Content

What is the Emulsion Polymer Market Size and Share?

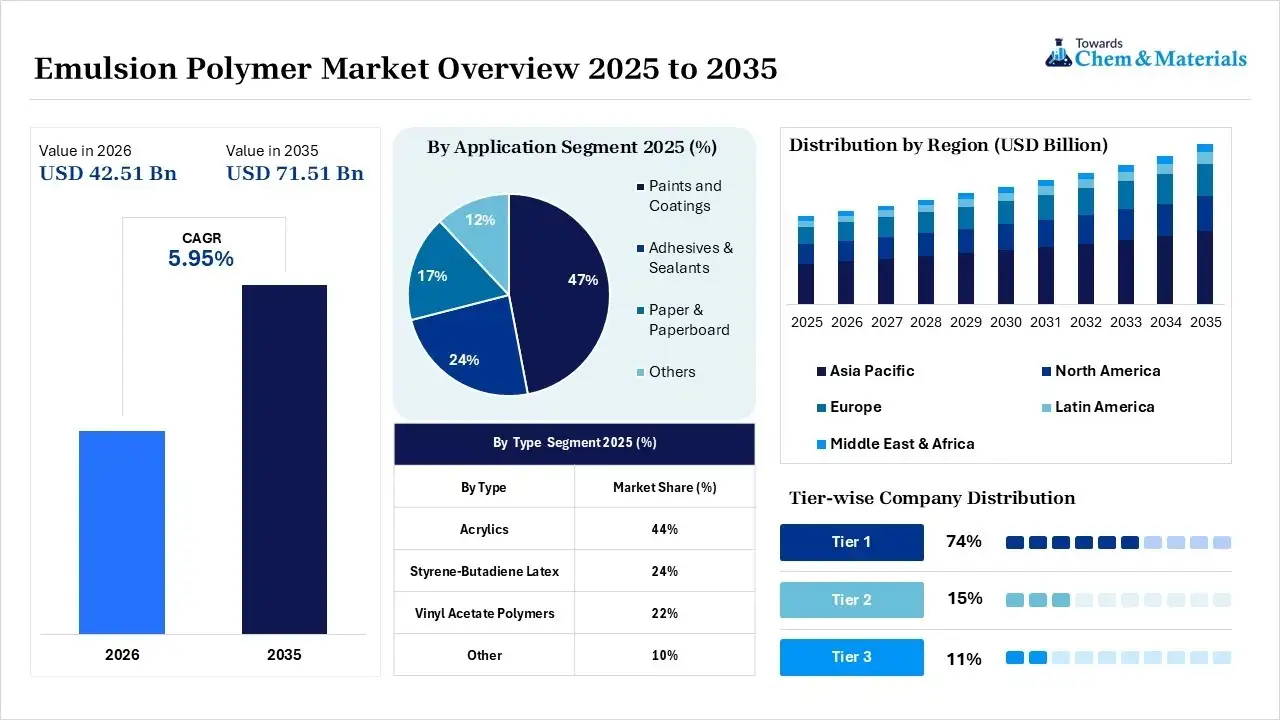

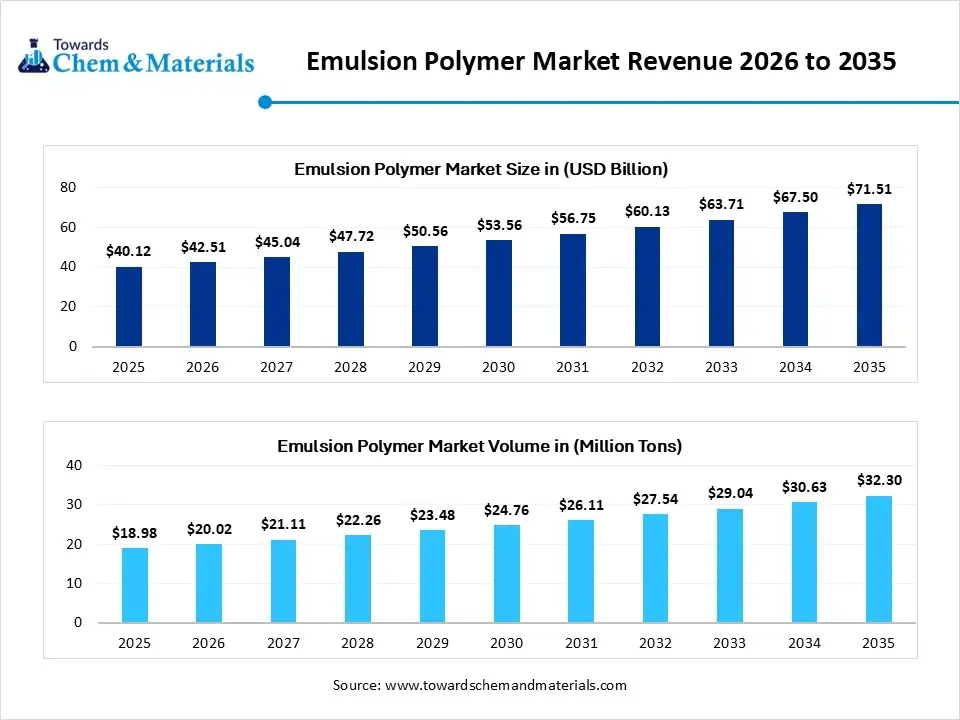

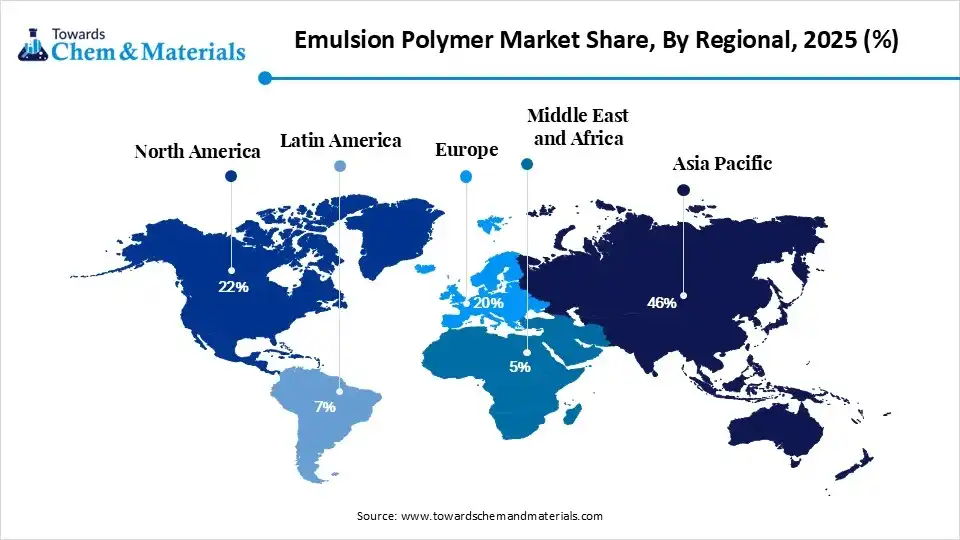

The emulsion polymer market size was valued at USD 40.12 billion in 2025, is estimated to reach USD 42.51billion in 2026, and is projected to reach USD 71.51billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the emulsion polymer market market with the largest revenue share of 46% in 2025 and is expected to grow at the fastest CAGR of 6.06% during the forecast period. In terms of volume, the emulsion polymer market is projected to grow from 18.98 million tons in 2025 to 32.30 million tons by 2035. growing at a CAGR of 5.46% from 2026 to 2035. The construction industry has been leading the emulsion polymer industry, while manufacturers are increasing by releasing innovative and sustainable coatings, paints, and adhesives. Also, the tailored solution is expected to create its own industry presence during the projected time period.

Market Highlights

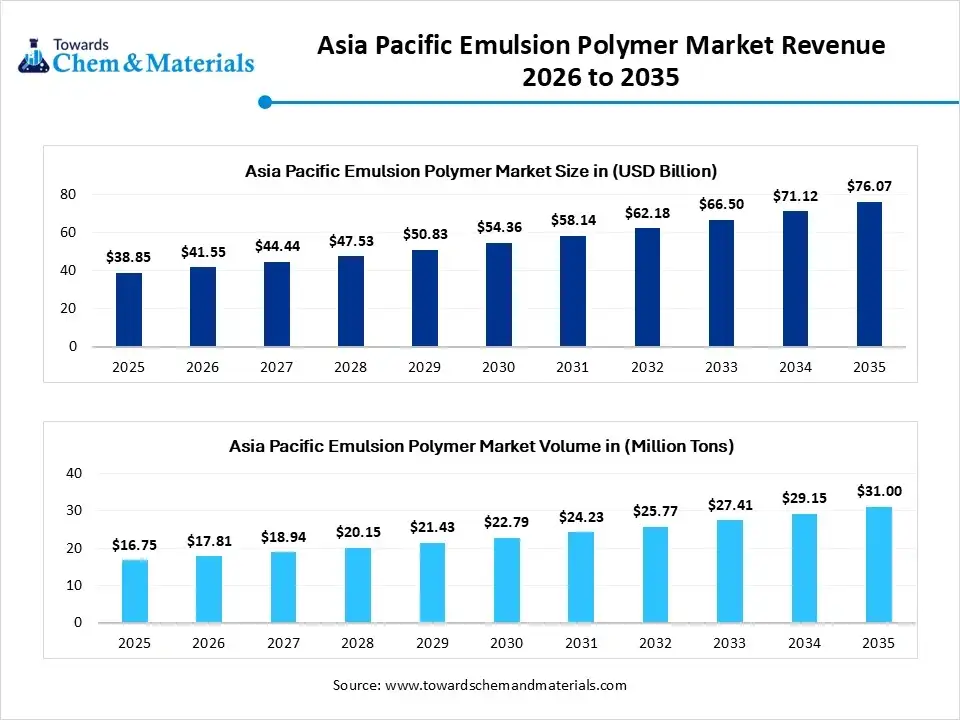

- By region, Asia Pacific dominated the market with a share of 46% in 2025, due to its combination of large-scale manufacturing, rapid urban development, and strong demand from construction, paints, packaging, textiles, and automotive industries.

- By region, North America held 22% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.8% in the forecast period, owing to as industries increasingly adopt sustainable manufacturing practices and high-performance materials.

- By type, the acrylics segment dominated the market with 44% share in 2025, as it offers an excellent balance of durability, weather resistance, flexibility, and long-term performance.

- By type, the vinyl acetate polymers segment held a 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.40% in the forecast period, owing to increasing use in cost-effective adhesives, construction materials, paper coatings, and packaging products.

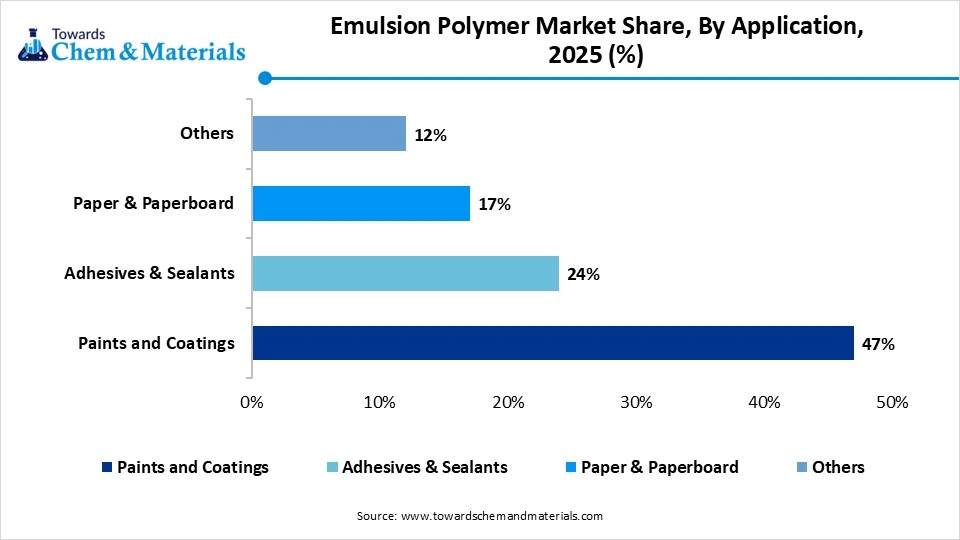

- By application, the paints and coatings segment dominated the market with 47% share in 2025, owing to emulsion polymers being essential for producing high-quality water-based coatings with excellent durability and appearance.

- By application, the adhesives & sealants segment held a 24% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.6% in the forecast period, owing to industries increasingly requiring lightweight, durable, and environmentally friendly bonding solutions.

- By end use, the building & construction segment dominated the market with 42% share in 2025, owing to emulsion polymers being widely used in architectural paints, waterproof coatings, flooring, roofing systems, cement modification, and insulation materials.

- By end use, the textiles & coatings segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.5% in the forecast period, owing to as manufacturers increasingly adopting emulsion polymers to improve fabric quality, durability, softness, wrinkle resistance, and protective finishes.

With the processing of heavy construction activities and a greater shift towards innovative coatings are acting as the primary industry leaders in the emulsion polymer industry in recent years. Also, the global implementations of sustainability and lower-emission coating promotions have been creating profitable avenues in the industry, where the manufacturers and producers are shifting from solvent-based manufacturing initiatives to water-based solutions quickly as global standards change and their regional applications nowadays.

- For instance, in April 2026, Nouryon introduced the latest technology that helps manufacturers produce water-based architectural paints that can withstand global low-emission paint demand, as per the company's claim. Also, the newly launched technology is known as the Alcosperse® OTA 100. (Source: www.nouryon.com)

Consumers are seeking durable, flexible, and environmentally friendly materials, which presents innovative business ideas for producers and manufacturers in the past few years. Later, initiatives like green buildings, tougher yet low-cost, and more easy handling material has strengthened industry potential. Furthermore, the automotive and advanced packaging sectors are main business diversions after the construction sector for the emulsion polymer owners.

Global Investment Flow for the Emulsion Polymer Market 2026

Leading companies are investing in new production plants, expanding existing manufacturing facilities, and creating partnerships and acquisitions to meet rising global demand, while these investments help companies improve supply reliability, shorten delivery times, and strengthen their presence in high-growth markets.

Many manufacturers are allocating more funding toward cleaner production methods and energy-efficient manufacturing processes. They are also investing in technologies that reduce emissions, improve resource efficiency, and support the production of environmentally responsible emulsion polymers.

- For Instance, in February 2026, Konishi completed the attainment of the spinoff from Mitsubishi. Also, the main motive of this acquisition is to strengthen the foundation of Konishi's acrylic emulsion business with a medium-term management plan as per the published report.(Source: www.indianchemicalnews.com)

- For instance, in February 2026, Dencoat unveiled its latest product line of waterproofing membranes. Also, the newly launched product is named Dencoat DPM and is specifically designed for residential, industrial, and commercial applications as per the company's claim.(Source: dencoat.com)

- Also, the investments are helping companies prepare for stricter environmental regulations while improving long-term competitiveness as per the latest survey.

Emulsion Polymer Market Trends

- The shift towards low-VOC and water-based products has driven the strategic transformation and sectoral scalability in the current period. Also, several major producers are actively investing in their R&D activities go produce environmentally friendly paints and coatings.

- The greater focused towards the high performance has allowed stakeholders to capitalize on growth opportunities in the current period. Moreover, industries such as automotive, packaging, and textiles are seen in demand for tailored or customized solutions according to their needs nowadays.

- The heavy demand in the infrastructure and construction projects is likely to strengthen the foundation for the future sector growth. Also, these materials have been observed to have greater usage in waterproof coating, decorative paints, and adhesives in recent years, which follows the industry sales lead.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 42.51Billion/ 20.02Million Tons |

| Expected Size in 2035 | USD 71.51 Billion/ 32.30Million Tons |

| Growth Rate | CAGR of 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Application, By End-use, By Region |

| Key Companies Profiled | Dow Chemical Company, Wacker Chemie AG, Synthomer plc, DIC Corporation, Trinseo PLC, Lubrizol Corporation, Organik Kimya |

Innovation Transforming Emulsion Polymer Production

The industry is actively moving toward smarter, cleaner, and more efficient production technologies. Instead of focusing only on increasing production volumes, manufacturers are improving the quality and sustainability of their products. Also, modern polymerization techniques allow companies to develop polymers with better durability, stronger adhesion, and improved weather resistance while using less energy during manufacturing. Furthermore, digital monitoring systems are helping manufacturers maintain consistent product quality and reduce production waste

Supply Chain Analysis of the Emulsion Polymer Market

- Production & Processing:Manufacturing emulsion polymers looks like blending a specialized chemical milk. Factories whip raw monomers into water using liquid soap to create billions of microscopic droplets, then add a starter chemical to kick off the reaction.

- This quickly bonds the liquids into a smooth, stable fluid used for everyday water-based paints and glues.

Celanese Corporation: Celanese Corporation is an absolute heavyweight in the emulsion polymer market, operating massive chemical manufacturing sites worldwide.- Key players: Celanese Corporation, BASF, The Dow Chemical Company, Arkema, and Synthomer

- Quality Testing and Certification:Testing emulsion polymers means confirming the milky fluid stays perfectly smooth and never separates on shelves.

- Labs spin samples at extreme speeds, check the precise size of the plastic droplets, and measure exactly how well the liquid sticks to surfaces. Passing these trials ensures the batch won't clump up inside commercial paint cans or glue bottles.

- BASF: BASF is a premier chemical powerhouse that runs strict quality control setups at its global production plants.

- Key agencies: Synthomer, Wacker Chemie, Trinseo, and Lubrizol Corporation

- Distribution to Industrial Users:Shipping emulsion polymers requires specialized, climate-controlled tanker trucks and sealed drums to stop the milky liquid from freezing or skinning over.

- Logistics teams map out rapid, direct routes to manufacturing plants to prevent the blended fluid from settling over time. This keeps bulk chemical batches completely fresh and stable for factory production lines.

- Univar Solutions: Univar Solutions is a premier global chemical distributor managing a massive, specialized logistics network.

- Key players: The Dow Chemical Company, Arkema, and Synthomer

Emulsion Polymer Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | U.S. Environmental Protection Agency (EPA) | TSCA Health & Safety Reporting Rules (40 CFR Part 712/716): Enforces strict data-gathering requirements on chemical feedstocks. | Monomer Reporting & Transparency: Compliance heavily stresses tracking and recording residual unreacted monomers. |

| Europe | European Chemicals Agency (ECHA) | EU REACH Regulation (EC No 1907/2006): Annex XVII, Entry 78 (amended under Commission Regulation (EU) 2026/1168) strictly regulates Synthetic Polymer Microparticles (SPMs). | Microplastics Restrictions & Annual Reporting: Waterborne polymer emulsions often fall under Synthetic Polymer Microparticles (SPMs). |

| China | State Administration for Market Regulation (SAMR) | GB 30981.1-2025: Limit of Harmful Substances of Coatings Part 1: Architectural Coatings | Mandatory Maximums: Waterborne emulsion polymers used across architectural walls and consumer goods must hit strict, non-negotiable numerical limits for harmful substances. |

Emulsion Polymer Market Dynamics

Driver

Premium and Eco-friendly Coating Adoption

The increasing demand for environmentally friendly materials across multiple industries has opened profitable avenues for the manufacturers. Also, the water-based emulsion polymers contain lower volatile organic compound (VOC) emissions than solvent-based alternatives, making them a preferred choice for manufacturers. In the current period, industries such as paints and coatings, construction, adhesives, paper, and textiles are adopting these materials to meet environmental regulations while maintaining product quality.

Restraint

Petrochemical Raw Material Volatility

The changing cost of petrochemical-based raw materials is anticipated to hamper the industry flow in the coming years. Prices of important feedstocks such as acrylic monomers, vinyl acetate, and styrene are influenced by crude oil prices, supply chain disruptions, and global economic conditions. These fluctuations increase production costs and make pricing difficult for manufacturers.

Opportunity

Sustainable and Advanced Material Emergence

As industries continue developing advanced and sustainable products is likely to create significant opportunities for the industry participants during the forecast period. Growing investments in green buildings, electric vehicles, flexible packaging, and modern infrastructure are increasing the demand for high-performance polymer solutions. Manufacturers are introducing innovative formulations with better durability, stronger adhesion, and improved weather resistance to meet evolving customer requirements. Furthermore, emerging economies are experiencing rapid industrialization and urbanization, creating new opportunities for paints, coatings, adhesives, textiles, and specialty applications.

Segmental Insights

Type Insights

The Acrylics Segment Dominated the Emulsion Polymer Market with 44% Market Share in 2025

The acrylics segment dominated the market with 44% share in 2025, as it offers an excellent balance of durability, weather resistance, flexibility, and long-term performance. Acrylic emulsion polymers are widely used in decorative paints, industrial coatings, waterproofing products, and construction materials where consistent quality is essential. In recent years, increasing investments in residential and commercial construction have supported demand for acrylic-based products.

") The vinyl acetate polymers segment held a 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.40% in the forecast period, owing to increasing use in cost-effective adhesives, construction materials, paper coatings, and packaging products. Manufacturers are improving product performance while maintaining competitive pricing, making these polymers attractive for large-scale industrial applications. Furthermore, growing investments in infrastructure, furniture manufacturing, flexible packaging, and sustainable construction materials are expected to increase future demand.

The vinyl acetate polymers segment held a 22% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.40% in the forecast period, owing to increasing use in cost-effective adhesives, construction materials, paper coatings, and packaging products. Manufacturers are improving product performance while maintaining competitive pricing, making these polymers attractive for large-scale industrial applications. Furthermore, growing investments in infrastructure, furniture manufacturing, flexible packaging, and sustainable construction materials are expected to increase future demand.

Application Insights

The Paints and Coatings Segment Dominated the Emulsion Polymer Market with 47% Market Share in 2025

The paints and coatings segment dominated the market with 47% share in 2025, owing to emulsion polymers being essential for producing high-quality water-based coatings with excellent durability and appearance. They improve adhesion, flexibility, weather resistance, and color stability while reducing environmental impact. In the current period, rapid construction activities, infrastructure development, and increasing renovation projects have significantly increased the demand for decorative and protective coatings.

") The adhesives & sealants segment held a 24% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.6% in the forecast period, owing to industries increasingly requiring lightweight, durable, and environmentally friendly bonding solutions. Rising demand from packaging, automotive, furniture, electronics, and construction sectors is encouraging manufacturers to adopt advanced water-based adhesive technologies. Furthermore, the expansion of e-commerce and flexible packaging industries is increasing the need for reliable adhesive products that offer strong performance with lower environmental impact.

The adhesives & sealants segment held a 24% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.6% in the forecast period, owing to industries increasingly requiring lightweight, durable, and environmentally friendly bonding solutions. Rising demand from packaging, automotive, furniture, electronics, and construction sectors is encouraging manufacturers to adopt advanced water-based adhesive technologies. Furthermore, the expansion of e-commerce and flexible packaging industries is increasing the need for reliable adhesive products that offer strong performance with lower environmental impact.

End Use Insights

The Building & Construction Segment Dominated the Emulsion Polymer Market with 42% Market Share in 2025

The building & construction segment dominated the market with 42% share in 2025, owing to emulsion polymers are widely used in architectural paints, waterproof coatings, flooring, roofing systems, cement modification, and insulation materials. These products improve durability, flexibility, crack resistance, and long-term structural performance. In recent years, growing investments in residential housing, commercial buildings, and public infrastructure projects have increased the consumption of emulsion polymer-based materials worldwide.

The textiles & coatings segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.5% in the forecast period, owing to as manufacturers increasingly adopting emulsion polymers to improve fabric quality, durability, softness, wrinkle resistance, and protective finishes. Growing consumer demand for functional textiles used in healthcare, sportswear, automotive interiors, and industrial applications is encouraging continuous product innovation. Furthermore, sustainable textile manufacturing practices are increasing the use of water-based polymer technologies that reduce environmental impact while maintaining product performance.

Regional Analysis

How Asia Pacific Dominated the Emulsion Polymer Market in 2025?

The Asia Pacific emulsion polymer market size was estimated at USD 18.46billion in 2025 and is projected to reach USD 33.25billion by 2035, growing at a CAGR of 6.06% from 2026 to 2035. Asia Pacific dominated the market with a share of 46% in 2025, due to its combination of large-scale manufacturing, rapid urban development, and strong demand from construction, paints, packaging, textiles, and automotive industries. Countries across the region continue investing in infrastructure, affordable housing, and industrial expansion, creating steady demand for water-based polymer products. Furthermore, the presence of major raw material suppliers and manufacturing facilities helps companies produce at competitive costs while serving both domestic and export markets.

China

China

The country produces large volumes of paints, coatings, adhesives, packaging materials, and construction products that depend on emulsion polymers, while manufacturers have increased investments in environmentally friendly production technologies to comply with stricter environmental regulations. At the same time, ongoing urban redevelopment, industrial modernization, and expanding exports continue supporting market growth.

Japan

- Rather than competing on production volume alone, the companies in Japan highlight innovation, product reliability, and specialty polymer development for automotive, electronics, construction, and industrial applications. Furthermore, manufacturers continue investing in research to improve product durability, sustainability, and production efficiency.

- The country's strong support for technology development allows local companies to supply premium products to both domestic and international markets.

Emulsion Polymer Market Evaluation in North America

North America held 22% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.8% in the forecast period, owing to as industries increasingly adopting sustainable manufacturing practices and high-performance materials. Growing investments in modern infrastructure, residential renovation, advanced packaging, and industrial coatings are creating new opportunities for emulsion polymer manufacturers. Furthermore, companies across the region continue developing innovative water-based products that meet strict environmental regulations while delivering excellent performance.

United States

The country is actively updating its strong construction, packaging, automotive, and industrial manufacturing sectors. Companies are increasing investments in advanced coating technologies, environmentally friendly adhesives, and high-performance building materials to meet changing customer needs. Furthermore, growing renovation activities, infrastructure improvement projects, and rising demand for sustainable products continue supporting market expansion.

Canada

The country is witnessing growth in the industry as demand increases for sustainable construction materials, protective coatings, and environmentally friendly adhesives. Also, the country's focus on energy-efficient buildings and green infrastructure projects is encouraging greater use of water-based polymer technologies. Furthermore, growth in packaging, wood processing, and industrial manufacturing is creating additional opportunities for emulsion polymer applications.

Europe Emulsion Polymer Industry Conditions

Europe held a 20% market share in 2025, owing to industries rapidly adopting sustainable and high-performance materials. Strict environmental regulations are encouraging manufacturers to replace solvent-based products with water-based emulsion polymers in paints, coatings, adhesives, and construction materials. Furthermore, increasing investments in energy-efficient buildings, infrastructure renovation, and sustainable packaging are creating new business opportunities.

Germany

Germany remains one of the leading countries in the region as its strong chemical industry and advanced manufacturing capabilities, while demand is supported by automotive production, industrial coatings, construction materials, and high-quality adhesives. In recent years, manufacturers have increased investments in sustainable production technologies and innovative polymer formulations that improve product performance while reducing environmental impact.

Italy

The country is experiencing steady growth in the industry, akin to increasing demand from construction, furniture, decorative coatings, textiles, and packaging industries. Also, the country has a strong manufacturing base that relies on high-quality adhesives, protective coatings, and specialty polymer products. Furthermore, renovation projects, infrastructure improvements, and growing interest in environmentally friendly materials are supporting higher consumption of water-based emulsion polymers.

Emulsion Polymer Market Survey in Latin America

Latin America held a 7% market share in 2025, driven by improving industrial activity and rising investments in construction, packaging, and consumer goods manufacturing. Urban development projects and increasing demand for affordable housing are supporting greater use of paints, coatings, and construction chemicals. Furthermore, manufacturers are adopting water-based polymer technologies to improve product quality and comply with evolving environmental standards.

Brazil

Rising investments in residential housing, commercial buildings, and infrastructure projects continue increasing demand for water-based coatings and construction materials in the country nowadays. Furthermore, growth in packaging, furniture manufacturing, and industrial production is creating additional opportunities for emulsion polymer applications. Local manufacturers are also focusing on improving production efficiency and developing sustainable products to meet changing market expectations.

Argentina

The country is witnessing growing demand from construction, packaging, agriculture, and industrial manufacturing sectors. Increasing renovation activities and infrastructure development are encouraging greater use of paints, coatings, adhesives, and waterproofing materials. Furthermore, manufacturers are gradually adopting modern polymer technologies to improve product quality and production efficiency.

Middle East and Africa Emulsion Polymer Sector Observation

The Middle East and Africa held a 5% market share in 2025, as increasing investments in infrastructure, urban development, and industrial diversification. Demand for high-quality paints, coatings, waterproofing materials, and construction chemicals continues rising as governments expand residential, commercial, and transportation projects. Furthermore, manufacturers are introducing water-based polymer technologies to improve sustainability and meet changing environmental expectations.

") Saudi Arabia

Saudi Arabia

Investments in smart cities, residential housing, tourism facilities, and industrial developments are increasing demand for architectural coatings, waterproofing materials, and advanced construction chemicals. Furthermore, the country is encouraging modern manufacturing and sustainable building practices, creating additional opportunities for water-based polymer products in the current period.

South Africa

The country is gradually expanding its industry through increasing demand from construction, mining, packaging, and industrial manufacturing sectors. Also, the infrastructure maintenance, commercial development, and residential construction projects continue supporting the consumption of paints, coatings, and adhesive products. Furthermore, manufacturers are adopting improved production technologies to deliver better-quality and environmentally friendly polymer solutions.

Recent Development

- In December 2025, Organik Kimya has introduced their latest styrene acrylic and acrylic polymer emulsions called as Orgal® Rooflex 35 and others. Also, these polymer emulsions are specifically designed for roof coatings while has the ability to offer greater resistance to weathering and UV, as per the published report.(Source: www.specialchem.com)

- In May 2025, EPS unveiled the latest acrylic emulsion, which is primarily designed for architectural coatings. Also, the newly launched emulsion is known as the EPS 2731, as per the published report, and this emulsion is able to enhance the performance of the architectural coatings, as per the published report.(Source: www.coatingsworld.com)

Competitive Analysis

global industry is moderately consolidated, with a mix of multinational chemical companies and regional manufacturers competing through product innovation, production expansion, and sustainable solutions. Also, rather than competing only on price, leading companies are focusing on developing high-performance water-based polymers that meet changing environmental regulations and customer expectations.

- BASF continues bolstering its position in the emulsion polymer industry by expanding production capacity and enhancing regional supply capabilities. One of the company's recent investments is the expansion of its dispersions production facility in South Africa through an additional production line.

- Arkema is continuing to expand its advanced materials business through its coating solutions segment. In recent years, the company has introduced new waterborne resin technologies designed to improve coating performance while reducing environmental impact.(Source: www.basf.com )

Top Vendors in the Emulsion Polymer Market & Their Offerings:

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Offerings | Key Strength |

| BASF SE | Market Pioneer & Global Tier-1 Leader | Ludwigshafen, Germany | Global footprints across Europe, North America, South America, and a highly expanding footprint in Asia-Pacific. | Acronal® and Joncryl® acrylic and styrene-acrylic waterborne dispersions. | Massive global R&D ecosystem and unparalleled manufacturing scale for architectural coatings and high-performance industrial barriers. |

| Arkema SA | Specialty Materials & High-Value Segment Leader | Colombes, France | Multi-regional presence with strong core operations in Europe and strategic production facility expansions in Asia. | Encor® and Synaqua® water-borne architectural acrylics, alkyd emulsions, and rheology modifiers. | Industry-leading expertise in high-performance eco-friendly coatings designed to comfortably pass hyper-strict global VOC and environmental regulations. |

| Celanese Corporation | Integrated Intermediate & VAE Segment Leader |

Dallas, Texas, United States | Strong Western and Asian Hubs with integrated large-scale chemical infrastructure networks. | EcoVae® vinyl acetate-ethylene (VAE) emulsions alongside premium vinyl-acrylic copolymer systems. | vertical raw-material integration (controlling its own acetyl chain inputs) which protects margins from raw material price volatility. |

Other Key Players

- Dow Chemical Company

- Wacker Chemie AG

- Synthomer plc

- DIC Corporation

- Trinseo PLC

- Lubrizol Corporation

- Organik Kimya

Segments Covered in the Report

By Type

- Acrylics

- Pure Acrylic Emulsions

- Styrene Acrylic Emulsions

- Acrylic Copolymer Emulsions

- Styrene-Butadiene Latex

- Carboxylated SBR Latex

- Non-Carboxylated SBR Latex

- Vinyl Acetate Polymers

- Polyvinyl Acetate (PVAc)

- Vinyl Acetate-Ethylene (VAE)

- Vinyl Acrylic Copolymers

- Other

- Polyurethane Dispersions

- Vinyl Ester Polymers

- Specialty Emulsion Polymers

By Application

- Paints and Coatings

- Architectural Paints

- Industrial Coatings

- Protective Coatings

- Decorative Coatings

- Adhesives & Sealants

- Construction Adhesives

- Packaging Adhesives

- Pressure Sensitive Adhesives

- Sealants

- Paper & Paperboard

- Paper Coating

- Paper Binding

- Packaging Paper

- Others

- Textile Finishing

- Nonwovens

- Leather Finishing

- Printing Inks

By End-use

- Building & Construction

- Residential Construction

- Commercial Construction

- Infrastructure

- Automotive

- Interior Components

- Exterior Coatings

- OEM Applications

- Chemicals

- Chemical Processing

- Industrial Manufacturing

- Textile & Coatings

- Textile Finishing

- Industrial Fabrics

- Protective Textiles

- Others

- Packaging

- Consumer Goods

- Furniture

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Tags

FAQ's

Select User License to Buy

Figures (6)