Content

What is the Current Tire Pyrolysis Products Market Size and Share?

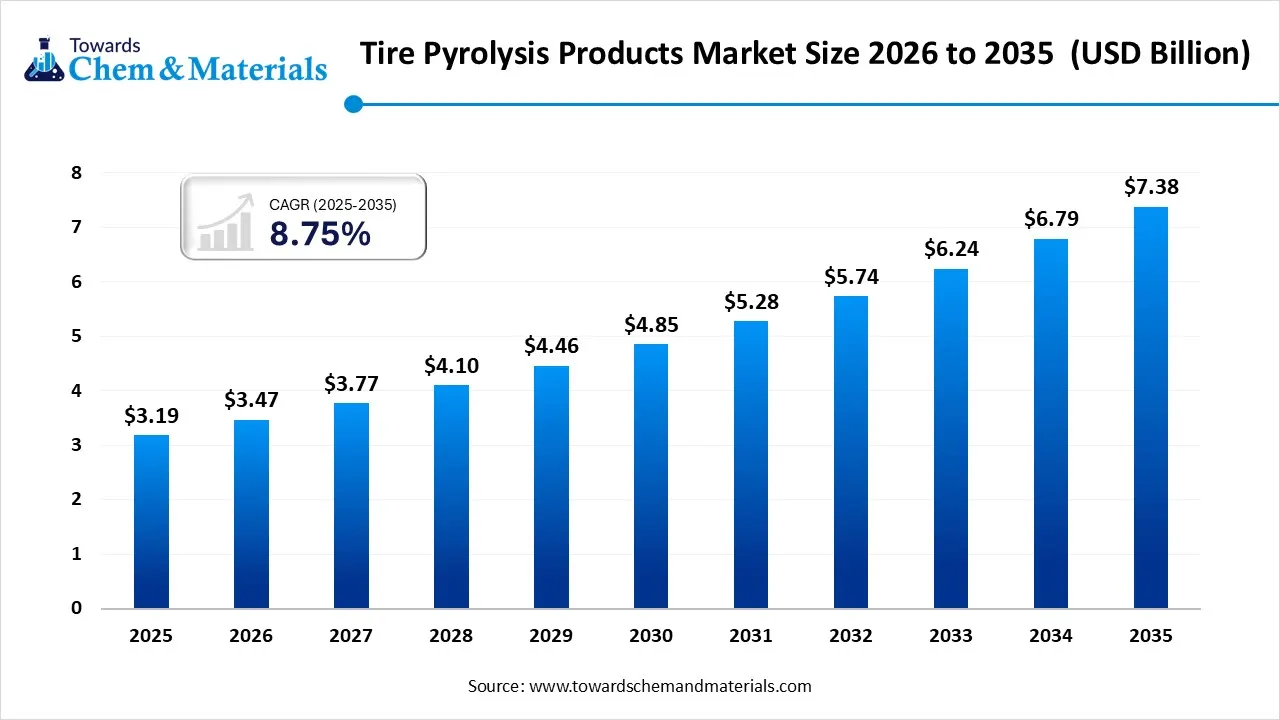

The global tire pyrolysis products market size was estimated at USD 3.19 billion in 2025 and is expected to increase from USD 3.47 billion in 2026 to USD 7.38 billion by 2035, growing at a CAGR of 8.75% from 2026 to 2035. Asia Pacific dominated the tire pyrolysis products market with the largest revenue share of 44% in 2025. The market is driven by circular economy principles, technological advancement, regulatory incentives and rising industrial demand.

")

Tire pyrolysis products are sustainable and high-value raw materials serving as replacements for virgin materials in tire and plastics manufacturing and advanced chemical recycling by conversion of waste into high-quality materials. Through thermal decomposition in oxygen-free environments, complex tires are fragmented down into secondary raw materials, offering low-carbon alternatives.

As the industry transitions from high-volume disposal to value-added manufacturing, with advancement like de-mineralization and distillation enable these products to meet demanding regulatory standards. Overall, these products serve as sustainable substitutes for crude oil and traditional supply chains from fossil fuel market volatility, aligning recycling and decarbonisation infrastructure.

Market Highlights

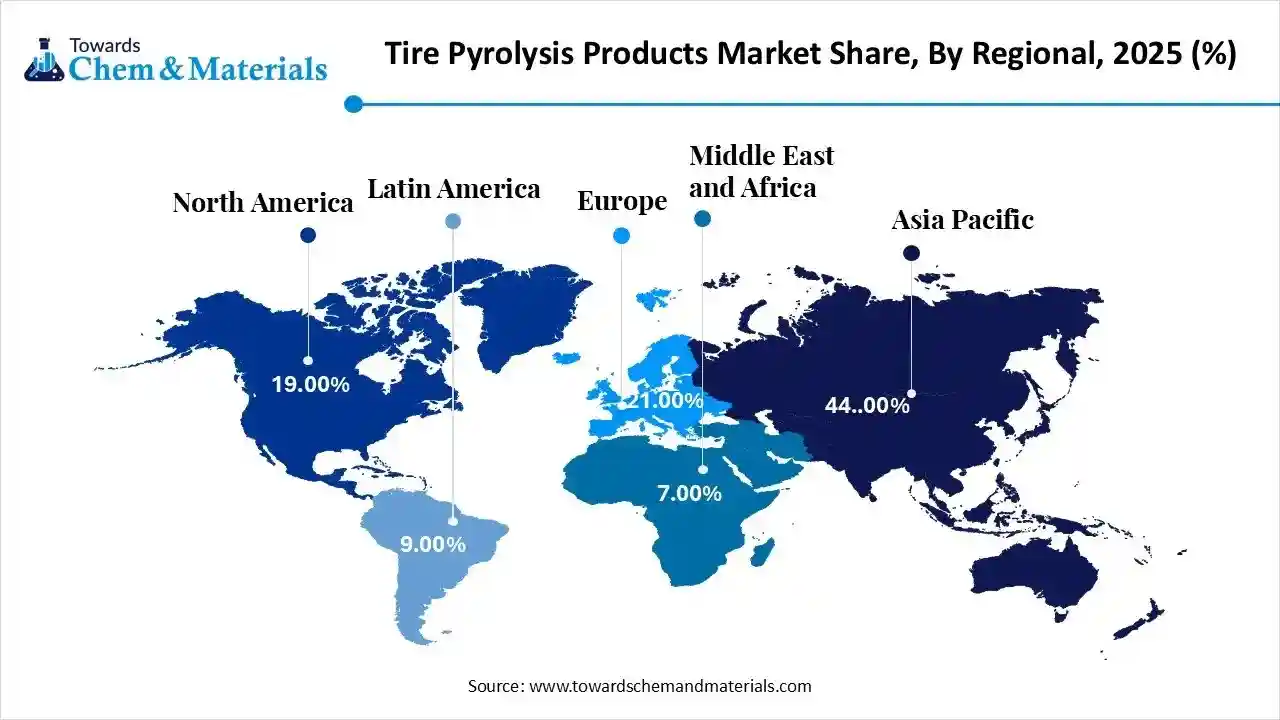

- The Asia-Pacific dominated the tire pyrolysis products market with the largest revenue share of 44% in 2025.

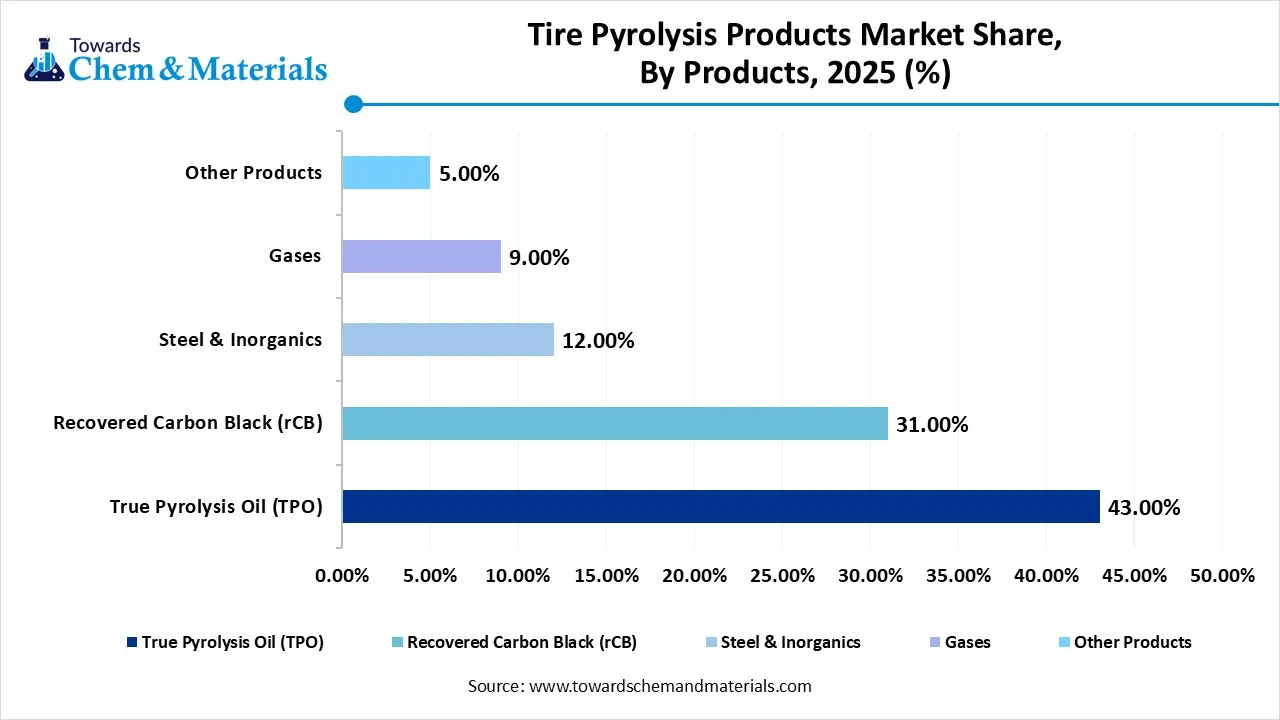

- By product, the true pyrolysis oil (TPO) segment dominated the market and accounted for the largest revenue share of 43.00% in 2025.

- By product, the recovered carbon black segment is expected to grow at the fastest CAGR of 11.85% from 2026 to 2035 in terms of revenue.

- By End-Use, the automotive segment led the market with the largest revenue share of 49.00% in 2025.

- By end use, chemical manufacturing segment is expected to grow at the fastest CAGR of 13.95% from 2025 to 2035 in terms of revenue.

Tire Pyrolysis Products Market Trends

- Stringent Regulatory Framework: The rising environmental concern pushing manufacturers to adopt the restrictive standards involves landfill bans, incentives for eco-friendly recycling and extended producer responsibility laws.

- Industrial Focus Towards Decarbonization: Market players are investing in low-carbon production technologies, such as electrified cracking and carbon capture, prioritizing the market with low-carbon content products.

- Government Initiatives and relationship: The government supports and invests in advanced recycling technologies to increase product longevity. The collaboration between producers, recyclers, consumer brands, and waste management companies is enabling market growth

- Extended Producer Responsibility (EPR): The robust EPR frameworks are shifting the operational responsibility of post-consumer waste management to producers, supporting investment in recycling infrastructure.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 3.47 Billion |

| Revenue Forecast in 2035 | USD 7.38 Billion |

| Growth Rate | CAGR 8.75% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product, By End Use, By Region |

| Key companies profiled | Bolder Industries, Pyrum Innovations, Neste, LD Carbon, BASF SE, Pryolyx, Klean Industries, Bridgestone, Metso, Bioenergy AE Cote-Nord, Green Fuel Nordic Oy, New Hope Energy, Marubeni Corporation, Contec S.A., Revolve Carbon Materials |

Key Technological Shifts and AI in the Tire Pyrolysis Products Market

The integration of AI and advanced engineering is revolutionising tire pyrolysis into precision-driven chemical manufacturing. The smart system utilized industrial Internet of Things sensors monitor gas emission and smart thermal control, using data-driven algorithms to maintain consistent molecular breakdown.

The AI-driven sorting aligns with continuous pyrolysis technology enhance feedstock purity. The digital twin technology simulates processes to optimise efficiency and predict maintenance for lower downtime, while Machine Learning minimises emissions and improves recovery, bridging waste management with scalable and next-generation circular economy solutions.

Tire Pyrolysis Products Market: Value Chain Analysis

Feedstock Procurement:

- The stage focuses on mechanical deconstruction include the collection, sorting and initial extraction of steel wire and shredding tires as chemical feedstock.

- Key Players: Murfitts Industries, Rueda Verde, Ecopneus, Genan and Liberty Tire Recycling

Pyrolysis Conversion and Technology Integration:

- The stage of pre-processed tire waste into thermochemical decomposition of rubber polymers in an oxygen-free environment by integration of AI-driven process control and automation.

- Key Players: Pyrum Innovation, Niutech Environment Technology, Beston Group, Klean Industries and Scandinavian

Enviro Systems AB

- Advanced Refining and Circular Application: The stage of upgrading raw pyrolysis output into industrial-grade circular feedstock and sustainable fuels using technological advancement into recovered carbon black to meet strict performance standards.

Key Players: Black Bear Carbon, Bolder Industries, Neste, Bridgestone Corporation and BASF SE

Regulatory Framework: Tire Pyrolysis Products Market

| Region | Regulation | Regulatory Focus |

| Regulatory Focus | Circular Economy Action Plan, ELV Regulations | The focus on CO2 reduction and high-value material recovery of pyrolysis products. |

| North America | State-level Waste Management and Recycling Laws | Standards for reclassification of thermochemical processes, ensuring pyrolysis manufacturing with exposure limit and solid waste disposal. |

| Asia Pacific | CPCB, EPR for Waste Tires, National Energy Consumption Standards | Focus on formalization of the recycling sector to ensure domestic tire waste and limit carbon black, mandates for tire production and energy consumption. |

Segmental Insights

Product Insights

Why the True Pyrolysis Oil (TPO) Segment Dominates the Tire Pyrolysis Products Market?

The true pyrolysis oil (TPO) segment dominated the market in 2025 accounting for 43.00% of total revenue. True Pyrolysis Oil (TPO) is the liquid fuel obtained from the thermal decomposition of waste tires in the absence of oxygen during the tire pyrolysis process. It typically accounts for about 40–50% of the total output and contains a complex mixture of hydrocarbons, including aromatics, paraffins, and olefins. It can also be used as a chemical feedstock because it contains valuable compounds like benzene, toluene, xylene, and limonene, which are useful in the production of solvents, resins, and other petrochemical products.

")

The recovered carbon black segment is anticipated to grow at the fastest CAGR of 11.85% during the forecast period. It is known as a high-value reinforcing agent and an eco-friendly alternative to traditional carbon black. It acts as a high-performance additive that supports decarbonization with a lower carbon footprint. It enables tire and rubber manufacturers to meet recycled-content goals without sacrificing robustness and quality. The technologically advanced processes have transformed raw char into a high-purity, technical-grade product that boosts its demand. As a result, automotive and industrial supply chains see it as a stable green product and secondary raw material, offering a sustainable way to reduce dependence on fossil fuels.

Tire Pyrolysis Products Market Share, By Products, 2025 (%)

| Product Type | Revenue Share, 2025 (%) |

| True Pyrolysis Oil (TPO) | 43.00% |

| Recovered Carbon Black (rCB) | 31.00% |

| Steel & Inorganics | 12.00% |

| Gases | 9.00% |

| Other Products | 5.00% |

By End-Use

Which End-use Dominated the Tire Pyrolysis Products Market?

The automotive segment dominated the market in 2025 accounting for 49.00% of total revenue. It is a key catalyst of circularity, shifting from waste producer to consumer of recycled materials like recovered carbon black and pyrolysis oil into automotive components. The development is driven by strong decarbonisation goals and the need to reduce reliance on virgin petrochemicals. Automotive manufacturers use these derivatives as engineered green commodities meeting rigorous safety and performance standards. The industrial strategic partnership focuses on standardizing materials and creating closed-loop supply chains that convert waste into high-performance automotive components, driving market expansion.

The chemical manufacturing segment is expected to grow at the fastest CAGR of 13.95% from 2026 to 2035. Defined as a high-value and advanced end-user segment for refined pyrolysis outputs. It shifts toward circular feedstocks, using tire pyrolysis oil as a sustainable alternative to crude liquid and naphtha in producing chemicals, polymers, and synthetic materials, ensuring its growth. Industry pressures to decarbonise and increasing regulatory demands drive demand for these derivatives as a drop-in product for low-carbon. Additionally, the supply chains focused on purification to meet high chemical standards during chemical synthesis make it suitable for bridging the gap between the pyrolysis industry and chemical producers.

Tire Pyrolysis Products Market Share, By End Use, 2025 (%)

| End Use | Revenue Share, 2025 (%) |

| Automotive | 49.00% |

| Industrial | 18.00% |

| Chemical Manufacturing | 11.00% |

| Construction | 9.00% |

| Paints & Coatings | 6.00% |

| Transportation | 4.00% |

| Other End Use | 3.00% |

Regional Insights

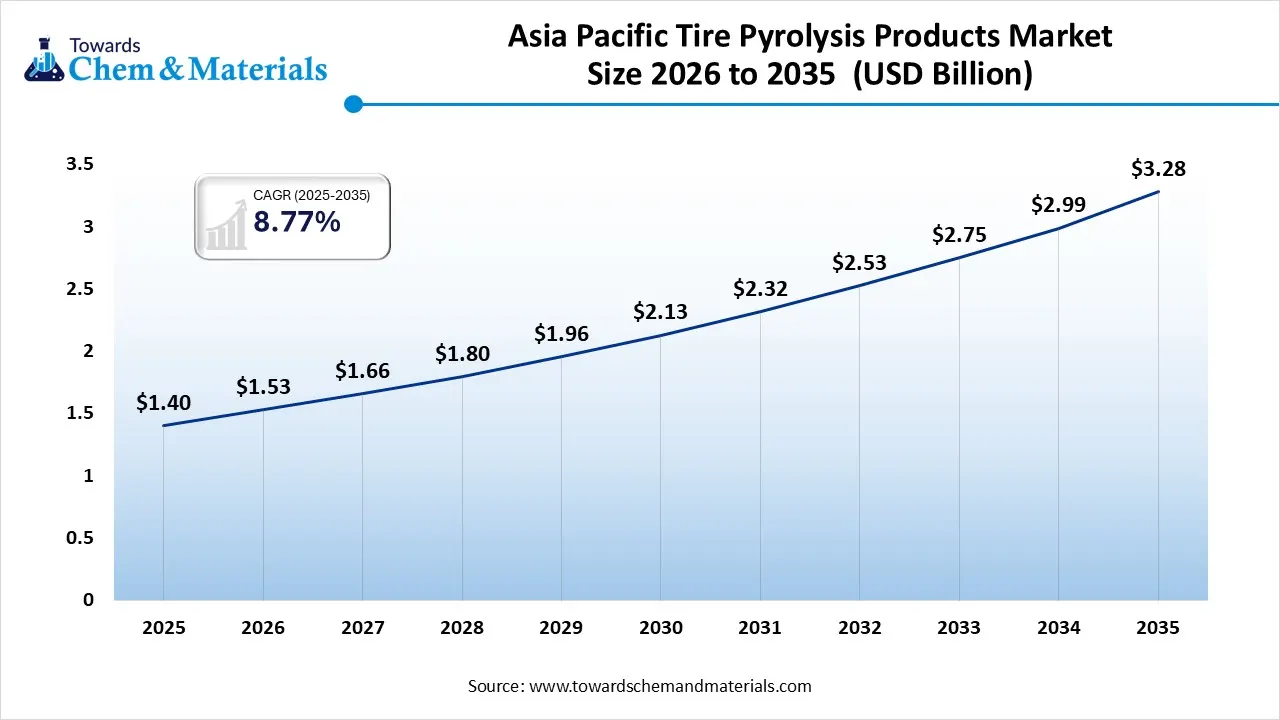

The tire pyrolysis products market size was valued at USD 1.40 billion in 2025 and is expected to be worth around USD 3.28 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 8.77% over the forecast period from 2026 to 2035.

")

Asia Pacific dominated the market in 2025, driven by the transition towards a circular economy and sustainable waste practices. The trend toward continuous pyrolysis technology improves yields, cost-effectiveness and product quality, especially for tire pyrolysis as an eco-friendly alternative to fossil fuels in the steel and cement industries. The region focuses on producing high-grade recovered carbon black, which is used for new tires and rubber products to meet strict environmental goals. Additionally, government regulations and producer responsibility policies discourage landfilling and promote resource recovery from end-of-life tires with sustainable output.

China Tire Pyrolysis Products Market Growth Trends

China leads the Asia Pacific market in processing high-quantity waste tires annually, using continuous pyrolysis systems, which are promoted by national initiatives and carbon neutrality goals. China transitioned from waste disposal to high-value manufacturing, with recovered carbon black utilised in domestic tire production in automated facilities. This growth is reinforced by environmental mandates that are accelerating large-scale, automated plants, making China the groundbreaker in circular rubber technology.

North America is expected to grow at the fastest CAGR in the market during the forecast period, revolutionizing towards industrial-scale circularity, driven by corporate decarbonization efforts. The region is increasingly integrating recovered carbon black into automotive component manufacturing to meet sustainability certifications. Additionally, North America utilized tire pyrolysis oil as chemical feedstocks and sustainable fuels, enabling global investment and supported by regulations and eco-friendly incentives that positioned them as manufacturers of high-quality materials for various industries.

")

U.S. Tire Pyrolysis Products Market Growth Trends

The U.S. market is expanding due to its pyrolysis infrastructure through significant investments from energy firms and private investors. The region is shifting towards decarbonization with strategic partnerships to meet recycled content mandates and reduce emissions. The U.S. surge for conversion of tire pyrolysis products into premium refinery value feedstock for circular plastics and aviation fuels, boosting its global presence in advanced chemical recycling.

Tire Pyrolysis Products Market Share, By Regional, 2025 (%)

| Region | Revenue Share, 2025 (%) |

| Asia Pacific | 44.00% |

| Europe | 21.00% |

| North America | 19.00% |

| Latin America | 9.00% |

| Middle East & Africa | 7.00% |

Europe Tire Pyrolysis Products Market Growth Trends

Europe show significant growth driven by its high-value circularity and stringent EU regulatory framework. The region preferred large industrial clusters co-locating pyrolysis with chemical and tire manufacturing to reduce logistics and securing sustainable supply through off-take agreements. The European government push for pyrolysis oil as a key resource for aviation fuels and plastics, encouraging recycled materials over virgin petrochemicals that strengthen its economic viability and advanced recycling facilities.

Germany Tire Pyrolysis Products Market Growth Trends

Germany is experiencing growth due to its focus on long-term partnerships with engineering firms and automotive innovators that produce high-purity feedstocks and sustainable fuels. The domestic tire manufacturers are rapidly adopting recovered carbon black to meet strict sustainability mandates. Germany emphasizes automated and continuous-feed technology aligns with environmental standards for the transformation of waste management into a high-value process. Germany's growth is supported by the national circular economy mandates.

Recent Developments

- In October 2025, Lummus Technology and InnoVent Renewables announced a strategic partnership to jointly license and deploy InnoVent's proprietary continuous tire pyrolysis technology. The alliance focuses on scalability and the advancement of circular solutions to lower tire waste and reduce environmental impact.(Source: www.lummustechnology.com)

- In May 2025, NEXEN TIRE and LD Carbon signed a long-term supply contract for recovered carbon black for sustainability. The agreement aimed at rCB into global manufacturing chain and to extend its use of environmentally friendly materials.(Source: newsroom.nexentire.com)

Top Companies in the Market and Their Offerings

- Bolder Industries: The global leader that offers sustainable alternatives like recovered carbon black to ensure better dispersion for industrial manufacturers.

- Pyrum Innovations: The technology developers specialise in thermolysis technology offers plant solutions and produce high-quality pyrolysis oil as chemical feedstock.

- Neste: The major leader focuses on chemical recycling of waste, refining tire pyrolysis oil into high-quality fuels and raw materials for the chemical industry.

- LD Carbon: The sustainable material producer that offer refined tire pyrolysis oil and high-purity rCB for a closed-loop supply chain and green feedstock.

- BASF SE: The major chemical manufacturers that purchase pyrolysis oil to use it as circular feedstock to produce new polymers.

- Pryolyx

- Klean Industries

- Bridgestone

- Metso

- Bioenergy AE Cote-Nord

- Green Fuel Nordic Oy

- New Hope Energy

- Marubeni Corporation

- Contec S.A.

- Revolve Carbon Materials

Segment Covered in the Report

By Product

- True Pyrolysis Oil (TPO)

- Recovered Carbon Black (rCB)

- Steel & Inorganics

- Gases

- Other Products

By End Use

- Automotive

- Industrial

- Paints & Coatings

- Chemical Manufacturing

- Construction

- Transportation

- Other End Use

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)