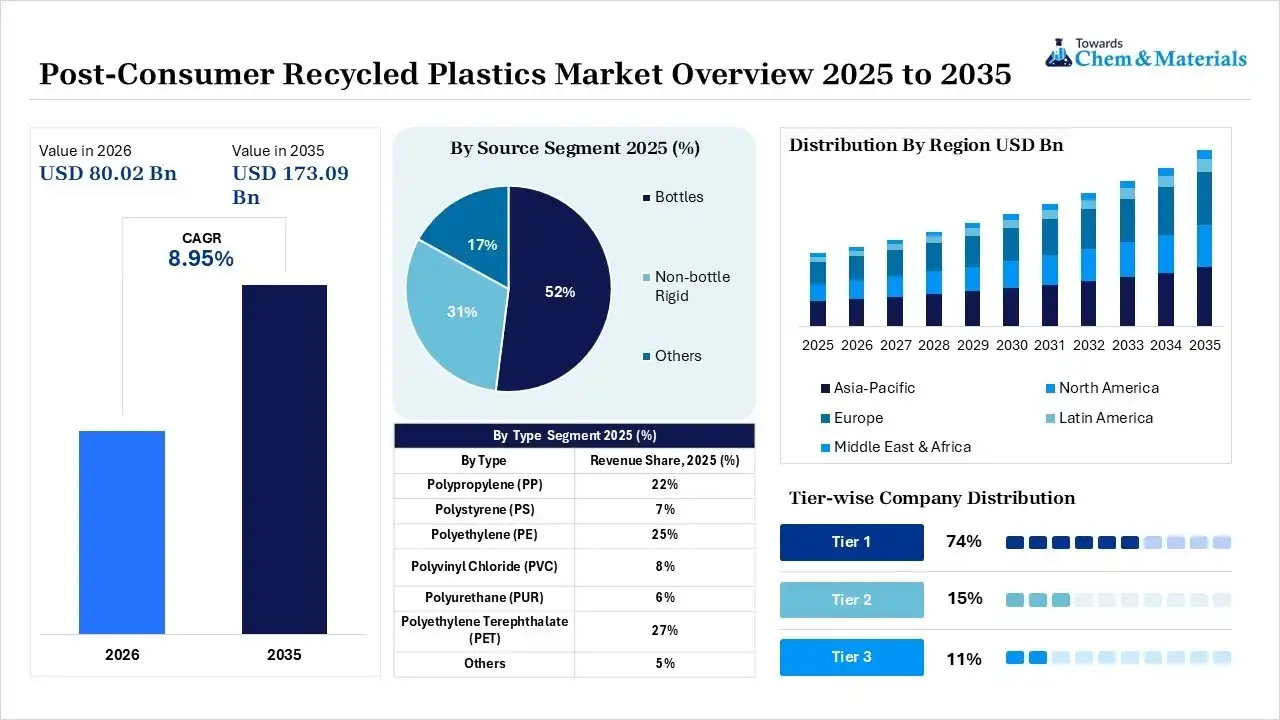

The post-consumer recycled plastics market size was valued at USD 73.45 billion in 2025, is estimated to reach USD 80.02 billion in 2026, and is projected to reach USD 173.09 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 8.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the post-consumer recycled plastics market with the largest revenue share of 34% in 2025 and is expected to grow at the fastest CAGR of 9.11% during the forecast period. In terms of volume, the post-consumer recycled plastics market is projected to grow from 58.96 million tons in 2025 to 129.07 million tons by 2035. growing at a CAGR of 8.15% from 2026 to 2035. The growth is propelled by strict regulatory compliance, a shift towards sustainability, and advancement in recycling solutions.

Key Takeaways

- By region, Asia Pacific dominated the market with 34% share in 2025 and is expected to grow at the fastest with a CAGR of 10.20% during the forecast period due to urban demand for recycled plastics and strong government support.

- By region, Europe held the 30% share in 2025, accelerated by strict recycling compliance and investment in circular content to meet circular economy goals.

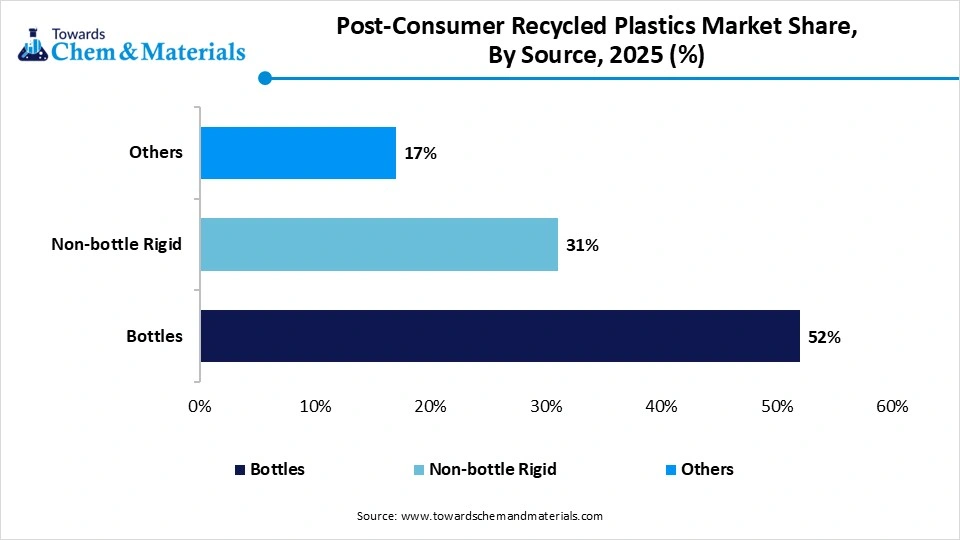

- By source, the bottles segment dominated the market with the largest share of 52% in 2025, driven by food-grade recycling capacity expansion and improvement in the deposit-return system.

- By source, the others segment held 17% market share in 2025 and is expected to grow at the fastest CAGR of 9.80% over the forecast period, fueled by advancements in film recovery solutions and government packaging recycling mandates.

- By type, the polyethylene terephthalate (PET) segment dominated the market with the largest share of 27% in 2025 due to its demand in food-grade &beverage packaging and adoption of recycled PET.

- By type, the polyurethane (PUR) segment held 6.0% market share in 2025 and is expected to grow at the fastest CAGR of 10.40% over the forecast period, driven by landfill diversion framework and development in chemical recycling technologies.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 73.45 Billion | CAGR (2026–2035): 8.95%

- Market Projected Size (2035): USD 173.09 Billion

- Asia Pacific: largest Market Revenue Share of 34% in 2025|USD 24.97 Billion

- Market Estimated Volume (2025): 58.96 Million Tons | Volume CAGR (2026–2035): 8.15%

- Market Projected Volume (2035): 129.07 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 930/Ton

- Average Selling Price: USD 1,290/Ton

- Pricing CAGR (2026–2035): 3.70%

The post-consumer recycled plastics market growth is enhanced by the stringent environmental, regulatory, and consumer pressures. These plastics originated from end-of-life packaging, electronics, household waste, and commercial waste, and are cleaned and reprocessed into high-quality plastics. As industries focus on reducing plastic waste and adopting recycled content to meet extended producer responsibility requirements. Manufacturers seeking to achieve sustainability through strategic collaboration that drives demand for high-quality reprocessed polymers.

Recycled plastics function as a mainstream, sustainable element of global manufacturing. Polyethylene terephthalate and high-density polyethylene maintain leadership positions due to their well-established infrastructure, which offers superior recycling rates and processing efficiency. The substantial investment in chemical recycling technologies like pyrolysis, depolymerization, and gasification. The integration of technologies breaks polymers into monomers to produce virgin-quality plastics in food-grade and flexible packaging. The major market players announced the acquisition of a recycling hub to protect essential feedstock and expand sustainable polymers.

Consumer demand for certified, sustainable resins, which is fueling interest in recycled plastics, focuses on reducing reliance on petrochemical supply chains. The domestic waste management framework requires secondary purification using virgin materials for high-performance applications. The technological transition drives automation, and the use of AI and near-infrared spectroscopy enables the production of high-quality, virgin plastics that meet strict food-contact and consumer safety values. Additionally, the innovation focuses on improving processing, standardizing resin grades, and expanding post-consumer waste collection, which boost market growth.

Market Trends

- Extended Producer Responsibility Goals: The trend is shaped by a shift towards circular plastics and the recycling of post-consumer waste, driving the market development.

- Advancement in Recycling Infrastructure: The major players focus on scaling advancement pyrolysis and depolymerization to produce high-purity recycled polymers in the market.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 80.02 Billion / 63.77 Million Tons |

| Revenue Forecast in 2035 | USD 173.09 Billion / 129.07 Million Tons |

| Growth Rate | CAGR 8.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Source, By Type, By Regions |

| Key companies profiled | BASF SE, SABIC, Evonik Industries AG, Sumitomo Chemical Co., Ltd, Arkema, Celanese Corporation, Eastman Chemical Company, Chevron Phillips Chemical Company, Exxon Mobil Corporation, Covestro AG |

Key Technological Shifts and AI in the Post-Consumer Recycled Plastics Market

The technological innovation is a key catalyst for the adoption of post-consumer recycled plastics. The integration of hyperspectral sensors provides precise chemical analysis. The AI-driven sorting detects complex polymers & flame retardants. Advancements in chemical recycling infrastructure, especially through pyrolysis, which breaks down contaminated films into pure monomers by removing smell, colors, and toxins.

IoT+ML platform boosts post-consumer waste management efficiency and performance of recycled plastics.

Cooperative R&D investments in emerging economies are rapidly advancing near-infrared (NIR) spectroscopy to detect molecular compositions of polymer and distinguish post-consumer polymer modifications. Additionally, the merging of digital passports and blockchain promotes transparency and transforming lifecycles of polymers.

Supply Chain Analysis of the Post-Consumer Recycled Plastics Market

- Feedstock Procurement and Primary Collection: The stage of sourcing and collection of mixed post-consumer plastic waste through municipal infrastructure, deposit-return system.

- Key Players: Republic Services, Veolia Waste Services, Waste Management Inc., Remodis, and Biffa

- Advanced Sorting and Polymer Refining: The stage of conversion of highly contaminated plastic into high-purity feedstock from high-speed sorting liners with NIR sensors, computer vision, and AI robotics to isolate specific polymers.

- Key Players: Indorama Ventures, ALPLA Group, Veolia Environmental Services, Clean Planet Energy, and KW Plastics

- High-Value Conversion and Manufacturers Integration: The stage of compounding, structural engineering, and through blending processes like extruders, blow-molding. The industrial plastic converter buys post-consumer recycled pellets and flakes for end-product manufacturing.

- Key Players: Dow Chemical & LyondellBasell, Berry Global, Amcor Plc., Unilever, and Coca-Cola Company.

Regulatory Framework: Post-Consumer Recycled Plastics Market

| Key Region | Primary Regulations | Regulatory Mechanism |

| Europe | EU Packaging & Packaging Waste Regulation and Plastic Packaging Tax | Regulation for minimum PCR content and penalties for virgin resins. |

| North America | State-Level Recycled Content Mandates and State EPR Laws | Standards for food & beverages to scale post-consumer content in bottles. The financial non-compliance administrative fees for the municipal collection system. |

| Asia Pacific | Action Plan for Plastic Pollution Control & Plastic Waste Management (PWM) Rules | Focus on recycling targets for packaging waste, with minimal PCR usage, and mandate high-capacity pyrolysis-based chemical recycling in the waste stream. |

| Latin America | Chile’s EPR Law and General Law for Waste Management | Law for collection and valorisation for industrial and domestic plastic waste. Mandates for 30% PCR integration in PET packaging. |

| Middle East & Africa | South Africa's EPR Regulations & UAE Ministerial Decision | Mandate waste picker integration and MRF sorting technology in domestic level. Focus on the single-use import prohibition |

Post-Consumer Recycled Plastics Market Dynamics

Driver

Regulatory Framework For Recycled Content

The regulatory framework for recycled content plays an essential role in market growth. Governments have introduced strict EPR policies and sector-specific regulations across sectors such as FMCG, automotive, consumer electronics, and beverages to achieve higher recycled content targets. The import and export penalties, audits, and trials reinforce procurement efforts, often sourcing 25%-50% PCR. This regulatory pressure has shifted PCR from an optional eco-friendly alternative to an indispensable raw material and high-purity product, supported by an established infrastructure

Restraints

Value Chain Contamination and Polymer Degradation

The main restraint in the market is contamination and thermal degradation of recycled plastics, with mixed waste. Repetitive high-heat extrusion damages the polymer composition, reducing strength and precision. The strict food safety standards require high-quality decontamination, which enables higher supply chain costs, limiting the supply of high-quality post-consumer recycled plastics in the market.

Opportunity

Advancement in Recycling for Food-Grade Application

The advancement of the market is increased by the development of advanced chemical recycling to process hard-to-abate plastic materials. The well-established process enables the breakdown of complex polymers into monomers by removing contamination and offering operational stability in large-scale production. The increasing demand for recycled plastics creates expanded opportunities to integrate pyrolysis and depolymerization methods. This opportunity fosters the quality of plastics to meet food-contact standards for food-safe recycled polymers.

Segmental Insights

Source Insights

The bottles segment dominated the market with 52% share in 2025, owing to its uniform melt indices and wall thicknesses, which maintain high purity and volumetric yield. It serves as a uniform feedstock stream from standardized production of beverage bottles, personal care bottles, and household chemical containers, capturing high-purity, clear polyolefins and polyesters. Additionally, this source focuses on vacuum-thermal decontamination to meet safety standards for food-grade and closed-loop packaging.

")

The others segment held the 17% market share in 2025 and is expected to grow at the fastest CAGR of 9.80% over the forecast period. It contains discarded plastic films, flexible packaging waste, e-commerce wraps, agricultural coverings, and synthetic fibers. This source focuses on LLDPE, and polyurethane blends rejected by municipal facilities. The recycling operators use advanced dissolution-precipitation and chemical pyrolysis to manufacture high-quality feedstocks for the packaging and textile sector by ensuring higher tensile strength.

The non-bottle rigid segment held the 31% market share in 2025, offers new opportunities to recover polystyrene and polypropylene from food trays, crates, containers, electronics closures, and industrial rigid packaging. The non-bottle rigid feedstock has diverse properties, blends, and pigments by ensuring superior impact resistance and strength. The technological shift is driving the utilization of laser spectroscopy and electrostatic separation to isolate specific polymers for the manufacturing of high-quality resins for automotive and construction infrastructure.

Post-Consumer Recycled Plastics Market Share, By Source, 2025 (%)

| By Source | Revenue Share, 2025 (%) |

| Bottles | 52% |

| Non-bottle Rigid | 31% |

| Others | 17% |

Type Insights

The polyethylene terephthalate (PET) segment dominated the market with the largest share of 27% in 2025. It is leading because of its clarity and gas-barrier ability. Operators utilize sorting setups and deposit systems to maintain a consistent supply of clean, single-polymer raw materials. The high-quality recycled and colored PET is a valuable asset due to its support from regulatory requirements to meet food-grade standards for consumer packaging. Additionally, recyclers implement solid-state polymerization to rebuild degraded PET chains and reestablish tensile strength.

The polyethylene (PE) segment held the 25% market share in 2025. The recycled PE is derived from HDPE, LLDPE, and LDPE waste. Recyclers practice advanced filtration and thermal processes to manufacture high-purity PE pellets by ensuring a stable supply chain and collection framework. Polyethylene offers a superior moisture barrier and impact resistance preferred in construction, packaging, and retail. The major companies' shift towards sustainability and the circular economy is accelerating the reliable supply of recycled polyethylene.

The polyurethane (PUR) segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 10.40% over the forecast period. Driven by a shift towards lower scope 3 emissions, where PU is highly specialized and reclaiming robust materials from end-of-life vehicles and insulation. Polyurethane is a thermosetting polymer that requires advanced cryogenic micronization to meet circular economy targets. The segment is advancing in catalytic glycolysis and acidolysis to break urethane bonds, converting waste into a liquid polyol to make new automotive and industrial foams.

The polypropylene (PP) segment held the 22% market share in 2025. Owing to the transition towards automotive sustainability and e-waste strategies, the usage of recycled PP for lightweight parts is reclaiming large amounts of rigid food containers and automotive bumpers. This converts rigid and flexible scrap into high-ductility, high-impact-resistance PP. This segment requires advanced supercritical fluid extraction and specialized additives to remove VOCs, ensure stable performance, and prevent degradation.

Post-Consumer Recycled Plastics Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Polypropylene (PP) | 22% |

| Polystyrene (PS) | 7% |

| Polyethylene (PE) | 25% |

| Polyvinyl Chloride (PVC) | 8% |

| Polyurethane (PUR) | 6% |

| Polyethylene Terephthalate (PET) | 27% |

| Others | 5% |

The polyvinyl chloride (PVC) segment held the 8% market share in 2025. As manufacturers incorporate recycled PVC into new green building infrastructure, they offer high flame retardance, strength, and weatherability. Due to PVC's high chlorine content, mixed post-consumer waste is isolated during recycling using X-ray fluorescence. Recyclers use solvent-based technology to recover durable materials, remove plasticizers and stabilizers, and process textiles.

The polystyrene (PS) segment held the 7% market share in 2025. PS requires advanced densification to produce high-quality circular and recycled polystyrene granules utilized in electronics and food packaging. rPS is a fast-growing material, regaining market share in lightweight expanded foam and high-impact packaging. Additionally, operators adopt thermal depolymerization for breaking polymers into pure styrene monomers.

Regional Insights

How Did the Asia Pacific Dominated the Post-Consumer Recycled Plastics Market in 2025?

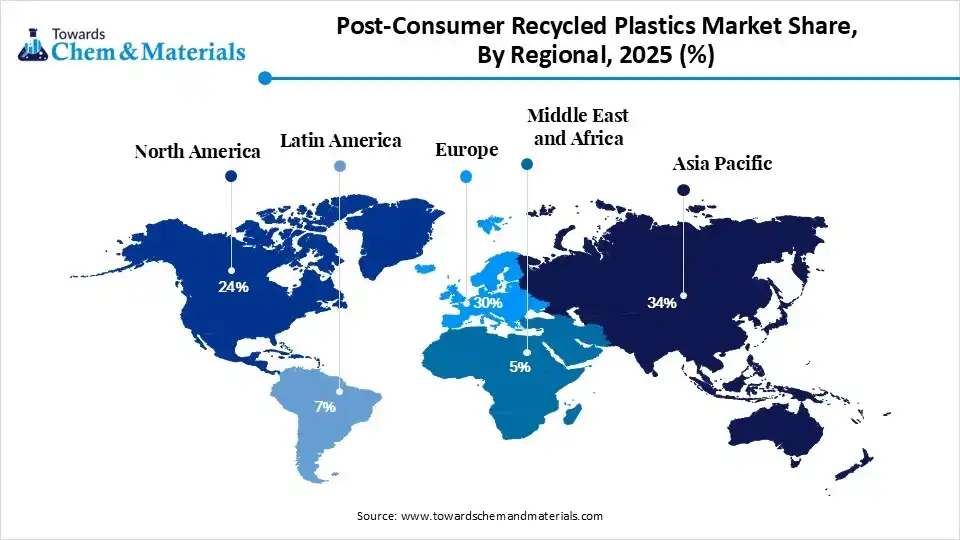

The Asia Pacific post-consumer recycled plastics market size was estimated at USD 24.97 billion in 2025 and is projected to reach USD 59.72 billion by 2035, growing at a CAGR of 9.11% from 2026 to 2035.Asia Pacific dominated the market with 34% share in 2025 and is expected to grow at the fastest with a CAGR of 10.20% during the forecast period. The growth is defined by high-tech automation for urban waste and post-consumer plastics. The region is seeing growing investment in optical sorting and processing of polyolefin and polyester waste to meet extended producer responsibility compliance. Additionally, domestic players focus on long-term supply contracts, positioning Asia Pacific as a high-quality circular-plastics export hub.

China

- Growth is propelled by extensive installation of automated near-infrared spectroscopy and a domestic focus on collecting municipal solid waste.

- China's expansion in industrial chemical depolymerization, mostly in electronics and textiles, is supported by green certification and automated separation hubs.

India

- India is launching a mechanical scrap recycling loop and a specialized food-grade compounding assembly using post-consumer polyolefins for domestic infrastructure.

- Stringent EPR requirements and government efforts to phase out single-use plastics drive investments in strategic petrochemical resin replacements.

The Europe post-consumer recycled plastics market size was estimated at USD 22.04 billion in 2025 and is projected to reach USD 52.79 billion by 2035, growing at a CAGR of 9.13% from 2026 to 2035.Europe held the 30% market share in 2025, driven by stringent EU regulations that set high recycled-content goals. Europe’s deposit-return schemes capture high-purity, food-grade PET. The regional circularity targets for reprocessed pellets to remove hazardous content and hard-to-rebate plastics, accelerating the domestic growth. European companies' investments in pyrolysis and depolymerization to recycle post-consumer waste.

Germany

- The country is at the lead of large-scale production of advanced hot-corrosive friction materials and the integration of chemical pyrolysis hubs.

- Germany's demanding packaging and environmental regulations for non-recyclable plastics are motivating local companies to develop improved collection and sorting solutions.

Italy

- Italy is focused on high-purity plastics using automated reverse-end-of-line machines, aligned with government carbon-neutrality targets and food-grade plastic production lines.

- The region is experiencing rapid scaling of enzymatic recycling and advanced polymer thermal cracking to achieve recycling commitments.

The North America post-consumer recycled plastics market size was estimated at USD 17.63 billion in 2025 and is projected to reach USD 42.41 billion by 2035, growing at a CAGR of 9.17% from 2026 to 2035.North America held 24% market share in 2025, fueled by a regional integrated collection solution and circular polymer economy commitments. The regional strict regulatory framework for virgin-quality resins and certified food-grade recycled polymers trading. North America's recyclers and petrochemical companies are investing in local mega-reclamation facilities, aligned with AI sorting and engineering, to produce rPE, rPP, and rPET.

United States

- The country is a leader in technological advancements, mainly in adopting AI-driven sorting robotics and restoring intrinsic viscosity through solid-state polymerization.

- Additionally, the US government encourages the use of high-performance, sustainable components from domestic recycled materials to meet regulatory compliance with Extended Producer Responsibility (EPR).

The Latin America post-consumer recycled plastics market size was estimated at USD 5.14 billion in 2025 and is projected to reach USD 12.98 billion by 2035, growing at a CAGR of 9.71% from 2026 to 2035.Latin America held 7% market share in 2025, due to modernized recycling. With Latin America's strict regulations and corporate sustainability commitments, domestic recyclers are installing automated NIR sorting systems. Regional packaging producers use food-grade recycled resins and focus on separating pure polyethylene terephthalate and polyolefins from post-consumer waste, thereby strengthening their market presence.

Brazil

- The local expansion is supported by their increased recovery of non-bottle rigid substrates and the employment of a high-performance friction waste system.

- Brazil's consumer demand for sustainable resin in civil and automotive infrastructure is driven by supply chain integration.

Argentina

Argentina's recycling infrastructure supports demand for post-consumer recycled plastics in manufacturing.

Driven by growing local interest, influenced by solid waste policies, and the rising adoption of reverse transport initiatives for reprocessed plastic content.

")

The Middle East & Africa post-consumer recycled plastics market size was estimated at USD 3.67 billion in 2025 and is projected to reach USD 9.52 billion by 2035, growing at a CAGR of 10.00% from 2026 to 2035.The Middle East & Africa held 5% market share in 2025, driven by MEA sustainability targets and plastic bans through the domestic waste reclamation network. Government funding supports the adoption of recycled polymers to reduce landfill waste. MEA domestic operators use automated near-infrared sorting to recover high-purity PET and polyurethane in the urban framework, boosting domestic expansion.

Saudi Arabia

- The expansion is fueled by a large-scale mechanical sorting framework and commercial crude-to-plastic circular loops through partnerships with petrochemical companies.

- Saudi Arabia's Vision 2030 sustainability standards and strict quality protocols create a suitable environment for green procurement and polymer diversion.

Post-Consumer Recycled Plastics Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 24% |

| Europe | 30% |

| Asia-Pacific | 34% |

| Latin America | 7% |

| Middle East & Africa | 5% |

Recent Developments

- In March 2026, TotalEnergies and Plastic Energy Technology began collaborative production at France's first large-scale TotalEnergies Plastic Energy advanced recycling (TEPEAR) plant located at TotalEnergies' zero-crude Grandpuits complex near Paris. This facility processes 15,000 tons of hard-to-recycle plastic waste each year, transforming it into sustainable feedstock for new plastic manufacturing.(Source: plasticenergy)

- In May 2025, Eni’s chemical subsidiary, Versalis, announced the start of operations at its new recycled polymer manufacturing plant in Porto Marghera, Italy. The facility is designed especially for consumer packaging and sustainable building materials. Through technological innovation and post-consumer plastics recycling.(Source: hydrocarbonprocessing)

Top Companies in the Post-Consumer Recycled Plastics Market

- BASF SE

- SABIC

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd

- Arkema

- Celanese Corporation

- Eastman Chemical Company

- Chevron Phillips Chemical Company

- Exxon Mobil Corporation

- Covestro AG

Segment Covered in the Report

By Source

- Bottles

- Beverage Bottles

- Water Bottles

- Personal Care Bottles

- Household Product Bottles

- Non-bottle Rigid

- Containers

- Crates & Boxes

- Caps & Closures

- Industrial Rigid Packaging

- Others

- Films

- Flexible Packaging Waste

- Agricultural Plastics

- Mixed Plastic Waste

By Type

- Polypropylene (PP)

- Rigid PP Recyclate

- Flexible PP Recyclate

- Polystyrene (PS)

- General Purpose PS

- High Impact PS

- Polyethylene (PE)

- HDPE

- LDPE

- LLDPE

- Polyvinyl Chloride (PVC)

- Rigid PVC

- Flexible PVC

- Polyurethane (PUR)

- Rigid PUR

- Flexible PUR

- Polyethylene Terephthalate (PET)

- Clear PET

- Colored PET

- Others

- ABS

- Nylon

- Polycarbonate

- Mixed Engineering Plastics

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Tags

FAQ's

Select User License to Buy

Figures (5)