Content

What is the Metal Abrasives Market Size and Share?

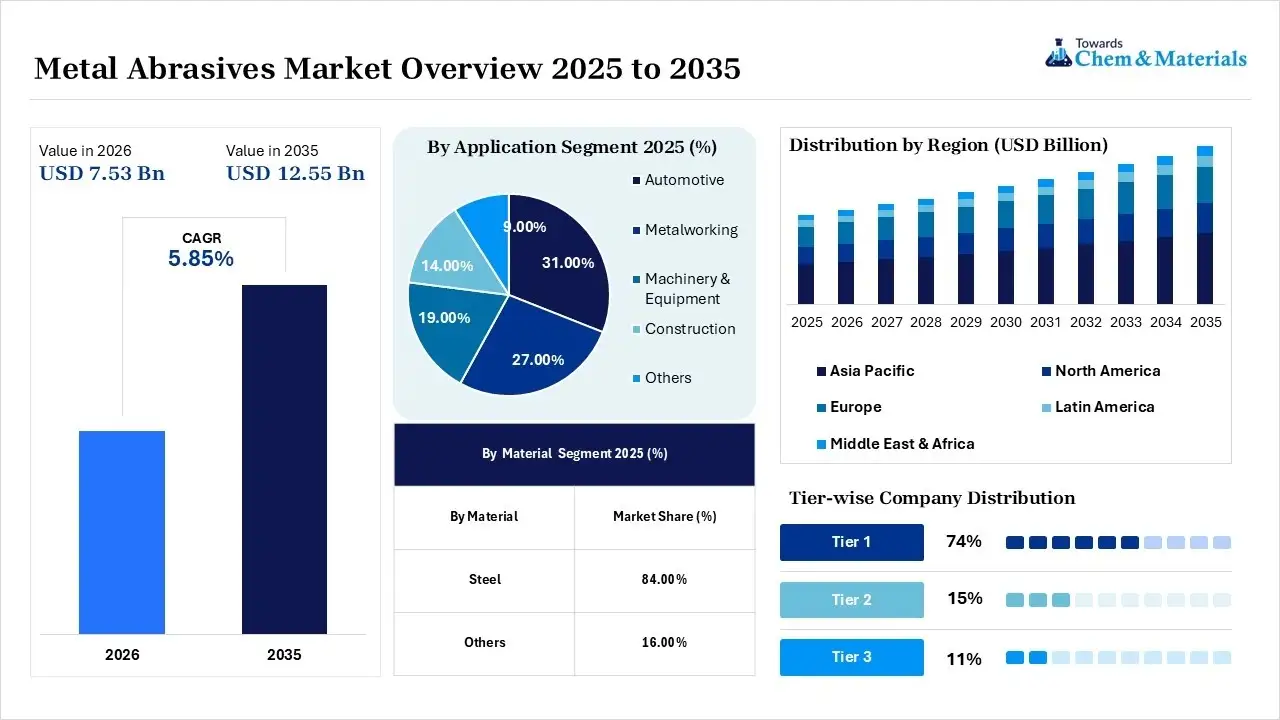

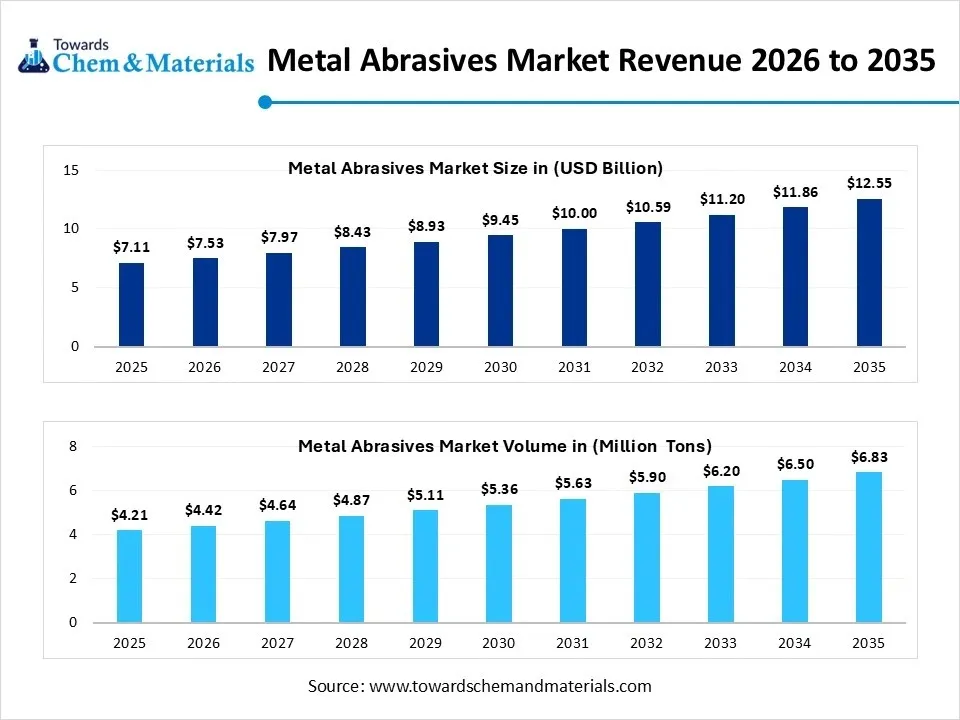

The global metal abrasives market size was valued at USD 7.11 billion in 2025, is estimated to reach USD 7.53 billion in 2026, and is projected to reach USD 12.55 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the metal abrasives market with the largest revenue share of 45% in 2025 and is expected to grow at the fastest CAGR of 5.96% during the forecast period. In terms of volume, the metal abrasives market is projected to grow from 4.21 million tons in 2025 to 6.83 million tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035.The increasing demand for precision surface preparation is the key factor driving market growth. Also, the surge in vehicle production globally coupled with the rise in industrial infrastructure projects in emerging economies can fuel market growth further.

Market Highlights

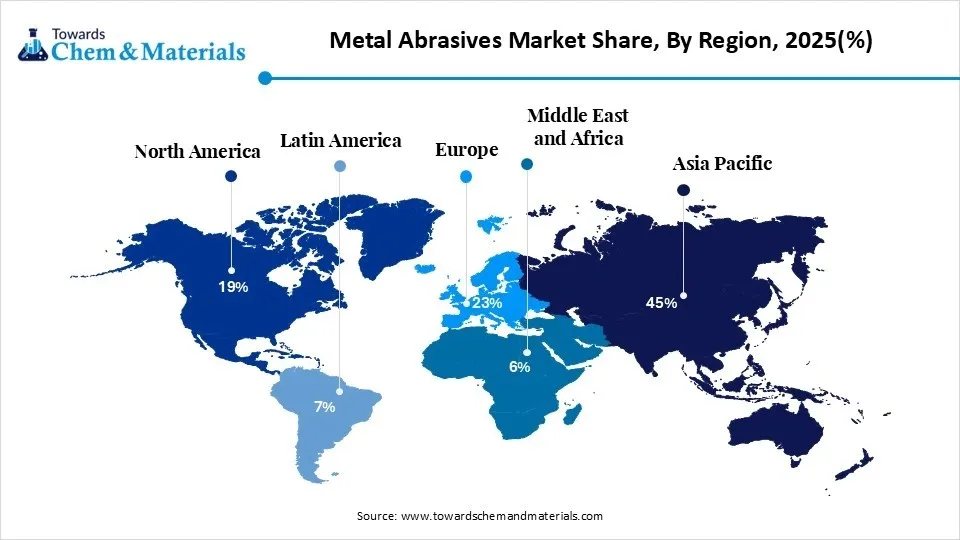

- By region, Asia Pacific dominated the market with the largest share of 45.0% in 2025. The dominance of the region can be attributed to the ongoing urbanization, extensive automotive manufacturing, and expanding infrastructure.

- By region, North America held a market share of 19% in 2025 and was expected to grow at the fastest CAGR of 6.80% over the forecast period. The growth of the region can be credited to the growing defense and aerospace manufacturing.

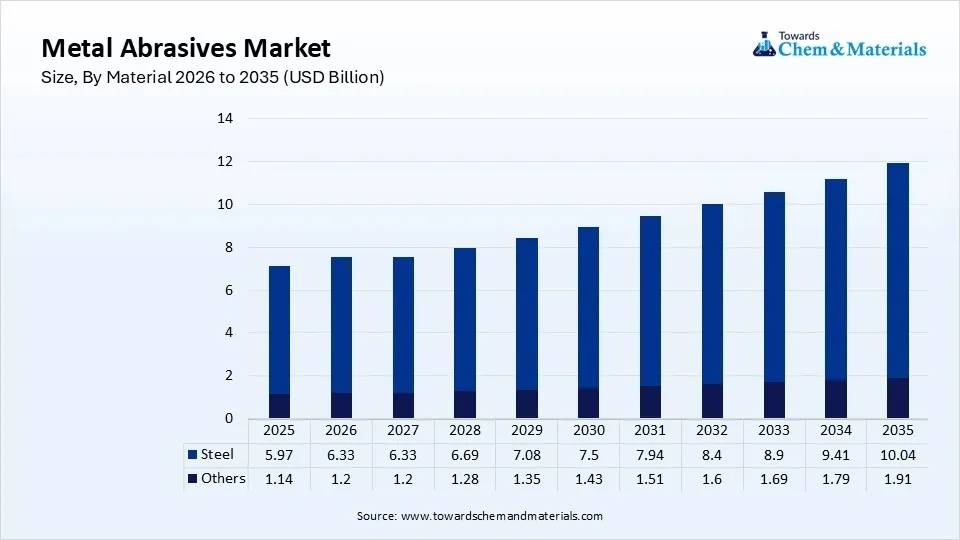

- By material, the steel segment dominated the market with the largest share of 84% in 2025. The steel is largely preferred over non-metallic alternatives because of its ability to be recycled multiple times without losing its abrasive efficacy.

- By material, the others segment held the market share of 16.0% and is expected to grow at the fastest CAGR of 6.50% over the forecast period. This segment encompasses non-steel metallic and mineral abrasives, which are important for specialized surface finishing.

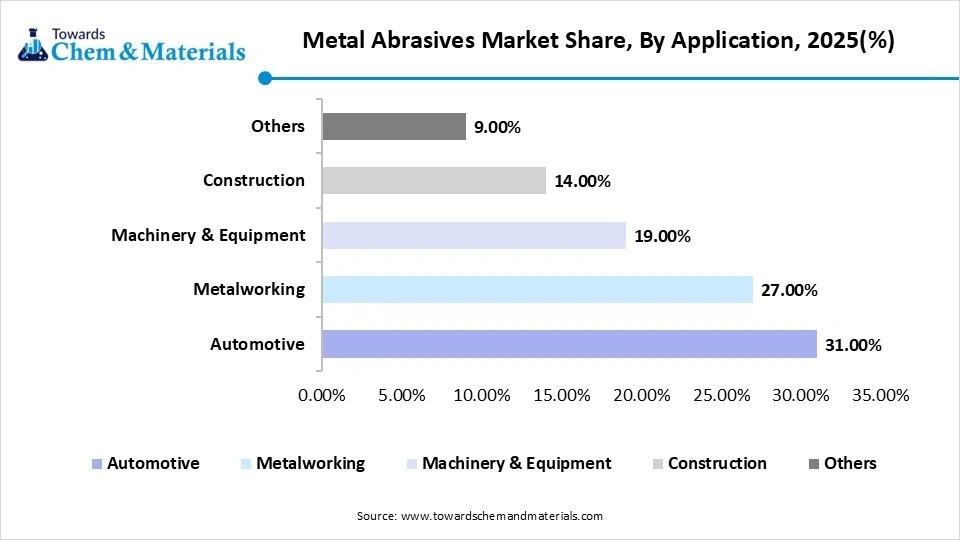

- By application, the automotive segment dominated the market with the largest share of 31.0% in 2025. The metal abrasives are crucial for shaping body panels, finishing powertrain components, and surface preparation before painting.

- By application, the metalworking segment held a market share of 27% in 2025 and is expected to grow at the fastest CAGR of 6.70% over the forecast period. This segment depends heavily on processes such as cutting, grinding, deburring, and surface cleaning.

The market is witnessing a notable growth because of the surge in production and industrial activity in various parts of the world. This demand is also rising as plants are increasingly implementing modern machines and automation systems.

- In October 2025, Everett Industries LLC introduced a 72-hour expedited shipping program for its 10-inch bench and 14/16-inch floor abrasive cutoff saws. To facilitate this rapid dispatch from the Warren, Ohio, manufacturing center, the units are kept preassembled and thoroughly factory tested.(Source: www.thefabricator.com)

Emerging economies are heavily investing in industrial infrastructure and improving domestic manufacturing capabilities.

Global Investment Flow for Metal Abrasives 2025

Major market players are increasingly investing in sustainable, closed-loop blasting and shot-peening technologies to minimize hazardous waste and emissions. These investments are mainly fueled by ESG policies, process efficiency, and automation.

- In 2025, the United States exported $567M of abrasive powder, being the 362nd most exported product in the United States. The major destinations of the United States' abrasive powder exports were Germany ($132M), Canada ($105M), Mexico ($94.5M), China ($37.4M), and Japan ($19.4M).(Source: oec.world)

Hence, investments are majorly concentrated on supplying these to the automotive, aerospace, and general manufacturing industries.

Metal Abrasives Market Trends

- The growing product demand from the automotive sector is the latest trend in the market shaping positive market growth. The sector is increasingly generating demand for its extensive use of grinding, polishing, and finishing equipment in production and maintenance operations.

- In recent years abrasives are finding a wide range of applications in smoothing surfaces, concrete grinding, tile cutting, and polishing of floors, and hence they have become crucial equipment at construction sites. Also, government programs are associated with infrastructure upgrades like bridges, roads, and public buildings, propelling demand for effective abrasive products.

- The ongoing innovations in grinding and finishing technologies are the future trend in the market driving market expansion. It involves simulation tools and advanced grinding strategies for precision machining. These advancements are creating high demand for high-precision abrasives in different sectors.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 7.53 Billion/ 4.42 Million Tons |

| Expected Size in 2035 | USD 12.55 Billion/ 6.83 Million Tons |

| Growth Rate | CAGR of 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Material, By Application, By Regions |

| Key Companies Profiled | Macro Group International, Metaltec Steel Abrasive, Grindwell Norton Ltd, Silcal Metallurgic Ltd., Siambrator Co., Ltd., Airblast-Abrasives B.V. |

AI-Powered Predictive Formulations in the Metal Abrasives Market

AI-powered predictive formulations are transforming the market by combining predictive analytics and machine learning into R&D and manufacturing; hence, market players are optimizing raw material rations and predicting abrasive lifespans. Furthermore, AI models can adjust process parameters during production to guarantee uniform density and hardness.

Supply Chain Analysis of the Metal Abrasives Market

Production & Processing

- It involves the production and application of abrasive media, like steel shot, steel grit, cut wire, and chilled iron, utilized for surface preparation, cleaning, descaling, and shot peening in big industries such as automotive production, aerospace, and metal fabrication.

- W Abrasives (Wheelabrator Group): A global leader specializing in steel shots and grits, highly focused on process optimization and digital diagnostic services for surface preparation.

- Other Key Players: Abrasives Inc., 3M India Ltd.

Quality Testing and Certification

- It includes strict compliance with international safety and performance standards. This technical assessment is needed for uniform hardness, precise grain size distribution, and material durability, which are critical for specialized industrial applications such as surface preparation, shot peening, and metal fabrication.

- 3M: A global leader known for its advanced ceramic abrasives and smart manufacturing processes.

- Other Key Players: Ervin Industries, W Abrasives

Distribution to Industrial Users

- It includes logistical and supply-chain frameworks dedicated to distributing industrial abrasive media, specifically steel shots and grits, directly to heavy manufacturing sectors. These specialized distribution channels guarantee that end-user facilities, including foundries, automotive component plants, and shipyards, maintain an uninterrupted supply of essential materials.

- Saint-Gobain: A French multinational that leverages a massive multi-plant manufacturing and local commercial distribution network to serve global industrial customers.

- Other Key Players: W Abrasives, Carborundum Universal Limited

Metal Abrasives Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | OSHA rules under 29 CFR 1910.1053 strictly enforce a Permissible Exposure Limit (PEL) of 50 µg/m³ for respirable crystalline silica. This has functionally driven the commercial industry to substitute sand with reusable metal abrasives. |

| European Union | Metal abrasives imported or manufactured over one metric ton per year must comply with EU REACH (EC No 1907/2006). Importers must guarantee the media contains less than 0.1% weight-by-weight of Substances of Very High Concern (SVHC). |

| China (MEE & NHC) | The National Health Commission enforces GBZ 2.1, which sets the exposure ceiling for silica and industrial dust at 0.1 mg/m³. This benchmark is strictly audited in automotive manufacturing hubs. |

Market Dynamics

Driver

Increasing Demand from Heavy Machinery Sectors

The market is increasingly gaining traction due to a surge in usage in the heavy equipment and automotive manufacturing sectors, which are the major factors driving market growth. Surface cleaning, deburring, and shot peening are crucial processes that improve the performance and longevity of necessary components. In addition, automotive manufacturers are implementing sophisticated surface preparation technologies to enhance coating adherence and corrosion resistance, with growing electric vehicle (EV) production globally.

Restraint

Strengthen Regulatory Requirements

Major market players are facing stringent environmental regulations addressing hazardous emissions, waste, and chemical binders, which is the major factor hindering market growth. Moreover, blasting operations are required to install premium filtration and dust-control systems to protect workers. Fines for non-compliance can exceed millions of dollars, imposing significant financial burdens on smaller competitors.

Opportunity

The Growth of Industrial Projects in Developing Economies

The ongoing urbanizing regions where heavy manufacturing and infrastructure projects are gaining traction are creating lucrative opportunities in the market. Major countries in Asia, Latin America, and the Middle East are heavily investing in energy, transportation, and urban development. Furthermore, government-sponsored economic initiatives are establishing a conducive environment for abrasive manufacturers to scale their manufacturing capabilities and operational capacity.

Segmental Insights

Material Insights

The steel segment dominated the market with the largest share of 84% in 2025. The steel is largely preferred over non-metallic alternatives because of its ability to be recycled multiple times without losing its abrasive efficacy. Steel is mainly used for shot peening, surface finishing, and gentle cleaning; it is also increasingly demanded in the aerospace and automotive sectors, where a uniform and smooth surface is necessary. In addition, in contrast to alternative blasting media such as slag, sand, and garnet, steel abrasives can be recycled and reused many more times prior to degradation. ")

The others segment held the market share of 16.0% and is expected to grow at the fastest CAGR of 6.50% over the forecast period. This segment encompasses non-steel metallic and mineral abrasives, which are important for specialized surface finishing, polishing, and cleaning applications where standard steel abrasives can cause damage or unwanted surface contamination. Also, this segment supplies nonferrous media essential for high-purity operations across the petrochemical, food processing, and medical industries. The rapid surge in aerospace engineering and electric vehicle (EV) components needs light alloys such as titanium and aluminium.

Metal Abrasives Market Share,By Material 2025(%)

| By Material | Market Share (%) |

| Steel | 84.00% |

| Others | 16.00% |

Application Insights

The automotive segment dominated the market with the largest share of 31.0% in 2025. The metal abrasives are crucial for shaping body panels, finishing powertrain components, and surface preparation before painting. These abrasives are increasingly used in the automotive sector for welding seam grinding, heavy material removal, and precision finishing of gears and engine components. Moreover, metallic abrasives, including steel shot and grit, are used for surface preparation, scale removal, and inducing compressive stresses in critical components such as springs and gears, thereby extending their operational fatigue life.

")

The metalworking segment held a market share of 27% in 2025 and is expected to grow at the fastest CAGR of 6.70% over the forecast period. This segment depends heavily on processes such as cutting, grinding, deburring, and surface cleaning to build structural steel, heavy machinery, and precision components. Furthermore, the ongoing expansion of automated blasting equipment impels market players to shift towards durable, premium metal abrasives to maximize overall equipment runtime. Cubic Boron Nitride (CBN) and diamond abrasives are increasingly used in the machining of hard, heat-treated steels and complex alloys, offering improved operational efficiency and significantly extended tool lifespans.

Metal Abrasives Market Share,By Application, 2025(%)

| By Application | Market Share (%) |

| Automotive | 31.0% |

| Metalworking | 27% |

| Machinery & Equipment | 19.00% |

| Construction | 14.00% |

| Others | 9.00% |

Regional Analysis

How did Asia Pacific Dominated the Metal Abrasives Market in 2025?

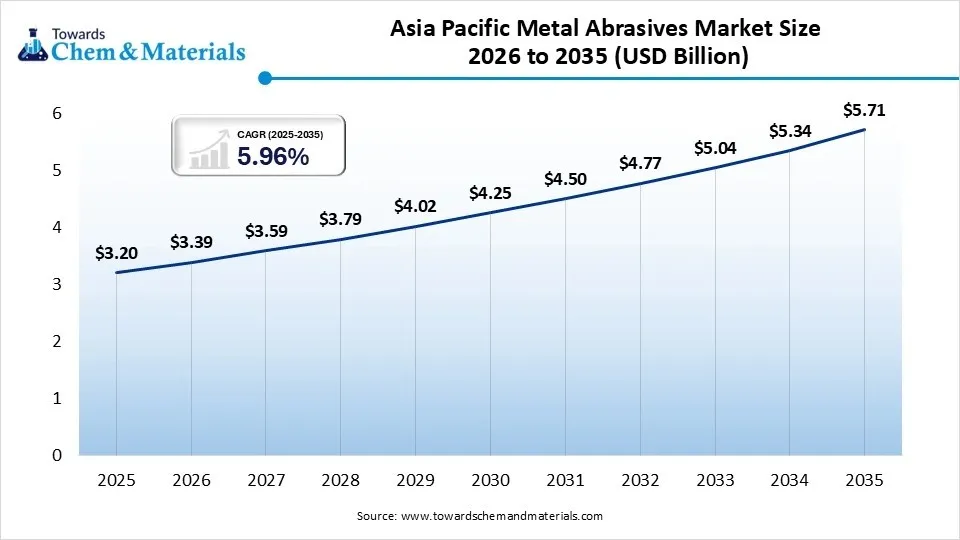

The Asia Pacific metal abrasives market size was estimated at USD 3.20 billion in 2025 and is projected to reach USD 5.71 billion by 2035, growing at a CAGR of 5.96% from 2026 to 2035. Asia Pacific dominated the market with the largest share of 45.0% in 2025. The dominance of the region can be attributed to the ongoing urbanization, extensive automotive manufacturing, and expanding infrastructure and construction projects in developing countries. In addition, the region is also driving major demand for shot peening, surface preparation, and vehicle finishing. This transition towards lightweight automotive materials has further boosted the demand for high-performance metal abrasives.

")

China

- The ongoing need for surface preparation, cutting, and precision finishing in machinery and pre-engineered components directly fuels demand.

- Industries are increasingly adopting durable metal abrasives like steel shots and grits to improve operational efficiency and reduce long-term processing costs.

India

- The push toward establishing India as a global manufacturing center has fuelled domestic production of machinery and metal components.

- The emerging electric vehicle (EV) market in India necessitates specialized abrasive finishing for battery enclosures, lightweight metals, and motor components.

The North America metal abrasives market size was estimated at USD 1.35 billion in 2025 and is projected to reach USD 2.38 billion by 2035, growing at a CAGR of 5.96% from 2026 to 2035. North America held a market share of 19% in 2025 and was expected to grow at the fastest CAGR of 6.80% over the forecast period. The growth of the region can be credited to the growing defense and aerospace manufacturing, a strong automotive and EV manufacturing sector, along with the rapid infrastructure reshoring initiatives. The ongoing transition toward electric vehicle (EV) component manufacturing and modernized tooling needs highly specialized surface finishing and metal fabrication solutions.

United States

- A strong regional shift toward Industry 4.0 and automated surface treatment systems enables manufacturers to optimize abrasive efficiency, fuelling the demand for durable and high-performance metal abrasive solutions.

- Surges in domestic investments in pre-engineered steel buildings and infrastructure projects continue to drive consumption in cutting, grinding, and descaling.

Canada

- Canadian manufacturing facilities are increasingly adopting robotics and automated blasting/grinding systems. This shift requires high-performance and durable metal abrasives.

- Stringent Canadian environmental regulations have forced abrasive manufacturers to focus on eco-friendly, recyclable metal abrasive products.

The Europe metal abrasives market size was estimated at USD 1.64 billion in 2025 and is projected to reach USD 2.89 billion by 2035, growing at a CAGR of 5.83% from 2026 to 2035.Europe held the market share of 23.00% in 2025. The growth of the region can be credited to the strong aerospace and automotive production base in the major countries along with the strict regional sustainability regulations. Also, capital-intensive construction projects, renewable energy infrastructure installations, and the modernization of European rail networks demand durable, high-performance abrasives for metal cutting, weld seam smoothing, and surface preparation, leading to market growth soon.

Germany

- Strict European environmental regulations and localized ESG goals compel German suppliers to adopt eco-friendly abrasives, such as recycled-bond systems.

- Automation in production needs smart abrasives designed to integrate seamlessly with robotic systems, boosting overall efficiency and reducing the need for human labor.

France

- The increasing adoption of automated blasting systems in factories is fueling the demand for high-performance, reusable metal abrasives that improve operational efficiency and reduce processing costs.

- The ongoing demand for pre-engineered structural steel and components used in construction and heavy machinery supports stable growth in metalworking.

The Latin America metal abrasives market size was estimated at USD 0.50 billion in 2025 and is projected to reach USD 0.88 billion by 2035, growing at a CAGR of 5.82% from 2026 to 2035. Latin America held the market share of 7.00% in 2025. The growth of the region can be driven by a surge in automotive production, infrastructure investments, and expanding metal fabrication and mining sectors. Moreover, the region serves as a premier center for the global mining industry. This position creates a sustained, large-scale requirement for grinding, cutting, and blasting abrasives.

Brazil

- Brazil is a major global supplier of automobiles and aircraft. The ongoing push for metal surface preparation, deburring, and precision component finishing drives heavy consumption of metal abrasives.

- Brazil's vast mining sector needs heavy-duty grinding and cutting abrasives for both mineral processing and the maintenance of large-scale extraction machinery.

Argentina

The demand for precision in component manufacturing continues to drive demand for bonded and coated abrasives across assembly plants in industrial hubs like Buenos Aires and Córdoba.

Increasing automation and the adoption of high-performance ceramic abrasives, which offer longer lifespans and superior finishing, are modernizing local production lines, driving country growth soon.

Metal Abrasives Market Share, By Region, 2025(%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 45.00% |

| Europe | 23.00% |

| North America | 19.00% |

| Latin America | 7.00% |

| Middle East & Africa | 6.00% |

The Middle East & Africa metal abrasives market size was estimated at USD 0.43 billion in 2025 and is projected to reach USD 0.75 billion by 2035, growing at a CAGR of 5.72% from 2026 to 2035. The Middle East & Africa held a market share of 6.00% in 2025. The growth of the region can be attributed to the surge in demand for oil & gas maintenance, ongoing infrastructure development, and heavy mining operations. Furthermore, growing emphasis on diversifying economies has facilitated increasing local aerospace, metalworking, and automotive assembly. Metal abrasives are crucial for cutting, stamping, and finishing vehicle parts

")

Saudi Arabia

- The diversification of Saudi Arabia's industrial base into localized automotive production and aerospace components necessitates precision abrasive tools for dimensional accuracy and superior surface finishing.

- High-profile infrastructure developments, such as smart cities like NEOM and the expansion of heavy industrial hubs, are exponentially increasing the demand for structural steel.

UAE

- UAE government initiatives emphasize expanding non-oil manufacturing and establishing local supply chains, leading to more metalworking and machinery utilization.

- Strategic collaborations, such as Emirates Global Aluminum’s adoption of digital automation, are increasing the need for high-performance, precision abrasives.

Competitive Analysis

The market is highly fragmented and moderately consolidated by major multinational players emphasizing strategic acquisitions, capacity expansion, and sustainable product innovations to counter stringent environmental regulations.

At the upcoming Grindinghub in Stuttgart, Germany, industry leader Weiler Abrasives will exhibit its state-of-the-art precision grinding solutions. The company will present advanced abrasives and power brushes for surface conditioning.

- Inlyte Energy and Ervin Industries have formalized a partnership to localize and secure the U.S. battery storage supply chain. Inlyte is currently finalizing the location for its inaugural domestic manufacturing facility and remains on schedule to commence commercial product shipments in 2027.(Source: www.etmm-online.com)(Source: www.manufacturingdive.com)

Recent Developments

- In April 2026, Roshel Inc., a Brampton-based manufacturer of defense and law enforcement vehicles, has entered a strategic joint venture with Algoma Steel. This partnership, known as Roshel Algoma Defence, will establish a sovereign Canadian supply chain for high-performance ballistic steel engineered to withstand explosive blasts and ballistic impacts.(Source: www.sootoday.com)

- In November 2025, Epiroc introduced its next-generation polycrystalline diamond (PCD) drill bits, engineered to provide superior wear resistance and an extended operational lifespan. These advanced components are specifically optimized for high-precision drilling within highly abrasive geological formations.(Source: im-mining.com)

Strategic Profiles of Key Players Shaping the Metal Abrasives Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| W Abrasives (Winoa Group) | Market Leader / Large-Scale Established Player | Le Cheylas, France | Global footprint across Europe, North America, Asia-Pacific, and South America. | Steel shot, steel grit, premium blasting media, and digital evaluation technologies (WAST). | High-performance environmental recycling solutions and optimized shot-peening media for automotive/steel sectors. |

| Ervin Industries | Prominent International Manufacturer / Innovation Pioneer | Ann Arbor, Michigan, USA | Comprehensive networks across North America and Europe, backed by global export operations. | Amasteel (cast steel shot and grit), Amachrome (stainless steel shot), and Amacast. | Industry benchmark for casting durability, material consistency, and structural fatigue resistance. |

| Vulkan INOX GmbH | Specialized Market Leader / Premium Niche Player | Hattingen, Germany | High concentration in Europe, with expanding export routes into global aerospace sectors. | Chronital (cast stainless steel shot) and Grittal (stainless steel grit) | Rust-free surface preparation, deburring, and surface finishing for non-ferrous metals and alloys. |

| Abrasives Inc. | Specialized Regional Leader | North Dakota, USA | Strong commercial hold across North American construction and industrial blasting networks. | Metallic steel shot/grit alongside non-metallic media (aluminum oxide, garnet, slag media). | High-volume versatility in commercial surface preparation and heavy-duty industrial coating removal |

Other Key Players

- Macro Group International

- Metaltec Steel Abrasive

- Grind well, Norton Ltd

- Silcal Metallurgic Ltd.

- Siambrator Co., Ltd.

- Air blast-Abrasives B.V.

Segments Covered in the Report

By Material

- Steel

- Steel Shot

- Cast Steel Shot

- Conditioned Steel Shot

- Steel Grit

- Angular Steel Grit

- High Carbon Steel Grit

- Low Carbon Steel Grit

- Stainless Steel Shot

- Stainless Steel Grit

- Others

- Cut Wire Abrasives

- Carbon Steel Cut Wire

- Stainless Steel Cut Wire

- Aluminum Cut Wire

- Zinc Shot

- Copper Shot

- Aluminum Shot

- Specialty Metal Abrasives

By Application

- Automotive

- Surface Preparation

- Shot Peening

- Component Cleaning

- Rust Removal

- Metalworking

- Foundries

- Forging

- Fabrication

- Surface Finishing

- Machinery & Equipment

- Industrial Machinery

- Agricultural Equipment

- Heavy Equipment

- Construction

- Structural Steel

- Bridges

- Reinforcement Components

- Others

- Aerospace

- Shipbuilding

- Railways

- Energy & Power

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

Select User License to Buy

Figures (6)