Content

Green Hydrogen Market Size, Share and Trends Report 2035

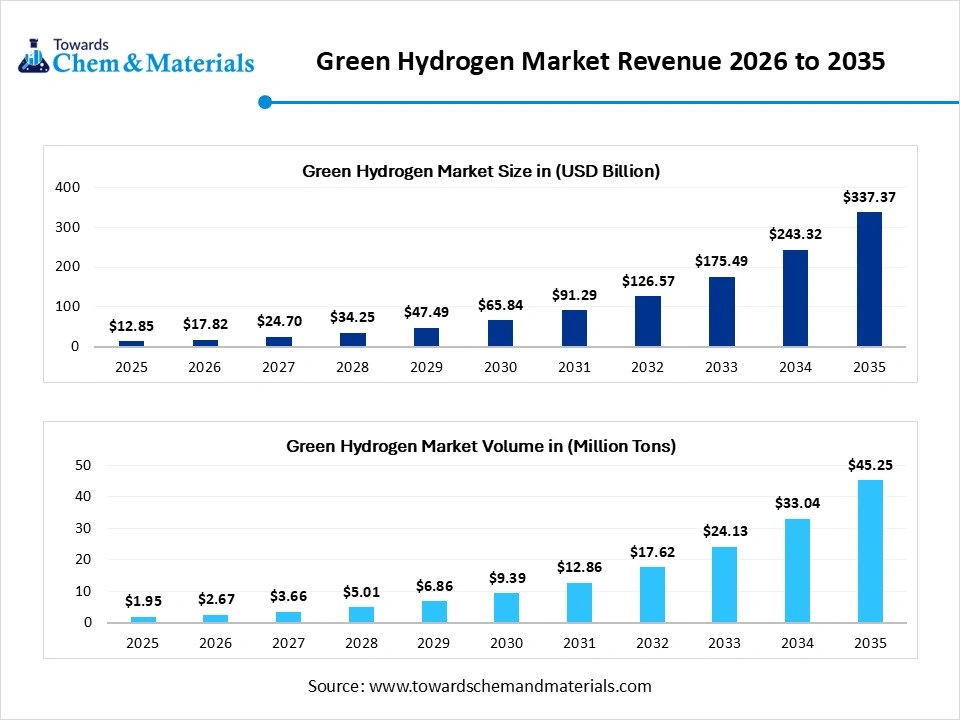

According to Towards Chemicals and Materials Analytics and Consulting, the global green hydrogen market was valued at USD 12.85 billion in 2025, is estimated to reach USD 17.82 billion in 2026, and is projected to reach USD 337.37 billion by 2035, growing at a CAGR of 38.65% from 2026 to 2035. In terms of volume, the green hydrogen market is projected to grow from 1.95 million tons in 2025 to 45.25 million tons by 2035. growing at a CAGR of 36.95% from 2026 to 2035.

Key Takeaways

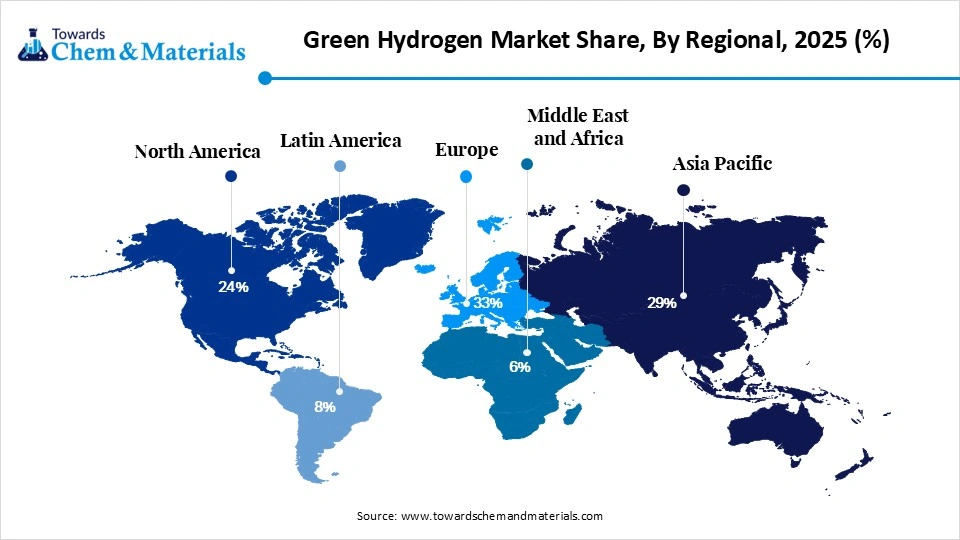

- By region, Europe dominated the green hydrogen market with 33% share in 2025.

- By region, Asia Pacific held the 29% market share in 2025 and is anticipated to have the fastest growth with a CAGR of 40.5% during the forecast period.

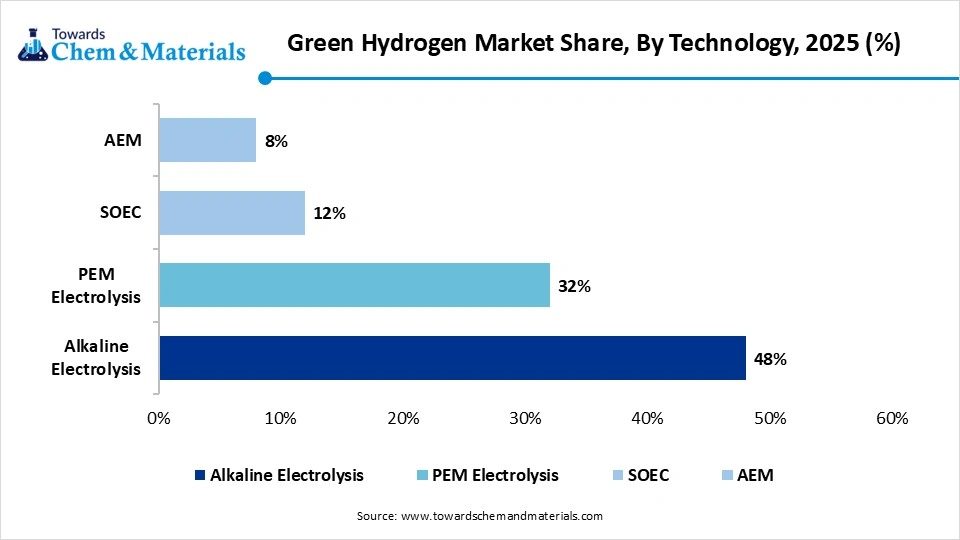

- By technology, the alkaline electrolysis segment dominated the market with 48% share in 2025.

- By technology, the PEM electrolysis segment held the 32% market share in 2025 and expects the fastest CAGR of 41.5% during the forecast period.

- By energy source, the solar energy segment dominated the market with 42% share in 2025.

- By energy source, the wind energy segment held the 33% market share in 2025 and expects the fastest CAGR of 39.2% during the forecast period.

- By application, the ammonia production segment dominated the market with 36% share in 2025.

- By application, the transportation segment held the 18% market share in 2025 and expects the fastest CAGR of 42.3% during the forecast period.

- By end-use industry, the chemicals segment dominated the market with 34% share in 2025.

- By end-use industry, the energy and utilities segment held the 20% market share in 2025 and expects the fastest CAGR of 39.6% during the forecast period.

- By distribution channel, the on-site generation segment dominated the market with 46% share in 2025 and expects the fastest CAGR of 38.7% during the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2026): USD 17.82 Billion | CAGR (2026–2035): 36.95%

- Market Projected Size (2035): USD 17.82 Billion

- Market Volume (2025): 1.95 Million Tons (MT) | Volume CAGR (2026–2035): 36.95%

- Market Projected Volume (2035): 45.25 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 3.25/kg

- Average Selling Price: USD 5.33/kg

- Pricing CAGR (2025–2035): -8.9%

Market Overview

The green hydrogen market is defined by its role as a pivotal zero-emission energy carrier in the global net-zero transition, produced via water electrolysis powered by renewable energy sources. It serves as a vital decarbonization solution for hard-to-abate sectors such as steelmaking, heavy transportation, chemicals, and fertilizers by replacing fossil-based feedstocks.

This sustainable, carbon-free energy carrier is poised for massive expansion, driven by urgent industrial decarbonization, aggressive government incentives, and plummeting renewable costs, marking a vital shift from grey to green energy solutions. By accelerating technology, the market is set to revolutionize high-emission industries and create a sustainable, scalable fuel alternative for a greener tomorrow.

Green Hydrogen Market Trends

- Demand in Industrial Decarbonization: The rising demand for green hydrogen in hard-to-abate sectors, specifically steel manufacturing (DRI), chemical production, including ammonia and methanol, and refining, makes it a critical component of net-zero strategies.

- Increasing Focus on Electrolyzer Scaling: Stringent regulatory frameworks, such as EU carbon border fees, and government incentives are accelerating the transition toward megawatt- and gigawatt-scale alkaline and PEM electrolyzer projects, flattening cost curves to compete with grey hydrogen.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 17.82 Billion / 2.67 Million Metric Tons |

| Expected Size and Volume by 2035 | USD 337.37 Billion / 45.25 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 38.65% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Europe |

| Segment Covered | By Technology, By Energy Source, By Application, By End-Use Industry, By Distribution Channel and By Region |

| Key companies profiled | Air Products and Chemicals, Inc., Linde plc, Siemens Energy AG, Air Liquide S.A., ENGIE SA, Shell plc, Nel ASA, Plug Power Inc., Uniper SE, Cummins Inc., Bloom Energy, Adani Green Energy, Reliance Industries, NTPC Limited, China Huaneng Group |

Key Technological Shifts and AI in the Green Hydrogen Market

The green hydrogen market is revolutionizing from a phase of ambitious announcements to a consolidation and industrial implementation phase, driven by significant technological advancements and AI integration. Green hydrogen technology is maturing through high-efficiency SOEC systems and flexible PEM scaling, while AEL and emerging AEM drive down costs for industrial decarbonization.

AI-driven digital twins and IoT sensors revolutionize green hydrogen by anticipating PEM/SOEC equipment failures to slash downtime, while optimizing energy coupling with renewables for maximum storage efficiency, reducing reliance on expensive noble metals like iridium.

Supply Chain Analysis of the Green Hydrogen Market

Raw Material and Energy Procurement

This stage focuses on sourcing the necessary clean electricity and materials for electrolyzer manufacturing, specifically precious metals and rare earth elements.

- Key Players: Orsted, Enel Green Power, Iberdrola, First Solar, and Johnson Matthey.

Electrolyzer Synthesis and Manufacturing

The manufacturing of technology to split water into hydrogen and oxygen. PEM and Alkaline dominate, with AEM and SOEC as emerging tech.

- Key Players: Plug Power, Thyssenkrupp Nucera, Siemens Energy, Nel ASA, John Cockerill, and Sungrow.

Hydrogen Production, Storage, and Transport

Electrolysis plants produce hydrogen, which is then conditioned for transportation, often reducing purity for advanced applications.

- Key Players: Linde Plc, Air Liquide, Air Products and Chemicals, ENGIE, and Nel ASA.

Regulatory Framework: Green Hydrogen Market

| Region | Key Regulation | Regulatory Focus |

| North America | Inflation Reduction Act (IRA) PTC, DOE Roadmaps, EPA | Focus on Production Tax Credits, cost reduction targets, and clean hydrogen hub development. |

| European Union | RED III, RFNBO Delegated Acts, CBAM, FuelEU Maritime | Binding targets for renewable hydrogen in industry, additionality rules, and strict carbon intensity thresholds. |

| Asia Pacific | China 15th FYP, METI Hydrogen Strategy, India National Mission | Focus on new quality productive forces, scaling electrolyzer manufacturing, and substituting gray hydrogen in chemical feedstock. |

| Global | ISO/TC 197, GHS, IEC Standards | Standardizing hydrogen quality, safety in transport/storage, and international certification for green hydrogen trade. |

Market Dynamics

Driver

Stringent Decarbonization Mandates and Supportive Regulatory Frameworks

Governments globally are enforcing net-zero targets and carbon pricing mechanisms, which accelerate investments in green hydrogen as a primary alternative to fossil-based feedstocks in steel, refining, and chemical sectors.

Restraints

High Production Costs and Infrastructure Bottlenecks

Despite falling costs of renewables, green hydrogen remains significantly more expensive than grey hydrogen, hindered by high initial capex for electrolyzers and a severe shortage of transport, storage, and distribution infrastructure to connect producers to end-users.

Opportunity

Industrial-Scale Energy Storage and Grid Balancing

Green hydrogen offers a long-term, seasonal energy storage solution for intermittent renewable sources, providing a vital opportunity for grid stability and large-scale, deep decarbonization in hard-to-abate industrial sectors.

Segmental Insights

Technology Insights

The Alkaline Electrolysis Segment Dominated the Green Hydrogen Market with 48% of Market Share in 2025

The alkaline electrolysis segment dominated the market with 48% share in 2025. This is primarily due to its maturity as a technology, lower capital costs, and suitability for large-scale industrial projects. Alkaline electrolyzers, having been developed over decades, are less expensive to build and operate, making them the preferred choice for large-scale, cost-sensitive projects. Additionally, they provide long operating periods and high reliability, which are ideal for continuous industrial use, aided by low power densities that enhance their durability.

The PEM electrolysis segment held the 32% market share in 2025 and is expected to experience the fastest CAGR of 41.5% during the forecast period. This growth is driven mainly by its compact design, high efficiency, and quick dynamic response to intermittent renewable energy sources such as wind and solar. PEM electrolyzers perform well under varying power conditions, making them highly suitable for integration with these renewable sources. They provide high current densities and efficient hydrogen production, with significant cost reductions anticipated, further promoting market adoption.

The Solid Oxide Electrolyzer Cell segment held 12% market share in 2025. This success can be attributed to its superior efficiency, ability to operate at high temperatures, and capability to integrate with industrial waste heat. Solid oxide systems achieve higher electrical efficiency than other electrolyzers, which reduces the overall levelized cost of hydrogen. They integrate smoothly with industrial processes that generate waste heat, facilitating high-temperature steam electrolysis, thereby significantly improving conversion efficiency.

Energy Source Insights

The Solar Energy Segment Dominated the Green Hydrogen Market with 42% of Market Share in 2025

The solar energy segment dominated the market with 42% share in 2025. This dominance is driven by decreasing solar photovoltaic costs, extensive scalability in high-irradiation regions, and effective pairing with electrolyzers to provide low-cost electricity. Lower electricity prices directly contribute to reducing the cost per kilogram of hydrogen produced via electrolysis. Solar farms can be built more rapidly and are often more modular than many other renewable energy sources, allowing for a swift response to rising demand and enhancing daily hydrogen generation rates.

Green Hydrogen Market Share, By Energy Source, 2025 (%)

| By Energy Source | Revenue Share, 2025 (%) |

| Solar Energy | 42% |

| Wind Energy | 33% |

| Hydropower | 15% |

| Hybrid Systems | 10% |

The wind energy segment held the 33% market share in 2025 and is projected to experience the fastest CAGR of 39.2% during the forecast period. This growth is fueled by its high efficiency, maturity, and abundance in coastal and open areas, including both offshore and onshore projects. Wind farms are increasingly being utilized to generate power for electrolyzers during periods of low demand, which assists with grid balancing and enables cost-effective hydrogen production. Enhancements in turbine capacity, design improvements, and declining costs make wind-based hydrogen production highly competitive.

The hydropower segment held the 15% market share in 2025. This can be attributed to its capability to provide consistent, round-the-clock, low-cost renewable electricity for electrolyzers, addressing the intermittency challenges posed by solar and wind energy. Hydropower generates some of the lowest-cost renewable electricity, which is essential for reducing the overall production costs of green hydrogen, as energy constitutes a significant part of the final cost. Many hydropower plants can easily integrate electrolyzers by utilizing existing dams, grid connections, and water resources to establish efficient, localized production hubs.

Application Insights

The Ammonia Production Segment Dominated the Green Hydrogen Market with 36% of Market Share in 2025

The ammonia production segment dominated the market with a 36% share in 2025. This leadership is largely driven by the urgent need for industrial decarbonization and agricultural sustainability as a replacement for the conventional, fossil-fuel-intensive Haber-Bosch process. Ammonia is an efficient method for storing and transporting hydrogen over long distances, positioning it as a primary carrier in the green energy transition. The ability to produce ammonia in large volumes for global trade is driving adoption, with the technology maturing to efficiently produce the necessary green hydrogen.

Green Hydrogen Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Ammonia Production | 36% |

| Refining | 22% |

| Power Generation | 14% |

| Transportation | 18% |

| Industrial Processes | 10% |

The transportation segment held the 18% market share in 2025 and is projected to experience the fastest CAGR of 42.3% during the forecast period. This growth is motivated by the need for zero-emission solutions in heavy-duty vehicles, shipping, and long-range transport, where battery electrification is limited. Stringent emission regulations, national decarbonization strategies, and subsidies for fuel cell technologies are accelerating adoption. Hydrogen fuel cell electric vehicles, particularly trucks, buses, trains, and maritime vessels, are increasingly replacing diesel vehicles, as they offer longer ranges and shorter refueling times.

The refining segment held the 22% market share in 2025. This is mainly driven by the urgent need to decarbonize traditional fossil-fuel-based processes such as hydrocracking and desulfurization. Refineries are shifting from fossil-based hydrogen to green hydrogen to comply with stringent carbon reduction regulations and achieve net-zero goals. Environmental standards for low-sulfur diesel and petrol are becoming more rigorous, requiring more intensive hydrodesulfurization processes, which consume substantial amounts of hydrogen.

End-Use Industry Insights

The Chemicals Segment Dominated the Green Hydrogen Market with 34% of Market Share in 2025

The chemicals segment dominated the market with 34% share in 2025. This dominance is primarily due to the immediate off-take for decarbonizing large-scale industrial feedstocks. As a hard-to-abate sector, chemical manufacturing is a priority for decarbonization efforts. The strong demand for fertilizers, polymers, and other intermediate chemicals drives sustained, large-scale consumption of green hydrogen. Leveraging established chemical production facilities allows for quicker adoption compared to new infrastructure projects.

Green Hydrogen Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Chemicals | 34% |

| Energy & Utilities | 20% |

| Mobility & Transportation | 16% |

| Metals & Mining | 12% |

| Oil & Gas | 10% |

| Others | 8% |

The energy and utilities segment held the 20% market share in 2025 and is projected to experience the fastest CAGR of 39.6% during the forecast period. This growth is linked to its advantages in decarbonization, grid stabilization, and long-duration energy storage. Utilities are increasingly adopting green hydrogen to address the intermittency of renewable energy sources, using it for long-term and seasonal storage to ensure energy resilience. This facilitates the conversion of excess renewable electricity into hydrogen or methane, supporting decarbonization goals and regulatory compliance.

The mobility and transportation segment held 16% market share in 2025, primarily due to its high energy density for heavy-duty vehicles, rapid refueling capabilities, and zero tailpipe emissions. Fuel cell electric trucks are leading the way in adoption due to their superior long-range capabilities compared to battery vehicles. The rapid expansion of refueling infrastructure and technological advancements is overcoming initial barriers to adoption. Stricter emission regulations are further solidifying green hydrogen as the preferred fuel for heavy transportation, industrial machinery, and logistics.

Distribution Channel Insights

The On-Site Generation Segment Dominated The Green Hydrogen Market With 46% Of Market Share In 2025

The on-site generation segment dominated the market with 46% share in 2025 and is expected to grow at the fastest CAGR of 38.7% over the forecast period. This growth is attributed to its capability to eliminate the high costs and logistical challenges associated with transporting and storing gaseous hydrogen. On-site production minimizes the substantial infrastructure investments required for pipelines, trucks, and ships, making merchant hydrogen less attractive in the early stages of the green hydrogen economy and enabling the direct conversion of electricity to green hydrogen.

Green Hydrogen Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Pipeline | 28% |

| On-site Generation | 46% |

| Merchant Supply | 26% |

The pipeline segment held 28% market share in 2025, mainly driven by the need for cost-effective, high-volume, and continuous transportation for industrial hubs. Key trends include repurposing existing natural gas networks and developing new infrastructure. Pipelines are the most efficient method for transporting large volumes over short to medium distances, which is essential for industrial hubs. Increased attention to high-strength steel alloys and specialized coatings is preventing hydrogen embrittlement and enhancing safety, making pipelines the preferred transportation choice.

Regional Insights

How Did Europe Dominated The Green Hydrogen Market In 2025?

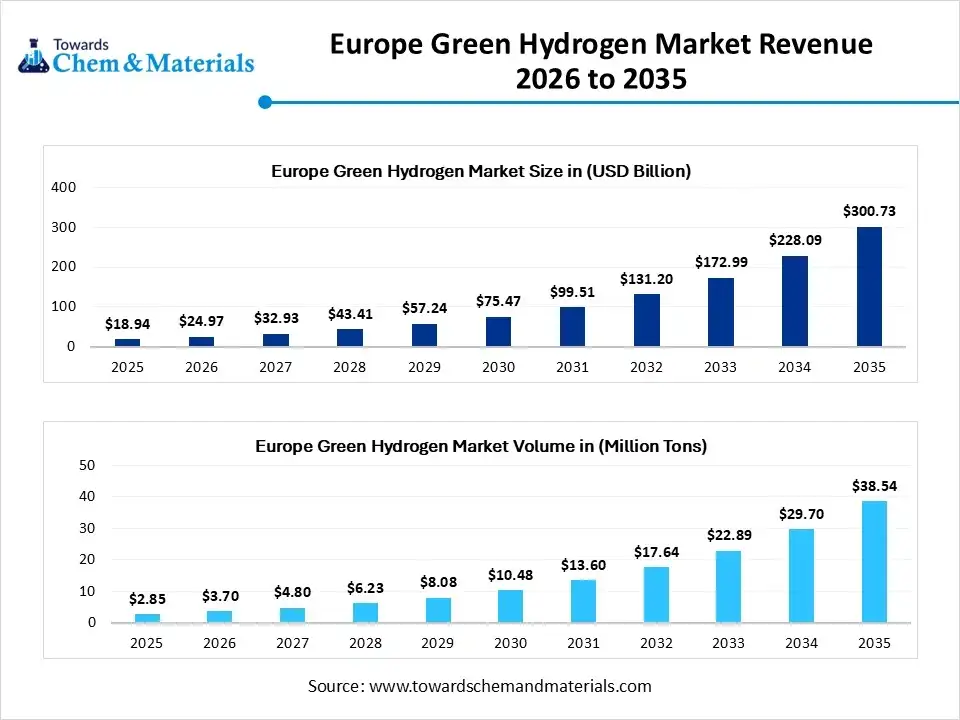

The Europe green hydrogen market size was estimated at USD 4.24 billion in 2025 and is projected to reach USD 113.02 billion by 2035, growing at a CAGR of 38.86% from 2026 to 2035 Europe has a strong demand for hydrogen in hard-to-abate sectors such as steel and chemical production. Europe is home to several leading electrolyzer manufacturers, including Siemens Energy, Nel ASA, ITM Power, and Thyssenkrupp Nucera, which set the standard for PEM and alkaline technologies and help unlock private investment in infrastructure and technology.

")

Germany Green Hydrogen Market Growth Trends

Germany plays a distinctive role within the region, with high demand for hydrogen from its energy-intensive industrial sectors, including steel and chemicals. Germany aims to be the global leader in hydrogen technologies, specifically in electrolyzer manufacturing, fuel cell development, and industrial applications, to achieve significant carbon dioxide emission reductions.

Asia Pacific Green Hydrogen Market Growth Trends

Asia Pacific held the 29% market share in 2025 and is anticipated to be the fastest-growing in the market with a CAGR of 40.5% during the forecast period, driven by rapid industrialization, aggressive government policies, and stringent decarbonization goals that support renewable energy integration. Key economies such as China, India, Japan, and South Korea have launched National Hydrogen Strategies, providing subsidies and financial incentives for clean hydrogen production. The region’s large refining, steel, chemical, and fertilizer industries are seeking to decarbonize, driving high demand for hydrogen and fostering long-term infrastructure investment.

India Green Hydrogen Market Growth Trends

India is rapidly positioning itself as a global leader within the region by leveraging its vast renewable energy potential to transition from an energy importer to a major exporter. With low-cost solar and wind power, India is projected to be among the lowest-cost producers, with a goal of bringing production costs down. India is promoting indigenous manufacturing of electrolyzers, which is crucial for reducing dependence on imports and scaling up production.

Recent Developments

- In January 2026, Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH and thyssenkrupp nucera announced a cooperation to promote green hydrogen and Power-to-X (PtX) markets in India during the India Energy Week in Goa to leverage GIZ's expertise in sustainable development and thyssenkrupp's technology in electrolysis.

- In December 2025, NTPC's research division, NETRA, is set to launch a green hydrogen facility at its Greater Noida campus, utilizing plasma gasification technology to convert waste into syngas for hydrogen production. The plant aims to produce one tonne of green hydrogen daily, marking NTPC's expansion into sustainable energy.

Top Companies in the Green Hydrogen Market

- Air Products and Chemicals, Inc.

- Linde plc

- Siemens Energy AG

- Air Liquide S.A.

- ENGIE SA

- Shell plc

- Nel ASA

- Plug Power Inc.

- Uniper SE

- Cummins Inc.

- Bloom Energy

- Adani Green Energy

- Reliance Industries

- NTPC Limited

- China Huaneng Group

Green Hydrogen Market Segments Covered in the Report

By Technology

- Alkaline Electrolysis (AEL)

- Conventional Alkaline

- Advanced Alkaline

- Proton Exchange Membrane (PEM)

- Low-temperature PEM

- High-pressure PEM

- Solid Oxide Electrolysis (SOEC)

- Tubular SOEC

- Planar SOEC

- Anion Exchange Membrane (AEM)

- Lab-scale AEM

- Commercial AEM

By Energy Source

- Solar Energy

- Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- Wind Energy

- Onshore Wind

- Offshore Wind

- Hydropower

- Hybrid Renewable Systems

- Solar + Wind

- Solar + Hydro

By Application

- Ammonia Production

- Fertilizers

- Industrial Chemicals

- Refining

- Hydrocracking

- Desulfurization

- Power Generation

- Fuel Cells

- Grid Injection

- Transportation

- Fuel Cell Vehicles (FCEVs)

- Aviation Fuel (e-fuels)

- Maritime Fuel

- Industrial Processes

- Steel Production (DRI)

- Methanol Production

By End-Use Industry

- Chemicals

- Energy and Utilities

- Mobility and Transportation

- Metals and Mining

- Oil and Gas

- Others

- Food Processing

- Electronics

By Distribution Channel

- Pipeline

- On-site Generation

- Merchant Supply

- Liquid Hydrogen

- Compressed Gas

By Region

- North America:

- U.S.

- Canada

- Mexico

- Rest of North America

- Latin America:

- Brazil

- Argentina

- Rest of Latin America

- Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

- GCC Countries

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (5)