Content

What is the Ferritic Stainless Steel Market Size And Share?

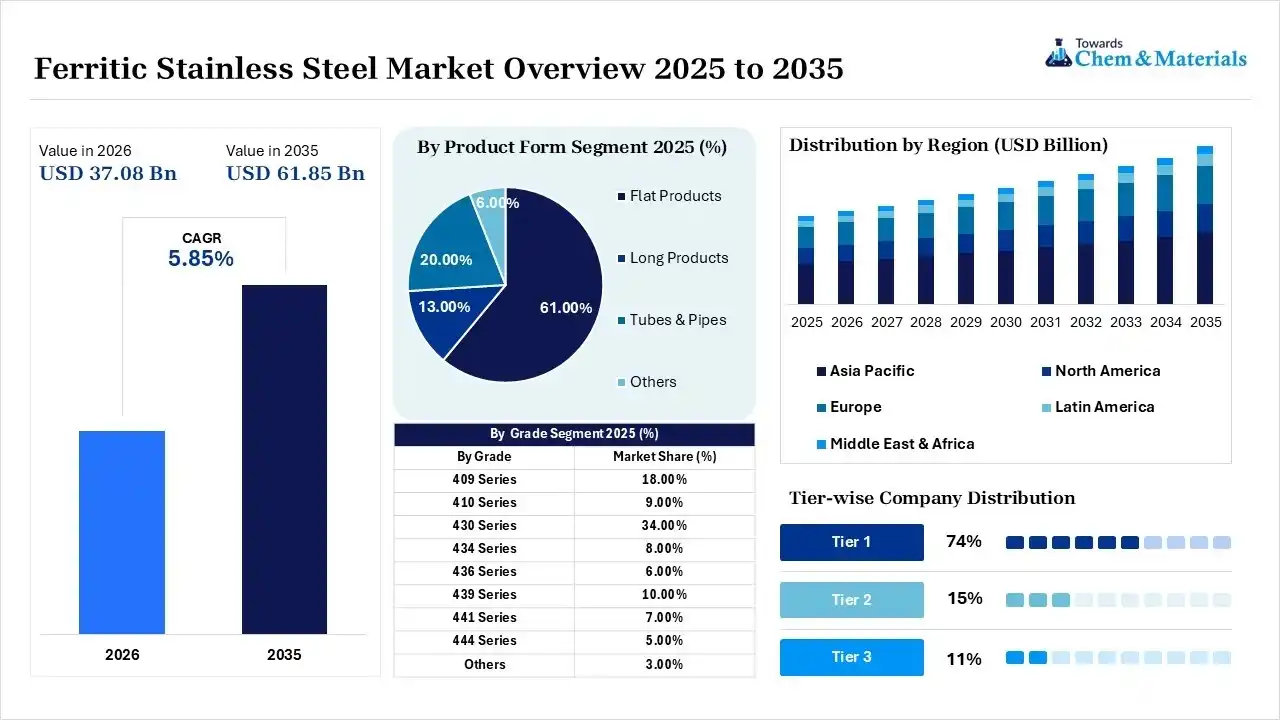

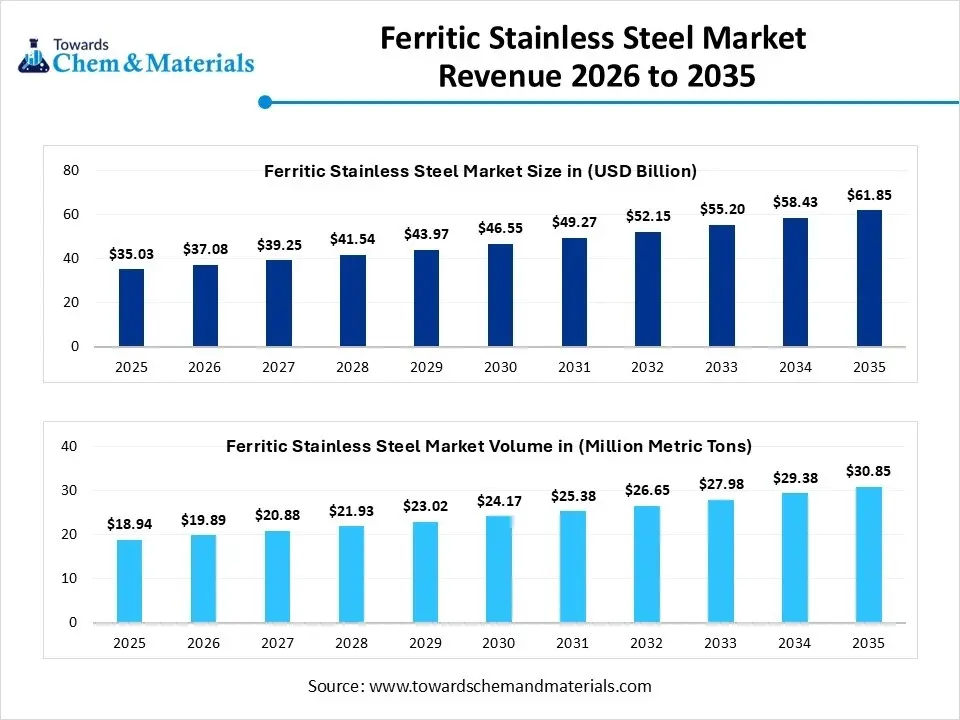

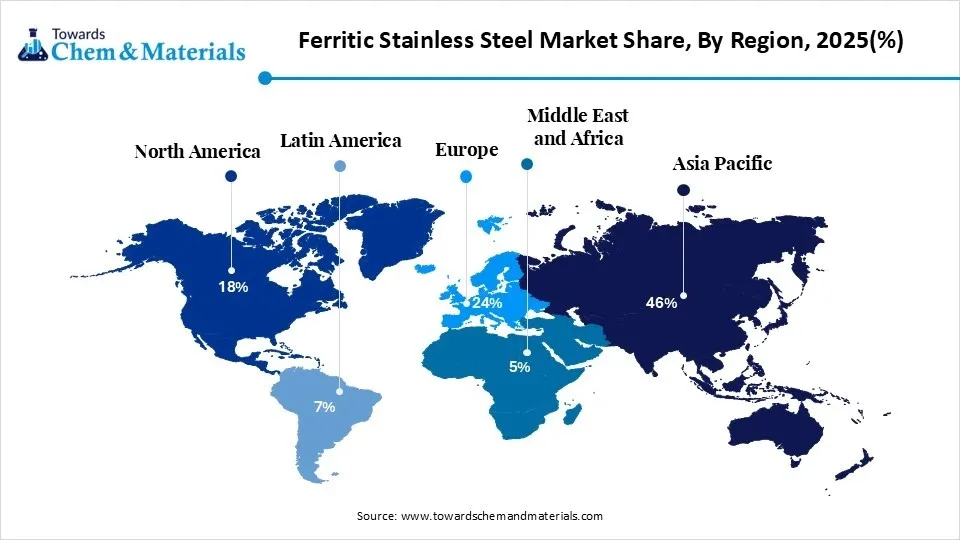

The global ferritic stainless steel market size was valued at USD 35.03 billion in 2025, is estimated to reach USD 37.08 billion in 2026, and is projected to reach USD 61.85 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035. Asia Pacific dominated the ferritic stainless steel market with the largest revenue share of 46.00% in 2025 and is expected to grow at the fastest CAGR of 5.97% during the forecast period.

The delivery of exceptional defense against corrosion and oxidation, which makes it a top choice for advanced-thinking automotive engineers. As a result, there is a significant surge in product demand as manufacturers actively integrate it into high-performance exhaust systems and key structural components.

Market Highlights

- By region, Asia Pacific dominated the market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 5.97% over the forecast period.

- By region, North America held a market share of 18.00% in 2025 and was expected to grow at the fastest CAGR of 6.13% over the forecast period.

- By grade, the 430 series segment dominated the market with the largest share of 34.00% in 2025 and is expected to grow at a CAGR of 5.01% over the forecast period.

- By grade, the 441 series segment held a market share of 7.00% in 2025 and is expected to grow at the fastest CAGR of 6.68% over the forecast period.

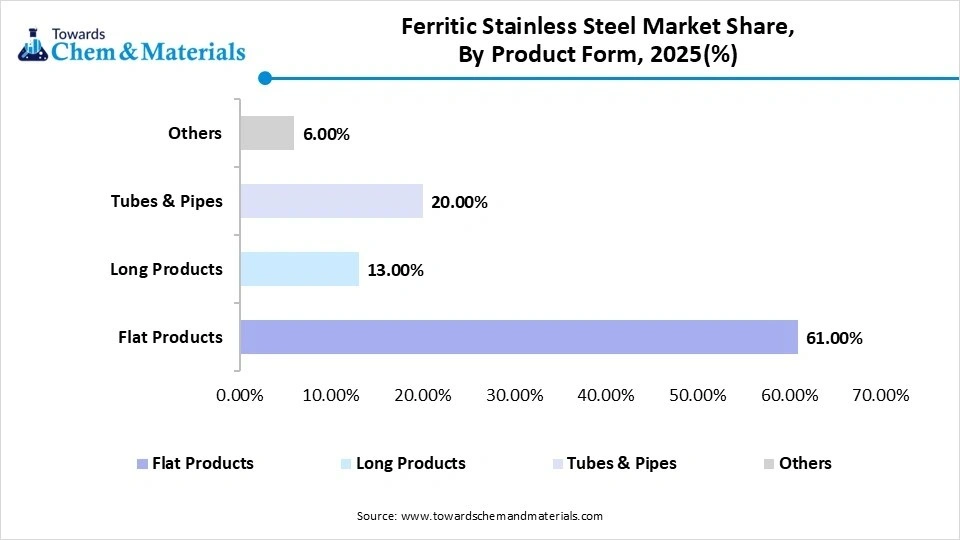

- By product form, the flat products segment dominated the market with the largest share of 61.00% in 2025 and is expected to grow at a CAGR of 5.43% over the forecast period.

- By product form, the other segment held a market share of 6.00% in 2025 and is expected to grow at the fastest CAGR of 6.18% during the forecast period.

- By finish, the 2B finish segment dominated the market with the largest share of 38.00% in 2025 and is expected to grow at a CAGR of 5.42% over the forecast period.

- By finish, the HL finish segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 6.37% over the forecast period.

- By thickness, the 1–3 mm segment dominated the market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 5.31% over the forecast period.

- By thickness, the above 6 mm segment held a market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 5.93% over the forecast period.

- By manufacturing process, the hot-rolled segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at a CAGR of 4.95% over the forecast period.

- By manufacturing process, the temper-rolled segment held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 6.14% over the forecast period.

- By end-use industry, the automotive segment dominated the market with the largest share of 37.00% in 2025 and is expected to grow at a CAGR of 5.56% over the forecast period.

- By end-use industry, the energy & power segment held a market share of 4.00% in 2025 and is expected to grow at the fastest CAGR of 6.45% during the study period.

- By distribution channel, the direct sales segment dominated the market with the largest share of 47.00% in 2025 and is expected to grow at a CAGR of 5.22% over the study period.

- By distribution channel, the online sales segment held a market share of 6.00% in 2025 and is expected to grow at the fastest CAGR of 7.21% over the forecast period.

According to Towards Chemicals and Materials Analytics and Consulting, the global ferritic stainless steel market volume was valued at 18.94 million metric tons in 2025 and is expected to surpass around 30.85 million metric tons by 2035, accelerating a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.

Major market players are heavily using ferritic stainless steel because of its lower carbon footprint and recyclability as compared to other stainless steel types, presenting lucrative opportunities in the market. Technological innovations in surface finishing and coating techniques enhanced the overall aesthetic appeal and durability of the material.

- In August 2025, the Swiss Steel Group, headquartered in Lucerne, Switzerland, and its French subsidiary, Ugitech, based in Ugine, have introduced the UGIWAM product line. This specialized wire range is designed for Directed Energy Deposition (DED) metal additive manufacturing and encompasses austenitic, ferritic, martensitic, duplex, and nickel-based alloys.(Source: www.metal-am.com)

The market is also experiencing a surge in the integration of Industry 4.0 manufacturing practices to ensure superior quality control and cost efficiency. Innovations in alloy formulations are a dynamic factor for market growth.

Global Investment Flow for Ferritic Stainless Steel 2026

The global investment flow for the market is undergoing a significant structural realignment, fueled mainly by aggressive infrastructure budgets and volatile nickel prices in emerging economies along with the macro shifts towards nickel-free and cost-effective alternative alloys.

- In March 2026, based on final U.S. Census Bureau data, the American Iron and Steel Institute (AISI) reported that total U.S. steel imports reached 1,650,000 net tons (NT) in January 2026, including 1,249,000 net tons (NT) of finished steel. These represent respective month-over-month increases of 4.6% and 7.7% compared to December 2025.(Source: www.steel.org)

- For instance, according to data released by the General Administration of Customs on June 9, China’s steel exports reached 10.341 million tonnes in May, representing a month-on-month increase of 843,000 tonnes, or 8.9%. Cumulative steel exports for the January–May period totaled 44.554 million tonnes.(Source: www.sunsirs.com )

Market Trends

- The ongoing growth of electric vehicle manufacturing and automotive production is the latest trend in the market shaping positive market growth. The components such as wires, steel bars, and profiles are crucial for producing exhaust systems and steering shafts, where heat resistance is necessary.

- In recent years, market players are rapidly transitioning to EAF and scrap-based stainless steel manufacturing to reduce carbon intensity and align with green procurement requirements. Also, digital traceability, near-net-shape manufacturing, and sustainability certifications are improving transparency and lessening lead times.

- The rise in product integration into green industries is the future trend in the market driving market growth. The trend is fueled by the push for renewable energy adoption, sustainability, and circular economy practices.Stainless steel is becoming necessary for green building certifications and hence used in sustainable construction projects.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 37.08 Billion/ 19.89 Million Metric Tons |

| Expected Size in 2035 | USD 61.85 Billion/ 30.85 Million Metric Tons |

| Growth Rate | CAGR of 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Grade, By Product Form, By Finish, By Thickness, By Manufacturing Process, By End-use Industry, By Distribution Channel |

| Key Companies Profiled | Thyssen Krupp, Pohang Iron & Steel (Posco), Ta Chen International, Jindal Stainless, Allegheny Flat Rolled Products, North American Stainless, AK Steel |

AI-Powered Predictive Formulations in the Ferritic Stainless Steel Market

AI-powered predictive formulations utilize deep neural networks and machine learning to model alloy composition and processing conditions, substantially boosting R&D in the market. Furthermore, AI and machine learning reduce overall operational costs and slash material waste by detecting optimal compositions that depend less on costly, volatile raw elements like nickel.

Supply Chain Analysis of the Ferritic Stainless Steel Market

Production & Processing

- It includes the precise methods used to shape the metal, melt raw materials, and finish its surface.

Ferritic steels are cost-effective and popular metals that contain a high amount of chromium but very little nickel, which makes them very magnetic and resistant to rust. - POSCO: South Korea's leader, commanding a massive footprint in Asia-Pacific. They excel in producing premium, high-surface-finish ferritic alloys for appliances and electronics.

- Other Key Players: Nippon Steel, Acerinox

Quality Testing and Certification

- It refers to the procedures and standards utilized to prove that a product is strong, safe, and rust resistant.

Ferritic stainless steel must pass these checks before it can be sold to a particular industry. Testing ensures the steel can handle heat, pressure, and stress without breaking or rusting. - Jindal Stainless (India): A massive manufacturer, especially in the growing Asian steel market.

- Other Key Players: Outokumpu, Nippon Steel

Distribution to Industrial Users

- It includes the sales channels utilized to deliver ferritic stainless steel directly to large businesses. This process skips retail stores.

- Steel makers send products directly to factories or building sites. These huge buyers then use the steel to make home appliances and make cars and heavy machines.

- Acerinox: A Spanish global leader with an extensive distribution network across the world.

- Other Key Players: China Baowu, Aperam

Ferritic Stainless Steel Market’s Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations & Standards | Focus Areas |

| United States | ASTM International & SAE International | ASTM A240, ASTM A480, SAE J405 | Standardizes chemical composition (e.g., Grade 430, 409); mandates thickness tolerances and mechanical testing for pressure vessels and automotive exhaust systems. |

| European Union | European Committee for Standardization (CEN) | EN 10088-2, EN 10088-4, REACH, RoHS | Defines technical delivery conditions for sheet/plate; strictly regulates hazardous substance restrictions and tracks carbon footprints under the CBAM (Carbon Border Adjustment Mechanism). |

| China | Standardization Administration of China (SAC) | GB/T 3280, GB/T 4237 | Regulates cold-rolled and hot-rolled stainless steel plates; dictates quality standards for high-volume manufacturing in consumer appliances and automotive sectors. |

What are the types of Ferritic Stainless Steel?

Group 1: Low Chromium / Utility Grades (10.5% – 14% Cr)

- These are the least expensive ferritic steels. Due to their low chromium content, they are meant to develop a light layer of surface rust over time and are best suited for non-decorative corrosive environments.

- Key Grades: Type 409, Type 410L.

- Common Uses: Automotive exhaust system silencers.

Group 2: Standard/Universal Grades (14% – 18% Cr)

- This is the most extensively used class of ferritic stainless steel. With a much higher chromium content, they give a far better corrosion resistance against organic acids, nitric acids, and sulfur gases. They are generally used as a cost-efficient alternative to austenitic 304 stainless steel in indoor environments.

- Key Grades: Type 430.

- Common Uses: Washing machine drums, kitchen sinks.

Group 3: Stabilized Grades (14% – 18% Cr + Stabilizers)

- These grades share the same chromium range as Group 2 but involve using elements such as niobium (Nb) or zirconium (Zr). These stabilizers prevent sensitization during welding, which gives them enhanced weldability and better formability than Group 2 alloys.

- Key grades: Type 430Ti, Type 439, Type 441.

- Common Uses: Heat exchanger tubes, tougher exhaust components

Market Dynamics

Driver

Rapid Infrastructure Expansion

The growing pace of industrial activities and infrastructure expansion, especially in emerging economies, is the major factor driving the growth of the market. Stainless steel is a crucial material in process equipment, industrial machinery, and construction applications because of its corrosion resistance, strength, and long lifecycle. In addition, the rise in waves of industrial modernization, such as renewable energy projects and urban development initiatives, is fueling consistent demand for stainless steel.

Restraint

Market and Economic Pressures

Domestic market players face severe profit margin erosion because of an unchecked influx of low-priced imported steel products, pushing local operators to aggressively compete on thin price margins, which is the major factor hindering the market growth. Moreover, ferritic manufacturers remain fully exposed to pricing violations and sudden regional export disruptions of chromium.

Opportunity

Growing Demand for High-Temperature Industrial Systems

There is a rise in demand for specialized high-temperature ferritic steel in chemical processing, power generation, and pollution control systems, creating massive opportunities in the near future. Furthermore, highly alloyed grades, including Type 446, offer extensive oxidation resistance at extreme temperatures, which serves as a cost-efficient substitute for nickel-based superalloys.

Segmental Insights

Grade Insight

The 430 series segment dominated the market with the largest share of 34.00% in 2025 and is expected to grow at a CAGR of 5.01% over the forecast period. The dominance of the segment can be attributed to the growing demand for home appliances and automotive trims along with steady prices. In addition, a surge in demand from an increasing middle class, especially across Asia-Pacific and Latin America, fuels wide volume consumption for 430-grade pots, pans, and indoor domestic utensils.

")

The 441 series segment held a market share of 7.00% in 2025 and is expected to grow at the fastest CAGR of 6.68% over the forecast period. The growth of the segment can be credited to the growing need for cost-effective, high-temperature-resistant materials in the automotive sector and surge in applications in green energy infrastructure. Type 441 is heavily adopted for solid-oxide fuel cell (SOFC) interconnect plates, hydrogen fuel cell stacks, and heat exchangers.

Ferritic Stainless Steel Market Share, By Grade, 2025(%)

| By Grade | Market Share (%) |

| 409 Series | 18.00% |

| 410 Series | 9.00% |

| 430 Series | 34.00% |

| 434 Series | 8.00% |

| 436 Series | 6.00% |

| 439 Series | 10.00% |

| 441 Series | 7.00% |

| 444 Series | 5.00% |

| Others | 3.00% |

Product Form Insight

The flat products segment dominated the market with the largest share of 61.00% in 2025 and is expected to grow at a CAGR of 5.43% over the forecast period. The dominance of the segment can be linked to the growing demand across construction, automotive, and appliance industries, along with the exceptional heat and corrosion resistance. Builders use flat sheets for wall panels and roofing. Also, ferritic steel resists rusting from rain and air, driving segment growth further.

")

The other segment held a market share of 6.00% in 2025 and is expected to grow at the fastest CAGR of 6.18% during the forecast period. The growth of the segment can be driven by the growing need for nickel-free alloys because of volatile raw material prices. A surge in green and renewable energy infrastructure needs materials that can bear high temperatures and harsh conditions without failing.

Ferritic Stainless Steel Market Share,By Product Form, 2025(%)

| By Product Form | Market Share (%) |

| Flat Products | 61.00% |

| Long Products | 13.00% |

| Tubes & Pipes | 20.00% |

| Others | 6.00% |

Finish Insight

The 2B finish segment dominated the market with the largest share of 38.00% in 2025 and is expected to grow at a CAGR of 5.42% over the forecast period. The growth of the segment is owing to the growing demand in manufacturing and excellent corrosion resistance. Moreover, stringent health and safety rules in hospitals, restaurants, and food plants need rust-free, clean materials. Ferritic stainless steel with a 2B finish conventionally fulfils these food contact standards.

The HL finish segment held a market share of 8.00% in 2025 and is expected to grow at the fastest CAGR of 6.37% over the forecast period. The growth of the segment is due to the growing need for modern fingerprint-resistant appliances and the transition towards cost-effective materials. Homeowners favoured sleek kitchen appliances. Market players are choosing ferritic HL grades to fulfil this demand while reducing overall manufacturing costs.

Ferritic Stainless Steel Market Share,By Finish, 2025(%)

| By Finish | Market Share (%) |

| No.1 Finish | 15.00% |

| 2B Finish | 38.00% (Dominating) |

| BA Finish | 16.00% |

| No.4 Finish | 18.00% |

| HL Finish | 8.00% |

| Mirror Finish | 3.00% |

| Others | 2.00% |

Thickness Insight

The 1–3 mm segment dominated the market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 5.31% over the forecast period. The dominance of the segment can be attributed to its stable pricing, low cost, and better corrosion resistance as compared to other sizes. Builders use 1–3 mm sheets for panels, roofing, and elevators; hence, demand is increasing because they do not rust directly and last for a long duration of time.

The above 6 mm segment held a market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 5.93% over the forecast period. The growth of the segment can be credited to its magnetic properties and strong performance in high-stress, elevated-temperature environments. Furthermore, this segment is finding a crucial niche in solar thermal power plants and solid oxide fuel cells (SOFCs).

Ferritic Stainless Steel Market Share,By Thickness, 2025(%)

| By Thickness | Market Share (%) |

| Below 1 mm | 18.00% |

| 1–3 mm | 46.00% |

| 3–6 mm | 24.00% |

| Above 6 mm | 12.00% |

Manufacturing Process Insight

The hot-rolled segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at a CAGR of 4.95% over the forecast period. The dominance of the segment can be linked to the surge in advanced infrastructure projects and rapid expansion of manufacturing industries. Hot-rolled ferritic steel contains high chromium but little to no nickel. As nickel prices are highly volatile, buttling stainless steel helps companies to avoid unexpected spikes.

The tempered roll segment held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 6.14% over the forecast period. The growth of the segment can be driven by growing demand for durable and cost-effective materials coupled with its high tensile strength. The temper rolling process allows manufacturers to increase the overall yield strength of the steel without heavy alloy additions.

Ferritic Stainless Steel Market Share,By Manufacturing Process, 2025(%)

| By Manufacturing Process | Market Share (%) |

| Hot Rolled | 36.00% (Dominating) |

| Cold Rolled | 31.00% |

| Annealed | 12.00% |

| Pickled | 10.00% |

| Temper Rolled | 11.00% |

End-use Industry Insight

The automotive segment dominated the market with the largest share of 37.00% in 2025 and is expected to grow at a CAGR of 5.56% over the forecast period. The dominance of the segment is owing to the surge in vehicle manufacturing and materials with high heat resistance. Ferritic stainless steel has a much lower thermal expansion coefficient and higher thermal conductivity as compared to austenitic steel, minimizing structural distortion.

- In October 2025, Ola Electric, India’s leading electric two-wheeler manufacturer, secured official government certification for an indigenously developed ferrite motor that completely eliminates the use of rare-earth magnets.(Source: www.business-standard.com)

The energy & power segment held a market share of 4.00% in 2025 and is expected to grow at the fastest CAGR of 6.45% during the study period. The growth of the segment is due to ongoing transition towards renewable energy and stringent heat-resistance regulations, along with the demand for durable and cost-effective materials. Additionally, power plants and turbines operate at high temperatures; hence, this material has a high boiling point.

Ferritic Stainless Steel Market Share,By End-use Industry, 2025(%)

| By End-use Industry | Market Share (%) |

| Automotive | 37.00% (Dominating) |

| Construction | 21.00% |

| Home Appliances | 19.00% |

| Industrial Equipment | 9.00% |

| Food Processing Equipment | 5.00% |

| Energy & Power | 4.00% |

| Transportation | 3.00% |

| Others | 2.00% |

Distribution Channel Insight

The direct sales segment dominated the market with the largest share of 47.00% in 2025 and is expected to grow at a CAGR of 5.22% over the study period. The dominance of the segment can be attributed to the surge in demand for high-purity, customized alloys and the rise in demand for electric vehicles (EVs). Moreover, direct sales connect engineers and steel makers to design unique metal blends.

The online sales segment held a market share of 6.00% in 2025 and is expected to grow at the fastest CAGR of 7.21% over the forecast period. The growth of the segment can be credited to the surge in B2B e-commerce platforms and growing demand for flexible, smaller bulk purchases by small and medium enterprises (SMEs). Furthermore, major market players are introducing dedicated e-commerce ecosystems to offer real-time pricing.

Ferritic Stainless Steel Market Share,By Distribution Channel, 2025(%)

| By Distribution Channel | Market Share (%) |

| Direct Sales | 47.00% |

| Distributors & Stockists | 31.00% |

| Online Sales | 6.00% |

| OEM Contracts | 16.00% |

What are the Benefits of Ferritic Stainless Steel?

Ferritic stainless steel is a cost-effective metal and contains lots of chromium and almost no nickel. It also resists heat, rust, and stress-corrosion cracking. Belonging to the 400-series family of stainless-steel alloys, its microstructure contains a high chromium content (ranging from 10.5% to 30%) with less carbon.

The ferritic steels possess a body-centered cubic (BCC) crystal structure. This differs from austenitic grades, which have a face-centered cubic structure. Hence, ferritic steels exhibit superior immunity to chloride-induced stress corrosion cracking. This makes them highly suitable for high-stress and marine environments.

They also exhibit mechanical properties closely linked with conventional carbon steels. When bent or cold-worked, they suffer from less "springback" than austenitic steels, which allows for convenient fabrication of thin-walled and lightweight shapes. These alloys exhibit a superior initial yield strength compared to standard austenitic grades such as 304, hence enabling engineering teams to minimize material thickness and realize critical weight-reduction objectives.

Regional Analysis

How did the Asia Pacific dominate the Ferritic Stainless Steel Market in 2025?

The Asia Pacific ferritic stainless steel market size was estimated at USD 16.11 billion in 2025 and is projected to reach USD 28.76 billion by 2035, growing at a CAGR of 5.97% from 2026 to 2035. Asia Pacific dominated the ferritic stainless steel market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 4.76% over the forecast period. The dominance of the region can be attributed to the increasing automotive sector demand, ongoing urbanization, and infrastructure projects in the emerging economies. In addition, the push for sustainable development has expanded the use of low-emission, "green" steel across multiple industries. In the automotive sector, this shift is crucial for lowering both production-phase and usage-phase carbon emissions.

")

China

China's large auto industry uses ferritic stainless steel to build vehicle exhaust systems. These parts must handle harsh heat and road salt without rusting. Also, China continues to invest heavily in public building projects like bridges and transit lines. Ferritic steel is highly popular in these projects because it is strong and needs very little maintenance over time.

India

Government initiatives such as the 'Make in India' campaign, smart city projects, and urban railway developments need vast amounts of structural and decorative stainless steel. India's expanding middle class is increasing its consumption of household goods. The food processing and kitchenware industries heavily rely on ferritic grades for safe, rust-proof items.

North America

The North America ferritic stainless steel market size was estimated at USD 6.31 billion in 2025 and is projected to reach USD 11.44 billion by 2035, growing at a CAGR of 6.13% from 2026 to 2035. North America held a market share of 18.00% in 2025 and was expected to grow at the fastest CAGR of 5.96% over the forecast period. The growth of the region can be credited to the growing demand for recycled, sustainable materials and stringent vehicle emissions standards. North America places a significant focus on recycling initiatives. Due to the high recyclability of this steel, its use substantially assists corporations in achieving stringent environmental construction and manufacturing standards.

United States

As the United States builds more electric vehicles (EVs) and modern cars, automakers need lightweight, rust-proof, and affordable metals; therefore, ferritic steel fits this need perfectly. Market players in the U.S. heavily substitute austenitic steels with ferritic alternatives to safeguard their supply chain from unpredictable spikes in global nickel markets.

Canada

Canada has stringent green building codes, so developers use ferritic stainless steel for architectural cladding and roofing because it is highly recyclable and lasts for decades without rusting. In addition, automakers in the country use ferritic grades to make lightweight parts, battery heat shields, and motor brackets that handle new types of heat.

Europe

The Europe ferritic stainless steel market size was estimated at USD 8.41 billion in 2025 and is projected to reach USD 15.15 billion by 2035, growing at a CAGR of 6.06% from 2026 to 2035. Europe held a market share of 24.00% in 2025 and was expected to grow at a CAGR of 4.94% over the forecast period. The growth of the region can be linked to the growing push towards renewable energy and strengthened sustainability initiatives. Major countries in the region, such as Germany, are increasingly investing in EVs. Hence, automakers are using ferritic stainless steel to build vehicle exhaust systems and battery packs.

Germany

Germany is home to a world-class automotive manufacturing base. Also, demand for specific ferritic grades like 409 remains high for exhaust systems, silencers, and structural parts, and is rapidly increasing. Stringent decarbonization laws like the EU Carbon Border Adjustment Mechanism (CBAM) inflate the cost of importing high-emission materials.

France

France is pushing hard to build EVs. Automakers are using ferritic stainless steel for exhaust systems, battery packs, and structural parts because it resists heat and corrosion well. In addition, French companies use this steel to build refrigerators, washing machines, and building roofs, leading to country growth soon.

Latin America

The Latin America ferritic stainless steel market size was estimated at USD 2.45 billion in 2025 and is projected to reach USD 4.64 billion by 2035, growing at a CAGR of 6.59% from 2026 to 2035. Latin America held a market share of 7.00% in 2025 and was expected to grow at a CAGR of 4.71% over the forecast period. The growth of the region can be driven by ongoing urbanization, extensively increasing production of home appliances along with the affordability of Grade 400 series steels. Moreover, Latin America is witnessing major infrastructure and housing development. Builders are using these materials for commercial facades and structural parts.

Brazil

The Brazilian market is expanding as the country invests in more urban and housing projects, fueling the need for basic, long-lasting stainless steel structural parts. The local manufacturing of cars and heavy vehicles uses substantial amounts of ferritic steel, especially in vehicle exhaust systems, for its excellent heat and corrosion resistance.

Argentina

Argentina’s active automotive hubs, supported by major players like Toyota Argentina, generate steady baseline demand for these specialty steel parts. Ferritic grades contain little to no expensive nickel, which makes them highly resistant to nickel price swings, giving Argentine manufacturers a predictable budget.

Middle East & Africa

The Middle East & Africa ferritic stainless steel market size was estimated at USD 1.75 billion in 2025 and is projected to reach USD 3.40 billion by 2035, growing at a CAGR of 6.87% from 2026 to 2035. The Middle East & Africa held a market share of 5.00% in 2025 and was expected to grow at a CAGR of 5.48% over the forecast period. The growth of the region can be attributed to the rapid urbanization and large-scale projects such as Saudi Arabia's NEOM city, which needs huge amounts of structural and architectural materials. Furthermore, MEA economies are increasingly transitioning towards local manufacturing, which makes it perfect for oil refineries and water desalination plants.

")

Saudi Arabia

Saudi Arabia depends heavily on desalination to survive. Ferritic steel resists rust from saltwater and harsh chemicals, which makes it the top choice for water treatment plants and piping. Also, national energy companies are expanding processing capacities where ferritic grades are used in oil refining equipment where heat and chemical resistance are required.

UAE

The UAE has a high number of cars; for those, ferritic steels (like Grade 409) are the top choice for vehicle exhaust systems because they handle extreme heat well. As the UAE shifts more toward electric vehicles (EVs), ferritic steel's lightweight yet sturdy nature is helping automakers reduce vehicle weight and extend battery life, driving market growth soon.

Competitive Analysis

The ferritic stainless steel market is moderately concentrated and structured. Top-tier global steel manufacturers dominate raw refining capacity, while a surge in the number of regional specialists focuses on high-specification, niche variants such as high-temperature ferritic steel. Major competitors like Jindal Stainless and POSCO lead the market, using vertical integration and local demand to secure their market.

- Luxembourg-based manufacturer Aperam adjusted its European alloy surcharges for austenitic stainless steel flat products. The Grade 304 surcharge decreased to EUR 2,339/ton from EUR 2,365/ton in June. Meanwhile, the Grade 316L surcharge increased to EUR 4,089/ton from EUR 4,056/ton in the prior month.(Source: yieh.com)

Recent Developments

- In November 2025, Baosteel Desheng Stainless Steel Co., Ltd. (Baosteel Desheng) achieved a significant milestone in its high-end stainless steel segment by completing the trial production of B444LM ultra-pure ferritic stainless steel in a 6.0 mm white-skinned specification.(Source: yieh.com)

Strategic Profiles of Key Players Shaping the Ferritic Stainless Steel Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| Outokumpu | Global Leader / High-Performance Pioneer | Helsinki, Finland | Strong footprint in Europe and the Americas, with a global sales network. | Broad range of premium ferritic sheets, coils, and strips (e.g., Core and Moda ranges). | : Advanced stabilization techniques (titanium/niobium alloying) that provide exceptional high-temperature oxidation resistance for automotive exhaust systems |

| Nippon Steel Corporation | Tier-1 Major / Technical Innovator | Tokyo, Japan | Dominant in the Asia-Pacific region, with extensive global export channels. | Ultra-pure ferritic stainless steels and high-grade functional sheets | Superior deep-drawing capabilities and high corrosion resistance, highly favored by global consumer appliance and electronic manufacturers. |

| Aperam | Regional Giant / Sustainability Focused | Luxembourg City, Luxembourg | Deeply integrated across Europe and South America. | Nickel-free ferritic grades, customized finishes, and precision strips | Market leader in cost-effective, nickel-free solutions optimized for domestic appliances and architectural cladding, backed by strong low-carbon production processes. |

Other Key Players

- Thyssen Krupp

- Pohang Iron & Steel(Posco)

- Ta Chen International

- Jindal Stainless

- Allegheny Flat Rolled Products

- North American Stainless

- AK Steel

Segments Covered in the Report

By Grade

- 409 Series

- 410 Series

- 430 Series

- 434 Series

- 436 Series

- 439 Series

- 441 Series

- 444 Series

- Others

- 445M2

- 446

- Specialty Ferritic Grades

By Product Form

- Flat Products

- Hot Rolled Coil

- Cold Rolled Coil

- Sheets

- Plates

- Strips

- Long Products

- Bars

- Rods

- Wire

- Tubes & Pipes

- Welded Pipes

- Seamless Pipes

- Others

By Finish

- No.1 Finish

- 2B Finish

- BA (Bright Annealed) Finish

- No.4 Finish

- HL (Hairline) Finish

- Mirror Finish

- Others

By Thickness

- Below 1 mm

- 1–3 mm

- 3–6 mm

- Above 6 mm

By Manufacturing Process

- Hot Rolled

- Cold Rolled

- Annealed

- Pickled

- Temper Rolled

By End-use Industry

- Automotive

- Exhaust Systems

- Catalytic Converter Components

- Structural Parts

- Construction

- Roofing

- Cladding

- Structural Components

- Home Appliances

- Washing Machines

- Refrigerators

- Ovens

- Dishwashers

- Industrial Equipment

- Food Processing Equipment

- Energy & Power

- Transportation

- Others

By Distribution Channel

- Direct Sales

- Distributors & Stockists

- Online Sales

- OEM Contracts

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (6)