Content

What is U.S. Organic Peroxide Market Size?

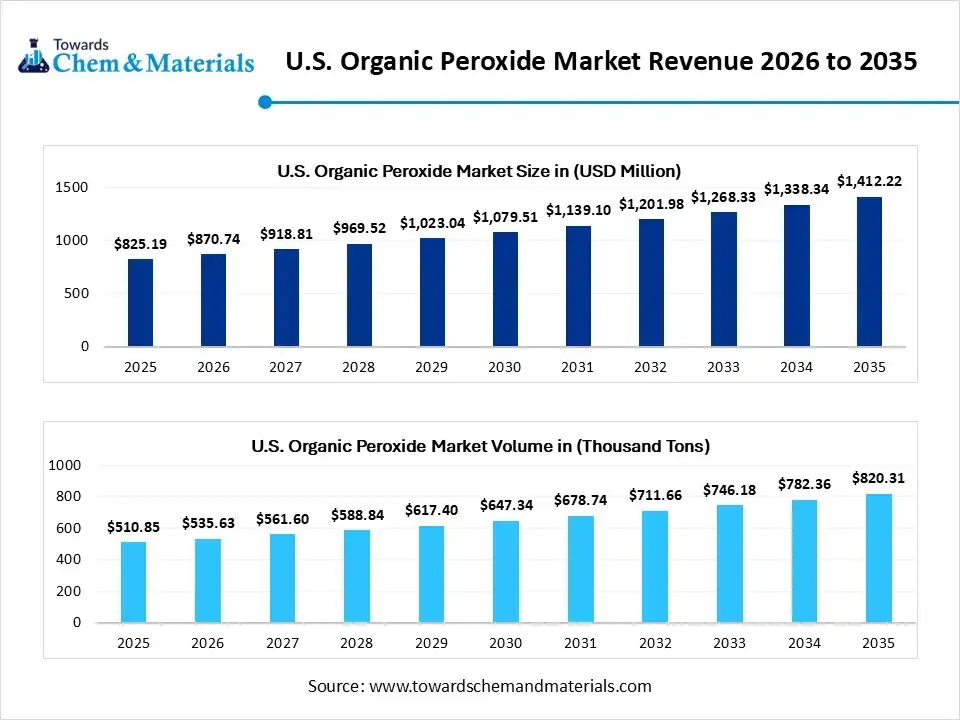

The U.S. organic peroxide market size was estimated at USD 825.19 million in 2025 and is expected to be worth around USD 1,412.22 million by 2035, growing at a CAGR of 5.52% from 2026 to 2035. In terms of volume, the U.S. organic peroxide industry is projected to grow from 510.85 thousand tons in 2025 to 820.31 thousand tons by 2035, exhibiting a compound annual growth rate (CAGR) of 4.85% over the forecast period from 2026 to 2035.Increasing demand for high-performance polymers is the key factor driving market growth. Also, a rise in automotive and infrastructure production, coupled with a shift towards sustainable curing agents, can fuel market growth further.

The market encompasses commercial manufacturing, distribution, and application of chemical compounds having an oxygen-oxygen bond. These highly reactive materials are used mainly as crucial initiators, catalysts, and cross-linking agents to produce synthetic rubbers, polymers, and specialized plastics. They are extensively used in industrial polymer manufacturing as well as in personal care and pharmaceutical classes.

Furthermore, the market benefits from a highly diverse application base, which propels its resilience during economic downturns. Additionally, continuous technological innovations are anticipated to improve the safety and efficacy of these compounds, hence increasing their attractiveness to end-users. As industries are emphasizing efficiency and sustainability, the market appears well-established for rapid growth in the upcoming year, reflecting a wider trend in material science.

Market Highlights

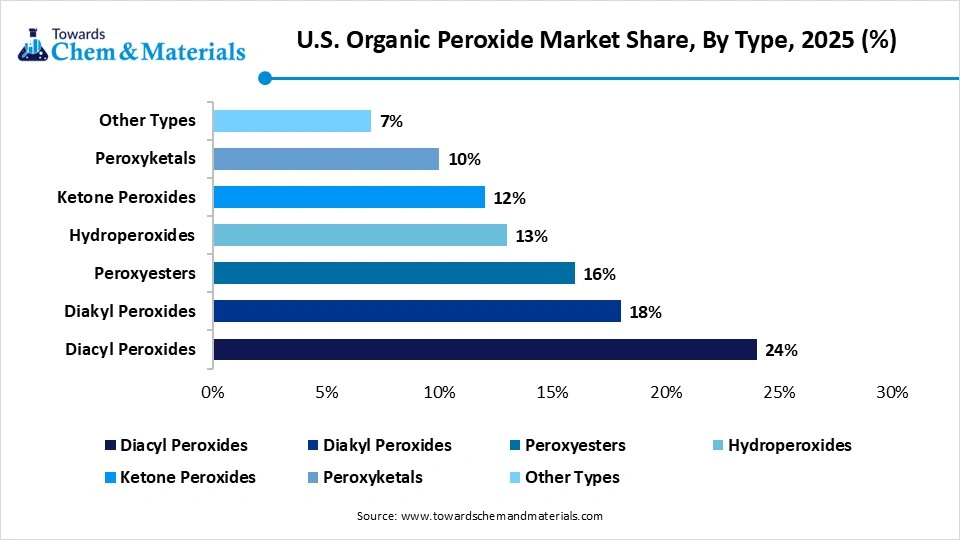

- By type, the diacyl peroxides segment dominated the market with the largest share of 24% in 2025. The dominance of the segment can be attributed to the increasing PVC polymerization demand.

- By type, the peroxyesters segment is expected to grow at the fastest CAGR of 6.72% over the forecast period. The growth of the segment can be credited to the growing use of controlled polymerization initiators.

- By function/application, the polymerization initiators segment dominated the market with the largest share of 39% in 2025. The dominance of the segment can be driven by a surge in the production of PVC.

- By function/application, the crosslinking agent segment is expected to grow at the fastest CAGR of 6.72% over the forecast period. The growth of the segment is owing to the increasing demand for crosslinked polythene.

- By form, the liquid peroxide segment dominated the market with the largest share of 46% in 2025 and is expected to grow at the fastest CAGR of 6.41% over the forecast period. The dominance and growth of the segment can be attributed to the increasing liquid peroxide utilisation.

- By distribution channel, the direct sales segment dominated the market with the largest share of 54% in 2025. The dominance of the segment can be driven by ongoing technical support integration.

- By distribution channel, the online retail/procurement portals segment is expected to grow at the fastest CAGR of 7.42% during the projected period. The growth of the segment is owed to the rapid adoption.

- By end-use industry, the polymer & plastic segment dominated the market with the largest share of 30% in 2025. The dominance of the segment can be attributed to the packaging and construction sector.

- By end-use industry, the composite & reinforced plastics segment is expected to grow at the fastest CAGR of 6.92% over the projected period. The growth of the segment can be credited to the increasing composite production.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 825.19 Million | CAGR (2026–2035): 5.52%

- Market Projected Size (2035): USD 1,412.22 Million

- Market Estimated Volume (2025): 510.85 Thousand Tons | Volume CAGR (2026–2035): 4.85%

- Market Projected Volume (2035): 820.31 Thousand Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 2,865 per Ton

- Average Selling Price: USD 3,598 per Ton

- Pricing CAGR (2026–2035): 2.15%

Market Trends

- Increasing product demand in the chemical sector is the latest trend in the market, shaping positive market growth. As industries are focusing on organic peroxides for cross-linking and polymerization processes. Also, the market growth is further fuelled by the rising demand for high-performance materials in different applications.

- The market is benefiting from a surge in emphasis on sustainable practices and renewable resources. As industries transition towards greener alternatives, organic peroxides extracted from renewable sources are rapidly gaining traction. This transition is likely to propel market growth, as companies are seeking to align with consumer preferences.

- Organic peroxides are extensively used as initiators in the polymerization process to produce several polymers. The growing demand for polymers and thermoplastics across various industrial applications is another major factor driving market growth over the foreseeable future.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 870.74 Million/ 535.63 Thousand Tons |

| Revenue Forecast in 2035 | USD 1,412.22 Million/ 820.31 Thousand Tons |

| Growth Rate | CAGR 5.52% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Function/Application, By Form, By Distribution Channel, By End-Use Industry, |

| Key companies profiled | Akzo Nobel, Arkema, United Initiators, Pergan GmbH, Chinasun Specialty Products, Jiangsu Yuanyang, Zibo Zhenghua, Laiwu Meixing, Hualun Chemical, and Dongying Haijing Chemical |

How Cutting-Edge Technologies Are Revolutionizing the U.S. Organic Peroxide Market?

Advanced technologies are transforming the market by improving safety, facilitating polymerization efficiency, and optimizing the manufacturing of lightweight and sustainable materials. Furthermore, companies are heavily deploying innovative stabilization techniques and specialized packaging to avoid temperature-causing self-reaction during transit and storage.

U.S. Organic Peroxide Market Supply Chain Analysis

- Feedstock Procurement:It involves the sourcing of essential raw materials, mainly organic acids, hydrogen peroxide, and various alcohols or ketones. It offers customized organic peroxide solutions and custom manufacturing.

- Major Players: Arkema Group, Nouryon

- Chemical Synthesis and Processing :It refers to the use of organic peroxides as crucial catalysts, intermediates, and reaction initiators. These radicals are used to transform monomer molecules into extensively used rubbers, plastics, and specialized chemical compounds.

- Major Players: United Initiators, Vanderbilt Chemicals, LLC

- Packaging and Labeling:It includes stringent safety regulations and specialized containers needed to handle these highly reactive, thermally unstable chemicals.

- Major Players: NOF Corporation, Pergan GmbH

- Regulatory Compliance and Safety Monitoring:It includes the rigorous protocols established to handle these highly reactive, thermally unstable, and potentially explosive chemicals.

- Major Players: United Initiators, NOF Corporation

U.S. Organic Peroxide Market's Regulatory Landscape: Regulations

| State | Key Regulation |

| California | (Cal/OSHA & Prop 65): Cal/OSHA enforces more aggressive Process Safety Management standards than federal OSHA, requiring lower thresholds for tracking hazardous processes. Furthermore, specific organic peroxide formulations must comply with clear chemical warning labels under California Proposition 65. |

| Texas | (TCEQ): As a major hub for plastics and polymer manufacturing, Texas enforces rigid air quality and industrial waste permits through the Texas Commission on Environmental Quality (TCEQ) for manufacturing plants and distributors handling raw organic peroxides. |

| New Jersey | (TCPA): The New Jersey Toxic Catastrophe Prevention Act (TCPA) mandates extra risk management and hazard assessments for facilities handling highly reactive chemicals, including specific organic peroxides, even at volumes below federal EPA limits. |

Market Dynamics

Drivers

Growing Emphasis on Renewable Resources

The market is benefiting from a surge in emphasis on renewable resources and sustainable practices, which is the major factor driving market growth. As industries are rapidly shifting towards organic and greener alternatives derived from renewable sources, companies are preferring sustainable products. In addition, this trend illustrates a wider shift toward sustainability, establishing the organic peroxide sector as an essential component in the transition to eco-friendly alternatives.

Restraint

Safety issues

The handling, transportation, and safety of organic peroxide are the major concerns hindering the market growth. Hence, to avoid any type of hazards and risks, the companies are focusing on several options for handling organic peroxide in the market. Moreover, the uneven geographical distribution and localized scarcity of raw materials act as another market restraint, constraining the consistent expansion and development of the organic peroxide industry.

Opportunity

Ongoing Development of Specialty Formulations

There is a significant opportunity for market players to invest in R&D to create safer, stable, and industry-specific organic peroxides. Advancements like encapsulated peroxides or blends, which provide better handling properties and minimize hazards, can open up new avenues in the market and applications. Furthermore, the expanding use of fiber-reinforced composites across the aerospace, wind energy, and automotive sectors offers significant growth potential. In this context, organic peroxides serve as vital curing agents for thermoset resins.

Segmental Insights

Type Insights

The diacyl peroxides segment dominated the market with the largest share of 24% in 2025. The dominance of the segment can be attributed to the growing demand for PVC polymerization in the construction and packaging sectors is driving market players to increasingly expand the applications of benzoyl peroxide in specialist plastics.The peroxyesters segment held the market share of 16% in 2025 and is expected to grow at the fastest CAGR of 6.72% over the forecast period. The growth of the segment can be credited to the growing use of controlled polymerization initiators in high-performance polymer manufacturing. The advanced resin system continues to expand industrial applications further.

")

The diacyl peroxides segment held the market share of 18% in 2025. The growth of the segment can be linked to the increasing polyolefin demand across the wire and cable industries. Thermal stability enhancements further support advanced polymer manufacturing. Demand from the automotive sector for lightweight components is driving consumption soon.

U.S. Organic Peroxide Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Diacyl Peroxides | 24% |

| Diakyl Peroxides | 18% |

| Peroxyesters | 16% |

| Hydroperoxides | 13% |

| Ketone Peroxides | 12% |

| Peroxyketals | 10% |

| Other Types | 7% |

Function/Application Insights

The polymerization initiators segment dominated the market with the largest share of 39% in 2025. The dominance of the segment can be driven by a surge in production of PVC and acrylic polymers and speciality resin manufacturing, supporting advanced peroxide utilization. Industrial polymer capacity growth will sustain market expansion soon.

The crosslinking agent segment held the market share of 22% in 2025 and is expected to grow at the fastest CAGR of 6.72% over the forecast period. The growth of the segment is owing to the increasing demand for crosslinked polythene across the cable and pipe industries, along with the growth in industrial polymer capacity.

The curing/hardening agents segment held the market share of 27% in 2025. The growth of the segment is due to expansion in wind energy and the automotive sector, coupled with the advanced resin system, which is improving industrial adoption. Composite and thermoset resin manufacturing continues driving curing agent demand.

U.S. Organic Peroxide Market Share, By Function/Application, 2025 (%)

| By Function/Application | Revenue Share, 2025 (%) |

| Polymerization Initiators | 39% |

| Curing/Hardening Agents | 27% |

| Crosslinking Agent | 22% |

| Bleaching/Oxidizing Agents | 12% |

Form Insights

The liquid peroxide segment dominated the market with the largest share of 46% in 2025 and is expected to grow at the fastest CAGR of 6.41% over the forecast period. The dominance and growth of the segment can be attributed to the increasing liquid peroxide utilisation for industrial process efficiency and automated dosing systems, enhancing operational performance.

The solid/powder peroxide segment held the market share of 37% in 2025. The growth of the segment can be credited to the powder formulations, which improve overall transportation safety and handling efficiency. Polymer production applications sustain steady market expansion further.

The paste/gel organic peroxide segment held the market share of 17% in 2025. The growth of the segment can be linked to the rising catalytic gel usage in composite manufacturing and stable formulation performance, improving industrial preference. Controlled curing application further drives market growth.

U.S. Organic Peroxide Market Share, By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Solid/Powder Peroxide | 37% |

| Liquid Peroxide | 46% |

| Paste/Gel Organic Peroxide | 17% |

Distribution Channel Insights

The direct sales segment dominated the market with the largest share of 54% in 2025. The dominance of the segment can be driven by ongoing technical support integration, improving supplier relationships, and large industrial buyers preferring long-term procurement agreements. High-volume polymer manufacturers sustain direct purchasing.

The online retail/procurement portals segment held the market share of 13% in 2025 and is expected to grow at the fastest CAGR of 7.42% during the projected period. The growth of the segment is owing to the rapid adoption of digital procurement, boosting speciality chemical purchasing and E-commerce platforms, and enhancing overall product accessibility for smaller buyers.

The distributors segment held the market share of 33% in 2025. The growth of the segment is due to regional supply chain expansion supporting distributor relevance and inventory optimization, enhancing procurement flexibility. Small and mid-sized manufacturers supporting channel demand.

U.S. Organic Peroxide Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 54% |

| Distributors | 33% |

| Online Retail/Procurement Portals | 13% |

End-Use Industry Insights

The polymer & plastic segment dominated the market with the largest share of 30% in 2025. The dominance of the segment can be attributed to the packaging and construction sector supporting polymer demand and advanced processing technologies improving utilisation. PVC and polyolefin production are driving peroxide consumption soon.

The composite & reinforced plastics segment held the market share of 15% in 2025 and is expected to grow at the fastest CAGR of 6.92% over the projected period. The growth of the segment can be credited to the increasing composite production in the wind energy and transportation sectors, along with the growing adoption of lightweight materials.

The rubber industry segment held the market share of 13% in 2025. The growth of the segment can be linked to the growing crosslinking peroxide demand for specialty manufacturing and automotive sealing applications. Industrial rubber processing sustains consumption further.

U.S. Organic Peroxide Market Share, By End-use Industry, 2025 (%)

| By End-use Industry | Revenue Share, 2025 (%) |

| Polymer & Plastic | 30% |

| Rubber Industry | 13% |

| Composite & Reinforced Plastics | 15% |

| Adhesives & Sealants | 9% |

| Paints & Coatings | 8% |

| Textile | 5% |

| Pharmaceuticals | 7% |

| Cosmetics & Personal Care | 4% |

| Pulp & Paper | 6% |

| Other End-use Industries | 3% |

Recent Development

- In May 2026, Nouryon, a global leader in specialty chemicals, launched Perkadox® PM-60ST-GR. This innovative organic peroxide technology is specifically formulated to upcycle degraded, recycled polypropylene. By restoring the polymer's mechanical properties and melt strength, the technology enables the reuse of recycled material in demanding automotive, packaging, and consumer goods applications.(Source: www.manilatimes.net)

U.S. Organic Peroxide Market Companies

- Akzo Nobel: Akzo Nobel's former specialty chemicals division now an independent company named Nouryon following its acquisition by the Carlyle Group is the undisputed global leader in the organic peroxide market. In the U.S., Nouryon acts as a primary initiator, crosslinking, and modifying agent supplier for the massive domestic polymers and plastics sector.

- Arkema: Arkema is a global leader in Specialty Materials, producing organic peroxides since 1953. In the U.S. market, they operate as a top-tier supplier of organic peroxide initiators and cross-linking agents, which are essential for polymer production, wire and cable manufacturing, and composite materials.

Other Companies in the Market

- United Initiators

- Pergan GmbH

- Chinasun Specialty Products

- Jiangsu Yuanyang

- Zibo Zhenghua

- Laiwu Meixing

- Hualun Chemical

- Dongying Haijing Chemical

Segments Covered in the Report

By Type

- Diacyl Peroxides

- Benzoyl Peroxide

- Lauroyl Peroxide

- Other Diacyl Peroxides

- Dialkyl Peroxides

- Dicumyl Peroxide

- Di-tert-butyl Peroxide

- Other Dialkyl Peroxides

- Peroxyesters

- tert-Butyl Peroxybenzoate

- tert-Butyl Peroxyacetate

- Other Peroxyesters

- Hydroperoxides

- Cumene Hydroperoxide

- tert-Butyl Hydroperoxide

- Other Hydroperoxides

- Ketone Peroxides

- MEKP (Methyl Ethyl Ketone Peroxide)

- Cyclohexanone Peroxide

- Peroxyketals

- 1,1-Di(tert-butylperoxy) Cyclohexane

- Other Peroxyketals

- Other Types

- Percarbonates

- Peroxydicarbonates

- Specialty Organic Peroxides

By Function/Application

- Polymerization Initiators

- PVC Polymerization

- Styrene Polymerization

- Acrylic Polymerization

- Curing/Hardening Agents

- Thermoset Resin Curing

- Composite Resin Hardening

- Crosslinking Agents

- Polyethylene Crosslinking

- Elastomer Crosslinking

- Bleaching/Oxidizing Agents

- Textile Oxidation

- Paper Bleaching

- Specialty Oxidation

By Form

- Solid/Powder Peroxide

- Granular

- Crystalline

- Liquid Peroxide

- Solvent-based Liquid

- Water-based Liquid

- Paste/Gel Organic Peroxide

- Catalyst Paste

- Gel Stabilized Peroxide

By Distribution Channel

- Direct Sales

- Long-term Industrial Contracts

- OEM Supply Agreements

- Distributors

- Chemical Distributors

- Regional Suppliers

- Online Retail/Procurement Portals

- B2B Procurement Platforms

- Specialty Chemical E-commerce

By End-Use Industry

- Polymer & Plastic

- PVC

- Polyethylene

- Polystyrene

- Rubber Industry

- Synthetic Rubber

- Specialty Elastomers

- Composite & Reinforced Plastics

- FRP Manufacturing

- Wind Energy Composites

- Adhesives & Sealants

- Industrial Adhesives

- Construction Sealants

- Paints & Coatings

- Industrial Coatings

- Automotive Coatings

- Textile

- Fabric Bleaching

- Technical Textiles

- Pharmaceuticals

- API Synthesis

- Disinfection Applications

- Cosmetics & Personal Care

- Acne Treatment Formulations

- Hair Bleaching Products

- Pulp & Paper

- Paper Bleaching

- Deinking Operations

- Other End-use Industries

- Electronics

- Water Treatment

- Agrochemicals

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (3)