Content

What is the current Europe Polypropylene Market Size and Share?

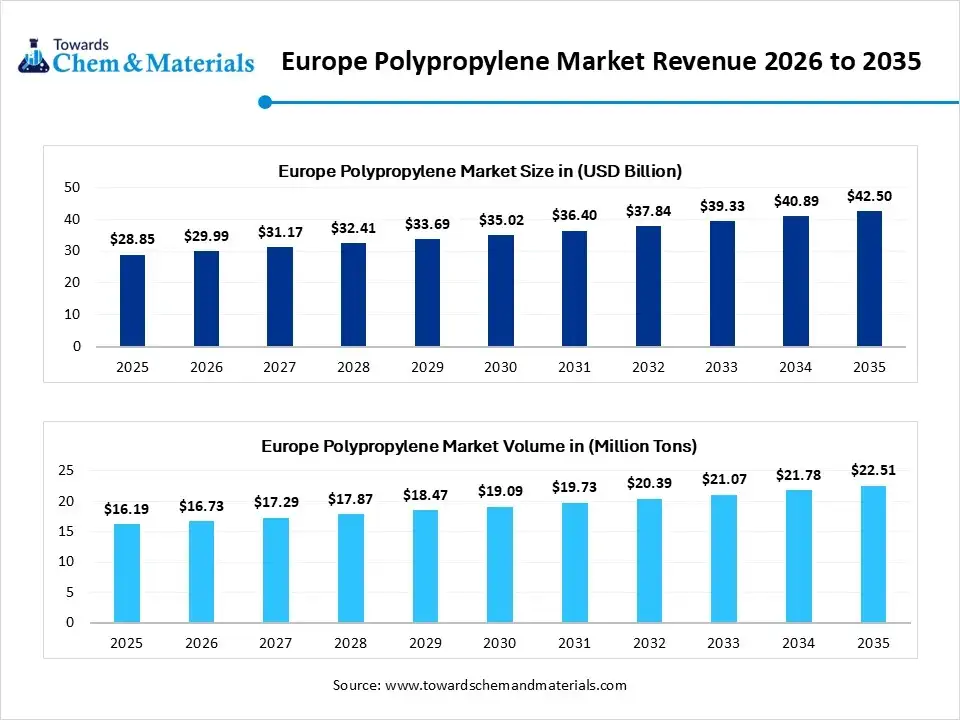

The Europe polypropylene market size was valued at USD 28.85 billion in 2025, is estimated to reach USD 29.99 billion in 2026, and is projected to reach USD 42.50 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 3.95% over the forecast period from 2026 to 2035. In terms of volume, the Europe polypropylene market is projected to grow from 16.19 million tons in 2025 to 22.51 million tons by 2035. growing at a CAGR of 3.35% from 2026 to 2035. Increasing demand for lightweight materials in automotive manufacturing is the key factor driving market growth. Also, the growth of the e-commerce packaging sector, coupled with the ongoing development of bio-based polymer alternatives, can fuel market growth further.

The market includes the manufacturing, trade, and consumption of a versatile thermoplastic polymer generally used in packaging, automotive parts, and textiles. The regional trade network involves the production and compounding of base polypropylene to create durable, lightweight, and chemically resistant plastics. The market is mainly driven by stringent European Commission regulations focusing on investments in mechanical recycling capacity and production.

Polypropylene is widely utilized throughout Europe for its versatility in both flexible and rigid packaging, as well as in structural components. Furthermore, expanding industrial requirements and increasing urban consumption are generating significant market opportunities for both virgin and recycled polypropylene grades.

Market Highlights

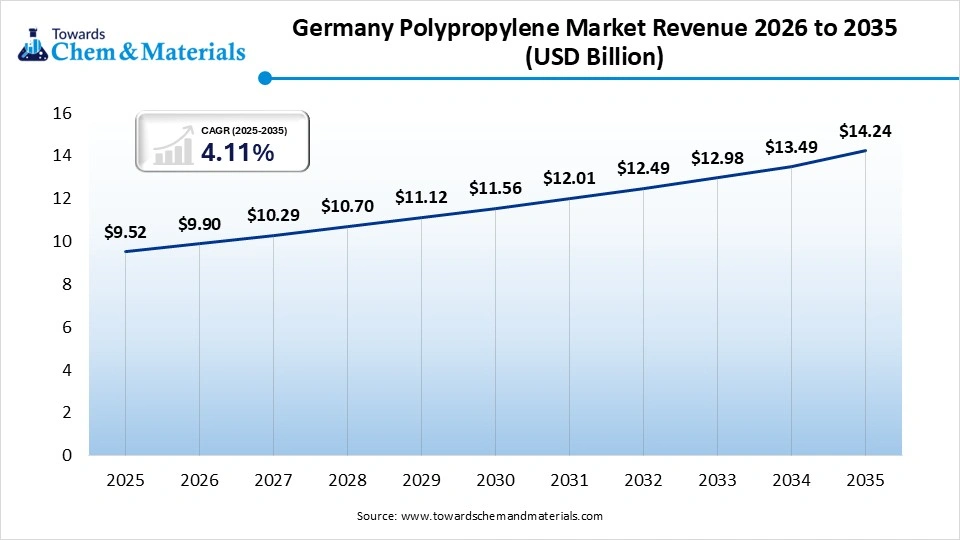

- By country, Germany dominated the market with the largest share of 33% in 2025. The dominance of the country can be attributed to the increasing demand for propylene across different sectors.

- By country, Spain is expected to grow at the fastest CAGR of 4.54% over the forecast period. The growth of the country can be credited to the increasing export activities.

- By polymer type, the homopolymer segment dominated the market with the largest share of 58% in 2025. The dominance of the segment can be attributed to the increasing demand for homopolymer polypropylene from the packaging industry.

- By polymer type, the copolymer segment is expected to grow at the fastest CAGR of 4.46% over the forecast period. The growth of the segment can be credited to the increasing demand for impact-resistant copolymers.

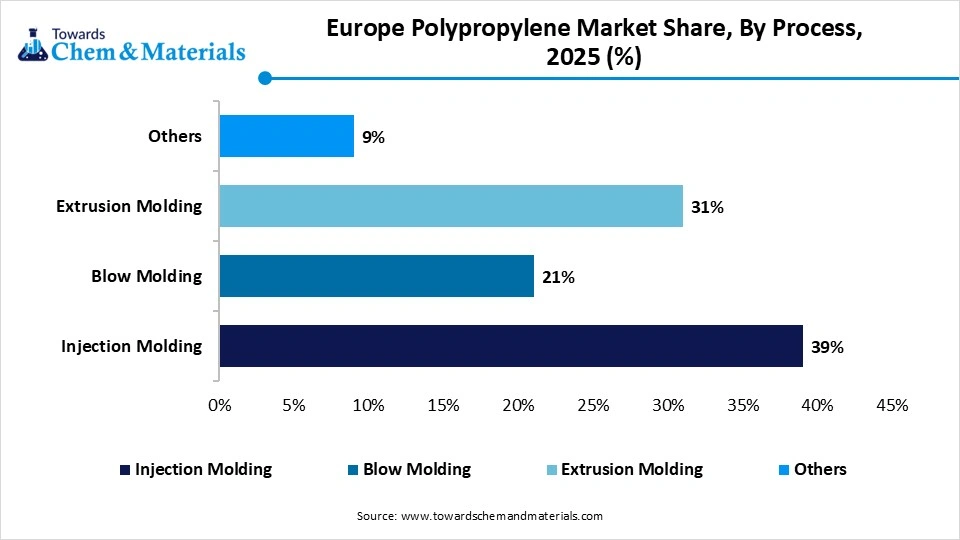

- By process, the injection molding segment dominated the market with the largest share of 39% in 2025. The dominance of the segment can be linked to the increasing demand for lightweight industrial components.

- By process, the extrusion molding segment is expected to grow at the fastest CAGR of 4.32% over the forecast period. The growth of the segment can be driven by increasing demand for BOPP films and materials from the packaging industry.

- By application, the film & sheet segment dominated the market with the largest share of 36% in 2025 and is expected to grow at the fastest CAGR of 4.64% over the forecast period. The dominance and growth of the segment can be attributed to the growing adoption of recyclable films.

- By end use, the packaging segment dominated the market with the largest share of 34% in 2025 and is expected to grow at the fastest CAGR of 4.92% over the forecast period. The dominance and growth of the segment can be driven by an increase in BOPP film production.

At a Glance

- Market Estimated Size (2025): USD 28.85 Billion | CAGR (2026–2035): 3.95%

- Market Projected Size (2035): USD 42.50 Billion

- Market Estimated Volume (2025): 16.19 Million Tons | Volume CAGR (2026–2035): 3.35%

- Market Projected Volume (2035): 22.51 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 1,445 per Ton

- Average Selling Price: USD 1,892 per Ton

- Pricing CAGR (2026–2035): 2.89%

Recent Trends

- An increasing focus on sustainability, circular economy, and recycling is the latest trend in the market shaping positive market growth. Market players are rapidly adopting mechanical and chemical recycling methods to minimize plastic waste and support resource efficiency.

- Automakers in the region are heavily using PP in dashboards, bumpers, and interior trim because of its exceptional strength-to-weight ratio and moldability. This trend is mainly fueled by fuel efficiency goals and EV lightweighting strategies.

- Ongoing innovations in polymerization are another major trend in the market, driving market growth. New catalyst technologies and advancements in blending technologies are facilitating customized PP grades with higher transparency, impact resistance, and thermal stability.

How Cutting-Edge Technologies Are Revolutionizing the Europe Polypropylene Market?

Advanced technologies are transforming the market by transitioning the focus from conventional manufacturing to circularity, advanced production, and vehicle lightweighting. Furthermore, the deployment of advanced 3D printing technologies with PP resins is converting prototyping and customized production across European healthcare and consumer electronics, impacting positive market expansion soon

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 29.99 Billion/ 16.73 Million Tons |

| Revenue Forecast in 2035 | USD 42.50 Billion/ 22.51 Million Tons |

| Growth Rate | CAGR 3.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Country | Germany |

| Segment Covered | By Polymer Type, By Application, By End Use, By Country |

| Key companies profiled | Harima Chemicals Group, Inc, BASF SE, Resinall Corp (U.S.), Ingevity (U.S.), OMNOVA Solutions Inc (U.S.), Arakawa Chemical Industries Ltd. (Japan), KRATON CORPORATION (U.S.), Arkema (France), Evonik Industries AG (Germany), Gellner Industrial LLC (U.S.), Shenghong Chemical (China), Meilida Pigment Industry Co., Ltd. (China), MHM Holding Beteiligungs GmbH (Germany), Advanced Micro Polymers Inc. (U.S.). |

Supply Chain Analysis of the Europe Polypropylene Market

- Feedstock Procurement: It is the sourcing & purchasing of raw materials, majorly propylene, or sustainable alternatives used by manufacturers to produce polypropylene.

- Major Players: SABIC, ExxonMobil Chemical Company

- Chemical Synthesis and Processing :It refers to the sequence of converting petroleum-derived raw materials into highly specialized, solid plastic resins. It also involves upstream monomer production, catalytic polymerization reactions, and compounding techniques.

- Major Players: TotalEnergies S.A., ExxonMobil Chemical Company

- Packaging and Labeling:It includes the use of PP resins and films for consumer and industrial packaging films utilized for high-grade graphic labels, and it is valued for its moisture resistance, transparency, and cost-effectiveness.

- Major Players: Taghleef Industries, Polinas

- Regulatory Compliance and Safety Monitoring:It involves stringent regulatory compliance and safety monitoring encompassing EU-wide laws governing chemical safety (REACH), food contact materials, and packaging waste mandates.

- Major Players: TotalEnergies, BASF SE

Europe Polypropylene Market's Regulatory Landscape

| Country | Key Regulation |

| Germany | As Europe's largest PP consumer—primarily for the automotive, construction, and advanced packaging sectors—Germany enforces compliance through the VerpackG (German Packaging Act). |

| France | France actively drives the healthcare- and pharmaceutical-grade PP markets. Under the AGEC Law (Anti-Waste for a Circular Economy Law), France enforces rapid phases-out of single-use plastics. |

| United Kingdom | Following Brexit, the UK operates independently of the EU PPWR under the UK Plastic Packaging Tax (PPT). This requires a tax of £210.82 per metric tonne (adjusted for inflation) on plastic packaging manufactured in or imported into the UK that contains less than 30% recycled plastic. |

Market Dynamics

Drivers

Expansion in E-commerce solutions

The market is expanding due to the ongoing growth of e-commerce and effective packaging solutions. As online shopping is increasingly gaining traction, the demand for protective packaging materials that ensure product safety during transit becomes more crucial. In addition, expanded polypropylene provides exceptional cushioning properties, which make it a key choice for packaging fragile items. This growth highlights the material's versatility and efficacy in adapting to the dynamic demands of the e-commerce sector, which in turn strengthens the polypropylene market.

Restraint

Fluctuations in Raw Material Prices

The price volatility of propylene and crude oil raw materials, especially propylene, is the major factor hindering the market growth. As it is petroleum-derived, its price directly affects manufacturing costs and profit level over time, posing challenges for market players with their strategies in the long run. Moreover, geopolitical tensions and supply chain disruptions further create this challenge to market growth. These factors also induce price volatility, which can severely impact manufacturers' profit margins and complicate long-term strategic planning.

Opportunity

Ongoing Development of Bio-based Polypropylene

The rapid development of bio-based polypropylene is the major factor creating lucrative opportunities in the market, boosted by both government agencies and consumers seeking sustainable alternatives. Government incentives optimize sustainable production behaviour among market players while collaborating with other industry players. Furthermore, the expanding recycling sector amplifies this trend by providing businesses with reliable, long-term revenue streams and sustained economic benefits.

Segmental Insights

Polymer Type Insights

The homopolymer segment dominated the market with the largest share of 58% in 2025. The dominance of the segment can be attributed to the increasing demand for homopolymer polypropylene from the packaging industry and cost-effective production, boosting its extensive adoption across the region.

The copolymer segment held the market share of 42% in 2025 and is expected to grow at the fastest CAGR of 4.46% over the forecast period. The growth of the segment can be credited to the increasing demand for impact-resistant copolymers and the rise in investment in copolymer innovation. Flexible packaging sector are highly adopting specialty polymer grades.

Process Insights

The injection molding segment dominated the market with the largest share of 39% in 2025. The dominance of the segment can be linked to the increasing demand for lightweight industrial components along with the high-volume production capabilities, improving overall manufacturing efficiency.

The extrusion molding segment held the market share of 31% in 2025 and is expected to grow at the fastest CAGR of 4.32% over the forecast period. The growth of the segment can be driven by increasing demand for BOPP films and materials from the packaging industry, coupled with the demand for rigid packaging. Improved recyclability boosts adoption across different applications.

The blow molding segment held the market share of 21% in 2025. The growth of the segment is owing to the surge in container manufacturing across the globe due to the rise in demand, along with its enhanced recyclability, which is improving adoption across various other applications.

")

Application Insights

The film & sheet segment dominated the market with the largest share of 36% in 2025 and is expected to grow at the fastest CAGR of 4.64% over the forecast period. The dominance and growth of the segment can be attributed to the growing adoption of recyclable films due to ongoing adoption of sustainability trends and growing utilisation of polypropylene films in food packaging applications.

The fiber segment held the market share of 23% in 2025. The growth of the segment can be credited to the growing consumption of polypropylene fiber due to the rise in demand for non-woven hygiene products. In addition, textile industries are adopting durable synthetic materials rapidly.

The other segment held the market share of 22% in 2025. The growth of the segment can be linked to the increase in durable material applications in pipe and appliance sectors, coupled with the ongoing development in multifunctional propulsive product development.

End Use Insights

The packaging segment dominated the market with the largest share of 34% in 2025 and is expected to grow at the fastest CAGR of 4.92% over the forecast period. The dominance and growth of the segment can be driven by an increase in BOPP film production due to growing demand for flexible packaging and sustainability trends supporting lightweight, recyclable film adoption.

The automotive segment held the market share of 26% in 2025. The growth of the segment is owing to the increasing polypropylene fiber consumption due to non-woven hygiene product demand and the textiles industry's adoption of durable synthetic fiber extensively.

The building & construction segment held the market share of 18% in 2025. The growth of the segment is due to EV production accelerating production of durable polymer materials, along with the automotive OEMs' improving fuel efficiency using lightweight plastics.

Country Insights

How did Germany Dominate the Europe Polypropylene Market in 2025?

The Germany Europe Polypropylene market size was estimated at USD 9.52 billion in 2025 and is projected to reach USD 14.24 billion by 2035, growing at a CAGR of 4.11% from 2026 to 2035.Germany dominated the market with the largest share of 33% in 2025. The dominance of the country can be attributed to the increasing demand for propylene across different sectors due to a surge in automotive manufacturing across major regions and advanced polymer processing technologies boosting regional production capacity. In addition, the ongoing implementation of sustainability regulations is driving adoption rapidly further.

The Spain held the market share of 14% in 2025 and is expected to grow at the fastest CAGR of 4.54% over the forecast period. The growth of the country can be credited to the increasing export activities boosting regional material demand, along with the surge in polymer manufacturing investment in emerging regions. Furthermore, expanding packaging and infrastructure industry is propelling propylene consumption shortly.

Recent Development

- In January 2026, Ineos Olefins & Polymers Europe, a Switzerland-based corporation, expanded its portfolio of "hybrid" polyolefins with the introduction of a new resin that integrates mechanically processed post-consumer recycled (PCR) content with high-performance virgin polymers.(Source: resource-recycling.com)

Europe Polypropylene Market Companies

- Harima Chemicals Group, Inc.:Harima Chemicals Group, Inc. operates in the European polypropylene market as a specialized manufacturer of pine chemical-derived functional additives and resins, often supporting the processing, bonding, and functional coating of polyolefins like polypropylene.

- BASF SE: BASF SE is a key player in the European polypropylene (PP) and polyolefins market, focusing heavily on specialty compounds, circular economy solutions, and advanced foam products rather than mass-commodity bulk production.

Other Companies in the Market

- Resinall Corp (U.S.)

- Ingevity (U.S.)

- OMNOVA Solutions Inc (U.S.)

- Arakawa Chemical Industries Ltd. (Japan)

- KRATON CORPORATION (U.S.)

- Arkema (France)

- Evonik Industries AG (Germany)

- Gellner Industrial LLC (U.S.)

- Shenghong Chemical (China)

- Meilida Pigment Industry Co., Ltd. (China)

- MHM Holding Beteiligungs GmbH (Germany)

- Advanced Micro Polymers Inc. (U.S.)

Segments Covered in the Report

By Polymer Type

- Homopolymer

- General Purpose Homopolymer

- High Crystallinity Homopolymer

- Raffia Grade Homopolymer

- Copolymer

- Random Copolymer

- Impact Copolymer

- Specialty Copolymer

By Process

- Injection Molding

- Thin Wall Injection Molding

- Technical Component Molding

- Automotive Component Molding

- Blow Molding

- Extrusion Blow Molding

- Injection Blow Molding

- Stretch Blow Molding

- Extrusion Molding

- Pipe Extrusion

- Sheet Extrusion

- Profile Extrusion

- Others

- Thermoforming

- Rotational Molding

- Compression Molding

By Application

- Fiber

- Nonwoven Fibers

- Staple Fibers

- Continuous Filament Fibers

- Film & Sheet

- Cast Films

- BOPP Films

- Extruded Sheets

- Raffia

- Woven Sacks

- Ropes & Twines

- Geotextiles

- Others

- Pipes

- Consumer Goods

- Industrial Components

By End Use

- Automotive

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Building & Construction

- Pipes & Fittings

- Insulation Materials

- Construction Sheets

- Packaging

- Flexible Packaging

- Rigid Packaging

- Food Packaging

- Medical

- Syringes

- Medical Packaging

- Diagnostic Components

- Electrical & Electronics

- Appliance Components

- Electrical Insulation

- Electronic Housings

- Others

- Consumer Goods

- Furniture

- Agriculture

By Country

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)