Content

What is the Precipitation Hardening Stainless Steel Market Size and Share?

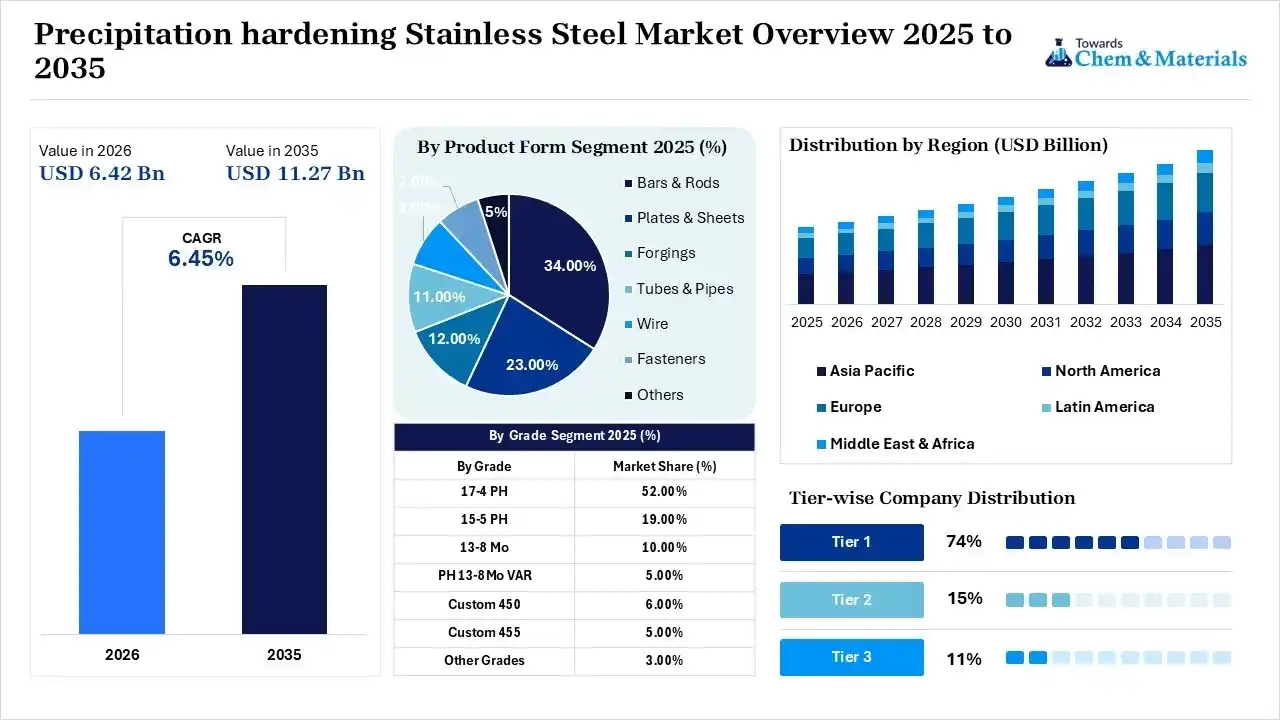

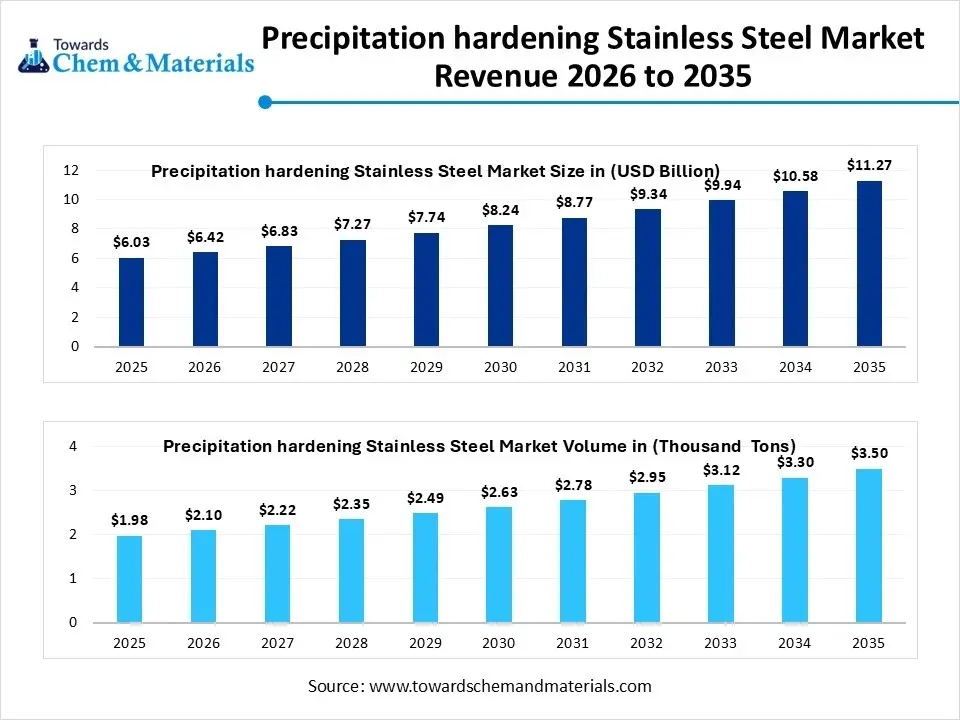

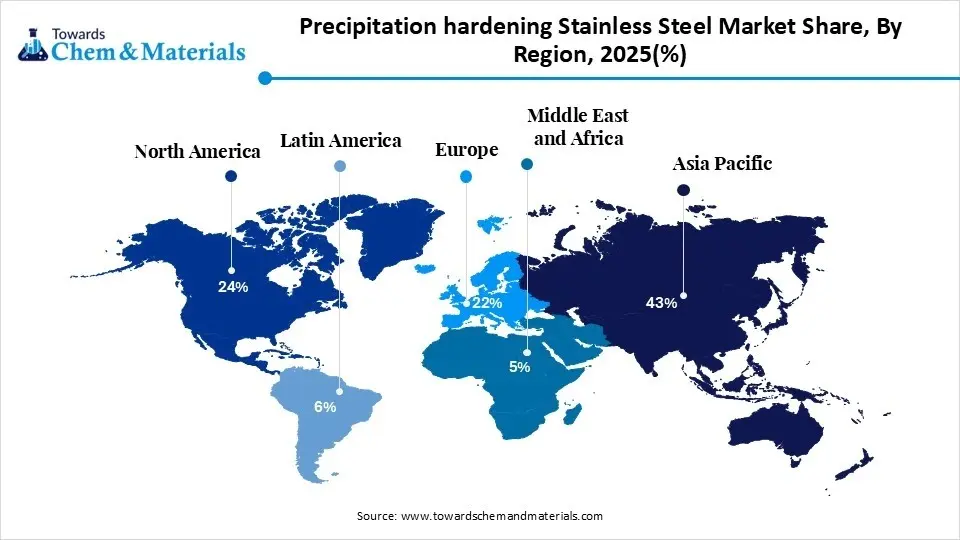

The global precipitation hardening stainless steel market size was valued at USD 6.03 billion in 2025, is estimated to reach USD 6.42 billion in 2026, and is projected to reach USD 11.27 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.45% over the forecast period from 2026 to 2035.Asia Pacific dominated the precipitation hardening stainless steel market with the largest revenue share of 43% in 2025 and is expected to grow at the fastest CAGR of 6.47% during the forecast period. In terms of volume, the precipitation hardening stainless steel market is projected to grow from 1.98 million metric tons in 2025 to 3.50 million metric tons by 2035. growing at a CAGR of 5.85% from 2026 to 2035. The surge in defence and aerospace manufacturing is the major factor leading market growth. Also, strong automotive demand for lightweight materials along with the ongoing innovations in heat treatment processes can impact positive market growth soon.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 43.0% in 2025. The dominance of the region can be attributed to the increasing demand from the automotive and aerospace industries.

- By region, North America held a market share of 24.00% in 2025 and was expected to grow at the fastest CAGR of 7.2% over the forecast period. The growth of the region can be credited to its strong automotive sector transition.

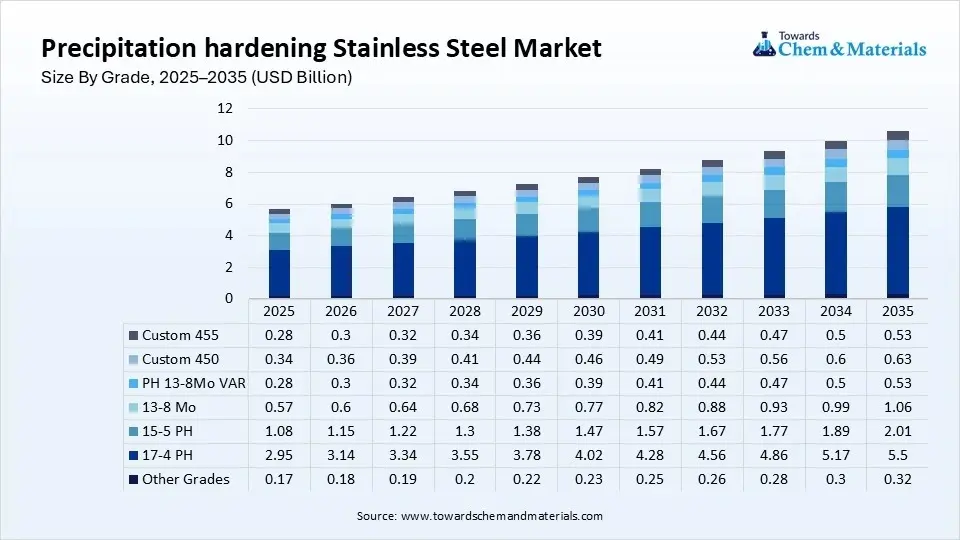

- By grade, the 17-4 PH segment dominated the market with the largest share of 52.0% in 2025. The growth of the segment can be attributed to its unique ability to combine the excellent strength of martensitic stainless steels.

- By grade, the 13-8 Mo segment held a market share of 10.00% in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period. The growth of the segment can be credited to the diffusion-controlled development of body-centred cubic (bcc) β-NiAl intermetallic nano-precipitates.

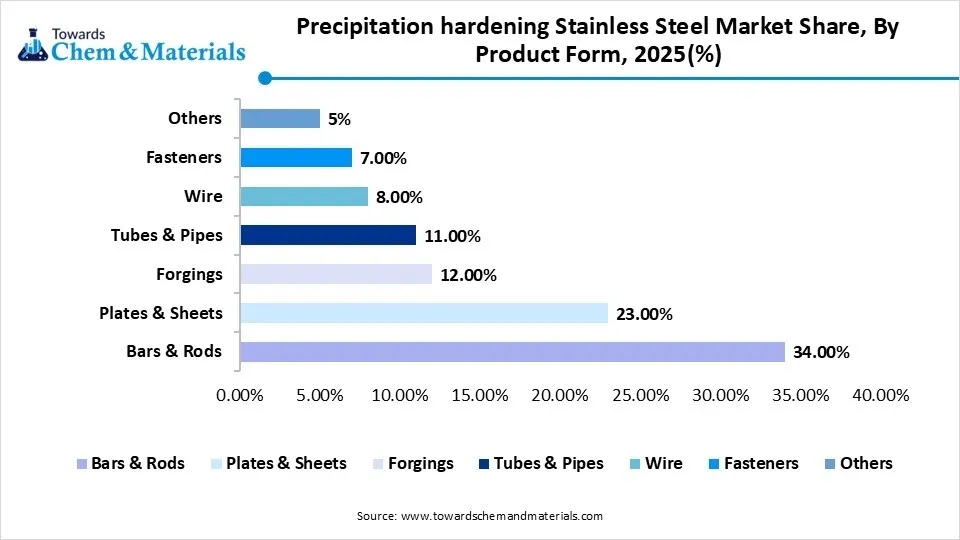

- By product form, the bars & rods segment dominated the market with the largest share of 34.0% in 2025. The dominance of the segment can be linked to the growing application in precision and high-stress sectors.

- By product form, the wire segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.0% over the forecast period. The growth of the segment can be driven by an ongoing and rapid transition towards electric vehicles (EVs).

- By manufacturing process, the hot rolling segment dominated the market with the largest share of 31% in 2025. The dominance of the segment is owing to the increasing aircraft manufacturing and military/defence spending along with the push towards renewable energy storage.

- By manufacturing process, the powder metallurgy segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.6% over the projected period. The growth of the segment is due to growing adoption of additive manufacturing.

- By heat treatment condition, the H900 segment dominated the market with the largest share of 24.0% in 2025. The dominance of the segment can be attributed to its ability to deliver peak tensile and yield strength.

- By heat treatment condition, the H1075 segment held a market share of 10.00% in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The growth of the segment can be credited to its better toughness.

- By end-use industry, the aerospace segment dominated the market with the largest share of 29.0% in 2025. The dominance of the segment can be linked to the growing need for next-generation commercial and defence aircraft.

- By end-use industry, the medical segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period. The growth of the segment can be driven by growth of the biomedical implant sector.

- By distribution channel, the Direct Sales segment dominated the market with the largest share of 46.0% in 2025. The dominance of the segment is owing to the growing demand for customised metallurgical solutions and rigorous traceability.

- By distribution channel, the OEM Supply Contracts segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The growth of the segment is due to growing industrial steel usage.

Industry leaders in aerospace and automotive sectors are heavily demanding precipitation-hardened alloys to develop lighter, stronger components that improve fuel efficiency and overall performance. Additionally, the continued expansion of commercial aviation is expected to drive the adoption of these advanced materials across other industries.

- For instance, in April 2026, Jindal Stainless has officially introduced its 'Jindal Infinity' stainless steel rebars to the Punjab retail market. The commercial rollout began in Amritsar via an intensive two-day engagement programme with industry professionals, architects, and structural engineers.(Source: scanx.trade)

Hence, the transition towards lighter systems creates a lucrative demand across both aftermarket and OEM applications. Growth of maintenance, repair, and overhaul operations is also boosting alloy consumption across component refurbishment and replacement parts.

Global Investment Flow for Precipitation Hardening Stainless Steel 2025

- Strategic investments are generally directed towards niche and high-value sectors like defence systems and aerospace structural components. Major players, particularly in Europe, are investing in "green steel" technologies to adapt to the EU Carbon Border Adjustment Mechanism (CBAM).

- In 2025, the United States exported $16.8B of iron & steel, being the 18th most exported product (out of 98) in the United States. The main destinations of the United States' iron & steel exports were Mexico ($5.87B), Canada ($3.92B), Turkey ($1.36B), Thailand ($833M), and India ($807M).(Source: oec.world)

- In 2025, the United States imported $25.6B of iron & steel, being the 20th most imported product (out of 98) in the United States. The main origins of the United States' iron & steel imports were Canada ($5.37B), Brazil ($3.9B), Mexico ($2.29B), South Korea ($1.43B), and Germany ($1.43B).(Source: oec.world)

- The growth of electric and hybrid vehicle platforms needs high-performance, lightweight materials for extreme stress and environments. Next-generation aerospace programmes and increasing defence budgets are major investment drivers. This investment specifically targets mills manufacturing high-strength-to-weight ratio alloys.

Precipitation Hardening Stainless Steel Market Trends

- Major companies in the market are focusing on developing advanced solutions like stainless steel powder, which is the latest trend in the market, shaping positive market growth. To improve material properties, propel production efficiency, and address the increasing need for corrosion-resistant and strong components.

- In recent years, the surge in aircraft production rates is expected to drive the growth of the market. The growth in aircraft production is boosted by increasing air travel needs and efforts to modernise fleets, as major airlines are seeking to accommodate more passengers and replace outdated ones.

- Rising product utilisation in high-performance industrial applications is the future trend in the market driving expansion. Energy, oil and gas, and medical device sectors are using these materials for their durability and corrosion resistance in demanding applications.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 6.42 Billion/ 2.10 Million Metric Tons |

| Expected Size in 2035 | USD 11.27 Billion/ 3.50 Million Metric Tons |

| Growth Rate | CAGR of 6.45% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Grade, By Product Form, By Manufacturing Process, By Heat Treatment Condition, By End-use Industry, By Distribution Channel |

| Key Companies Profiled | Nippon Steel Corporation, Thyssenkrupp AG, Cleveland-Cliffs Inc., Kobe Steel Ltd., Sandvik AB, Outokumpu Oyj, Aperam S.A., Daido Steel Co Ltd. |

AI-Powered Predictive Formulations in the Precipitation Hardening Stainless Steel Market

AI-powered predictive formulations in the market are increasingly replacing conventional trial-and-error by using thermodynamic data and machine learning (ML) algorithms to facilitate alloy composition and heat-treatment profiles. Furthermore, machine learning helps forecast grain growth, fraction percentages and precipitate behaviour during continuous cooling.

Supply Chain Analysis of the Precipitation Hardening Stainless Steel Market

Production & Processing

- It refers to the specific metallurgical and manufacturing techniques utilised to create high-strength, corrosion-resistant alloys.

- These specialised steels are crucial for demanding applications in automotive, aerospace and oil & gas, fuelled by aerospace and heavy machinery demands.

- ATI (Allegheny Technologies Inc.): A leading U.S.-based manufacturer specialising in high-performance speciality metals, particularly supplying advanced PH alloys (such as Custom 455) to the aerospace and defence sectors.

- Other Key Players: Acerinox, Outokumpu

Quality Testing and Certification

- It ensures that materials like grades 17-4PH and 15-5PH should meet stringent medical, aerospace and industrial standards.

- It also involves verification of chemical composition, hardness, tensile strength and microstructure, supported by mill test certificates (EN 10204 3.1) accompanying shipments.

- Sandvik AB: A major global supplier of high-performance, gas-atomised speciality steel powders and aerospace grades.

- Other Key Players: Outokumpu Oyj, Jindal Stainless Limited

Distribution to Industrial Users

- It includes a direct-to-B2B supply chain where steel producers and service centres sell precipitation hardening (PH) stainless steel directly to end-use sectors such as aerospace, oil & gas, and medical devices.

- Because of their specialised nature, they are rarely sold through generic retail channels.

Sandvik AB: A Swedish high-tech engineering group that is a major producer and supplier of advanced stainless steels and speciality alloys.

- Other Key Players: POSCO, Nippon Steel

Precipitation Hardening Stainless Steel Market’s Regulatory Landscape: Global Regulations

What are the Types of Precipitation Hardening Stainless Steel?

- Martensitic PH Stainless Steels

- These are the most common PH alloys, e.g., 17-4 PH, also known as Grade 630. They are generally delivered in a soft "solution-treated" condition, which makes them easy to machine.

- Common Grades: 17-4 pH, 15-5 pH, and 13-8 mol.

- Semi-Austenitic PH Stainless Steels

- These alloys maintain an austenitic structure after cooling from the annealing temperature, which makes them highly ductile and exceptionally well-suited for demanding cold-forming and deep-drawing processes.

- Common Grades: 17-7 PH (SUS631) and 15-7 Mo (SUS632J1).

- Austenitic PH Stainless Steels

- These alloys retain a consistent austenitic structure throughout both the annealing and ageing phases. They exhibit non-magnetic properties and deliver excellent mechanical performance in high-temperature environments.

- Common Grades: A-286

Precipitation Hardening Stainless Steel Market Dynamics

Driver

Ongoing Transition Towards Alloy Formulations

Market players are increasingly developing innovative precipitation-hardening alloy grades integrating enhanced thermal resistance, better corrosion control and longer fatigue life. In addition, these materials are supporting next-generation aerospace engines, high-performance industrial systems and EV powertrains. This shift is also opening new avenues for suppliers providing specialised alloy solutions specific to harsh environments and high-precision engineering demands.

Restraint

Tedious Multi-Step Thermal Processing

Achieving full strength needs rigid process adherence across rapid cooling, solution treating and subsequent ageing cycles, which is the major factor hindering market growth. Moreover, semi-austenitic variants need sub-zero conditioning down to -100°F to ensure complete martensitic transformation. Also, low-cost foundries often skip complete ageing steps to reduce costs, which leads to latent part failure.

Opportunity

The Rise of Additive Manufacturing & 3D Printing

The surge in digital manufacturing enables complex geometries to be printed directly using PH stainless steel powders, creating lucrative opportunities in the market. This significantly cuts material waste and minimises lead times for prototype components. Furthermore, the shift toward green hydrogen depends on electrolyser plates capable of withstanding constant electrochemical stress. Hence, high-performance alloys provide a notable operational and economic edge over standard carbon steel in this application.

Segmental Insights

Grade Insight

The 17-4 PH segment dominated the market with the largest share of 52.0% in 2025. The growth of the segment can be attributed to its unique ability to combine the excellent strength of martensitic stainless steels with the robust corrosion resistance of austenitic grades. In addition, 17-4 PH is highly sought after for demanding aerospace components like jet engine parts, aircraft fittings, and fasteners where high tensile strength is necessary.

") The 13-8 Mo segment held a market share of 10.00% in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period. The growth of the segment can be credited to the diffusion-controlled development of body-centred cubic (bcc) β-NiAl intermetallic nano-precipitates within a structured lath martensite matrix. Also, the growth is mainly dependent on time and temperature during the ageing cycle.

The 13-8 Mo segment held a market share of 10.00% in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period. The growth of the segment can be credited to the diffusion-controlled development of body-centred cubic (bcc) β-NiAl intermetallic nano-precipitates within a structured lath martensite matrix. Also, the growth is mainly dependent on time and temperature during the ageing cycle.

Precipitation hardening Stainless Steel Market, By Grade, 2025(%)

| By Grade | Market Share (%) |

| 17-4 PH | 52.00% |

| 15-5 PH | 19.00% |

| 13-8 Mo | 10.00% |

| PH 13-8Mo VAR | 5.00% |

| Custom 450 | 6.00% |

| Custom 455 | 5.00% |

| Other Grades | 3.00% |

Product Form Insight

The bars & rods segment dominated the market with the largest share of 34.0% in 2025. The dominance of the segment can be linked to the growing application in precision and high-stress sectors such as defence, aerospace and medical devices, where an excellent strength-to-weight ratio and corrosion resistance are crucial. PH bars and rods (such as grade 17-4 PH) are heavily used to forge aircraft fasteners, turbine blades, and jet engine components.

")

The wire segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.0% over the forecast period. The growth of the segment can be driven by the ongoing and rapid transition towards electric vehicles (EVs) and the rise in demand for precision manufacturing across various end-use sectors. These wires are crucial for producing high-performance aerospace fasteners and flexible bellows.

Precipitation hardening Stainless Steel Market, By Product Form, 2025(%)

| By Product Form | Market Share (%) |

| Bars & Rods | 34.00% |

| Plates & Sheets | 23.00% |

| Forgings | 12.00% |

| Tubes & Pipes | 11.00% |

| Wire | 8.00% |

| Fasteners | 7.00% |

| Others | 5% |

Manufacturing Process Insight

The hot rolling segment dominated the market with the largest share of 31% in 2025. The dominance of the segment is owing to the increasing aircraft manufacturing and military/defence spending along with the push towards renewable energy storage. The surge in adoption of precipitation-hardening stainless steel in innovative medical devices, where it fulfils strict regulatory codes for sterilisation and corrosion resistance, also drives segment growth further.

The powder metallurgy segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.6% over the projected period. The growth of the segment is due to the growing adoption of additive manufacturing and metal injection moulding (MIM) across automotive, aerospace and medical device sectors. Moreover, advancements in gas atomisation technologies have improved powder characteristics further.

Precipitation hardening Stainless Steel Market, By Manufacturing Process, 2025(%)

| By Manufacturing Process | Market Share (%) |

| Hot Rolling | 31.0% (Dominating) |

| Cold Rolling | 24.00% |

| Forging | 18.00% |

| Casting | 12.00% |

| Powder Metallurgy | 8.00% |

| Additive Manufacturing | 7.00% |

- For instance, in July 2025, FOMAS Group is expanding its reach into the aerospace additive manufacturing sector by supplying high-quality, gas-atomised metal powders through its MIMETE brand. Supported by decades of deep metallurgical expertise, the company has established itself as a key supplier of premium materials for advanced 3D printing applications.(Source: www.voxelmatters.com)

Heat Treatment Condition Insight

The H900 segment dominated the market with the largest share of 24.0% in 2025. The dominance of the segment can be attributed to its ability to deliver peak tensile and yield strength and its crucial role across extreme-stress industries such as defence, aerospace and oil and gas. The H900 segment sees persistent use in drilling and exploration equipment where parts must bear intense pressure and corrosive environments without deforming.

The H1075 segment held a market share of 10.00% in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The growth of the segment can be credited to its better toughness, exceptional resistance to stress corrosion cracking and ability to resist pitting and cracking. Furthermore, the H1075 ageing treatment is particularly created to offer peak resistance to SCC in harsh environments.

Precipitation hardening Stainless Steel Market, By Heat Treatment Condition, 2025(%)

| By Heat Treatment Condition | Market Share (%) |

| Solution Annealed | 20.00% |

| H900 | 24.0% |

| H925 | 8.00% |

| H1025 | 16.00% |

| H1075 | 10.00% |

| H1100 | 9.00% |

| H1150 | 9% |

| Other Aging Conditions | 4% |

End-use Industry Insight

The aerospace segment dominated the market with the largest share of 29.0% in 2025. The dominance of the segment can be linked to the growing need for next-generation commercial and defence aircraft coupled with the enforcement of stringent manufacturing and safety regulations. In addition, a surge in global defence spending directly impacts higher manufacturing volumes for military aircraft, helicopters, and missiles.

The medical segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period. The growth of the segment can be driven by growth of the biomedical implant sector and a surge in need for high-strength, corrosion-resistant orthopaedic implants and surgical instruments. Also, pH-neutral stainless steels withstand repeated high-temperature and chemical sterilisation processes without causing any degradation.

Precipitation hardening Stainless Steel Market,By End-use Industry, 2025(%)

| By End-use Industry | Market Share (%) |

| Aerospace | 29.00% |

| Oil & Gas | 18.00% |

| Automotive | 12.00% |

| Medical | 8.00% |

| Chemical Processing | 9.00% |

| Marine | 6.00% |

| Defense | 8% |

| Energy | 5% |

| Industrial Machinery | 3% |

| Others | 2% |

Distribution Channel Insight

The direct sales segment dominated the market with the largest share of 46.0% in 2025. The dominance of the segment is owing to the growing demand for customised metallurgical solutions, rigorous traceability and extended technical support in high-stakes sectors such as defence and aerospace. Furthermore, the ongoing transition towards lightweight high-strength materials in hybrid and electric vehicles needs exact alloy formulation, supporting producer-to-engineer relationships.

The OEM Supply Contracts segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The growth of the segment is due to growing industrial steel usage and fluctuations in necessary alloying elements such as nickel, chromium, and molybdenum. Automotive lines heavily depend on gas-atomised and high-uniformity spherical grades, which are secured via strategic OEM sourcing.

Precipitation hardening Stainless Steel Market, By Distribution Channel, 2025(%)

| By Distribution Channel | Market Share (%) |

| Direct Sales | 46.00% |

| Distributors & Stockists | 28.00% |

| OEM Supply Contracts | 18.00% |

| Online Industrial Platforms | 8.00% |

What are the Benefits of Precipitation Hardening Stainless Steel?

Precipitation hardening (PH) stainless steel gives an excellent blend of ultra-high tensile strength (850–1700 MPa), high corrosion resistance and the ability to be conveniently machined in a soft state before being heat-treated to exact specifications.

They offer much more robust toughness than conventional plain martensitic stainless steels while retaining better corrosion performance in harsh marine and chemical environments. Due to these benefits, these alloys are extensively used in crucial applications such as industrial machinery, aerospace components and offshore marine equipment.

Regional Analysis

How did Asia Pacific Dominated the Precipitation Hardening Stainless Steel Market in 2025?

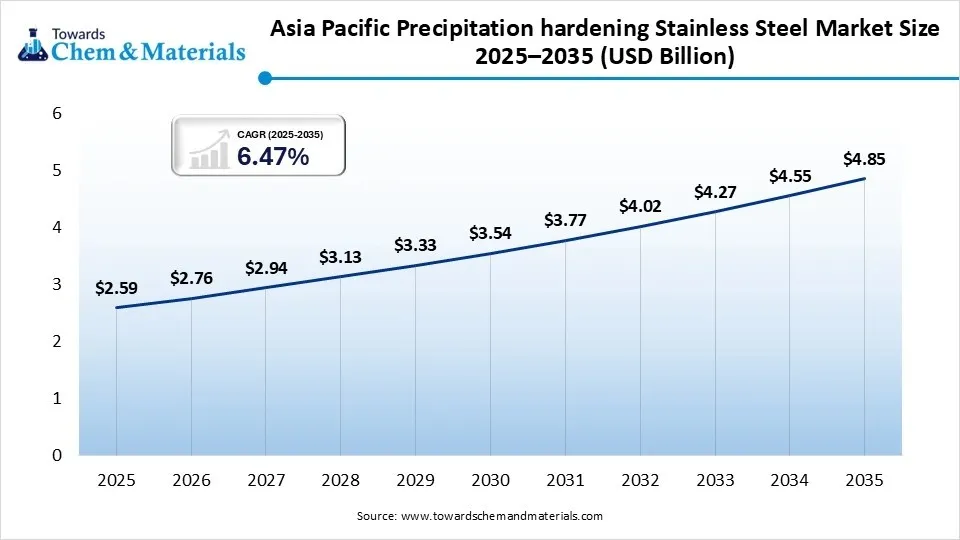

The Asia Pacific precipitation hardening stainless steel market size was estimated at USD 2.59 billion in 2025 and is projected to reach USD 4.85 billion by 2035, growing at a CAGR of 6.47% from 2026 to 2035. Asia Pacific dominated the market with a share of 43.0% in 2025. The dominance of the region can be attributed to the increasing demand from the automotive and aerospace industries along with the ongoing infrastructure development in emerging economies. In addition, the region's transition to next-generation renewable energy infrastructure and nuclear reactors needs highly stress-tolerant stainless-steel grades.

") China

China

- The ongoing shift toward electric and hybrid vehicles requires lightweight, highly durable materials for structural, battery, and drivetrain components in the country. Also, growing investments in renewable energy, nuclear power, and domestic oil/gas extraction necessitate materials that can withstand extreme environments without degrading.

India

- The automotive sector in India is expanding rapidly, with a shift towards lightweight, durable materials to meet crash-safety standards and support the rising electric and hybrid vehicle platforms. The need for high-strength, corrosion-resistant, and sterilisable surgical instruments and advanced medical devices is continuously pushing PH stainless steel consumption in an upward direction.

North America

The North America precipitation hardening stainless steel market size was estimated at USD 1.45 billion in 2025 and is projected to reach USD 2.70 billion by 2035, growing at a CAGR of 6.41% from 2026 to 2035. North America held a market share of 24.00% in 2025 and was expected to grow at the fastest CAGR of 7.2% over the forecast period. The growth of the region can be credited to its strong automotive sector transition, aerospace manufacturing and extensive infrastructure modernisation. Also, the push for strict automotive efficiency standards needs durable and lightweight materials.

United States

Automotive engineers are increasingly specifying high-strength alloys to produce lighter structural components and battery enclosures for electric vehicle (EV) platforms. Investments in additive manufacturing, digital process analytics, and precision heat-treating technologies are optimising production and lowering overall costs.

Canada

The increasing demand for lightweight, corrosion-resistant, and high-tensile components such as landing gear, turbine blades, and engine parts is a primary growth driver in the country. Urban infrastructure and environmental mandates, such as those implemented in Toronto's green building codes, need the use of long-lasting, highly durable structural steel.

Europe

The Europe precipitation hardening stainless steel market size was estimated at USD 1.33 billion in 2025 and is projected to reach USD 2.48 billion by 2035, growing at a CAGR of 6.43% from 2026 to 2035. Europe held a market share of 22.00% in 2025. The growth of the region can be linked to the increasing need for high-strength materials in harsh environments and the shift towards electric vehicles (EVs). Moreover, ongoing manufacturing in next-generation aerospace programmes and a surge in defence expenditures depend heavily on PH alloys to fulfil rigorous strength-to-weight standards.

Germany

Germany's world-class medical technology sector depends heavily on PH stainless steel for precision surgical instruments and implantable devices that demand exceptional hardness and biocompatibility. The transition to electric and hybrid vehicles needs lightweight yet highly robust materials, propelling regional demand for precipitation-hardened alloys.

France

The country's demand for durable, corrosion-resistant, and high-strength medical components uses precision-treated PH alloys to build advanced surgical instruments and implants. French automotive manufacturers are increasingly substituting traditional low-sulphur or carbon steels with high-strength, corrosion-resistant alloys.

Latin America

The Latin America precipitation hardening stainless steel market size was estimated at USD 0.36 billion in 2025 and is projected to reach USD 0.68 billion by 2035, growing at a CAGR of 6.57% from 2026 to 2035. Latin America held a market share of 6.00% in 2025. The growth of the region can be driven by ongoing urbanisation and a surge in demand for corrosion-resistant materials, along with the expanding aerospace and automotive sectors. Moreover, precipitation-hardening (PH) stainless steels, such as the widely used 17-4 PH alloy, are increasingly used in medical device manufacturing. They are valued for combining biological safety and exceptional structural durability.

Brazil

Increasing vehicle manufacturing across emerging markets in Brazil has fuelled the need for durable, high-strength, and lightweight materials. Surged construction activities for residential and commercial structures, particularly in urban centres throughout Mexico and Brazil, are fuelling the demand for durable metals.

Argentina

Global players in the country, such as Tsingshan Holding Group, have established strategic ties in Argentina, solidifying a steady pipeline of base material supply. The country's massive agricultural export market drives consistent demand for robust, wear-resistant, and corrosion-resistant processing equipment.

Middle East & Africa

The Middle East & Africa precipitation hardening stainless steel market size was estimated at USD 0.30 billion in 2025 and is projected to reach USD 0.56 billion by 2035, growing at a CAGR of 6.44% from 2026 to 2035. The Middle East & Africa held a market share of 5.00% in 2025. The growth of the region can be attributed to the growing oil and gas extraction, huge destination projects and surge in infrastructure projects. Furthermore, regional governments are extending their aviation, aerospace and defence capabilities, leading to regional growth soon.

") Saudi Arabia

Saudi Arabia

Massive developments such as NEOM and the Red Sea Project are propelling unprecedented demand for highly durable, high-strength materials in commercial construction. Also, the country is expanding its domestic aerospace and military manufacturing capabilities; therefore, lightweight yet exceptionally strong PH stainless steels are in high demand.

UAE

The UAE government's push toward green steelmaking, sustainable production, and circular economy practices is shifting procurement toward high-durability materials that lower lifecycle maintenance costs, leading to market growth shortly. Increasing local industrialisation has also driven the need for wear-resistant and highly precise stainless-steel parts across high-performance industries.

Recent Developments

- In May 2026, Canada is launching a C$1 billion loan programme to help industries affected by US tariffs. This initiative specifically targets businesses that manufacture and export steel, aluminium, and copper products. This is anticipated to allow companies to adapt to new trade conditions and remain competitive in foreign markets.(Source: gmk.center )

https://gmk.center/en/news/canada-is-launching-a-730-million-program-for-industry-in-response-to-u-s-tariffs/

Competitive Analysis

- The market is consolidated and highly competitive, consisting of global steel giants and specialised alloy manufacturers emphasising premium, vacuum-melted products for crucial applications. Suppliers are targeting aerospace and medical segments, emphasising vacuum induction melting (VIM) and vacuum arc remelting (VAR) techniques to reduce impurities.

- ArcelorMittal S.A. is positioning itself as a core player in the global precipitation hardening (PH) stainless steel market. The company operates primarily through its specialised heavy plate and speciality alloy subsidiary.

- Nippon Steel Corporation manufactures multi-phase and precipitation hardening grades (such as the popular 630/17-4 PH compositions) designed to bear high stress without compromising corrosion resistance (NAS630).(Source: www.nipponsteel.com),(Source: industeel.arcelormittal)

Strategic Profiles of Key Players Shaping the Precipitation Hardening Stainless Steel Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| Carpenter Technology | Market Leader / Premium Specialty Alloy Producer | Wyomissing,Pennsylvania, USA | Global (Americas, Europe, Asia-Pacific) | CarTech Custom 455, Custom 465, 15-5 PH, and 17-4 PH stainless steels. | Ultra-high strength vacuum induction melted (VIM) steels for critical aerospace components. |

| Swiss Steel Group | Global Producer / Long Products Specialist | Lucerne, Switzerland | Global production and distribution networks. | PH steel bars, wire rods, and semi-finished long products. | Advanced corrosion resistance combined with high structural hardness for severe industrial environments. |

| AK Steel (Cleveland-Cliffs) | Major Industrial Supplier / Original PH Innovator | Cleveland, Ohio, USA | North America (Primary manufacturing focus) | Standard 17-4 PH, 15-5 PH, and 17-7 PH flat-rolled sheets and plates. | Invented the original 17-4 PH alloy, holding deep technical data sets for aerospace and chemical processing. |

Other Key Players

- Nippon Steel Corporation

- Thyssenkrupp AG

- Cleveland-Cliffs Inc.

- Kobe Steel Ltd.

- Sandvik AB

- Outokumpu Oyj

- Aperam S.A.

- Daido Steel Co Ltd.

Segments Covered in the Report

By Grade

- 17-4 PH (AISI 630)

- Solution Annealed

- H900

- H1025

- H1150

- 15-5 PH

- H900

- H1025

- H1075

- 13-8 Mo

- Solution Treated

- Aged Condition

- PH 13-8Mo VAR

- Custom 450

- Custom 455

- Other PH Stainless Steel Grades

By Product Form

- Bars & Rods

- Round Bars

- Flat Bars

- Hex Bars

- Plates & Sheets

- Hot Rolled

- Cold Rolled

- Forgings

- Tubes & Pipes

- Seamless

- Welded

- Wire

- Fasteners

- Others

By Manufacturing Process

- Hot Rolling

- Cold Rolling

- Forging

- Casting

- Powder Metallurgy

- Additive Manufacturing

By Heat Treatment Condition

- Solution Annealed

- H900

- H925

- H1025

- H1075

- H1100

- H1150

- Other Aging Conditions

By End-use Industry

- Aerospace

- Aircraft Structures

- Landing Gear

- Engine Components

- Oil & Gas

- Downhole Equipment

- Valves

- Pumps

- Automotive

- Transmission Components

- Performance Parts

- Medical

- Surgical Instruments

- Orthopedic Devices

- Chemical Processing

- Marine

- Defense

- Energy

- Industrial Machinery

- Others

By Distribution Channel

- Direct Sales

- Distributors & Stockists

- OEM Supply Contracts

- Online Industrial Platforms

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (6)