Content

What is the Current Size of the Electric Vehicle Plastics Market and Its Projected Growth?

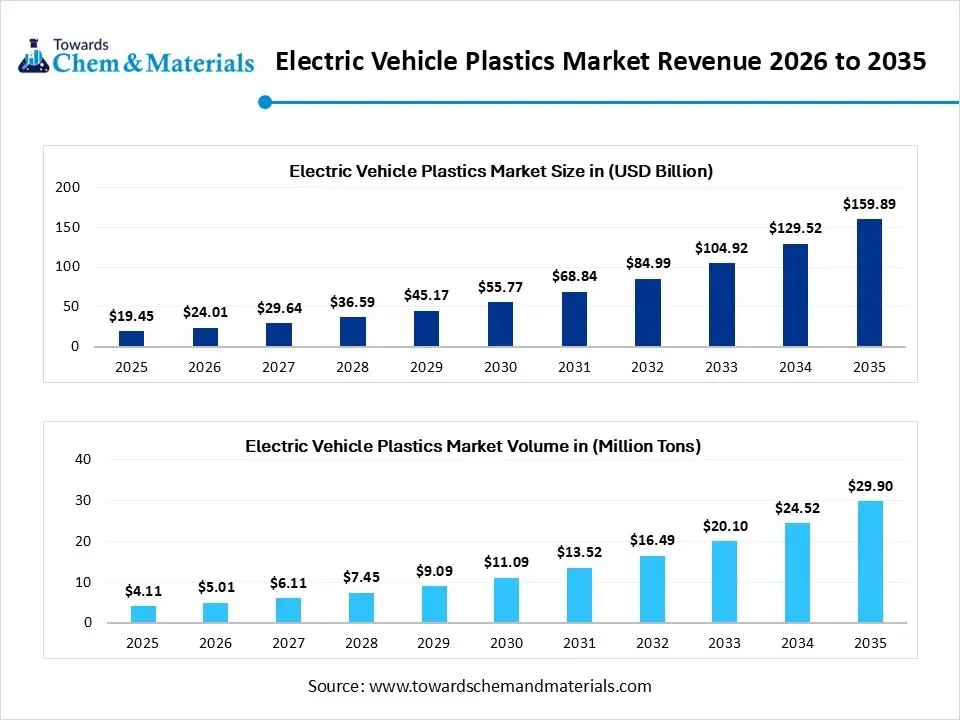

The global electric vehicle plastics market size was estimated at USD 19.45 billion in 2025 and is expected to increase from USD 24.01 billion in 2026 to USD 159.89 billion by 2035, growing at a CAGR of 23.45% from 2026 to 2035. In terms of volume, the market is projected to grow from 4.11 million tons in 2025 to 29.90 million tons by 2035. growing at a CAGR of 21.95% from 2026 to 2035.The growth is driven by demand for high-performance engineering plastics, sustainability goals, extended producer responsibility and integration of smart and HMI systems.

Market Highlights

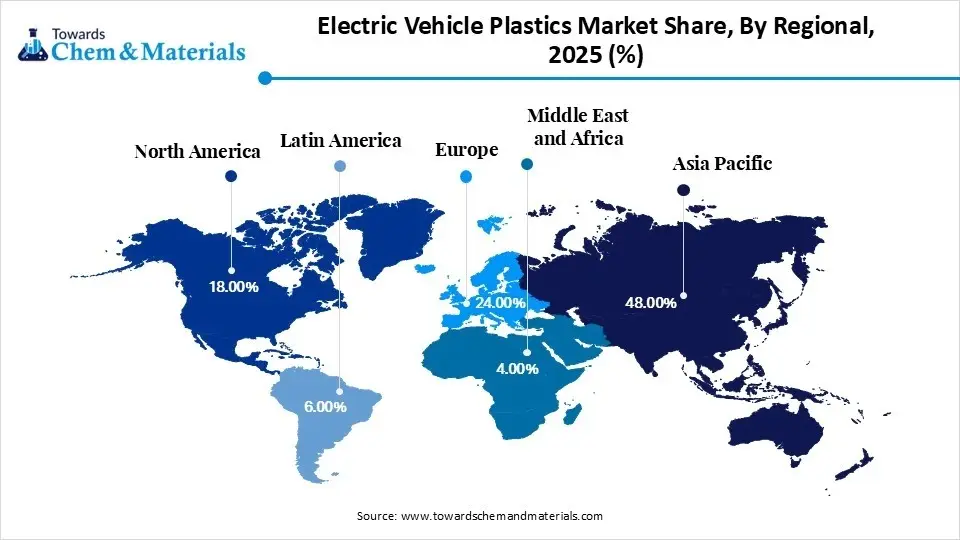

- By region, Asia Pacific dominated the electric vehicle plastics market by holding a 48% share in 2025 due to its massive manufacturing and innovation hub.

- By region, Europe expects the fastest growth with the 22% market share from 2026 to 2035 due to regional sustainability focus and stringent regulatory framework.

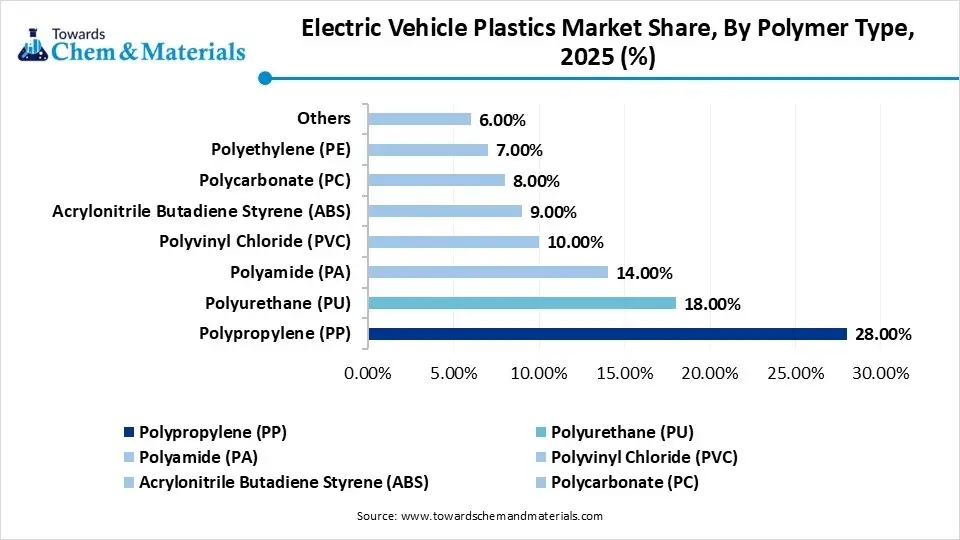

- By polymer type, the polypropylene (PP) segment held the largest 28% share in the market in 2025 due to its ultra-lightweighting and higher cost-performance.

- By polymer type, the polyurethane (PU) segment held the second largest share of 18% in 2025 due to its ability to provide battery safety and superior thermal management in modern electrification.

- By application, the interior components segment dominated the market with 30% share in 2025, driven by its merger of sustainable premiumship and automotive lightweighting

- By application, the battery components segment held the second largest share of 21% in 2025 due to its ability to provide electrochemical safety and thermal management.

- By vehicle type, the passenger EVs segment dominated the market with 52% share in 2025, driven by rising focus on consumer-driven innovation and a modern environment consumer base.

- By vehicle type, the electric two-wheelers segment held the second largest share of 20% in 2025 due to its power-to-weight ratio and its shift towards the circular economy.

- By processing technology, the injection molding segment dominated with a held 40% share in the market in 2025 due to rising focus on light weighting and performance efficiency by integrating with smart manufacturing

- By processing technology, the 3D printing segment held the second largest share of 15% in 2025 due to the implementation of additive manufacturing in automotive and rapid prototyping

- By end-use component function, the structural plastics segment dominated with a held 32% share in the market in 2025 due to its mechanical stability, safety and radical part consolidation.

- By end-use component function, the insulation plastics segment held the second largest share of 26% due to demand for electrical safety and thermal management systems.

Market Size and Volume Forecast

- Market Size (2025): USD 19.45 Billion | CAGR (2026–2035): 23.45%

- Market Projected Size (2035): USD 159.89 Billion

- Market Volume (2025): 4.11 Million Tons (MT) | Volume CAGR (2026–2035): 21.95%

- Market Projected Volume (2035): 29.90 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 3,870/Ton

- Average Selling Price: USD 4,780/Ton

- Pricing CAGR (2026–2035): 4.85%

Market Overview

The electric vehicle plastics market is a high- tech evolution in automotive engineering, aligning with advanced polymers that are crucial for electrification. It focuses on lightweighting with high- performance resins like PP, PA, and PC to reduce battery weight and improve driving range. The innovations in electric vehicles include flame- retardant grades for safety, high-voltage insulation and thermal management. Additionally, the consumer focuses on sustainability, and the automotive industry shifts towards recycled and bio- based resins to reduce the carbon footprint of the vehicle. The market represents engineered plastics for structural integrity, crash safety, and energy efficiency, which is driving the expansion.

Recent Market Trends

- Rising Demand in Automotive Scaling: The demand for lightweight, high-performance power sources in aerospace, automotive and commercial transit is accelerating the adoption of advanced engineered plastics in electric vehicles.

- Value Chain Reshoring and Vertical Integration: The global automotive efforts towards localizing production of high-purity plastics and advanced electrochemical materials, targeting domestic supply security.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 24.01 Billion / 5.01 Million Tons |

| Revenue Forecast in 2035 | USD 159.89 Billion / 29.90 Million Tons |

| Growth Rate | CAGR 23.45% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Polymer Type, By Application, By Vehicle Type, By Processing Technology, By End-Use Component Function, By Region |

| Key companies profiled | Asahi Kasei Corporation, BASF SE, Borealis GmbH, Celanese Corporation, Covestro AG, DuPont, Envalior (DSM Engineering Materials), Evonik Industries AG, Huntsman International LLC, INEOS AG, LANXESS, LG Chem, LyondellBasell Industries, Röhm GmbH, RTP Company, SABIC, Solvay, TORAY INDUSTRIES, INC. Solvay |

Key Technological Shifts and AI in the Electric Vehicle Plastics Market

AI and technological development are transforming the market from reactive engineering to predictive material science. The integration of molecular modelling and machine learning is accelerating the discovery and optimized strength-to-weight ratios. The development of smart plastics with embedded sensors and self-healing capabilities necessitates the importance of battery housing.

The generative design improves lightweighting by creating efficient, biomimetic structural components for EVs. Additionally, the robotic sorting optimizing manufacturing, maximizes vehicle range and safety, supporting the circular economy using integration of high-purity recycled resins with precision.

Trade Analysis of the Electric Vehicle Plastics Market: Import and Export Statistics

- Vietnam exported 150,924 shipments of electric vehicle plastics.

- China exported 11,549 shipments of electric vehicle plastics.

- Japan exported 8,594 shipments of electric vehicle plastics.

- From July 2024 to June 2025, the world exported 68,311 shipments of electric vehicle plastics.

Electric Vehicle Plastics Market: Supply Chain Analysis

- Raw Material and Resin Manufacturing: The key stage that focuses on molecular engineering of base resins and development of specialized plastics to meet thermal stability and flame-retardant requirements.

- Key Players: BASF SE, LyondellBasell, DuPont, SABIC and Dow

- Advanced Components Fabrication: The precision conversion technologies to transform raw resins into functional parts to achieve lightweighting. The manufacturers create battery enclosures, coolant manifolds and high-voltage connector housings.

- Key Players: LG Chem, Covestro AG, Solvay, Celanese Corporation and Lanxess

- Automotive Integration and Final Assembly: The final stage, where OEMs integrate plastic components into electric vehicles by adopting closed-loop recycling to reclaim plastics from end-of-life electric vehicles.

- Key Players: Tesla, BYD, Hyundai Motor Group, Tesla and Volkswagen Group

Regulatory Framework: Electric Vehicle Plastics Market

| Region | Key Regulation | Regulatory Focus |

| Europe | EU ELV Directive | Mandates recycled plastic content and regulations focus on circularity and carbon footprint in new vehicles. |

| Asia Pacific | GB Standards, Plastic Waste Management Rule | Focus on thermal diffusion that requires plastic battery packs and strict mandates for thermal management. |

| North America | UL 94, Standard for Safety, Inflation Reduction Act | Standard for flammability and incentives or domestic sourcing and advanced lightweighting |

| Global | UN ECE R100, IEC (CTI) | Regulates the comparative tracking index to ensure plastics prevent electrical arcing |

Segmental Insights

Polymer Type Insights

Polypropylene (PP) Segment Dominated the Electric Vehicle Plastics Market with 28% of Market Share in 2025

Polypropylene (PP) segment dominated the electric vehicle plastics market with 28% share in 2025. The leadership is driven by its ultra-lightweight and cost-effectiveness in superior performance. The PP utilized in heavy battery engineering accelerates vehicle longevity and energy density. The segment acts as a solution for aerodynamic underbody shields, battery tray and interior trims by offering chemical resistance and recyclability to meet circular economy targets and sustainability.

Polyurethane (PU) segment held the second largest share of 18% in 2025 due to its superior dumping, high impact resistance and durability that offers battery safety and thermal management for potting resins, gap fillers and encapsulants. The PU provides a lightweight solution for acoustic insulation and seating framework by lowering noise, vibration and harshness in the EV cabin. The rising transition towards bio-based polyurethanes to reduce carbon footprint in the automotive sector positions the segment as a pillar of modern electrification.

")

Polyamide (PA) segment held the third largest share of 14% in 2025 due to its thermal stability and mechanical robustness. The segment acts as a metal replacer that substitutes alloys in battery enclosures and high-voltage connectors by offering better heat resistance, chemical durability and lightweighting. Additionally, the PA utilizes specialised flame-retardants and ensures safety innovation and reliability of the electrified fleet.

PVC segment held the fourth largest share of 10% in 2025, driven by its flame-retardancy and electrical insulation in high-voltage wiring harnesses and cable management. The PVC's dielectric strength enables safe transmission in the electric drivetrain, while its impact durability and corrosion resistance make it ideal for exterior sealant and underbody protection. As the industry is shifting towards non-phthalate plasticizer to meet sustainability goals, driving the adoption of PVC in the mass-scale electric market.

Electric Vehicle Plastics Market Share, By Polymer Type, 2025 (%)

| By Polymer Type | Revenue Share, 2025 (%) |

| Polypropylene (PP) | 28.00% |

| Polyurethane (PU) | 18.00% |

| Polyamide (PA) | 14.00% |

| Polyvinyl Chloride (PVC) | 10.00% |

| Acrylonitrile Butadiene Styrene (ABS) | 9.00% |

| Polycarbonate (PC) | 8.00% |

| Polyethylene (PE) | 7.00% |

| Others | 6.00% |

- Polypropylene (PP) leads the market with a share of 28.00%. Its lightweight and durable properties make it a preferred choice in electric vehicle applications, including interior and exterior components.

- Polyurethane (PU) accounts for 18.00% of the market. PU's versatility and high performance in insulation and cushioning materials contribute to its use in electric vehicle parts like seating and interior panels.

- Polyamide (PA) holds 14.00% of the market. PA's strength, resistance to heat, and chemical properties make it ideal for engine components, electrical parts, and other high-stress applications.

- Polyvinyl Chloride (PVC) makes up 10.00% of the market. PVC is commonly used for wiring insulation and interior parts due to its durability and cost-effectiveness.

- Acrylonitrile Butadiene Styrene (ABS) represents 9.00% of the market. ABS is favored for its impact resistance and ease of processing, making it suitable for interior and exterior parts.

- Polycarbonate (PC) holds 8.00% of the market. Its high impact resistance and optical clarity make it ideal for headlights, lenses, and other transparent parts.

- Polyethylene (PE) makes up 7.00% of the market. PE is used in electric vehicles for fuel tanks, battery components, and insulation materials due to its strength and flexibility.

- Others account for 6.00% of the market. This category includes various other polymers used in niche applications across electric vehicles.

Application Insights

Interior Components Segment Dominated the Electric Vehicle Plastics Market with 30% of Market Share in 2025

The interior components segment dominated the electric vehicle plastics market with 30% share in 2025. It represents the integration of automotive lightweighting and sustainable luxury that serves as a key hub for human-machine interface innovation. The interior components are key to the circular economy that drives the adoption of recycled content and bio-based resins, which is premium for a near-silent electrified cabin.

Battery components segment held the second largest share of 21% in 2025, driven by its ability to provide electrochemical safety and thermal management with automotive lightweighting. The segment provides superior battery energy density and utilizes advanced flame retardant, which is crucial for cell-to-pack spacer, battery enclosures and busbar covers. Additionally, this component offers protection and safeguards the high-voltage integrity of the electric drivetrain.

The exterior components segment held the third largest share of 18% in 2025, due to its automotive lightweighting and energy efficiency. The segment is a key hub for aerodynamic innovation that focuses on creating integrated sensors, updated wheel covers and active grille shutters. The exterior segment ensures safety, impact resistance and corrosion protection to meet circular economy targets.

Under-the-hood components segment held the fourth largest of 13% in 2025. The expansion is driven by the superior thermal profiles of the electric drivetrain. The segment represents a catalyst for thermal management development for coolant pumps, integrated manifolds and valves. These components ensure high reliability of power electronics align with the circular economy, which utilized heat-stabilized recycled composites.

Electric Vehicle Plastics Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Interior Components | 30.00% |

| Exterior Components | 18.00% |

| Under-the-Hood Components | 13.00% |

| Battery Components | 21.00% |

| Electrical Components | 10.00% |

| Structural Components | 8.00% |

- Interior Components lead the market with a share of 30.00%. Plastics are widely used in seats, dashboards, and trim parts due to their lightweight and design flexibility.

- Exterior Components account for 18.00% of the market. These plastics are used for body panels, bumpers, and mirrors, offering durability and resistance to environmental factors.

- Under-the-Hood Components hold 13.00% of the market. Plastics in this category are used for engine components, cooling systems, and other parts that require heat resistance and strength.

- Battery Components represent 21.00% of the market. Plastics are essential in battery casings and insulation, providing safety and structural integrity to electric vehicle batteries.

- Electrical Components make up 10.00% of the market. Plastics in electrical applications are used for wiring insulation, connectors, and housings, ensuring safety and reliability in the vehicle's electrical systems.

- Structural Components account for 8.00% of the market. Plastics used in structural components offer strength and weight reduction, contributing to the vehicle's overall performance and efficiency.

Vehicle Type Insights

Passengers EVs Segment Dominated the Electric Vehicle Plastics Market with 52% of Market Share in 2025

Passenger EVs segment dominated the electric vehicle plastics market with 52% share in 2025, driven by consumer-driven innovation to extend driving range and lightweight. The segment is key for interior and exterior revolution integrated with the circular economy, which focuses on superior acoustic insulation and impact safety for modern, eco-conscious consumers.

Electric two-wheelers segment held the second largest share of 20% in 2025, a functional tool that ensures a power-to-weight ratio and high-performance engineering plastics that maximize battery range and urban modernization. The segment offers weather-resistant body panels, compact battery housing and vibration-dampening components that utilizing recycled resins to achieve a sustainable solution for eco-conscious commuters.

The commercial EVs segment held the third largest share of 18% in 2025, characterized by its durability-driven framework that is ideal for mechanical stress and high-duty cycles of logistics and public transport. The segment is focused on innovation for maintaining structural integrity and weatherability in rigorous electrified fleet operations.

The electric buses segment held the fourth largest share of 10% in 2025 because it stabilises mass transit efficiency with occupant safety. The electric buses replace steel frames with high-strength composites by maximizing passenger payload and driving range. Along with the stringent public procurement mandates and an automotive sector shift towards interior sustainability, driving the segment presence in urban transit.

Electric Vehicle Plastics Market Share, By Vehicle Type, 2025 (%)

| By Vehicle Type | Revenue Share, 2025 (%) |

| Passenger EVs | 52.00% |

| Commercial EVs | 18.00% |

| Electric Two-Wheelers | 20.00% |

| Electric Buses | 10.00% |

- Passenger EVs lead the market with a share of 52.00%. Plastics are extensively used in interior, exterior, and structural components to reduce weight and enhance performance in passenger electric vehicles.

- Commercial EVs account for 18.00% of the market. Plastics in commercial electric vehicles help improve durability, reduce weight, and enhance efficiency in larger vehicle structures.

- Electric Two-Wheelers make up 20.00% of the market. Plastics play a crucial role in reducing the overall weight and improving the design and performance of electric motorcycles and scooters.

- Electric Buses hold 10.00% of the market. Plastics are used in various parts of electric buses, including body panels and interior components, to reduce weight and increase energy efficiency.

Processing Technology Insights

Injection Molding Segment Dominated the Electric Vehicle Plastics Market with 40% of Market Share in 2025.

Injection molding Segment dominated the electric vehicle plastics market with 40% share in 2025, driven by rising manufacturers' focus on lightweighting, battery longevity, and performance efficiency. The adoption of all-electric molding machines that offer energy efficiency with the integration of smart manufacturing to meet safety standards for EVs positions the segment as key for modern automotive technology.

The 3D printing segment held the second largest share of 15% in 2025 due to rapid prototyping and adoption of additive manufacturing in automotive for developing complex geometric and lightweight structures. The segment utilizing high-performance polymers and carbon filaments to optimize battery range and thermal management. Additionally, 3D printing provides design flexibility and slashes lead times in EVs.

Blow molding segment held the third largest share of 14% in 2025. The segment specialized in the manufacturing of hollow components required for thermal and fluid containment. The process replaces heavy metal with lightweight structures like HVAC ducting and battery cooling circuits. The blow moulding enables space-optimized designs and provides structural integrity for next-generation all-electric vehicles.

Extrusion segment held the fourth largest share of 12% in 2025, due to its space efficiency and safety for complex EVs. The segment is forcing molten high-performance polymers to develop thin-walled systems for protecting high-voltage wiring and battery cooling circuits. The process offers superior chemical resistance and electrical insulation, which extends battery range.

Electric Vehicle Plastics Market Share, By Processing Technology, 2025 (%)

| By Processing Technology | Revenue Share, 2025 (%) |

| Injection Molding | 40.00% |

| Blow Molding | 14.00% |

| Thermoforming | 10.00% |

| Extrusion | 12.00% |

| Compression Molding | 9.00% |

| 3D Printing | 15.00% |

- Injection Molding holds the largest share of the market with 40.00%. This technology is widely used for producing precise and complex plastic parts used in various components of electric vehicles.

- Blow Molding accounts for 14.00% of the market. It is commonly used for producing hollow plastic parts, such as fuel tanks and air ducts, in electric vehicles.

- Thermoforming holds 10.00% of the market. This process is used for shaping plastic sheets into large, lightweight components for vehicle interiors and exteriors.

- Extrusion represents 12.00% of the market. Extruded plastics are used in applications like trim, seals, and other structural components in electric vehicles.

- Compression Molding makes up 9.00% of the market. This technology is used for manufacturing high-strength parts, often used in vehicle panels and structural applications.

- 3D Printing accounts for 15.00% of the market. 3D printing is increasingly used for producing custom parts, prototypes, and components in electric vehicle development due to its precision and flexibility.

End-Use Component Function Insights

The Structural Plastics Segment Dominated the Electric Vehicle Plastics Market with 32% of Market Share in 2025

The Structural plastics segment dominated the electric vehicle plastics market with 32% share in 2025, driven by its mechanical endurance and its role in automotive lightweighting, which uses high-performance composites to ensure structural integrity and crashworthiness. The segment is a key tool for battery enclosure advancement, which provides safety and enables radical part consolidation, aligning with advancing circular economy goals.

The Insulation plastics segment held the second largest share of 26% in 2025, driven by demand for electrical safety and thermal management in electric vehicles. The insulation plastics provide dielectric strength, heat resistance, and chemical reliability to protect wiring harnesses, connectors, and busbars by preventing arching and short circuits. The segment is key for power electronics, which sets demanding performance standards.

The functional plastics segment held the third largest share of 24% in 2025 due to its specialized engineering in mission-critical operations. The segment is focused on advanced material science to enable smart surfaces and HMI components. Additionally, the segment provides electromagnetic interference shielding and fluid handling for intricate manifolds, which is essential for modern electrification.

The Decorative plastics segment held the fourth largest share of 18% in 2025 due to its advanced surface finishing and rising demand for sustainable luxury. The segment utilized high-performance resin to create ultralight backlit dashboards, an advanced roof system and minimalist door trims. The segment leads in the adoption of bio-based content with HMI integration for smart surfaces with superior scratch resistance and UV stability.

Electric Vehicle Plastics Market Share, By End-Use Component Function, 2025 (%)

| By End-Use Component Function | Revenue Share, 2025 (%) |

| Structural Plastics | 32.00% |

| Insulation Plastics | 26.00% |

| Decorative Plastics | 18.00% |

| Functional Plastics | 24.00% |

- Structural Plastics lead the market with a share of 32.00%. These plastics are essential for the construction of the vehicle’s frame and body, offering strength and reducing overall weight.

- Insulation Plastics account for 26.00% of the market. Used primarily for electrical and battery insulation, these plastics enhance the safety and performance of electric vehicles by preventing electrical failures.

- Decorative Plastics hold 18.00% of the market. These plastics are used in vehicle interiors and exteriors for aesthetic purposes, including trim, dashboard components, and exterior panels.

- Functional Plastics make up 24.00% of the market. These plastics serve specific functions, such as components for thermal management, seals, and other performance-related parts in electric vehicles.

Regional Insights

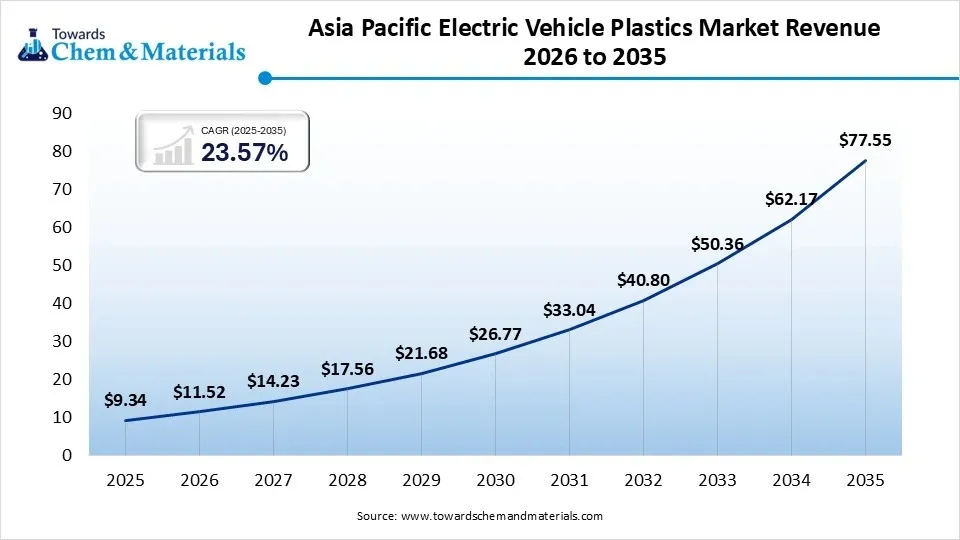

The Asia Pacific electric vehicle plastics market size was valued at USD 9.34 billion in 2025 and is expected to be worth around USD 77.55 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 23.57% over the forecast period from 2026 to 2035.Asia Pacific dominated the electric vehicle plastics market with 48% share in 2025, representing the key manufacturing and innovation hub, driven by a robust supply chain and stringent government electrification mandates. The region consumes high- performance plastics like PP, PA, and PC for EVs and two-wheelers. The domestic players pioneering flame- retardant and thermal management systems, which are pushing the region towards innovation. Additionally, the region emphasises sustainability by integrating recycled content and biopolymers, shaping a low- carbon future.

China Electric Vehicle Plastics Market Growth Trends

China's market is the global leader in electrification, fueled by its new energy vehicle output and integrated domestic supply chain. The region focuses on high-performance plastics for lightweighting and battery energy density. The region is leading advanced engineering resins and shifting towards advancing recycling and bio- based materials in batteries, dashboards, and aerodynamic parts, supported by a strategic partnership.

Europe expects the fastest growth with 22% market share during the forecast period, because the region focuses on sustainability, carbon neutrality and a circular economy. The region is developing in lightweighting to maximise battery range while meeting strict recycled content rules and low-carbon standards. Additionally, Europe also leads in high- voltage safety with flame- retardant polymers and thermal systems for premium EVs and buses that boosting the regional expansion.

")

Germany Electric Vehicle Plastics Market Growth Trends

Germany market represents the technology-driven laboratory infrastructure and is an electrified leader in advanced polymer science. The region developed high-performance resins for lightweighting and the safety of EVs. The regional player integrating recycled and bio-based plastics in battery enclosures and cockpits is driving the domestic growth. Overall, Germany sets global standards for flame retardancy and crashworthiness in passenger EVs and buses.

Electric Vehicle Plastics Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 48.00% |

| Europe | 24.00% |

| North America | 18.00% |

| Latin America | 6.00% |

| Middle East & Africa | 4.00% |

- Asia-Pacific holds the largest share of the market, contributing 48.00% to the global revenue, driven by the region's rapid adoption of electric vehicles and a strong manufacturing base.

- Europe accounts for 24.00% of the market share, supported by stringent environmental regulations and significant investments in electric vehicle infrastructure.

- North America represents 18.00% of the market, fueled by growing demand for electric vehicles in countries like the United States and Canada, along with increasing governmental incentives.

- Latin America contributes 6.00% of the market share, with expanding electric vehicle initiatives and infrastructure development, though it remains a smaller market compared to other regions.

- Middle East & Africa holds the smallest share of the market at 4.00%, reflecting a relatively slower adoption of electric vehicles in these regions, though interest is gradually growing due to sustainability efforts.

Recent Developments

- In January 2026, ProLogium and Darfon Energy Tech announced a strategic collaboration at CES 2026, which focuses on launching solid-state battery solutions precisely for light electric vehicles and e-bikes. The partnership addresses the demand for performance efficiency, safety and improvement in user experience. (Source: prologium.com)

- In October 2025, Mitsui Chemicals and Polyplastics, a subsidiary of Daicel Corporation, announced a strategic agreement for marketing operations for engineered plastics, specifically ARLEN® and AURUM® brands. The partnership aimed at enhancing the Polyplastics customer network in the electrical and automotive sectors.(Source: www.daicel.com)

Top Companies in the Market and Their Offerings

- Asahi Kasei Corporation

- BASF SE

- Borealis GmbH

- Celanese Corporation

- Covestro AG

- DuPont

- Envalior (DSM Engineering Materials)

- Evonik Industries AG

- Huntsman International LLC

- INEOS AG

- LANXESS

- LG Chem

- LyondellBasell Industries

- Röhm GmbH

- RTP Company

- SABIC

- Solvay

- TORAY INDUSTRIES, INC.

Segment Covered in the Report

By Polymer Type

- Polypropylene (PP)

- Homopolymer PP

- Copolymer PP

- Polyurethane (PU)

- Flexible PU Foam

- Rigid PU Foam

- Polyamide (PA)

- PA6

- PA66

- Polyvinyl Chloride (PVC)

- Flexible PVC

- Rigid PVC

- Acrylonitrile Butadiene Styrene (ABS)

- Polycarbonate (PC)

- PC Blends

- Polyethylene (PE)

- HDPE

- LDPE

- Others

- PBT

- PET

- PPS

By Application

- Interior Components

- Dashboard

- Seats

- Door Panels

- Cabin Linings

- Exterior Components

- Bumpers

- Grilles

- Body Panels

- Under-the-Hood Components

- Engine Covers

- Fluid Reservoirs

- Battery Components

- Battery Housing

- Battery Insulation

- Thermal Management Parts

- Electrical Components

- Connectors

- Wiring Insulation

- Structural Components

- Lightweight Frames

- Reinforcement Parts

By Vehicle Type

- Passenger Electric Vehicles

- Hatchbacks

- Sedans

- SUVs

- Commercial Electric Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric Two-Wheelers

- Electric Buses

By Processing Technology

- Injection Molding

- Blow Molding

- Thermoforming

- Extrusion

- Compression Molding

- 3D Printing/Additive Manufacturing

By End-Use Component Function

- Structural Plastics

- Insulation Plastics

- Electrical Insulation

- Thermal Insulation

- Decorative Plastics

- Functional Plastics

- Flame Retardant Plastics

- Conductive Plastics

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)