Content

What is the C-9 Solvent Market Size and Share?

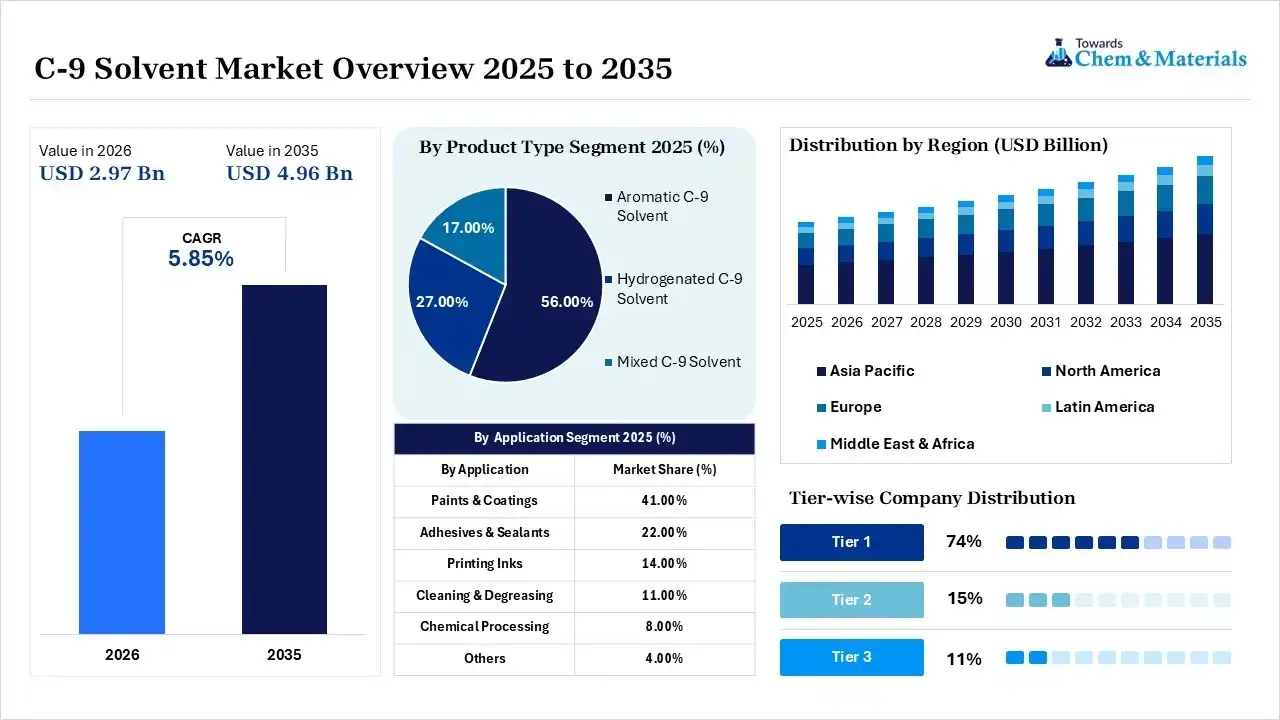

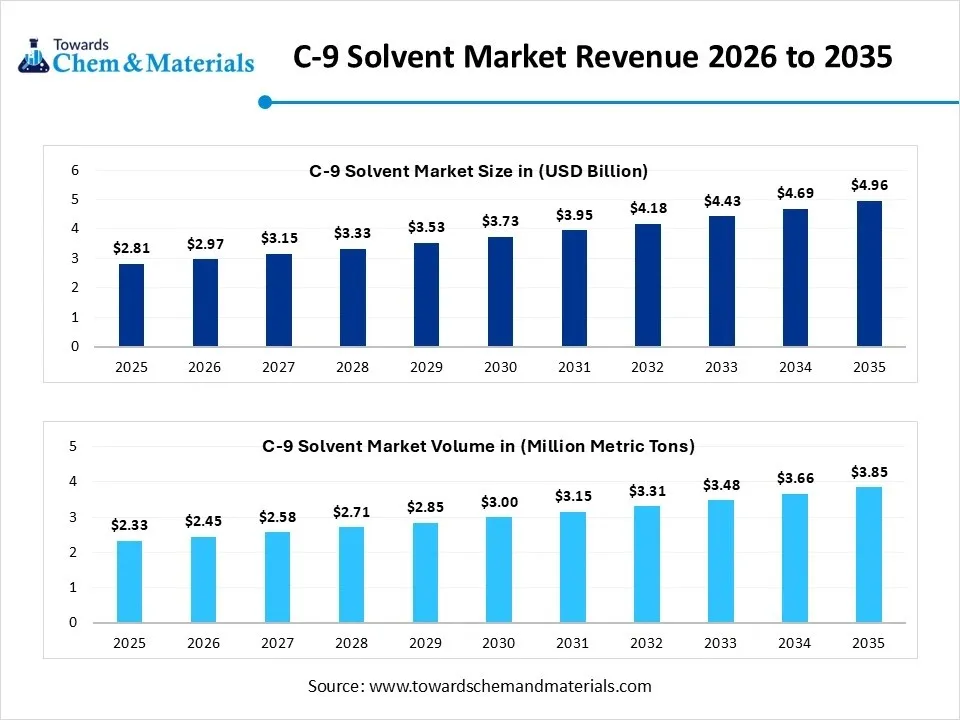

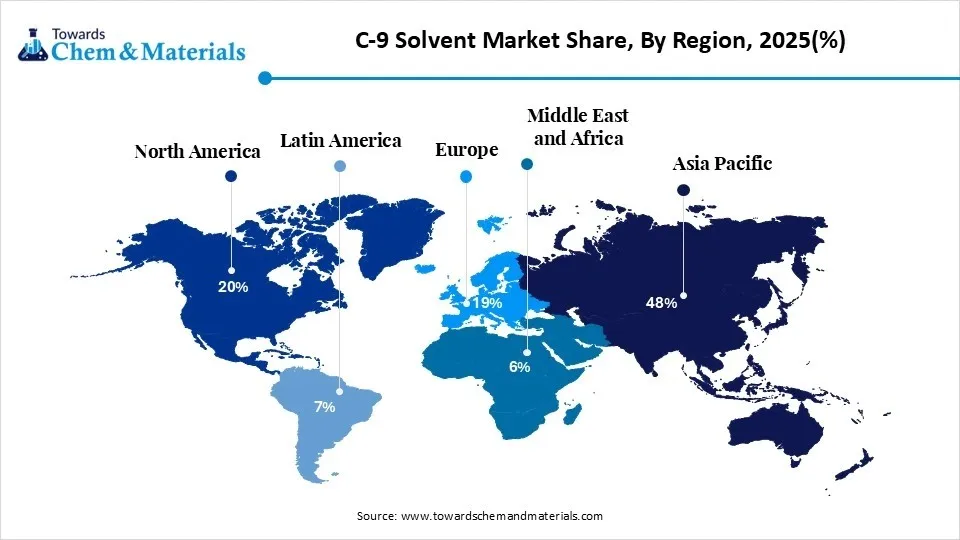

The global C-9 solvent market size was valued at USD 2.81 billion in 2025, is estimated to reach USD 2.97 billion in 2026, and is projected to reach USD 4.96 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035. Asia Pacific dominated the C-9 solvent market with the largest revenue share of 48% in 2025 and is expected to grow at the fastest CAGR of 5.97% during the forecast period.

The Ongoing refinery investments as well as downstream investments in petrochemicals also enhance production efficiency and long-term supply security. The C-9 solvent market is on the verge of continued growth, driven by a number of key sectors, such as paints, coatings, adhesives, agrochemicals, and construction. Market demand will continue to be strong thanks to rising investments in infrastructure, growth in industrial manufacturing, growth in automotive production, and the shift to low-VOC solvent formulations.

Market Highlights

- The Asia Pacific dominated the C-9 solvent market with the largest revenue share of 48% in 2025 and is expected to grow at a CAGR of 5.97% during the forecast period.

- The North America held 20% market share in 2025 and is expected to grow at a CAGR of 5% during the forecast period.

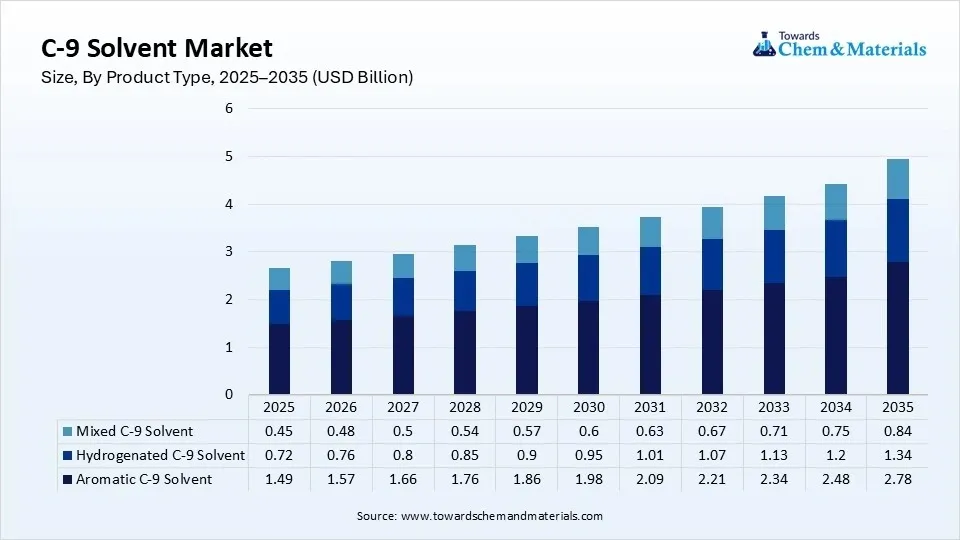

- By product type, the aromatic C-9 solvent segment dominated the market with the largest share of 56% in 2025 and is expected to grow at a CAGR of 5.5% during the forecast period.

- By product type, the hydrogenated C-9 solvent segment held 27% market share in 2025 and is expected to grow at the fastest CAGR of 6.6% over the forecast period.

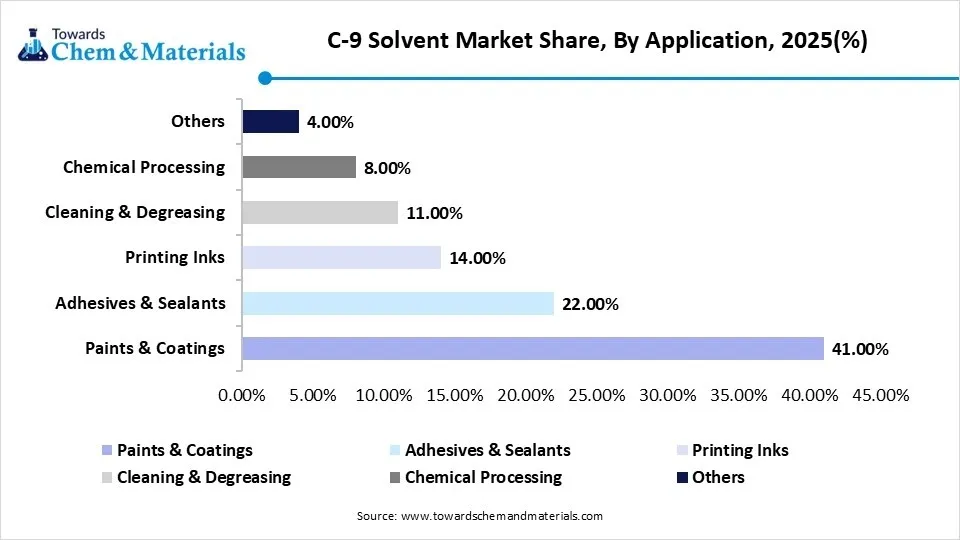

- By application, the paints & coatings segment dominated the market with the largest share of 41% in 2025 and is expected to grow at a CAGR of 5.6% during the forecast period.

- By application, the adhesives & sealants segment held 22% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period.

- By end use, the construction segment dominated the market with the largest share of 33% in 2025 and is expected to grow at a CAGR of 5.6% during the forecast period.

- By end use, the chemical segment held 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.5% over the forecast period.

According to Towards Chemicals and Materials Analytics and Consulting, the global C-9 solvent market volume was valued at 2.33 million metric tons in 2025 and is expected to surpass around 3.85 million metric tons by 2035, accelerating a compound annual growth rate (CAGR) of 5.15% over the forecast period from 2026 to 2035.

The chemicals used in architectural coatings, industrial paints, and protective finishes with high-performance C-9 solvents are also in demand as construction activities grow. Continued growth in automotive manufacturing continues to drive solvent use in OEM and refinishing uses. As agrochemical production grows, so will the need for efficient solvent carriers to enhance the stability of the formulation and the dispersion of the ingredients. Increased rubber processing and adhesive production also contribute to solvent use by improving the compatibility between rubber and adhesive in various industrial applications to improve the processing efficiency.

The increasing regulations for the environment could push manufacturers to create hydrogenated C-9 solvents that have less odor, lower volatile organic compound (VOC) emissions, and less risk in the workplace. Growing investments in the petrochemical industry in the Asia Pacific offer opportunities for production in the region and improved supply security.

- For instance, in November 2025, Construction of a heavy naphtha catalytic reforming and hydrotreating unit began at Sonatrach's Arzew Industrial Zone in Algeria. The project will expand refinery production and boost the demand for aromatic hydrocarbons for chemical applications.(Source: al24news.dz)

As specialty adhesives, industrial sealants, and high-quality printing inks are increasingly required for specific applications, product development continues to support this. Circular economy programs also promote investments in sustainable production and solvent recovery technology. The key players in the market are ExxonMobil, Shell, Eastman Chemical Company, Chevron Phillips Chemical Company, TotalEnergies, Reliance Industries, Indian Oil Corporation Limited (IOCL), Haldia Petrochemicals, S-OIL Corporation, and Korea Petrochemical Industry Co., Ltd.

The C-9 solvent value chain continued to get stronger with growing investment in naphtha crackers and aromatic hydrocarbon production. Refiners are scaling up capacity on the upstream side to ensure a reliable feedstock supply and minimise supply disruptions. These projects help boost production efficiency and benefit industries downstream, such as paints and coatings, adhesives, and specialty chemicals.

Manufacturers are investing large amounts of capital in cleaner solvent technologies that meet tighter and tighter environmental regulations. Production technologies are also encouraging producers to reduce VOCs while maintaining solvent performance, through hydrogenation methods and emission-control systems, among other measures, which are leading to more energy-efficient production.

Major petrochemical players are still investing in the upgrading of refineries and backward integration to secure feedstocks and boost production resilience. Increased aromatic recovery, lower operational costs, and reduced energy use with advanced processing technologies.

Market Trends

- Paints and coatings continue to be the top consumer of C-9 solvents because of their good solvent properties and slow evaporation rates. Solvent demand continues to be fueled by growth in residential building, infrastructure modernization, and the manufacturing of automobiles throughout the world.

- Manufacturers are still being incentivized by environmental regulations to replace conventional aromatic solvents with those that are less harmful through VOC reduction, lower levels of odor, and are hydrogenated.

- Petrochemical companies push more and more to combine refining and downstream chemical production to guarantee the uninterrupted availability of the aromatic feedstocks. Backward integration enhances efficiency in production and minimises reliance on raw materials and supply chains.

- C-9 solvent producers are finding new opportunities in industrial adhesives, sealants, rubber processing, and specialty manufacturing. For advanced adhesive formulations, solvents with good resin compatibility and controlled drying properties are needed.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 2.97 Billion/ 2.45 Million Metric Tons |

| Expected Size in 2035 | USD 4.96 Billion/ 3.85 Million Metric Tons |

| Growth Rate | CAGR of 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Production Process, By Purity, By Application, By End-use Industry, By Distribution Channel, By Region |

| Key Companies Profiled | ExxonMobil, Shell, Eastman Chemical Company, INEOS, LyondellBasell, Formosa Plastics Corporation, Mitsubishi Chemical, Eni (Versalis) |

Key Technological Shifts and AI in the C-9 Solvent Market

Hydrogenation technologies are becoming increasingly popular with manufacturers to prevent the creation of C-9 solvents that emit VOC, reduce the amount of aromatics in the solvent, and are cleaner in terms of odor. These higher grades meet strict environmental standards and have outstanding solvency and resin compatibility. Refiners are also being encouraged to upgrade their manufacturing plants to provide more modern facilities and increase their premium solvent offering for specialty chemical applications, coatings, and adhesives, as customers increasingly demand sustainable chemical products. Automated refining systems, digital process control, and predictive maintenance platforms are being introduced into solvent production facilities, and these solutions are still being integrated by petrochemical manufacturers. These technologies enhance operational efficiency, catalyst utilization, energy efficiency, and product quality.

Supply Chain Analysis of the C-9 Solvent Market

Feedstock Procurement

- This phase includes procurement of heavy aromatic naphtha, pyrolysis gasoline, reformate streams, and other petroleum-derived hydrocarbons used to produce C-9 solvents.

- Stable feedstock supply, refinery integration, and efficient logistics guarantee uninterrupted production and reduce the price volatility of feedstocks in global petrochemical supply chains.

- Essel Gas & Power Limited: Reliance Industries' integrated refinery and petrochemical plants provide assured availability of aromatic feedstocks.

- Other Key Players: ExxonMobil, Shell plc, Indian Oil Corporation Limited (IOCL), and Saudi Aramco.

Chemical Synthesis and Processing

- The aromatic feedstocks are treated by the refineries through catalytic reforming, fractional distillation, hydrogenation, purification technologies, and high-quality C-9 solvent grades are produced.

- Advanced process control optimizes production, energy use, environmental compliance, and operational efficiency, while enhancing aromatic composition and purity of the product and lowering production costs.

- Chevron Phillips Chemical: Produces high-purity aromatic solvents using state-of-the-art refining technologies and ensures consistent quality and industrial performance.

- Other Key Players: Eastman Chemical Company, TotalEnergies, S-OIL Corporation, SK Geo Centric.

Formulating and Blending Compounds

- Purified C-9 solvents are mixed with specialty hydrocarbons and performance additives to obtain the desired volatility, flash point, evaporation rate, and solvency properties.

- Formulations tailored for coatings, adhesives, agrochemicals, and printing inks, as well as for application-specific performance for specialty industrial applications.

- Minor Player: Insco, Jr. Player: Indiana University of Health Science.

- Insco: Eastman creates special solvent blends that enhance the compatibility of resins, application efficiency, and formulation performance in industrial applications.

- Other Key Players: Monument Chemical, DEZA a.s., Shell Chemicals, and ExxonMobil Chemical.

Regulatory Framework: C-9 Solvent Market

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| Asia Pacific | Ministry of Ecology and Environment (China), Central Pollution Control Board (India), Ministry of Environment (Japan) | China VOC Emission Standards, India's Chemical (Management and Safety) Rules, Japan Chemical Substances Control Law (CSCL) | VOC emission reduction, hazardous chemical management, workplace safety, industrial air quality, sustainable solvent production, and environmental compliance. |

| North America | U.S. Environmental Protection Agency (EPA), Occupational Safety and Health Administration (OSHA), Environment and Climate Change Canada (ECCC) | Clean Air Act (CAA), Toxic Substances Control Act (TSCA), Hazard Communication Standard (HCS), Canadian Environmental Protection Act (CEPA) | VOC control, worker safety, chemical registration, hazardous substance handling, emissions monitoring, and environmental protection. |

| Europe | European Chemicals Agency (ECHA), European Commission | REACH Regulation (EC 1907/2006), CLP Regulation (EC 1272/2008), Industrial Emissions Directive (IED), Solvent Emissions Directive (SED) | Chemical registration, solvent classification, emission reduction, occupational health, environmental sustainability, and industrial compliance. |

What is C-9 Solvent, and What Are the Major Types of C-9 Solvent?

C-9 solvent is a mixture of aromatic hydrocarbons exhibiting the properties of a petroleum solvent, which contains the majority of aromatic compounds with a total of 9 carbon atoms. It is formed during the refining and processing of petroleum streams, especially those of aromatic fractions from petrochemical processing. The principal ingredients are aromatic hydrocarbons, primarily trimethylbenzene and ethyltoluene isomers, and other related hydrocarbons that have outstanding solvent properties. C-9 solvent has become an important raw material in a number of industrial applications because of its powerful dissolving ability, controlled evaporation, and ability to be used with a variety of chemical formulations.

Growing industrial manufacturing, construction, production of automotive coatings, packaging growth, and growth of chemical processing industries are driving the demand for C-9 solvents. They are useful in possible alternative formulation processes because they are capable of delivering good solvency without compromising the desired drying and application properties.

How Many Major Categories of C-9 Solvents are There?

C-9 solvents can be broadly grouped by the production processes, the chemical composition, and the end-use applications. The major types include:

Heavy Aromatic Solvent (HAS):

Heavy aromatic solvents are by-products of the petroleum refining processes and have a high concentration of aromatic hydrocarbons. They are high in aromatic properties and have high solvency power with lower evaporation rates. Industrial coatings, paints, pesticides, agricultural formulations, printing and cleaning agents are examples of applications that typically use HAS grades.

Aromatic Hydrocarbon Resin (C-9 Resin):

C-9 resin is a solid thermoplastic resin that is manufactured by a polymerization process of C-9 aromatic hydrocarbon fractions. Serves as a tackifier, adhesion promoter, and performance modifier in various applications. With their exceptional compatibility and bonding characteristics, these resins are extensively employed in adhesives, sealants, rubber compounds, printing inks, and hot-melt road marking materials.

Specialty/Cut Grades:

Solvent grades are specialty grades of solvents that are created by using certain distillation processes to obtain the desired boiling range and evaporation rate. Specially formulated grades for precision performance applications, including offset printing inks, specialty coatings, and superior industrial formulations. They have a controlled evaporation profile, which contributes to more efficient processing as well as product quality.

C-9 Solvent Market Dynamics

Driver

Paints and Coatings Boom

The consumption of C-9 solvents is still expanding rapidly in the construction, automotive manufacturing, and industrial infrastructure sectors around the world. The solvents possess excellent solvency, evaporation control, and compatibility with resins employed in paints, coatings, adhesives, and rubber products. Growing infrastructure investments in emerging economies continue to drive market demand, as do rising protective coatings, marine applications, and industrial maintenance spending in various industrial sectors.

Restraint

Stringent Environmental Regulations:

Amplification of VOC emission regulations continues to pose challenges for established C-9 solvent producers. Governments are adopting increasingly demanding criteria for emissions, worker exposure, chemical handling, and hazardous air pollutants. Compliance requires big capital expenditures for cleaner production technologies, emission control equipment, and reformulated solvent products. Demand for aromatic solvents is also under pressure in environmentally controlled applications due to growing customer demand for water-based and bio-based products.

Opportunity

Low-VOC and Low-Odor Innovations:

Manufacturers of environmentally friendly C-9 solvents have good opportunities to improve due to a growing demand for such products in various industrial applications. High-purity, low-odor solvents are possible because of advanced refining technologies for use in premium coatings, specialty adhesives, electronics, and chemical processing applications. Increased investment in sustainable manufacturing, solvent recovery technologies, and circular economy projects continues to foster innovation and bolster market opportunities in developed and emerging economies.

C-9 Solvent Key Benefits and Industrial Uses

Paints and Coatings Applications:

C-9 is widely utilized in industrial paints and coating formulations where its excellent resin-dissolving ability and viscosity control properties are needed. It aids in achieving smooth application, uniform coating thickness, and better surface appearance for manufacturers. In automotive coatings, marine coatings, and protective coatings for infrastructure like bridges, C-9 solvent is used to improve gloss, surface hardness, durability, and water resistance. The low evaporation rate also enhances drying efficiency and coating quality.

Printing Ink Production:

C-9 solvent is a key component of offset printing inks and specialty inks. It enhances pigment dispersion, keeps the ink viscosity in check, and ensures an even ink flow during printing processes. The solvent's evaporation rates aid in maintaining uniformity of drying times while minimizing problems like uneven printing or drying times. It also helps to increase the water-resistant properties and improve the performance of printed items.

Agricultural Chemical Formulations:

C-9 solvent is used as an effective solvent and carrier in the agrochemical industry for non-water-soluble pesticides, herbicides, and other crop protection products. It can ensure even distribution of the active ingredient, enhance formulation stability, and aid penetration through a waxy leaf surface. These properties help to increase the bioavailability and efficacy of use of agricultural chemicals.

Adhesives and Rubber Processing:

C-9 solvent is an excellent solvent for synthetic rubbers, resins, and polymer materials, which is useful for the adhesive and rubber industries. It is commonly employed in road marking formulations, sealants, hot-melt, and pressure-sensitive adhesives. The solvent promotes bonding characteristics, increases processing flexibility, and enables the creation of long-lasting industrial products.

Industrial Cleaning and Specialty Applications:

C-9 solvent's good solvency properties are also used in specialty chemical formulations and industrial cleaning. It cleanses organic residues, oils, and other contaminants while keeping formulation efficiencies at a maximum in a wide range of industrial applications.

Segmental Insights

Product Type Insights

The aromatic C-9 solvent segment dominated the market with the largest share of 56% in 2025 and is expected to grow at a CAGR of 5.5% over the forecast period, owing to good solvency, high resin compatibility, and low production cost. It is used on a broad front in paints, coatings, printing inks, rubber processing, and industrial cleaning. Its widespread industrial use and good availability from petroleum refineries also contributed to its well-established market position in both developed and emerging economies.

")

The hydrogenated C-9 solvent segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 6.6% over the forecast period. Rising regulations continue to push the use of grades with lower amounts of odors, aromatic compounds, and VOCs. These solvents provide a better working environment protection and still have good formulation stability and solvency. The market is projected to grow at a faster pace in the long term due to the increasing demand for premium coatings, adhesives, electronics, and specialty chemicals.

C-9 Solvent Market Share, By Product Type, 2025(%)

| By Product Type | Market Share (%) |

| Aromatic C-9 Solvent | 56.00% |

| Hydrogenated C-9 Solvent | 27.00% |

| Mixed C-9 Solvent | 17.00% |

Application Insights

The paints & coatings segment dominated the market with the largest share of 41% in 2025 and is expected to grow at a CAGR of 5.6% over the forecast period, due to the demand for solvents remaining strong from all sectors of residential construction as well as commercial infrastructure, automotive manufacturing, and industrial maintenance. The C-9 solvents are indispensable components of coatings formulations in both the architectural and industrial sectors, providing superior resin dissolution, viscosity control, drying, and coating durability.

")

The adhesives & sealants segment held the 22% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period, as demand for packaging, automotive assembly, and industrial manufacturing increases. C-9 solvents provide better resin compatibility, application consistency, and drying capabilities, and can be used to formulate high-performance adhesives for a wide range of industrial applications.

C-9 Solvent Market Share, By Application, 2025(%)

| By Application | Market Share (%) |

| Paints & Coatings | 41.00% |

| Adhesives & Sealants | 22.00% |

| Printing Inks | 14.00% |

| Cleaning & Degreasing | 11.00% |

| Chemical Processing | 8.00% |

| Others | 4.00% |

End Use Insights

The construction segment dominated the market with the largest share of 33% in 2025 and is expected to grow at a CAGR of 5.6% over the forecast period. Demand for paints, coatings, waterproofing materials, adhesives, and sealants is still growing due to the increased residential housing, commercial buildings, transportation infrastructure, and industrial projects. Long-term consumption of C-9 solvent-based construction materials remains robust as the economy of emerging economies continues to urbanize.

The chemical segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.5% over the forecast period, owing to the continuing growth in specialty chemicals production, industrial resins, agrochemicals, and performance materials. C-9 solvents are used as effective processing agents, reaction solvents, and formulation additives, and are used in chemical production facilities to enhance manufacturing efficiency and product consistency.

C-9 Solvent Market Share, By End-Use Industry, 2025(%)

| By End-Use Industry | Market Share (%) |

| Construction | 33.00% |

| Automotive | 22.00% |

| Chemical | 18.00% |

| Packaging | 14.00% |

| Industrial Manufacturing | 8.00% |

| Others | 5.00% |

Regional Insights

How Did the Asia Pacific Dominate the C-9 Solvent Market In 2025?

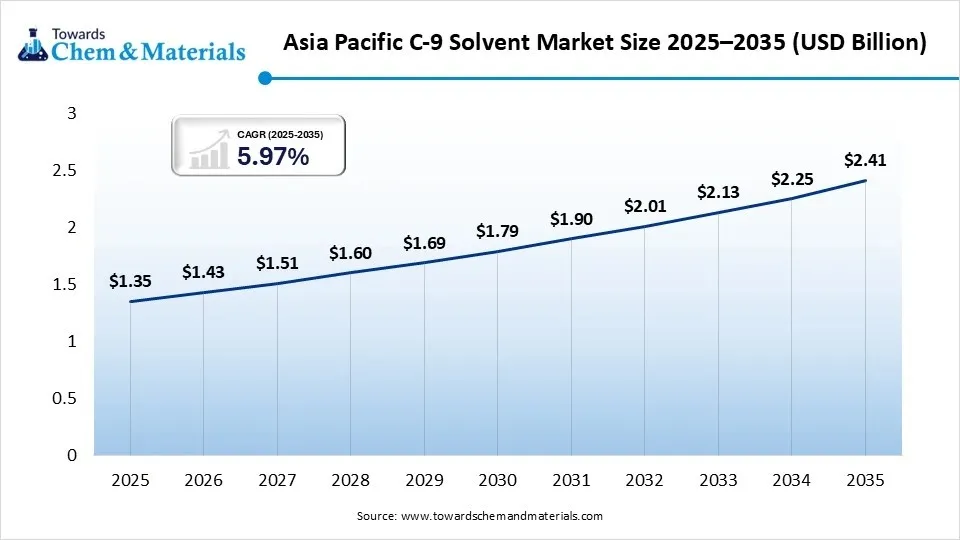

The Asia Pacific c-9 solvent market size was estimated at USD 1.35 billion in 2025 and is projected to reach USD 2.41 billion by 2035, growing at a CAGR of 5.97% from 2026 to 2035. Asia Pacific dominated the C-9 solvent market with the largest share of 48% in 2025 and is expected to grow at the fastest CAGR of 6.6% during the forecast period, driven by robust demand for petrochemicals, growth in paints and coatings applications, and increased infrastructure investments. The solvent market was also boosted by fast industrialisation in China, India, South Korea, and Southeast Asia. The integration of refineries, the boom in car production, and the development of more and more specialized chemicals boosted the local supply chains and also helped to invest in cleaner and more valuable solvent technologies.

")

China continued to be the world's biggest producer and consumer of C-9 solvents, thanks to its massive refining capacity and mature petrochemical industry. Demand for the products continued to drive market growth from construction, automotive coatings and adhesives, and industrial manufacturing. The government investment in refinery modernization and specialty chemicals reinforced domestic production and boosted the competitiveness of supply chains within the Asia Pacific region.

The India demand for C-9 solvents continued to be strong in India, driven by expanding construction, automotive production, packaging, and agrochemical industries. Investment in petrochemical plant construction and refinery capacity increased and enhanced the domestic availability of feedstocks, while decreasing reliance on imports. Other downstream industries experienced additional long-term market growth due to government support of industrial manufacturing and specialty chemical production.

Nort America

The North America c-9 solvent market size was estimated at USD 0.56 billion in 2025 and is projected to reach USD 1.02 billion by 2035, growing at a CAGR of 6.18% from 2026 to 2035. North America held 20% market share in 2025 and is expected to grow at a CAGR of 5% during the forecast period. The region grew on the strength of its well-established petrochemical facilities, specialty coating demand, and ongoing investment in sustainable solvent technologies. Environmental regulations pushed the use of lower VOC solvent formulations. Demand for automotive refinishers, specialty chemicals, and industrial manufacturing continued to be strong in the United States and Canada for the long term.

The U.S. was the largest market in the region due to its integrated refining operations and high specialty chemicals industry. Solvent demand was bolstered by steady growth in advanced coatings, adhesives, industrial manufacturing, and sustainable chemical technology investments. The country has continued to gain a competitive edge in the global hydrocarbon solvent industry, with the innovation of lower-emission production technologies.

Growth in the Canada region's industrial coatings, mining, construction, and chemical manufacturing sustained the demand for Canada. As more industrial chemicals became environmentally friendly, manufacturers started to use lower-emission solvent formulations. Stable supply chains of petrochemicals and cross-border trade with the United States further boosted market growth opportunities.

Europe

The Europe c-9 solvent market size was estimated at USD 0.53 billion in 2025 and is projected to reach USD 0.97 billion by 2035, growing at a CAGR of 6.23% from 2026 to 2035. Europe held 19% market share in 2025 and is expected to grow at a CAGR of 4.9% over the forecast period. Low VOC and sustainable solvent technologies developed rapidly in the region as a result of the rigorous environmental laws. The market expanded with strong investments in specialty chemicals, industrial coatings, and the development of the circular economy. Ongoing refinery modernization, coupled with cutting-edge manufacturing processes, further enhanced production efficiency and reinforced Europe's leading role in sustainable chemical production.

Germany was a major European market due to its sophisticated motor vehicle, coatings, and specialty chemical sectors. Meanwhile, continuous investment in industrial innovation and environmentally friendly production further boosted the demand for solvents. Premium chemical intermediates for various industrial uses were also produced with the aid of advanced technologies of the refinery and strict quality criteria.

Demand was steady in France in construction, aerospace coatings, industrial manufacturing, and specialty chemicals. An increase in investment in environmentally-friendly production technologies led to greater use of cleaner hydrocarbon solvents. The government's sustainability programmes and industrial modernisation also contributed to the long-term market development of various downstream sectors.

Latin America

The Latin America c-9 solvent market size was estimated at USD 0.20 billion in 2025 and is projected to reach USD 0.37 billion by 2035, growing at a CAGR of 6.35% from 2026 to 2035. Latin America held 7% market share in 2025 and is expected to grow at a CAGR of 5.4% over the forecast period. The continued progress of the regional refinery modernization programmes and investment in petrochemicals further bolstered existing production capacity and enhanced the supply security. There was also a general use of C-9 solvents for coatings, adhesives, printing inks, and specialty chemical uses, which drove increases in their use. Moreover, the enhancement of industrial capacity and expansion of the focus on domestic chemical production are likely to bring in additional growth opportunities during the forecast period.

Brazil

Growth in construction, automotive production, and demand for industrial coatings, as well as increased manufacturing operations, kept Brazil as the region's biggest market. The steady demand for solvents was driven by growth in infrastructure and higher usage of paints, adhesives, and chemical formulations in various end-use sectors. Increased investment in the petrochemical industry and boosting the refining capacity reinforced the domestic supply and encouraged the growth of the domestic demand in manufacturing and infrastructure.

Solvent demand in mining, industrial maintenance, infrastructure, and specialist coatings continued to be stable in Chile. Rapid expansion of construction projects, mineral processing industries, and modernization of manufacturing resulted in increased use of high-performance hydrocarbon solvents in a wide range of industrial applications. Solvent use also rose due to higher investments in industrial facilities and infrastructure improvements. Also, the increasing industrial diversification is providing C-9 solvent suppliers with additional opportunities in specialty applications.

Middle East & Africa

The Middle East & Africa c-9 solvent market size was estimated at USD 0.17 billion in 2025 and is projected to reach USD 0.32 billion by 2035, growing at a CAGR of 6.53% from 2026 to 2035. The Middle East & Africa held 6% market share in 2025 and is expected to grow at a CAGR of 5.8% over the forecast period due to the abundant petroleum resources, refinery expansion projects, and rising investments in the petrochemical sector. Long-term regional demand continued to be bolstered by expanding construction and industrial diversification and the development of chemical facilities downstream. Infrastructure investments, coatings manufacturing, and specialty chemical applications are helping to promote the use of solvents as well. Furthermore, strategic projects related to the development of domestic refining and petrochemical capabilities are strengthening the supply network in the region and providing opportunities for further growth in the market.

")

Saudi Arabia continued to be the biggest regional producer, however, due to the presence of large-scale refining facilities, significant hydrocarbon reserves, and growing downstream investments in petrochemicals. Nationwide industrial diversification programs helped the production of higher-value chemical products and boosted the processing power of hydrocarbons for domestic and export markets. Demand for C-9 solvents continued to grow with higher investments in petrochemical complexes, specialty chemicals, and industrial manufacturing.

South Africa maintained its support for the regional demand by virtue of its mining operations, industrial coatings, construction chemicals, and manufacturing. The deployment of new infrastructure and a rise in industrial modernisation led to a greater use of specialty solvents in various industrial sectors and boosted regional market growth. Automotive production, chemical processing, and industrial maintenance were also contributing to solvent demand.

Competitive Analysis

- The C-9 solvent market is still very competitive, and the major petrochemical companies are studying refinery integration, development of new specialty solvents, expansion of production capacity, and developing sustainable formulation technologies. The players are building their market strength by expanding capacities, developing advanced processing technologies, forming strategic alliances, and investing in low VOC solvent solutions. Companies are also scaling up manufacturing operations in the region to enhance their supply reliability and cater to the increasing demand from the coatings, adhesives, construction, agrochemicals, and specialty chemical industry segments.

- For instance, in April 2025, Neville Chemical Company expanded its NEVOXY® EPX product line with two new bio-epoxy modifiers: NEVOXY® ECO-L2 and NEVOXY® ECO-LH, which will help to improve the performance of epoxy systems. Low color, high solids products provide protective coatings, marine applications, industrial maintenance, epoxy flooring, primers, and solvent-free formulations.(Source: www.nevchem.com)

- In November 2025, Eastman Chemical announced that it will establish a new business unit dedicated to renewable carbon sourcing and solvent recovery, the ethyl acetate business, within its Circular Solutions division. The project aims to make better use of bio-based ethanol and to lower the emissions of the bio-based ethanol produced compared to that of the conventional solvent products, but at the same time maintain the same performance.(Source: www.incheechem.com)

Recent Developments

- In March 2025, Indian Oil Corporation Limited (IOCL) is expected to sign a Memorandum of Understanding (MoU) for the development of a Dual-feed Naphtha Cracker facility in Odisha. The project will increase the production capacity of the petrochemical industry and expand the capacity of the chemical industries in the downstream with FICCI.(Source: indianchemicalnews)

- In October 2025, ChemPoint highlighted Chevron Phillips Chemical’s Soltrol® Isoparaffin Solvents, which are formulated to provide a range of high-purity, low odor, low toxicity options with controlled vaporization and versatile use in coatings, cleaners, agrochemicals, and industrial processes.(Source: chempoint.com)

Top Players in the Market & Their Offerings

| Company | Company Type / Position | Major Headquarters | Geographic Presence | C-9 Solvent Offerings | Key Strength |

| Chevron Phillips Chemical Company | Petrochemical and specialty chemicals producer | The Woodlands, Texas, USA | North America, Europe, Asia Pacific, Middle East | Aromatic hydrocarbon products, C-9 fractions, specialty chemical intermediates | Advanced refining technologies and high-quality aromatic production capabilities |

| TotalEnergies | Integrated energy and petrochemical company | Courbevoie, France | Europe, Middle East, Africa, Asia Pacific, Americas | Hydrocarbon solvents, petrochemical derivatives, aromatic feedstocks | Integrated refining operations and diversified global chemical portfolio |

| Reliance Industries Limited | Integrated refining and petrochemical manufacturer | Mumbai, India | India, Asia Pacific, Middle East, Global markets | Aromatic hydrocarbons, petrochemical derivatives, solvent-grade products | Large-scale refining capacity and strong backward integration through the Jamnagar complex |

Other Key Players

- ExxonMobil

- Shell

- Eastman Chemical Company

- INEOS

- LyondellBasell

- Formosa Plastics Corporation

- Mitsubishi Chemical

- Eni (Versalis)

Segment Covered in the Report

By Product Type

- Aromatic C-9 Solvent

- High Flash Grade

- Low Flash Grade

- High Purity Grade

- Hydrogenated C-9 Solvent

- Low Odor Grade

- High Purity Grade

- Mixed C-9 Solvent

- Industrial Grade

- Commercial Grade

By Application

- Paints & Coatings

- Architectural Coatings

- Industrial Coatings

- Marine Coatings

- Automotive Coatings

- Adhesives & Sealants

- Solvent-Based Adhesives

- Pressure-Sensitive Adhesives

- Construction Sealants

- Printing Inks

- Flexographic Inks

- Gravure Inks

- Packaging Inks

- Cleaning & Degreasing

- Industrial Cleaning

- Metal Cleaning

- Equipment Cleaning

- Chemical Processing

- Resin Manufacturing

- Petrochemical Processing

- Specialty Chemicals

- Others

- Rubber Processing

- Agrochemicals

- Consumer Products

By End-Use Industry

- Construction

- Residential

- Commercial

- Infrastructure

- Automotive

- OEM

- Aftermarket

- Chemical

- Petrochemicals

- Specialty Chemicals

- Packaging

- Flexible Packaging

- Rigid Packaging

- Industrial Manufacturing

- Machinery

- Metal Fabrication

- Others

- Marine

- Aerospace

- Electronics

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)