Content

What is the Polystyrene Market Size and Share?

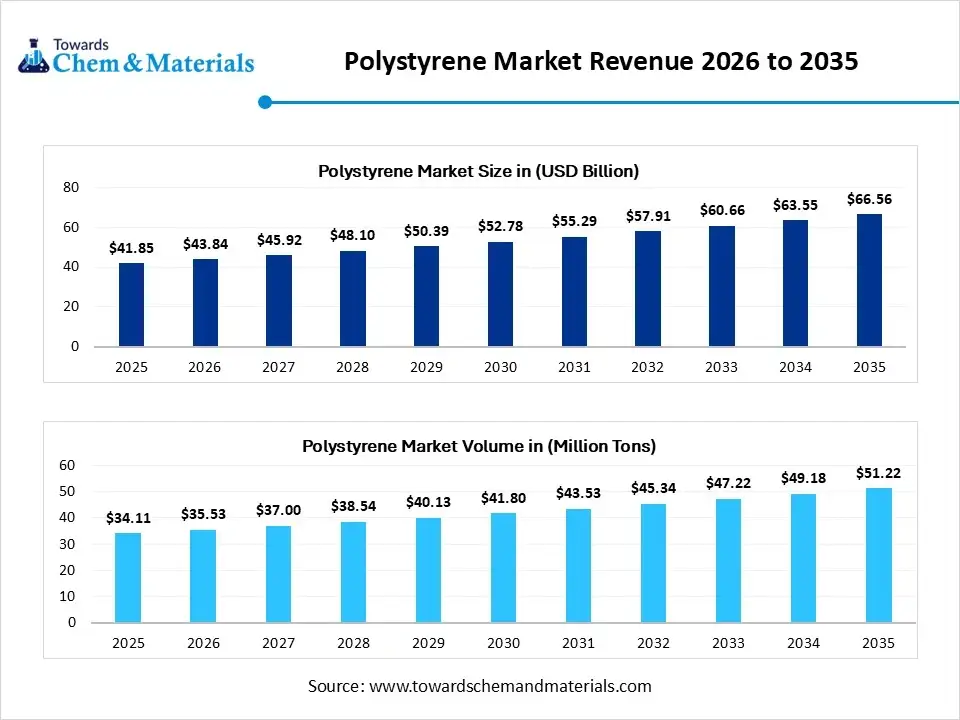

The global polystyrene market size was valued at USD 41.85 billion in 2025, is estimated to reach USD 43.84 billion in 2026, and is projected to reach USD 66.56 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 4.75% over the forecast period from 2026 to 2035. Asia Pacific dominated the polystyrene market with the largest revenue share of 39% in 2025 and is expected to grow at the fastest CAGR of 4.88% during the forecast period. In terms of volume, the polystyrene industry is projected to grow from 34.11 million tons in 2025 to 51.22 million tons by 2035. growing at a CAGR of 4.15% from 2026 to 2035. The market growth is driven by demand for packaging, which keeps going up; construction is expanding too; consumer goods production is rising; insulation use is getting bigger; and industrial manufacturing grows.

The polystyrene market is basically about making, refining, and selling versatile thermoplastic polymers, which are used everywhere from packaging and construction to electronics, healthcare, and everyday consumer items. People like polystyrene because it is lightweight, it tends to be cost-efficient, it performs well as an insulator, it handles impact fairly well, and it molds easily into complicated shapes. A lot of the market movement comes from packaging needs that keep getting bigger, more building work happening, more appliance manufacturing, and also more demand for protective supplies in logistics.

Within that market, high-impact polystyrene (HIPS), expandable polystyrene (EPS), and general-purpose polystyrene (GPPS) are still broadly chosen for industrial use, and they show up in many product categories. At the same time, new recycling technologies, more sustainable material concepts, and better manufacturing techniques are quietly changing how the industry behaves, day to day. On top of that, rules focusing on waste reduction and circular economy routines are pushing producers to consider polystyrene options that are recyclable and chemically recycled, which sounds kind of fancy, but the idea is pretty practical.

Market Highlights

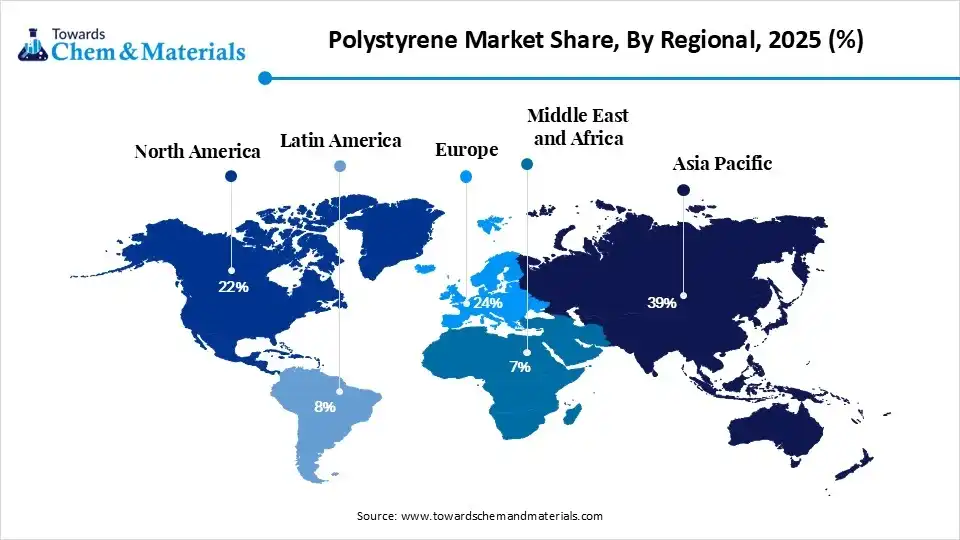

- By region, Asia Pacific dominated the polystyrene market by holding 39% share in 2025 and is expected to grow at the fastest, with a CAGR of 6.10% during the forecast period, as urbanization increases construction insulation material consumption.

- By region, Europe held the 24% market share in 2025, driven by circular economy initiatives which encourage advanced recycling technologies.

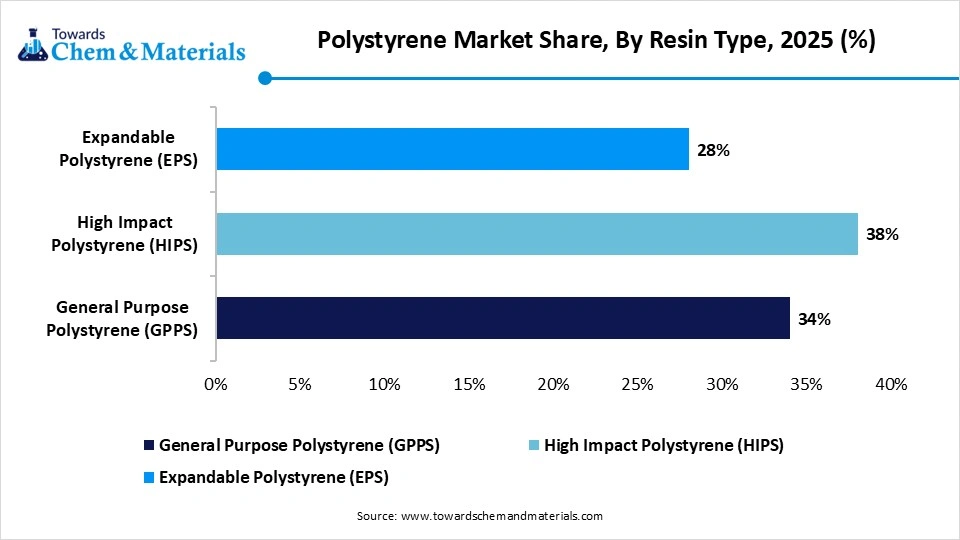

- By resin type, the high impact polystyrene (HIPS) segment dominated the market with the largest share of 38% in 2025, driven by automotive interior applications.

- By resin type, the expandable polystyrene (EPS) segment held 28% market share in 2025 and is expected to grow at the fastest CAGR of 5.6% over the forecast period as E-commerce packaging increases protective foam application growth.

- By form type, the foams segment dominated the market with the largest share of 47% in 2025, and is expected to grow at the fastest CAGR of 5.50% over the forecast period, driven by thermal insulation applications.

- By end-use, the packaging segment dominated the market with the largest share of 42% in 2025 as food packaging and e-commerce sectors increase polystyrene consumption.

- By end-use, the building & construction segment held 26% market share in 2025 and is expected to grow at the fastest CAGR of 5.7% over the forecast period due to infrastructure development expanding EPS construction applications globally.

Lightweight and Insulated: The Rise of Polystyrene in Modern Industries

The polystyrene market is expected to seen in rapid growth owing to its widespread application in industries such as packaging, construction, and consumer electronics in the current period. Moreover, the demand for lightweight, molding, and insulation is severely contributing to the industry's growth in recent years. Also, these properties make polystyrene a preferred material across the heavy industries. Moreover, the expansion of construction projects has led to a major consumer base for the industry in the past few years, as construction developers are increasingly using polystyrene in their activities. Also, the rising environmental concerns are leading to the development of bio-based alternatives and encouraging the use of recycled plastic in the current period, as per observation.

Market Trends

- Sustainability and Chemical Recycling Revolution:Single-use plastics are becoming increasingly restricted, and investments are being made in emerging chemical recycling technologies. New developments by manufacturers are making post-consumer polystyrene waste into high-purity recycled feedstock for food use and industrial applications. The adoption of closed-loop recycling systems keeps growing worldwide due to circular economy programs, sustainability policies, and regulatory regulations.

- Packaging Innovation Driving Material Demand:Polystyrene is still a good choice for high-end packaging applications because of its clarity, lightness, and flexibility. Brands are increasingly making use of GPPS in cosmetic packages, food package and retail products. The market for packaging is continuing to grow in consumer markets due to the need for attractive, highly functional, and affordable packaging.

- Building Insulation Expansion:New energy efficiency codes are driving the use of EPS and XPS insulation materials. To enhance the thermal performance, energy efficiency, and sustainability of a building, construction companies are using polystyrene insulation products. Demand for high-quality insulating materials persists and is being fueled by an increasing number of residential, commercial, and infrastructure projects throughout the world.

- Rising Adoption of High-Impact Polystyrene:High Impact Polystyrene is seeing some growth in electronics, appliances, and automotive applications. HIPS is used in manufacturing because it is easier to process, has a higher impact resistance, and is more durable. Demand for specialized HIPS grades continues to grow, particularly in the Middle East and Asia, due to continued growth in automotive light-weighting, consumer electronics production, and household appliances.

Market Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 43.84 Billion/ 35.53 Million Tons |

| Revenue Forecast in 2035 | USD 66.56 Billion/ 51.22 Million Tons |

| Growth Rate | CAGR 4.75% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Resin Type, By Form Type, By End-Use, By Regions |

| Key Companies Profiled | KUMHO PETROCHEMICAL, Atlas Molded Products, Innova, Alpek S.A.B. de C.V., Americas Styrenics LLC (AmSty), Versalis SpA, SABIC, BASF SE, Total, CHIMEI, Formosa Chemicals & Fibre Corp., INEOS Styrolution Group GmbH, LG Chem, Synthos, Trinseo |

Key Technological Shifts and AI in the Polystyrene Market

Technological progress is transforming polystyrene manufacturing, via automation, newer polymerization approaches, and also more sustainable recycling ideas that actually stick. AI-driven production setups help dial in temperature control, better use of catalysts, and overall process efficiency. Because of that, the output stays more consistent, and the operational costs drop. Then, machine learning systems go further by forecasting equipment maintenance, so downtime is minimized, usually without too much drama. There are also digital quality-check arrangements that lean on computer vision to spot imperfections and keep the material performance bar in place.

Supply Chain Analysis of the Polystyrene Market

- Feedstock Procurement: Getting benzene, ethylene, and other petrochemical derivatives used in the production of styrene monomer at a stable price and quality.

- Key Players: Shell, Saudi Aramco, ExxonMobil

- Chemical Synthesis and Processing:The raw polystyrene resin having desired physical and chemical properties is obtained by catalytic polymerization of styrene monomers.

- Key players: INEOS Styrolution, TotalEnergies, Trinseo

- Quality Testing and Certification of Polystyrene: Once made, materials are subject to thermal/mechanical/safety testing to ensure they meet regulatory requirements and are ready for sale.

- Key Players: SGS, Intertek, TÜV SÜD

Regulatory Framework: Polystyrene Market

| Region | Key Regulation | Regulatory Focus |

| Asia Pacific | Plastic Waste Management Amendment | focus on transitioning to a circular economy through centralized online reporting, mandatory recycled content usage, and flexible credit trading. |

| North America | Farewell to Foam Act | seeks to phase out the nationwide sale and distribution of expanded polystyrene (EPS) or "Styrofoam" |

| European Union | Packaging and Packaging Waste Regulation (PPWR) | designed to slash packaging waste, boost circularity, and harmonize standards across the European Union. |

Market Dynamics

Drivers

Expanding Construction and Insulation Applications

Over the years, the demand for polystyrene-based insulation materials has been rising rapidly, especially in the developed world, due to rapid urbanization, modernization of infrastructure, and the rising rate of residential construction activities. For energy-efficient buildings, Expanded Polystyrene (EPS) and Extruded Polystyrene (XPS) are both excellent, as they offer good thermal insulation, moisture protection, and durability. As energy-saving standards become more stringent and the government increases its support for green-building initiatives, the use of cutting-edge insulation solutions is being reinforced.

The growth of the packaging, electronics, and automotive industries

Weak demand for heavy-duty protective packages is fueled by the growth of e-commerce, food delivery, and consumer goods markets. But the high rigidity and transparency of polystyrene, combined with its design flexibility makes it a popular material in electronics and the automotive industry. Continued growth in appliance production, electronic devices, and light vehicle components continues to stimulate growth, regionally and around the world.

Restraints

Strict Environmental Rules and Plastic Bans

The emergence of environmental issues with plastic waste and marine pollution has led to the introduction of more stringent laws on polystyrene products. Single-use plastic bans, restrictions on foam packaging, and EPR requirements make compliance more expensive for manufacturers. This new pressure is driving companies to shift to other materials and to invest heavily in sustainable product development projects.

Waste management and price volatility of feedstocks

The production of polystyrene is highly sensitive to changes in prices for crude oil, the source of styrene monomer. Volatile raw material costs affect profitability and operating decisions. Moreover, poor recycling facilities, low recovery rates, and the growing public awareness of plastic pollution remain major problems throughout the value chain.

Opportunities

Chemical Recycling and Circular Economy Development

New technologies are emerging to advance chemical recycling with the ability to produce virgin monomer quality PS. These innovations help to achieve the goals of the circular economy and to minimise the amount of waste that is sent to landfill and resources that are used. The rising importance of sustainability regulations and the growing corporate commitment to sustainability are spurring significant investments in recycling plants and closed-loop manufacturing processes.

Bio-Based Materials and Advanced Insulation Solutions

New opportunities for growth through research and development of bio-based polystyrene alternatives, low-emission blowing agents, and insulation products with graphite. The advanced formulations enhance the thermal performance, energy efficiency, and environmental sustainability. Commercialization of next-generation polystyrene technologies is gaining momentum as a result of increased demand for premium construction materials and sustainable packaging products in the various sectors.

Segmental Insights

Resin Type Insights

The high impact polystyrene (HIPS) segment dominated the market with the largest share of 38% in 2025, as it possessed the best impact resistance, durability, and processing flexibility. Widespread adoption is maintained by strong demand from consumer electronics, appliance, and automotive interior end-users. Its continued use in flame-retardant and high gloss grades continues to make a strong impression in industrial and commercial applications.

")

The expandable polystyrene (EPS) segment held the 28% market share in 2025 and is expected to grow at the fastest CAGR of 5.6% over the forecast period, thanks to the growing demand for thermal insulation and protective packaging applications. The use of EPS in the construction sector is being fostered for energy-efficient buildings, and the e-commerce sector is growing, increasing packaging consumption. The lightweight nature, its insulation, and cost-effectiveness are driving it to be used in a range of end-use sectors.

The general purpose polystyrene (GPPS) segment held 34% market share in 2025. General-purpose Polystyrene (GPPS) is still a valuable product for its transparency, rigidity, and processability. It is widely used in food packaging, consumer goods, and disposable products. Attractive packaging solutions and cost-efficient manufacturing processes are still driving consumption across a number of industries globally.

Polystyrene Market Share, By Resin Type, 2025 (%)

| By Resin Type | Revenue Share, 2025 (%) |

| General Purpose Polystyrene (GPPS) | 34% |

| High Impact Polystyrene (HIPS) | 38% |

| Expandable Polystyrene (EPS) | 28% |

Form Type Insights

The foams segment dominated the market with the largest share of 47% in 2025 and is expected to grow at the fastest CAGR of 5.50% over the forecast period, as the foams are used in various sectors such as insulation, protective packaging, and food-service applications. Growing construction activities and increasing demand for energy-efficient materials continue to boost foam consumption. With the e-commerce & food delivery industry growing, the demand for durable & lightweight foam packaging solutions continues to be accelerated.

The films & sheets segment held the 24% market share in 2025. Transparent sheets are very popular in food packaging, retail packaging, and thermoformed products. They offer a cost-effective solution to the manufacture of packages that are lightweight and durable, and that are visually appealing.

The injection molding segment held 21% market share in 2025, due to the increased demand for precision-molded plastic components in electronics, appliances, and consumer goods sectors. Molded products have high dimensional stability and processing efficiency when using polystyrene. The ongoing rise of lightweight components for industry and consumer applications is continuing to drive the expansion of injection molding throughout the world.

The other form types segment held 8% market share in 2025. Extruded profiles and specialty shapes are used in special industrial and construction applications. Decorative building materials, custom product design, and special industrial applications prop up demand. Stable growth opportunities for these specialized polystyrene forms are achieved through the continuous innovation of the product and diversification across the end-use sectors.

Polystyrene Market Share, By Form Type, 2025 (%)

| By Form Type | Revenue Share, 2025 (%) |

| Foams | 47% |

| Films & Sheets | 24% |

| Injection Molding | 21% |

| Other Form Types | 8% |

End-Use Insights

Packaging Dominated the Polystyrene Market with 42% of Market Share in 2025

The packaging segment dominated the market with the largest share of 42% in 2025, as it was used in food containers, packaging protection, and transportation applications in the industrial sector. Polystyrene provides lightweight protection, cost-effectiveness, and flexibility in design. The demand for safe product transportation, the growth of food delivery services, and the expansion of e-commerce activities are other factors that are contributing to the growth of the packaging sector.

The building & construction segment held the 26% market share in 2025 and is expected to grow at the fastest CAGR of 5.7% over the forecast period. The growing demand for thermal insulation materials is fueling the growth of the building and construction market. Insulation products made of polystyrene offer increased building performance, lower operating costs, and greater energy efficiency. The extensive growth of infrastructure, urbanization, and the increasingly stringent energy conservation standards are still contributing to the spread of use in the construction sector.

The electrical & electronics segment held 15% market share in 2025, driven by increased production of consumer electronics, electrical components, and appliances. Electronic housings and appliance parts demand durability, thermal insulation, and flexibility in the manufacturing process, which is being met by polystyrene. The demand for specialized polystyrene materials is still growing due to the advancement of technology and the increasing usage of electronics.

The consumer goods segment held 12% market share in 2025. Polystyrene is widely used in the consumer goods sector for packaging in household products, toys, personal care items, and lifestyle accessories. The low cost and lightweight properties of the material make it preferred by manufacturers, along with its design flexibility. Market growth is further driven by consumers' continued increased spending and a higher demand for convenient everyday products.

Polystyrene Market Share, By End-Use, 2025 (%)

| By End-Use | Revenue Share, 2025 (%) |

| Packaging | 42% |

| Building & Construction | 26% |

| Electrical & Electronics | 15% |

| Consumer Goods | 12% |

| Other End-use Industries | 5% |

Regional Insights

How Did The Asia Pacific Dominate The Polystyrene Market In 2025?

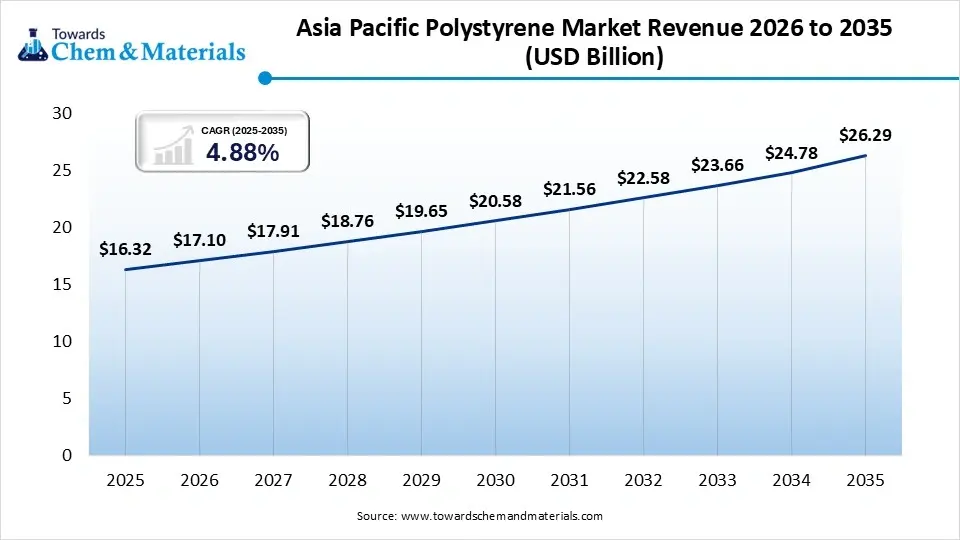

The Asia Pacific polystyrene market size was estimated at USD 16.32 billion in 2025 and is projected to reach USD 26.29 billion by 2035, growing at a CAGR of 4.88% from 2026 to 2035.Asia Pacific dominated the market by holding 39% share in 2025 and is expected to grow at the fastest with a CAGR of 6.10% during the forecast period, driven by rapid industrialization, urbanization, and growing manufacturing. Demand is continuing to be helped by growth in the packaging, electronics, and construction industries. The regional market leadership is further bolstered by the growing share of e-commerce, infrastructure investments, and growing consumer product manufacturing.

China

- HIPS, GPPS, and EPS are used in consumer and industrial applications, and the demand for them is expected to rise due to their strong electronics manufacturing ecosystem.

- In residential and commercial buildings, the increasing pace of urbanization and expansion of infrastructure increases the demand for insulation materials.

- Logistics and transportation of goods are driving logistics packaging requirements that depend on protective packaging.

- Expansion of advanced manufacturing in the U.S. bolsters domestic production and processing of polystyrene.

India

- Growth in the packaging industry leads to a growing market for GPPS and EPS products across the country.

- The rising demand for lightweight packaging materials due to the growth of the food delivery and retail industry.

- The development of infrastructure allows the spreading of thermal insulation solutions in buildings.

- As appliance and electronics production continues to increase, so will the demand for impact-resistant grades of polystyrene.

The Europe polystyrene market size was estimated at USD 10.04 billion in 2025 and is projected to reach USD 16.31 billion by 2035, growing at a CAGR of 4.97% from 2026 to 2035.Europe held the 24% market share in 2025. The energy-efficient construction, advanced packaging industries, and the sustainability efforts help keep Europe at the top of market growth. The strict environmental laws stimulate recycling innovation and promote the use of the circular economy. The building sector is growing due to the increasing demand for insulation materials and sustainable packaging solutions, which in turn is responsible for the continued consumption of polystyrene products in the region.

Germany

- Demand for durable HIPS applications is driven by strong automotive and electronics industries.

- The new energy-efficient building codes drive increased use of EPS insulation materials.

- Advanced recycling technologies help to foster sustainable polystyrene production and use.

- Development of high-performance and specialty polystyrene formulations is stimulated by industrial innovation.

France

- The growing demand for transparent and lightweight GPPS products continues with the growth of the food packaging industry.

- Circular economy projects promote the use of recycled and recyclable polystyrene products.

- As more homes are renovated, more insulation goes into the homes.

- As consumer demand for sustainable packaging grows, so does market innovation and growth.

The North America polystyrene market size was estimated at USD 9.21 billion in 2025 and is projected to reach USD 14.98 billion by 2035, growing at a CAGR of 4.98% from 2026 to 2035.North America held 22% market share in 2025, owing to its packaging industry, appliance manufacturing industry, and construction industry. Developing markets with recycling infrastructure and sustainable material technologies. Insulating materials, protective packaging, and industrial applications continued to be in demand due to technological advancement and the growing environmental compliance programmes.

United States

- Food packaging and consumer goods are the other areas that have high demand for PS products.

- Increased chemical recycling investments enhance sustainability and material recovery.

- The growing construction activity promotes the use of insulation-grade EPS for infrastructure projects.

- The high-tech manufacturing allows for the development of specialty and high-performance polystyrene materials.

Canada

- As the energy-efficiency requirements are raised, more and more people are now using polystyrene insulation materials in their buildings.

- As the cold-chain logistics industry continues to expand, the demand for temperature-controlled packaging grows.

- Recycling facilities investments reinforce the circular economy efforts in the plastics sector.

Growing demand for consumer goods drives the growth of GPPS and HIPS material demand.

")

The Latin America polystyrene market size was estimated at USD 3.35 billion in 2025 and is projected to reach USD 5.66 billion by 2035, growing at a CAGR of 5.38% from 2026 to 2035.Latin America held 8% market share in 2025. Latin America is growing steadily, with food packaging, consumer goods production, and infrastructure growth, among others, driving growth. As the urban population grows and industrialization increases, the demand for polystyrene products grows. Retail logistics and transport infrastructure, and construction and engineering projects, are improving to offer an environment of opportunity throughout the region.

Brazil

- The expansion of the food processing and food packaging industries leads to higher local polystyrene demand.

- Insulation-grade EPS products are being used to meet growing demand in infrastructure development projects.

- The increase in demand for insulation-grade EPS products is met by infrastructure development projects.

- Growth of retail and e-commerce activities intensifies protective packaging needs.

- Specialty polystyrene applications will be created with industrial diversification.

Chile

- With increasing investments in construction, the demand for energy-efficient insulating materials increases.

- The more logistics are expanded, the more lightweight protective packaging products are needed.

- Resin demand is steady and is being fueled by growth in consumer goods manufacturing.

- Strategies aimed at sustainability promote the use of advanced recycling and waste management.

The Middle East & Africa polystyrene market size was estimated at USD 2.93 billion in 2025 and is projected to reach USD 4.99 billion by 2035, growing at a CAGR of 5.47% from 2026 to 2035.The Middle East & Africa held 7% market share in 2025, driven by the growth in infrastructure projects, industrial diversification, and the production of consumer products. Demand for insulation materials is rising with the increase in construction activities and steadily increasing with packaging applications. Economic development programs and industrial investments promote widespread use of polystyrene in various fields.

Polystyrene Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 22% |

| Europe | 24% |

| Asia-Pacific | 39% |

| Latin America | 8% |

| Middle East & Africa | 7% |

Saudi Arabia

- The demand for insulation materials is high in large-scale infrastructure projects and smart city projects.

- Industrial diversification strategies help to support growth in the packaging and manufacturing industries.

- An increase in the retail industry increases the use of protective packaging materials.

- Expansion of the petrochemical sector enhances the supply of raw materials.

South Africa

- The growth of the construction sector is helping to drive EPS insulation in commercial projects.

- Consumer goods production grows, which leads to an increase in the demand for GPPS and HIPS materials.

- The relatively new food packaging industry is pushing the use of lightweight solutions.

- Increased use of advanced polymer products through industrial modernization programs.

Recent Developments

- In February 2026, UpSolv, a Canadian company, launched its first polystyrene resins via physical recycling of styrenic waste, with FDA-approved processes. Successful trials on rigid polystyrene, EPS, and XPS are now producing made-to-spec batches in Montreal.(Source: www.globalinsulation.com)

- In February 2026, BEWI launched Norway's first expanded polystyrene (EPS) recycling facility in Fredrikstad, allowing local collection, processing, and reuse of recycled EPS in insulation production. This integration supports the rising demand for recycled-content insulation and complies with regulatory trends in the construction and packaging industries. (Source: www.recycling-magazine.com)

Top Companies list

- KUMHO PETROCHEMICAL

- Atlas Molded Products

- Innova

- Alpek S.A.B. de C.V.

- Americas Styrenics LLC (AmSty)

- Versalis SpA

- SABIC

- BASF SE

- Total

- CHIMEI

- Formosa Chemicals & Fibre Corp.

- INEOS Styrolution Group GmbH

- LG Chem

- Synthos

- Trinseo

Segment Covered in the Report

By Resin Type

- General Purpose Polystyrene (GPPS)

- Extrusion Grade GPPS

- Injection Molding Grade GPPS

- Optical Grade GPPS

- High Impact Polystyrene (HIPS)

- Medium Impact HIPS

- High Gloss HIPS

- Flame Retardant HIPS

- Expandable Polystyrene (EPS)

- White EPS

- Grey EPS

- Flame Retardant EPS

By Form Type

- Foams

- Insulation Foams

- Protective Packaging Foams

- Food Service Foams

- Films & Sheets

- Thermoformed Sheets

- Transparent Films

- Laminated Sheets

- Injection Molding

- Appliance Components

- Consumer Product Casings

- Industrial Molded Parts

- Other Form Types

- Extruded Profiles

- Decorative Components

- Specialty Shapes

By End-Use

- Packaging

- Food Packaging

- Protective Packaging

- Industrial Packaging

- Building & Construction

- Thermal Insulation

- Roofing Systems

- Decorative Construction Materials

- Electrical & Electronics

- Appliance Housings

- Electronic Casings

- Insulating Components

- Consumer Goods

- Household Products

- Toys

- Personal Care Packaging

- Other End-use Industries

- Healthcare

- Automotive

- Agriculture

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (7)