Content

What is the Algae-based Bioplastics Market Size and Share?

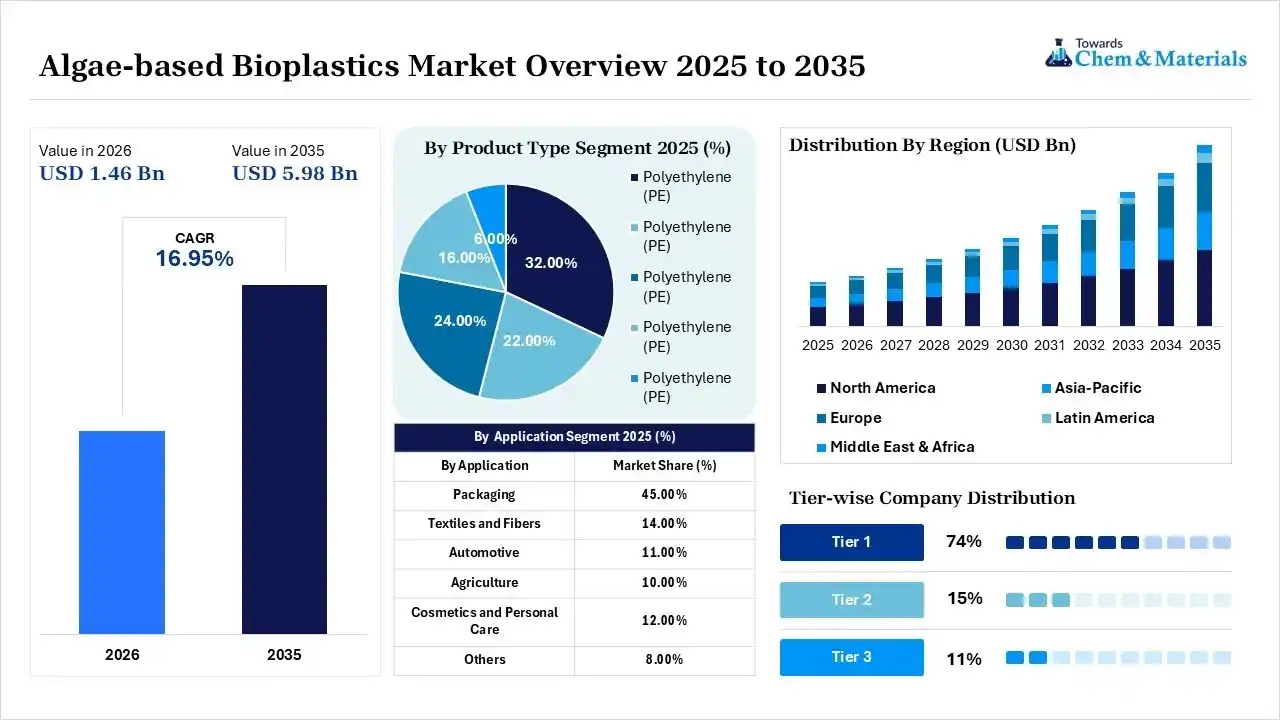

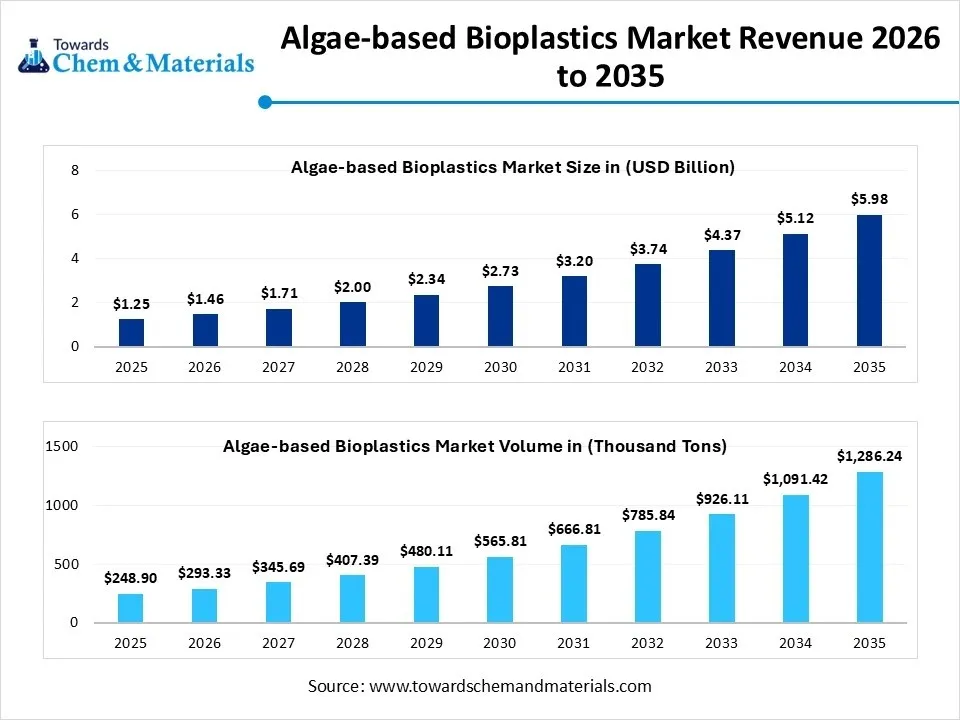

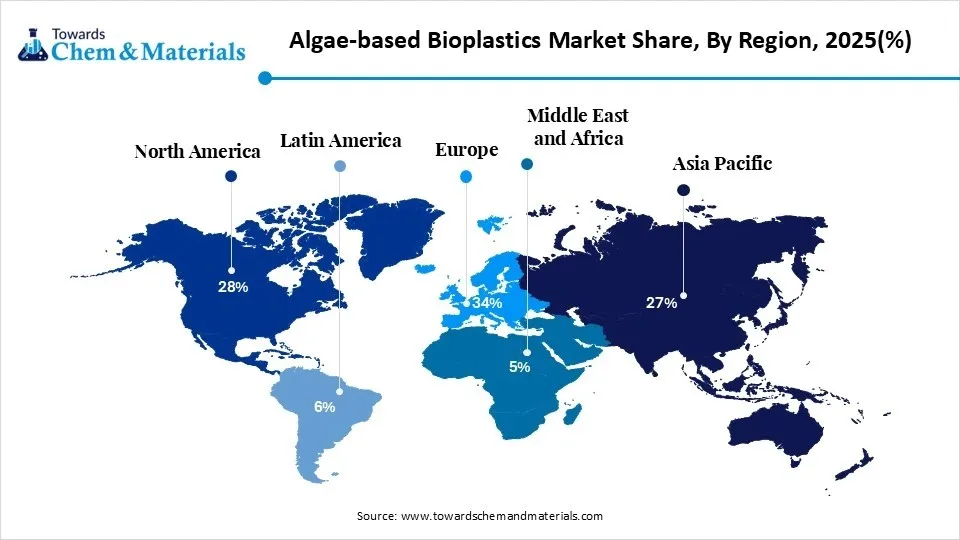

The global algae-based bioplastics market size was valued at USD 1.25 billion in 2025, is estimated to reach USD 1.46 billion in 2026, and is projected to reach USD 5.98 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 16.95% over the forecast period from 2026 to 2035.Europe dominated the algae-based bioplastics market with the largest revenue share of 34.0% in 2025 and is expected to grow at the fastest CAGR of 16.96% during the forecast period. In terms of volume, the algae-based bioplastics market is projected to grow from 248.9 thousand tons in 2025 to 1,286.2 thousand tons by 2035. growing at a CAGR of 17.85% from 2026 to 2035.Sustainable packaging alternatives is the key factor driving market growth. Also, stringent environmental regulations coupled with the ongoing innovations in polymer science can fuel market growth further.

Market Highlights

- By region, Europe dominated the market with the largest share of 34.0% in 2025. The dominance of the region can be attributed to the increasing consumer preference towards sustainable packaging.

- By region, Asia Pacific held a market share of 27.0% in 2025 and is expected to grow at the fastest CAGR of 18.40% over the forecast period. The growth of the region can be credited to the growing demand for sustainable packaging in emerging economies.

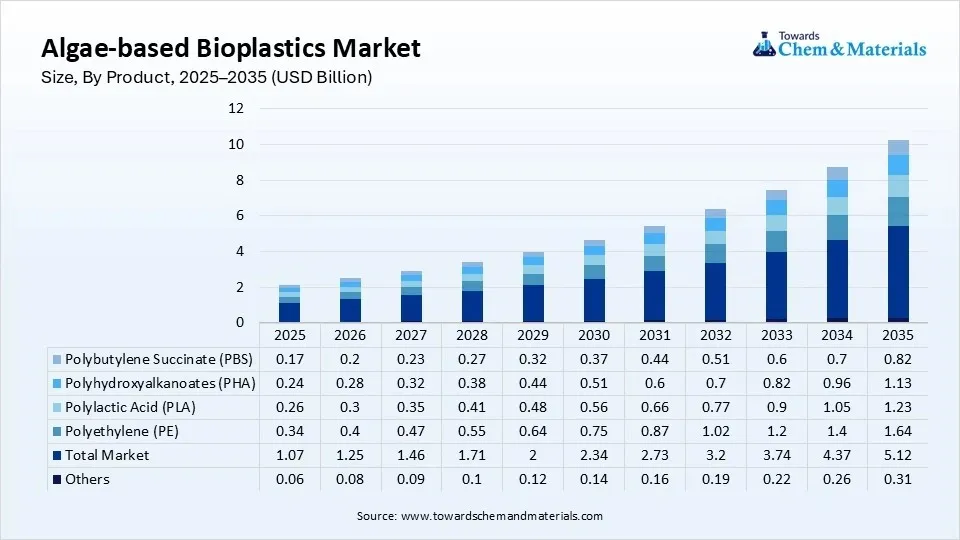

- By product type, the polyethylene (PE) segment dominated the market with the largest share of 32.0% in 2025. This segment acts as a sustainable "drop-in" substitute for conventional petroleum-based PE, providing identical durability and flexibility.

- By product type, the polyhydroxyalkanoates (PHA) segment held a market share of 16.0% in 2025 and is expected to grow at the fastest CAGR of 20.80% over the forecast period. Produced through the microbial fermentation of algal biomass, polyhydroxyalkanoate (PHA) biopolymers are highly prized for their exceptional marine biodegradability.

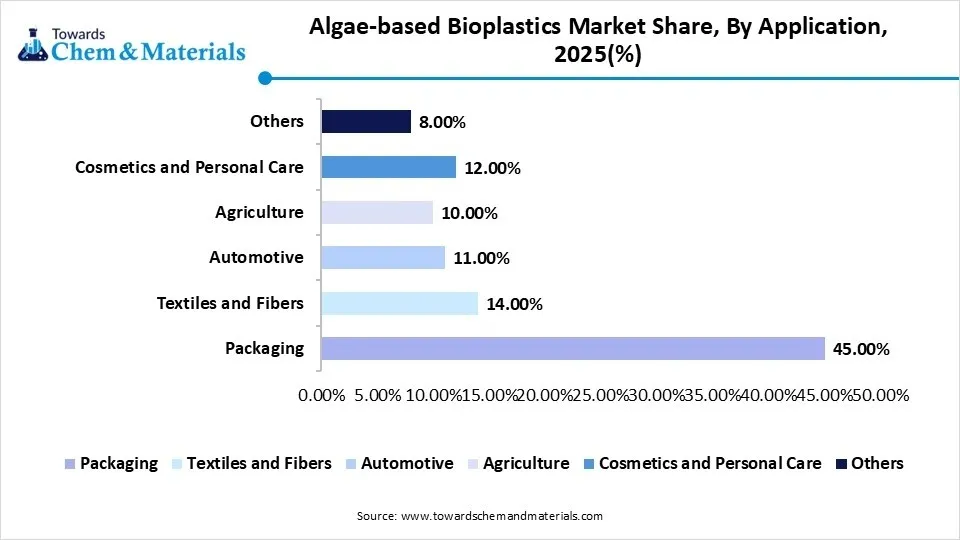

- By application, the packaging segment dominated the market with the largest share of 45.0% in 2025. This segment increasingly relies on algae to manufacture flexible films, biodegradable food containers, and e-commerce bags.

By application, the cosmetics and personal care segment held the market share of 12.0% in 2025 and is expected to grow at the fastest CAGR of 18.90% over the forecast period. Major beauty brands are using algae-based packaging to achieve a "zero-waste" or "circular economy" aesthetic.

Major consumer goods companies, retail groups, and food service operators are increasingly implementing stringent sustainability targets, such as packaging recyclability or compostability commitments, presenting crucial opportunities in the market. Major organizations are heavily engaging in development agreements with algae-material market players to validate supply chains and material performance.

- In June 2026, a prominent European research initiative, the LOCALITY Algae Project, achieved a major milestone in scaling innovative algae-based products. After screening nearly 70 ingredients to identify optimal strains, researchers successfully manufactured an industrial-scale aquafeed prototype.(Source: wwd.com)

Global Investment Flow for Algae-based Bioplastics 2026

The investment flows are mainly distinguished by AI-driven biomanufacturing, strategic corporate alliances, and regional policy mandates rather than pure venture capital for startups.

In April 2026, India's plastics exports expanded by 11.6%, achieving its first monthly increase in five months. This increase was partially supported by the clearance of previous backlogs, which had faced logistical delays due to shipping disruptions caused by the ongoing West Asian crisis.(Source: plexconcil.org)

According to data from the ICIS Supply and Demand Database, China's exports of commodity chemicals and plastics demonstrated sustained growth, with May volumes reaching a record of approximately 6.2 million tonnes, representing a 6% increase from April. Furthermore, export volumes from March to May 2026 registered a 43% year-on-year increase.(Source: www.icis.com)

Algae-Based Bioplastics Market Trends

- Increasing environmental awareness is the latest trend in the market shaping positive market growth. Consumers are rapidly becoming more aware of the ecological impact of conventional plastics, which leads to an increase in demand for sustainable alternatives.

- Government initiatives and regulations focused on minimizing plastic waste in recent years are playing an important role in the market. Many regions have imposed bans on single-use plastics, which has facilitated a growing demand for bioplastics as a viable alternative to conventional plastics.

- Partnerships and collaboration between major market players and stakeholders are the future trend in the market driving expansion. These companies are joining forces with NGOs, research institutions, and other players to boost innovation and fuel the development of bioplastics.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 1.46 Billion/ 293.3 Thousand Tons |

| Expected Size in 2035 | USD 5.98 Billion/ 1,286.2 Thousand Tons |

| Growth Rate | CAGR of 16.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Application, By Region |

| Key Companies Profiled | BZEOS, FLEXSEA, BLOM, Eranova, Sway Innovation Co., ALGBIO, PT Seaweedtama Biopac Indonesia |

AI-Powered Predictive Formulations in the Algae-based Bioplastics Market

Artificial intelligence is transforming the market by shifting material science past trial-and-error. ML algorithms like multi-objective genetic algorithms and artificial neural networks (ANN) are now used to forecast how varying ratios of algal polymers will perform in the future. In addition, algorithms can calculate structural properties that control biodegradability and ensure sustainable materials break down effectively.

Supply Chain Analysis of the Algae-based Bioplastics Market

Production & Processing

- It involves cultivating algae, harvesting the biomass, and extracting biopolymers such as starches or polyhydroxyalkanoates (PHAs).

- It also includes refining these extracts or blending them with other polymers, fueled by thermo-mechanical methods such as compression molding to produce final biodegradable products.

- Notpla Limited: A prominent UK-based sustainable packaging startup utilizing seaweed extracts to create biodegradable, edible, and zero-waste packaging solutions.

- Other Key Players: Algix, BZEOS

Quality Testing and Certification

- It is the process of verifying that seaweed and microalgae-based materials should fulfill stringent international benchmarks for safety, environmental sustainability, and mechanical performance.

- It also ensures that bioplastics are sustainable, biodegradable, and safe for consumer use.

- Lifeasible: A leading biotechnology company that provides solutions and technical processes for biopolymer extraction and tailoring.

- Other Key Players: Evoware, FLEXSEA

Distribution to Industrial Users

- It refers to a business-to-business (B2B) supply framework wherein producers of algae-based polymers and resins supply materials directly to large-scale commercial and industrial sectors.

- These enterprises subsequently integrate these biopolymers into broader production pipelines to manufacture finished commercial goods.

- Corbion N.V.: A major global player in biochemicals, producing lactic acid and bio-based polymers (PLA) heavily used in various industrial applications.

- Other Key Players: Evoware, Corbion N.V.

Algae-based Bioplastics Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union | Algae-based bioplastics used in food packaging must pass identical, rigorous migration tests to conventional plastics under Regulation (EU) No. 10/2011, alongside ecotoxicity screens under the European standard EN 13432. |

| United States | California (via AB 1201) and Washington state heavily restrict the terms "biodegradable" or "bio-based" on retail packaging. Products must achieve explicit third-party certification under ASTM D6400 standards for industrial composability to use these terms. |

| China | China regulates bioplastics tightly through national GB standards, requiring strict limits on heavy metals, mandatory trace labeling, and a high minimum organic carbon content. |

Market Dynamics

Driver

Increasing Consumer Demand for Sustainable Products

The surge in consumer demand for sustainable products is the major factor driving market growth. As consumers are increasingly becoming aware of their health, they are rapidly seeking products that are compatible with their values. In addition, by integrating bioplastics into their product offerings, organizations are significantly strengthening their market position. This strategic alignment addresses changing consumer demands for sustainable alternatives and serves as a key driver for the sustained expansion of the bioplastics industry.

Restraint

Food Security and Environmental Complexities

The current generation of bioplastics depends heavily on food crops such as corn and sugarcane. Diverting agricultural land to plastic manufacturing threatens good supply and increases food prices, hindering market growth. Moreover, processing raw crops includes high energy consumption, chemical fertilizers, and heavy water usage. If a plant relies on non-renewable energy, its carbon footprint can cancel its sustainability benefits.

Opportunity

Use of Advanced Material Blends and Composites

Manufacturing composite polymers by blending algae with existing bioplastics such as polyhydroxyalkanoates (PHA) and polylactic acid (PLA) enhances thermal properties, mechanical strength, and moisture barriers, creating future opportunities in the market. Furthermore, market innovators are expanding into the fashion industry by integrating algae-based biofoams into footwear manufacturing and processing biomass into sustainable textile fiber. Algal-derived polysaccharides, such as alginate and carrageenan, demonstrate substantial promise for biocompatible medical applications, advanced wound management, and sophisticated drug delivery systems.

Segmental Insights

Product Type Insight

The polyethylene (PE) segment dominated the market with the largest share of 32.0% in 2025. This segment acts as a sustainable "drop-in" substitute for conventional petroleum-based PE, providing identical durability, flexibility, and barrier properties with a substantially reduced carbon footprint. In addition, extracted from algae oils and biomass, bio-PE retains the moisture-barrier capabilities, structural integrity, and chemical resistance of fossil-fuel PE. Hence, market players are favoring algae-based PE, as it needs no major equipment upgrades for extrusion or molding, significantly minimizing the overall cost of adopting sustainable materials. Algae cultivation avoids land-use conflicts associated with crop-based bioplastics like corn or sugarcane, which makes it an increasingly attractive feedstock.

")

The polyhydroxyalkanoates (PHA) segment held a market share of 16.0% in 2025 and is expected to grow at the fastest CAGR of 20.80% over the forecast period. Produced through the microbial fermentation of algal biomass, polyhydroxyalkanoate (PHA) biopolymers are highly prized for their exceptional marine biodegradability and structural versatility when evaluated against alternatives such as polylactic acid (PLA). Growing global restrictions on single-use plastics directly impel market players towards fully marine-degradable PHA. Also, algae avoid competing with agricultural land or freshwater resources used for standard crop-based bioplastics.

Algae-based Bioplastics Market Share,By Product Type , 2025(%)

| By Product Type | Market Share (%) |

| Polyethylene (PE) | 32.00% |

| Polyethylene (PE) | 22.00% |

| Polyethylene (PE) | 24.00% |

| Polyethylene (PE) | 16.00% |

| Polyethylene (PE) | 6.00% |

Application Insight

The packaging segment dominated the market with the largest share of 45.0% in 2025. This segment increasingly relies on algae to manufacture flexible films, biodegradable food containers, and e-commerce bags. Advancements are specifically emphasizing enhancing barrier properties and extending shelf life. Algae-derived materials, like polylactic acid (PLA) and polyhydroxyalkanoates (PHA), are engineered to match the flexibility and tensile strength of traditional plastics. Moreover, major companies are using materials such as sodium alginate extracted from seaweed to create flexible, clear films created for dry product packaging.

")

The cosmetics and personal care segment held the market share of 12.0% in 2025 and is expected to grow at the fastest CAGR of 18.90% over the forecast period. Major beauty brands are using algae-based packaging to achieve a "zero-waste" or "circular economy" aesthetic. The material is generally marketed towards eco-aware consumers who demand non-fossil and cruelty-free fuel-derived containers. Furthermore, beyond their utilization in structural packaging, algae-derived extracts, specifically hydrocolloids and lipids, are integrated directly into cosmetic formulations to serve as antioxidants, moisturizing agents, photoprotective elements, and rheology modifiers.

Algae-based Bioplastics Market Share, By Application, 2025(%)

| By Application | Market Share (%) |

| Packaging | 45.00% |

| Textiles and Fibers | 14.00% |

| Automotive | 11.00% |

| Agriculture | 10.00% |

| Cosmetics and Personal Care | 12.00% |

| Others | 8.00% |

Regional Analysis

How did Europe Dominated the Algae-based Bioplastics Market in 2025?

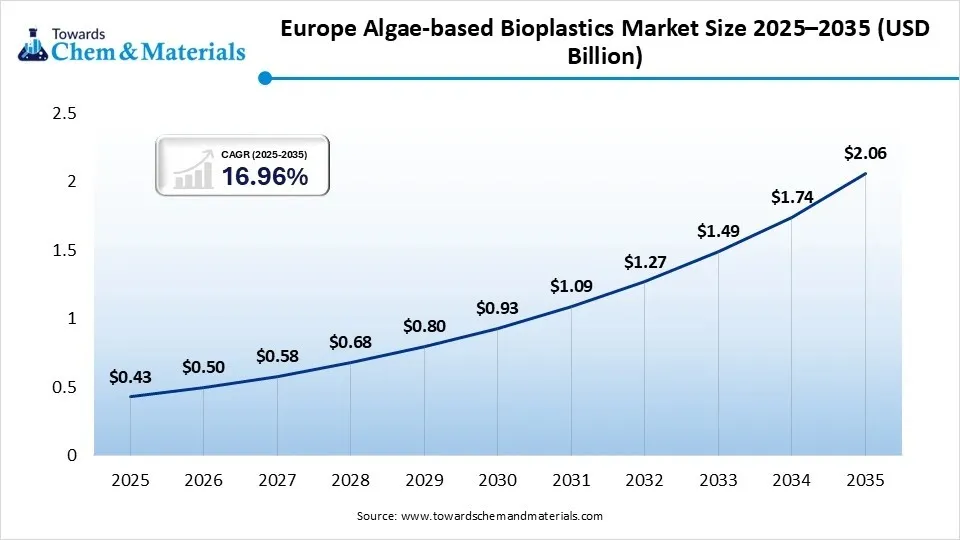

The Europe The Asia Pacific algae-based bioplastics market size was estimated at USD 0.43 billion in 2025 and is projected to reach USD 2.06 billion by 2035, growing at a CAGR of 16.96% from 2026 to 2035. Europe dominated the market with the largest share of 34.0% in 2025. The dominance of the region can be attributed to the increasing consumer preference towards sustainable packaging and the surge in investments in regional algae production industry innovations. In addition, major consumer brands in the region, especially in textiles, cosmetics, and food and beverage, have robust net-zero goals.

")

Germany

Algae-based bioplastics help achieve SDG targets in the country because algae sequester CO₂ rapidly and do not require freshwater or arable land, avoiding competition with food crops. German consumers are highly environmentally conscious and increasingly willing to pay premium prices for eco-friendly packaging and biodegradable products.

France

France is aggressively phasing out single-use plastics and enforcing the European Single Use Plastics (SUP) Directive. Algae-based solutions are highly prioritized as they are recognized as truly plastic-free. French innovators use local stranded green macroalgae and seaweed as raw materials, directly addressing coastal pollution and preventing ecological damage.

Asia Pacific

The Asia Pacific algae-based bioplastics market size was estimated at USD 0.34 billion in 2025 and is projected to reach USD 1.64 billion by 2035, growing at a CAGR of 17.04% from 2026 to 2035.Asia Pacific held a market share of 27.0% in 2025 and was expected to grow at the fastest CAGR of 18.40% over the forecast period. The growth of the region can be credited to the growing demand for sustainable packaging in emerging economies such as China, India, and Japan. Also, the region's extensive coastlines offer optimal conditions for cultivating macroalgae and microalgae, which makes it a highly scalable and cost-effective source of biomass.

China

China’s aggressive national mandates to ban or restrict single-use plastics have pressured industries to transition to eco-friendly alternatives. Research and development within China, emphasizing blending algal biomass with established polymers to improve thermal and mechanical properties.

India

India's national bans on specific single-use plastics have forced companies to seek scalable, biodegradable alternatives. FMCG and automotive manufacturing giants operating in India are increasingly shifting to green packaging to meet their net-zero and ESG goals.

North America

The North America algae-based bioplastics market size was estimated at USD 0.35 billion in 2025 and is projected to reach USD 1.70 billion by 2035, growing at a CAGR of 17.12% from 2026 to 2035.North America held a market share of 28.00% in 2025. The growth of the region can be linked to the substantial private R&D investments and increasing consumer preference for sustainable alternatives to petroleum-based plastics. Regional and state-level legislative mandates, aimed at curbing single-use plastics and mitigating carbon emissions, are optimizing industries to transition toward biodegradable packaging and sustainable consumer goods, leading to regional growth further.

United States

U.S. companies are adopting algae-derived packaging materials, such as those produced by American startups and manufacturers, to meet ESG (Environmental, Social, and Governance) targets and satisfy consumer preferences. Ongoing research into algal bioplastics' current market trends and technical aspects has improved the mechanical and thermal strength of algae-based composites, driving market growth soon.

Canada

R&D advancements in mixing algae biomass with traditional bioplastics improve the thermal, barrier, and mechanical properties of the final composite materials. A highly eco-conscious Canadian retail base is fuelling commercialization and pushing major brands to adopt biodegradable packaging alternatives.

Latin America

The Latin America algae-based bioplastics market size was estimated at USD 0.08 billion in 2025 and is projected to reach USD 0.39 billion by 2035, growing at a CAGR of 17.16% from 2026 to 2035.Latin America held a market share of 6.00% in 2025. The growth of the region can be driven by increasing environmental awareness, strict regulations on single-use plastics, and a rise in demand for sustainable agricultural packaging. Cultivators are increasingly adopting algae-derived bioplastics for biodegradable agricultural films and mulch sheets. These advanced materials provide a dual benefit: to ensure robust crop protection during the growing cycle while actively enriching the soil substrate upon decomposition.

Brazil

Brazil's vast coastline and high annual sunlight provide an optimal environment for large-scale microalgae cultivation. Brazil already hosts established, large-scale industrial algae operations. The technical expertise, wastewater utilization infrastructure, and lipid extraction capabilities already present in the region form a strong foundation for scaling up bioplastic polymer production.

Middle East and Africa

The Middle East & Africa algae-based bioplastics market size was estimated at USD 0.06 billion in 2025 and is projected to reach USD 0.33 billion by 2035, growing at a CAGR of 18.59% from 2026 to 2035.The Middle East & Africa held a market share of 5.00% in 2025. The growth of the region can be attributed to the algae's ability to grow without utilizing freshwater or arable land along with the stringent environmental policies. Furthermore, governments, including those of the UAE, Saudi Arabia, and South Africa, are implementing stringent regulations on single-use plastics to advance a circular economy and reduce carbon emissions.

")

Saudi Arabia

Companies are exploring downstream integration by coupling microalgae cultivation with industrial carbon capture systems for CO₂ feeding and local wastewater treatment facilities for nutrient provisioning. Leading industrial and manufacturing hubs like Riyadh, Jeddah, and Dammam are witnessing high adoption rates of biopolymers, particularly within the PE (polyethylene) segments.

UAE

The UAE has implemented strict bans on single-use plastics (e.g., Dubai's ban on single-use bags) and the wider goal to reach Net-Zero by 2050. Microalgae and macroalgae can be cultivated using the UAE's abundant coastlines and marine resources without exhausting the country's highly scarce freshwater supplies.

Competitive Analysis

The competitive landscape is distinguished by a mix of specialized biotechnology startups, research-driven companies, and strategic alliances emphasizing the commercialization of sustainable alternatives to petroleum-based plastics.

Notpla reached a major organizational milestone, securing €4 million in Horizon Europe funding to combat a primary driver of plastic pollution: disposable coffee cups. In partnership with 14 European entities, the company is developing a fully natural, home-compostable cup range with zero plastic coatings.

- Algix LLC pioneers the production of sustainable materials by converting aquatic biomass and nuisance algae into eco-friendly bioplastics. Operating from their Meridian, Mississippi facility, the company utilizes proprietary extrusion compounding technology to transform this biomass into their flagship line of Solaplast pellets.(Source: businessalabama.com),(Source: maritime-forum.ec.europa.eu)

Recent Developments

- In June 2026, Balrampur Chini Mills Limited, in strategic collaboration with the Lucknow Cantonment Board, formally launched Bioyug Green Command 2026. This initiative introduces a dedicated platform designed to accelerate India’s bioplastics ecosystem and promote sustainable consumption.(Source: www.chinimandi.com)

- In December 2025, Renaissance BioScience teamed up with UK-based Biome Bioplastics on a two-year, CAD $1.5 million project aimed at producing renewable bioplastic building blocks through advanced fermentation. The collaboration is backed by advisory services and funding from the National Research Council of Canada's Industrial Research Assistance Program and UK Research and Innovation’s Innovate.(Source: www.indianchemicalnews.com)

Strategic Profiles of Key Players Shaping the Algae-based Bioplastics Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| Algix | Market Pioneer / Established Leader | Meridian, Mississippi, USA | Global distribution (North America, Europe, Asia) | Algae-blended resins and thermoplastic compounds (Bloom brand) | High-volume commercialization and scaling of flexible foam infrastructure. |

| Erthos | Innovator / High-Growth Scale-up | Toronto, Canada | North America and manufacturing partnerships in Asia | Plant and algae-infused raw materials to replace traditional plastics | Seamless compatibility with existing plastic manufacturing machinery. |

| Loliware | Market Disrupter / Sustainability Specialist | New York, USA | North America and expanding European markets | Algae-derived pellets (SeaTech) for straws, utensils, and flexible packaging | High-speed, regenerative processing that replaces single-use plastics entirely. |

Other Key Players

- BZEOS

- FLEXSEA

- BLOM

- Eranova

- Sway Innovation Co.

- ALGBIO

- PT Seaweedtama Biopac Indonesia

Segments Covered in the Report

By Product Type

- Polyethylene (PE)

- Bio-based HDPE

- Bio-based LDPE

- Bio-based LLDPE

- Polypropylene (PP)

- Injection Grade

- Film Grade

- Fiber Grade

- Polylactic Acid (PLA)

- Extrusion Grade

- Injection Molding Grade

- 3D Printing Grade

- Polyhydroxyalkanoates (PHA)

- PHB

- PHBV

- Medium Chain Length PHA

- Others

- Algae-Based Polyurethane

- Algae Blends

- Starch-Algae Composites

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Food Packaging

- Beverage Packaging

- Textiles and Fibers

- Apparel Fibers

- Industrial Fibers

- Nonwoven Fabrics

- Automotive

- Interior Components

- Trim Parts

- Under-the-Hood Components

- Agriculture

- Mulch Films

- Seed Coatings

- Plant Pots

- Cosmetics and Personal Care

- Containers

- Tubes

- Caps & Closures

- Others

- Consumer Goods

- Electronics

- Medical Products

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)