Content

What is Low-Density Polyethylene (LDPE) Market Size and Share?

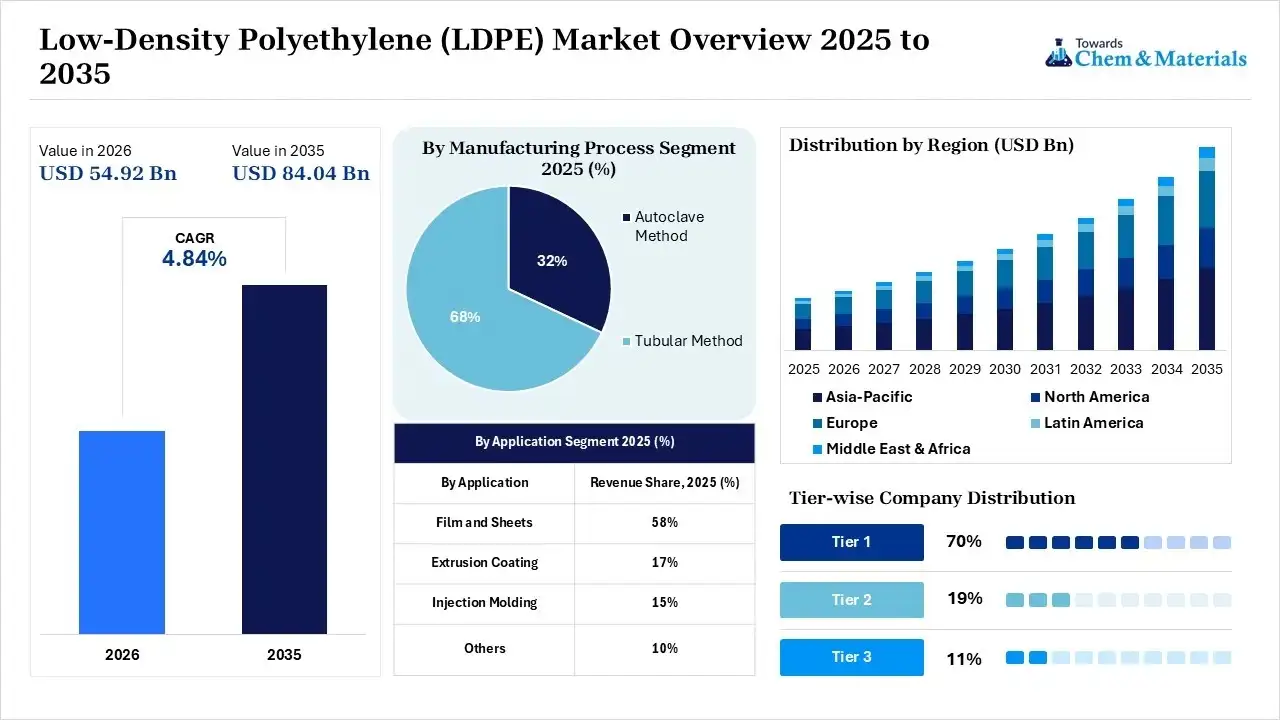

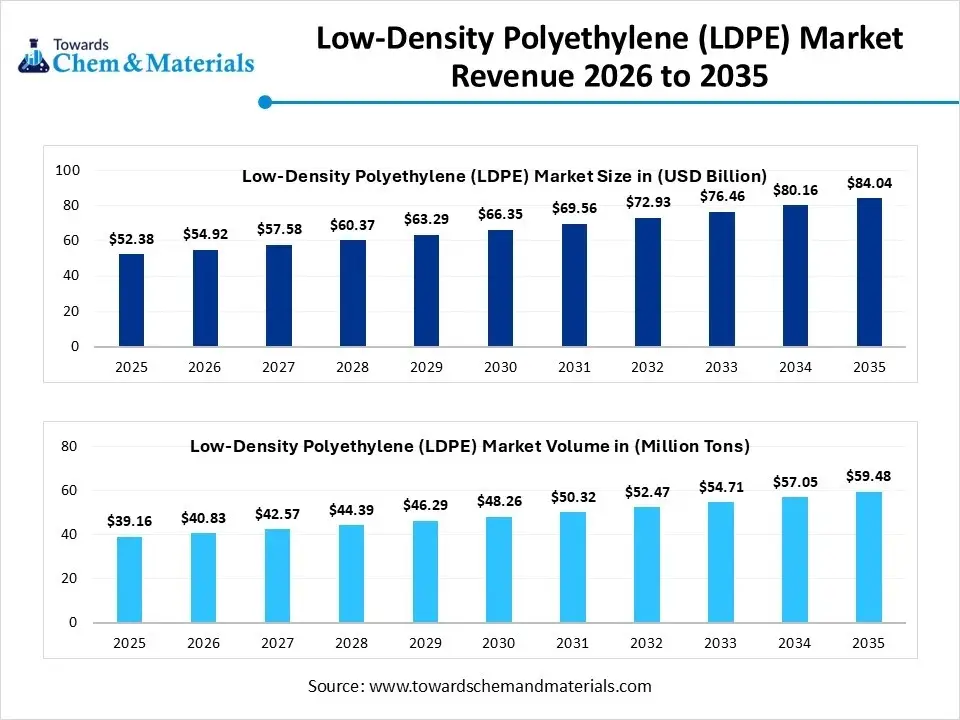

The global low-density polyethylene (LDPE) market size was valued at USD 52.38 billion in 2025, is estimated to reach USD 54.92 billion in 2026, and is projected to reach USD 84.04 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 4.84% over the forecast period from 2026 to 2035.Asia Pacific dominated the low-density polyethylene market with the largest revenue share of 46% in 2025 and is expected to grow at the fastest CAGR of 4.96% during the forecast period. In terms of volume, the low-density polyethylene market is projected to grow from 39.16 million tons in 2025 to 59.48 million tons by 2035. growing at a CAGR of 4.27% from 2026 to 2035.Food, pharmaceutical, and e-commerce are the key application areas that are driving the growth of the market. Growth in the use of these in agricultural film, medical packaging, and wire and cable insulation, as well as substantial investment in recyclable and bio-based LDPE grades, is additionally bolstering market expansion.

Market Overview")

Market Highlights

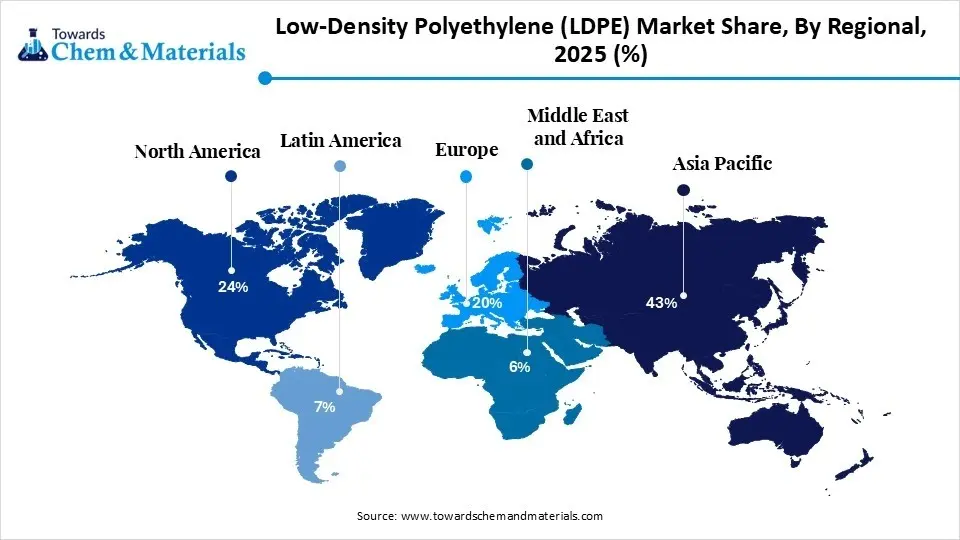

- By region, Asia Pacific dominated the market share 43% in 2025. the growth is driven by rapid industrialization, urbanization, and an increasing middle-class population.

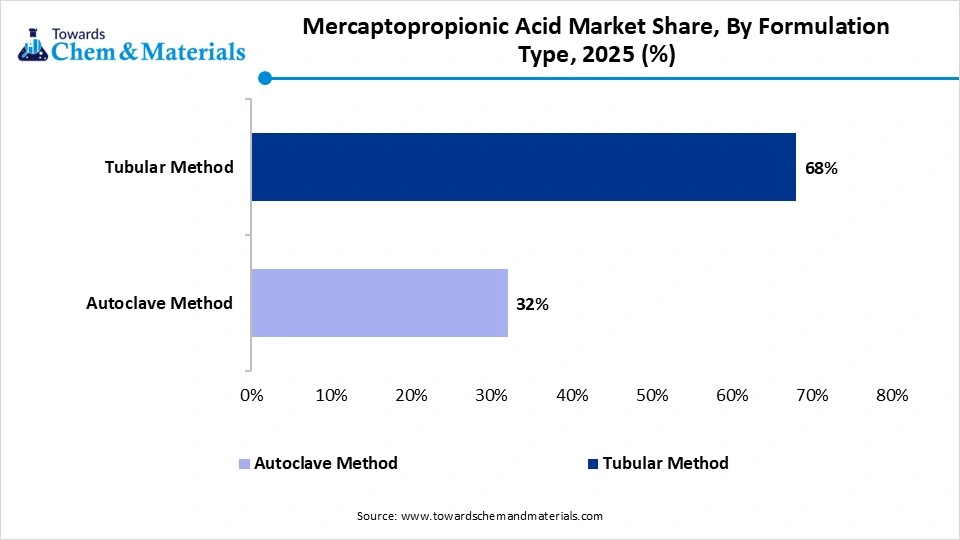

- By manufacturing process, the tabular method segment dominated the market share 68% in 2025. The increasing demand for premium-grade LDPE drives the growth.

- By application, the film and sheets segment dominated the low-density polyethylene (LDPE) market share 58% in 2025. Rising demand for sustainable and eco-friendly alternatives drives the growth of the market.

Market Revenue 2026 to 2035")

The market of Low-Density Polyethylene (LDPE) continues to grow because of its applications in flexible packaging, agricultural films, cable insulation, consumer goods, and medical applications. The expansion of e-commerce and packaged food markets has made the packaging materials lightweight, durable, and moisture-resistant. The increasing penetration of renewable energy systems, EV charging stations, and telecommunication networks is also contributing to LDPE usage in wire and cable.

In addition, sustainability initiatives are also leading the way in innovation of recyclable, chemically recycled, and bio-based LDPE grades for the goals of the circular economy. Medical packaging applications are also emerging as a lucrative growth segment due to the rising demand for sterile and high-purity packaging.

- For instance, in January 2026, Braskem released its I'm green™ bio-based LDPE grade for healthcare and hygiene packaging applications, which provides material from renewable feedstock that has a negative cradle-to-gate carbon footprint, high stiffness, and temperature resistance.(Source: www.braskem.com)

Rising Demand for Durable and Flexible Materials

Low-density polyethylene is a type of thermoplastic polymer that is made from the monomer ethylene, with having the properties like flexibility, low density, and high ductility, which results from its highly branched molecular structure. This structure gives the LDPE its characteristics, like lightweight, chemical resistance, waterproofing, and easy processing into thin films and sheets. They are commonly used in plastic bags, packaging films, containers, insulation for wires and cables, and various other consumable goods.

The drivers for the growth of the low-density polyethylene (LDPE) market are the rising demand for flexible and lightweight packaging across various industries, including food and beverage, pharmaceuticals, and consumer goods. LDPE’s excellent moisture barrier properties, durability, and ease of processing make it ideal for applications such as films, bags, and wraps.

Additionally, the rapid growth of e-commerce has increased the need for protective and adaptable packaging materials. Furthermore, the rapid urbanization and infrastructure development, especially in emerging economies, are driving the use of LDPE in construction films, insulation, and agricultural applications, further fueling market expansion.

Market Trends

- The growing demand for sustainable and recycled LDPE due to the shift towards biobased LDPE and environmental regulation has helped the market to grow.

- The surge in demand for lightweight, flexible, and moisture-resistant packaging for e-commerce, food, and pharmaceuticals drives the market's growth.

- Innovation and technological advancement in processing and manufacturing methods, like autoclave and tubular methods, improve and strengthen the process efficiency.

- Use of AI and IoT for process optimization and digitalization in supply chain management, especially in logistics, inventory, and quality control, helps the market to grow.

Market Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 54.92 Billion/ 40.83 Million Tons |

| Expected Size by 2035 | USD 84.04 Billion/ 59.48 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR is 4.84% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Manufacturing Process, By Application, By Region |

| Key Companies Profiled | Braskem, Chevron Phillips Chemical Company, INEOS, Mitsui Chemicals Inc., Formosa Plastics Corporation, Reliance Industries Limited, SABIC, Sasol, LyondellBasell Industries Holdings B.V, China Petrochemical Corporation, Shell, Petkim Petrokimya Holding A.Åž, Qatar Petrochemical Company (QAPCO) Q.P.J.S.C., Exxon Mobil Corporation, BASF SE |

Market Opportunity

The Growing Demand for Sustainable and Recyclable Packaging Solutions

One significant opportunity in the low-density polyethylene (LDPE) market is the increasing demand for sustainable and recyclable packaging materials, particularly in emerging economies. As environmental regulations tighten and consumer awareness around plastic pollution grows, companies are actively seeking eco-friendly alternatives to conventional plastics, which drives the growth of the market.

This shift creates a favorable market environment for LDPE manufacturers that can innovate with recycled or bio-based LDPE solutions. By investing in advanced recycling technologies and sustainable production methods, manufacturers can not only meet regulatory requirements but also tap into a growing segment of environmentally conscious consumers, thus gaining a competitive edge and unlocking new revenue streams.

Market Challenge

The Growing Regulatory Pressure and Ban on Single-Use Plastic

A major challenge in the low-density polyethylene (LDPE) market is the growing regulatory pressure and backlash against single-use plastics. Governments worldwide are implementing bans and restrictions on plastic bags and packaging, which are key applications for LDPE.

This has forced manufacturers to adopt recycled content, which is costly and technologically demanding which ultimately hindering the growth and is a challenge. The inconsistent recycling infrastructure is also a big limitation and challenge to overcome.

Supply Chain Analysis of the Low-Density Polyethylene (LDPE) Market

Feedstock Procurement

- The process includes the sourcing of ethylene obtained mainly from natural gas liquids and the naphtha cracking process that are used as primary raw materials for the production of LDPE. The availability, stability, and efficiency of the feedstocks are important factors in production costs and the supply of polyethylene resins to the downstream producers.

- ExxonMobil Chemical Company: A major global refiner and producer of ethylene and petrochemical feedstocks, with integrated refining and petrochemical operations to supply large-scale ethylene production for LDPE manufacturing.

- Other Key Players: LyondellBasell Industries, SABIC

Chemical synthesis and processing.

- In this step, ethylene monomers are subjected to high-pressure free-radical polymerization to give LDPE resin having a branched structure of its molecules. Advanced reactor technologies increase the efficiency of production, consistency of the product, and utilization of the energy, while allowing manufacturers to satisfy the increasing demand of the packaging, agriculture, and industrial sectors.

- Dow Inc.: One of the world's largest producers of LDPE that applies sophisticated polymerization technologies to create high-value-added LDPE grades for global applications in packaging, industrial, and specialty markets.

- Other key players: Reliance Industries Limited, Sinopec.

Compound Formulation and Blending

- It contains additives like antioxidants, UV stabilizers, slip agents, and processing aids, which improve the flexibility and durability, weather resistance, and processing performance of LDPE resin. Special formulations allow LDPE to be used in various packaging films, also in agricultural covers, medical products, and cable insulation.

- INEOS Group: Formulates specialty polyethylene products for enhanced processing characteristics and end product properties in a variety of industrial and packaging applications.

- Other Key Players: SABIC, Dow Inc.

Market Segmental Insights

Manufacturing Process Insights

The autoclave method segment dominated the low-density polyethylene (LDPE) market share 32% in 2025. The autoclave process is one of the two primary methods used to manufacture Low-Density Polyethylene (LDPE). In this process, polymerization of ethylene occurs at very high pressures and elevated temperatures around 200–300°C in a stirred high-pressure reactor, or autoclave.

The high-pressure conditions promote the formation of long-chain branching, giving LDPE its distinctive properties like softness, flexibility, high clarity, and good impact resistance. LDPE produced through the autoclave process is especially suitable for high-quality films, coatings, and pharmaceutical or food-grade packaging, where optical clarity and mechanical flexibility are crucial.

Market Share, By Manufacturing Process, 2025 (%)") While this process is more energy-intensive and costly than the tubular method, it allows for better control over molecular structure, resulting in premium-grade LDPE, which increases the demand for the segment and helps in the expansion of the market.

While this process is more energy-intensive and costly than the tubular method, it allows for better control over molecular structure, resulting in premium-grade LDPE, which increases the demand for the segment and helps in the expansion of the market.

The tubular method segment expects significant growth in the low-density polyethylene (LDPE) market during the forecast period. The tubular process is the other primary method used to produce Low-Density Polyethylene (LDPE) and differs significantly from the autoclave process.

In this method, ethylene polymerization occurs in a vertical tubular reactor at moderate pressures and high temperatures, about 200–300°C. The polymerization is initiated by a free radical catalyst, and the process occurs in a continuous flow system, where the polymer is formed and then extruded out of the reactor. The tubular process is more cost-effective and energy-efficient compared to the autoclave method, making it suitable for large-scale production of LDPE.

However, the polymer produced by this process tends to have less branching than that from the autoclave process, resulting in lower flexibility and clarity. As a result, LDPE made via the tubular process is typically used for industrial applications, such as piping, packaging films, and agricultural films, where high strength and durability are prioritized over optical properties, which drives the demand for the market in the industrial sector.

Application Insights

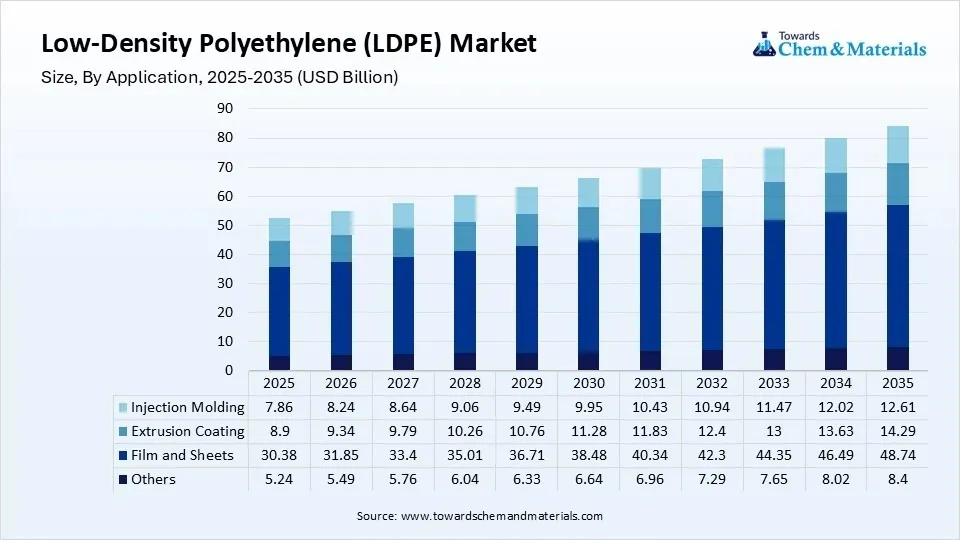

The film and sheets segment dominated the low-density polyethylene (LDPE) market share 58% in 2025. Film and sheet are the largest application segments in the market, accounting for a significant share due to LDPE’s excellent flexibility, moisture resistance, and lightweight properties. Market Size, By Application, 2025-2035 (USD Billion)")

LDPE films are widely used in packaging, including grocery bags, shrink wraps, bread bags, and food packaging films, where transparency, softness, and sealing ability are essential. In agriculture, LDPE films are used for greenhouse covers, mulch films, and silage bags, providing UV protection and preserving soil moisture.

Construction-grade sheets made from LDPE are employed as vapor barriers and protective wraps due to their chemical resistance and durability. The segment benefits from the rising demand for sustainable and recyclable packaging solutions, with manufacturers increasingly integrating recycled content into film and sheet production to meet environmental regulations and consumer expectations.

The extrusion coating segment expects significant growth in the low-density polyethylene (LDPE) market during the forecast period. Extrusion coating is a key application of Low-Density Polyethylene (LDPE), where a thin layer of LDPE is melted and applied to substrates such as paper, aluminum foil, or other plastic films to enhance their properties. This process significantly improves the moisture resistance, grease barrier, and sealability of the coated material, making it ideal for liquid packaging cartons (like milk and juice boxes), food wrappers, and paper cups.

LDPE’s good adhesion, flexibility, and clarity make it a preferred material for this process. The extrusion coating segment is experiencing steady growth, especially in the food and beverage industry, driven by the rising need for hygienic and durable packaging. Additionally, advancements in multilayer coating technologies are expanding the use of LDPE in complex packaging structures that combine multiple barrier and mechanical properties, which drives the growth of the market.

Regional Insights

How did the Asia Pacific dominate the Low-Density Polyethylene (LDPE) Market in 2025?

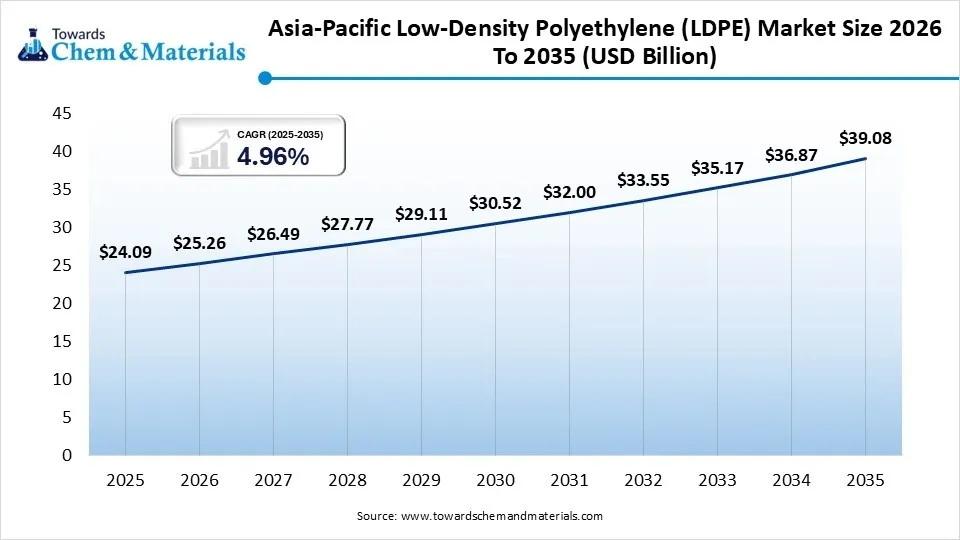

The Asia Pacific low-density polyethylene market size was estimated at USD 24.09 billion in 2025 and is projected to reach USD 39.08 billion by 2035, growing at a CAGR of 4.96% from 2026 to 2035.Asia Pacific dominated the market with 46% share in 2025, owing to its high packaging manufacturing industry, growing food processing industry, and increasing e-commerce activities. The market enjoyed the growth momentum from strong demand for flexible packaging films, agricultural covers, and consumer goods packaging. Moreover, the production capacity gains of petroleum chemicals and the rise of industrialisation in emerging economies further boosted the consumption capabilities and supply of LDPE in the region.

Market Size 2026 To 2035 (USD Billion)") China

China

- The large packaging manufacturing base resulted in high consumption of LDPE films, pouches, and protective wraps.

- The growth of e-commerce resulted in a rise in the need for lightweight mailers, courier bags, and stretch films.

- Large-scale production of competitive LDPE resins was possible through integrated petrochemical complexes for the converters.

India

- The expanding packaged food industry increased the demand for LDPE films, pouches, and flexible forms of packaging.

- The use of LDPE for greenhouse covers and mulch film applications was expanded with growing agricultural activities.

- As retail stores and e-commerce channels increased their share of the market, consumers' demand for affordable polyethylene-based packaging materials grew.

The North America low-density polyethylene market size was estimated at USD xx billion in 2025 and is projected to reach USD xx billion by 2035, growing at a CAGR of xx% from 2026 to 2035.North America held 21% market share in 2025 and is expected to grow at the fastest CAGR of 5.8% during the forecast period, with good demand in the food packaging, healthcare packaging, industrial films, and wire and cable insulation applications of LDPE. The cost-competitive ethylene production was made possible by the availability of abundant shale-gas-based ethylene feedstocks, while the rise of recycling ethylene and circular economy activities saw the growth of sustainable LDPE products in various industries.

United States

- Demand for LDPE films, wraps, and protective packaging was high in the strong food packaging industry.

- Nationwide, competitive LDPE manufacturing and steady availability of feedstocks were facilitated by the shale-based ethylene production.

- As recycling efforts increased, there was a growth in the development of circular and post-consumer recycled polyethylene grades.

Canada

- The growth of the packaging and consumer goods industries contributed to the high consumption of flexible LDPE-based materials.

- The country's polyethylene resin production and supply were reliable, with strong support from the petrochemical industry.

- The new sustainability goals led to the use of recyclable and recycled LDPE packaging solutions.

Europe held 18% market share in 2025, owing to the increasing demand for sustainable packaging materials and the regulations favouring the recovery of plastics. Demand drivers continued to be food, pharmaceutical, and industrial packaging applications. The investments in chemical recycling technology, bio-based polyethylene, and circular economy programs continued to drive innovation and further solidify the region's leadership in the development of sustainable LDPE.

Germany

- The growing demand for high-performance LDPE film and bag applications in the large packaging conversion industry.

- Regulations on the circular economy encouraged the use of polyethylene products that are made from recycled and renewable-feedstock products throughout the country.

- The demand for LDPE protective films and packaging materials was high in the industrial sector.

France

- Specialty LDPE grades had a strong impact on consumption in the food and pharmaceutical packaging markets.

- The rise of sustainable initiatives drove the use of bio-based and recyclable polyethylene packaging in the country.

- Continued growth of the market for LDPE was seen across industries owing to the increasing need for lightweight packaging materials.

Latin America held 8% market share in 2025, owing to an increase in the demand for packaged foods, agricultural films, and consumer products. The growing food processing industries and retail distribution networks led to the growing demand for flexible packaging materials. The demand for flexible packaging materials was high due to the expansion of retail distribution networks and food processing industries. The increased use of greenhouse films, mulch films, and protective films in agriculture also made a significant contribution to the consumption of LDPE in the region.

Brazil

- The flexible LDPE packaging application was in demand by the large food processing industry at the national level.

- Moisture-retaining mulch and greenhouse films increased with the expansion of the agricultural sector.

- Higher consumption of polyethylene packaging and film products was fueled by the increasing consumption of consumer goods.

Chile

- Demand for protective packaging applications and greenhouse film applications grew a great deal due to good agricultural exports.

- The continued demand for food packaging was a driver of steady demand for LDPE films and wraps.

- The adoption of polyethylene-based agricultural solutions all over the country was encouraged by the modernization of farming practices.

The Middle East & Africa held 7% market share in 2025, due to favourable support from the petrochemical manufacturing capabilities, a rise in packaging production, and agricultural activities. The market was expanding throughout the region with competitive LDPE production driven by the availability of abundant feedstock and the growing demand for flexible packaging, industrial liners, greenhouse films, and healthcare packaging applications.

Market Share, By Regional, 2025 (%)") Saudi Arabia

Saudi Arabia

- Widespread petrochemical facilities provided the world with ample supply and export potential for LDPE.

- The rising demand in demand for polyethylene films, bags, and protective wrapping materials in the growing packaging sector.

- Development projects for agriculture led to the use of LDPE greenhouse and irrigation film solutions.

South Africa

- Due to the expansion of the retail and food packaging sectors, the consumption of flexible LDPE products has risen considerably.

- Demand for polyethylene films and crop protection materials was driven by increasing agricultural activities.

- Industry packaging demands have increased the use of durable packaging solutions, based on LDPE.

Recent Developments

- In February 2026, NOVA Chemicals launched two grades of recycled polyethylene (rPE-IN3 and rPE-IN4) for non-food applications in North America. The recycled LDPE and LLDPE grades were created at the company's SYNDIGO1 mechanical recycling facility for can liners, shrink films, protective packaging, carry-out bags, and heavy-duty sacks.(Source: www.indianchemicalnews.com)

- In November 2025, Borouge introduced Bormed LE6607-PH, the first medical-grade LDPE product made in the United Arab Emirates, in November 2025. The material, which is based on Borealis' Bormed technology, was developed for pharmaceutical and medical packaging applications such as blow-fill-seal bottles, ampoules, and sterile packages for the healthcare sector.(Source: plasticstoday.com)

Top Companies List

Market Companies")

- Braskem

- Chevron Phillips Chemical Company

- INEOS

- Mitsui Chemicals, Inc.

- Formosa Plastics Corporation

- Reliance Industries Limited

- SABIC

- Sasol

- LyondellBasell Industries Holdings B.V

- China Petrochemical Corporation

- Shell

- Petkim Petrokimya Holding A.Åž

- Qatar Petrochemical Company (QAPCO) Q.P.J.S.C.

- Exxon Mobil Corporation

- BASF SE

Segments Covered in the Report

By Manufacturing Process

- Autoclave Method

- Tubular Method

By Application

- Film and Sheets

- Extrusion Coating

- Injection Molding

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (7)