Content

What is the Current Fiberglass Fabric Market Size and Share?

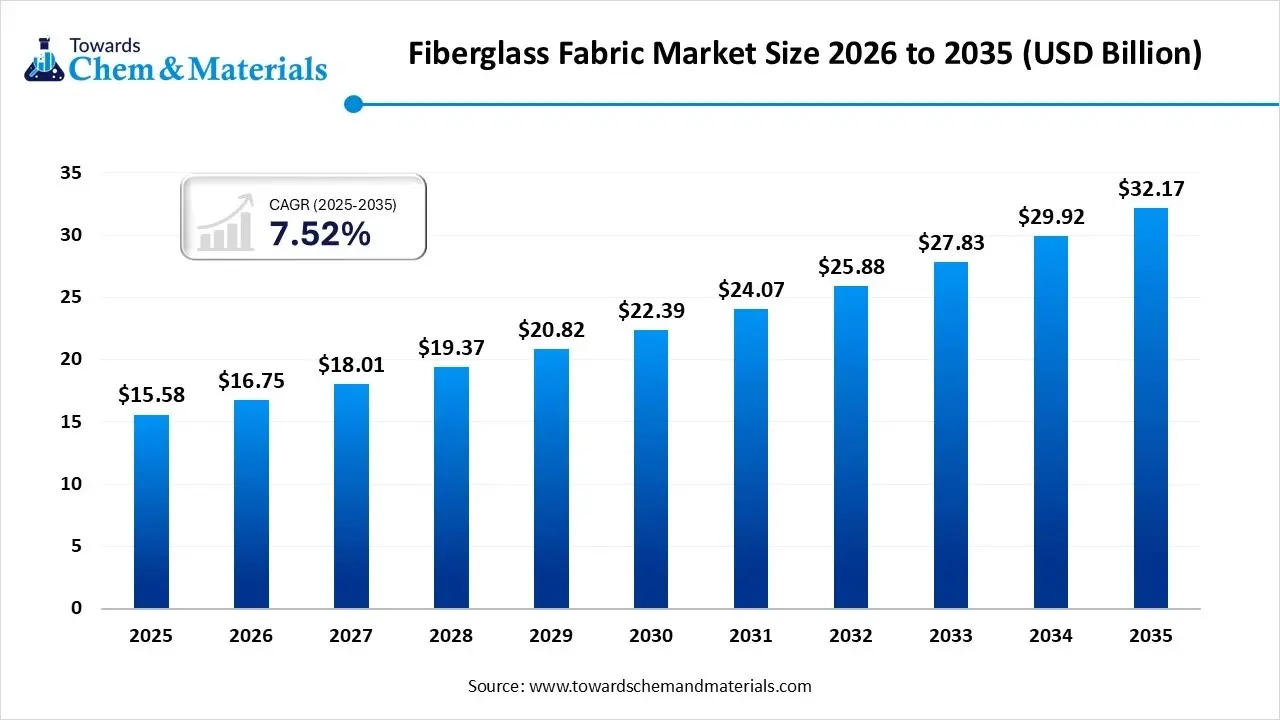

The global fiberglass fabric market size was estimated at USD 15.58 billion in 2025 and is expected to increase from USD 16.75 billion in 2026 to USD 32.17 billion by 2035, growing at a CAGR of 7.52% from 2026 to 2035. Asia Pacific dominated the fiberglass fabric market with the largest revenue share of 42% in 2025.The growth of the market is driven by the increasing demand for lightweight and high-strength materials in various sectors to increase efficiency. Fiberglass fabric is a high-performance material woven from fine glass filaments, offering exceptional tensile strength, fire resistance, and dimensional stability. Used as structural reinforcement in composites, it provides a lightweight, corrosion-resistant alternative to metals in aerospace, automotive, wind energy, and construction, enabling durable, thermally stable industrial solutions.

Market Highlights

- The Asia Pacific dominated fiberglass fabric market with the largest revenue share of 42% in 2025. The growth is driven by the infrastructure development projects and plans.

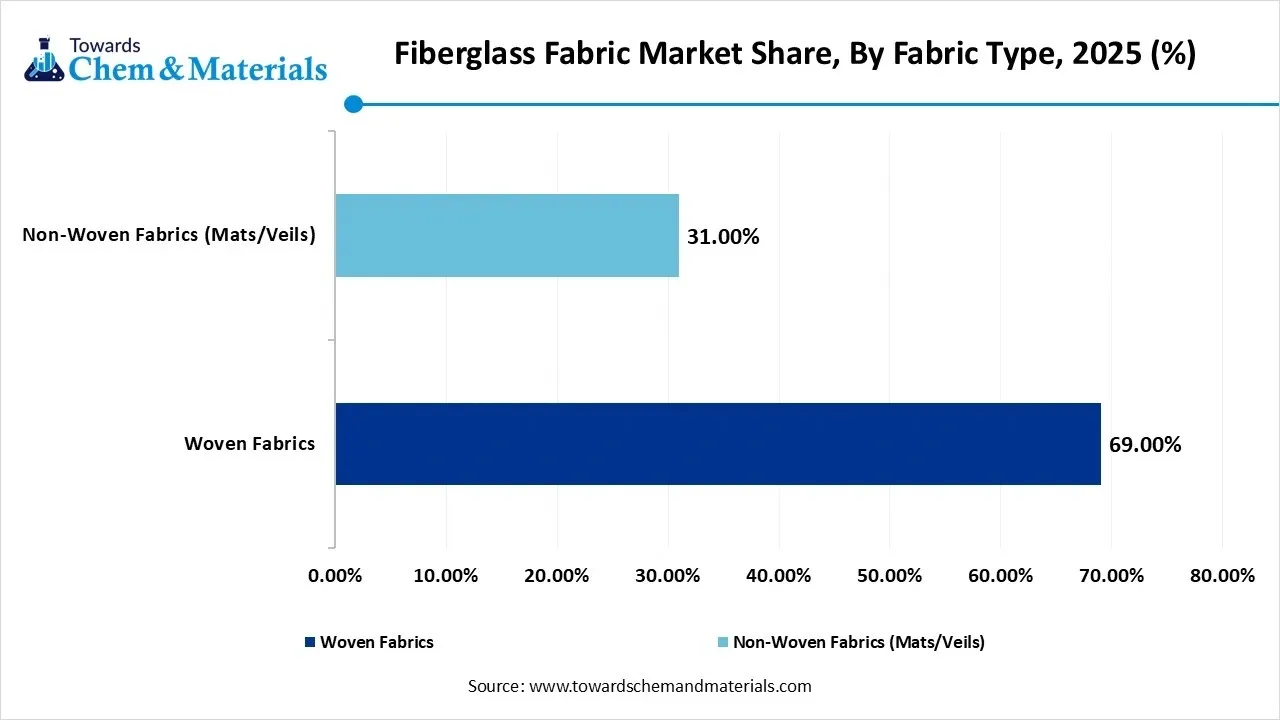

- By fabric type, the woven fabrics segment dominated the market and accounted for the largest revenue share of 69% in 2025.These fabrics are widely used in construction reinforcement, composite manufacturing, marine parts, and wind turbine blades.

- By fiber type, the e-glass segment led the market with the largest revenue share of 74% in 2025.The material’s compatibility with various resins and ease of processing further increase its adoption in large-scale manufacturing.

- By application, the construction & infrastructure segment dominated the market and accounted for the largest revenue share of 39% in 2025. Their resistance to corrosion, moisture, and chemicals makes them suitable for long-term structural durability.

- By weight, the lightweight fabrics (<200 g/m²) segment dominated the market and accounted for the largest revenue share of 45% in 2025.Their lower weight improves processing efficiency and reduces overall material usage.

Trade Analysis of Fiberglass Fabric Market: Import & Export Statistics

- Based on Global Export Data, the world exported 137,012 Fiberglass shipments from June 2024 to May 2025, by 12,831 verified exporters and 16,826 buyers, representing a 46% YoY increase.

- Vietnam, the United States, and Mexico are the top importers of Fiberglass, while China (156,519 shipments), Vietnam (83,497), and the United States (43,095) are the leading exporters.

- Additionally, for Fiberglass Woven Fabric, there were 41 shipments worldwide from Feb 2024 to Jan 2025 (TTM), with 13 verified exporters and 17 buyers, a 116% YoY rise.

- The United Arab Emirates, Vietnam, and Nepal are the main importers, while China (7,516 shipments), Vietnam (1,964), and South Korea (545) are the top exporters.

Growth Trends:

- Growth in Renewable Energy (Wind): The demand for lightweight, durable materials for wind turbine rotor blades is a primary driver for specialized, high-strength fiberglass fabrics.

- Automotive Light-weighting: Increasing use in vehicles to improve fuel efficiency and structural performance is fueling market demand.

- Material Advancements (Multi-axial Fabrics): Shift towards non-crimp, multi-axial fiberglass fabrics (NCFs) that offer superior mechanical performance and fiber alignment, replacing traditional stitched layers.

- Sustainability Focus: Manufacturers are increasingly focusing on eco-friendly production methods, recycling efforts, and the integration of bio-based resins.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 16.75 Billion |

| Revenue Forecast in 2035 | USD 32.17 Billion |

| Growth Rate | CAGR 7.52% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Fabric Type, By Fiber Type, By Application, By Weight, By Regions |

| Key companies profiled | Owens Corning, Saint-Gobain Performance Plastics / Vetrotex, Hexcel Corporation, Johns Manville, China Jushi Co., Ltd., Chongqing Polycomp International Corp. (CPIC), Taishan Fiberglass Inc. (CTG), Nippon Electric Glass Co., Ltd., AGY Holding Corp., BGF Industries, Inc., Porcher Industries, Saertex GmbH & Co. KG, Taiwan Glass Ind. Corp., Sinoma Science & Technology Co., Ltd., Ahlstrom |

Key Technological Shifts in the Fiberglass Fabric Market:

The fiberglass fabric market is shifting toward high-performance, sustainable, and automated production. The growth of the market is driven by the rise of thermoplastic composites for better recyclability, 3D weaving, and automated fiber placement (AFP) to increase production speed and design complexity. Furthermore, advanced fibers are improving resin compatibility, supporting the demand for lightweight materials in wind energy, automotive, and construction sectors.

Fiberglass Fabric Market Value Chain Analysis

Chemical Synthesis and Processing

- Fiberglass fabric is a high-performance, flexible material synthesized by melting raw mineral materials into glass and fiberizing them, followed by textile processing and chemical surface treatments (sizing) to enhance adhesion to resin matrices.

- Key players Owens Corning, China Jushi Co., Ltd., Saint-Gobain, and Hexcel Corporation

Quality Testing and Certification

- Fiberglass fabric requires plastic-free certification, CE Certificate, REACH Certificate, and NSF/ANSI 61, which are offered by various regulatory bodies.

- Key players: ISO, ASTM, and EN standards

Distribution to Industrial Users

- Fiberglass fabric is utilized in building construction, automotive panels, aircraft parts, wind turbine blades, and in the chemical industry for storage tanks and piping.

- Key players: Nippon Electric Glass Co., Ltd., BGF Industries, Inc., Auburn Manufacturing, Inc., and Porcher Industries.

Fiberglass Fabric Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Regulatory Body | Focus Areas |

| United States | EPA (Environmental Protection Agency) OSHA (Occupational Safety & Health Administration) DOT (Department of Transportation) |

Clean Air Act (CAA) – VOC, particulate emissions Clean Water Act (CWA) – effluent/NPDES OSHA 29 CFR (Safety/Hazard Communication) Resource Conservation and Recovery Act (RCRA) |

Air emissions from composite factories Dust control & silica exposure Worker safety & hazard communication Transport of resin/chemical additives |

| European Union | European Chemicals Agency (ECHA) European Commission National Environment & Workplace Safety Authorities |

REACH Regulation (EC 1907/2006) CLP Regulation (EC 1272/2008) Industrial Emissions Directive (IED) EU Waste Framework Directive |

Chemical registration & hazard classification Emission/effluent limits & BAT Worker protection Waste management & recycling |

| China | Ministry of Ecology and Environment (MEE) SAMR / SAC (Standardization) |

Air & Water Pollution Prevention Laws MEE Order No. 12 – New Chemical Registration National product standards (GB) |

Emissions & effluent compliance Chemical registration Product quality & safety standards |

Segmental Insights

Fabric Type Insights

How did the Woven Fabrics Segment Dominate the Fiberglass Fabric Market in 2025?

The woven fabrics segment dominated the fiberglass fabric market, accounting for 69% of the market in 2025, due to their high mechanical strength, dimensional stability, and uniform structural performance. Their interlaced fiber structure provides superior tensile strength and durability. Growing infrastructure development and the expansion of renewable energy installations continue to drive strong demand for woven fiberglass materials globally.

The non-woven fabrics segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, as they are valued for their lightweight structure, flexibility, and excellent insulation and filtration properties. Their random fiber orientation allows uniform coverage and enhanced surface properties. Rising adoption in HVAC systems, energy-efficient buildings, and industrial filtration solutions supports the steady growth of this segment.

Fiberglass Fabric Market Share, By Fabric Type , 2025 (%)

| By Fabric Type | Revenue Share, 2025 (%) |

| Woven Fabrics | 69.00% |

| Non-Woven Fabrics (Mats/Veils) | 31.00% |

Fiber Type Insights

Which Fiber Type Segment Dominates the Fiberglass Fabric Market in 2025?

The e-glass (electrical glass) segment dominated the fiberglass fabric market, accounting for 74% of the market in 2025, due to its cost-effectiveness, good electrical insulation, and balanced mechanical properties. They are widely used in construction, transportation, and consumer goods composites where moderate strength and corrosion resistance are required. Growth in the infrastructure, marine, and wind energy sectors continues to sustain demand for E-glass-based fabrics.

The s-glass (specialty/high-strength) segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, as they are high-performance reinforcements known for their superior tensile strength, stiffness, and heat resistance compared to E-glass. Increasing demand for lightweight yet strong materials in aerospace and high-end composites supports the expansion of this segment.

Fiberglass Fabric Market Share, By Fiber Type , 2025 (%)

| By Fiber Type | Revenue Share, 2025 (%) |

| E-Glass (Electrical Glass) | 74.00% |

| S-Glass (Specialty/High Strength) | 12.00% |

| C-Glass (Chemical Resistant) | 8.00% |

| Others (A-Glass, D-Glass, Ar-Glass) | 6.00% |

Application Insights

How did the Construction and Infrastructure Segment Dominate the Fiberglass Fabric Market in 2025?

The construction & infrastructure segment dominated the fiberglass fabric market, accounting for 39% of the market in 2025, are widely used for reinforcement in concrete, roofing materials, insulation systems, and waterproofing membranes. Rapid urbanization, green building initiatives, and infrastructure modernization programs globally are driving demand for fiberglass reinforcements that enhance structural lifespan and energy efficiency.

The wind energy segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, as they are essential for manufacturing turbine blades and nacelle components. Expansion of renewable energy capacity and government incentives for wind power development significantly contribute to the rising consumption of fiberglass fabrics in this segment.

Fiberglass Fabric Market Share, By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Construction & Infrastructure | 39.00% |

| Wind Energy | 24.00% |

| Transportation (Automotive/Marine) | 16.00% |

| Aerospace & Defense | 12.00% |

| Electrical & Electronics | 9.00% |

Weight Insights

Which Weight Segment Dominates the Fiberglass Fabric Market in 2025?

The lightweight fabrics (<200 g/m²) segment dominated the fiberglass fabric market, accounting for 45% of the market in 2025, as they are primarily used in applications requiring flexibility, ease of handling, and surface finishing. Growth in electronics manufacturing, energy-efficient insulation, and lightweight composite components in the automotive and aerospace industries drives demand for this category.

The heavyweight fabrics (>500 g/m²) segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, as they are used in high-strength and structural applications such as marine hulls, industrial equipment, wind turbine blades, and heavy-duty laminates. Industrialization, renewable energy expansion, and demand for long-lasting composite structures continue to support strong adoption of heavyweight fiberglass fabrics.

Fiberglass Fabric Market Share, By Weight , 2025 (%)

| By Weight | Revenue Share, 2025 (%) |

| Lightweight Fabrics (<200 g/m²) | 45.00% |

| Medium-Weight Fabrics (200–500 g/m²) | 35.00% |

| Heavyweight Fabrics (>500 g/m²) | 20.00% |

Regional Insights

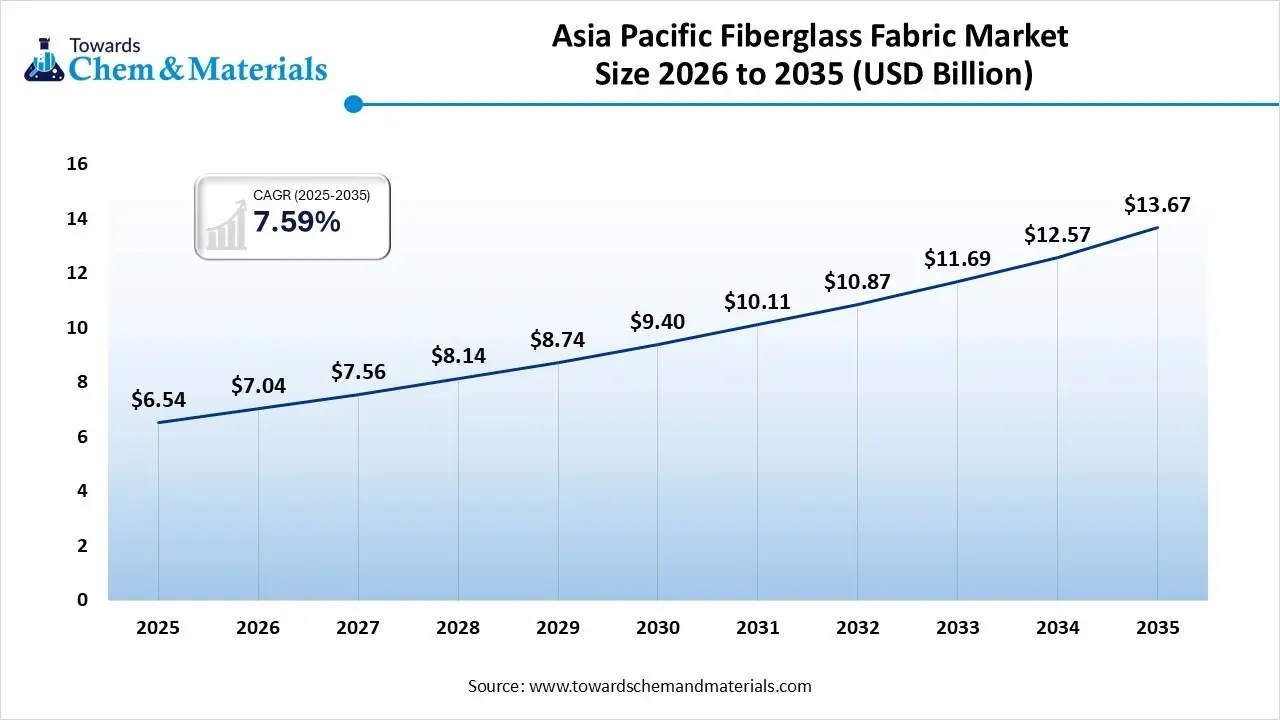

The Asia Pacific fiberglass fabric market size was valued at USD 6.54 billion in 2025 and is expected to be worth around USD 13.67 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 7.59%? over the forecast period from 2026 to 2035.

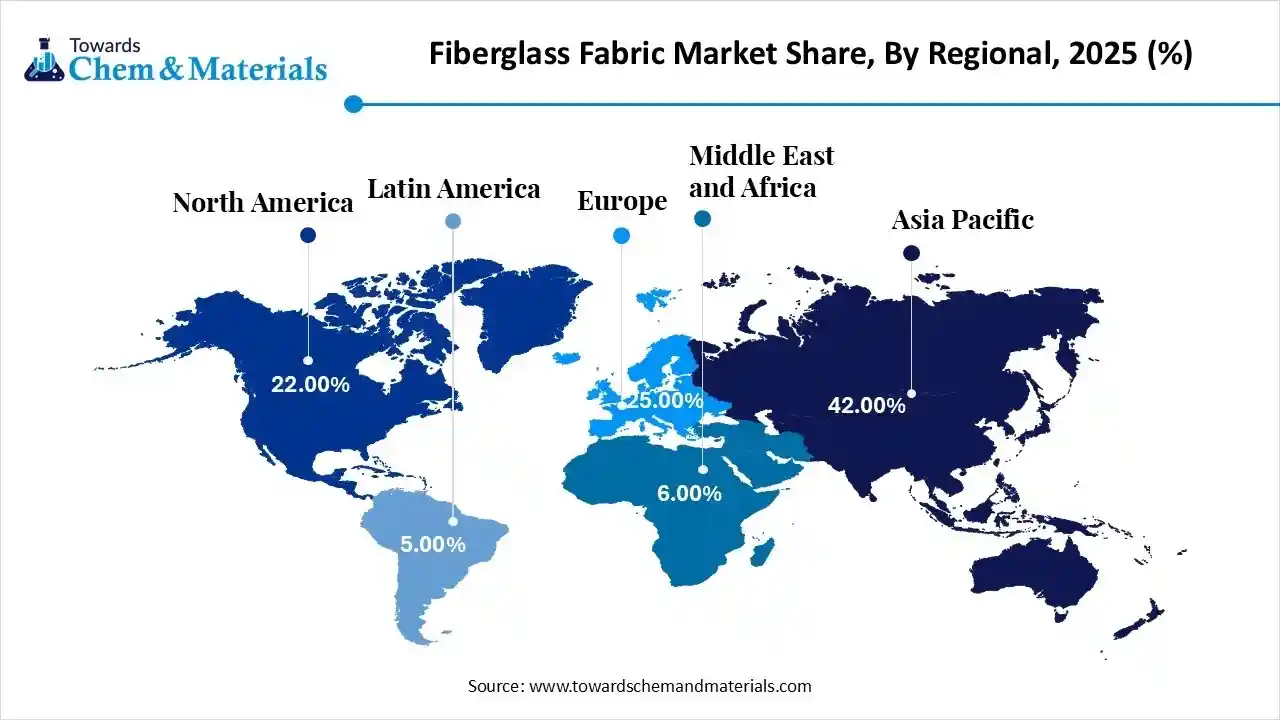

Asia Pacific dominated the market with a share of 42% in 2025, due to rapid industrialization, infrastructure development, and expanding renewable energy capacity. The region benefits from large-scale construction activity, increasing automotive production, and strong electronics and marine manufacturing sectors. Cost-effective production and growing domestic composite industries further accelerate fiberglass fabric adoption.

China: Fiberglass Fabric Market Growth Trends

China dominates regional demand, driven by massive infrastructure projects, leading wind turbine manufacturing capacity, and a strong construction sector. The country’s expanding automotive and marine industries also rely on fiberglass composites for lightweight and corrosion-resistant components. Government support for renewable energy development significantly boosts fiberglass fabric consumption in wind power applications.

North America: Fiberglass Fabric Market Growth Analysis

North America fiberglass fabric market segment accounted for the major revenue share of 22.00% in 2025. North America is expected to have fastest growth in the market in the forecast period between 2026 and 2035, driven by strong demand from the construction, aerospace, wind energy, and automotive composites industries. Growth is also supported by increasing investments in renewable energy projects, particularly wind turbine blade manufacturing, where fiberglass fabrics are widely used for reinforcement and structural strength.

United States: Fiberglass Fabric Market Growth Trends

The United States leads regional demand due to its robust aerospace, defense, and wind energy sectors. Fiberglass fabrics are widely utilized in various applications. Expanding infrastructure modernization programs and growth in industrial equipment manufacturing further drive consumption. Strong R&D capabilities and the presence of major composite manufacturers strengthen the country’s position in high-performance fiberglass fabric applications.

Europe: Fiberglass Fabric Market Growth Analysis

Europe fiberglass fabric market segment accounted for the major revenue share of 25.00% in 2025. Europe demonstrates stable growth in fiberglass fabric consumption, supported by stringent energy efficiency standards, expansion of wind power capacity, and strong automotive lightweighting initiatives. The region emphasizes sustainable construction and advanced composite materials, driving demand for reinforced fabrics in insulation, roofing membranes, and structural composites. Aerospace and rail transportation modernization programs also contribute to steady market expansion.

Fiberglass Fabric Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 22.00% |

| Europe | 25.00% |

| Asia Pacific | 42.00% |

| Latin America | 5.00% |

| Middle East & Africa | 6.00% |

Germany: Fiberglass Fabric Market Growth Trends

Germany is a key contributor, supported by its strong automotive engineering and industrial manufacturing base. The country’s focus on lightweight materials for EV production and advanced industrial machinery increases fiberglass fabric use in composite parts and insulation systems. Additionally, Germany’s leadership in wind energy manufacturing boosts demand for fiberglass reinforcements used in turbine blade production.

Recent Developments

- In October 2025, Stäubli launched the SAFIR PRO S37 automatic drawing-in machine at ITMA ASIA + CITME 2025, which is designed to handle technical yarns like fiberglass for manufacturing products such as printed circuit boards. Key features include fiberglass compatibility, high-speed performance, and Active Warp Control for precise yarn recognition and efficient processing.(Source: www.indiantextilemagazine.in)

- In May 2024, the AZULIK Mobility EK is a doorless electric car prototype with a fluid, organic fiberglass body manufactured by Roth Fablab for the AZULIK Basin development. Launched in May 2024, its design is inspired by Roth Architecture's style and organic architecture, featuring a natural material interior, including a tropical zapote wood steering wheel and waterproof nautical fabric upholstery for three occupants.(Source: www.designboom.com)

Top players in the Fiberglass Fabric Market & Their Offerings:

- Owens Corning: Owens Corning is a global leader in fiberglass composites and fabrics, offering OC® Advantex and other high-performance woven fabrics used in construction reinforcement, wind energy blades, automotive, aerospace, and industrial applications. Its products are known for durability, lightweight performance, and wide resin compatibility.

- Saint-Gobain Performance Plastics / Vetrotex: Saint-Gobain (Vetrotex) offers fiberglass fabrics and reinforcements for construction, industrial, marine, and transportation markets. Its StarRov® and related fabric products deliver strength, thermal resistance, and fire performance for structural and insulation applications.

- Hexcel Corporation: Hexcel supplies high-performance fiberglass fabrics and composite materials tailored for aerospace, defense, wind energy, and other demanding sectors. Its engineered fabrics provide superior tensile strength, thermal, and dimensional stability, serving advanced composite manufacturers.

- Johns Manville: Johns Manville produces fiberglass fabrics and reinforcement textiles used in insulation, construction composites, and industrial applications. Its product offerings focus on consistent quality, high tensile performance, and compatibility with resins for diverse end uses.

- China Jushi Co., Ltd.

- Chongqing Polycomp International Corp. (CPIC)

- Taishan Fiberglass Inc. (CTG)

- Nippon Electric Glass Co., Ltd.

- AGY Holding Corp.

- BGF Industries, Inc.

- Porcher Industries

- Saertex GmbH & Co. KG

- Taiwan Glass Ind. Corp.

- Sinoma Science & Technology Co., Ltd.

- Ahlstrom

Segments Covered

By Fabric Type

- Woven Fabrics

- Plain

- Twill

- Satin

- Non-Woven Fabrics (Mats/Veils)

By Fiber Type

- E-Glass (Electrical Glass)

- S-Glass (Specialty/High Strength)

- C-Glass (Chemical Resistant)

- Others (A-Glass, D-Glass, Ar-Glass)

By Application

- Construction & Infrastructure

- Wind Energy

- Transportation (Automotive/Marine)

- Aerospace & Defense

- Electrical & Electronics

By Weight

- Lightweight Fabrics (<200 g/m²)

- Medium-Weight Fabrics (200–500 g/m²)

- Heavyweight Fabrics (>500 g/m²)

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (4)