Content

What is the Current Fluorinated Polymers Market Size and Share?

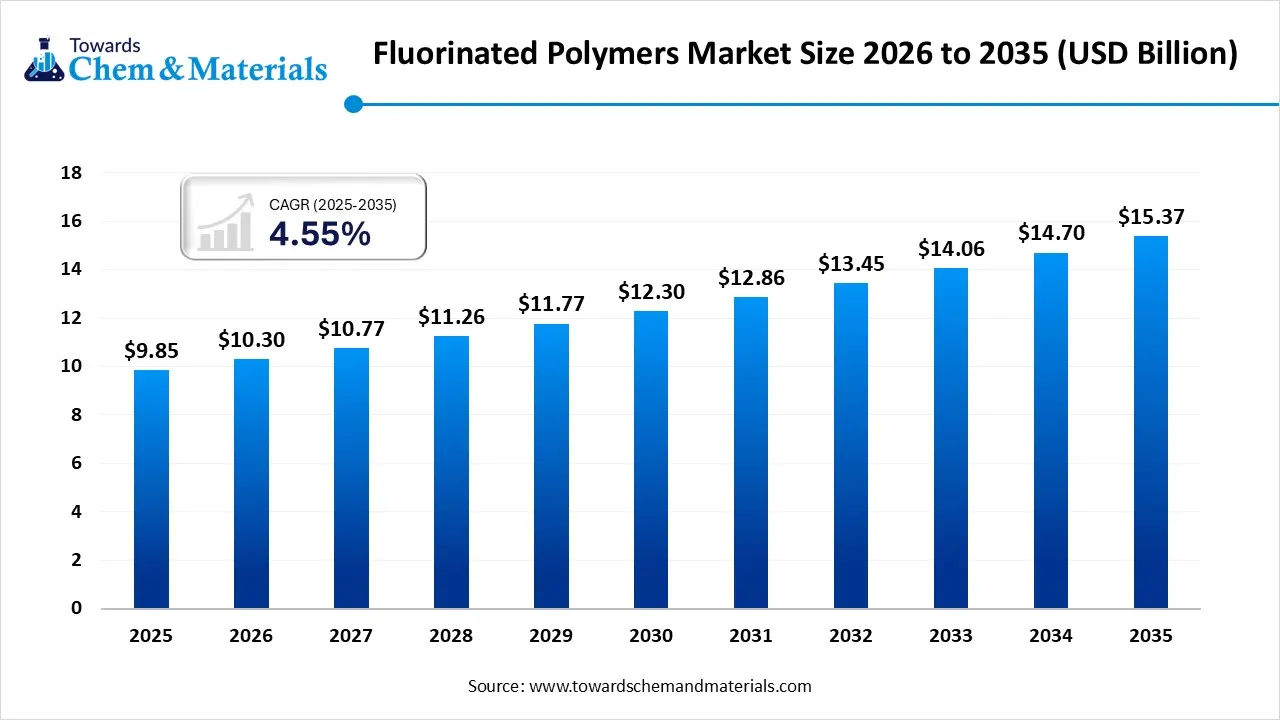

The global fluorinated polymers market size was estimated at USD 9.85 billion in 2025 and is expected to increase from USD 10.30 billion in 2026 to USD 15.37 billion by 2035, growing at a CAGR of 4.55% from 2026 to 2035. Asia Pacific dominated the fluorinated polymers market with the largest revenue share of 45.65% in 2025. The growth driven by regulatory-driven innovation, high-performance industrial applications and renewable energy infrastructure. The fluorinated polymers market is driven by specialty chemicals industry, characterized by its balance of chemical inertness, thermal stability, and low surface energy, moving toward ultra-purity polymers and regulatory-driven formulation. These resins are vital for advanced semiconductor fabrication for sub-nanometer chip processing. As the market integrates AI-driven materials informatics and transitions toward sustainability, with investments in non-surfactant manufacturing and recycling systems to meet global safety standards. Additionally, its specialty polymer architectures for medical devices, high-frequency telecommunications, and green energy applications are strengthening market dominance.

Market Highlights

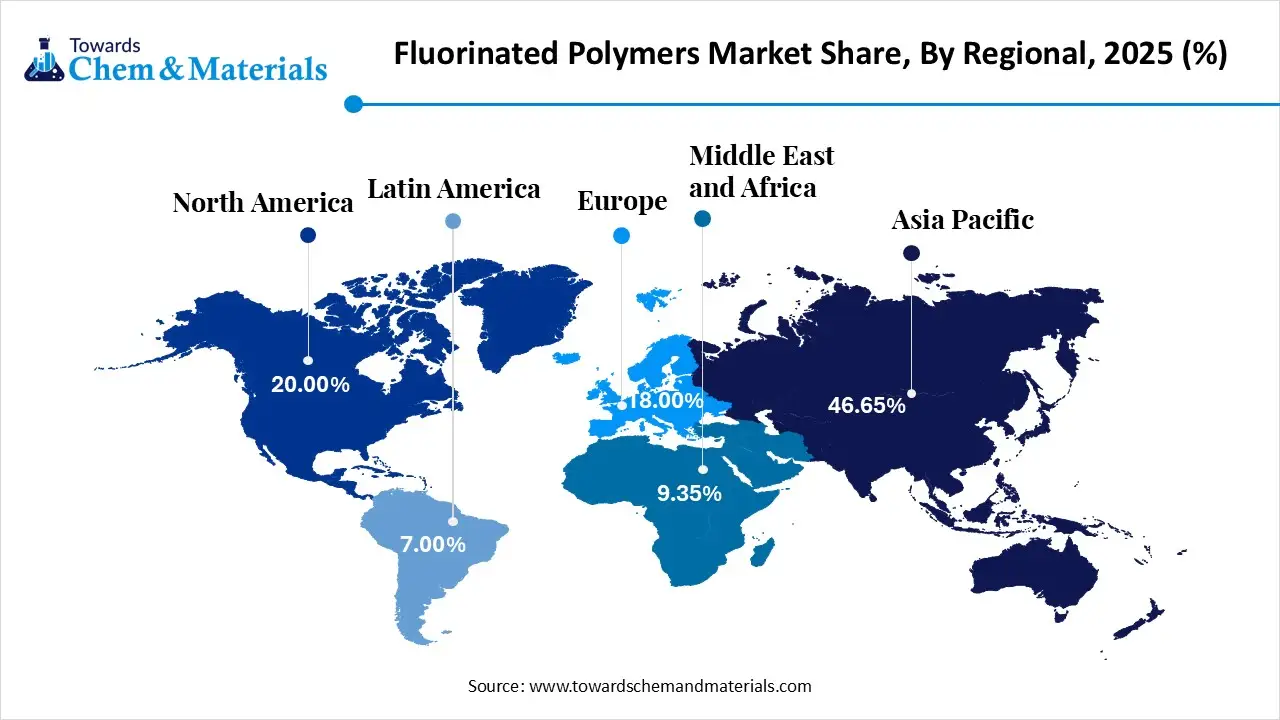

- The Asia Pacific dominated the fluorinated polymers market with the largest revenue share of 45.65% in 2025, due to rapid industrialization, rising demand in electronics, automotive and solar applications.

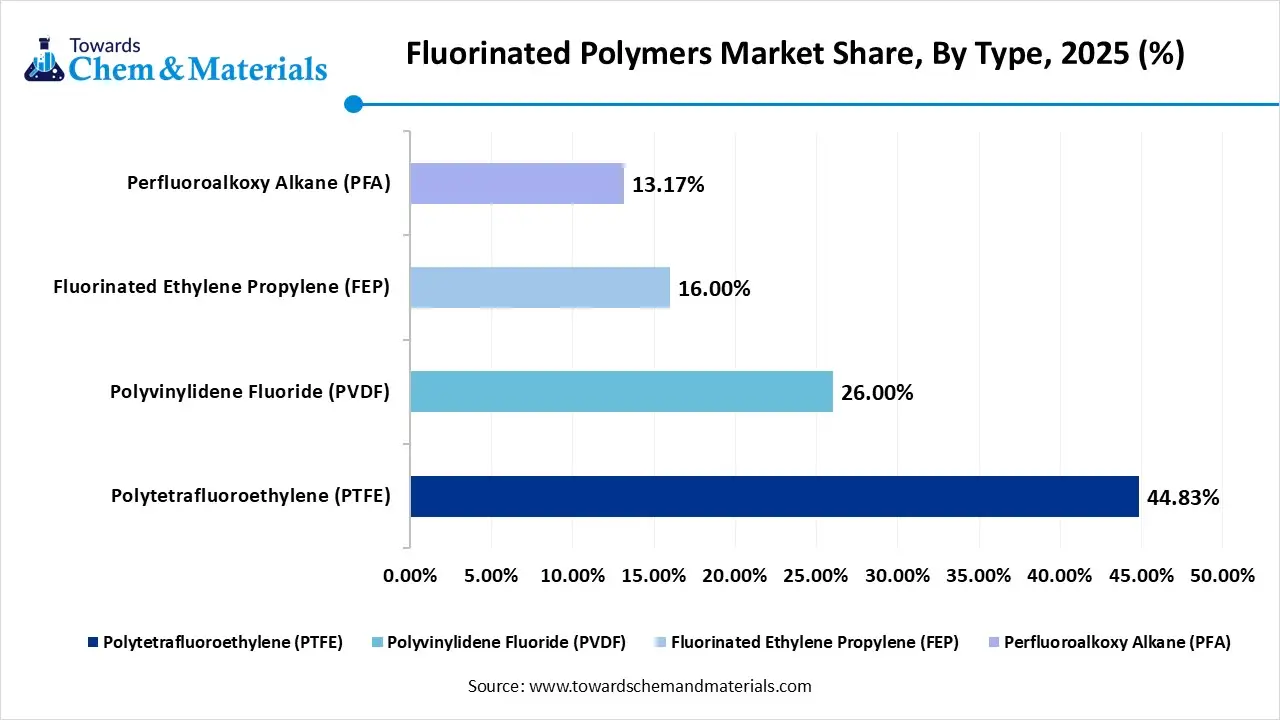

- By type, the polytetrafluoroethylene (PTFE) segment dominated the market and accounted for the largest revenue share of 44.83% in 2025, due to its thermal stability, low friction and chemical inertness.

- By type, the polyvinylidene fluoride (PVDF) segment is expected to grow at the fastest CAGR of 4.9% from 2026 to 2035 in terms of share, due to its demand in wire insulation, lithium-ion batteries and chemical processing equipment.

- By application, the electrical and electronics segment led the market with the largest revenue share of 30.19% in 2025. due to its dielectric and thermal stability in 5G infrastructure, semiconductors and electronic components, due to its dielectric and thermal stability in 5G infrastructure, semiconductors and electronic components.

Key Technological Shifts and AI in the Fluorinated Polymers Market

Technological advancement and AI are transforming the market by accelerating molecular discovery and optimizing manufacturing workflows. AI predicts properties of new polymers that focus on the development of sustainable, chemical-resistant formulations as sustainable alternatives.

In manufacturing, AI-enhanced process control improves the formation of ultra-high-purity grades using real-time sensor data, reducing waste and improving structural integrity. The blending of advanced simulation and 3D printing enables complex geometries, making AI an enabler for next-generation custom-functional materials by offering performance efficiency.

Trade Analysis of the Fluorinated Polymers Market: Import and Export Statistics

- China exported 320 shipments of fluorinated polymers.

- The United States exported 278 shipments of fluorinated polymers.

- Japan exported 223 shipments of fluorinated polymers.

- From July 2024 to June 2025, the world exported 595 shipments of fluorinated polymers.

Recent Market Trends

- Rising Focus on High-Purity Fluoropolymers: The focus on ultra-high-purity grades of perfluoroalkoxy (PFA) and fluorinated ethylene propylene (FEP) that offer resistance and sub-nanometre cleanliness used in semiconductor fabrication and advanced chipmaking.

- Regulatory-Driven Revolution: The stringent regulation for PFAS is driving the innovation shift towards non-fluorosurfactant technologies by maintaining the chemical properties and thermal stability of the polymers.

- Green Energy transition: The rising demand for fluoropolymers in green energy infrastructure, especially PVDF in binder and separator coatings in EVs, while the surge for the hydrogen economy is reshaping the market.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 10.30 Billion |

| Revenue Forecast in 2035 | USD 15.37 Billion |

| Growth Rate | CAGR 4.55% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Application, By Region |

| Key companies profiled | Arkema S.A., Gujarat Fluorochemicals Limited, The Chemours Company, 3M, Solvay S.A., Daikin Industries, Ltd, AGC Inc., Kureha Corporation, Dongyue Group Ltd, Halopolymer OJSC |

Market: Value Chain Analysis

- Feedstock Procurement: The stage involves the extraction of minerals(fluorspar) and the initial production of a chemical precursor for the entire fluorine chemical industry

- Key Player: Sinochem, The Chemours Company, GFL (Gujarat Fluorochemicals Ltd), and Daikin Industries

- Manufacturing and Processing: The chemical precursor is converted into organic fluoride monomers like vinylidene fluoride, hexafluoropropylene, and tetrafluoroethylene by using distillation and membrane-based purification and then polymerised into high-performance resins.

- Key Players: Gujarat Fluorochemicals, Arkema, Kureha Corporation, Daikin Industries and AGC Inc.

- Fabrication and End-Use Application: The final stage of shaping resins into specialized components by using fabrication techniques and the addition of secondary value films, coatings and molded parts for end-user sectors

- Key Players: Tesla, AkzoNobel, Boeing, The Chemours Company, W.L. Gore & Associates, Saint-Gobain and 3M Company

Regulatory Framework: Fluorinated Polymers Market

| Region | Key Regulations | Regulatory Focus |

| European Union | REACH Regulation, European Society for Paediatric Endocrinology and POP Regulation | Focus on EDCs found in fluorinates substance and universal PFAS restriction for PTFE and PVDF used in energy and medical sectors. |

| North America | TSCA Section | Regulation for reporting and recordkeeping for identifying the environmental exposure from fluoropolymer manufacturing |

| Asia Pacific | Hazardous Chemicals Safety Law, Chemical Substances Control Law, EPR rules and PFOA Emission Controls | Standards focus on PFOA/PFOS elimination to upgrade green polymerization and ensure semiconductor supply chain, manufacturers' bans, and waste management. |

Segmental Insights

Type Insights

Why the Polytetrafluoroethylene (PTFE)Segment Dominates the Fluorinated Polymers Market?

The polytetrafluoroethylene (PTFE)segment dominated the market accounting for more than 44.83% in 2025 in terms of global revenue, recognised for its chemical resistance and ability to withstand high temperatures by maintaining structural stability. It is key material for non-stick and low-friction applications, acting as a barrier against corrosive fluids and as an insulator for electrical systems due to its dielectric strength. Additionally, PTFE requires unique fabrication methods like ram extrusion and compression molding that make them high-purity and reliable component in critical infrastructure.

The polyvinylidene fluoride (PVDF) segment is the fastest-growing in the market during the forecast period due to its piezoelectric properties, mechanical strength and chemical resistance. It’s melt-processable by using molding and extrusion, making it a useful binder for battery electrodes and fluid handling systems resistant to solvents and acids. Its superior UV stability and weather resistance make it ideal for protective films and architectural coatings. The industry's focus on advanced energy storage and water filtration is boosting its demand in the electrochemical and chemical processing industries.

Fluorinated Polymers Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Polytetrafluoroethylene (PTFE) | 44.83% |

| Polyvinylidene Fluoride (PVDF) | 26.00% |

| Fluorinated Ethylene Propylene (FEP) | 16.00% |

| Perfluoroalkoxy Alkane (PFA) | 13.17% |

Application Insights

How did the Electrical and Electronics Segment hold the Largest Share in the Fluorinated Polymers Market?

The electrical and electronics segment held the largest revenue share in the market accounting for more than 30.19% in 2025 in terms of global revenue. It serves as a key pillar of innovation, offering polymers with superior thermal and insulating properties essential for high-performance wiring and microchip manufacturing. Their low dissipation properties and dielectric strength ensure interference-free signals, and their chemical inertness preserves intricate microchips free from contaminants. These materials also provide fire resistance and temperature tolerance without degradation, supporting dense electronic architectures in applications like telecommunications and aerospace systems.

The industrial processing segment is experiencing the fastest growth in the market during the forecast period. acting as an operational driver in protecting infrastructure in harsh chemical and thermal conditions. These materials resist reactive reagents, enabling safe containment and transportation, with applications in gaskets, seals, and joints that withstand solvents and pressure in chemical and refineries. Their low surface energy creates self-lubricating environments that reduce maintenance by preventing residue accumulation and wear friction. Moreover, as modern manufacturing demands grow, these resins remain crucial for the durability, operational efficiency and safety of global industrial systems with higher purity standards.

Fluorinated Polymers Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Electrical & Electronics | 30.19% |

| Industrial Processing | 18.00% |

| Automotive & Transportation | 14.00% |

| Building & Construction | 12.00% |

| Medical & Healthcare | 8.00% |

| Other Applications | 17.81% |

Regional Insights

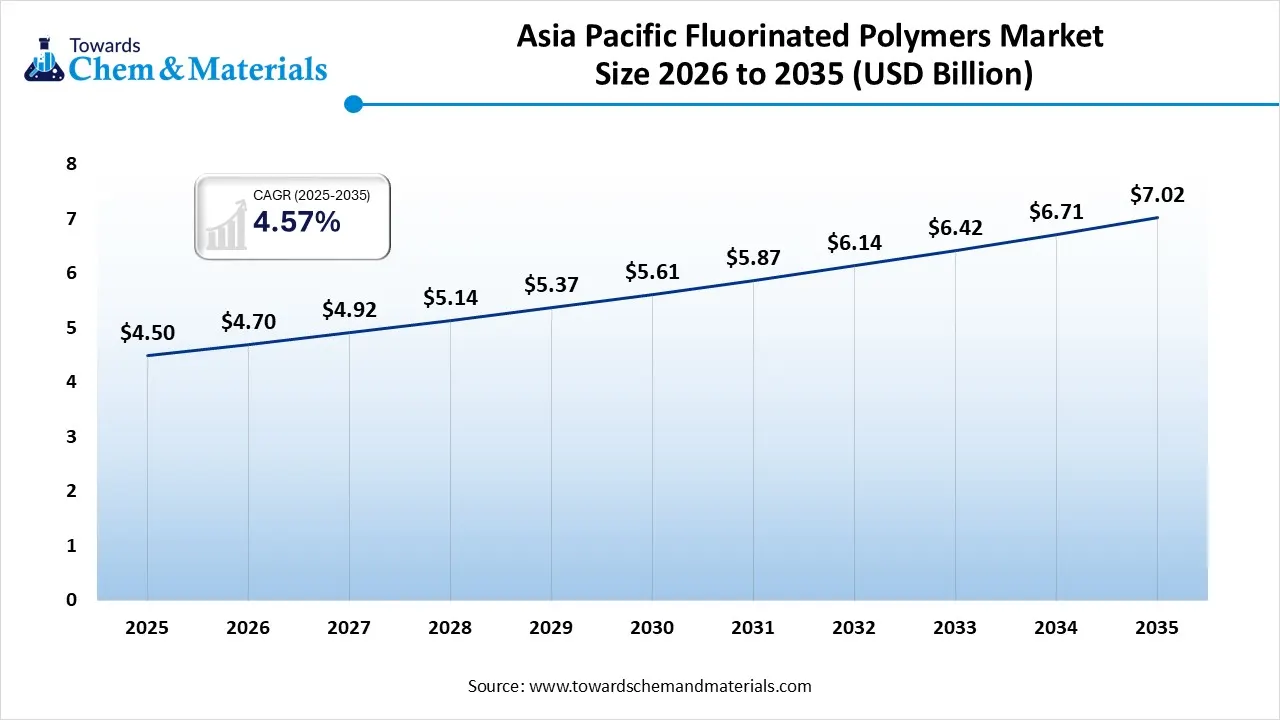

The Asia Pacific fluorinated polymers market size was valued at USD 4.50 billion in 2025 and is expected to be worth around USD 7.02 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 4.57% over the forecast period from 2026 to 2035.Asia Pacific dominated the market share 45.65% in 2025.

It is a major manufacturing and consumer hub, driven by the electronics and automotive industries. It dominates the lithium-ion battery supply chain, supporting electric mobility by providing high-performance binders and separator coatings. The region dominance is driven by its transition toward vertical integration, with local production of raw materials and rapid deployment of 5G & semiconductor fabrication. Furthermore, environmental standards are pushing toward process innovation and development of domestic high-value specialty grades, that making the Asia pacific as key pillar for material innovation and industrial growth.

China Fluorinated Polymers Market Growth Trends

China market is driven by its high production and consumption, known for its raw fluorspar supply chain. It is a key innovator in battery-grade PVDF, crucial for its electric vehicle sector. The industry focuses on quality migration and shifting from high-volume resins to ultra-high-purity polymers to boost semiconductor self-sufficiency, boosting the regional expansion. Additionally, China focuses on environmental compliance using advanced filtration and closed-loop systems.

North America is expected to grow at the fastest CAGR in the market during the forecast period accounting for 20.00% of total revenue, due to pioneer-grade innovation and ultra-high-purity standards for domestic advanced manufacturing. It serves as a testing ground for modern aerospace and medical applications that demand biocompatibility and environmental resilience. Major investments are supporting sustainable formulations aligned with environmental regulations. The region also promotes semiconductor independence and regulatory transformation with demand for polymers that withstand aggressive fabrication processes. Additionally, the regional technical service model, offering custom high-performance solutions for defense and clean energy sectors, fosters a sustainable chemical lifecycle.

U.S. Fluorinated Polymers Market Growth Trends

The U.S. market is known for advanced materials, driven by aerospace, satellite, and quantum computing needs. It leads in purity-critical manufacturing, supporting domestic semiconductor re-shoring. The country's competitive edge to develop bio-based, sustainable fluoropolymers that meet environmental standards, enabling its domestic growth. It supports energy security with high-durability components for battery storage while the U.S. shifts towards bespoke polymers, with technical expertise and safety compliance allowing growth.

Fluorinated Polymers Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 20.00% |

| Europe | 18.00% |

| Asia Pacific | 45.65% |

| Latin America | 7.00% |

| Middle East & Africa | 9.35% |

Europe Fluorinated Polymers Market Growth Trends

The Europe market sets global standards for regulation, led by strict environmental and safety infrastructure, accounting for 18.00% of total revenue.The region is transitioning to eco-innovation that is driving manufacturers' focus on high-purity, low-impact formulations aligned with the European Green Deal. It is a technological hub for advanced mobility, producing chemical-resistant materials for scaling battery invention and hydrogen networks. Additionally, as Europe market emphasizes lifecycle stewardship, advanced recycling, and sustainable materials that accelerating the expansion.

Germany Fluorinated Polymers Market Growth Trends

Germany’s market is prominent for precision chemical engineering, driven by high-quality standards in the automotive and mechanical industries. It specializes in high-purity solutions that resist chemical attack and maintain thermal stability. The region significantly invests in future-proof resins, balancing performance with environmental standards. Germany promotes green energy by delivering durable membranes and binders for green hydrogen and next-generation batteries. Overall, Germany's industry is expanding through integrated innovation, mission-critical materials, and delivering bespoke solutions for demanding environments.

Recent Developments

- In August 2025, Chemours announced a strategic agreement with an India-based SRF Limited to manufacture fluoropolymers and fluoroelastomers. This collaboration aims to provide secure production capacity for critical industries like semiconductors, aerospace, oil& gas and the automotive industry.(Source: www.chemours.com)

- In July 2025, AGC Inc. launched new grades in its AFLAS™ FFKM fluoroelastomer series produced entirely without surfactants and fluorinated polymerization solvents during the manufacturing process. This technology is initially targeting high-temperature semiconductor manufacturing equipment.(Source: www.agc.com)

Top Companies in the Market and Their Offerings

- Arkema S.A.: The global leader in sustainable fluorochemistry, and offers high-performance resins used in lithium-ion batteries and weather-resistant coatings.

- Gujarat Fluorochemicals Limited: The global manufacturer that utilizing integrated manufacturing base to provide a reliable supply chain and inert resins for telecommunications, textiles and industrial processing.

- The Chemours Company: The global provider of advanced fluoroelastomers and high-purity resin for semiconductor, automotive and aerospace industries.

- 3M

- Solvay S.A.

- Daikin Industries, Ltd

- AGC Inc.

- Kureha Corporation

- Dongyue Group Ltd

- Halopolymer OJSC

Segment Covered in the Report

By Type

- Polytetrafluoroethylene (PTFE)

- Polyvinylidene Fluoride (PVDF)

- Fluorinated Ethylene Propylene (FEP)

- Perfluoroalkoxy Alkane (PFA)

By Application

- Electrical & Electronics

- Industrial Processing

- Automotive & Transportation

- Building & Construction

- Medical & Healthcare

- Other Applications

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)