Content

What is the current Bio-Based Platform Chemicals Market Size and Share?

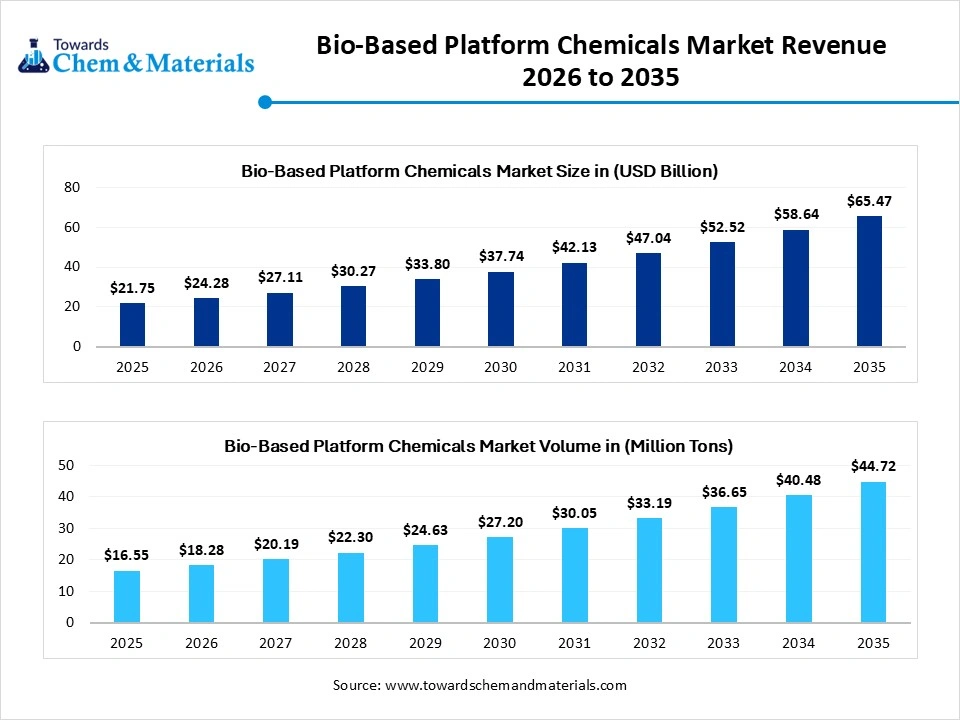

The global bio-based platform chemicals market size was valued at USD 21.75 billion in 2025, is estimated to reach USD 24.28 billion in 2026, and is projected to reach USD 65.47 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 11.65% over the forecast period from 2026 to 2035. In terms of volume, the bio-based platform chemicals market is projected to grow from 16.55 million tons in 2025 to 44.72 million tons by 2035. growing at a CAGR of 10.45% from 2026 to 2035. The sudden shift towards eco-friendly manufacturing has fueled industry potential in recent years. Bio-based platform chemicals are intermediate building blocks derived from renewable biomass such as sugars, starches, and lignocellulose used to produce bioplastics, solvents, and fuels, offering a sustainable alternative to fossil-based feedstocks. Key examples include lactic acid, succinic acid, and 5-hydroxymethylfurfural (5-HMF), which are crucial for creating high-value industrial materials.

The bio-based platform chemicals market is significant for enabling the transition to a sustainable, low-carbon circular economy by replacing petroleum-based raw materials with renewable biomass, agricultural waste, and algae. Valued heavily, the market is growing significantly due to rising demand for eco-friendly, bio-based polymers and chemicals in the packaging, textile, and automotive sectors.

The market is crucial for shifting from fossil fuel-based feedstocks to renewable resources like biomass, agricultural waste, and algae, thereby aligning with global sustainability initiatives. Innovation in biotechnology, including genetic engineering and fermentation, is improving production efficiency and lowering the cost of manufacturing bio-based alternatives, making them more competitive with petrochemicals. The adoption of these chemicals helps industries improve their environmental footprint, meeting consumer and regulatory pressure for cleaner-label products, particularly in cosmetics, food packaging, and agriculture.

Market Highlights

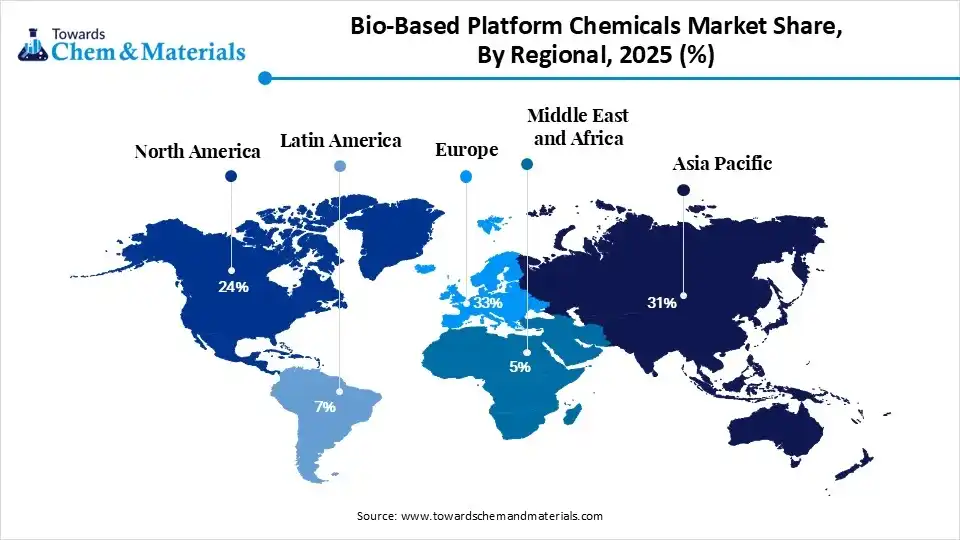

- By region, Europe dominated the market with a share of 33% in 2025. Strong sustainability regulations accelerate the commercialization of bio-based chemicals rapidly.

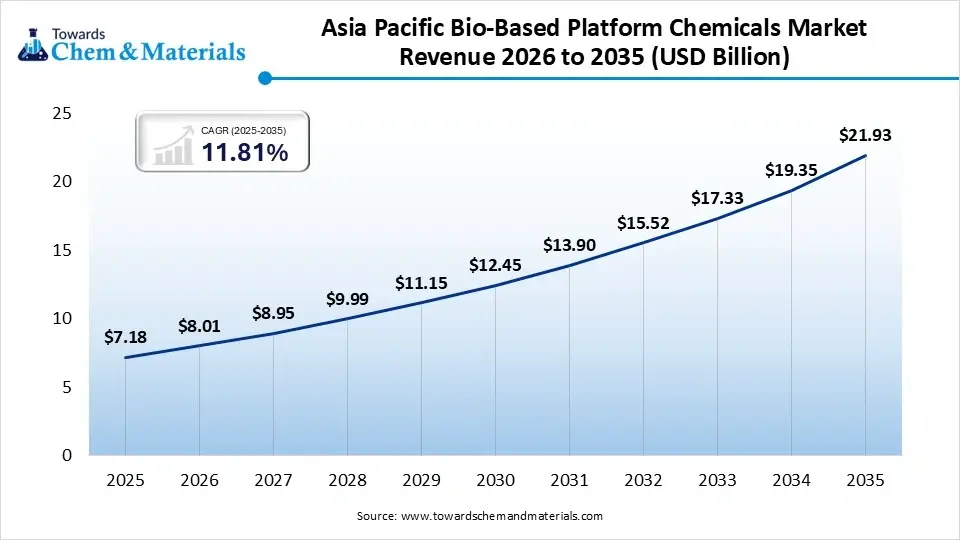

- By region, Asia Pacific held the market share of 31% in 2025 and is expected to grow fastest in the market with the CAGR of 13.40% in the forecast period. China and India continue to aggressively expand their industrial biotechnology production capacity.

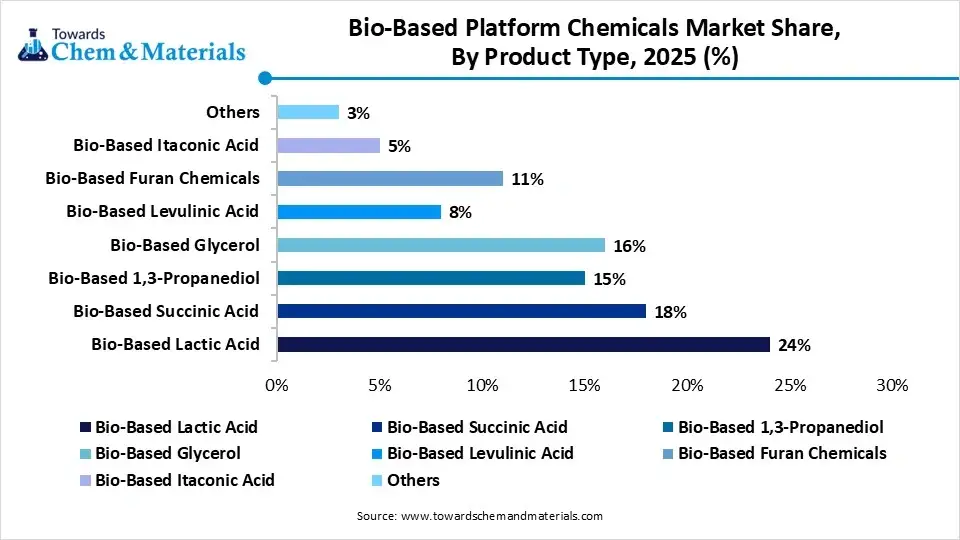

- By product type, the bio-based lactic acid segment dominated the market with 24% share in 2025. Rising demand for biodegradable PLA plastics accelerates lactic acid consumption globally

- By product type, the bio-based furan chemicals segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 14.20% in the forecast period. Growing interest in bio-based resins and fuels boosts furfural and HMF demand significantly.

- By feedstock, the sugarcane segment dominated the market with 29% share in 2025. High fermentable sugar content supports cost-efficient bio-based chemical production processes.

- By feedstock, the lignocellulosic biomass segment held 18% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.80% in the forecast period. Agricultural residue utilization reduces dependence on food-based feedstocks significantly.

- By production technology, the fermentation segment dominated the market with 48% share in 2025. Fermentation technology remains widely adopted for producing organic acids and alcohols.

- By production technology, the synthetic biology platforms segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.40% in the forecast period. Precision metabolic engineering enhances yield and selectivity for specialty chemicals.

- By application, the bioplastics segment dominated the market with 31% share in 2025. Global bans on single-use plastics are accelerating the adoption of bioplastic materials rapidly.

- By application, the biofuels segment held 9% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.80% in the forecast period. Sustainable aviation fuel development boosts demand for renewable chemical intermediates.

- By end-use industry, the packaging segment dominated the market with 28% share in 2025. Compostable and biodegradable packaging demand rises across the retail and food industries.

- By end-use industry, the healthcare segment held 12% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.90% in the forecast period. Medical-grade biopolymers gain traction in packaging and drug delivery applications.

- By distribution channel, the direct sales segment dominated the market with 46% share in 2025. Large chemical producers maintain direct relationships with industrial end users globally.

- By distribution channel, the online B2B platforms segment held 7% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.10% in the forecast period. Digital procurement platforms improve price transparency and supply chain efficiency.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 21.75 Billion | CAGR (2026–2035): 11.65%

- Market Projected Size (2035): USD 65.47 Billion

- Europe: largest Market Revenue Share of 33% in 2025.

- Market Estimated Volume (2025): 16.55 Million Tons | Volume CAGR (2026–2035): 10.45%

- Market Projected Volume (2035): 44.72 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 2,185/Ton

- Average Selling Price (2025): USD 3,045/Ton

- Pricing CAGR (2025–2035): 3.29%

Bio-Based Platform Chemicals Market Growth Trends:

- Emerging Green Chemicals: High-value platform chemicals like succinic acid, lactic acid, and furfural are seeing rapid adoption as industries look to replace petrochemicals in sustainable packaging and bioplastics.

- Technological Advancements: Breakthroughs in microbial fermentation and enzymatic conversion are lowering production costs, helping bio-based alternatives compete economically with traditional fossil-derived chemicals.

Corporate Sustainability: Accelerating corporate commitments to replace petrochemicals with renewable, biomass-derived alternatives to reduce carbon footprints.

Key Technological Shifts in the Bio-Based Platform Chemicals Market:

The bio-based platform chemicals market is undergoing a rapid transformation, driven by a shift toward sustainable feedstock, advanced metabolic engineering, and optimized downstream processing to lower production costs by up to 20%. Key shifts include utilizing second-generation feedstocks (waste/biomass), adopting digital AI-driven processes, and integrating hybrid chemical-biological production to replace petrochemicals. Shifting away from food-based sources to lignocellulosic biomass, agricultural residues, and waste-to-chemical routes to reduce dependence on fossil resources.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 24.28 Billion/ 18.28 Million Tons |

| Revenue Forecast in 2035 | USD 65.47 Billion / 44.72 Million Tons |

| Growth Rate | CAGR 11.65% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Europe |

| Segment Covered | By Product Type, By Feedstock, By Production Technology, By Application, By End-Use Industry, By Distribution Channel, By Regions |

| Key companies profiled | Cargill Incorporated, BASF SE, Braskem S.A, Corbion N.V., Novonesis, dsm-firmenich, GFBIOCHEMICALS, Mitsubishi Chemical Group Corporation, PTT Global Chemical Public Company Limited, DuPont, Tate & Lyle, Evonik Industries AG, Aktin Chemicals, Inc., Champlor, LyondellBasell Industries Holdings B.V., NIPPON SHOKUBAI CO., LTD., Novozymes A/S, part of Novonesis Group. |

Supply Chain Analysis of Bio-Based Platform Chemicals Market:

Bio-Based Chemical Production & Processing

- Bio-based platform chemicals are produced from renewable feedstocks such as biomass, agricultural residues, sugar, and vegetable oils through fermentation, catalytic conversion, and biochemical processing to create intermediates for sustainable chemicals and materials.

- Key players: BASF, Braskem, Corbion, Cargill

Quality Testing and Certification

- Bio-based platform chemicals must meet standards for bio-based content, sustainability, purity, and environmental compliance before industrial use.

- Key players: International Organization for Standardization, ASTM International, U.S. Department of Agriculture, European Chemicals Agency

Distribution to Industrial Users

- Bio-based platform chemicals are supplied to polymer manufacturers, packaging industries, pharmaceutical companies, cosmetics producers, and specialty chemical manufacturers.

- Key players: Braskem, Corbion, Cargill.

Bio-Based Platform Chemicals Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); United States Department of Agriculture (USDA); Food and Drug Administration (FDA) | Toxic Substances Control Act (TSCA); USDA BioPreferred Program; Renewable Chemical Production Tax Incentives | Renewable feedstocks, green chemistry, product safety | The U.S. promotes bio-based chemicals through federal procurement programs and sustainability initiatives, encouraging the replacement of petrochemical-based products. |

| European Union | European Commission; European Chemicals Agency (ECHA) | REACH Regulation; EU Green Deal; Circular Economy Action Plan | Sustainable chemicals, carbon reduction, circular economy | The EU strongly supports bio-based platform chemicals through green chemistry regulations and carbon-neutral industrial policies. |

| China | Ministry of Ecology and Environment (MEE); National Development and Reform Commission (NDRC) | Circular Economy Promotion Law; Green Manufacturing Policies | Sustainable industrial development, bioeconomy | China is expanding investments in bio-based chemicals to reduce dependence on fossil feedstocks and lower industrial emissions. |

| India | Ministry of Chemicals and Fertilizers; Ministry of Environment, Forest and Climate Change (MoEFCC) | National Policy on Biofuels; Green Chemistry Initiatives | Renewable feedstock utilization, industrial sustainability | India is increasingly promoting biomass-based chemicals under its bioeconomy and sustainable manufacturing initiatives. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of the Environment | Biomass Industrialization Strategy; Green Growth Strategy | Bioeconomy, carbon neutrality | Japan supports bio-based platform chemicals as part of its decarbonization and green innovation strategies. |

| Brazil | Ministry of Agriculture and Livestock (MAPA); Brazilian Institute of Environment and Renewable Natural Resources (IBAMA) | RenovaBio Program; National Bioeconomy Policies | Sugarcane-based chemicals, renewable feedstocks | Brazil benefits from abundant biomass resources and a strong ethanol infrastructure supporting bio-based chemical production. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Bio-Based Platform Chemicals Market?

The global bio-based platform chemicals market is primarily driven by stringent environmental regulations, corporate net-zero commitments, and volatile crude oil prices. Innovations in biotechnology, specifically synthetic biology and metabolic engineering, are significantly reducing production costs and increasing the scalability of green, renewable chemical alternatives. Governments worldwide are pushing for a circular economy. Policies like the European Green Deal mandate the reduction of greenhouse gas (GHG) emissions and fossil fuel reliance, directly boosting demand for bio-based substitutes.

Restrains

What are the Key Growth Restraints of the Bio-Based Platform Chemicals Market?

The bio-based platform chemicals market’s growth is primarily restrained by the high production costs and complex processing technologies required compared to traditional petrochemicals. This price gap, coupled with fluctuating feedstock supplies and massive infrastructure capital requirements, severely limits mass commercialization and price competitiveness. Heavy reliance on agricultural biomass like sugarcane, corn, and vegetable oils exposes manufacturers to seasonal crop yields, weather-related disruptions, and supply chain volatility. The use of edible crops for chemical production raises ethical and sustainability concerns over arable land usage, forcing a tricky transition toward lignocellulosic (non-food) biomass.

Opportunities

What are the Key Growth Opportunities of the Bio-Based Platform Chemicals Market?

The bio-based platform chemicals market is experiencing rapid growth, driven by stringent environmental regulations, corporate sustainability goals, and the need to replace petroleum-based derivatives. Key opportunities are emerging in green packaging, eco-friendly consumer goods, and biotechnology advancements that lower production costs. The shift away from single-use plastics is a primary driver. Platform chemicals like lactic acid and succinic acid are essential for synthesizing biodegradable bioplastics (like PLA), directly answering the massive demand from global e-commerce and food packaging.

Segmental Insights

Product Type Insights

The Bio-Based Lactic Acid Segment Dominated The Market With 24% Market Share In 2025

The bio-based lactic acid segment dominated the market with 24% share in 2025. With surging global demand for biodegradable plastics like Polylactic Acid (PLA), green solvents, and strict bans on single-use plastics, the sector is experiencing rapid expansion as a renewable alternative to petroleum-based chemicals. Global sustainability mandates and single-use plastic bans are heavily incentivizing shifts to bio-based materials.

The bio-based furan chemicals segment held 11% market share in 2025 and is expected to grow the fastest, with a CAGR of 14.20% over the forecast period, driven by global sustainability mandates and the need for bioplastics like PEF. Bio-based furans are recognized as top-tier biomass valorization tools, directly replacing petrochemical equivalents like benzene. This segment is a focal point in the growing bio-based platform chemicals market.

Feedstock Insights

The Sugarcane Segment Dominated The Market With 29% Market Share In 2025

The sugarcane segment dominated the market with 29% share in 2025, due to its high carbohydrate content, which yields cost-effective biofuels, bioplastics, and industrial chemicals. Sugarcane serves as a highly efficient, renewable feedstock. Advancements in fermentation technologies allow for the efficient conversion of both raw sugarcane sugars and bagasse into high-value platform chemicals.

Bio-Based Platform Chemicals Market Share, By Feedstock, 2025 (%)

| By Feedstock | Revenue Share, 2025 (%) |

| Sugarcane | 29% |

| Corn | 24% |

| Lignocellulosic Biomass | 18% |

| Vegetable Oils | 12% |

| Algae Biomass | 7% |

| Industrial Organic Waste | 10% |

The lignocellulosic biomass segment held 18% market share in 2025 and is expected to grow the fastest, with a CAGR of 13.80% over the forecast period, due to its high availability, cost-effectiveness, and ability to bypass food vs. fuel competition. This expansion is driving the transition toward circular bioeconomies and eco-friendly polymer alternatives. The biomass is efficiently broken down into valuable platform chemicals via advanced fermentation and catalytic processes.

Production Technology Insights

The Fermentation Segment Dominated The Market With 48% Market Share In 2025

The fermentation segment dominated the market with 48% share in 2025, driven by carbon-neutrality mandates and the push to replace petrochemicals. Improved microbial and precision fermentation technologies are revolutionizing the production of building-block chemicals like lactic acid, bio-succinic acid, and bio-alcohols. Genetic engineering and metabolic engineering of microorganisms are continually increasing yield and expanding the range of accessible chemical building blocks.

Bio-Based Platform Chemicals Market Share, By Production Technology, 2025 (%)

| By Production Technology | Revenue Share, 2025 (%) |

| Fermentation | 48% |

| Catalytic Conversion | 18% |

| Thermochemical Conversion | 12% |

| Biorefinery Processing | 14% |

| Synthetic Biology Platforms | 8% |

The synthetic biology platforms segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 15.40 % in the forecast period by enabling precision engineering of microorganisms to produce high-value chemicals efficiently. This segment serves as the backbone for scaling sustainable, biorefinery production of core chemical building blocks like lactic acid, succinic acid, and bioplastics.

Application Insights

The Bioplastics Segment Dominated The Market With 31% Market Share In 2025

The bioplastics segment dominated the market with 31% share in 2025. Driven by strict environmental regulations and high demand for sustainable packaging, bioplastics dictate market expansion and drive continuous innovations in green chemistry. Stringent single-use plastics bans by local governments, alongside international carbon reduction mandates, strongly favor bio-derived platform chemicals.

Bio-Based Platform Chemicals Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Bioplastics | 31% |

| Solvents | 14% |

| Resins & Polymers | 19% |

| Pharmaceuticals | 9% |

| Cosmetics & Personal Care | 11% |

| Food & Beverage Additives | 7% |

| Biofuels | 9% |

The biofuels segment held 9% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.80% in the forecast period, rapidly expanding as industries and governments mandate the shift from fossil fuels to cleaner energy alternatives. This renewable energy demand is co-producing high-value biochemicals, fueling an overall growth and expansion of the market.

End-Use Industry Insights

The Packaging Segment Dominated The Market With 28% Market Share In 2025

The packaging segment dominated the market with a 28% share in 2025, driven by the urgent global push for sustainable, eco-friendly materials and stricter regulations on single-use plastics. Platform chemicals like succinic acid, lactic acid, and bio-based polyethylene are extensively used to create biodegradable packaging solutions.

Bio-Based Platform Chemicals Market Share, By End-use Industry, 2025 (%)

| By End-use Industry | Revenue Share, 2025 (%) |

|

Packaging

|

28% |

| Automotive | 13% |

| Textile | 14% |

| Healthcare | 12% |

| Consumer Goods | 15% |

| Agriculture | 10% |

| Energy | 8% |

The healthcare segment held 12% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.90% in the forecast period, driven by the rising demand for eco-friendly excipients, active pharmaceutical ingredients (APIs), and biodegradable medical packaging. Pharmaceutical companies are increasingly adopting biobased platform chemicals like bio-glycerol, succinic acid, and lactic acid to reduce their carbon footprint and align with green chemistry principles.

Distribution Channel Insights

The Direct Sales Segment Dominated The Market With 46% Market Share In 2025

The direct sales segment dominated the market with a 46% share in 2025, as manufacturers look to streamline supply chains and build closer relationships with industrial end-users like pharmaceuticals, bioplastics, and agriculture. This model cuts out traditional middlemen, allowing producers to meet exact specifications and improve profit margins. Favorable environmental policies and circular economy initiatives in regions are accelerating the adoption of bio-based substitutes over conventional fossil fuel chemicals.

Bio-Based Platform Chemicals Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 46% |

| Specialty Chemical Distributors | 30% |

| Contract Supply Agreements | 17% |

| Online B2B Platforms | 7% |

The online B2B platforms segment held a 7% market share in 2025 and is expected to grow the fastest, with a CAGR of 15.10% over the forecast period as chemical manufacturers and distributors digitize their procurement processes, streamline supply chains, and increase their global reach to meet strict sustainability and carbon-reduction targets. B2B e-commerce eliminates traditional middlemen, allowing verified buyers to source bio-based chemicals directly from biorefineries and green chemistry innovators.

Regional Insights

How did Europe Dominate the Bio-Based Platform Chemicals Market in 2025?

Europe dominated the market with a 33% share in 2025, driven by strict regional climate regulations, heavy investments in green chemistry, and comprehensive governmental policies to eliminate dependency on fossil fuels. Europe is a growing region due to strict environmental regulations, circular economy initiatives, and carbon-neutral industrial strategies. driven by strict regional climate regulations, heavy investments in green chemistry, and comprehensive governmental policies to eliminate dependency on fossil fuels.

")

Germany Bio-Based Platform Chemicals Market Growth Factor

Germany’s bio-based platform chemicals market is primarily driven by the nation's ambitious carbon-neutral goals, stringent environmental regulations, and a robust domestic biotechnology sector. Major investments by industry leaders in advanced biorefineries continue to propel market expansion. Germany leads in green chemistry innovation and sustainable industrial production supported by advanced R&D capabilities.

Asia Pacific Bio-Based Platform Chemicals Market Growth Factor

Asia Pacific held the market share of 31% in 2025 and is expected to grow fastest in the market with the CAGR of 13.40% over the forecast period, driven by robust government support for green industrialization, a massive manufacturing base, and abundant renewable feedstocks in economies like China and India. Stricter environmental regulations on single-use plastics across the APAC region are propelling the adoption of biodegradable bioplastics, which directly drives the need for bio-based chemicals like succinic acid and lactic acid.

China Bio-Based Platform Chemicals Market Growth Factor

The growth of the bio-based platform chemicals market in China is primarily driven by strict government environmental regulations like carbon neutrality goals, the Five-Year Plans emphasizing green chemistry, vast biomass availability, and rising demand for sustainable bio-plastics and eco-friendly packaging materials. China leads the regional market with strong investments in bio-based industrial infrastructure and an increasing focus on reducing dependence on petrochemicals.

Recent Developments

- In September 2025, The Tata Chemicals Limited (TCL)–TERI Centre of Excellence (CoE) on Biochemicals, inaugurated on September 23, 2025, is a research and biomanufacturing hub located in Gurugram, India. Its primary goal is to accelerate India's transition from fossil-based chemical production to sustainable, bio-based alternatives.(Source: teriin.org)

- In April 2026, Sun Chemical in April 2026, the company has launched AquaHeat, a new range of bio-based and food-safe inks specifically designed for high-temperature food packaging.(Source: www.packaginginsights.com)

Top players in the Bio-Based Platform Chemicals Market & Their Offerings:

- Cargill Incorporated: Cargill produces bio-based platform chemicals derived from renewable feedstocks such as corn and sugar. The company supplies ingredients for bioplastics, personal care, food additives, and industrial applications.

- BASF SE: BASF develops bio-based intermediates and specialty chemicals for polymers, coatings, and industrial applications, focusing on sustainable chemistry and low-carbon production technologies.

- Braskem S.A.: Braskem is a leading producer of bio-based chemicals and biopolymers, particularly bio-based polyethylene derived from sugarcane ethanol.

- Corbion N.V.: Corbion specializes in lactic acid and algae-based ingredients used in food preservation, bioplastics, and biochemical production.

- Novonesis: Novonesis (formerly Novozymes) develops enzymes and biotechnology solutions supporting bio-based chemical production through advanced fermentation processes.

Other Top Players Are

- dsm-firmenich

- GFBIOCHEMICALS

- Mitsubishi Chemical Group Corporation.

- PTT Global Chemical Public Company Limited

- DuPont

- Tate & Lyle

- Evonik Industries AG

- Aktin Chemicals, Inc.

- Champlor

- LyondellBasell Industries Holdings B.V.

- NIPPON SHOKUBAI CO., LTD.

- Novozymes A/S, part of Novonesis Group

Segments Covered:

By Product type

- Bio-Based Succinic Acid

- Petroleum Replacement Grade

- Industrial Grade

- Bio-Based Lactic Acid

- Food Grade

- Polymer Grade

- Pharmaceutical Grade

- Bio-Based 1,3-Propanediol

- Textile Grade

- Cosmetic Grade

- Bio-Based Glycerol

- Crude Glycerol

- Refined Glycerol

- Bio-Based Levulinic Acid

- Fuel Additive Grade

- Chemical Intermediate Grade

- Bio-Based Furan Chemicals

- IIFurfural

- Hydroxymethylfurfural (HMF)

- Bio-Based Itaconic Acid

- Others

- Sorbitol

- Xylitol

- Glucaric Acid

By Feedstock

- Sugarcane

- Corn

- Lignocellulosic Biomass

- Agricultural Residues

- Forestry Residues

- Vegetable Oils

- Algae Biomass

- Industrial Organic Waste

By Production Technology

- Fermentation

- Microbial Fermentation

- Enzymatic Fermentation

- Catalytic Conversion

- Thermochemical Conversion

- Pyrolysis

- Gasification

- Biorefinery Processing

- Synthetic Biology Platforms

By Application

- Bioplastics

- PLA

- PHA

- PBS

- Solvents

- Green Industrial Solvents

- Specialty Solvents

- Resins & Polymers

- Polyesters

- Polyurethanes

- Pharmaceuticals

- Drug Formulation

- Active Ingredients

- Cosmetics & Personal Care

- Skin Care Ingredients

- Hair Care Ingredients

- Food & Beverage Additives

- Sweeteners

- Preservatives

- Biofuels

- Fuel Blending

- Sustainable Aviation Fuel Intermediates

By End-Use Industry

- Packaging

- Flexible Packaging

- Compostable Packaging

- Automotive

- Interior Components

- Bio-based Coatings

- Textile

- Fibers

- Performance Fabrics

- Healthcare

- Medical Polymers

- Drug Delivery Systems

- Consumer Goods

- Household Products

- Electronics Components

- Agriculture

- Biodegradable Mulch Films

- Agrochemical Intermediates

- Energy

By Distribution Channel

- Direct Sales

- Specialty Chemical Distributors

- Contract Supply Agreements

- Online B2B Platforms

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)