Content

Engineered Polymers Market Trends, Growth and Market Size Analysis

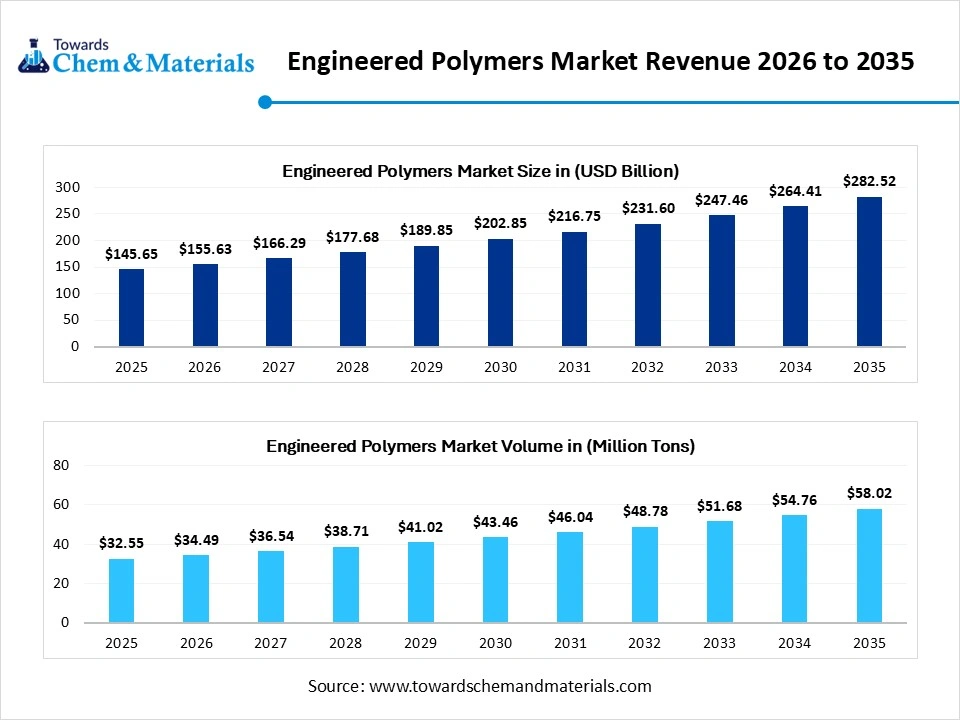

The global engineered polymers market Size was valued at USD 145.65 billion in 2025, is estimated to reach USD 155.63 billion in 2026, and is projected to reach USD 282.52 billion by 2035, growing at a CAGR of 6.85% from 2026 to 2035. In terms of volume, the Engineered Polymers market is projected to grow from 32.55 million tons in 2025 to 58.02 million tons by 2035. growing at a CAGR of 5.95% from 2026 to 2035. The growth of the market is enhanced by rising focus on capacity expansion, technological innovation, recycling technologies, sustainability practices, and value-added applications.

Market Highlights

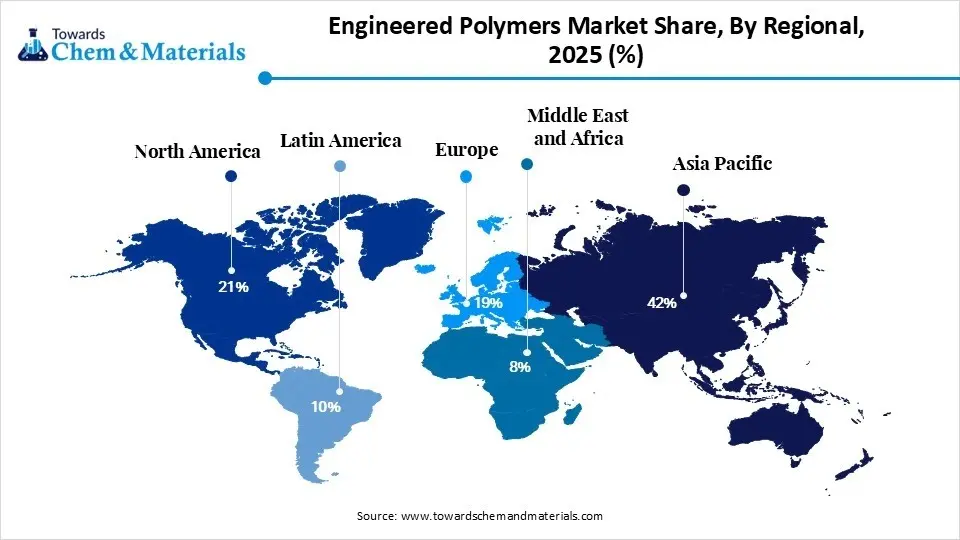

- By region, Asia Pacific dominated the engineered polymers market by holding 42% share in 2025 and is expected to grow at the fastest with a CAGR of 7.5% during the forecast period.

- By region, North America held the 21% market share in 2025 and expects notable growth in the market with 6.20% CAGR during the forecast period.

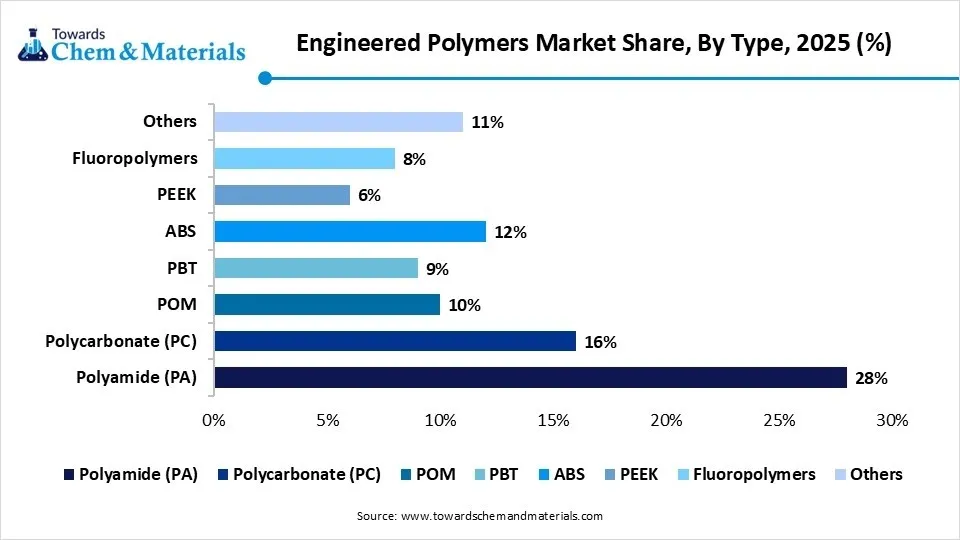

- By type, the polyamide (PA) segment dominated the market with the largest share of 28% in 2025

- By type, the PEEK segment held 6% market share in 2025 and is expected to grow at the fastest CAGR of 8.5% over the forecast period.

- By form, the pellets segment dominated the market with the largest share of 46% in 2025

- By form, the films & sheets segment held 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period.

- By end-use industry, the automotive segment dominated the market with the largest share of 32% in 2025

- By end-use industry, the electrical & electronics segment held 24% market share in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period.

- By processing technology, the injection molding segment dominated the market with the largest share of 44% in 2025

- By processing technology, the compression molding segment held 10% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 145.65 Billion | CAGR (2026–2035): 6.85%

- Market Projected Size (2035): USD 282.52 Billion

- Market Volume (2025): 32.55 Million Tons | Volume CAGR (2026–2035): 5.95%

- Market Projected Volume (2035): 58.02 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 3.19/kg

- Average Selling Price: USD 4.28/kg

- Pricing CAGR (2025–2035): 3.6%

Market Overview

Engineered polymers are recognized for their dimensional stability, chemical resistance, oxidative stability, and strength-to-weight ratio. Industry increasingly focuses on metal-to-plastic conversion and high-performance thermoplastics, making them key for advanced manufacturing.

The transition towards a circular economy and sustainability is shaping the invention of bio-based engineering polymers and the integration of recyclable technologies in precision-driven infrastructure. Additionally, the regulatory compliance and governmental initiatives for end-of-life management of polymers are fueling the market growth.

Market Trends

- Emerging Integration of Sustainable Polymers: The rising focus towards sustainability, driving the adoption of bio-based and recycled polymers align with advanced polymer processing technologies shaping the trend.

- Focus on Metal-to-Plastic Conversion: The industrial strategic shift focuses on the replacement of heavy metal with high-performance polymers to lower the environmental impact, weight reduction, and operation cost.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 155.63 Billion / 34.49 Million Tons |

| Revenue Size and Volume Forecast in 2035 | USD 282.52 Billion / 58.02 Million Tons |

| Growth Rate | CAGR 6.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Form, By End-Use Industry, By Processing Technology, By Regions |

| Key companies profiled | Grand Pacific Petrochemical Corporation, Mitsubishi Engineering-Plastics Corporation, Wittenburg Group, BASF SE, Asahi Kasei Corporation, SABIC, DuPont, LG Chem, Toray, Covestro AG, Piper Plastics Corp., Chevron Phillips Chemical Company LLC, Daicel Corporation, Evonik Industries AG, Eastman Chemical Company, Ascend Performance Materials, Lanxess, Celanese Corporation, Ravago, Teknor Apex, Trinseo LLC, Polyplastics Co., Ltd., Ngai Hong Kong Company Ltd., Ginar Technology Co., Ltd. |

Key Technological Shifts and AI in the Engineered Polymers Market

The technological advancement and AI-driven smart manufacturing are transforming the engineered polymers market. Machine learning is driving autonomous material discovery. The predictive analytics lowering R&D cycle for high-performance PEEK, PC, polyamide, and LCP aligns with re-compounding post-consumer recycled polymers.

The adoption of injection molding, extrusion, and blow molding enables real-time defect detection and energy optimization by maximizing operation yield and precision. The technological shift is boosting the scaling of sustainable chemistry in engineered polymers and industrial automation to meet demanding standards in EV and 5G infrastructure.

Supply Chain Analysis of the Engineered Polymers Market

- Raw Material Sourcing: The stage of initial feedstock, where fossil fuels are cracked and refined into key chemical precursors and resin production that is found in engineered polymers.

- Key Players: ExxonMobil, Sinopec, Reliance Industries, LyondellBasell, and Saudi Aramco

- Polymerization and Technical Compounding: The stage where key monomers are converted into high-performance polyamides, POM, PEEK, and Polycarbonates through advanced polymerization. These polymers are mixed with specialty additives, reinforcing fibers, and flame retardants for heavy-duty applications.

- Key Players: Celenese Corporation, Solvay, Covestro AG, Evonik Industries, Victrex plc, and BASF SE

- Distribution and End-Use Integration: The stage involves specialized logistics where engineered polymers are integrated into final components for OEMs. The stage utilizes injection molding, 3D printing, and extrusion for medical implants, battery housing, and aerospace components.

- Key Players: Avient Corporation, Supreme Industries Ltd., Kingfa Science & Technology, Bhansali Engineering Polymers Ltd and Nexeo Plastics

Regulatory Framework: Engineered Polymers Market

| Region | Key Regulations | Regulatory Focus |

| European Union | REACH Revision, PPWR and RoHS | Registration of polymers and focus on SVHC used in high-performance fluoropolymers, and restricting microplastics in the automotive and packaging sectors. |

| North America | EPA standards, TSCA, and PFAS Strategic Roadmap | Focus on workers' safety and performance of engineered polymers. Restrictions for PFAS are formed during the fluorination of plastic containers and surface coating. |

| Asia Pacific | BIS, Plastic Waste Management Rules, GB Standards, Quality Control Orders | Mandating BIS certification for quality control and import safety of engineering resins. Focus on standardization in local manufacturing of engineered polymers in EV battery housing and electrical connectors |

| Global | Annex XVII of Microplastics | Focus on physical particle restrictions like polymer powders, granules used in industrial processes |

Engineered Polymers Market Dynamics

Driver

Strong Government Funding and Strategic Partnership

The government initiative enables the acceleration of domestic manufacturing of specialized polymers. The governmental regulatory framework is encouraging major players to implement engineered polymers as replacements for metals in industrial landscapes through strategic collaboration and agreements.

Restraints

Raw Material Instability and Import Dependency

The need for specialized feedstock is driving the supply chain towards price volatility in advanced grade and reliance on imports for specialty and advanced polymer, restraining broader industrial adoption in domestic scale.

Opportunity

Massive Investment in Industrial Infrastructure

The transition towards a circular economy enables the opportunity for the adoption of bio-based feedstock, mass balance certified materials, and chemically recycled polymers in semiconductor reshoring, electrification, high-speed telecommunication, and healthcare expansion through sustainable investments.

Segmental Insights

Type Insights

The Polyamide (PA) Segment Dominated the Engineered Polymers Market with 28% of Market Share in 2025

The polyamide (PA) segment dominated the market with the largest share of 28% in 2025, driven by its high-utility resins like PA6, PA66, and specialty polyamides that balance mechanical stability and thermal resilience. The industry demand for flame-retardant and glass-reinforced polyamides makes them key for metal replacement in critical environments and electrification. The segment is key to the innovation of renewable polyamides and high-performance polyamides that allow manufacturers to meet durability standards and stringent decarbonization goals.

The polycarbonate (PC) segment held the 16% market share in 2025, due to its optical clarity, dimensional stability, and impact strength to replace glass and metal. As the market shifts towards bio-attribute polycarbonate and optical-grade resins in 5G infrastructure, electrification, and electronic applications to meet demanding sustainability and light-weighting targets. Additionally, PC is valued for its shatter resistance and superior heat deflection.

The PEEK segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 8.5% over the forecast period. It is a key solution for ultra-performance metal replacement due to its ability to provide dimensional stability and mechanical resilience at temperatures exceeding 240 °C. PEEK is key for aerospace, deep-sea energy infrastructure, medical, and transportation sectors. The segment growth is driven by its additive manufacturing innovation and technological integration.

The ABS segment held a 12% market share in 2025 due to its ease fabrication, lustrous finish, and impact resistance. In automotive, electronic housings, and consumer goods, it serves as a durable and cost-effective solution by maintaining heat stability and chemical resistance. Additionally, the increasing industrial demand for structural integrity and aesthetic appeal is boosting the demand for ABS.

The POM segment held 10% market share in 2025, driven by demand for high-precision engineering where POM offers a low coefficient of friction, moisture resistance, and chemical inertness in consumer electronics, medical delivery devices, and automotive fuel systems. The POM expansion is fueled by demand for low-VOC alternatives and high-flow to meet modern health and safety standards.

Form Insights

The Pellets Segment Dominated the Engineered Polymers Market with 46% of Market Share in 2025

The pellets segment dominated the market with the largest share of 46% in 2025, due to its ease of handling, higher processibility and uniformity in precision injection molding, extrusion, and blow molding processes. The pellets like PC, ABS, and polyamide set a standard for metal replacement, miniaturization in 5G electronics, and automotive lightweighting. The shift towards bio-based pellets enables integration of advanced compounding manufacturers to achieve zero process modification.

The resins segment held the 22% market share in 2025, driven by its structural integrity and impact resistance that categorized into high-performance thermosets and thermoplastics. The resins are engineered with specialty additives and dielectric strength essential for industrial-grade components. The segment shift towards chemically recycled resins and sustainable infrastructure to meet decarbonization targets in heavy-duty applications.

The films & sheets segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. Because it offers barrier protection and dimensional stability through specialized polymers like fluoropolymers, polycarbonate, PEEK, and BOPET. Films are key in lithium-ion battery insulation, lightweight glazing, and flexible electronics by maintaining optical purity and surface-critical function. Additionally, films & sheet enables miniaturization and down-gauging through modern multi-layer co-extrusion.

The fibers segment held 14% market share in 2025, serving as a key form that offers structural composites, thermal endurance, and superior protection that transforms specialized polymers into reinforcement fibers. The application sector utilizes engineered polymers like carbon fiber precursors, LCP, and aramids. The demand for high-tensile filaments aligns with 3D printing and weight reduction strategies by providing tensile toughness and abrasion resistance enable growth.

End-Use Industry Insights

The Automotive Segment Dominated the Engineered Polymers Market with 32% of Market Share in 2025

The automotive segment dominated the market with the largest share of 32% in 2025. The growth is driven by the automotive shift towards metal replacement and vehicle lightweighting. Engineers are focused on high-performance polymers for battery housings, interior components, under-the-hood components, and electrical systems. Engineered polymers maintaining strength-to-weight ratio and integrate PCR content to meet decarbonization and passenger safety.

The electrical & electronics segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 7.5% over the forecast period, accelerated by industrial moves towards high-speed 5G connectivity and device miniaturization. Engineered polymers provide superior heat resistance, flame retardancy, signal integrity, and higher dielectric constant for modern semiconductor and smart infrastructure. Rising consumer demand for green electronics enables the adoption of halogen-free and recycled polymers in connectors, housings, and circuit boards.

The industrial segment held the 14% market share in 2025, driven by industrial demand for chemical inertness, superior wear resistance, and durability for heavy-duty machinery components and fluid-handling systems. Engineered polymers are crucial for automated factory systems and corrosion resistance through the integration of Industry 4.0 advancements. Industry sector used PEEK, POM, and UHMWPE that act as a metal replacement in industrial manufacturing infrastructure.

The consumer goods segment held 12% market share in 2025, due to consumer demand for sustainable performance and circularity in engineered polymers. The segment combines aesthetic resilience with industrial-grade durability by utilizing PC, ABS, and polyamides. The engineered polymers are a premium solution for household applications, packaging, sports equipment, and power tools. The segment integrates bio-based feedstock for high-end consumer hardware.

Processing Technology Insights

The Injection Molding Segment Dominated the Engineered Polymers Market with 44% of Market Share in 2025

The injection molding segment dominated the market with the largest share of 44% in 2025. It is a key processing technology represent the optimization for high-precision and mass-scale production. Its leadership is accelerated by its structural uniformity and tight tolerance and integration of functional additives and reinforcing fibers for automotive, medical, and electronics sectors. The injection molding is key for ABS, Polyamide, and PC into near-net-shape components.

The extrusion segment held the 26% market share in 2025. This technology offers axial strength and surface stability by optimizing production lines for industrial conduits, medical-grade tubing, films, and aerospace cable insulation. By combining advanced multi-layer co-extrusion with extrusion enable moisture and thermal protection for high-stress fluid handling systems by ensuring higher material utility and precision.

The compression molding segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period, represent for key catalyst for the processing of fiber-reinforced composite and ultra-high-performance polymers. Compression molding offers lower material degradation, structural density, and superior dimensional accuracy. This technology is suitable for thermosetting epoxies, PEEK, and PTFE for metal replacement in heavy-duty applications.

The blow molding segment held the 12% market share in 2025, known for the transformation of engineered polymers into high-integrity vessels for automotive and industrial sectors. Blow molding creates a high-performance hollow component and leak-proof structure by maintaining impact resistance and a chemical barrier. Additionally, this process leverages 3D suction and provides uniform wall distribution in industrial reservoirs.

Regional Insights

How Did the Asia Pacific Dominated the Engineered Polymers Market in 2025?

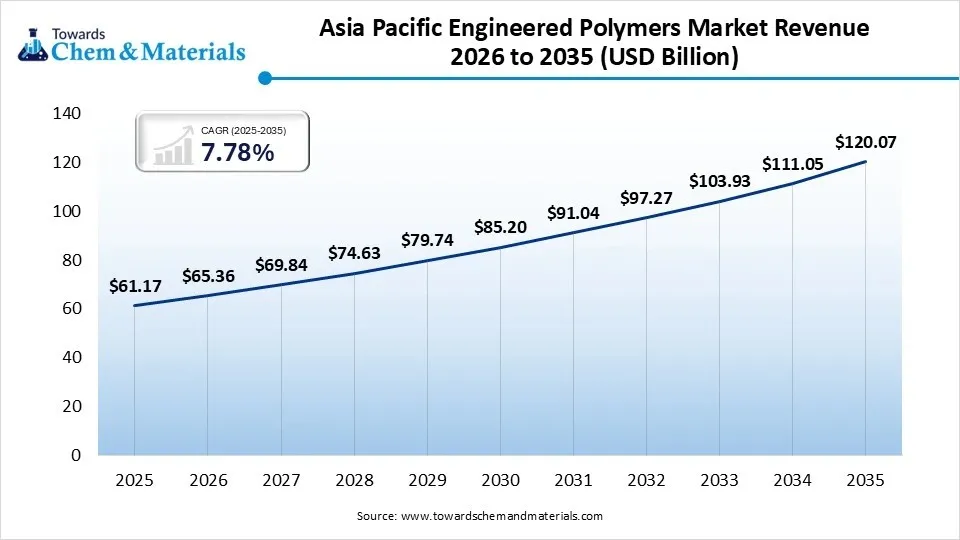

The Asia Pacific Engineered Polymers market size was estimated at USD 61.17 billion in 2025 and is projected to reach USD 120.07 billion by 2035, growing at a CAGR of 7.78% from 2026 to 2035.Asia Pacific dominated the market by holding 42% share in 2025 and is expected to grow at the fastest with a CAGR of 7.5% during the forecast period. The regional expansion is driven by emphasise for industrial automation and infrastructural advancement. The domestic players focus on the sustainable sourcing of bio-based polymers and specialty resins in the automotive and electronics sectors. Asia Pacific government initiatives for the circular economy and strict environmental regulation are fueling the opportunity for material innovation and advanced polymer engineering.

")

China Engineered Polymers Market Growth Trends

China market is defined by the rapid shift towards electrification and rollout of advanced 5G infrastructure, where China serves as a high-end innovation hub. The domestic leaders focus on achieving vertical integration in industrial solutions. The regional strategic shift towards the decarbonization initiative and the circular polymer ecosystem is strengthening its presence in the market through sustainable engineered polymer chemistry.

North America Engineered Polymers Market Growth Trends

North America held the 21% market share in 2025 and is expected to experience notable growth in the market with a 6.20% CAGR during the forecast period, due to its manufacturing hub for specialty polymers and next-generation additives through technological integration. The regional industry focuses on aerospace lightweighting, high-tech semiconductor fabrication, electrification, and defense-grade reliability. North America dominates in molecular recycling and bio-based feedstock to meet stringent corporate ESG targets.

U.S. Engineered Polymers Market Growth Trends

The United States market is known for its defense-grade resilience and technological precision. The region focuses on aerospace and medical innovation through bio-based feedstock and molecular recycling practices. U.S. surge for localized EV battery supply chain and capacity expansion in industrial sectors is fueling the domestic expansion.

Recent Developments

- In April 2026, Dow and RDM Group announced the launch of Multiboard CirculaRR as an innovative fibre-based food packaging solution that is made with recycled fibres and recycled plastic. The innovative solution advances circularity in food packaging, such as frozen food and dry pet food.(Source: corporate.dow.com )

- In April 2026, Michelin inaugurated PolMixLab, the joint laboratory that focuses on innovation of next-generation sustainable polymers. The associated research laboratory focuses on high-performance polymers and rubber of the future for industrial applications.(Source: rubberworld.com)

- In October 2025, Mitsui Chemicals and Polyplastics announced a strategic collaboration aimed at enhancing the engineering plastic product customer network and marketing operation. The high-performance engineering plastics, especially ARLEN® and AURUM®, are developed and sold by Mitsui Chemicals through contract.(Source: jp.mitsuichemicals.com)

Top Companies in the Engineered Polymers Market

- Grand Pacific Petrochemical Corporation

- Mitsubishi Engineering-Plastics Corporation

- Wittenburg Group

- BASF SE

- Asahi Kasei Corporation

- SABIC

- DuPont

- LG Chem

- Toray

- Covestro AG

- Piper Plastics Corp.

- Chevron Phillips Chemical Company LLC

- Daicel Corporation

- Evonik Industries AG

- Eastman Chemical Company

- Ascend Performance Materials

- Lanxess

- Celanese Corporation

- Ravago

- Teknor Apex

- Trinseo LLC

- Polyplastics Co., Ltd.

- Ngai Hong Kong Company Ltd.

- Ginar Technology Co., Ltd.

Segment Covered in the Report

By Type

- Polyamide (PA)

- PA6

- PA66

- Specialty Polyamides (PA11, PA12)

- Polycarbonate (PC)

- Polyoxymethylene (POM)

- Polybutylene Terephthalate (PBT)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyether Ether Ketone (PEEK)

- Fluoropolymers

- PTFE

- PVDF

- Others

- PPS

- LCP

- PSU

By Form

- Pellets

- Fibers

- Films & Sheets

- Resins

By End-Use Industry

- Automotive

- Interior Components

- Under-the-hood

- Electrical Systems

- Electrical & Electronics

- Connectors

- Circuit Boards

- Housings

- Industrial

- Machinery Components

- Pipes & Fittings

- Consumer Goods

- Appliances

- Packaging

- Medical

- Devices

- Implants

- Aerospace

- Others

By Processing Technology

- Injection Molding

- Extrusion

- Blow Molding

- Compression Molding

- Others

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)