Content

What is the current Biopolymers Market Size and Share?

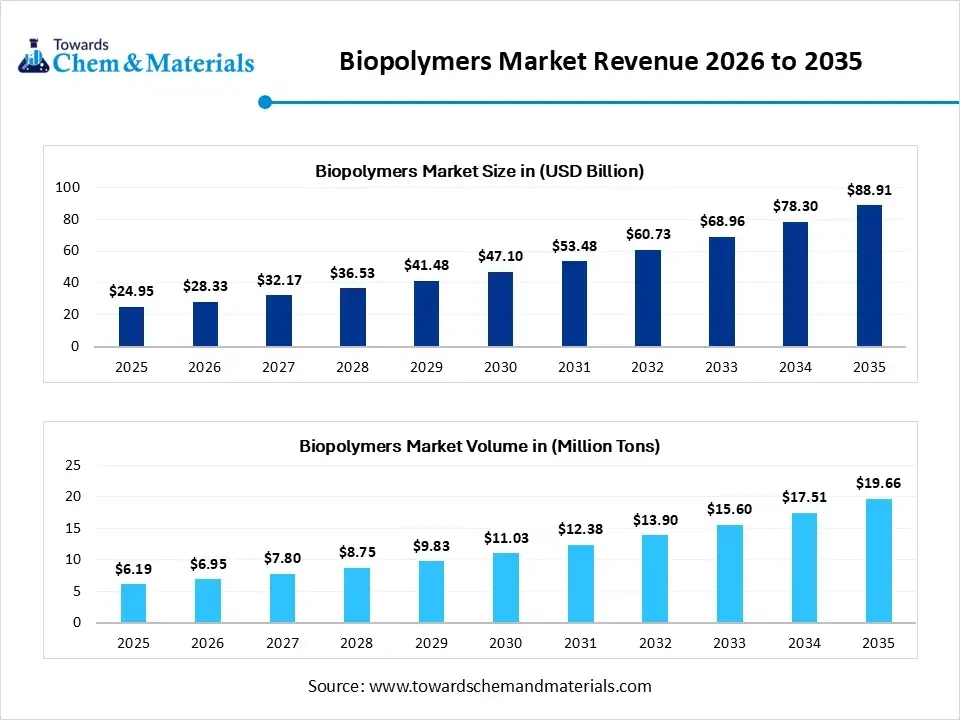

The global biopolymers market size was valued at USD 24.95 billion in 2025, is estimated to reach USD 28.33 billion in 2026, and is projected to reach USD 88.91 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 13.55% over the forecast period from 2026 to 2035. In terms of volume, the biopolymers market is projected to grow from 6.19 million tons in 2025 to 19.66 million tons by 2035. growing at a CAGR of 12.25% from 2026 to 2035.The growth of the market is driven by the stringent environmental regulations and the shift toward sustainable, eco-friendly packaging.

What Is the Significance of the Biopolymers Market?

The biopolymers market plays a crucial role in shifting the global economy toward sustainability. Replacing traditional petroleum plastics with renewable, biodegradable alternatives cuts greenhouse gases, reduces microplastic pollution in oceans, & supports strict ESG standards and bans on single-use plastics. Conventional plastics can take hundreds of years to degrade, but biopolymers made from resources like starch, cellulose, and microorganisms decompose naturally, helping to reduce landfill size.

Increasing global regulations, like bans on single-use plastics, with corporate sustainability goals, are urging industries to move away from fossil fuels. Besides environmental benefits, biopolymers are vital in healthcare, as they are biocompatible and used in advanced wound dressings, tissue scaffolds, and drug delivery systems. They are also used in environmentally friendly films and coatings that naturally break down, reducing soil contamination. Advances in high-performance biopolymers offer strength-to-weight ratios comparable to those of synthetic plastics, helping automakers reduce vehicle weight and enhance energy efficiency.

Key Takeaways

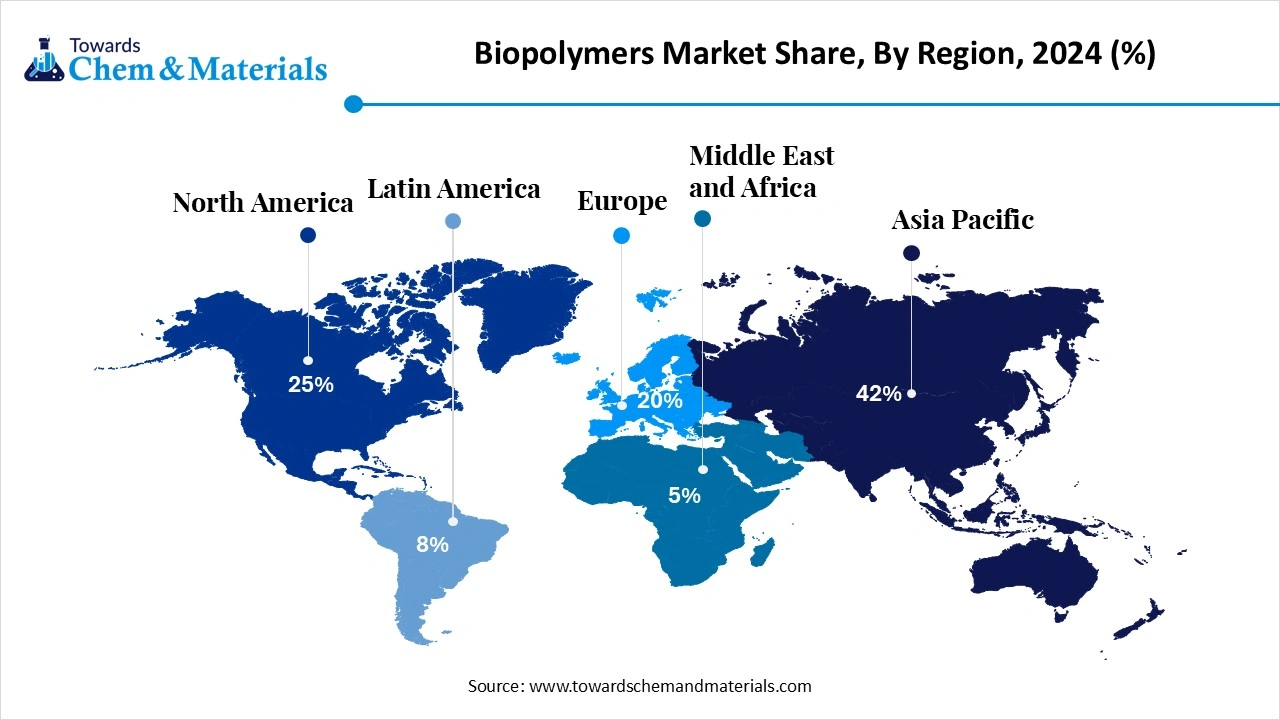

- By region, Europe dominated the market with a share of 34% in 2025. Strict environmental regulations accelerate biodegradable polymer adoption.

- By region, Asia Pacific held 31% market share in 2025 and is expected to experience the fastest growth with a CAGR of 15.2% in the forecast period. Rising consumer awareness increases sustainable product demand.

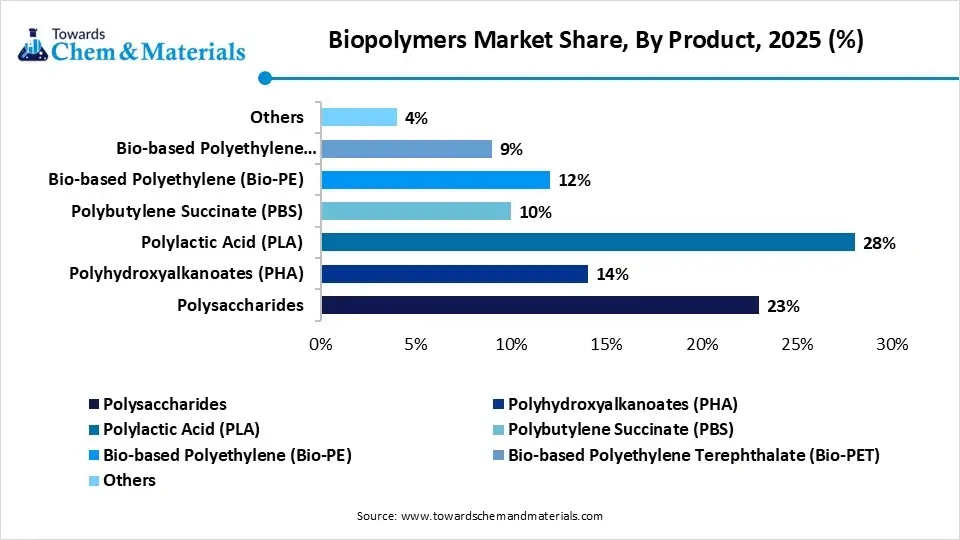

- By product, the polylactic acid (PLA) segment dominated the market with 28% share in 2025. The packaging and 3D printing sectors significantly increase PLA utilization.

- By product, the polyhydroxyalkanoates (PHA) segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.6% in the forecast period. Marine biodegradable properties increase PHA demand in sustainable packaging.

- By applications, the films segment dominated the market with 31% share in 2025. Compostable packaging demand significantly increases biopolymer film usage.

- By applications, the medical implants segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.1% in the forecast period. Biocompatible materials expand usage in orthopedic and tissue engineering.

- By end-use, the packaging segment dominated the market with 42% share in 2025 and is expected to have the fastest growth with a CAGR of 14.8% in the forecast period. Food and beverage companies expand compostable packaging adoption.

Growth Trends

- Surge in PHA Demand: Polyhydroxyalkanoates (PHA) are experiencing massive growth due to their fully biodegradable nature, biocompatibility, and versatility across both packaging and medical applications.

- Raw Material Innovation: The industry is moving beyond food-crop reliance. Innovations are focusing on agricultural residues, sugarcane, starch, and microbial fermentation to synthesize polymers.

- Fossil Fuel Volatility: Fluctuating crude oil prices are pushing manufacturers to explore renewable, bio-based raw materials like sugarcane, starch, and agricultural residues.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 28.33 Billion / 6.95 Million Tons |

| Expected Size by 2035 | USD 88.91 Billion/ 19.66 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 13.55% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product, By Applications, By End-Use, By Regions |

| Key Companies Profiled | Archer Daniels Midland Company, DuPont de Nemours, Inc., Novamont S.p.A., BiologiQ, Inc., Mitsubishi Chemical Group Corporation, Danimer Scientific, Toray Industries, Inc., Biome Bioplastics Limited, Plantic Technologies Limited, FKuR Kunststoff GmbH. |

Key Technological Shifts in the Biopolymers Market with Integration of AI:

The biopolymers market is undergoing a massive transformation, driven by innovations in synthetic biology, material science, and circular economy demands. Rapid advancements in microbial fermentation, machine learning-based process optimization, and high-performance feedstock development are overcoming historical cost and performance barriers. Manufacturers utilize ML algorithms to monitor and optimize polymerization and fermentation conditions. AI-driven models analyze complex production data to maintain structural consistency, mechanical strength, and thermal resistance.

Biopolymers Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | U.S. FDA and EPA | Title 21 of the Code of Federal Regulations and Toxic Substances Control Act (TSCA) |

- food safety and impact on pesticides | These agencies are closely watching the manufacturers' activity within the major sectors. |

| European Union | European Medicines Agency and European Food Safety Authority | Regulations (EU) 2023/ 2055 Microplastic Restriction | Food and food pacakaging and biopharmaceuticals | The European Union has sectoral safety standards, like EM has its own standards, and EFSA has its own |

| China | Inventory of Existing Chemical Substances in China (IECSC). | MEE Order No. 12 | Observe and regulate the latest chemical substances | This regulatory body has seen under the heavy implementation and safety standards in China while observing the environmental impact of chemical substances. |

| India | Genetic Engineering Appraisal Committee (GEAC) and Food Safety and Standards Authority of India (FSSAI) | Not having primary regulation and depending upon these regulatory bodies | Major approval of the genetically engineered organism | India is seeking the primary regulation that can lead to safety standards and compliance. |

Supply Chain Analysis of the Biopolymers Market:

- Biopolymer Production & Processing:Biopolymers are produced from renewable feedstocks such as corn starch, sugarcane, cellulose, algae, and vegetable oils through fermentation and polymerization processes to create biodegradable and bio-based materials.

- Key players: NatureWorks, BASF, TotalEnergies, Corbion, Novamont

- Quality Testing and Certification:Biopolymers must meet standards for biodegradability, compostability, bio-based content, material strength, and environmental safety compliance before commercialization.

- Key players: International Organization for Standardization, ASTM International, TÜV Austria, European Chemicals Agency

- Distribution to Industrial Users:Biopolymers are supplied to packaging manufacturers, agriculture industries, textile companies, consumer goods manufacturers, and automotive sectors for sustainable material applications.

Biopolymers Market Dynamics

| Drivers | Restrains | Opportunities |

| Technological Advancements: | High Production and Material Costs: | Sustainable Packaging Solutions: |

| Innovations in polymer chemistry and bio-refining have improved the durability, heat resistance, and cost-efficiency of biopolymers | Biopolymers cost significantly more per metric tonne to produce than traditional oil-based plastics. | Biopolymers are in high demand for food and beverage packaging, driven by strict waste regulations and the move toward a circular economy. |

| Volatility of Fossil Fuel Prices: | Performance Limitations: | Healthcare and Biomedical Expansion: |

| The fluctuating costs and unpredictable availability of petroleum resources have encouraged manufacturers to switch to renewable, bio-based feedstocks like corn, sugarcane, and agricultural waste. | Certain biopolymers exhibit lower thermal resistance, fragility, and higher permeability to water vapor or oxygen when compared to traditional plastics. | Because many biopolymers are biocompatible and non-toxic, they offer strong growth potential in medical devices, tissue engineering, and drug delivery systems. |

| Consumer Demand & Brand Commitments: | Disposal and Infrastructure Gaps: | High-Performance PHA (Polyhydroxyalkanoates): |

| Rising environmental awareness has led consumers to actively choose sustainable products. In response, major global brands have integrated bio-based materials into their long-term corporate sustainability and circular economy strategies. | Many biodegradable plastics require industrial-level composting temperatures to break down efficiently; they do not decompose effectively in standard household compost or landfill environments. | The development of PHA is a significant growth engine. Modern PHA grades provide excellent mechanical stability and heat resistance, allowing them to replace traditional synthetic plastics in industrial applications. |

Segmental Insights

Product Insights

The polylactic acid (PLA) segment dominated the market with 28% share in 2025, driven by rising bans on single-use plastics and high-volume demand for sustainable food and packaging materials. Stricter government bans on single-use plastics, coupled with corporate sustainability goals, have accelerated the adoption of bio-based options in e-commerce and retail.

The polysaccharides segment held 23% market share in 2025, driven by its unparalleled renewability, biodegradability, and functional versatility. Shifting consumer preferences toward eco-friendly packaging and clean-label foods, paired with strict global bans on single-use plastics, have positioned polysaccharides as the most widely used natural polymers.

")

The polyhydroxyalkanoates (PHA) segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.6% in the forecast period, driven by its unique ability to naturally decompose in diverse environments, including soil and ocean water, without leaving toxic residues. PHAs are synthesized by microorganisms through the fermentation of organic waste, agricultural by-products, and carbon feedstocks. This directly aligns with global circular economy goals and corporate Environmental, Social, and Governance commitments.

The bio-based polyethylene (Bio-PE) segment held 12% market share in 2025, fueled by an increasing global push toward circular economies, strict single-use plastic bans, and surging consumer demand for sustainable, carbon-neutral materials. Bio-PE is primarily derived from ethanol made from sugarcane or other biomass, rather than fossil fuels. By substituting fossil carbon with atmospheric carbon absorbed by the plants during growth, it significantly lowers the overall carbon footprint.

Biopolymers Market Share, By Product, 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Polysaccharides | 23% |

| Polyhydroxyalkanoates (PHA) | 14% |

| Polylactic Acid (PLA) | 28% |

| Polybutylene Succinate (PBS) | 10% |

| Bio-based Polyethylene (Bio-PE) | 12% |

| Bio-based Polyethylene Terephthalate (Bio-PET) | 9% |

| Others | 4% |

Applications Insights

The films segment dominated the market with 31% share in 2025, due to strict single-use plastic ban, rising consumer demand for sustainable packaging, and advancements in bio-plastics like PLA and PHA that improve moisture, temperature, and tear resistance. Biodegradable mulch films are seeing high adoption because they degrade directly into the soil, eliminating the need for removal and disposal.

The bottle segment held 18% market share in 2025, primarily driven by strict government bans on single-use plastics, corporate sustainability goals, and major innovations in plant-based materials like Polylactic Acid (PLA). Industry giants such as Coca-Cola, Danone, and Nestlé are actively transitioning to biodegradable or 100% bio-based packaging to achieve net-zero targets and improve public brand perception.

The fibers segment held 16% market share in 2025, due to surging demand in the sustainable apparel sector, advancements in thermal processing, and increased utilization in high-value medical textiles. The inherent biocompatibility and non-toxic nature of biopolymer fibers have led to a massive spike in medical textiles. They are extensively deployed for wound care, resorbable sutures, and tissue engineering scaffolds.

The medical implants segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.1% in the forecast period, due to rising demand for biocompatible, biodegradable, and smart polymers. Driven by an aging global population, increasing chronic diseases, and a strong preference for minimally invasive surgeries, biopolymers are now standard in orthopedic, cardiovascular, and dental implants.

Biopolymers Market Share, By Applications, 2025 (%)

| By Applications | Revenue Share, 2025 (%) |

| Films | 31% |

| Bottle | 18% |

| Fibers | 16% |

| Seed Coating | 7% |

| Vehicle Components | 11% |

| Medical Implants | 8% |

| Other Applications | 9% |

End-Use Insights

The packaging segment dominated the market with 42% share in 2025 and is expected to have the fastest growth with a CAGR of 14.8% in the forecast period, due to a combination of strict global bans on single-use plastics, booming consumer demand for eco-friendly products, and advancements in bio-based materials like PLA. Government policies and outright bans on single-use plastics are forcing manufacturers to adopt sustainable alternatives.

The consumer goods segment held 18% market share in 2025, due to a collective shift toward environmental accountability, stringent regulations on single-use plastics, and advancements in bio-materials. Brands are rapidly integrating biopolymers like Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) to meet evolving buyer preferences for eco-friendly alternatives. Regulatory bodies globally are instituting policies and bans to diminish plastic waste. This forces consumer goods and packaging companies to find sustainable waste management solutions and alternative materials.

The automotive segment held 14% market share in 2025, due to strict governmental emission regulations and automakers' commitments to ESG goals. Biopolymers provides a lightweight alternative to traditional metals and plastics which enhances fuel efficiency, with a high recycling rate to decrease overall carbon footprints. Biopolymers offer a high recyclability rate and support the circular economy through improved closed-loop recycling and composting.

The textiles segment held 13% market share in 2025, driven by the global fashion and apparel industry's urgent shift toward sustainability to reduce environmental waste and reliance on petroleum. The demand for biopolymers is surging in specialized fields like medical textiles, bio-absorbable wound dressings, drug delivery, protective clothing, and domestic/home textiles.

Biopolymers Market Share, By End-use, 2025 (%)

| By End-use | Revenue Share, 2025 (%) |

| Packaging | 42% |

| Consumer Goods | 18% |

| Automotive | 14% |

| Textiles | 13% |

| Agriculture | 9% |

| Other End-Uses | 4% |

Regional Insights

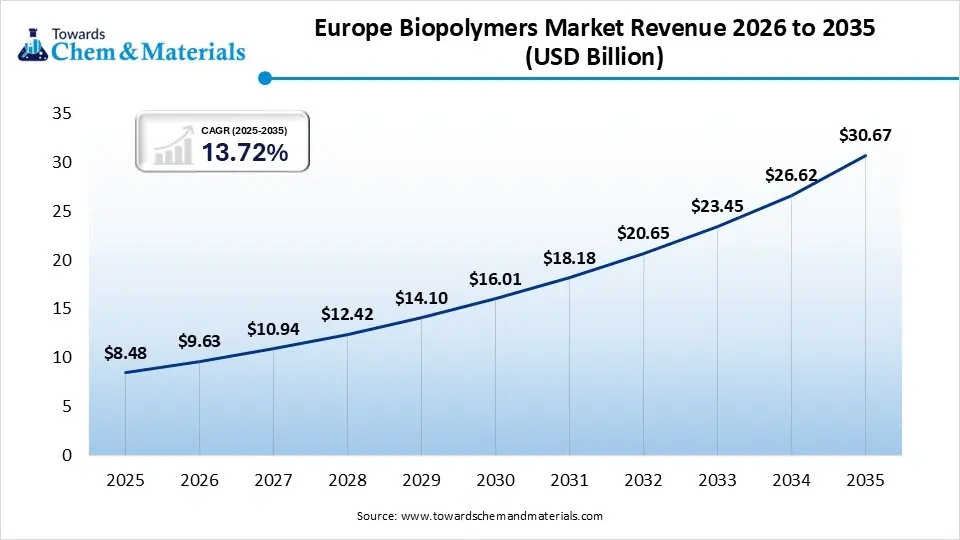

The Europe biopolymers market size was estimated at USD 8.48 billion in 2025 and is projected to reach USD 30.67 billion by 2035, growing at a CAGR of 13.72% from 2026 to 2035.Europe dominated the market with a share of 34% in 2025, driven by stringent EU environmental legislation such as the Packaging and Packaging Waste Regulation, massive public demand for sustainable products, and heavy investments in large-scale biorefineries. The region benefited from the scaling of large industrial manufacturing plants. Notably, major investments, like Futerro's €500 million fully integrated circular biorefinery in Normandy, France, significantly boosted regional production capacity for materials like Polylactic Acid (PLA).

Countries

Germany

- Germany boasts a highly advanced waste separation and composting system, particularly the Duales System Deutschland / Green Dot. This established framework naturally supports the disposal, collection, and industrial composting of biopolymers.

- Germany's heavy concentration of automotive manufacturers like Volkswagen, BMW, and Mercedes-Benz is fueling research into bio-based and biodegradable interior components to meet aggressive lightweighting and sustainability targets.

Italy

- Italy operates under some of Europe’s most aggressive single-use plastic bans and waste management policies. The adoption of the EU’s Packaging and Packaging Waste Regulation heavily forces producers to utilize recyclable, reusable, and biodegradable materials.

- Italy is widely considered a European hub for the bio-based economy, largely due to major local innovators like Novamont. The country prioritizes transitioning from linear consumption models to closed-loop recycling and composting.

Asia Pacific Biopolymers Market Growth Factor

The Aisa Pacific biopolymers market size was estimated at USD 7.73 billion in 2025 and is projected to reach USD 28.01 billion by 2035, growing at a CAGR of 13.74% from 2026 to 2035.Asia Pacific held 31% market share in 2025 and is expected to experience the fastest growth with a CAGR of 15.2% in the forecast period, driven by stringent government bans on single-use plastics, massive investments in renewable chemical subsidies, and abundant local agricultural raw materials.The region’s agricultural strength gives manufacturers access to cheap, localized raw materials. Countries like Thailand and Indonesia heavily leverage their vast cassava and sugarcane industries to produce bioplastics cost-effectively.

Countries

India

- The Central and State governments have aggressively phased out single-use plastics. This regulatory pressure forces industries to adopt sustainable, biodegradable packaging alternatives.

- Government incentive schemes such as the PMKSY scheme and private investments are lowering import dependencies by boosting domestic manufacturing, thus making biopolymers more accessible and cost-effective.

China

- China’s rollout of stringent regulations, such as bans on non-biodegradable single-use plastics and plastic bags in major cities, forces the shift towards biodegradable alternatives.

- The Chinese government provides substantial financial resources, subsidies, and incentives to transform the country into the world's largest biopolymer producer, leading to rapid capacity scaling.

Japan

- Japan’s government has enacted progressive waste management laws to curb single-use plastics and promote a circular bio-economy, pushing industries to adopt biodegradable and bio-based alternatives.

- Japan's highly advanced manufacturing sector is heavily investing in material science. This has yielded better-performing polymers and cheaper production methods, making bioplastics more competitive against traditional synthetics.

North America Biopolymers Market Growth Factor

The North America market size was estimated at USD 5.49 billion in 2025 and is projected to reach USD 20.00 billion by 2035, growing at a CAGR of 13.80% from 2026 to 2035.North America held 22% market share in 2025, driven by strict government bans on single-use plastics, rising consumer preference for eco-friendly packaging, and strong corporate sustainability commitments across the region. Aggressive legislative bans and phase-outs on single-use plastics across U.S. states and Canadian federal mandates require industries to pivot toward biodegradable alternatives. Beyond packaging, lightweighting in the automotive sector and increasing use of bioresorbable polymers in medical implants and devices are unlocking new revenue streams.

Countries

U.S.

- Biopolymers are highly biocompatible, fueling their adoption in advanced healthcare sectors for drug delivery systems, surgical sutures, and tissue engineering.

- The instability and fluctuating costs of petroleum the primary raw material for conventional plastics make biopolymers an increasingly cost-competitive and economically stable long-term alternative.

Canada

Federal and provincial policies, including the national ban on various single-use plastics, require industries to transition toward circular, biodegradable alternatives.

The Canadian agricultural sector heavily utilizes biodegradable mulch films, seed coatings, and plant pots to improve soil quality and reduce labor costs associated with plastic removal.

Latin America Biopolymers Market Growth Factor

The Latin America market size was estimated at USD 1.75 billion in 2025 and is projected to reach USD 6.67 billion by 2035, growing at a CAGR of 14.32% from 2026 to 2035.Latin America held 7% market share in 2025 and is experiencing rapid expansion, driven primarily by tightening regional environmental regulations, surging consumer demand for sustainable packaging, and the region's abundant agricultural feedstock, with Brazil leading regional production. The region's vast agricultural capabilities, specifically in Brazil and Argentina, allow for highly cost-effective biopolymer production using renewable resources like sugarcane, corn starch, and agricultural residues.

Brazil

- Brazil is uniquely positioned as a global leader in agricultural raw materials. The wide availability of sugarcane serves as an excellent, cost-effective base for bio-based polyethylene, granting local manufacturers a distinct production advantage.

- A cultural shift toward eco-consciousness, with Corporate Social Responsibility initiatives, is driving the demand for biodegradable and bio-based products, mainly in the flexible packaging, food & beverage industries.

Argentina

- Consumer preference for sustainable packaging and products is soaring, compelling manufacturers to pivot from traditional petroleum-based plastics to biodegradable alternatives.

- Biodegradable bioplastics are increasingly utilized in farming for mulch films, seed coatings, and plant pots to improve soil quality and eliminate the labor-intensive removal of plastic waste.

Middle East and Africa Biopolymers Market Growth Factor

The Middle East and Africa market size was estimated at USD 1.50 billion in 2025 and is projected to reach USD 5.78 billion by 2035, growing at a CAGR of 14.44% from 2026 to 2035.The Middle East and Africa held 6% market share in 2025, driven by strict government bans on single-use plastics, growing eco-conscious consumerism, and expanding demand from food packaging, automotive, and agricultural sectors. The market is experiencing rapid expansion, with regional revenue projections climbing as urbanization increases. There is a strong regional shift toward biodegradable and compostable packaging solutions due to rising awareness among consumers about the environmental impact of synthetic plastics.

Counties

Saudi Arabia

- The core driving force for bioplastics adoption in the Kingdom is the push for a circular economy under Saudi Vision 2030 and the Saudi Green Initiative.

- The government is heavily funding sustainable projects and implementing stricter environmental regulations aimed at reducing plastic waste by up to 35% and ensuring all packaging is recyclable and reusable.

UAE

- Strict bans on single-use plastic bags and styrofoam products across Dubai, Abu Dhabi, and the Northern Emirates are forcing companies to adopt biodegradable alternatives.

- The UAE Circular Economy Policy 2021-2031 is actively driving the phase-out of non-biodegradable waste, pushing manufacturing sectors toward bio-based polymers.

")

Country level Investments & Funding Trends for the Biopolymers Industry:

- India: The renowned sugar company in India, called Balrampur Chini Mills, is planning to invest in a biopolymer plant in India. The investment is worth 2,850 crore as per the published report.(Source: www.thehindubusinessline.com)

- China – the government of China is estimated to impose CO2 emissions in the coming years, where the estimated demand for biobased plastic is 2.53 million tons, according to a survey.(Source: www.plasticstoday.com )

- Europe- the European Union has launched an action plan development of biopolymers, with boosting the capacity of bioplastic production.(Source: www.european-bioplastics.org)

Valus Chain Analysis of Biopolymers Market:

- Distribution to Industrial Users: The major distributors and industrial users are providing custom blends and on-time deliveries, where the eco-friendly shift is contributing to the industry's potential.

- Key Players: Total Corbion PLA, BASF, and Nature Works

- Chemical Synthesis and Processing: Chemical synthesis and processing of biopolymers are divided into various processes, such as dehydration, hydrolysis, esterification, and polycondensation.

- Regulatory Compliance and Safety Monitoring: The regulatory and safety framework depends upon the national and international standards. Mostly, the regulations are implemented according to the respective regional regulatory bodies.

Recent Development

- In April 2026, NatureWorks officially opened a new, fully integrated Ingeo™ biopolymer manufacturing facility in Thailand, marking the company's first dual-production site globally. The Nakhon Sawan facility, which utilizes renewable feedstocks, adds 75,000 metric tons of annual capacity to support growing Asian demand for applications in packaging and 3D printing.(Source: www.businesswire.com)

- In December 2025, Emirates Biotech unveiled Embio, a premium line of polyLactic acid (PLA) biopolymers proudly manufactured in the United Arab Emirates. Engineered as a direct, eco-friendly replacement for conventional petroleum plastics, this homegrown product line underscores the company's core mission to advance biotechnology and regional environmental sustainability.(Source: interplasinsights.com)

- In December 2025, Ecogenesis Biopolymers officially released genTPU, a new plant-based thermoplastic polyurethane filament engineered specifically for Fused Deposition Modeling (FDM) 3D printing. The launch represents a significant milestone in sustainable additive manufacturing, introducing the industry’s first fully biodegradable flexible TPU filament.(Source: www.voxelmatters.com)

Top Vendors in the Biopolymers Market & Their Offerings:

- NatureWorks LLC: One of the largest producers of Polylactic Acid (PLA), marketed under the Ingeo brand, primarily used in packaging and 3D printing.

- Braskem: The pioneer in bio-based polyethylene (Bio-PE) made from sugarcane ethanol, supplying bio-based plastics for packaging, automotive, and consumer goods.

- BASF SE: A major supplier of certified compostable bioplastics, notably through its Ecoflex and Ecovio product lines.

- TotalEnergies Corbion: A global leader specializing in PLA and lactide derivatives used in packaging, agriculture, and durable goods.

Other Top Players Are

- Archer Daniels Midland Company

- DuPont de Nemours, Inc.

- Novamont S.p.A.

- BiologiQ, Inc.

- Mitsubishi Chemical Group Corporation

- Danimer Scientific

- Novamont S.p.A.

- Toray Industries, Inc.

- Biome Bioplastics Limited

- Plantic Technologies Limited

- FKuR Kunststoff GmbH

Segments Covered in the Report

By Product

- Polysaccharides

- Starch-Based Biopolymers

- Cellulose-Based Biopolymers

- Chitosan

- Alginate

- Polyhydroxyalkanoates (PHA)

- Short Chain Length PHA

- Medium Chain Length PHA

- Copolymer PHA

- Polylactic Acid (PLA)

- Thermoforming PLA

- Injection Molding PLA

- Fiber Grade PLA

- Polybutylene Succinate (PBS)

- Bio-based PBS

- Blended PBS

- Bio-based Polyethylene (Bio-PE)

- HDPE Grade

- LDPE Grade

- LLDPE Grade

- Bio-based Polyethylene Terephthalate (Bio-PET)

- Partially Bio-based PET

- Fully Bio-based PET

- Others

- Polyamide Biopolymers

- Protein-Based Biopolymers

- Lignin-Based Biopolymers

By Applications

- Films

- Agricultural Films

- Packaging Films

- Compostable Films

- Bottle

- Beverage Bottles

- Personal Care Bottles

- Pharmaceutical Bottles

- Fibers

- Textile Fibers

- Nonwoven Fibers

- Industrial Fibers

- Seed Coating

- Crop Protection Coatings

- Controlled Release Coatings

- Vehicle Components

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Medical Implants

- Orthopedic Implants

- Drug Delivery Implants

- Tissue Engineering Materials

- Other Applications

- 3D Printing

- Consumer Electronics

- Adhesives

By End-Use

- Packaging

- Flexible Packaging

- Rigid Packaging

- Food Service Packaging

- Consumer Goods

- Household Products

- Personal Care Products

- Electronics Accessories

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Textiles

- Apparel

- Home Textiles

- Technical Textiles

- Agriculture

- Mulch Films

- Seed Treatment Products

- Controlled Release Fertilizers

- Other End-Uses

- Healthcare

- Construction

- Aerospace

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Tags

FAQ's

Select User License to Buy

Figures (5)