Content

What is the current Asia Pacific Material Informatics Market Size and Share?

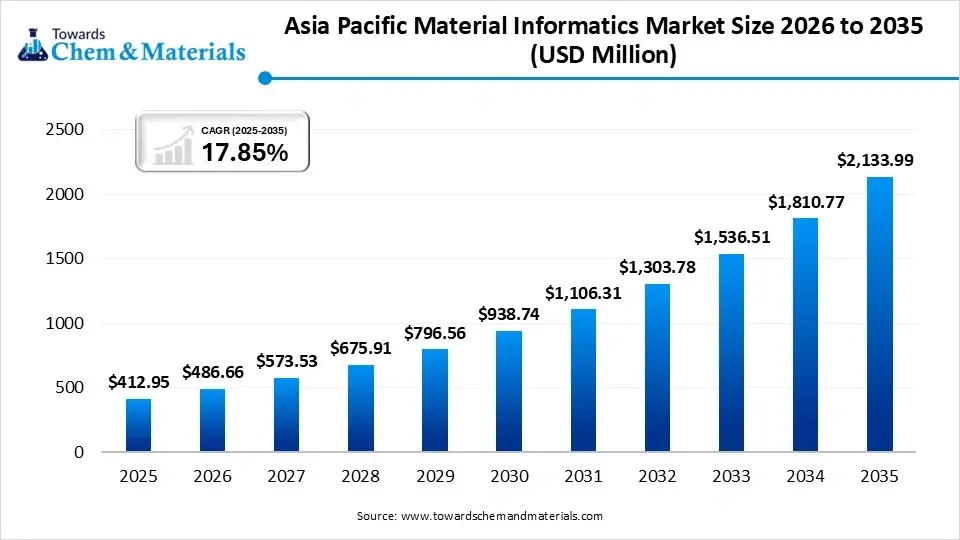

The Asia Pacific material informatics market size was valued at USD 412.95 million in 2025, is estimated to reach USD 486.66 million in 2026, and is projected to reach USD 2,133.99 million by 2035, exhibiting a compound annual growth rate (CAGR) of 17.85% over the forecast period from 2026 to 2035.The growth of the market is driven by heavy government investments, large talent pools, and booming electronics, semiconductor, and clean energy manufacturing sectors.

The Asia Pacific material informatics market is expanding. It plays a key role in using artificial intelligence (AI), machine learning, and data science to speed up materials discovery, reducing the time and cost to develop advanced materials for vital sectors like electronics, automotive, and renewable energy. APAC is a leading center for semiconductor, microelectronics, and EV battery manufacturing. Material informatics is crucial for creating the next generation of conductive, sustainable, and high-performance materials.

")

Traditional trial-and-error approaches can take years, but AI-driven modeling enables researchers to simulate complex material behaviors instantly, significantly reducing innovation timelines. Government initiatives such as China's "Made in China 2025," India's biotech and green materials hubs, and Japan's computer-assisted research institutes invest heavily in tech-enabled material development to stay competitive. Industry players like Schrödinger, Citrine Informatics, and Mat3ra offer platforms that combine experimental data with deep learning, empowering regional scientists.

The region also benefits from using deep tensor algorithms and AI to optimize hybrid materials and advanced ceramics for robotics and automotive applications. Focus areas include display technologies and semiconductor substrates, where AI improves production yields. The region is rapidly adopting these technologies by leveraging its large talent pool in data science to advance pharmaceuticals and eco-friendly chemical solutions.

Market Highlights

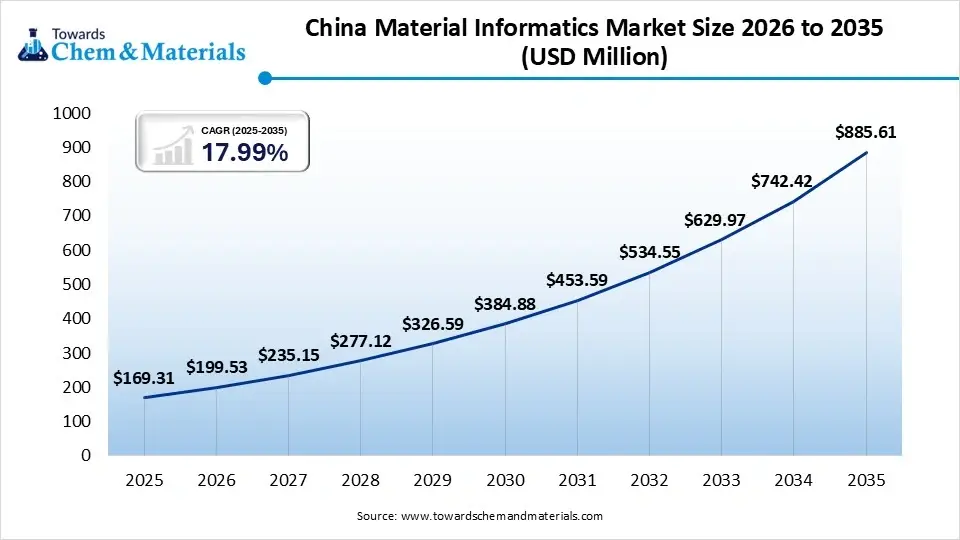

- The China Material Informatics market size was estimated at USD 169.31 million in 2025 and is projected to reach USD 885.61 million by 2035, growing at a CAGR of 17.99% from 2026 to 2035.

- The India Material Informatics market size was estimated at USD 86.72 million in 2025 and is projected to reach USD 458.81 million by 2035, growing at a CAGR of 18.13% from 2026 to 2035.

- The Japan Material Informatics market size was estimated at USD 74.33 million in 2025 and is projected to reach USD 394.79 million by 2035, growing at a CAGR of 18.17% from 2026 to 2035.

- The South Korea Material Informatics market size was estimated at USD 53.68 million in 2025 and is projected to reach USD 288.09 million by 2035, growing at a CAGR of 18.3% from 2026 to 2035.

- The Australia Material Informatics market size was estimated at USD 28.91 million in 2025 and is projected to reach USD 160.05 million by 2035, growing at a CAGR of 18.66% from 2026 to 2035.

- By country, China dominated the market with a share of 41% in 2025. Massive semiconductor and EV investments drive informatics adoption.

- By country, India held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.41% in the forecast period. Expanding technology ecosystem increases AI material research investments.

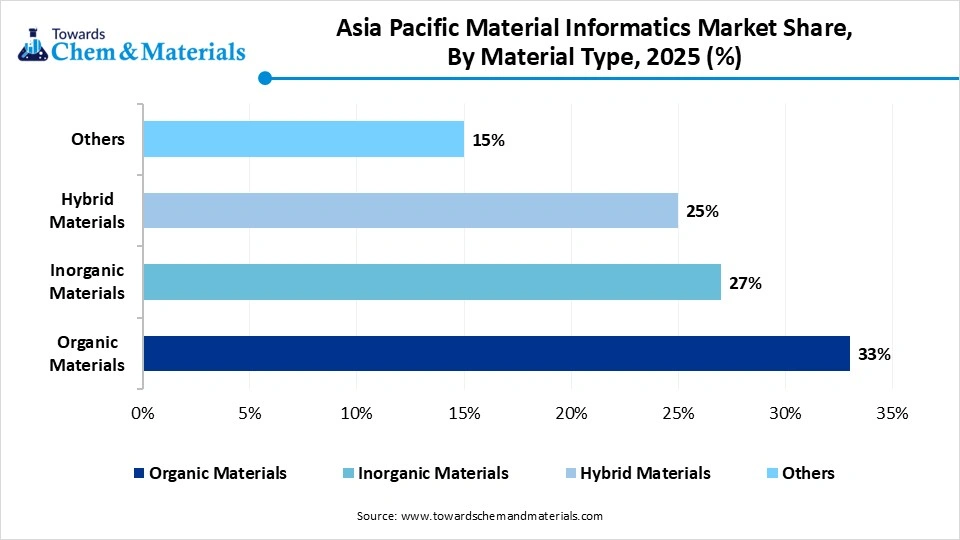

- By material type, the organic materials segment dominated the market with 33% share in 2025. Polymer innovation accelerates AI-driven material discovery projects.

- By material type, the hybrid materials segment held 25% market share in 2025 and is expected to have the fastest growth with a CAGR of 19.48% in the forecast period. Nanocomposite research drives the adoption of advanced simulation platforms.

- By technology, the machine learning segment dominated the market with 36% share in 2025. Predictive analytics improves material discovery speed significantly.

- By technology, the deep tensor segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.04% in the forecast period. Deep learning frameworks improve complex material property prediction.

- By end-use, the material science segment dominated the market with 29% share in 2025. Advanced material discovery increases informatics platform adoption.

- By end-use, the electronics and semiconductors segment held 23% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.16% in the forecast period. Semiconductor miniaturization boosts advanced material analytics demand.

RecentGrowth Trends:

- Green Energy & EVs: Surging demand for high-performance batteries, solar cells, and eco-friendly polymers requires rapid screening and testing of new chemical formulas.

- Electronics & Semiconductors: With microelectronics and nanotechnology miniaturization, companies are leaning on AI for material simulation to cut defect rates and boost yields.

- Industrial Backing: Heavy government subsidies and funding are rapidly accelerating the shift from traditional, trial-and-error chemistry to AI-driven, data-backed material discovery.

Key AI Technological Shifts in the Asia Pacific Material Informatics Market:

The Asia Pacific material informatics market is rapidly accelerating, driven by the integration of artificial intelligence (AI), machine learning, and quantum-inspired computing. This technological shift allows regional industries to slash material research times from decades to mere months, vastly cutting design costs for semiconductors, green energy, and advanced manufacturing. The region sees high adoption of quantum-inspired digital annealers to efficiently solve complex, multi-dimensional problems in molecular simulation, which traditional computing struggles to handle.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 486.66 Million |

| Revenue Forecast in 2035 | USD 2,133.99 Million |

| Growth Rate | CAGR 17.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Segment Covered | By Material Type, By Technology, By End-Use, By Country |

| Key companies profiled | Dassault Systèmes SE, IBM Corporation, Microsoft Corporation, ABB Ltd, Hitachi High-Tech Corporation, TDK Corporation, Lattice Technology, Inc., Alpine Electronics Inc., BASF Japan, Toray, Mitsui Chemicals, Citrine Informatics, Schrödinger, Inc., Exabyte Inc. / Mat3ra, Phaseshift Technologies. |

Supply Chain Analysis of the Asia Pacific Material Informatics Market:

- Material Informatics Platform Development & Data Processing:Material informatics platforms integrate artificial intelligence, machine learning, and big data analytics to accelerate material discovery, optimization, and performance prediction across industries such as electronics, energy, and advanced manufacturing. The Asia Pacific market is witnessing rapid growth due to increasing R&D investments and industrial digitalization initiatives.

- Key players: Citrine Informatics, Schrodinger, Dassault Systèmes, Hitachi.

- Quality Testing and Certification:Material informatics solutions must comply with data security standards, AI validation frameworks, computational modeling requirements, and industrial quality protocols to ensure reliability and accuracy in material development workflows.

- Key players: International Organization for Standardization, International Electrotechnical Commission, National Institute of Standards and Technology, Materials Genome Initiative.

- Distribution to Industrial Users:Material informatics solutions are adopted across semiconductor manufacturing, battery development, aerospace, automotive, chemicals, healthcare, and electronics industries for faster innovation and reduced R&D costs. Asia Pacific is emerging as the fastest-growing region due to strong industrial and technology investments.

- Key players: Citrine Informatics, Dassault Systèmes, Hitachi.

Asia Pacific Material Informatics Regulatory Landscape: Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| China | Ministry of Industry and Information Technology (MIIT); Ministry of Science and Technology (MOST) | Made in China 2025; AI Development Policies | AI-driven material discovery, semiconductor innovation | China is heavily investing in AI and advanced materials research to strengthen domestic semiconductor, battery, and manufacturing capabilities. |

| Japan | Ministry of Economy, Trade and Industry (METI); New Energy and Industrial Technology Development Organization (NEDO) | Society 5.0 Initiative; Green Innovation Fund | Smart manufacturing, advanced materials R&D | Japan promotes material informatics for next-generation electronics, robotics, and energy-efficient technologies. |

| South Korea | Ministry of Trade, Industry and Energy (MOTIE); Korea Institute of Science and Technology (KIST) | Digital New Deal; Materials Innovation Policies | Semiconductor materials, battery materials | South Korea supports AI-powered material discovery to enhance competitiveness in electronics and EV battery industries. |

| India | Department of Science and Technology (DST); Ministry of Electronics and Information Technology (MeitY) | National AI Strategy; Semiconductor Mission | Digital manufacturing, material research | India is expanding investments in AI-enabled materials research and semiconductor ecosystem development. |

| Singapore | Agency for Science, Technology and Research (A*STAR); Economic Development Board (EDB) | Research, Innovation and Enterprise (RIE) Plans | Smart manufacturing, advanced material analytics | Singapore supports material informatics through strong R&D infrastructure and digital innovation initiatives. |

| Australia | Commonwealth Scientific and Industrial Research Organisation (CSIRO); Department of Industry, Science and Resources | National AI Action Plan; Advanced Manufacturing Initiatives | Sustainable materials, mining innovation | Australia focuses on material informatics for mining, renewable energy, and industrial applications. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Asia Pacific Material Informatics Market?

The market is majorly driven by massive government R&D investments, the expansion of high-tech manufacturing industries such as electronics and electric vehicles, and the integration of Artificial Intelligence (AI) to enhance the discovery of innovative, sustainable materials. The booming semiconductor, electric vehicle (EV) battery, and consumer electronics industries in China, South Korea, India, and Japan require custom, high-performance materials like lightweight composites and heat-resistant alloys. Stricter environmental regulations and a regional push toward a circular economy are driving the need for material informatics to identify eco-friendly polymers, non-hazardous components, and green energy materials.

Restrains

What are the Key Growth Restraints of the Asia Pacific Material Informatics Market?

Key restraints in the Asia Pacific material informatics market include a significant shortage of technical experts, high maintenance and service costs, and the insufficient volume and quality of available material data. The cross-disciplinary nature of this field demands professionals who are experts in both data science/machine learning and materials science. There is a noted talent gap in this localized niche, which slows down the adoption of AI-driven material discovery. Predictive machine learning models rely heavily on robust, historically accurate, and clean databases. In many emerging sectors within Asia Pacific, material property data remains siloed, unstandardized, or scarce, directly limiting the effectiveness of informatics software.

Opportunities

What are the Key Growth Opportunities of the Asia Pacific Material Informatics Market?

The Asia Pacific material informatics market is experiencing the world's fastest regional growth, driven by rapid industrialization, heavy R&D investments, and the integration of AI in materials science. It enables companies to cut material discovery timelines by years, identify unique chemical formulations, and develop sustainable products. Governments and industries are heavily prioritizing green chemistry and eco-friendly substitutes. Informatics tools help forecast the lifecycle impacts of materials, design bio-based alternatives, and identify pathways for plastic recycling. The region's vast artificial intelligence infrastructure is a major catalyst. Machine learning models allow researchers to analyze massive datasets, perform high-throughput screening, and predict properties without needing expensive, time-consuming physical experiments.

Segmental Insights

Material Type Insights

The organic materials segment dominated the market with 33% share in 2025, fueled by accelerated R&D in the chemicals, electronics, and semiconductor sectors, along with an industry-wide shift toward predictive AI and machine learning in material design. There is surging demand for high-performance organic electronics, flexible displays, and sustainable, eco-friendly polymers. Material informatics allows companies to drastically reduce the time spent synthesizing and testing new organic compounds and formulations.

")

The inorganic materials segment held 27% market share in 2025, driven by the accelerated adoption of AI and machine learning. Inorganic material design is seeing significant adoption in the development of next-generation batteries, semiconductors, and energy systems. The inorganic sector is bolstered by the urgent need for solid-state electrolytes and advanced superalloys to support the electric vehicle (EV) and renewable energy supply chains.

The hybrid materials segment held 25% market share in 2025 and is expected to have the fastest growth with a CAGR of 19.48% in the forecast period, driven by the adoption of AI and machine learning. This growth is primarily accelerated by increasing demands in the electronics, automotive, and energy sectors for specialized, high-performance materials. Companies and institutions are shifting from traditional trial-and-error methods to data-driven AI models, allowing them to rapidly discover and optimize new hybrid materials.

Asia Pacific Material Informatics Market Share, By Material Type, 2025 (%)

| By Material Type | Revenue Share, 2025 (%) |

| Organic Materials | 33% |

| Inorganic Materials | 27% |

| Hybrid Materials | 25% |

| Others | 15% |

Technology Insights

The machine learning segment dominated the market with 36% share in 2025, driven by AI integration, which enables the rapid discovery of advanced materials for semiconductors, EV batteries, and electronics. Rapid expansion in the automotive, semiconductor, and renewable energy sectors requires high-speed material configuration. Major economies are heavily backing AI infusion into materials science through national programs and robust private-public partnerships.

The deep tensor segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.04% in the forecast period. This technology leverages advanced machine learning to analyze multi-dimensional data structures for faster materials discovery. Deep tensor methods are favored over traditional statistical analysis because they scale effectively, allowing researchers to simulate material properties with incredible accuracy and significantly reduce physical testing times.

The statistical analysis segment held 18% market share in 2025, driven by the massive industrial base and the urgent need to accelerate the discovery of advanced chemicals, polymers, and semiconductor materials. Statistical analysis, including quantitative structure-activity relationship (QSAR) modeling, is used for predictive process modeling to determine specific material functions and behaviors.

Asia Pacific Material Informatics Market Share, By Technology, 2025 (%)

| By Technology | Revenue Share, 2025 (%) |

| Machine Learning | 36% |

| Deep Tensor | 24% |

| Statistical Analysis | 18% |

| Digital Annealer | 13% |

| Others | 9% |

End-Use Insights

The Material Science Segment Dominated The Market With 29% Market Share In 2025

The material science segment dominated the market with 29% share in 2025, propelled by the integration of AI, machine learning, and data science. This technological shift dramatically reduces the time and cost required to discover and optimize advanced materials. Significant advancements in nanotechnology, quantum computing, and generative AI are generating entirely new classes of smart, sustainable, and functional materials.

The electronics and semiconductors segment held 23% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.16% in the forecast period. By leveraging artificial intelligence and data-driven insights, this segment enables rapid material discovery and optimization to meet the skyrocketing demands of consumer electronics, 5G technologies, and advanced computing. Companies are utilizing material informatics to slash the time and cost associated with synthesizing new advanced materials such as novel polymers and solid-state materials.

The chemical and pharmaceutical segment held 18% market share in 2025, driven by the rapid adoption of artificial intelligence and machine learning, which is streamlining complex compound formulation, drastically accelerating drug discovery, and reducing time-to-market across the region. Pharmaceutical and chemical companies are leveraging AI to predict molecular properties and optimize formulations. This cuts traditional trial-and-error costs and speeds up the discovery of new active ingredients.

Asia Pacific Material Informatics Market Share, By End-use, 2025 (%)

| By End-use | Revenue Share, 2025 (%) |

| Material Science | 29% |

| Chemical and Pharmaceutical | 18% |

| Electronics and Semiconductors | 23% |

| Automotive | 14% |

| Aerospace and Defense | 10% |

| Others | 6% |

Country Level Analysis

The China material informatics market size was estimated at USD 169.31 million in 2025 and is projected to reach USD 885.61 billion by 2035, growing at a CAGR of 17.99% from 2026 to 2035.China dominated the market with a share of 41% in 2025, fueled by the integration of AI in advanced manufacturing, government-backed R&D, and supply-chain localization, which drives the growth and expansion of the market. China is a leader in EV and battery manufacturing. Material informatics is heavily utilized to discover solid-state electrolytes and lightweight superalloys, ensuring the country retains a competitive edge in next-generation energy storage. The surging demand for renewable energy technologies and green manufacturing solutions is fueling a need for entirely new categories of high-performance, sustainable materials.

")

The India material informatics market size was estimated at USD 86.72 million in 2025 and is projected to reach USD 458.81 billion by 2035, growing at a CAGR of 18.13% from 2026 to 2035.India held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 20.41% in the forecast period, driven by the urgent need to accelerate material discovery, reduce R&D costs, and leverage AI to build localized supply chains. The drive for domestic semiconductor manufacturing and advanced electronic components requires the faster development of highly specific conductive and insulating materials. National programs pushing for technological innovation and the digitalization of materials science are heavily funding computational materials research across the Asia Pacific region.

Asia Pacific Material Informatics Market Share, By Country, 2025 (%)

| By Country | Revenue Share, 2025 (%) |

| China | 41% |

| India | 21% |

| Japan | 18% |

| South Korea | 13% |

| Australia | 7% |

Recent Development

- In August 2025, Mitsui, QSimulate, and Quantinuum launched QIDO (Quantum-Integrated Discovery Orchestrator), a hybrid computing platform designed to cut R&D costs and accelerate timelines for drug and materials discovery. The platform delivers high-precision chemical reaction modeling. This allows enterprise researchers to streamline complex workflows and make critical product development decisions much earlier in the cycle.(Source: www.quantinuum.com)

Top players in the Asia Pacific Material Informatics Market & Their Offerings

- Dassault Systèmes SE: Dassault Systèmes develops simulation and digital twin solutions integrated with material informatics tools for industrial design, manufacturing, and advanced engineering applications.

- IBM Corporation: IBM leverages AI, machine learning, and cloud computing technologies to support materials research, chemical simulations, and industrial innovation initiatives.

- Microsoft Corporation: Microsoft supports material informatics through cloud computing, AI infrastructure, and advanced analytics solutions for industrial R&D and manufacturing optimization.

- ABB Ltd.: ABB integrates AI-driven industrial automation and material optimization technologies to improve manufacturing efficiency and advanced materials processing.

- Materials Zone: Materials Zone offers cloud-based collaborative material informatics platforms that combine AI, laboratory data management, and predictive analytics for accelerated materials innovation.

Other Top Players Are

- Hitachi High-Tech Corporation

- TDK Corporation

- Lattice Technology, Inc.

- Alpine Electronics Inc.

- BASF Japan

- Toray

- Mitsui Chemicals

- Citrine Informatics

- Schrödinger, Inc.

- Exabyte Inc. / Mat3ra

- Phaseshift Technologies

Segments Covered

By Material Type

- Organic Materials

- Polymers

- Biomaterials

- Organic Electronic Materials

- Inorganic Materials

- Ceramics

- Metals & Alloys

- Glass Materials

- Hybrid Materials

- Nanocomposites

- Polymer-Ceramic Hybrids

- Metal-Organic Frameworks

- Others

- Smart Materials

- Quantum Materials

- Energy Storage Materials

By Technology

- Machine Learning

- Predictive Modeling

- Neural Networks

- Reinforcement Learning

- Deep Tensor

- Tensor-Based Optimization

- Deep Learning Frameworks

- AI Simulation Models

- Statistical Analysis

- Regression Analysis

- Bayesian Modeling

- Multivariate Analysis

- Digital Annealer

- Quantum-Inspired Computing

- Combinatorial Optimization

- High-Speed Simulation

- Others

- Cloud-Based Informatics

- High-Performance Computing

- Data Mining Platforms

By End-Use

- Material Science

- Advanced Material Discovery

- Nanotechnology Research

- Sustainable Material Development

- Chemical and Pharmaceutical

- Drug Formulation

- Catalyst Development

- Specialty Chemical Discovery

- Electronics and Semiconductors

- Semiconductor Materials

- Conductive Materials

- Battery Materials

- Automotive

- Lightweight Materials

- EV Battery Materials

- Coating Materials

- Aerospace and Defense

- Composite Materials

- Heat-Resistant Materials

- Structural Materials

- Others

- Energy & Utilities

- Academic Research

- Consumer Goods

By Country

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)