Content

What is the Powder Metallurgy Market Size and Share?

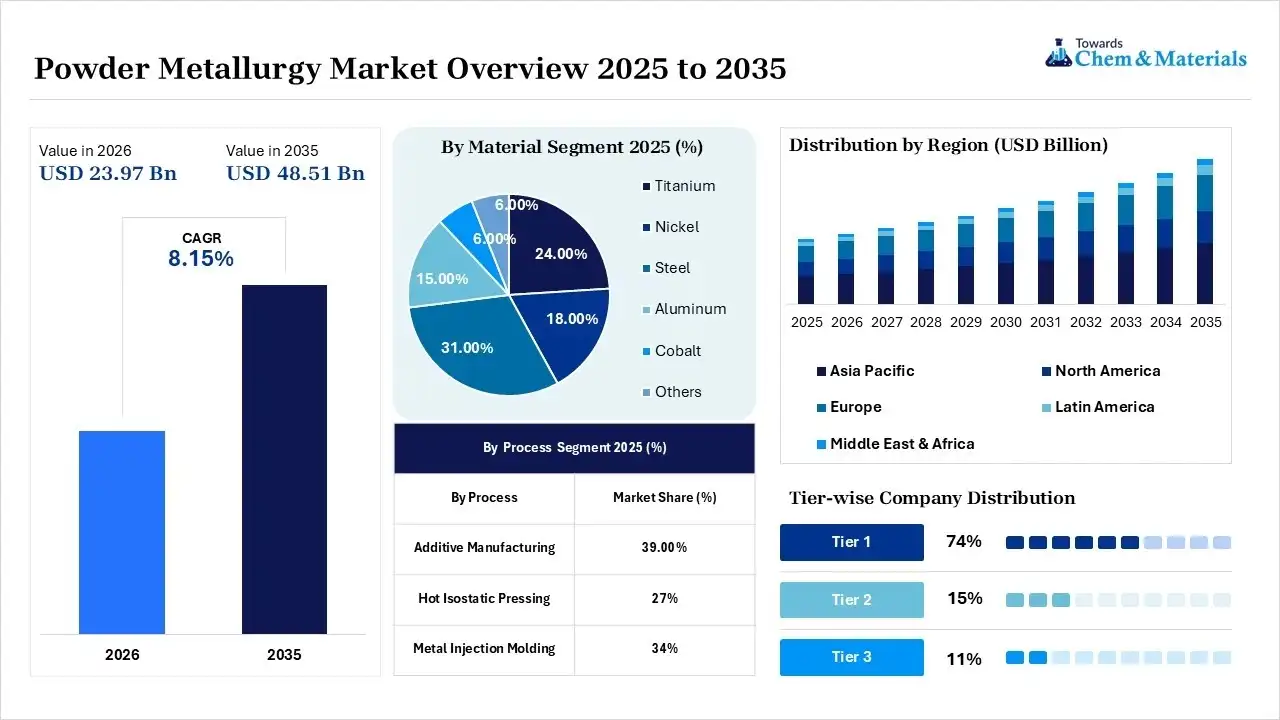

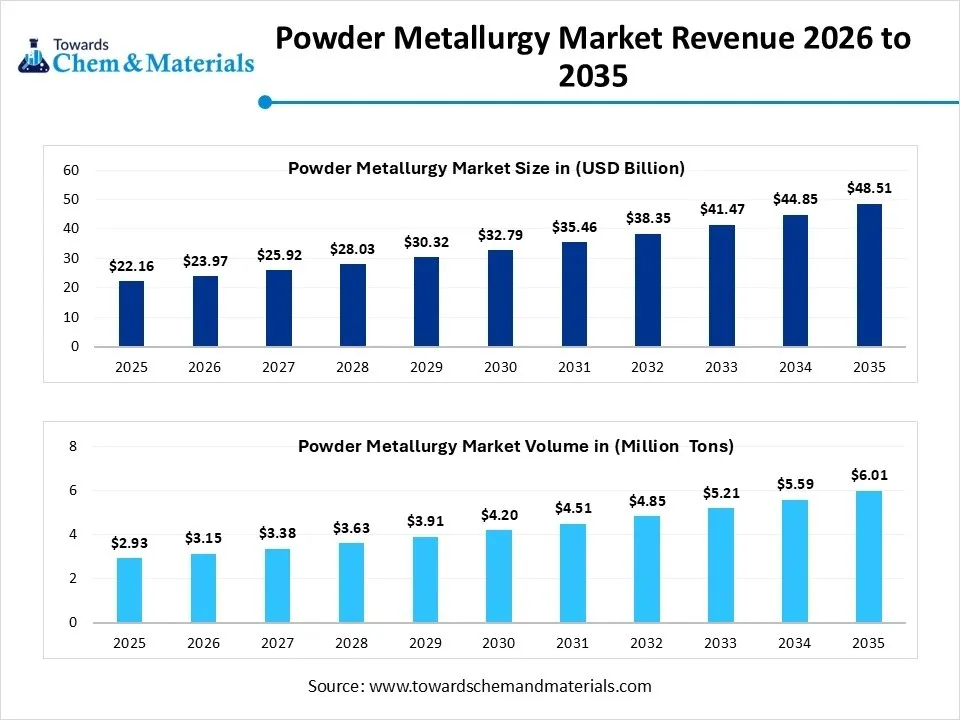

The global powder metallurgy market size was valued at USD 22.16 billion in 2025, is estimated to reach USD 23.97 billion in 2026, and is projected to reach USD 48.51 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 8.15% over the forecast period from 2026 to 2035.Asia Pacific dominated the powder metallurgy market with the largest revenue share of 43% in 2025 and is expected to grow at the fastest CAGR of 8.27% during the forecast period. In terms of volume, the powder metallurgy market is projected to grow from 2.93 million tons in 2025 to 6.01 million tons by 2035. growing at a CAGR of 7.45% from 2026 to 2035.The growth of the market is driven by the growing demand from the automotive industry for lightweight materials to increase fuel efficiency, the shift towards electric vehicles, and the rise of 3D printing, which fuels the growth of the market. The key collaborations between major players like Hoganas AB and GKN Power Metallurgy involve major sectors such as aerospace, automotive, and defense OEM, which increases the demand and growth of the market.

Market Highlights

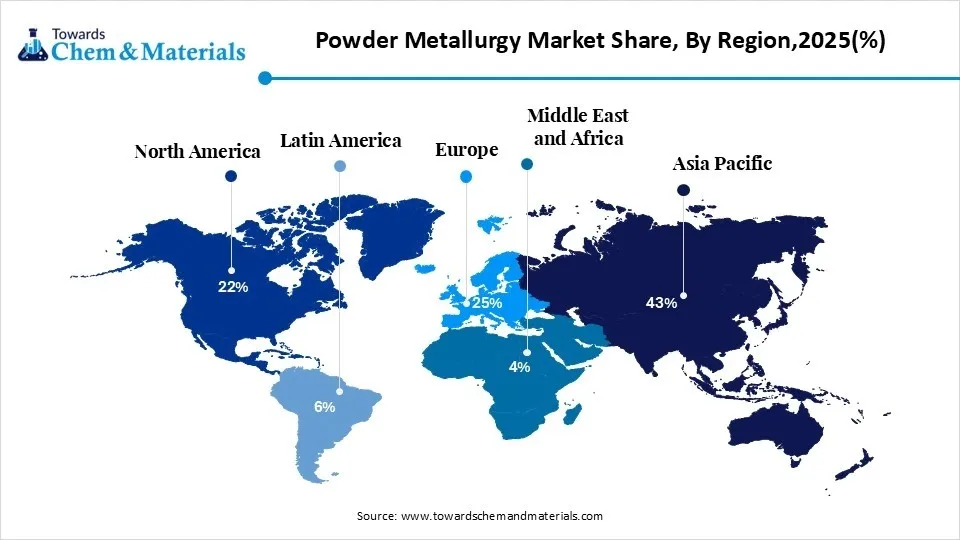

- By region, Asia Pacific dominated the market with a share of 43% in 2025. Manufacturing expansion strengthens regional demand.

- By region, North America held 22% market share in 2025 and is expected to experience the fastest growth with a CAGR of 9.40% in the forecast period. Aerospace innovation increases powder usage.

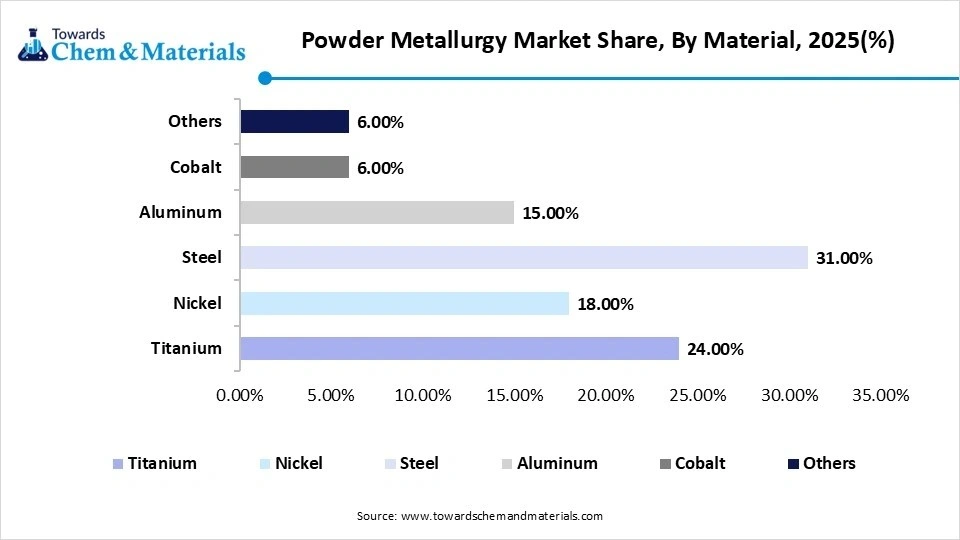

- By material, the steel segment dominated the market with a 31% share in 2025. Automotive production drives steel powder demand.

- By material, the titanium segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.80% in the forecast period. Growing demand in aerospace increases titanium powder consumption.

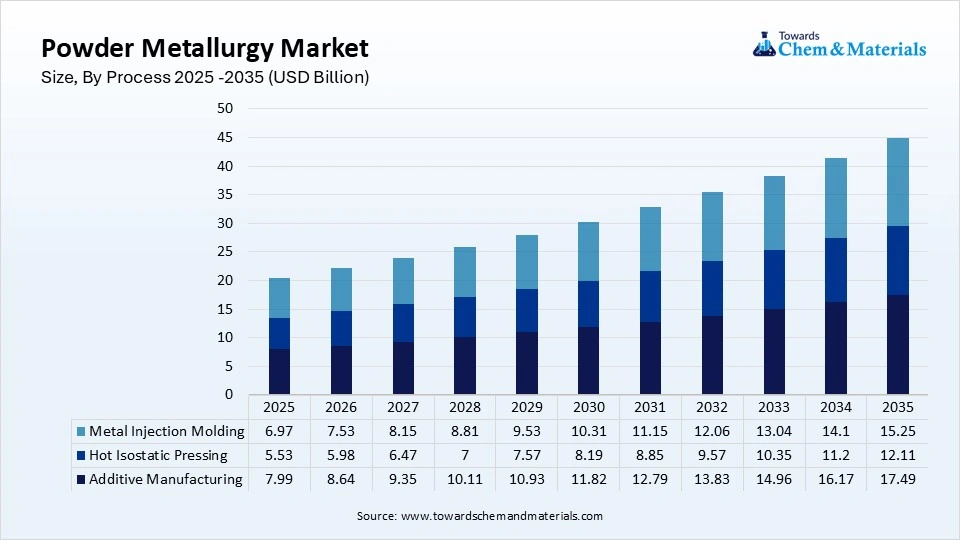

- By process, the additive manufacturing segment dominated the market with a 39% share in 2025 and is expected to have the fastest growth with a CAGR of 12.10% in the forecast period. Industrial 3D printing expands across sectors.

- By application, the automotive segment dominated the market with a 37% share in 2025. Vehicle electrification expands powder metallurgy applications.

- By application, the medical & dental segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.9% in the forecast period. Personalized implants increase powder utilization.

- By end use, the OEMs segment dominated the market with a 73% share in 2025. Large-scale manufacturing secures consistent demand. Personalized implants increase powder.

- By end use, the AM operators segment held 27% market share in 2025 and is expected to have the fastest growth with a CAGR of 11.80% in the forecast period. Contract manufacturing services expand globally.

Powder Metallurgy Market: Expanding Application In Major Sectors

According to Towards Chemicals and Materials Analytics and Consulting, the powder metallurgy market volume is expected to increase from 2.93 million tons in 2025 to 3.15 million tons in 2026 and reach 6.01 million tons by 2035, growing at a CAGR of 7.45% over 2026-2035.

The powder metallurgy market is expanding rapidly due to the global focus on vehicle lightweighting, the surge in electric vehicle (EV) adoption, and the growth of metal additive manufacturing. PM is preferred because it shapes complex metal components with nearly 97% material efficiency and produces less waste than traditional machining. This manufacturing sector is highly efficient, transforming fine metal powders into precise, complex parts through pressing and heating. It is important because it reduces metal waste, enables the creation of unique materials, and lowers production costs. The process produces parts that are very close to their final size, requiring little to no additional shaping.

It enables the development of porous metals used in self-lubricating engine parts or filters, something that is impossible with traditional casting. Vehicles benefit from lightweight gears and bearings made through this method, which enhances fuel efficiency and supports electric drivetrains. Aerospace applications include using strong, lightweight metals like titanium to save fuel and withstand high temperatures. Additionally, it is employed in manufacturing affordable, custom hip stems and porous spinal implants, as well as porous, customizable titanium parts for bone implants and joint replacements that bond easily with the human body.

- For instance, the DSH technologies, a Pineville, North Carolina-based provider of debinding and sintering services, launched a membership program. The launch aims at direct access for manufacturers to the metallurgical expertise, process, and laboratory services.

(Source: www.voxelmatters)

Global Investment Flow for Powder Metallurgy Market 2026

The major giants such as GKN Sinter Metals, Sumitomo Electric Industries, Sandvik AB, Carpenter Technology Corporation, Höganäs AB, Advanced Technology & Materials Co. Ltd. (AT&M), and Hitachi Chemical are investing heavily in the production of soft magnetic composites and scaling up of plants, which increases market growth.

Major industry giants are aggressively investing in powder metallurgy to support electric vehicles (EVs), aerospace, and automation. Key 2026 trends feature massive capacity expansions, vertical acquisitions, and the development of sustainable, low-carbon metal powders.

The Odisha Government has signed a landmark Memorandum of Understanding (MoU) with Adani Enterprises Limited (AEL) and Abu Dhabi-based International Resources Holding (IRH) to build an integrated greenfield aluminium project. Valued at ₹1.08 lakh crore (USD 11.5 billion), this venture is officially recorded as the largest metallurgy

- Foreign Direct Investment (FDI) in India’s history.(Source: www.newindianexpress.com)

- Carpenter Technology Corporation is investing $354.25 million to expand its specialty metals manufacturing plant in Limestone County, Alabama, a move projected to create at least 62 jobs over three years. The company is involved in the manufacture of specialty metals, especially for the aerospace industry.(Source: www.sedc.org)

Market Growth Trends:

- The Rise of Electric Vehicles:The growing demand for lightweight materials to increase fuel efficiency, as the auto industry is the biggest user of powder metallurgy. To save battery life, the automotive industry needs ultra-lightweight parts in EVs, which is a growing trend in the market.

- 3D Printing (Additive Manufacturing): The growing use of metal powders in 3D printers and demand from aerospace and medical companies for 3D printing to print highly complex, custom parts layer by layer, like rocket engine nozzles or hip replacements, is a growing trend.

- Medical Device Production: Medical and dental fields are adopting powder metallurgy. Components like implants and surgical tools utilize metal injection molding for precise, safe fits. Which is a growing trend driving growth.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 23.97 Billion/ 3.15 Million Tons |

| Expected Size in 2035 | USD 48.51 Billion/ 6.01 Million Tons |

| Growth Rate | CAGR of 8.15% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Material, By Process, By Application, By End Use, By Region |

| Key Companies Profiled | Sumitomo Electric Industries, ATI Inc. (Allegheny Technologies), H.C. Starck Tungsten Powders, Miba AG, Hitachi Chemical Company, Kennametal Inc., BASF SE, Kymera International, Schunk Group, Proterial, Ltd., Fine Sinter Co., Ltd., Porite Corporation, JFE Steel Corporation, MolyWorks Materials Corporation, Advanced Technology & |

Powder Metallurgy Market: Innovation Through AI Integration

The integration of AI in the powder metallurgy market is a key technological shift, as it is used for material discovery, production efficiency, and quality control. It shifts manufacturing from manual, trial-and-error methods to a precise, data-driven, and automated process. Key technological shifts include predictive material design, dynamic process control, real-time defect detection, and predictive maintenance, which drive the growth of the market. For instance, AI-assisted monitoring has been shown to achieve over 99% accuracy in identifying specific internal defects in sintered metal products.

Supply Chain Analysis of Powder Metallurgy Market:

Chemical Production and Processing

- Metal powders are produced through oxide reduction, precipitation, or thermal decomposition. The powders are further mixed with binders and pressed into molds, then heated below the melting point by a process called sintering. This creates strong, complex metal parts with very little waste.

- Höganäs AB manufactures iron, steel, stainless steel, and specialty metal powders for powder metallurgy applications. Its products are widely used to produce precision components for automotive, industrial machinery, and additive manufacturing.

- Key players: Höganäs AB, GKN Powder Metallurgy, Rio Tinto Metal Powders, Miba AG

Quality Testing and Certification

- Powder metallurgy materials must comply with standards for particle size distribution, density, compressibility, mechanical strength, chemical composition, and product reliability before commercial use.

GKN Powder Metallurgy develops precision-engineered powder metallurgy components and advanced materials that comply with stringent automotive and industrial quality standards, supporting lightweight and high-performance applications - Key Authorities & Standards: International Organization for Standardization, ASTM International, Metal Powder Industries Federation, SAE International.

Distribution to Industrial Users

- Powder metallurgy products are supplied to automotive manufacturers, aerospace companies, industrial equipment manufacturers, medical device producers, electronics companies, and energy industries for precision component manufacturing.

- Miba AG supplies powder metallurgy components for automotive, industrial, and energy applications, offering high-performance sintered parts that improve efficiency, durability, and precision in demanding operating environments.

- Key players: Höganäs AB, GKN Powder Metallurgy, Miba AG.

Powder Metallurgy Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Occupational Safety and Health Administration; Environmental Protection Agency | OSHA Metal Powder Safety Standards; Clean Air Act | Worker safety, emissions control, advanced manufacturing | The U.S. promotes powder metallurgy for automotive, aerospace, medical devices, and additive manufacturing applications. |

| European Union | European Chemicals Agency; European Commission | REACH Regulation; Industrial Emissions Directive | Chemical safety, sustainable manufacturing | Europe emphasizes energy-efficient powder metallurgy processes and recyclable metal powders. |

| China | Ministry of Industry and Information Technology; Ministry of Ecology and Environment | Environmental Protection Law; Advanced Manufacturing Policies | Precision components, industrial modernization | China is expanding powder metallurgy production to support automotive, electronics, and industrial machinery sectors. |

| India | Ministry of Heavy Industries; Bureau of Indian Standards | BIS Metallurgical Standards; National Manufacturing Policies | Automotive components, industrial production | India is increasing the adoption of powder metallurgy in automotive and engineering industries to improve manufacturing efficiency. |

| Japan | Ministry of Economy, Trade and Industry | Industrial Standardization Act; Industrial Safety Regulations | High-performance metal powders, precision engineering | Japan focuses on advanced powder metallurgy technologies for automotive, aerospace, and electronics applications. |

| Germany | Federal Ministry for Economic Affairs and Energy, German Institute for Standardization | REACH Compliance; DIN Powder Metallurgy Standards | Lightweight components, additive manufacturing | Germany leads innovation in powder metallurgy for precision engineering, automotive, and industrial applications. |

Powder Metallurgy Market Dynamics

| Drivers | Restrains | Opportunities |

| Automotive Lightweighting & Electrification: | High Material Costs: | Additive Manufacturing: |

| The growing demand for lightweight and advanced materials for automotive and other industries to reduce weight drives the growth of the market. | The metal powders are very expensive as their production requires high-energy processing and complex processes, and strict quality control, which challenges the growth of the market. | Metal 3D printing relies entirely on fine metal powders. It enables you to create complex, customized parts for aerospace and medicine with almost zero material waste. |

| EV Motor Manufacturing: | Massive Equipment Investment: | Aerospace and Defense: |

| The rising demand for specialized components and soft magnetic composites, which allow electric motors to run more efficiently, drives the growth of the market. | The high setup cost, automated compactors, and high heat furnaces are major restraints to growth and also restrict small companies from entering the market. | Powder metallurgy allows the production of lightweight, heat-resistant titanium and nickel alloy parts. This reduces total aircraft weight and improves fuel efficiency. |

| Material Recycling & Sustainability: | Mechanical Limitation: | Medical Devices: |

| The PM process generates very little scrap, and it allows manufacturers to easily use recycled metal powders, which lowers both costs and environmental impact. | The default and uneven density of parts and weaker mechanical properties in comparison to traditional forging are major restraints in the growth of the market. | Biocompatible metal powders are perfect for surgical tools and custom orthopedic implants. The process ensures precise fits for patient-specific needs. |

Segmental Insights

Material Insights

The steel segment dominated the market with a 31% share in 2025 because steel is cheap, strong, and easy to get. Powder metallurgy is a process that melts metal into a fine powder and shapes it under extreme heat and pressure. This process makes "near-net-shape" parts. Think of it like baking cookies; you use exactly the dough you need instead of cutting shapes out of a giant sheet and throwing away the scraps.

For instance, Sandvik launched Osprey MAR 55, a patent-pending metal additive manufacturing tool steel powder designed specifically to "bridge the gap between maraging steels and carbon-bearing tool steels". It eliminates the traditional compromise between the weldability of carbon-free maraging steels and the performance of carbon-bearing steels.")

The titanium segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.80% in the forecast period, due to its exceptional strength-to-weight ratio, corrosion resistance, and biocompatibility. This growth is driven by rising demand from the aerospace, defense, and healthcare industries. Aircraft and defense companies use titanium powder to build lightweight, durable, and fuel-efficient engine and structural parts. Lighter planes use less fuel, which lowers both costs and carbon emissions.

Powder Metallurgy Market Share, By Material, 2025(%)

| By Material | Market Share (%) |

| Titanium | 24.00% |

| Nickel | 18.00% |

| Steel | 31.00% |

| Aluminum | 15.00% |

| Cobalt | 6.00% |

| Others | 6.00% |

Process Insights

The additive manufacturing segment dominated the market with a 39% share in 2025 and is expected to have the fastest growth with a CAGR of 12.10% in the forecast period. It lets engineers make complex, lightweight, and custom parts that are impossible to build with normal tools. Companies like GE Aviation use additive manufacturing to print complex parts, like jet fuel nozzles, using titanium powder. This drops part counts and saves major weight. 3D printing builds objects layer by layer. It only uses the exact powder needed. This cuts material waste compared to cutting parts out of a big block of metal.

") Metal Injection Molding held the market share of 34% in 2025 by combining the complex shaping of plastic molding with the strength of metal. Recent technological advancements in sintering allow MIM parts to achieve nearly 100% density, making them just as strong as traditionally forged metals. Growing applications in automotive parts and heavy investments such as facility expansions by firms like INDO-MIM drive the growth of the market.

Metal Injection Molding held the market share of 34% in 2025 by combining the complex shaping of plastic molding with the strength of metal. Recent technological advancements in sintering allow MIM parts to achieve nearly 100% density, making them just as strong as traditionally forged metals. Growing applications in automotive parts and heavy investments such as facility expansions by firms like INDO-MIM drive the growth of the market.

Powder Metallurgy Market Share, By Process, 2025(%)

| By Process | Market Share (%) |

| Additive Manufacturing | 39.00% |

| Hot Isostatic Pressing | 27% |

| Metal Injection Molding | 34% |

Application Insights

The automotive segment dominated the market with a 37% share in 2025 through cost reduction, lightweighting, and electric vehicle (EV) advancements. PM methods, like compression molding, compress metal powder into finished parts. This process cuts the total cost per part by 15 to 25% compared to traditional machining. Auto companies want lighter cars to improve gas mileage and battery range. PM uses lightweight metals like aluminum and titanium. These powders drop component weight by up to 50% while keeping the same strength.

The medical & dental segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.9% in the forecast period because it uniquely enables the production of highly customized, lightweight, and biocompatible parts. The core factors like patient-specific customization, bone integration, better healing, biocompatible materials, precision, and size drive the growth and expansion of the market.

Aerospcae Foam Market Share, By Application, 2025(%)

| By Application | Market Share (%) |

| Aerospace & Defense | 24.00% |

| Automotive | 37.00% |

| Medical & Dental | 15.00% |

| Oil & Gas | 10.00% |

| Industrial | 14.00% |

End Use Insights

The OEMs segment dominated the market with a 73% share in 2025 because OEMs use metal powder to mass-produce cheap and lightweight parts, which helps in making parts of automotive like lighter cars, increasing the efficiency of gas and battery, which drives the growth. Key reasons for growth are less waste, fast and cheap mass production, and complex shapes supporting the expansion of the market. The growing partnership between GKN Powder Metallurgy and Hoganas AB, which produces and creates custom metal powders matching their specific design goals driving growth and expansion of the market.

The AM operators segment held 27% market share in 2025 and is expected to have the fastest growth with a CAGR of 11.80% in the forecast period, driven by its ability to bridge the gap between design and production using 3D printing, fueling the growth. The segment is expanding due to several major factors like rising demand for custom parts, shift to serial production, innovations in efficiency, and regional expansion, which fuel the growth of the market.

For Instance, BLT-PrintInsight is an intelligent quality management software platform developed by Xi'an Bright Laser Technologies (BLT) for metal Laser Beam Powder Bed Fusion (PBF-LB) Additive Manufacturing. It is designed to track and manage the full 3D printing lifecycle by combining real-time monitoring with in-depth traceability.

Aerospcae Foam Market Share, By End Use, 2025(%)

| By End Use | Market Share (%) |

| OEMs | 73.00% |

| AM Operators | 27.00% |

Regional Analysis

How did Asia Pacific Dominate the Powder Metallurgy Market in 2025?

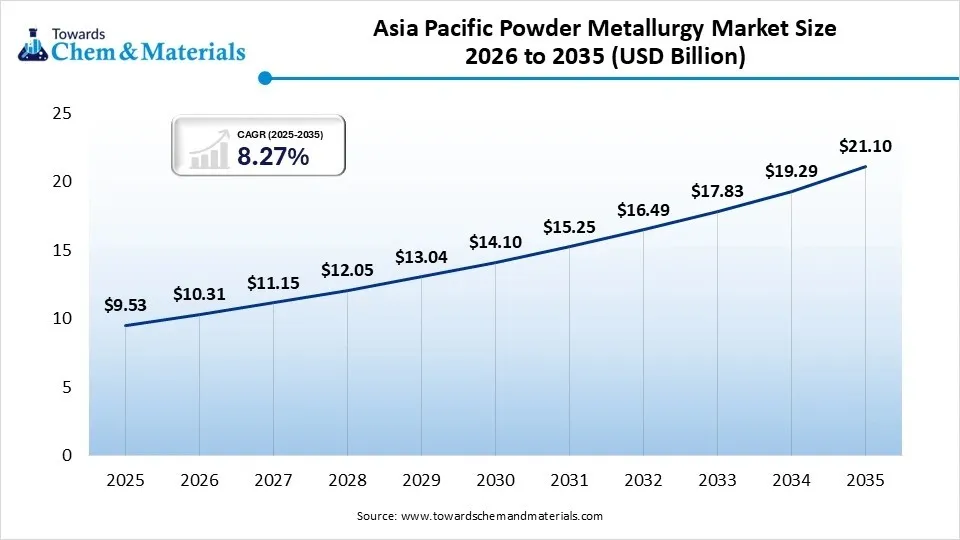

The Asia Pacific powder metallurgy market size was estimated at USD 9.53 billion in 2025 and is projected to reach USD 21.10 billion by 2035, growing at a CAGR of 8.27% from 2026 to 2035. Asia Pacific dominated the market with a share of 43% in 2025, due to the massive automotive production, rapid industrialization, and booming consumer electronics manufacturing in China, India, and Japan, which drive the growth of the market. The growing demand from factories due to the presence of major hubs and the demand for powder-based sintering to create cost-effective gears and bearings drive the growth of the market. Metal injection molding is a technology that is highly used and adopted by the Asian smartphone and consumer electronics industry, as it mass produces complex, high-precision shapes using metal powders, driving growth and expansion of the market.

")

- For instance, China’s rapid domestic expansion and aggressive export growth of New Energy Vehicles (NEVs) act as a primary driver of the global rare earth element (REE) market, allowing Beijing to tighten its vertical integration from raw mineral extraction to downstream advanced manufacturing.(Source:rareearthexchanges.com)

India

- The Indian automotive sector is the largest sector, which increases demand for lightweight materials to build lighter vehicles, supporting the growth of the market.

- The Government Make in India Push, which encourages companies to build factories in India, boosts local production, fueling demand in the market.

- The market is also growing due to demand for additive manufacturing and 3D printing. It allows aerospace and medical companies in India to create highly complex parts that traditional machines cannot make.

China

China is a major and a powerhouse for powder metallurgy, producing thousands of tons of metal powder annually, and increased demand from automotive and other sectors further fuels the production and demand.

China also has a major and cost-effective supply chain for metal powders, with the presence of major suppliers like NBTM New Materials Group and JH MIM, further reports the strong growth of the market in the region.

North America Powder Metallurgy Market Growth Factor

The North America powder metallurgy market size was estimated at USD 4.88 billion in 2025 and is projected to reach USD 10.91 billion by 2035, growing at a CAGR of 8.38% from 2026 to 2035. North America held the market share of 22% in 2025 and is expected to have the fastest growth with a CAGR of 9.40% in the forecast period. The growth of the market is driven by the need for lightweight electric vehicle (EV) parts, increased 3D printing (additive manufacturing), and high defense spending. The presence of a large aerospace and defense sector in the region, as these industries require high-performance, heat-resistant metal powders for missiles, jets, and satellites, further supports the growth of the market. Industrial automation demand is increasing, and demand for high-quality, wear-resistant gear and magnetic gears supports the growth and expansion of the market in the region.

U.S.

- The U.S. powder metallurgy market is a multi-billion-dollar industry, and raw metal and powders are produced by major suppliers, companies like ATI Inc. and Carpenter Technology Corporation.

- The major manufacturers operated heavily in the U.S. industrial Midwest, with companies like GKN Powder Metallurgy (headquartered in Detroit, Michigan) leading the global market.

- The industry is heavily supported by the Metal Powder Industries Federation (MPIF), which represents major North American powder producers, part makers, and equipment suppliers.

Canada

- The raw powder production, as Canada produces high-quality metal powders for global use, like Rio Tinto Iron and Titanium, they manufacture famous ATOMET iron and steel powders. These are used to make heavy-duty metal parts for cars and tools.

- Canadian factories mold these powders into custom parts for different industries. AMKAD Metal Components Inc. (Ontario) manufactures custom metal parts. They focus on strength and precision. TMetal Inc. (Richmond Hill, Ontario) produces powdered metal parts and specialized metal shapes.

Europe Powder Metallurgy Market Growth Factor

The Europe powder metallurgy market size was estimated at USD 5.54 billion in 2025 and is projected to reach USD 12.37 billion by 2035, growing at a CAGR of 8.36% from 2026 to 2035. Europe held a market share of 25% in 2025, due to growing demand to produce the metal powder so as to reduce waste by reusing metal powders and relying on resource-efficient processes supporting sustainability trends, which drives growth. This process is highly cost-effective and creates very little waste. Europe is a global leader in this manufacturing process, driven by major automotive, aerospace, and medical device industries. Europe's PM industry is heavily concentrated in Germany, Sweden, and the UK. These nations host massive manufacturing supply chains, ranging from raw metal powder production to final component fabrication.

UK

- The European sustainability trends and initiatives due to growing environmental concerns drive demand for powder metal to reuse it and demand from large firms, for example, the GKN PLC plant in Redditch, driving growth of the market.

- Companies like Makin Metal Powders (UK) Ltd. in Lancashire make copper and bronze powders for global shipping.

- Suppliers like William Rowland supply metals like aluminum and zinc, rising metal powder production.

Italy

- Italy has a strong presence in the powder metallurgy industry, which supplies metal powders to cars, medical tools, and bikes. Major producers include Pometon in Venice, which makes up to 80,000 metric tons of iron and non-ferrous powders yearly.

- The growth of the market is primarily driven by the demand from the automotive and aerospace sectors. Italy's advanced manufacturing sector is increasingly using 3D printing methods using metal powder, which drives the growth of the market

Latin America Powder Metallurgy Market Growth Factor

The Latin America powder metallurgy market size was estimated at USD 1.33 billion in 2025 and is projected to reach USD 3.15 billion by 2035, growing at a CAGR of 9.00% from 2026 to 2035. Latin America held a market share of 5% in 2025, due to the growing automotive production, the need for lighter metal parts and less expensive parts, and industrialization, which increases the demand for the market. Manufacturers like Dicoi S.A. (based in Buenos Aires) specialize in pressing and sintering ferrous and non-ferrous components, exporting to countries like Brazil and Mexico. Companies like Metalpó produce millions of sintered parts for domestic appliances and the automotive sector. They also use water atomization to supply copper powders to regional markets.

Brazil

- The growing investments in additive manufacturing and domestic parts lightweighting boost the demand for powder metallurgy. The key growth factors include the growing automotive need, sustainability, and cost efficiency drive growth.

- Metalpó company produces up to 120 million sintered parts yearly for alternators and other machinery. They work with carbon iron, stainless steel, and bronze.

Argentina

- The strong local automotive industry, industrial machinery needs, and 3D printing. The process uses almost 100% of the raw material. This makes it cheaper to manufacture complex items.

- The growing metal powder production and local automotive industry presence, and sustainability trends like cutting waste and lowering costs drive growth of the market.

Middle East and Africa Powder Metallurgy Market Growth Factor

The Middle East and Africa powder metallurgy market size was estimated at USD 0.89 billion in 2025 and is projected to reach USD 2.18 billion by 2035, growing at a CAGR of 9.37% from 2026 to 2035. The Middle East and Africa held a market share of 5% in 2025, due to aggressive regional government plans, expanding aerospace needs, and a strong drive for eco-friendly manufacturing, which drives the growth of the market. Governments are heavily funding local factories. For example, Saudi Arabia's Vision 2030 aims to build local auto and defense parts. These policies encourage the use of powder metallurgy. The MEA region is famous for heavy industry. Industries use hot isostatic pressing (a high-pressure heating method) to make extremely strong metal tools. These tools survive harsh desert mining and drilling conditions.

")

Saudi Arabia

- Saudi Arabia wants to move away from oil dependency by building its own manufacturing centers in cities like Riyadh, Jeddah, and Dammam. The government encourages local production of cars and aerospace parts to lower import costs.

- Additive manufacturing is a fancy term for 3D printing. In 3D printing, machines use very fine metal powders to build parts. This technology is highly popular in Saudi Arabia's defense and aerospace projects because it creates custom parts with almost zero waste.

UAE

- The UAE is localizing its defense and aerospace sectors. For instance, the local EDGE Group was awarded a $240 million contract to manufacture specialized missile components. This requires the advanced precision of powder metallurgy.

- The UAE launched the National Additive Manufacturing Strategy. This government plan gives rewards and support to factories that use 3D printing and powder metallurgy.

Recent Developments

- In April 2026, Volkmann partnered with HP Additive Manufacturing Solutions to launch vPort, a semi-automated, enclosed powder handling station for the HP Metal Jet S100 printer. The system integrates cleaning, sieving, and refilling to enhance operator safety and provide a lower-cost alternative to fully automated post-processing solutions.(Source: 3dprintingindustry.com)

- In May 2026, Euler Viewer is a free web-browser platform launched by Icelandic startup Euler to monitor metal 3D printing builds in real time. It helps operators view and analyze underutilized powder bed images to spot defects early without adding new hardware.(Source: metrology.news)

- In May 2026, Mastrex, based in Mount Laurel, New Jersey, launched the MX300, a Laser Beam Powder Bed Fusion (PBF-LB) metal additive manufacturing machine. It targets both rapid prototyping and full-scale metal part production.(Source: www.metal-am.com)

- In October 2025, Globus Metal Powders Ltd, based in Middlesbrough, UK, launched POWDER-IQ (Powder Oversight & Waste-Defence through Real-time In-line Qualification). Backed by Innovate UK, this six-month feasibility study and demonstrator aims to make metal powder processing smarter, cleaner, and more efficient.

(Source: www.metal-am.com) - In August 2025, Continuum Powders, based in Houston, Texas, announced the commercial availability of its OptiPowder M247 and M247LC (low-carbon variant) nickel-based superalloys. Historically locked behind slow and cost-prohibitive investment casting techniques, this launch adapts the high-temperature material specifically for Metal Binder Jetting and other non-laser powder bed fusion routes.(Source: www.pim-international.com)

Competitive Analysis

The key players like GKN Powder Metallurgy, Höganäs AB, Carpenter Technology Corporation, and Sumitomo Electric are major giants in the market. To stay competitive, companies are forming strategic partnerships to improve materials and production methods.

The powder metallurgy market features strong global competitors who focus on automation, lightweighting, and new alloys. Technology firms are partnering with manufacturers to introduce AI-assisted compaction and smart monitoring, which decrease part defects.

- Luxembourg-based metal powder producer AM 4 AM entered into a strategic partnership with Gränges Powder Metallurgy (GPM) to share an advanced materials testing and characterisation platform. The partnership revolves around relocating GPM’s specialized materials characterisation equipment park to the AM 4 AM facility in Foetz, Luxembourg.(Source: www.epma.com)

Top players in the Powder Metallurgy Market & Their Offerings:

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Powder Metallurgy Offerings | Key Offering/Strength |

| Höganäs AB | Global leader in metal powder production | Höganäs | Europe, North America, Asia Pacific | Iron powders, stainless steel powders, additive manufacturing powders, soft magnetic materials | Extensive metal powder portfolio with strong expertise in powder metallurgy and sustainable manufacturing |

| GKN Powder Metallurgy | Leading powder metallurgy components manufacturer | Bonn | Europe, North America, Asia Pacific | Powder metal components, metal powders, advanced sintered parts, additive manufacturing solutions | Global manufacturing footprint and expertise in precision-engineered powder metal components |

| Rio Tinto Metal Powders | Producer of ferrous metal powders | Sorel-Tracy | North America, Europe, Asia Pacific | Iron powders for automotive, industrial, welding, and additive manufacturing applications | High-quality ferrous powders with advanced atomization technologies |

| Sandvik AB | Advanced metal powder and materials supplier | Stockholm | Europe, North America, Asia Pacific | Metal powders for powder metallurgy, additive manufacturing, and cemented carbide applications | Strong innovation in high-performance metal powders and advanced materials |

| Carpenter Technology Corporation | Specialty alloy and metal powder manufacturer | Philadelphia | North America, Europe, Asia Pacific | Titanium, nickel, stainless steel, and specialty alloy powders for powder metallurgy and additive manufacturing | High-performance alloy powders for aerospace, medical, energy, and industrial applications |

Other Top Players Are

- Sumitomo Electric Industries

- ATI Inc. (Allegheny Technologies)

- H.C. Starck Tungsten Powders

- Miba AG

- Hitachi Chemical Company

- Kennametal Inc.

- BASF SE

- Kymera International

- Schunk Group

- Proterial, Ltd.

- Fine Sinter Co., Ltd.

- Porite Corporation

- JFE Steel Corporation

- MolyWorks Materials Corporation

- Advanced Technology & Materials Co., Ltd. (AT&M)

Segments Covered:

By Material

- Titanium

- Commercially Pure Titanium

- Titanium Alloys

- Nickel

- Pure Nickel Powder

- Nickel Alloys

- Steel

- Stainless Steel

- Low-Alloy Steel

- Tool Steel

- Aluminum

- Pure Aluminum

- Aluminum Alloys

- Cobalt

- Pure Cobalt

- Cobalt Alloys

- Others

- Copper

- Iron

- Tungsten

- Molybdenum

- Precious Metals

By Process

- Additive Manufacturing

- Powder Bed Fusion

- Binder Jetting

- Directed Energy Deposition

- Hot Isostatic Pressing

- Capsule HIP

- HIP Densification

- Metal Injection Molding

- Feedstock Preparation

- Injection Molding

- Debinding & Sintering

By Application

- Aerospace & Defense

- Aircraft Components

- Engine Components

- Defense Systems

- Automotive

- Powertrain

- Transmission

- Chassis

- EV Components

- Medical & Dental

- Orthopedic Implants

- Dental Implants

- Surgical Instruments

- Oil & Gas

- Valves

- Pumps

- Drilling Components

- Industrial

- Bearings

- Gears

- Filters

- Cutting Tools

By End Use

- OEMs

- Automotive OEMs

- Aerospace OEMs

- Medical OEMs

- Industrial OEMs

- AM Operators

- Service Bureaus

- Contract Manufacturers

- Research Centers

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (6)