Content

What is the Asia Pacific Emulsion Polymer Market Size and Share?

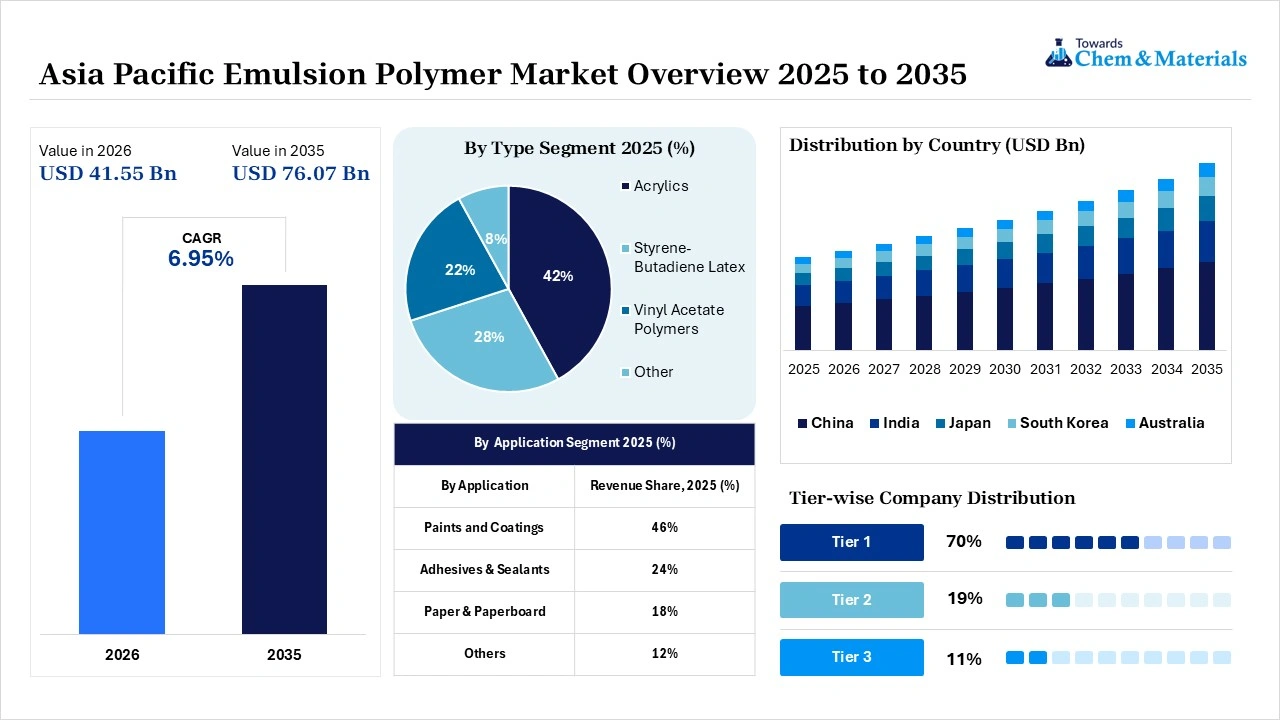

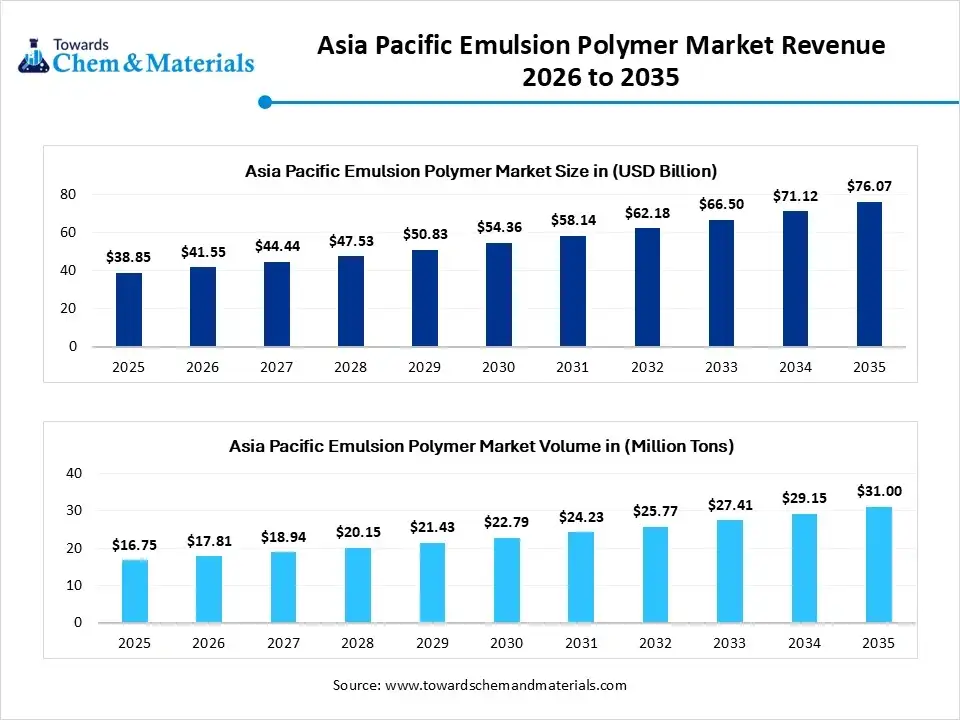

The Asia Pacific emulsion polymer market size was valued at USD 38.85 billion in 2025, is estimated to reach USD 41.55 billion in 2026, and is projected to reach USD 76.07 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.95% over the forecast period from 2026 to 2035.China dominated the emulsion polymer market with the largest revenue share of 48% in 2025 and is expected to grow at the fastest CAGR of 7.06% during the forecast period. In terms of volume, the Asia Pacific emulsion polymer market is projected to grow from 16.75 million tons in 2025 to 31.00 million tons by 2035. growing at a CAGR of 6.35% from 2026 to 2035.The growth of the market is driven by the growing demand and initiatives for expansion, which fuel the market's growth.

Market Highlights

- By country, China dominated the market with a share of 48% in 2025. Large-scale construction activity and manufacturing dominance sustain regional leadership.

- By country, India held 22% market share in 2025 and is expected to experience the fastest growth with a CAGR of 8.35% in the forecast period. Rapid urbanization and industrialization accelerate construction chemical consumption.

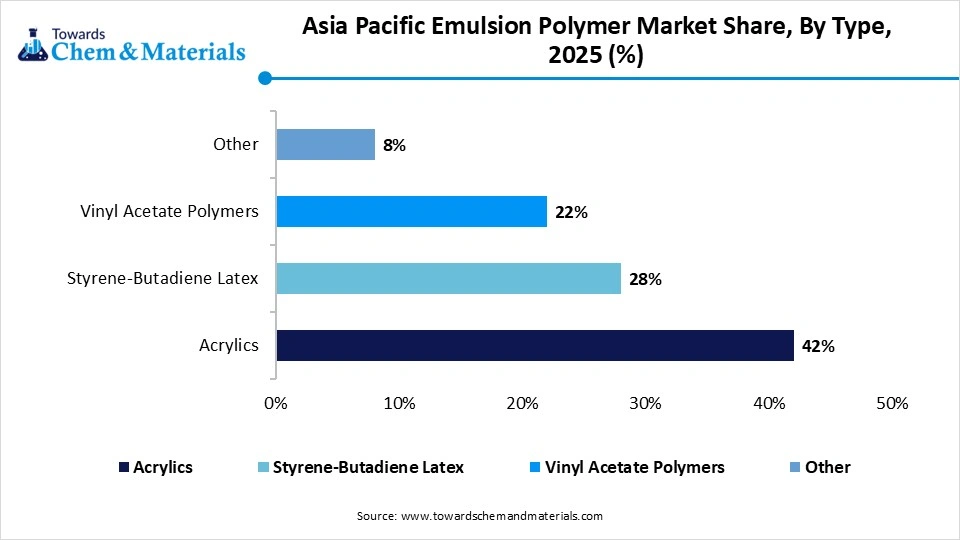

- By type, the acrylics segment dominated the market with 42% share in 2025. Strong demand from low-VOC architectural coatings supports acrylic adoption across the Asia Pacific.

- By type, the other segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.10% in the forecast period. Specialty emulsion technologies gain traction in high-performance coatings applications.

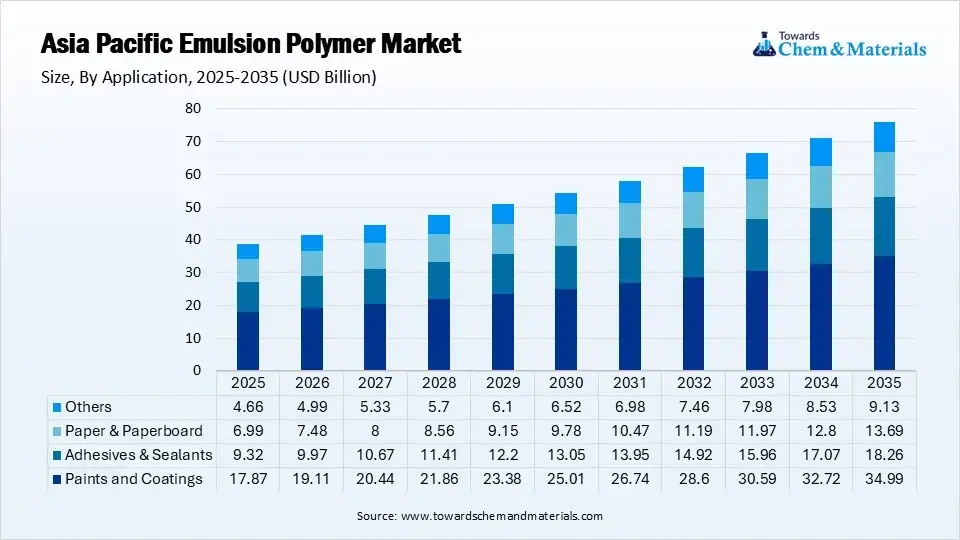

- By application, the paints and coatings segment dominated the market with 46% share in 2025. Rapid urbanization and infrastructure development increase decorative coating demand.

- By application, the other segment held 12% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.95% in the forecast period. Textile finishing and nonwoven applications increase specialty emulsion requirements.

- By end-use, the building & construction segment dominated the market with 39% share in 2025. Residential and commercial construction projects boost coatings and adhesive demand.

- By end-use, the textile & coatings segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.05% in the forecast period. Technical textile manufacturing increases advanced emulsion consumption significantly.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 38.85 Billion | CAGR (2026–2035): 6.95%

- Market Projected Size (2035): USD 76.07 Billion

- China: Revenue Share of 48% in 2025|USD 18.65 Billion

- Market Estimated Volume (2025): 16.75 Million Tons | Volume CAGR (2026–2035): 6.35%

- Market Projected Volume (2035): 31 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,855/Ton

- Average Selling Price (2025): USD 2,160/Ton

- Pricing CAGR (2026–2035): 3.55%

The Asia Pacific emulsion polymer market is globally key as it is the largest consumer and fastest-growing center for water-based polymer formulations. This growth is driven by rapid urbanization and green building initiatives, making the region dominant due to its dependence on eco-friendly, low-VOC materials in construction and manufacturing.

The building sector is the largest industry, supported by major government infrastructure projects, swift residential housing expansion, and increasing disposable incomes, which sustain high demand for emulsion polymers used in concrete modification, waterproofing, and architectural coatings.

As health and environmental concerns lead to the phase-out of traditional solvent-based systems across manufacturing sectors, water-based polymer emulsions gain importance because they lower VOC emissions and provide a safer, sustainable alternative for indoor and outdoor use.

Stricter environmental regulations in fast-developing economies encourage the adoption of green building materials, significantly boosting emulsion polymer technology. These polymers are vital binders in the extensive paints and coatings, and adhesives sectors, valued for their excellent film formation, adhesion, and durability. Countries like China and India are major manufacturing hubs, benefiting from affordable raw materials, land, and labor.

Market Growth Trends

- The Shift to Water-Based Systems: Driven by strict government regulations on volatile organic compound emissions, manufacturers across automotive, textiles, and packaging are actively replacing traditional solvent-based formulations with eco-friendly, water-based polymer emulsions.

- Construction & Infrastructure Boom: Increased public spending and a rising middle class are accelerating construction activities in the region. Emulsion polymers are critical ingredients in architectural coatings, waterproofing membranes, and sealants, directly benefiting from this expansion.

- Automotive and Consumer Durables: Developing economies in Southeast Asia and India are witnessing higher disposable incomes, leading to an uptick in automobile manufacturing and consumer appliances. Emulsion polymers are extensively used in interior coatings, adhesives, and synthetic leather for these sectors.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 41.55 Billion / 17.81 Million Tons |

| Revenue Forecast in 2035 | USD 76.07 Billion / 31.00 Million Tons |

| Growth Rate | CAGR 6.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Type, By Application, By End-Use, By Country |

| Key Companies Profiled | Synthomer plc, Trinseo PLC, Arkema S.A, DIC Corporation, JSR Corporation, BASF SE, Clariant, Dow, Akzo Nobel N.V., OMNOVA Solutions, Asahi Kasei Corporation, Dairen Chemical Corporation, Nova Polychem, Kamsons Chemicals Pvt. Ltd., Apcotex Industries Ltd., Sumitomo Chemical |

Key Technological Shifts in the Asia Pacific Emulsion Polymer Market

The Asia Pacific emulsion polymer market is pivoting rapidly toward sustainability, bio-based latex technologies, and high-performance applications. Driven by tightening regulations and urban infrastructure growth in countries like China and India, the industry is transitioning to low-VOC, water-based coatings and advanced nanomaterial-infused polymers. The market is witnessing a rise in specialty engineered polymers, like conductive polymers, designed to meet the rigorous high-performance demands of electronics and consumer goods.

Supply Chain Analysis of the Asia Pacific Emulsion Polymer Market

- Polymer Production & Emulsion Processing:Emulsion polymers are produced through emulsion polymerization processes using monomers such as acrylics, vinyl acetate, styrene-butadiene, and vinyl chloride to manufacture water-based polymer dispersions for coatings, adhesives, textiles, and paper applications. The Asia Pacific market is expanding rapidly due to strong growth in the construction, packaging, and automotive industries.

- Key players: BASF, Arkema, Synthomer, Wacker Chemie

- Quality Testing and Certification:Emulsion polymers must comply with standards for viscosity, particle size distribution, adhesion performance, VOC emissions, and environmental safety regulations for industrial and consumer applications.

- Key players: International Organization for Standardization, ASTM International, Bureau of Indian Standards, European Chemicals Agency

- Distribution to Industrial Users:Emulsion polymers are supplied to paints and coatings manufacturers, adhesives and sealants producers, textile processing industries, paper and packaging companies, and construction material manufacturers across the Asia Pacific region.

- Key players: BASF, Arkema, Synthomer.

Asia Pacific Emulsion Polymer Regulatory Landscape: Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| China | Ministry of Ecology and Environment (MEE); Ministry of Industry and Information Technology (MIIT) | Environmental Protection Law; VOC Emission Standards | Low-VOC coatings, industrial sustainability | China promotes water-based emulsion polymers to reduce VOC emissions in paints, adhesives, and construction applications. |

| India | Ministry of Environment, Forest and Climate Change (MoEFCC); Bureau of Indian Standards (BIS) | Environment Protection Act; BIS Paint & Coating Standards | Sustainable coatings, chemical safety | India is encouraging eco-friendly emulsion polymers due to increasing infrastructure and construction activities. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of the Environment | Chemical Substances Control Law (CSCL); Air Pollution Control Act | Chemical safety, low-emission materials | Japan emphasizes high-performance and environmentally friendly emulsion polymer technologies. |

| South Korea | Ministry of Environment (MOE); Ministry of Trade, Industry and Energy (MOTIE) | K-REACH; Clean Air Conservation Act | Sustainable polymers, emissions reduction | South Korea supports advanced water-based polymer systems for coatings and electronics applications. |

| Australia | National Industrial Chemicals Notification and Assessment Scheme (NICNAS); Department of Climate Change, Energy, the Environment and Water | Industrial Chemicals Act; Environmental Protection Regulations | Chemical registration, sustainability | Australia regulates polymer chemicals with strong emphasis on environmental safety and industrial compliance. |

| Southeast Asia | ASEAN Chemicals Regulatory Framework; National Environmental Agencies | ASEAN Harmonized Chemical Standards | Industrial coatings, adhesives, packaging | Southeast Asian countries are increasingly adopting low-VOC and water-based polymer technologies across industrial sectors. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Asia Pacific Emulsion Polymer Market?

The Asia Pacific emulsion polymer market is primarily propelled by rapid urbanization, infrastructure development, and strict environmental regulations, pushing the demand for water-based, eco-friendly alternatives. The booming paints, coatings, and construction sectors in developing economies like China and India act as the strongest catalysts. Stringent government policies aimed at reducing volatile organic compound emissions are driving manufacturers away from traditional solvent-based materials. This has spurred a massive shift toward sustainable, water-based emulsion polymers. Growing consumer and industrial awareness regarding sustainability has prompted ongoing innovation. The development of bio-based emulsion polymers aligns with regional "green building" initiatives and biofuel policies.

Restrains

What are the Key Growth Restraints of the Asia Pacific Emulsion Polymer Market?

The primary restraints for the Asia Pacific emulsion polymer market include the high volatility of petrochemical-based raw material prices like styrene and acrylic monomers, stringent environmental regulations regarding VOC emissions, and stiff competition from alternative materials like solvent-based coatings and natural resins. Emulsion polymers rely heavily on petrochemical derivatives such as styrene, butadiene, and acrylates. These raw materials are tied to crude oil prices, their cost fluctuate significantly. Governments in the Asia Pacific region are increasingly focused on reducing carbon footprints and limiting volatile organic compound emissions, particularly in countries like China and India

Opportunities

What are the Key Growth Opportunities of the Asia Pacific Emulsion Polymer Market?

The Asia Pacific emulsion polymer market is driven by a booming construction sector, rising demand for water-based paints, and stringent eco-friendly regulations. Key growth opportunities are driven by strict environmental regulations regarding VOC emissions, rapid urbanization, and a surging demand for eco-friendly architectural coatings, adhesives, and sustainable packaging across rapidly industrializing hubs like China and India. Rapid urbanization and massive state-sponsored infrastructure projects drive substantial demand for emulsion polymers in architectural paints, cement modifications, sealants, and waterproofing. Growing consumer and industry awareness of environmental issues is accelerating the adoption of eco-friendly, biodegradable, and recyclable polymer emulsions in food packaging and paper coatings.

Segmental Insights

Type Insights

The acrylics segment dominated the market with 42% share in 2025, driven primarily by booming construction activities, increasing infrastructure investments, and strict environmental regulations that mandate the use of low-VOC, eco-friendly water-based coatings. Acrylic emulsions act as primary binders, offering superior weather resistance, UV stability, and durability for both interior and exterior surfaces. Stricter regional policies limiting harmful solvents are pushing manufacturers to shift toward sustainable, water-based acrylic emulsions.

")

The styrene-butadiene latex segment held 28% market share in 2025, driven by the region's booming paper packaging industry, surging infrastructure development, and a strong shift toward sustainable manufacturing in countries like China, India, and Japan. Rapid urbanization and infrastructure projects in developing economies are accelerating market growth. SB latex is widely used as a modifying agent in concrete, mortars, and sealants due to its excellent tensile strength, thermal stability, and superior waterproofing capabilities.

The vinyl acetate polymers segment held 22% market share in 2025, driven by booming construction in developing nations, a major shift toward eco-friendly water-based products, and surging demand for high-performance adhesives and paints. VAP is a fundamental building block for polyvinyl acetate and ethylene-vinyl acetate adhesives. Rising demands for sustainable, low-emission adhesives from the packaging, woodworking, and textile industries are accelerating segment growth.

The other segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.10% in the forecast period. The other segment includes polyurethane dispersions, fluoropolymer emulsions, and silicone-modified emulsions. The polyurethane dispersions segment is riven by stringent environmental regulations limiting VOC emissions and a booming demand for eco-friendly, water-based coatings in the automotive, construction, and textile sectors. The fluoropolymer emulsions segment is driven by stringent environmental regulations limiting VOC emissions and a booming construction sector that requires high-performance coatings. The silicone-modified emulsions segment is driven by increasing demand for high-performance coatings, stringent environmental regulations requiring low-VOC formulations, and expanding applications.

Asia Pacific Emulsion Polymer Market Share,By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Acrylics | 42% |

| Styrene-Butadiene Latex | 28% |

| Vinyl Acetate Polymers | 22% |

| Other | 8% |

Application Insights

The Paints And Coatings Segment Dominated The Asia Pacific Emulsion Polymer Market With 46% Market Share In 2025

The paints and coatings segment dominated the market with 46% share in 2025, experiencing rapid growth due to surging construction activity, strict environmental regulations curbing VOC emissions, and a shift toward water-based technologies. Emulsion polymers provide vital durability and adhesion properties to architectural and industrial paints.

Consumers and governments are demanding green coatings. Emulsion polymers allows the production of water-based paints that emit significantly lower toxic VOCs compared to traditional solvent-based alternatives.

The adhesives & sealants segment held 24% market share in 2025, driven by robust demand in building, automotive, and packaging sectors. The shift toward water-based, eco-friendly formulations is a primary catalyst, enabling emulsion polymers to replace solvent-based alternatives across multiple industries. Booming infrastructure investments supported by policies like India’s "Make in India" and China's "Made in China 2025" are heavily propelling structural adhesive and sealant usage. Additionally, vehicle lightweighting trends are increasing the demand for high-performance adhesives over traditional mechanical fasteners.

")

The paper & paperboard segment held 18% market share in 2025, due to surging demand for eco-friendly packaging, stringent plastic-ban regulations, and the rapid growth of regional e-commerce. Emulsion polymers are crucial for enhancing paper packaging with grease resistance, moisture barriers, and high-quality printability. These polymers improve paper strength, gloss, and smoothness, meeting the high aesthetic standards required for commercial printing and retail displays.

The other segment held 12% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.95% in the forecast period. The other segment includes textile finishing, nonwoven applications, and leather processing. The textile finishing segment is growing, driven by rising demand for high-performance fabrics, increasing regional textile manufacturing, and a strong shift toward eco-friendly, water-based chemical treatments. The nonwoven applications segment is driven primarily by soaring demand for disposable hygiene products, medical textiles, and eco-friendly manufacturing. The leather processing segment is driven by surging demand for sustainable synthetic leather and stringent environmental regulations. Manufacturers are increasingly replacing traditional solvent-based treatments with sustainable polymer emulsions.

End-Use Insights

The building & construction segment dominated the market with 39% share in 2025, driven by growing urbanization & disposable incomes across developing nations like China & India. This booming infrastructure and residential development are fueling demand for eco-friendly, high-performance materials. Governments across the Asia Pacific are enforcing strict environmental regulations to curb VOC emissions.

The automotive segment held 21% market share in 2025, due to rising vehicle production and strict environmental regulations. Emulsion polymers, specifically acrylics and styrene-butadiene latex, are heavily used in water-borne paints, coatings, and adhesives. EVs require lightweight materials, advanced battery adhesives, and specialized acoustic dampening. Emulsion polymers such as acrylics and styrene-butadiene latex are essential for manufacturing these high-performance components.

The chemicals segment held 16% market share in 2025, largely propelled by a massive shift toward sustainable, low-VOC (Volatile Organic Compound) chemical formulations. Stringent environmental regulations and booming end-use industries like construction and automotive are driving strong demand. Expanding chemical usage in automotive coatings, adhesives, and consumer durables continues to push regional market growth.

The textile & coatings segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.05% in the forecast period, driven by a regional shift toward eco-friendly, water-based formulations and surging infrastructure investments. This segment benefits from enhanced fabric finishing capabilities and stringent environmental regulations restricting toxic solvent emissions. In the textile sector, polymer emulsions are in high demand for finishing processes that improve fabric durability, water resistance, and elasticity.

Country Level Analysis

The China emulsion polymer market size was estimated at USD 18.65 billion in 2025 and is projected to reach USD 36.89 billion by 2035, growing at a CAGR of 7.06% from 2026 to 2035.China dominated the market with a share of 48% in 2025, primarily driven by strict environmental regulations requiring low-VOC formulations, massive infrastructure development, and a surging demand for water-based, eco-friendly coatings, adhesives, and paints. Government initiatives pushing for sustainable manufacturing processes and restricting Volatile Organic Compounds (VOCs) compel manufacturers to shift from solvent-based to water-based polymer emulsions. The booming e-commerce and consumer goods sectors are significantly driving up the use of emulsion polymers for paper coatings and pressure-sensitive adhesives.

The India emulsion polymer market size was estimated at USD 8.55 billion in 2025 and is projected to reach USD 17.12 billion by 2035, growing at a CAGR of 7.19% from 2026 to 2035.India held 22% market share in 2025 and is expected to experience the fastest growth with a CAGR of 8.35% in the forecast period. This growth is primarily fueled by massive infrastructure development, rapid urbanization, and a surging demand for eco-friendly, water-based paints, coatings, and adhesives across the automotive and construction sectors. India benefits from the easy availability of low-cost raw materials, cheap labor, and established manufacturing infrastructure, making it a highly profitable and rapidly scaling market for both local and global chemical players.

Recent Developments

- In September 2025, Shalimar Paints introduced three premium, eco-friendly, and durable product lines: Hero Insignia, Hero Weather Guard 12, and Superlac PU Gloss, targeting luxury residential and commercial segments. These new offerings feature zero VOC levels, anti-scuff properties, and extended warranties ranging from 10 to 12 years.(Source: www.manufacturingtodayindia.com)

- In December 2025, Indicus Paints launched Neotė, branded as India’s first luxury heritage paint line, featuring an "India Modern" aesthetic inspired by Tamil Nadu's cultural legacy. The premium, low-VOC interior emulsion offers a velvet-touch finish with advanced stain-resistant, antimicrobial technology.(Source: rprealtyplus.com)

Top players in the Asia Pacific Emulsion Polymer Market & Their Offerings

- Synthomer plc: Synthomer is a major producer of emulsion polymers used in paints, coatings, adhesives, construction chemicals, and textiles. The company focuses on water-based and low-VOC polymer technologies.

- Trinseo PLC: Trinseo offers latex binders and specialty emulsion polymers for coatings, paper, carpet backing, and adhesive applications across Asia Pacific.

- Arkema S.A.: Arkema develops advanced acrylic emulsions and specialty polymer dispersions used in coatings, construction, packaging, and pressure-sensitive adhesives.

- DIC Corporation: DIC manufactures emulsion polymers and resins for printing inks, coatings, adhesives, and industrial applications, with a strong presence in Japan and Southeast Asia.

- JSR Corporation: JSR produces synthetic latex and emulsion polymers used in paper processing, automotive, electronics, and coatings industries.

Other Top Players Are

- BASF SE

- Clariant

- Dow

- Akzo Nobel N.V.

- OMNOVA Solutions

- Asahi Kasei Corporation

- Dairen Chemical Corporation

- Nova Polychem

- Kamsons Chemicals Pvt. Ltd.

- Apcotex Industries Ltd.

- Sumitomo Chemical

Segments Covered

By Type

- Acrylics

- Pure Acrylic Emulsion

- Styrene Acrylic Emulsion

- Acrylic Copolymer Emulsion

- Styrene-Butadiene Latex

- Carboxylated SBR Latex

- Non-carboxylated SBR Latex

- High Solids SBR Latex

- Vinyl Acetate Polymers

- Vinyl Acetate Ethylene (VAE)

- Polyvinyl Acetate (PVA)

- Vinyl Acrylic Emulsion

- Other

- Polyurethane Dispersions

- Fluoropolymer Emulsions

- Silicone Modified Emulsions

By Application

- Paints and Coatings

- Architectural Coatings

- Industrial Coatings

- Protective Coatings

- Adhesives & Sealants

- Pressure Sensitive Adhesives

- Construction Adhesives

- Packaging Adhesives

- Paper & Paperboard

- Paper Coating

- Paper Binding

- Barrier Coatings

- Others

- Textile Finishing

- Nonwoven Applications

- Leather Processing

By End-Use

- Building & Construction

- Residential Construction

- Commercial Construction

- Infrastructure Projects

- Automotive

- OEM Coatings

- Interior Applications

- Tire Cord Applications

- Chemicals

- Specialty Chemicals

- Industrial Processing

- Polymer Modification

- Textile & Coatings

- Technical Textiles

- Decorative Textiles

- Industrial Fabric Coatings

- Others

- Packaging

- Consumer Goods

- Electronics

By Country

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (5)