Content

What is Duplex Stainless Steel Pipe Market Size and Share?

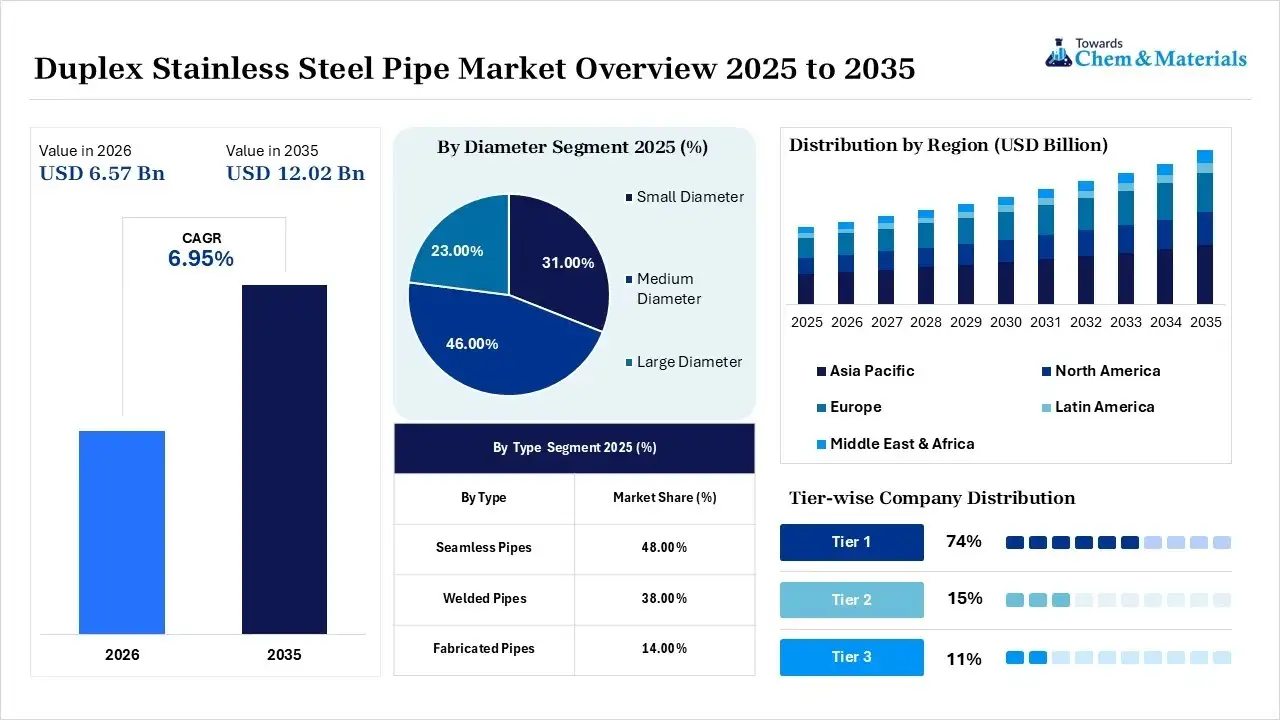

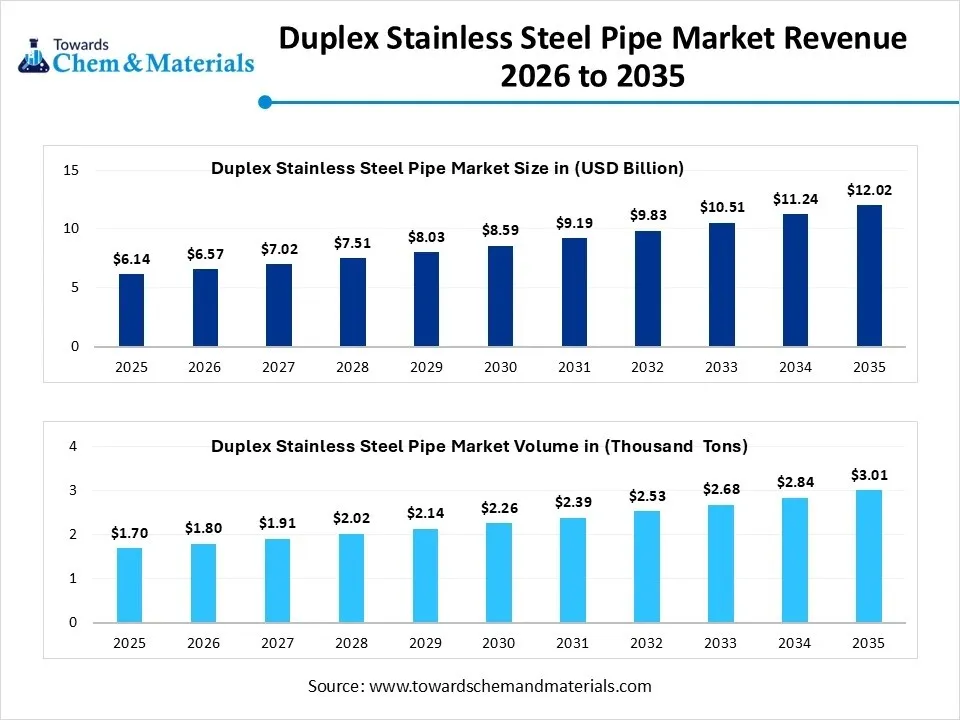

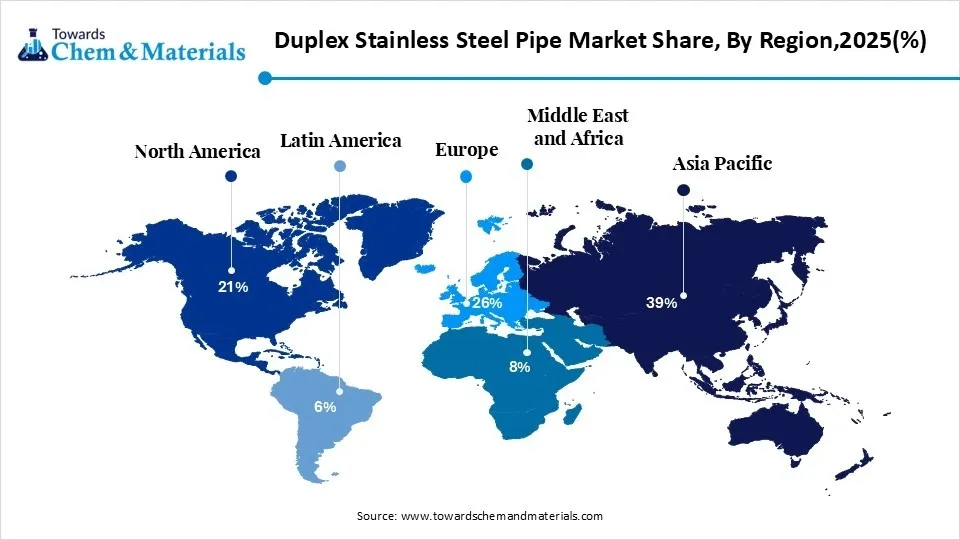

The duplex stainless steel pipe market size was valued at USD 6.14 billion in 2025, is estimated to reach USD 6.57 billion in 2026, and is projected to reach USD 12.02 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the duplex stainless steel pipe market with the largest revenue share of 39% in 2025 and is expected to grow at the fastest CAGR of 7.11% during the forecast period. In terms of volume, the duplex stainless steel pipe market is projected to grow from 1.70 million tons in 2025 to 3.01 million tons by 2035. growing at a CAGR of 5.87% from 2026 to 2035. Superior to conventional stainless steel pipes in terms of mechanical strength, excellent resistance to chloride-induced corrosion, and prolonged service life, duplex stainless steel continues to put duplex stainless steel in the spotlight for challenging applications across the globe. The growing investments in the offshore oil and gas exploration, developments in desalination and water treatment infrastructure, and growing demand for corrosion-resistant piping systems in chemical processing and power generation industries are further accelerating the growth.

Market Highlights

- By region, Asia Pacific dominated the duplex stainless steel pipe market by holding 39% share in 2025, owing to the increasing industrialization, infrastructure investments, and growing steel manufacturing capacity.

- By region, North America held 21% market share in 2025 and is expected to grow at the fastest with a CAGR of 7.8% during the forecast period, due to the growing investments in energy infrastructure and offshore developments.

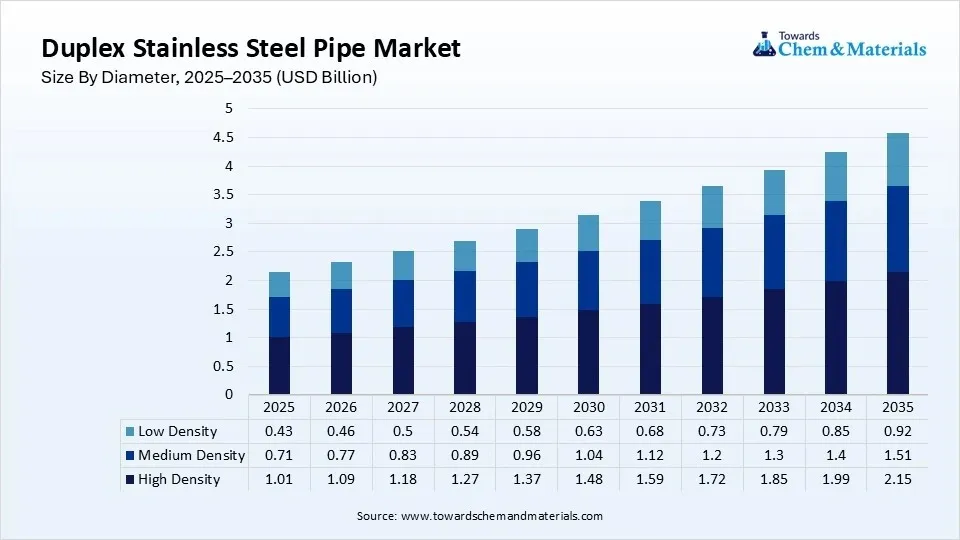

- By diameter, the medium diameter segment dominated the market with the largest share of 46% in 2025, as it is widely used in various industrial and construction applications and in oil & gas transportation systems.

- By diameter, the large diameter segment held 23% market share in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period due to the growth of pipeline projects and desalination plants.

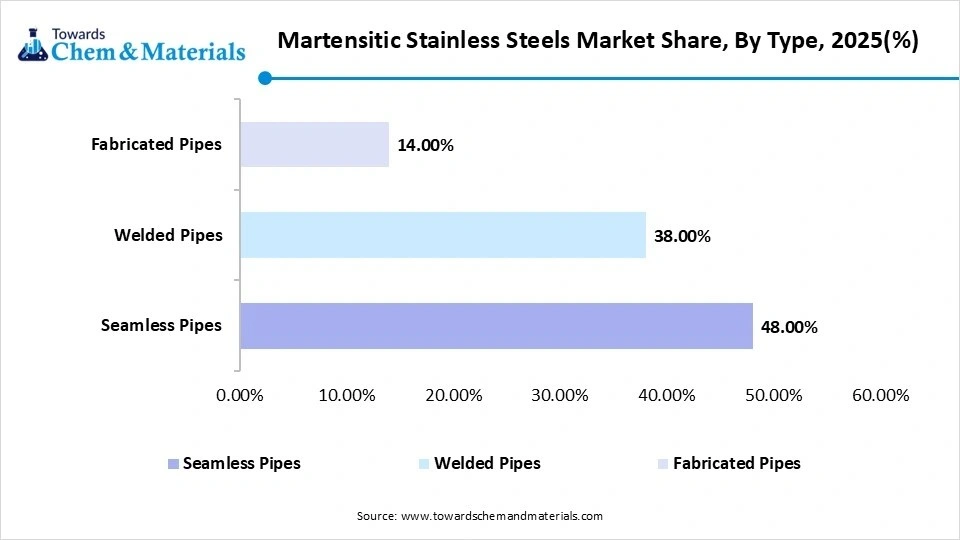

- By type, the seamless pipes segment dominated the market with the largest share of 48% in 2025, due to their high strength, reliability, and pressure resistance in critical areas of industrial use.

- By type, the welded pipes segment held 38% market share in 2025 and is expected to grow at the fastest CAGR of 7.3% over the forecast period, as technological innovations in welding and cost competitiveness are driving growth in the market.

- By application, the oil and gas segment dominated the market with the largest share of 41% in 2025, driven by increased offshore exploration and pipeline expansion activities.

- By application, the water treatment segment held 14% market share in 2025 and is expected to grow at the fastest CAGR of 7.8% over the forecast period, due to rising global investments in water treatment and desalination infrastructure.

- By end use, the construction segment dominated the market with the largest share of 49% in 2025, driven by increased demand for durable structural piping for infrastructure projects.

- By end use, the energy segment held 19% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period, driven by investments in renewable energy, carbon capture, and power generation facilities.

The numerous offshore oil and gas projects, desalination plants, chemical processing plants, and energy infrastructure projects are adding to the demand for duplex and super duplex stainless steel pipes because of their remarkable mechanical strength, corrosion resistance, and extremely long service life. The duplex stainless steel pipe market is growing at a steady pace, and the industries are increasingly opting for high-performance piping materials, which can be used under high pressure and in highly corrosive environments. The continued growth of steel production and infrastructure work will further drive the demand for duplex stainless steel products in various end-use industries in the long term.

- For instance, in 2026, India's crude steel output hit 14.09 million tonnes in April, with finished steel demand rising 8.1% year-over-year, bolstered by robust demand from construction, infrastructure, and manufacturing industries, driving future duplex stainless steel pipe consumption.(Source: www.pib.gov.in)

Ongoing product improvements and enhancements in alloy development, automated welding technology, exact heat treatment, and sustainable steel production continue to optimize product performance and lifecycle costs. Furthermore, the increasing hydrogen production, carbon capture facilities, and renewable energy projects are opening up new opportunities for duplex stainless steel piping solutions in various industrial segments around the world.

Global Investment Movement for Duplex Stainless Steel Pipe Market

Across Asia Pacific and the Middle East, investments are being made in new petrochemical complexes, refineries, and specialty chemical manufacturing plants, all in the wake of a fast-paced industrialization. These facilities demand very reliable piping systems that are able to run at high temperatures, in harsh chemical environments, and in continuous industrial processing.

- Industrial piping systems are another example of the enhanced faith in advanced engineering infrastructure being enjoyed by the markets. For instance, in June 2026, DEE Development Engineers won process piping contracts valued at more than ₹170 crore in India and Thailand, boosting its manufacturing prowess in the energy and industrial infrastructure sectors, and meeting the growing demand for advanced piping solutions.(Source: themachinemaker.com)

There is a significant rise, from the government, in investments in water treatment facilities, including desalination plants, wastewater recycling facilities, and water infrastructure in the industrial sector, in water-stressed regions. Ideal for reverse osmosis systems, seawater intake pipelines, and high-pressure desalination, duplex stainless-steel pipes provide excellent resistance to chloride induced corrosion and biofouling.

Market Trends

- Investments in desalination plants and the use of advanced water treatment facilities are increasing at an accelerating rate in response to global water scarcity. As a result of these properties, duplex stainless-steel pipes have been adopted as the preferred material choice due to their outstanding resistance to chloride corrosion, high strength, and durability in continuous exposure to highly saline operation environments.

- While oil and gas continue to be the dominant application areas, duplex stainless steel pipes are being used more and more in offshore wind, geothermal, hydrogen production, and carbon capture systems. Their durability under extreme operating conditions helps to facilitate the shift towards clean and sustainable energy systems.

- Manufacturers are increasing the range of product offerings to accommodate lower cost grades for infrastructure applications and higher corrosion resistance grades for highly corrosive industrial applications, lean duplex grades, and super duplex alloys, respectively. This variety allows end users to maximize lifecycle performance and project economics based on several applications.

- As technologies like laser welding continue to develop and improve, production efficiency is constantly improved, and defects and manufacturing costs are reduced. The technological developments are making it possible to use duplex stainless steel pipes in an increasing number of industrial processes, construction, marine engineering, and transportation infrastructure.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 6.57 Biilion/ 1.80 Million Metric Tons |

| Market Size by 2035 | USD 12.02 Billion/ 3.01 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 6.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Diameter, By Type, By Application, By End Use Industry, By Region |

| Key Profiled Companies | Jindal Stainless, Sumitomo Corporation, Special Piping Materials, Pankh Stainless India, Alleima, Mukesh Steel India, Supreme Steel & Engineering Co., Relinox Stainless, SMM Industries LLP, Youfa Group, Kalp Alloys, Kanak Metal |

Key Technological Shifts in the Duplex Stainless Steel Pipe Market

Stainless steel manufacturers keep experimenting with new grades that offer increased corrosion resistance, tensile strength, and extended service life over standard grades of stainless steels, such as lean duplex stainless steel, super duplex stainless steel, and hyper duplex stainless steel. The advanced alloys are finding new uses in the offshore energy, desalination, chemical processing, and hydrogen infrastructure sectors.

Laser welding, orbital welding, and robotic fabrication technologies are rapidly being taken up in the industry in order to enhance the quality of the welds, reduce heat-affected zones, and maintain an adequate ferrite-austenite structure, which is essential for high performance in mechanical properties and corrosion resistance. Customized duplex stainless steel parts are being manufactured using Wire Arc Additive Manufacturing (WAAM) and Laser Powder Bed Fusion (L-PBF) technologies with minimal material loss. These technologies are applicable to very specific uses in the aerospace, nuclear power, chemical processing, and high-tech manufacturing industries.

Supply Chain Analysis of the Duplex Stainless Steel Pipe Market

Feedstock Procurement

- The supply chain starts with the sourcing of key raw materials like iron ore, chromium, nickel, molybdenum, manganese, and nitrogen from the world's leading mining companies.

- These alloying elements affect the corrosion resistance, mechanical properties, weldability, and durability of duplex stainless steel pipes.

- Glencore: A supplier of high-quality nickel, chromium, and other alloying metals that aid in duplex stainless steel production across the globe.

- Other Key Players: Vale, Anglo American, BHP.

Chemical Synthesis and Processing

- The raw materials are melted, refined, and alloyed with the help of an electric arc furnace and argon oxygen decarburization technology.

- Controlled heat treatment is used to create the balanced ferritic-austenitic microstructure, which contributes to the superior mechanical properties of duplex stainless steel.

- Outokumpu: Advanced refining technologies and high recycled stainless steel (RSS) content in major player grades are used in the production of premium duplex stainless steel grades.

- Other Key Players: Acerinox, Sandvik, Nippon Steel.

Compound Formulation and Blending

- Hot rolling, cold drawing, extrusion, and precision welding processes are used to transform the refined duplex stainless steel into seamless and welded pipes.

- Manufacturers' solution anneal, pickle, straighten, dimensionally calibrate, and conduct non-destructive testing prior to commercial distribution.

- Tubacex: Produces seamless duplex and super duplex stainless steel tubular products for use in extremely challenging industrial and energy applications.

- Other Key Players: Tenaris, Vallourec, Valinox

Regulatory Framework: Duplex Stainless Steel Pipe Market

| Region | Regulatory Body | Key Regulation | Regulatory Focus |

| Asia Pacific | Bureau of Indian Standards (BIS), Standardization Administration of China (SAC) | IS 6911, GB/T Stainless Steel Standards | Regulates manufacturing quality, corrosion resistance, and safety requirements for industrial stainless steel pipe applications. |

| North America | ASTM International, American Society of Mechanical Engineers (ASME) | ASTM A790/A790M, ASME Boiler and Pressure Vessel Code (BPVC) | Establishes pressure vessel standards, corrosion performance, product quality, mechanical strength, and safe industrial piping system operations. |

| Europe | European Committee for Standardization (CEN), European Commission | EN 10216-5, Pressure Equipment Directive (PED 2014/68/EU) | Ensures CE compliance, manufacturing consistency, pressure equipment safety, quality assurance, and reliable performance across industrial piping applications. |

Types of Duplex Stainless Steel Pipes:

Lean Duplex

Lean duplex stainless steel is characterized by lower Ni and Mo content that is an economical choice with high mechanical strength and corrosion resistance. It is being used widely in structural engineering and industrial construction applications, as well as in storage tanks and bridges.

Standard Duplex

The duplex microstructure of standard duplex stainless steel gives rise to a range of excellent properties, such as strength, corrosion resistance, and durability. It is extensively used in oil and gas pipelines, pressure vessels, marine equipment, and chemical processing plants.

Super Duplex

Super duplex stainless steel is used in areas where there is a high chromium and molybdenum content, providing a high resistance to chloride corrosion and high pressure. It is extensively used in offshore oil rigs, subsea pipelines, desalination plants, and marine structures.

Hyper Duplex

The hyper duplex stainless steels are high-alloy advanced materials designed to function in very corrosive environments. It offers excellent corrosion resistance, strength, and durability, and is appropriate for deep-water offshore, chemical processing, and highly acidic applications.

Market Dynamics

Drivers

Investments In Energy and Industrial Infrastructure

The increased exploration of the offshore oil and gas fields is still driving demand for duplex stainless steel pipes in global energy infrastructure projects. The desalination industry and chemical industries demand more and more corrosion-resistant piping systems that can perform under harsh environmental conditions. The modernization of infrastructure further promotes adoption throughout industrial processing, marine engineering, and commercial construction. They have a long life span and have comparatively low maintenance needs, which makes their lifecycle performance better for end users.

Restraints

Complicated Manufacturing Processes

To keep the duplex steel balanced ferritic-austenitic structure, the alloy composition and careful heat treatment are required. To maintain the mechanical strength and resistance to corrosion, special welding techniques and highly qualified technical personnel are necessary for the fabrication process. The more complicated the production, the higher the manufacturing costs are relative to conventional stainless steel products. These factors can limit the adoption of these projects in industrial and infrastructure sectors, where costs are important considerations.

Opportunities

New Opportunities in The Field Of Hydrogen Infrastructure And Desalination Projects

Worldwide, duplex stainless steel pipes have been gaining more and more interest in hydrogen production and carbon capture, as well as in desalination applications. The industries demand piping systems that can withstand corrosion, pressure, and a hostile chemical environment for longer periods of time. Lean duplex grades are also an economic option for commercial infrastructure and industrial processing plants. Long-term market opportunities are likely to be available in various end-use sectors due to the rising investments in sustainability.

Segmental Insights

Diameter Insights

The medium diameter segment dominated the market with the largest share of 46% in 2025, as these pipes are widely employed in oil and gas transmission systems, chemical processing and refining plants, water treatment plants, and in industrial manufacturing plants. They provide a perfect combination of pressure handling, structure strength, installation flexibility, and overall project cost effectiveness. They are known to be compatible with various industrial uses worldwide, making them the choice of engineering contractors. The industrial infrastructure, pipeline modernization, and process industries investment are expected to keep control of the segment over the forecast period.

The large diameter segment held the 23% market share in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period, due to cross-country pipeline investments, offshore oil and gas developments, and desalination plants. The pipes are very efficient for high-pressure and highly corrosive operating conditions in order to convey a large volume of fluid. Demand continues to rise rapidly as developed and emerging economies embark on more energy security and water infrastructure projects. The growing use of pipelines in industries will present long-term growth opportunities for manufacturers.")

Type Insights

The seamless pipes segment dominated the market with the largest share of 48% in 2025, owing to the high-pressure resistance, superior mechanical strength, and performance in harsh industrial environments. They are extensively used in offshore drilling rigs, petroleum refinery and processing plants, power generation, and chemical plants where a high degree of operational reliability is desired. Reduced maintenance needs and longer service life further enhance lifecycle economics for industrial operators. Seamless duplex stainless steel pipes are still in demand as investment in energy infrastructure continues.

- For instance, in July 2026, SMS Group won the contract for installing two seamless tube rolling lines in China from Baosteel Steel Pipe. The project will increase the capacity of premium seamless pipe production and meet the growing market demand for high-end tubular solutions in the industrial field.(Source: www.sms-group.com)

The welded pipes segment held the 38% market share in 2025 and is expected to grow at the fastest CAGR of 7.3% over the forecast period. The continuous development of laser welding, orbital welding, and automatic inspection technology has brought great convenience to product quality and manufacturing efficiency. These innovations not only lower production costs but also extend the use of innovations in construction, industrial processing, and infrastructure development projects. Better weld integrity and dimensional accuracy also boost customer confidence in welded duplex pipe solutions. Long-term segment growth continues due to the continued expansion of manufacturing investments.

")

- For instance, in May 2026, with the first production of API 5L X100 welded pipes, ArcelorMittal Nippon Steel India (AMNSI) became the first Indian steel company to produce the pipes. The innovation helps to reinforce offshore, marine, and high-pressure engineering applications with superior manufacturing capabilities.(Source: www.manufacturingtodayindia.com)

Application Insights

The oil and gas segment dominated the market with the largest share of 41% in 2025, as the piping systems must withstand high levels of corrosion under severe conditions for offshore drilling platforms, subsea pipelines, LNG terminals, and refinery operations. Duplex stainless steel pipes are characterized by excellent durability, chloride resistance, superior mechanical strength, and pressure resistance in chloride rich environment. They have a long life span that helps to lower the maintenance cost and unplanned downtime of critical energy infrastructure.

- In July 2025, Centravis announced two modernization projects in July of 2025, both with a total cost of US$14.5 million to increase the production of seamless pipes with corrosion resistance. The investment is for developing and expanding carbon capture technologies and other advanced oil and gas applications in the United States and Europe. (Source: odessa-journal.com)

The water treatment segment held the 14% market share in 2025 and is expected to grow at the fastest CAGR of 7.8% over the forecast period. Worldwide, investments in desalination plants, municipal water systems, and industrial wastewater treatment are gaining momentum, promoting the adoption of the product. Duplex stainless steel pipes exhibit outstanding corrosion resistance to chloride, biofouling, and aggressive chemicals. They have a long operating life, which means that they have low maintenance requirements in high salinity operating conditions. The global growth of water infrastructure projects is anticipated to drive continued strong market growth.

End Use Insights

The construction segment dominated the market with the largest share of 49% in 2025, due to its outstanding resistance to corrosion and durability. Duplex stainless steel pipes are being used more and more in commercial buildings, bridges, industrial facilities, and public infrastructure. They are highly mechanically strong, resulting in a longer service life and lower maintenance/replacement costs. Increased urbanization and government investments in infrastructure are still fueling demand for residential and non-residential construction. The use of sustainable construction methods further promotes the use of long-lasting stainless steel piping systems.

The energy segment held the 19% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period. Advanced corrosion-resistant piping solutions are needed for renewable energy, hydrogen production, carbon capture, and offshore power projects. Duplex stainless steel pipes may work reliably for long periods of time under high pressure and a harsh environment. Further growth in investment in decarbonisation and clean energy infrastructure remains to support the long-term growth of the market.

- In June 2026, SeAH Steel, a provider of high-value steel pipes to a project for carbon capture, utilization, and storage (CCUS) that is backed by the UK government in June 2026. The project reinforces the company's footing in the decarbonized energy infrastructure and broadens the use of advanced piping systems.(Source: www.asiae.co.kr)

Regional Insights

How Did the Asia Pacific Dominate the Duplex Stainless Steel Pipe Market In 2025?

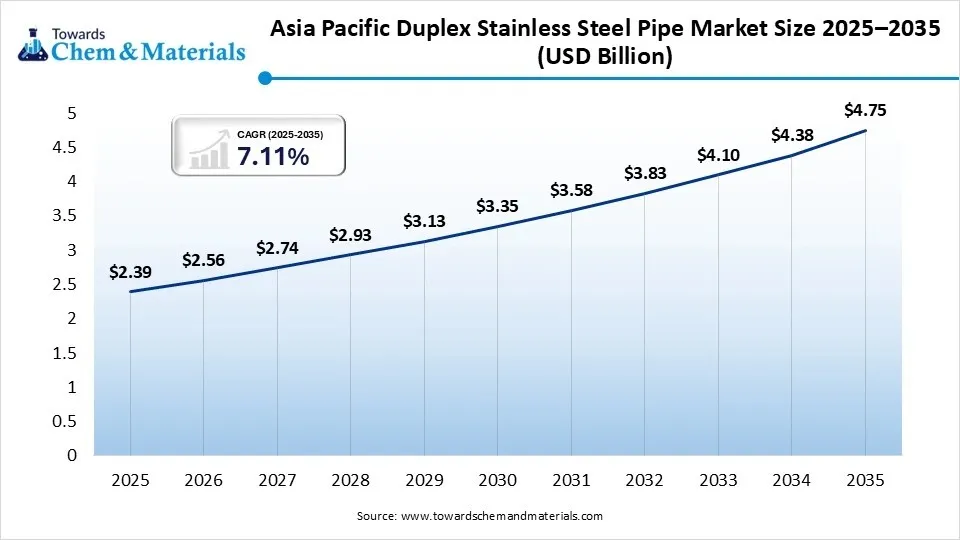

The Asia Pacific duplex stainless steel pipe market size was estimated at USD 2.39 billion in 2025 and is projected to reach USD 4.75 billion by 2035, growing at a CAGR of 7.11% from 2026 to 2035. Asia Pacific dominated the market with the largest share of 39% in 2025. Industrialization, oil and gas development, and desalination and chemical processing investment provided a boost to the region's development. China, India, Japan, and South Korea are pushing ahead with their own stainless steel production capacities. In addition, government investment in energy security, industrial modernization, and transportation infrastructure is promoting demand for corrosion-resistant piping solutions across the region.

") China

China

- China continued to be the major market participant in the Asia Pacific region due to its large stainless steel production capacity and development of the industrial infrastructure. Investments in the development of petrochemical plants, LNG terminals, desalination plants, and chemical processing plants are continuing to result in product demand.

- The country is also scaling up the production of high-value duplex stainless steel to cater to some of its local demand and for exports. Industrial modernization is also supported by government-backed programs, which help boost the long term growth of the market.

India

The demand for duplex stainless steel pipes is also growing in India as a result of the growing investment in refinery expansion in India, water infrastructure projects, and industrial manufacturing projects. Domestic government initiatives to promote domestic steel production and infrastructure modernization are ongoing and are also creating new market opportunities. Urbanization and increased energy projects are also seeing these being used more widely throughout the industry.

- For instance, in August 2025, Rhinox began operations at a new 11-acre, stainless steel pipe manufacturing plant in Haryana. The cutting-edge plant boosts the country's production capacity and caters to the growing demand for precision-made stainless steel piping systems in various industrial applications.(Source: infra.economictimes.indiatimes.com)

North America

The North America duplex stainless steel pipe market size was estimated at USD 1.29 billion in 2025 and is projected to reach USD 2.58 billion by 2035, growing at a CAGR of 7.18% from 2026 to 2035.North America held 21% market share in 2025 and is expected to grow at the fastest CAGR of 7.8% during the forecast period. The projects started with increased investments in LNG infrastructure, hydrogen production, desalination, and carbon capture, and continue to support regional demand. Adoption is also spurred by strict industrial safety standards and the increasing number of replacements for aging pipeline infrastructure. Long-term market growth is expected to be sustained by increasing use in the energy, water treatment, and chemical industries.

United States

The United States is the biggest regional market due to the presence of a large number of oil and gas exploration activities, a high level of petrochemical processing, and advanced manufacturing. Carbon capture technology, hydrogen infrastructure, and offshore energy projects have seen continued investment to support the demand for corrosion-resistant piping systems. Market growth is further bolstered by infrastructure modernization programs and stringent industrial standards across multiple industries.

Canada

Canada's use of duplex stainless steel pipe increases as investments are made in the oil sands, LNG export facilities, mining, and water treatment plant projects. The development of energy transition and industrial modernisation processes is leading to a broader use of corrosion-resistant piping systems. The projected growth in capital expenditure in various resource-based industries will help drive stable market growth.

Europe

The Europe duplex stainless steel pipe market size was estimated at USD 1.60 billion in 2025 and is projected to reach USD 3.19 billion by 2035, growing at a CAGR of 7.14% from 2026 to 2035.Europe held 26% market share in 2025, owing to its rich industrial heritage and dedicated commitment to sustainable infrastructure. Increasing investments in renewable power, offshore wind, hydrogen, and chemical processing are continuing to drive market demand. Environmental laws are strict and require industries to use pipe materials that will last long and resist rust. Regional manufacturers are also carrying on investing in advanced stainless steel production technologies.

Germany

Germany continues to be one of the biggest markets in Europe, thanks to its robust engineering sector, industrial manufacturing prowess, and plans for infrastructure modernization. The demand for high-performance stainless steel piping solutions is ongoing in chemical processing, energy infrastructure, and bridge construction applications. The ongoing investment in sustainable industrial development further supports market growth over the long run.

- For instance, in December 2025, Interpipe provided 300 tons of stainless steel pipes for a bridge construction over the Saale River in Germany. The project points to the increasing need for quality pipe solutions for the major infrastructure projects in Europe.(Source: interpipe.biz )

France

France is still rolling out duplex stainless steel pipe applications in nuclear power, the chemical industry, desalination, and industrial plants. Long-term product adoption is fostered by the government's efforts on sustainable industrial development and energy transition. A growing number of water treatment and high-tech manufacturing plants also support the growth of the regional market.

Latin America

The Latin America duplex stainless steel pipe market size was estimated at USD 0.37 billion in 2025 and is projected to reach USD 0.78 billion by 2035, growing at a CAGR of 7.74% from 2026 to 2035.Latin America held 7% market share in 2025, with growing investments in offshore energy production, industrial infrastructure, and mining. The continued growth of desalination initiatives and the modernization of water treatment plants are driving an ongoing demand for corrosion-resistant pipes. The governments are also pushing infrastructure initiatives to make industries more productive and efficient at resource utilization. Market growth is likely to be boosted by an increase in foreign investments.

") Brazil

Brazil

Brazil is a leader in the region's oil production, especially in the offshore sector, as well as in the processing of petrochemicals, mining, and industrial manufacturing. Demand for durable stainless steel piping systems remains strong as infrastructure development and expansion of energy sector activities continue to grow. Premium duplex stainless steel products are also developed through the modernization of industrial facilities.

Chile

The use of duplex stainless steel pipes is steadily rising in Chile in the fields of industrial water management, desalination plants, and mining operations. Copper production is increasing, and infrastructure needs for sustainable development are driving demand for piping solutions that have exceptional corrosion resistance. The market is projected to experience steady growth throughout the forecast period as a result of the expansion of industrial development.

Middle East & Africa

The Middle East & Africa duplex stainless steel pipe market size was estimated at USD 0.49 billion in 2025 and is projected to reach USD 1.02 billion by 2035, growing at a CAGR of 7.74% from 2026 to 2035.The Middle East & Africa held 7% market share in 2025, driven by the growing desalination capacity and investments in oil & gas in the region. The demand for duplex stainless steel pipes is still being supported by the rapid diversification of industries and the modernization of infrastructure in the region. As water security efforts continue to proliferate more and more, so do the numbers of desalination and wastewater treatment installations. The market is anticipated to grow as a result of increased investments in energy and industrial projects.

Saudi Arabia

Saudi Arabia remains heavily pursuing the development of desalination facilities, petrochemical production, hydrogen initiatives, and industrial diversification efforts. It is definitely a tremendous boost in the demand for corrosion-resistant duplex stainless steel piping systems in critical infrastructure applications. The investments for Vision 2030 will further boost long-term market expansion.

South Africa

The durability of pipes is becoming more important in South Africa with the growth of demand for them in projects such as mining, water treatment, chemical processing, and industrial infrastructure. Investment in the modernization of industries and the development of resources continues to drive market growth in various industries. During the forecast period, opportunities are likely to increase with the rising adoption of advanced stainless steel products.

Competitive Analysis

The overall market is moderately fragmented, and major industries are competing with each other through product innovation, capacity expansion, strategic partnerships, and investments in advanced manufacturing technologies. Businesses are developing high-performance seamless and welded duplex pipes for critical applications in oil & gas, desalination, chemical processing, hydrogen, and renewable energy businesses. Other sustainability programs, automation, and production efficiency enhancements are emerging as important competitive differentiators as well. As these market participants expand their distribution networks across the globe, they are also adding manufacturing capabilities to address the rising demand for corrosion-resistant piping.

- In June 2026, On June 2026, Alleima opened the production facility Tube Mill 2026 in Sandviken, SEK 330 million invested. The expansion will enable Alleima to meet growing worldwide demand for traditional nuclear reactors, as well as for small modular reactors (SMR), and boost the company's market share in high-performance stainless steel tubing.(Source: www.alleima.com)

- In May 2026, Youfa Group put the F700 high-frequency ERW pipe mill and the ultra-large diameter spiral pipe production line into operation in Jiangsu, China. This investment greatly boosts the manufacturing capability, anti-corrosion capability, and production capacity of large-diameter welded pipe for overseas infrastructure projects. (Source: www.youfasteelpipe.com)

Recent Developments

- In May 2026, Tenaris confirmed the purchase of Artrom Steel Tubes S.A.'s seamless steel pipe business in Romania. The buy adds Tenaris' uninterrupted pipe manufacturing presence in Europe and reinforces its ability to meet the needs of energy, industrial, and infrastructure customers for high-performance tubular products. (Source: ir.tenaris.com)

Top Players in the Market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Duplex Stainless Steel Pipe Offerings | Key Offering/Strength |

| Outokumpu | Market Leader | Finland | Global | Duplex and super duplex stainless steel pipes | Sustainable stainless steel production and advanced corrosion-resistant grades |

| Sandvik | Premium Manufacturer | Sweden | Global | High-performance seamless duplex tubes | Advanced materials for extreme industrial environments |

| Acerinox | Leading Stainless Steel Producer | Spain | Global | Duplex stainless steel products | Wide product portfolio and global manufacturing network |

Other Key Players

- Jindal Stainless

- Sumitomo Corporation

- Special Piping Materials

- Pankh Stainless India

- Alleima

- Mukesh Steel India

- Supreme Steel & Engineering Co.

- Relinox Stainless

- SMM Industries LLP

- Youfa Group

- Kalp Alloys

- Kanak Metal

Segment Covered in the Report

By Diameter

- Small Diameter

- Below 2 inches

- 2–6 inches

- Medium Diameter

- 6–12 inches

- 12–24 inches

- Large Diameter

- Above 24 inches

- Heavy-wall Large Diameter

By Type

- Seamless Pipes

- Hot Finished

- Cold Finished

- Welded Pipes

- ERW Pipes

- TIG Welded

- Laser Welded

- Fabricated Pipes

- Custom Fabricated

- Heavy Industrial Fabricated

By Application

- Oil and Gas

- Upstream

- Midstream

- Downstream

- Chemical Processing

- Petrochemical Plants

- Fertilizer Plants

- Industrial Chemicals

- Water Treatment

- Desalination

- Municipal Water

- Industrial Water

- Power Generation

- Thermal Power

- Nuclear Power

- Renewable Energy Plants

- Marine

- Shipbuilding

- Offshore Platforms

- Port Infrastructure

By End Use Industry

- Construction

- Commercial Buildings

- Infrastructure

- Automotive

- Exhaust Systems

- Structural Components

- Aerospace

- Hydraulic Systems

- Aircraft Structures

- Energy

- Oil & Gas Infrastructure

- Renewable Energy

- Power Plants

- Food and Beverage

- Dairy Processing

- Beverage Plants

- Food Processing Equipment

By Regions

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (6)