Content

What is the current Long Steel Products market size and share?

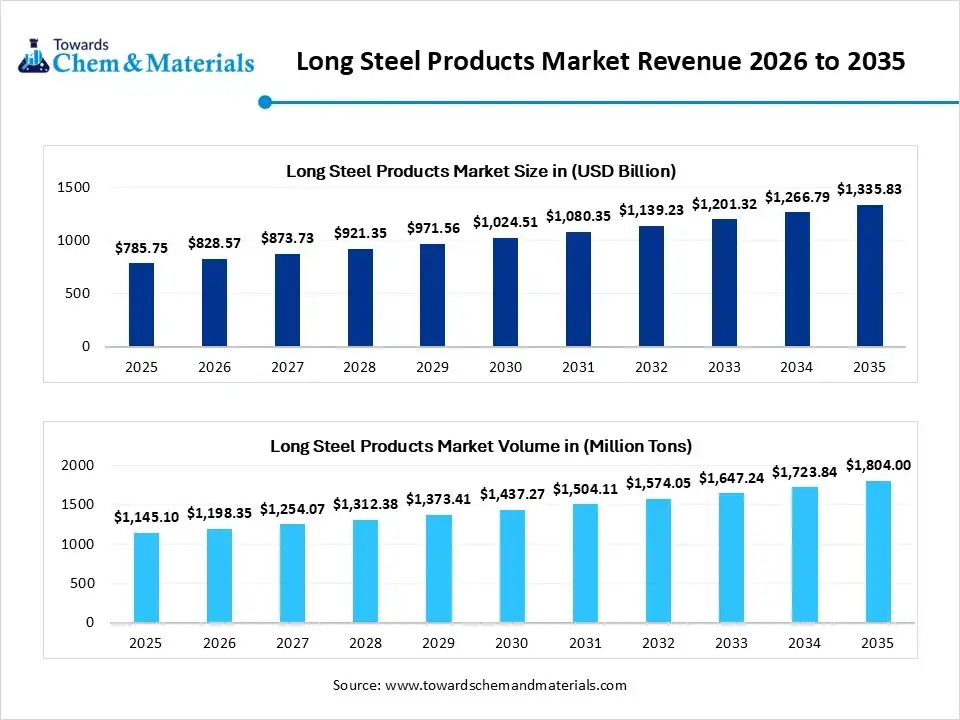

The global long steel products market was valued at USD 785.75 billion in 2025, is estimated to reach USD 828.57 billion in 2026, and is projected to reach USD 1,335.83 billion by 2035, growing at a CAGR of 5.45% from 2026 to 2035. In terms of volume, the long steel products market is projected to grow from 1,145.1 million tons in 2025 to 1,804 million tons by 2035. growing at a CAGR of 4.65% from 2026 to 2035. Long steel products are a type of steel material manufactured using billets and hot rolling. They have high strength and offer ease of fabrication. They are available in an elongated shape and have excellent welding properties. They have structural shape diversity and excellent elasticity. They are classified into types like structural sections, rails, rebar, merchant bars, wire rods, and others. Long steel products are used in producing engine parts, spring manufacturing, window frames, mining projects, residential towers, and developing railway tracks.

Key Takeaways

- By region, Asia Pacific led the market with a 49% share in 2025 and is expected to grow at the fastest rate in the market with a CAGR of 6.40% during the forecast period due to the presence of massive infrastructure projects.

- By region, Europe held the second largest share of 21% in the market in 2025 and expects a notable growth in the market with CAGR of 4.90% during the forecast period, due to the renewable energy investment.

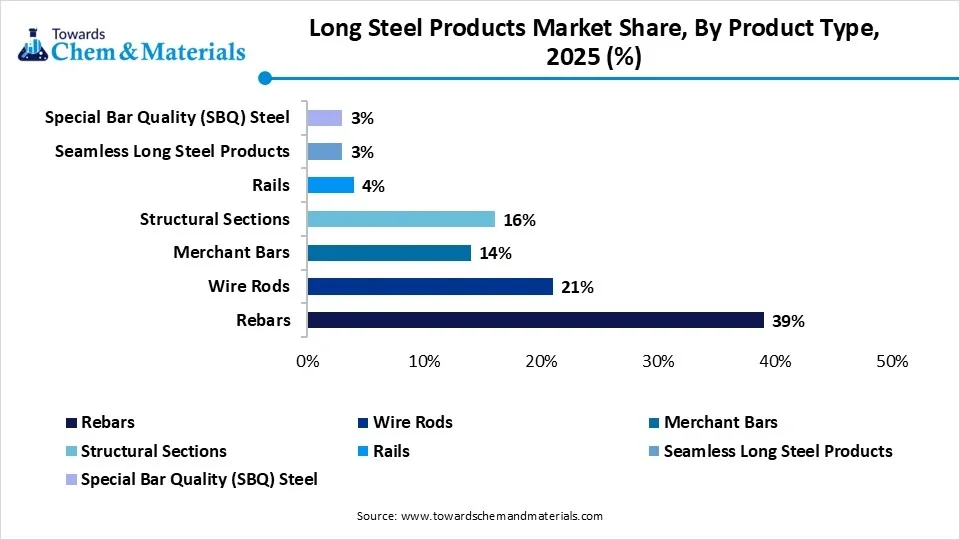

- By product type, the rebars segment led the market with a 39% share in 2025 due to the need in construction projects.

- By product type, the structural sections segment held the 16% market share in 2025 and is expected to grow at the 5.9% CAGR in the market during the forecast period due to the rise in non-residential construction.

- By material type, the carbon steel segment led the market with a 68% share in 2025 due to its versatility in construction activities.

- By material type, the alloy steel segment held the 21% market share in 2025 and is expected to grow at the 5.9% CAGR in the market during the forecast period due to the increased utilization in EVs.

- By manufacturing process, the basic oxygen furnace segment led the market with a 34% share in 2025 due to its high purity levels.

- By manufacturing process, the electric arc furnace segment held the 28% market share in 2025 and is expected to grow at the 6.4% CAGR in the market during the forecast period due to the green steel demand.

- By end-use industry, the construction segment led the market with a 52% share in 2025 due to the rise in repairing aging infrastructure.

- By end-use industry, the energy & power segment held the 10% market share in 2025 and is expected to grow at the 6.1% CAGR in the market during the forecast period due to the strong solar plants.

- By application, the reinforcement segment led the market with a 41% share in 2025 due to the urban expansion.

- By application, the structural support segment held the 24% market share in 2025 and is expected to grow at the 5.9% CAGR in the market during the forecast period due to the expanding industrial warehouses.

- By distribution channel, the direct sales segment led the market with a 46% share in 2025 due to the growing project-based demand.

- By distribution channel, the online procurement platforms segment held the 8% market share in 2025 and is expected to grow at the 7.1% CAGR in the market during the forecast period due to the rise in 24/7 ordering.

- By grade, the mild steel grade segment led the market with a 43% share in 2025 due to the high ductility.

- By grade, the high tensile grade segment held the 27% market share in 2025 and is expected to grow at the 6.2% CAGR in the market during the forecast period due to the development of mega-projects.

At a Glance

- Market Estimated Size (2025): USD 785.75 Billion | CAGR (2026–2035): 5.45%

- Market Projected Size (2035): USD 1,335.83 Billion

- Asia Pacific: largest Market Revenue Share of 49% in 2025.

- Market Estimated Volume (2025): 1,145.10 Million Tons | Volume CAGR (2026–2035): 4.65%

- Market Projected Volume (2035): 1,804.00 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 549 per Ton

- Average Selling Price (2025): USD 739 per Ton

- Pricing CAGR (2025–2035): 3.12%

Long Steel Products Market Trends:

- Growing Renewable Energy Infrastructure:- The rising manufacturing of tidal turbines and the expansion of transmission towers increase the use of long steel products like rebar, rods, and others. The expanding hydropower plants and solar trackers increase the use of long steel products.

- Transition to Green Steel:- The focus on decarbonization and the need to meet net-zero targets increases demand for green steel. The decarbonization mandates in the infrastructure industry increase green steel use.

- Expansion of Industries:- The development of warehouses and the need for various machinery in industries increases the use of long steel products. The expanding production units and growing industrial manufacturing increase the adoption of long steel products.

Key Technological Shifts in Long Steel Products Market:

The long steel products market is experiencing major technological shifts like robotics, 3D printing, digitalization, smart sensors, machine learning, digital twins, and IoT. The technological changes driven by the demand for optimizing efficiency, lowering defects, green production, and decarbonization. The incorporation of artificial intelligence is the prominent change in the market, driven by demand for automating quality control.

AI analyzes surface defects and easily adjusts production parameters. AI optimizes the efficiency of inventory and predicts equipment failures. AI enables high-quality production and supports minimizing carbon emissions. AI supports yield improvements and reduces scrap. AI lowers storage costs and optimizes the routes of transformation. AI efficiently handles hazardous tasks and offers real-time alerts in unsafe conditions. Overall, AI helps to meet consumer expectations and supports better management of resources.

Supply Chain Analysis of the Long Steel Products Market

Feedstock Procurement

The stage acquires feedstocks like sponge iron, ferro alloys, ferrous scrap, billets, steel scrap, merchant billets, pig iron, and fluxes.

- Key Players:- ArcelorMittal, Tata Steel, Steel Dynamics, Inc., Nucor Corporation, JSW Steel, Gerdau S.A.

Chemical Synthesis and Processing

The stage includes steps like primary steelmaking, refining using techniques like desulfurization, de-gassing, & alloying, continuous casting, hot rolling, controlled cooling, and final treatment like heat treatment & surface treatment.

- Key Players:- Nippon Steel Corporation, Nucor Corporation, Jindal Steel & Power, ArcelorMittal, POSCO Holdings, Deluxe Metal Processing Chemicals Ltd.

Quality Testing and Certifications

Quality testing performs tests like the bend test, hardness test, bond strength test, tensile strength test, ultrasonic test, and chemical composition test. Certifications like BIS Certification, CE Marking, Mill Test Certificate, and ISO 9001:2015.

- Key Players:- Bureau Veritas, TUV SUD, SGS, Intertek Group, Element Materials Technology

Regulatory Framework: Long Steel Products Market

| Country | Key Regulations | Regulatory Focus |

| India |

|

Minimizing carbon emissions, protecting local producers, and prioritizing quality standards |

| United States |

|

Decarbonization, ensuring product safety, and energy efficiency |

| China |

|

Low-carbon production, stabilizing supply chains, and high-quality development |

Long Steel Products Market Dynamics

Driver

Surging Infrastructure Drives Market Growth

The focus on enhancing industrial productivity and the extensive government funding increases infrastructure development. The expanding urban mobility projects and the modernization of infrastructure increase the adoption of long steel products. The high government spending on industrial corridors and the growth in commercial infrastructure increase the use of long steel products like structural steel and others.

The construction of dams and the explosion of transportation networks increase demand for long steel products. The focus on longevity of infrastructure and interest in metro systems increases demand for long steel products. The shift to green infrastructure and the development of earthquake-resistant structures increases the use of long steel products. The surging infrastructure is a key driver for the market growth.

Restraints

High Capital Investment Restrains Market Growth

The high upfront expenditures and the high financing costs are a big challenge for the market. The adoption of green technologies and the continuous upgradation of the older plants increase capital investment. The development of integrated manufacturing facilities and the strong technological infrastructure increases the capital investment. The high consumption of electricity and long gestation period increase the capital investment.

The heavy machinery requirement and modern environmental regulations are responsible for high capital investment. The raw materials requirement and the use of sustainable technologies increase the capital investment. The upgradation of manufacturing requires heavy investment. So, the high capital investment is the major restraint for market growth.

Opportunity

Expansion of Warehouses Unlocks Market Opportunity

The e-commerce surge and the modernization of logistics increase demand for the development of warehouses. The rapid construction of warehouses and the need for obstruction-free floors increase the use of long steel products. The utilization of automated racking systems and the focus on modular design in warehouses increases the use of long steel products.

The huge utilization of automated machinery and the development of a strong roof structure increase demand for long steel products. The open floor areas and extensive foundations in modern warehouses increase the adoption of long steel products. The need for cold storage and surging manufacturing activities increases the use of long steel products. The expansion of warehouses creates an opportunity for market growth.

Segmental Insights

Product Type Insights

The Rebars Segment Dominated The Long Steel Products Market In 2025 With A 39% Share

The rebars segment dominated the market with a 39% share in 2025 due to the growing investment in public infrastructures. The concrete structures in construction and the growth in urban areas increase demand for long steel products. The expansion of housing structures and the high concentration of industries increases the use of rebars. The high-strength, commodity nature, excellent mechanical bonding, low cost, and superior seismic performance of rebars drive the segment growth.

The structural sections segment held a share of 16% in the market in 2025 and is expected to grow at the fastest CAGR of 5.9% during the forecast period due to the rise in modular construction. The expansion of airports and the surging green building projects increase the use of structural sections. The expanding urban commercial buildings and the development of industrial infrastructure increase demand for structural sections. The rise in multi-story buildings and growing hospital construction supports the segment growth.

Material Type Insights

The Carbon Steel Segment Dominated The Market In 2025 With A 68% Share

The carbon steel segment dominated the market with a 68% share in 2025 due to its high availability. The development of bridges and the transition to sustainable construction increase demand for carbon steel. The development of the structural framework of constructions and the housing needs increases the use of carbon steel. The high manufacturing efficiency, affordability, recyclability, and high strength of carbon steel drive the segment growth.

Long Steel Products Market Share, By Material Type, 2025 (%)

| By Material Type | Revenue Share, 2025 (%) |

| Carbon Steel | 68% |

| Alloy Steel | 21% |

| Stainless Steel | 11% |

The alloy steel segment held the 21% market share in 2025 and is expected to grow at the fastest CAGR of 5.9% during the forecast period due to the growing demand for durable materials. The increased investment in skyscrapers and the development of engine components increases demand for alloy steel. The use of fuel-efficient vehicles and the rise in modern engineering increase the adoption of alloy steel. The transportation system development and growing industrial machinery use support the segment growth.

Manufacturing Process Insights

The Basic Oxygen Furnace (BOF) Segment Dominated The Market In 2025 With A 34% Share

The basic oxygen furnace (BOF) segment dominated the market with a 34% share in 2025 due to the growing mass production. The rapid processing focus and the availability of low-cost feedstock increase the use of the basic oxygen furnace. The production of cleaner steel and the rising integrated steel making increases the adoption of the basic oxygen furnace. The high productivity, self-sufficient energy, and excellent precision in the basic oxygen furnace drive the segment growth.

Long Steel Products Market Share, By Manufacturing Process, 2025 (%)

| By Manufacturing Process | Revenue Share, 2025 (%) |

| Basic Oxygen Furnace (BOF) | 34% |

| Electric Arc Furnace (EAF) | 28% |

| Induction Furnace | 12% |

| Continuous Casting | 10% |

| Hot Rolling | 11% |

| Thermo-Mechanical Treatment | 5% |

The electric arc furnace (EAF) segment held the 28% market share in 2025 and is expected to grow at the fastest CAGR of 6.4% during the forecast period due to the lowering operating cost. The green steel production and scrap recycling increase the use of the electric arc furnace. The development of diverse steel products and the focus on lowering energy usage increase the use of the electric arc furnace. The high flexibility, lower capital cost, and excellent operational efficiency of the electric arc furnace support segment growth.

End-Use Industry Insights

The Construction Segment Dominated The Market In 2025 With A 52% Share

The construction segment dominated the market with a 52% share in 2025 due to the growing high-rise construction. The expansion of load-bearing applications and the complex architectural designs increases demand for long steel products. The development of commercial buildings and the global investment in rail networks increases demand for long steel products. The growing renovation projects drive the segment growth.

Long Steel Products Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Construction | 52% |

| Automotive | 15% |

| Industrial Manufacturing | 11% |

| Energy & Power | 10% |

| Shipbuilding | 7% |

| Agriculture Equipment | 5% |

The energy & power segment held a share of 10% in the market in 2025 and is expected to grow at the fastest CAGR of 6.1% during the forecast period due to the growing electrification of infrastructure. The development of wind turbine towers and the expansion of smart grids increase demand for long steel products. The expanding metro projects and the rise in green energy use increase the adoption of long steel products. The expanding hydroelectric projects support the segment growth.

Application Insights

The Reinforcement Segment Dominated The Market In 2025 With A 41% Share

The reinforcement segment dominated the market with a 41% share in 2025 due to the growing global construction activities. The focus on building integrity and the need to enhance the structural durability of construction increases demand for long steel products. Investing in metro rail systems and a growth in residential housing drives demand for long steel products. The modern construction projects drive the segment growth.

Long Steel Products Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Reinforcement | 41% |

| Structural Support | 24% |

| Fasteners & Components | 11% |

| Rail Tracks | 6% |

| Wire Products | 10% |

| Machinery Components | 8% |

The structural support segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 5.9% during the forecast period due to the huge need for commercial buildings. The expansion of large-scale projects and lighter foundations enhnace the use of long steel products. The development of solar structures and power plant construction boosts segment growth.

Distribution Channel Insights

The Direct Sales Segment Dominated The Market In 2025 With A 46% Share

The direct sales segment dominated the market with a 46% share in 2025. The growing bulk purchases in large-scale projects and focus on direct contracts increase the adoption of direct sales. The need for consistent quality and supply chain control increases demand for direct sales. The customization of long steel products and focus on building long-term relationships increases demand for direct sales, driving the overall segment growth.

Long Steel Products Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 46% |

| Steel Service Centers | 24% |

| Distributors & Traders | 22% |

| Online Procurement Platforms | 8% |

The online procurement platforms segment held a share of 8% in the market in 2025 and is expected to grow at the fastest CAGR of 7.1% during the forecast period. The easy access to line pricing and transparent supply options increases buying from online procurement platforms. The availability of centralized dashboards and the focus on avoiding shortages increase online buying. Users focus on comparing rates and need to lower intermediate margins, which increases online buying, supporting the segment growth.

Grade Insights

The Mild Steel Grade Segment Dominated The Market In 2025 With A 43% Share

The mild steel grade segment dominated the market with a 43% share in 2025 due to its high weldability. The development of reinforcing bars and the need for high-strength reinforcements increases the use of mild steel grades. The expanding structural applications and the expansion of commercial real estate increase the adoption of mild steel grade. The fencing manufacturing and rising fabrication increase the use of mild steel grade. The excellent versatility, abundant availability, superior fabricability, and high ductility of mild steel grades drive the segment growth.

Long Steel Products Market Share, By Grade, 2025 (%)

| By Grade | Revenue Share, 2025 (%) |

| Mild Steel Grade | 43% |

| High Tensile Grade | 27% |

| Corrosion Resistant Grade | 15% |

| Heat Resistant Grade | 8% |

| Wear Resistant Grade | 7% |

The high tensile grade segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 6.2% during the forecast period. The focus on lowering carbon emissions in construction projects and growth in high-rise construction increases demand for high tensile grade. The focus on minimizing transportation costs and the need to enhance building safety increases the use of high tensile grade. The advanced metallurgy and lightweighting of automotive support the segment growth.

Regional Insights

Why Asia Pacific Dominated the Long Steel Products Market?

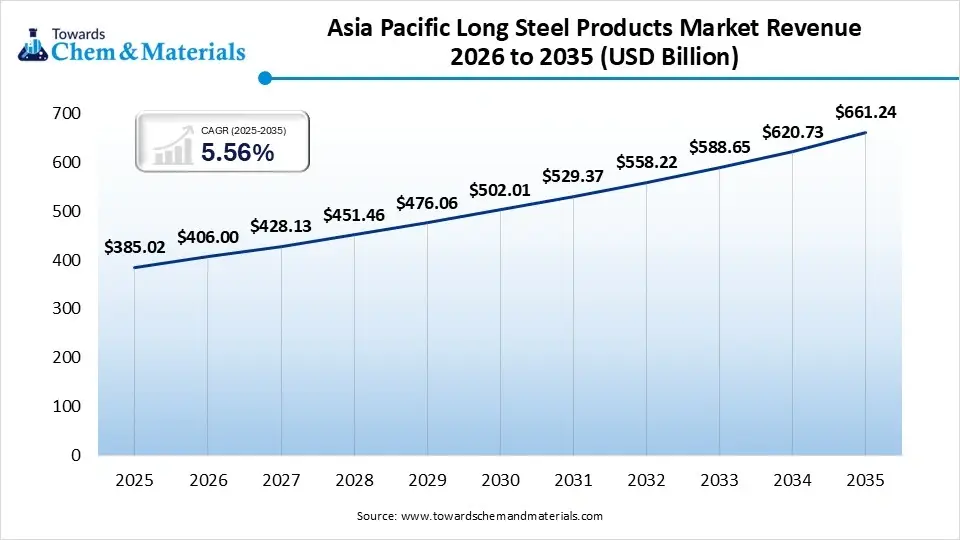

The Asia Pacific long steel products market size was estimated at USD 385.02 billion in 2025 and is projected to reach USD 661.24 billion by 2035, growing at a CAGR of 5.56% from 2026 to 2035. The development of transport projects and the vast industrial ecosystem increases the adoption of long steel products. The large-scale manufacturing units and the increased investment in rail construction increase demand for long steel products. The expanding electrical industry drives the market growth.

")

Role of Long Steel Products in China

China is the leading contributor to the market in the Asia Pacific region. The strong government backing for steel firms and the massive urbanization increase the use of long steel products. The development of Belt and Road projects and the low manufacturing cost increase the adoption of long steel products. The expansion of real estate construction supports the overall market growth.

Europe Long Steel Products Market Trends

Europe held the second largest share of 21% in the market in 2025 and expects a notable growth in the market with CAGR of 4.90% during the forecast period. The rise in green infrastructures and the advancement in manufacturing increase demand for long steel products. The growing urban revitalization projects and the development of sustainable building projects increase the adoption of long steel products. The heavy investment in green hydrogen increases the production of green steel. The rise in high-strength steel drives the market growth.

Germany’s Contribution to Long Steel Products

Germany is rapidly growing in the market. The burgeoning infrastructure investment and the advancements in automotive products increase demand for long steel products. The surging technological modernization and the well-established engineering heritage increase the adoption of long steel products. The growing urban development and the rising heavy machinery manufacturing increase the use of long steel products, supporting the market growth.

Recent Developments

- In April 2026, Jindal Stainless launched stainless steel rebars, Jindal Infinity, in Punjab. The rebars are useful across applications like real estate, coastal developments, and metros. The rebars offer excellent seismic performance and enhanced structural safety. The rebar offers excellent durability and is made from billets cast.

- In April 2026, JSW One introduced a new steel tubes & pipes brand, One Helix Pipes & Tubes. The brand is available in Andhra Pradesh, Tamil Nadu, southern Karnataka, and Telangana initially. The brand concentrated on developing a consistent quality of pipes and tubes. The brand offers the engineering and construction industries.

Top Companies List

- ArcelorMittal:- The Luxembourg-based company manufactures long steel products like rails, sheet piling, sections, wire rods, rebar, merchant bars, special sections, and bars for diverse industrial applications.

- China Baowu Group:- The Shanghai-based company offers products like bars, pipe, structural sections, specialty long products, rods, and tube products for industrial and construction applications.

- Nucor Corporation:- The company manufactures products like merchant bar quality, engineered bar quality, structural steel, rebar, steel piling for industrial machinery, infrastructure, and non-residential construction.

Long Steel Products Market Companies List

- Nippon Steel Corporation

- Tata Steel

- POSCO Holdings

- Ansteel Group

- Shougang Group

- Celsa Group

- Gerdau S.A.

- HBIS Group

- JSW Steel Limited

- Jiangsu Shagang Group

- JFE Steel Corporation

Long Steel Products Market Segments Covered

By Product Type

- Rebars

- Mild Steel Rebars

- High Strength Deformed Bars

- Corrosion Resistant Rebars

- Wire Rods

- Carbon Steel Wire Rods

- Alloy Steel Wire Rods

- Stainless Steel Wire Rods

- Merchant Bars

- Flats

- Angles

- Channels

- Rounds

- Structural Sections

- Beams

- H-Beams

- I-Beams

- Columns

- Rails

- Heavy Rails

- Light Rails

- Seamless Long Steel Products

- Special Bar Quality (SBQ) Steel

By Material Type

- Carbon Steel

- Low Carbon Steel

- Medium Carbon Steel

- High Carbon Steel

- Alloy Steel

- Chromium Alloy Steel

- Nickel Alloy Steel

- Molybdenum Alloy Steel

- Stainless Steel

- Austenitic

- Ferritic

- Martensitic

By Manufacturing Process

- Basic Oxygen Furnace (BOF)

- Electric Arc Furnace (EAF)

- Induction Furnace

- Continuous Casting

- Hot Rolling

- Thermo-Mechanical Treatment

By End-Use Industry

- Construction

- Residential Construction

- Commercial Construction

- Infrastructure Projects

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Rail Transportation

- Industrial Manufacturing

- Energy & Power

- Wind Energy

- Oil & Gas

- Transmission Infrastructure

- Shipbuilding

- Agriculture Equipment

By Application

- Reinforcement

- Structural Support

- Fasteners & Components

- Rail Tracks

- Wire Products

- Machinery Components

By Distribution Channel

- Direct Sales

- Steel Service Centers

- Distributors & Traders

- Online Procurement Platforms

By Grade

- Mild Steel Grade

- High Tensile Grade

- Corrosion Resistant Grade

- Heat Resistant Grade

- Wear Resistant Grade

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)