Content

What is the Current Specialty Fuel Additives Market Size and Share?

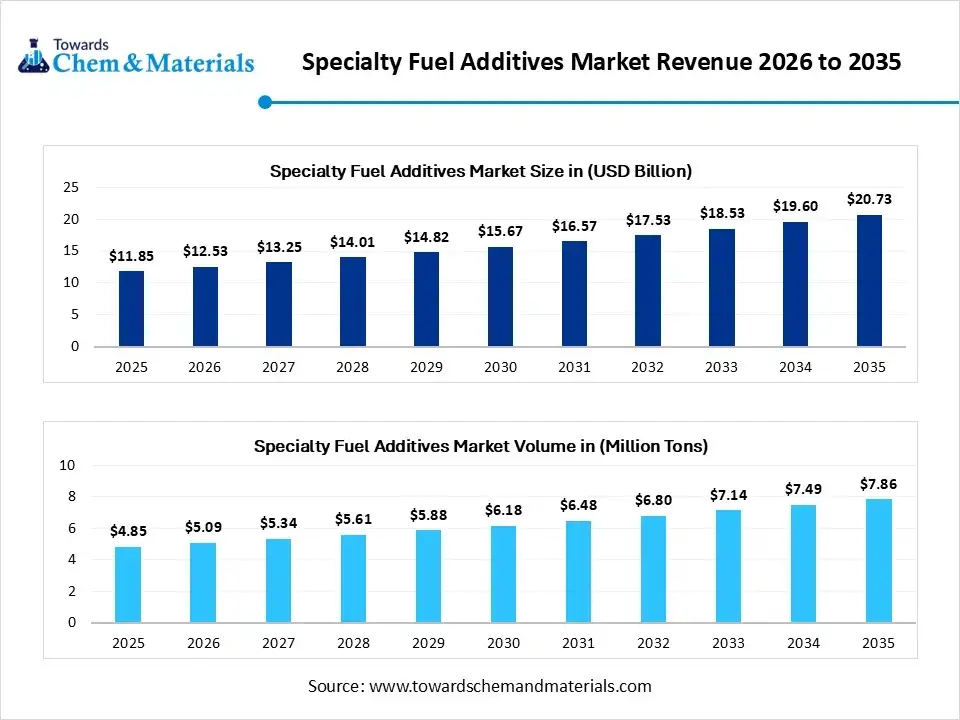

The global specialty fuel additives market size was valued at USD 11.85 billion in 2025, is estimated to reach USD 12.53 billion in 2026, and is projected to reach USD 20.73 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.75% over the forecast period from 2026 to 2035. Asia Pacific dominated the specialty fuel additives market with the largest revenue share of 36% in 2025 and is expected to grow at the fastest CAGR of 5.89% during the forecast period. In terms of volume, the specialty fuel additives industry is projected to grow from 4.85 million tons in 2025 to 7.86 million tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035. Growing use of biofuel blends is the key factor driving market growth. Also, increasing demand for higher engine efficiency coupled with the stringent environmental regulations can fuel market growth further.

Market Highlights

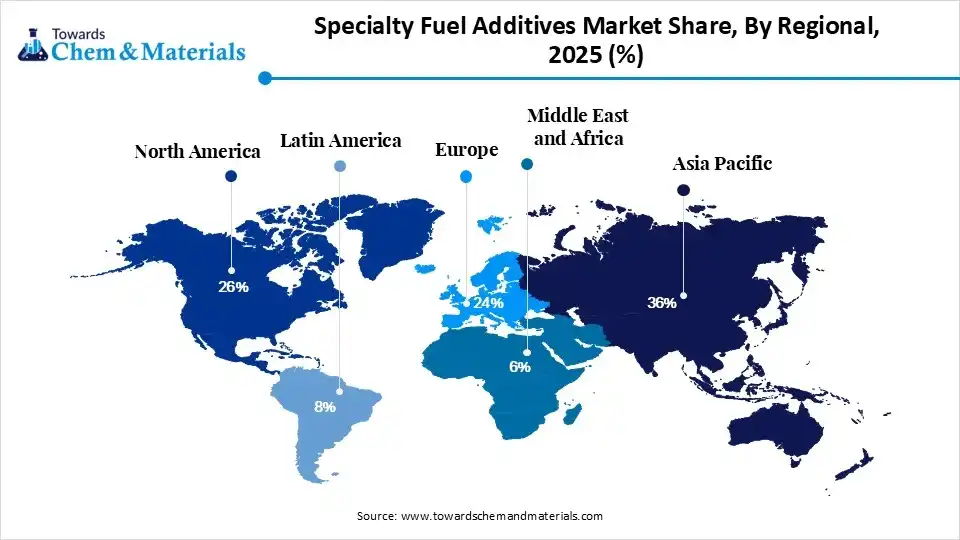

- By region, Asia Pacific dominated the market with the largest share of 36.0% in 2025 and is expected to grow at the fastest CAGR of 6.80% over the forecast period. The dominance and growth of the region can be attributed to the growing vehicle ownership.

- By region, North America held the market share of 26.00% in 2025. The growth of the region can be credited to the increasing need for sustainable biofuels.

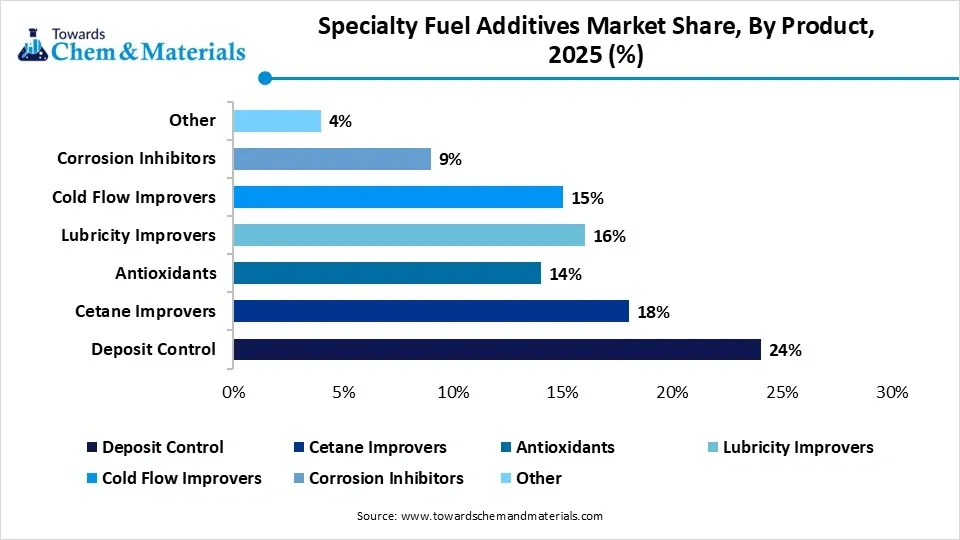

- By product, the deposit control segment dominated the market with the largest share of 24.0% in 2025. The dominance of the segment can be attributed to the increasing demand for better fuel economy.

- By product, the cold flow improvers segment held the market share of 15.00% in 2025 and is expected to grow at the fastest CAGR of 6.4% over the forecast period. The growth of the segment can be credited to the growing demand to prevent injector fouling.

- By application, the gasoline segment dominated the market with the largest share of 41.0% in 2025. The dominance of the segment is owing to the growing need for deposit-control detergents to fuel engine efficiency.

- By application, the diesel segment held the market share of 38.00% and was expected to grow at the fastest CAGR of 6.1% during the forecast period. The growth of the segment is due to the ongoing push towards bio-based alternatives.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 11.85 Billion | CAGR (2026–2035): 5.75%

- Market Projected Size (2035): USD 20.73 Billion

- Asia Pacific: largest Market Revenue Share of 36% in 2025|USD 4.27 Billion

- Market Estimated Volume (2025): 4.85 Million Tons | Volume CAGR (2026–2035):4.95%

- Market Projected Volume (2035): 7.86 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 2,190/Ton

- Average Selling Price (2025): USD 2,950/Ton

- Pricing CAGR (2026–2035): 3.7%

These are specialized chemical compounds mixed into and blended into diesel, gasoline, and aviation fuels to propel efficiency, performance, and compliance with stringent environmental regulations. The market further includes additives such as cold flow improvers, deposit control agents, and lubricity improvers, which minimize harmful emissions and expand engine lifespan.

The continuous need for specialty fuel additives, which unclog injectors, mitigate nozzle deposits, eliminate engine knocking, and ensure fuel safety, drives sustained demand in the automotive sector. The integration of these additives is anticipated to accelerate the expansion of the market. A surge in gasoline consumption in China and the United States is likely to be a major driving force for specialty fuel additives in different applications.

Market Trends

- Increasing consumption of fuel additives in the automotive industry is the latest trend in the market, shaping positive market growth. Specialty fuel additives can reduce fuel deposits in the injector nozzle of engines, minimize knocking, and give other parameters of fuel quality and safety.

- There is a notable surge in demand for high-performance fuels, boosted by the automotive sector's push for improved efficiency and minimized emissions. As consumers are increasingly becoming aware of the environment, the demand for fuels that fulfill strict performance standards are becoming crucial.

- Technological innovations in chemical formulations are another major factor driving market growth by allowing the development of more efficient and effective fuel additives. Moreover, the integration of nanotechnology in fuel additives is coming as a game changer, enhancing the overall performance metrics.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 12.53 Billion/ 5.09 Million Tons |

| Revenue Forecast in 2035 | USD 20.73 Billiion/ 7.86 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 5.75% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product, By Application, By Region |

| Key Companies Profiled | BASF, Infineum International Limited, Albemarle Corporation, Baker Hughes Company, Dow, Chevron Oronite Company LLC, The Lubrizol Corporation, TotalEnergies, Dorf Ketal, Clariant, NewMarket Corporation, Innospec |

How Are Cutting-Edge AI Technologies Revolutionizing the Specialty Fuel Additives Market?

Artificial intelligence is revolutionizing the market by driving R&D, lowering supply chain inefficiencies, and optimizing chemical formulations. By using predictive analytics and machine learning, market players can significantly minimize product development cycles. Furthermore, AI models can precisely simulate complex combustion properties and fuel-additive interactions, allowing researchers to discover new formulas.

Supply Chain Analysis of the Specialty Fuel Additives Market

- Feedstock Procurement:It refers to the sourcing and buying of essential raw materials like alcohols, petroleum derivatives, and bio-based chemicals used to produce additives.

- Major Players: Innospec, The Lubrizol Corporation

- Chemical Synthesis and Processing:It refers to the core industrial production and refining phase where raw chemical elements are synthesized to create advanced fuel performance enhancers.

- Major Players: Evonik Industries, Infineum International

- Packaging and Labeling:It includes the specialized chemical containers, product tags, and safety seals used to safely store, transport, and identify high-value performance chemicals.

- Major Players: Chevron Oronite, Baker Hughes

- Regulatory Compliance and Safety Monitoring:It ensures fuel additives fulfill stringent environmental mandates, toxicity criteria, and global safety standards. It needs market players to rigorously test their chemical formulations.

- Major Players: Infineum, BASF SE

Specialty Fuel Additives Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | Clean Air Act Section 211(b): Manufacturers must register any commercial fuel additive with the EPA prior to sale. The registration process requires data on chemical composition, emission profiles, and potential health risks. |

| European Union | REACH Regulation (EC 1907/2006): Any manufacturer or importer of specialty fuel additives exceeding 1 metric ton per year must fully register the chemical under REACH. Additives flagged as Substances of Very High Concern (SVHC) face immediate restriction or phase-outsREACH |

| China | China VI (6b) Fuel Standards: Enforced nationally, this framework mirrors and occasionally exceeds European and U.S. emission parameters. It explicitly restricts aromatic hydrocarbons, benzene, and polycyclic aromatic hydrocarbons (PAHs), limiting fuel sulfur to 10 ppm. |

Market Dynamics

Driver

Increasing Consumer Awareness

Consumer awareness regarding fuel performance and quality is the major factor driving growth of the market. As consumers are increasingly becoming aware of the benefits of utilizing high-grade fuels and additives, there is a rising need for products that promise superior engine performance and longevity. In addition, educational initiatives spearheaded by manufacturers and industry players are promoting a greater understanding of the benefits of specialty fuel additives, hence driving higher adoption rates further.

Restraint

High Raw Material Costs

The high cost associated with raw materials and volatility in crude oil and chemical feedstocks is the major factor hindering the growth of the market. Price fluctuation affects the overall manufacturing costs and may impede market penetration, particularly in price-sensitive regions. Moreover, the growing market penetration of alternative fuel technologies, such as electric vehicles, may progressively diminish reliance on conventional fuel systems, hence introducing long-term market volatility.

Opportunity

Technological Innovations in Bio-based Additives

As sustainability becomes crucial, bio-based fuel additives are increasingly gaining traction. These additives, extracted from renewable sources, provide alternatives to traditional synthetic additives. Companies are heavily exploring biodegradable additives and biofuels, which can minimize the carbon footprint of fuel products. Furthermore, advancements in engine design have prompted a shift toward specialized fuel additives tailored to specific powertrain configurations. Formulations optimized for high-performance, hybrid-electric, or diesel engines are increasingly prevalent, which ensures superior component compatibility and extended asset longevity.

Segmental Insights

Product Insights

The deposit control segment dominated the market with the largest share of 24.0% in 2025. The dominance of the segment can be attributed to the increasing demand for better fuel economy and the demand to prevent injector fouling in high-pressure and modern engines. In addition, governments across the globe are enforcing stringent limits on particulate matter.

The cold flow improvers segment held the market share of 15.00% in 2025 and is expected to grow at the fastest CAGR of 6.4% over the forecast period. The growth of the segment can be credited to the growing demand to prevent injector fouling in high pressure and modern engines. The growing integration of biodiesel and ethanol creates new opportunities in the market.

")

The cetane improvers segment held the market share of 18.00% in 2025. The growth of the segment can be linked to the stringent emission norms fuelling adoption in transportation fuels. Refiners are using cetane improvers to enhance low-quality diesel blends.

The lubricity improvers segment held the market share of 16.00% in 2025. The growth of the segment can be driven by growing demand for cleaner energy and stricter emission control standards. Lubricity additives are crucial to minimize friction and prevent premature wear and failure in injectors, fuel pumps, and engine components.

Application Insights

The gasoline segment dominated the market with the largest share of 41.0% in 2025. The dominance of the segment is due to the growing need for deposit-control detergents to fuel engine efficiency along with the growing demand to maintain fuel quality in modern vehicles. The extensive integration of ethanol into gasoline has surged the demand for corrosion inhibitors.

The diesel segment held the market share of 38.00% and was expected to grow at the fastest CAGR of 6.1% during the forecast period. The growth of the segment is due to the ongoing push towards bio-based and sustainable fuel alternatives coupled with the growth in marine and automotive sectors.

The aviation turbine fuel segment held the market share of 14.00% in 2025. The growth of the segment can be attributed to the growing need for commercial air travel and stringent global emissions norms. Government bodies need cleaner combustion and reduced greenhouse gas (GHG) emissions.

The other segment held the market share of 7.00% in 2025. The growth of the segment can be credited to the surge in specialty additive requirements and growing adoption of fuel performance enhancement solutions. Marine fuel optimization increases additive interaction globally.

Regional Insights

How did Asia Pacific Dominate the Specialty Fuel Additives Market in 2025?

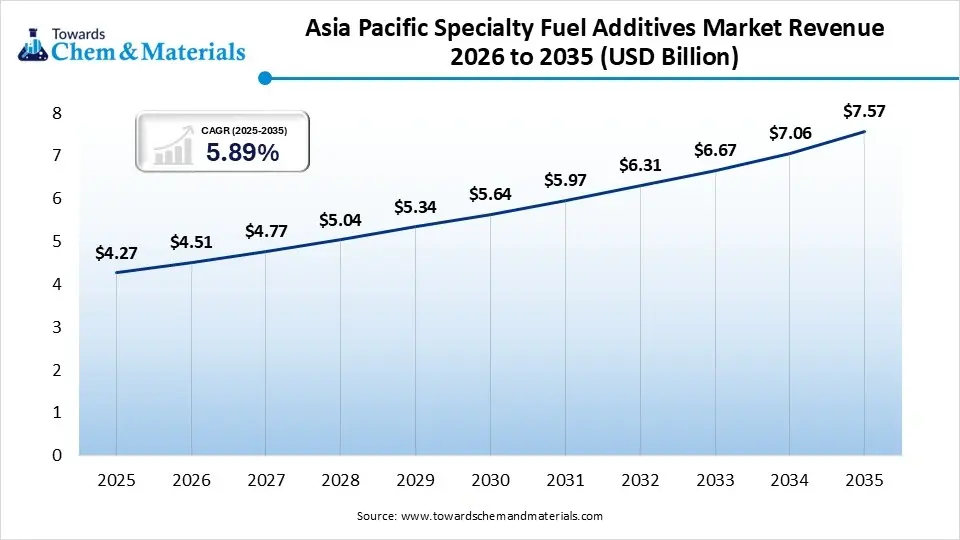

The Asia Pacific specialty fuel additives market size was estimated at USD 4.27 billion in 2025 and is projected to reach USD 7.57 billion by 2035, growing at a CAGR of 5.89% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 36.0% in 2025 and is expected to grow at the fastest CAGR of 6.80% over the forecast period. The dominance and growth of the region can be attributed to the growing vehicle ownership, ongoing urbanization, and stringent vehicular emission standards in emerging economies. In addition, the demand to enhance fuel economy is propelling the demand for specialty additives.

China

- The ongoing growth of air passenger traffic and freight transportation has surged the demand for high-performance aviation fuels.

- Significant investments in domestic refining capabilities and foreign expansions are driving local product innovation.

India

- Rapid industrialization has led to a massive spike in on-road vehicles, needing high-performance gasoline and diesel.

- Consumers and fleet operators are heavily adopting deposit control and lubricity additives to boost fuel economy.

The North America market size was estimated at USD 3.08 billion in 2025 and is projected to reach USD 5.49 billion by 2035, growing at a CAGR of 5.95% from 2026 to 2035.North America held the market share of 26.00% in 2025. The growth of the region can be credited to the increasing need for sustainable biofuels and the demand for innovative formulations to safeguard high-efficiency engines. Also, the ongoing transition towards renewable diesel and ethanol blends has surged the demand for specialized additives to prevent phase separation.

United States

- The United States holds the world's largest aerospace sector. The rising active general aviation and commercial fleet directly boosts the consumption of specialized jet fuel additives.

- The push towards renewable diesel and biofuel blending and the demand for higher fuel economy in commercial and aerospace sectors can fuel market expansion.

Canada

- The country's growing oil sands operations and refining industry boost demand for specialty additives. These products maintain and stabilize fuel quality during long-term storage and transportation.

- Federal and provincial regulations targeting fewer greenhouse gas (GHG) emissions impel fleet operators and refiners to adopt clean-burning and high-performance fuel additives.

The Europe market size was estimated at USD 2.84 billion in 2025 and is projected to reach USD 5.08 billion by 2035, growing at a CAGR of 5.99% from 2026 to 2035.Europe held the market share of 24.00% in 2025. The growth of the region can be linked to the increasing adoption of bio-based fuels and the need for improved fuel economy. The strong presence of a highly established automotive production sector, especially in Germany and the UK, propels the development of multi-functional fuel additives that minimize engine wear.

Germany

- Germany's world-renowned automotive manufacturing industry depends heavily on premium and high-performance engines.

- The ongoing transition towards blending biofuels and renewable synthetics into traditional fuels requires specialized fuel stabilizers and corrosion inhibitors.

The Latin America market size was estimated at USD 0.95 billion in 2025 and is projected to reach USD 1.76 billion by 2035, growing at a CAGR of 6.36% from 2026 to 2035.Latin America held the market share of 8.00% in 2025. The growth of the segment can be driven by massive transportation and agricultural sectors along with increasing automotive ownership. Moreover, fleet operators are rapidly adopting innovative specialty additives to maximize fuel economy, leading to market expansion soon.

Brazil

- The expanding fleet of turbocharged direct-injection (TGDI) engines and premium gasoline vehicles needs sophisticated multifunctional additive packages.

- Additives such as deposit control agents, antioxidants, and cetane improvers are essential to meet regulatory standards.

Argentina

- Increasing environmental concerns in the country have facilitated tougher vehicular and industrial emissions standards.

- Argentina's push to upgrade local refining capabilities and enhance base fuel quality needs downstream additive solutions.

The Middle East & Africa market size was estimated at USD 0.71 billion in 2025 and is projected to reach USD 1.35 billion by 2035, growing at a CAGR of 6.64% from 2026 to 2035.The Middle East & Africa held the market share of 6.00% in 2025. The growth of the region is due to the rapid investments in upgrading refining infrastructure in the Middle East, especially to manufacture ultra-low-sulfur diesel (ULSD). Furthermore, governments in the region are increasingly adopting stringent emissions standards, creating a need for deposit control additives.

")

Saudi Arabia

- A surge in consumer and industrial transition towards high-octane premium gasoline and ultra-low-sulfur diesel is boosting the demand for specialty additive chemistry.

- Ongoing economic development has drastically expanded large commercial vehicle fleets, manufacturing sectors, and transit systems.

UAE

- The UAE enforces stringent environmental policies and vehicle emission standards to enhance air quality, benefiting refineries and commercial fleets.

- Ongoing investments in logistics, non-oil industries, aviation, & public transport infrastructure drives the demand for heavy-duty commercial vehicles.

Recent Developments

- In March 2026, Cosmo Speciality Chemicals, a subsidiary of Cosmo First Limited, introduced an expanded portfolio of high-performance masterbatches. This strategic expansion bolsters the company's specialty chemical offerings and solidifies its competitive presence in the market for value-added polymer solutions.(Source: www.indianchemicalnews.com)

- In March 2026, Infineum, a premier global provider of specialty additives, formally inaugurated a state-of-the-art blending facility in India, representing a strategic expansion of its regional operations.(Source: www.indianchemicalnews.com)

Specialty Fuel Additives Market Companies

- BASF

- Infineum International Limited

- Albemarle Corporation

- Baker Hughes Company

- Dow

- Chevron Oronite Company LLC

- The Lubrizol Corporation

- TotalEnergies

- Dorf Ketal

- Clariant

- NewMarket Corporation

- Innospec

Segments Covered

By Product

- Deposit Control

- Polyether Amine Detergents

- PIB Amine Detergents

- Carrier Fluid Systems

- Cetane Improvers

- 2-Ethylhexyl Nitrate

- Di-tert-butyl Peroxide

- Nitrate Ester Formulations

- Antioxidants

- Aminic Antioxidants

- Phenolic Antioxidants

- Lubricity Improvers

- Fatty Acid Esters

- Acid-based Lubricity Agents

- Polymer Lubricity Additives

- Cold Flow Improvers

- EVA Copolymers

- Polyalkyl Methacrylates

- Wax Crystal Modifiers

- Corrosion Inhibitors

- Amine-based Inhibitors

- Imidazoline-based Inhibitors

- Film-forming Inhibitors

- Other

- Octane Improvers

- Conductivity Improvers

- Metal Deactivators

- Dye Markers

By Application

- Gasoline

- Passenger Vehicles

- Small Engines

- Marine Gasoline Engines

- Diesel

- Heavy-duty Vehicles

- Off-road Equipment

- Rail Transport

- Aviation Turbine Fuel

- Commercial Aviation

- Military Aviation

- General Aviation

- Other

- Marine Fuels

- Industrial Fuels

- Biofuel Blends

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (5)